Global Urinary Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.39 Billion |

| Market Size (2031) | USD 8.2 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

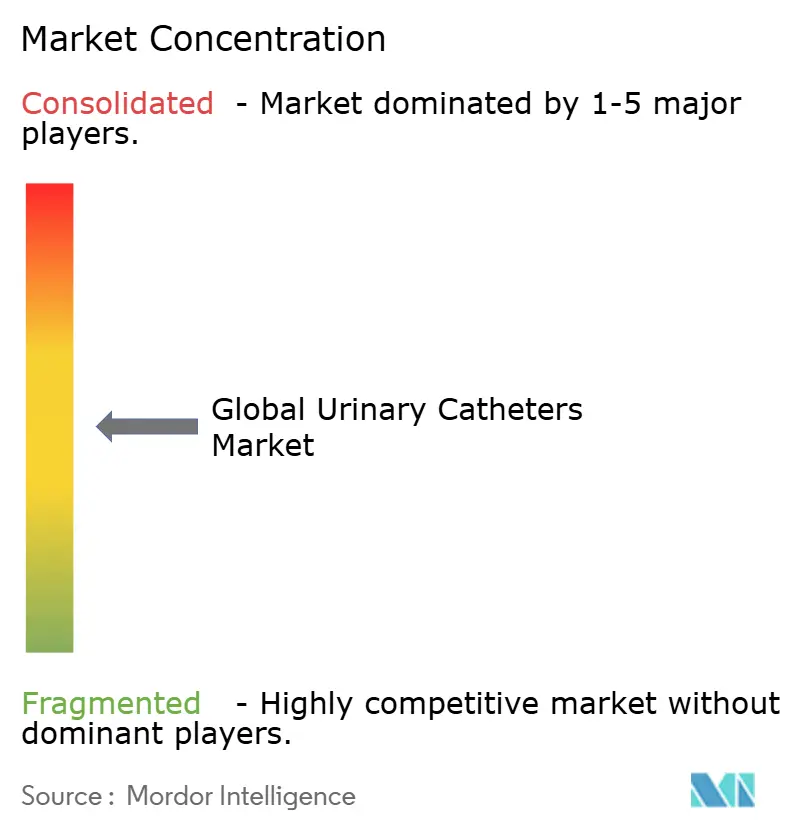

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Urinary Catheters Market Analysis by Mordor Intelligence

The urinary catheters market size is expected to grow from USD 6.08 billion in 2025 to USD 6.39 billion in 2026 and is forecast to reach USD 8.2 billion by 2031 at 5.12% CAGR over 2026-2031. Growth is supported by population ageing, rising urinary incontinence prevalence, and continuous product innovation that blends antimicrobial coatings with digital monitoring features. Value-based care incentives are steering hospitals toward premium catheters that cut infection risk, while home-care adoption is accelerating as reimbursement expands. Regulatory demands such as the EU Medical Device Regulation and the planned DEHP phase-out are encouraging sustainable biomaterials, lifting development costs but also opening niches for eco-friendly designs. Competitive intensity is heightening as large incumbents acquire, partner or launch new coating chemistries to retain share in an increasingly outcomes-driven market landscape.

