DNA Polymerase Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 331.13 Million |

| Market Size (2030) | USD 417.91 Million |

| Growth Rate (2025 - 2030) | 4.77% CAGR |

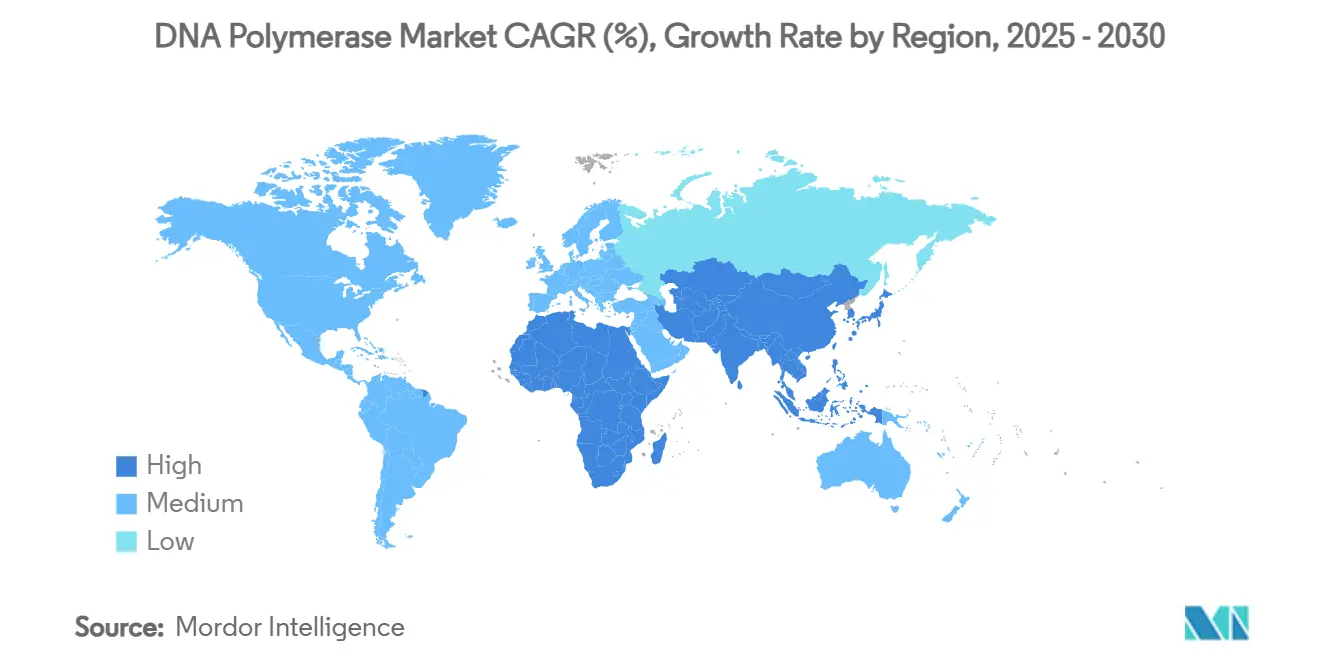

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

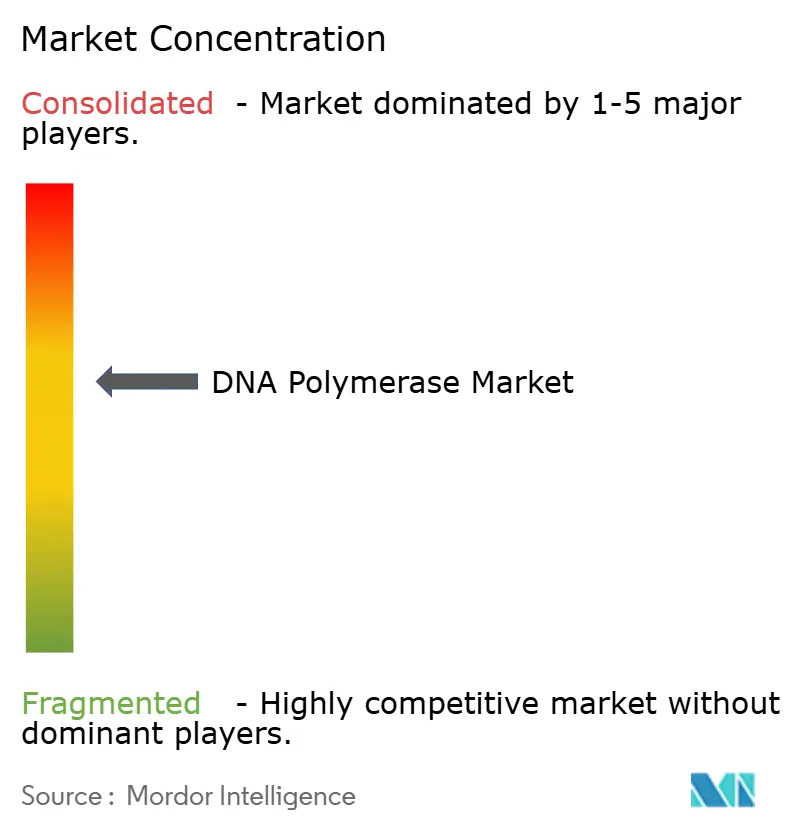

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNA Polymerase Market Analysis by Mordor Intelligence

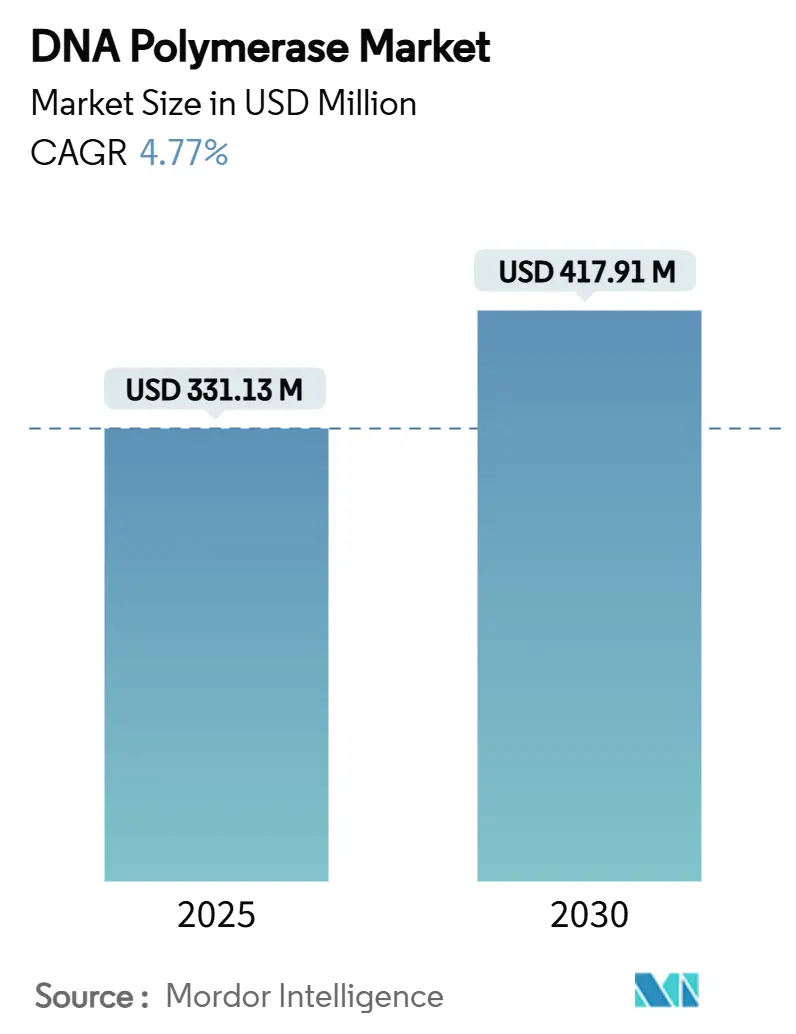

The DNA polymerase market size reached USD 331.13 million in 2025 and is forecast to rise to USD 417.91 million by 2030, reflecting a 4.77% CAGR. Growth is anchored in sustained demand from molecular diagnostics, next-generation sequencing (NGS) and synthetic-biology applications that surged after the COVID-19 pandemic. Standard PCR still underpins most laboratory workflows, yet high-fidelity enzymes, lyophilized formats and point-of-care (POC) solutions now attract the fastest capital inflows. Prokaryotic Taq variants remain price leaders, but proof-reading alternatives are gaining share as oncology and rare-disease researchers demand higher accuracy. Geopolitical