Key Report Takeaways

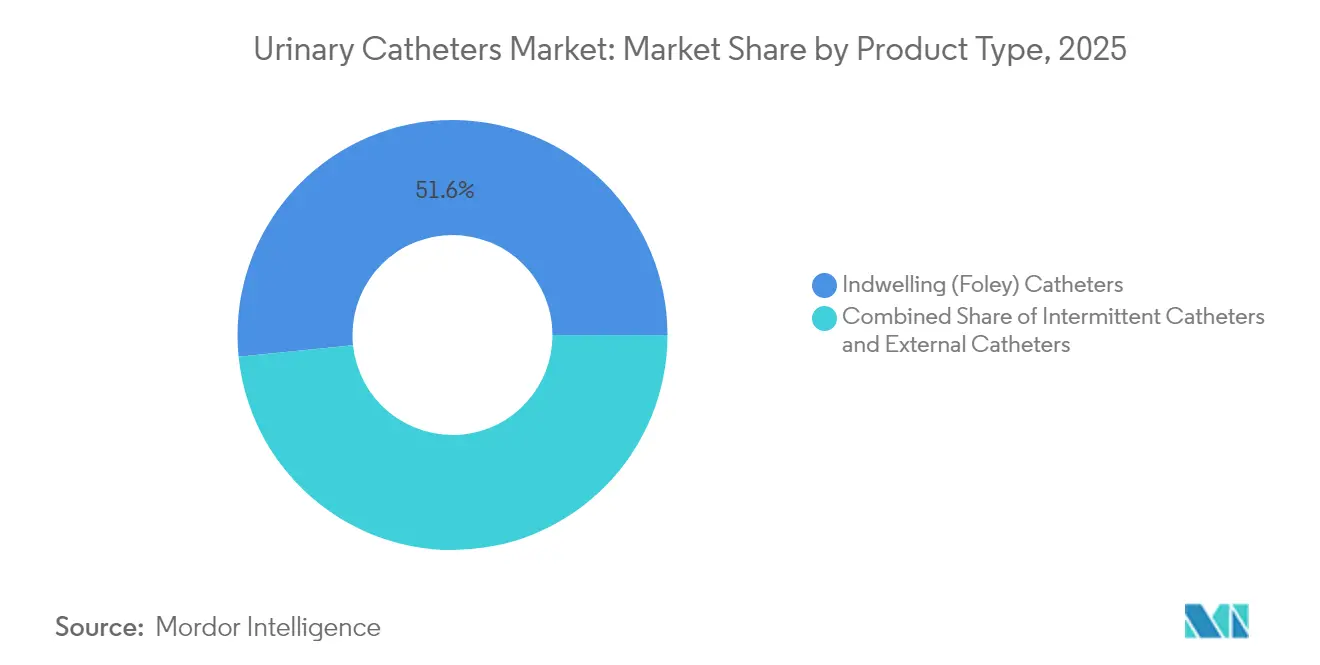

- By product type, indwelling catheters led with 51.62% of the urinary catheters market share in 2025; intermittent catheters are projected to log the fastest 5.73% CAGR to 2031.

- By gender, female patients generated 65.10% of 2025 revenue, while the male segment is set to grow at 6.05% CAGR through 2031.

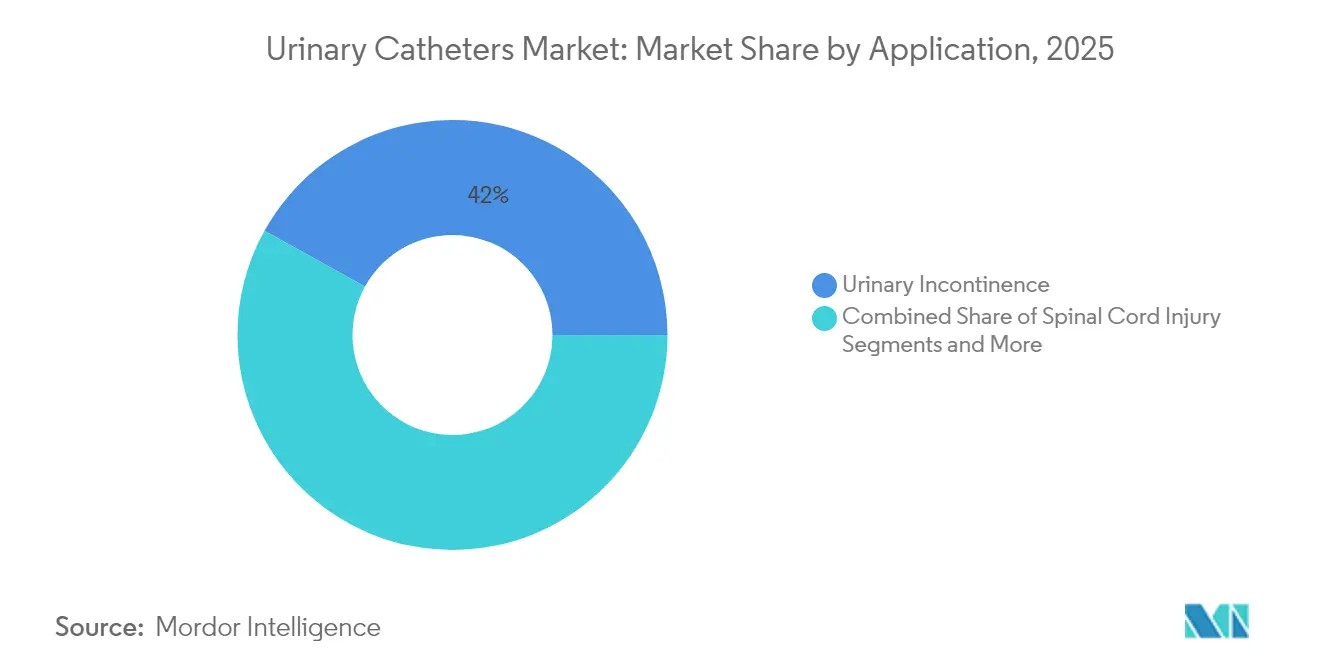

- By application, urinary incontinence accounted for a 41.95% slice of the urinary catheters market size in 2025, whereas spinal cord injury demand is advancing at a 6.44% CAGR to 2031.

- By end user, hospitals captured 66.88% revenue in 2025, yet the home-care channel is forecast to expand 6.79% annually to 2031.

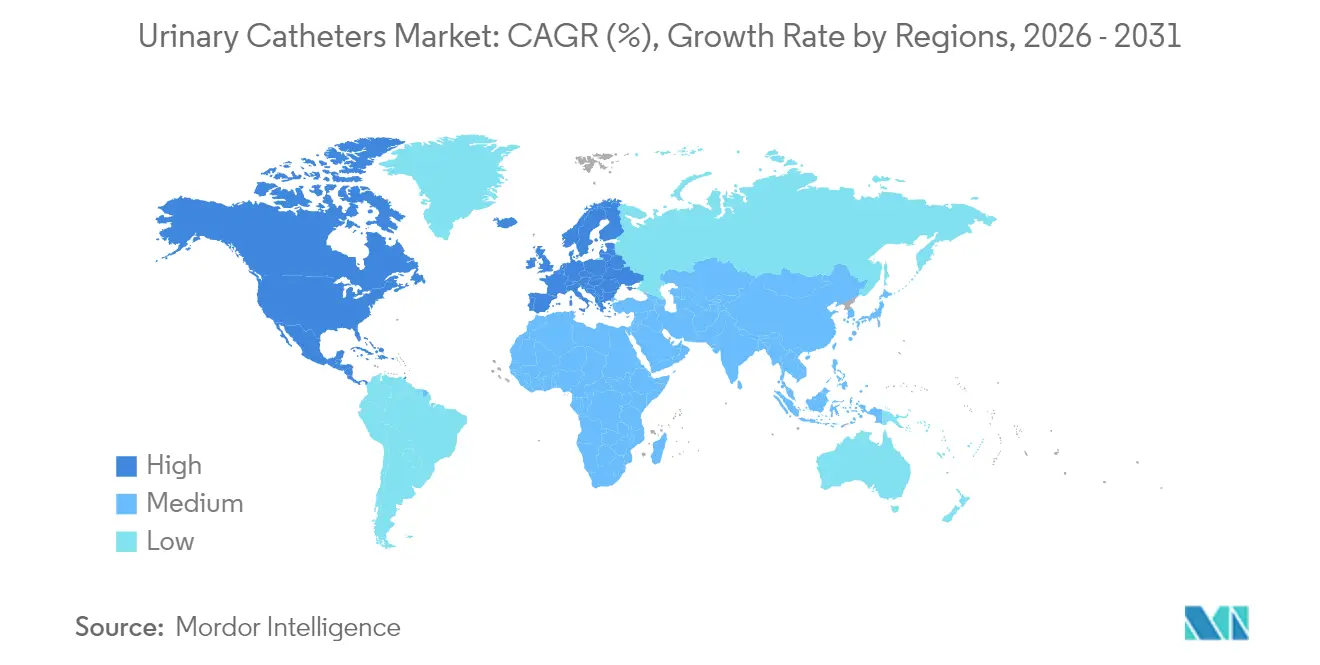

- By geography, North America dominated with 40.05% 2025 sales, and Asia-Pacific is expected to post the quickest 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Urinary Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of urinary incontinence | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Growing geriatric population | +1.0% | Asia-Pacific & North America | Long term (≥ 4 years) |

| Technological advances in coatings & biomaterials | +0.8% | North America, Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Increasing surgical procedure volumes | +0.7% | Global developed markets | Medium term (2-4 years) |

| E-commerce-enabled rise in self-catheterization | +0.5% | North America & Europe | Short term (≤ 2 years) |

| Introduction of female external urine-management devices | +0.4% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Urinary Incontinence

Nursing homes report 76.5% incontinence prevalence, underscoring sustained demand for indwelling, intermittent and external devices [1]Daniela Furlanetto, “Urinary Incontinence in Nursing Homes,” BMC Geriatrics, bmcgeriatrics.biomedcentral.com. Functional incontinence now comprises 45.5% of cases, widening the addressable pool beyond older adults. Associated complications such as dermatitis and falls elevate care costs, positioning catheters as essential therapeutic tools rather than disposable commodities. Annual nursing-home expenditures tied to incontinence approach USD 5 billion, prompting insurers to back products that lower secondary morbidities. Higher diagnosis rates in skilled-nursing facilities versus home-care settings accentuate the importance of robust infection-resistant designs. As prevalence rises among community-dwelling seniors, manufacturers see clear momentum in supplying self-catheterization kits bundled with digital education.

Growing Geriatric Population

Benign prostatic hyperplasia (BPH) cases more than doubled from 1990 to 2022, reaching 112.5 million and affecting 80% of men older than 70. Spinal cord injury incidence of 23.77 per million adds decades-long catheter dependence, while population growth contributes nearly 95% of the uplift in case volumes. These overlapping morbidities create complex multi-indication scenarios that demand device portfolios tuned to neurogenic bladder, post-operative retention and chronic dysfunction in the same patient. As health systems grapple with multimorbidity in ageing cohorts, procurement priorities tilt toward versatile platforms that streamline inventory while satisfying diverging clinical needs.

Technological Advances in Coatings & Biomaterials

Catheter-associated urinary tract infections (CAUTIs) strike 8.5% of catheterized patients and account for 80% of nosocomial UTIs [2]Ibraheem Tay, “Silver-Alloy Catheters and CAUTI,” BMC Urology, bmcurol.biomedcentral.com. Silver-alloy surfaces cut bacterial adherence, and AI-guided drainage designs are emerging to thwart encrustation. ConvaTec embeds hydrophilic additives inside the polymer matrix to keep friction low across repeated insertions. Reusable intermittent systems such as Aurie demonstrated undetectable microbial counts after 100 sterile cycles [3]Mikael Johansson, “Reusable Intermittent Catheter Sterility,” Urology, urologyjournal.org . The pending DEHP phase-out in Europe accelerates the pivot to plant-based polymers even though bioplastics currently carry up to 40% cost premiums.

Increasing Surgical Procedure Volumes

Post-operative urinary retention affects as many as 70% of specific surgical cohorts, making temporary catheterization routine in enhanced recovery protocols. Medicare Part B spends more than USD 120 million each year on BPH interventions, reinforcing predictable peri-operative demand. Minimally invasive BPH solutions such as UroLift rose from 1.4% of procedures in 2015 to 16% in 2022, creating opportunities for specialty catheters suited to office-based settings. Hospitals increasingly seek devices that support same-day discharge and automatic urine-output monitoring, further blurring lines between urology and digital health ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High risk & cost burden of CAUTI | –0.9% | Developed markets | Medium term (2-4 years) |

| Availability of non-catheter therapies for incontinence | –0.6% | North America & Europe | Long term (≥ 4 years) |

| Emerging single-use plastics regulation | –0.5% | Europe & North America | Medium term (2-4 years) |

| Limited reimbursement for premium smart/antimicrobial catheters | –0.4% | Emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Risk & Cost Burden of CAUTI

Intensive-care CAUTI rates average 8.83% and extend hospital stays, attracting financial penalties under value-based purchasing. Hospitals are rolling out nurse-led removal algorithms that trimmed retention from 30% to 6.7% in hip-fracture patients, demonstrating that prevention can erode procedure volume. Wide disparity between high- and low-income countries means adoption curves for antimicrobial catheters remain uneven. Payors favor devices with robust infection data, yet spending caps push providers to shorten catheter duration, dampening unit sales even as premium ASPs hold.

Availability of Non-Catheter Therapies for Incontinence

Neuromodulation, implants and new pharmacotherapies are broadening the therapeutic arsenal. UroMems’ smart sphincter implant met all six-month endpoints in the first female feasibility study and secured USD 47 million to scale trials. Boston Scientific’s USD 3.7 billion purchase of Axonics signifies confidence in catheter-free incontinence management. The FDA approved gepotidacin, the first oral antibiotic for uncomplicated UTIs in 30 years, potentially moderating catheter use by preventing recurring infections. These options reduce chronic indwelling dependence and may redirect spending toward curative pathways over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Indwelling Dominance Amid Intermittent Innovation

Indwelling Foley devices retained 51.62% revenue in 2025 and remain the cornerstone of acute in-patient care. Intermittent catheters, however, are forecast to grow 5.73% annually, propelled by evidence of lower infection incidence and higher patient comfort. External catheters occupy a niche yet benefit from high user-satisfaction scores and clear reimbursement coding in the United States.

Design competition now hinges on hydrophilic coatings, integrated lubrication packets and antimicrobial alloys. ConvaTec reports that hydrophilic models already contribute 60% of Continence Care turnover, and new HCPCS reimbursement codes effective 2026 are expected to boost premium adoption. Engineering advances such as micro-hole drainage channels lower residual volumes to under 6 mL, a benchmark that supports patient safety in both hospital and home settings.

By Gender: Female Segment Leadership Drives Innovation

Female users generated 65.10% of 2025 demand due to a 61% prevalence of urinary incontinence in women older than 50. Male demand is projected to advance 6.05% CAGR through 2031 as BPH and post-prostatectomy care require intermittent or temporary devices.

Innovation pathways diverge by anatomy. ConvaTec launched a women-specific intermittent line that is scaling across Europe following strong clinician acceptance. For male patients, clean intermittent self-catheterization yields fewer complications after BPH surgery versus indwelling alternatives. External male systems designed around latex-free sheaths are carving a preventive role by eliminating insertion trauma altogether, positioning the urinary catheters market for differential growth across gender lines.

By Application: Incontinence Leadership with SCI Growth Momentum

Urinary incontinence represented 41.95% of revenue in 2025, anchoring the urinary catheters market amid demographic expansion. Spinal cord injury demand is forecast to post a 6.44% CAGR as survival extends and neurogenic bladder management protocols become standardized worldwide.

Application complexity is rising: hydrophilic intermittent devices reduce UTI incidence in SCI cohorts, while early removal strategies cut complications after pelvic surgery. Technology such as the Optilume BPH Catheter achieved 67.5% patient improvement at two years, illustrating the market’s move toward indication-specific efficacy. Developers focusing on flexible portfolios addressing multiple pathologies are best positioned to capture cross-over purchasing in hospital formularies.

By End User: Hospital Dominance with Home-Care Acceleration

Hospitals held 66.88% of consumption in 2025, reflecting mandatory catheterization in surgery, emergency and intensive-care pathways. The home-care channel is forecast to expand 6.79% yearly as Medicare now funds female external systems under durable medical equipment codes at 80% co-pay coverage.

E-commerce distribution platforms, telehealth and automated drainage monitors are simplifying self-catheterization at home. Innovations such as intelligent bladder-irrigation pumps with Bluetooth analytics are enabling continuity of care that rivals inpatient oversight. Long-term-care facilities remain critical, yet rising regulatory scrutiny on CAUTI prevention incentivizes faster discharge to home settings, further lifting ambulatory demand within the urinary catheters market.

Geography Analysis

North America contributed 40.05% of 2025 sales, underpinned by Medicare reimbursement for premium external systems and an estimated USD 11 billion national spend on urologic disorders. Streamlined 510(k) pathways facilitate innovation: recent clearances include wireless urodynamic platforms that eliminate diagnostic catheters, yet still spur follow-on treatment device uptake.

Europe is shaped by stringent regulation. Half of local manufacturers trimmed product lines due to MDR certification costs, concentrating share with well-capitalized multinationals. The DEHP restriction effective July 2030 accelerates the shift to bioplastic substrates despite 20-40% higher input costs . Device makers with early-stage green portfolios are likely to capture hospital tenders that favor sustainability metrics embedded in purchasing frameworks.

Asia-Pacific is on track for a 7.12% CAGR, propelled by rising procedure volumes, expanding insurance coverage and a domestic medtech sector expected to top USD 225 billion by 2030. China’s spinal cord injury caseload grew 63% since 1990, translating into sustained intermittent-catheter demand. Emerging hubs such as Taiwan show double-digit gains in catheter imports, benefiting firms that pair off-shore manufacturing with localized regulatory know-how. Diverse reimbursement rules, however, require tailored go-to-market playbooks to avoid pricing misalignment.

Mordor Intelligence provides coverage of the global urinary catheters market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The urinary catheters market is moderately concentrated, with Coloplast, Becton Dickinson, B.Braun, Teleflex and ConvaTec commanding a majority of global revenue. Players leverage infection-control technology, portfolio breadth and geographic reach to defend share. Boston Scientific’s USD 3.7 billion Axonics purchase underscores escalating interest in adjacent continence solutions that may limit catheter dependency. Teleflex plans to split into two entities by 2026, creating a dedicated urology and acute-care business to sharpen R&D focus.

Manufacturers are racing to differentiate through material science. ConvaTec’s FeelClean platform embeds lubricious agents in the polymer backbone, whereas Bactiguard’s noble-metal alloy Foley line obtained the first MDR approval for an indwelling catheter in 2023, offering proven antimicrobial performance. Smart sensors that enable real-time flow analytics are another frontier, with start-ups licensing AI algorithms to legacy OEMs seeking rapid market entry.

Supply-chain resilience also shapes strategy after pandemic-era shortages drove the FDA to classify urinary catheters among 142 critical devices. Firms with vertically integrated molding, extrusion and coating capacity tout lower risk of back-orders, a factor increasingly factored into long-term hospital purchasing contracts. Sustainable sourcing and recyclable packaging further enter bid evaluations as single-use plastics scrutiny grows.

Global Urinary Catheters Industry Leaders

Boston Scientific Corporation

Hollister Incorporated

Teleflex Incorporated

B Braun Melsungen AG

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: UroMems reported all participants in the first female feasibility study of the UroActive smart implant met six-month endpoints; USD 47 million financing secured to advance pivotal trials.

- January 2023: Bactiguard received MDR approval for its latex BIP Foley Catheter incorporating a noble-metal alloy coating to lower microbial adhesion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the urinary catheter market as the yearly revenue generated from new, single-use or reusable indwelling (Foley), intermittent, and external catheters that drain urine from the bladder in clinical or home settings worldwide. The model tracks manufacturer list prices, which are translated to ex-factory net values after typical distributor discounts and adjusted for returned or recalled units.

Scope exclusion: accessories such as drainage bags, lubrication gels, and infection-control dressings do not form part of the market value.

Segmentation Overview

- By Product Type

- Indwelling (Foley) Catheters

- Intermittent Catheters

- External/Condom Catheters

- By Gender

- Male

- Female

- By Application

- Urinary Incontinence

- Benign Prostate Hyperplasia

- Spinal Cord Injury

- Post-operative Urinary Retention

- Others

- By End User

- Hospitals

- Long-term Care Facilities

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with practicing urologists, infection-control nurses, procurement managers, and catheter distributors across North America, Europe, and several high-growth Asian and Latin American countries. These conversations clarified real-world usage patterns, typical replacement frequencies, premium-coating uptake, and regional price dispersions that secondary sources only hinted at.

Desk Research

We gathered foundational data from open sources such as the Centers for Disease Control and Prevention, the World Health Organization, Eurostat hospital procedure statistics, the European Association of Urology, and peer-reviewed journals that quantify catheter-associated UTI incidence. Company 10-Ks, FDA 510(k) databases, and national customs records supplied shipment volumes and average selling prices. D&B Hoovers and Dow Jones Factiva aided us in checking financial consistency and news-driven demand spikes. This list illustrates key references; many additional public documents were consulted for validation.

Market-Sizing & Forecasting

A top-down construct starts with procedure counts, prevalence of urinary incontinence, and spinal-cord-injury cohorts, which are then mapped to catheterization rates and adjusted for average annual catheter use per patient group. Results are cross-checked with bottom-up supplier revenue roll-ups and channel checks to fine-tune totals. Key model drivers include 1) geriatric population growth, 2) urological surgery volume, 3) average catheter unit price shifts, 4) CAUTI reduction regulations, 5) home-based self-catheterization adoption, and 6) regional reimbursement shifts. Forecasts employ multivariate regression blended with three-scenario sensitivity around coating premium uptake and aging-curve inflection. Gaps in distributor-level data are bridged through proportional allocation using import share and hospital bed density indicators.

Data Validation & Update Cycle

Outputs undergo variance checks against historic trade data and previously published values; any outlier prompts re-interview or desk re-work before sign-off. Reports refresh each year, and interim revisions trigger when recalls, reimbursement resets, or policy bans materially sway demand. A final analyst pass ensures clients receive the most recent baseline.

Why Our Urinary Catheters Baseline Commands Reliability

Published estimates often diverge because firms choose different product mixes, price assumptions, and refresh cadences.

Key gap drivers include whether external OTC catheters are counted, how aggressively female self-catheterization growth is projected, and whether developing markets are fully represented. One global consultancy reports about USD 6.5 billion for 2025 by adding retail-channel external devices, while a trade journal quotes only USD 2.6 billion after limiting scope to hospital Foley and intermittent units; an industry database shows USD 3.7 billion for 2024 by tracking the top seven economies only.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.08 B (2025) | Mordor Intelligence | |

| USD 6.54 B (2025) | Global Consultancy A | Counts retail external catheters and includes OTC pricing at consumer mark-ups |

| USD 2.60 B (2025) | Trade Journal B | Limits scope to hospital purchases in 15 developed countries only |

| USD 3.70 B (2024) | Industry Database C | Excludes external catheters and omits Latin America, Africa, and the Middle East |

In sum, Mordor's disciplined product scope, transparent price normalization, and annual refresh cadence deliver a balanced, traceable baseline that decision-makers can rely on for planning and benchmarking.

Key Questions Answered in the Report

What is the current Global Urinary Catheters Market size?

The urinary catheters market size reached USD 6.39 billion in 2026 and is projected to hit USD 8.2 billion by 2031.

Who are the key players in Global Urinary Catheters Market?

Boston Scientific Corporation, Hollister Incorporated, Teleflex Incorporated, B Braun Melsungen AG and Medtronic PLC are the major companies operating in the Global Urinary Catheters Market.

Which is the fastest growing region in Global Urinary Catheters Market?

Asia-Pacific is forecast to expand at a 7.12% CAGR between 2026 and 2031 on the back of rising procedure volumes and improving reimbursement.

Which region has the biggest share in Global Urinary Catheters Market?

In 2025, the North America accounts for the largest market share in Global Urinary Catheters Market.

Which catheter type holds the largest share?

Indwelling Foley catheters led with 51.62% of the urinary catheters market share in 2025.

Page last updated on: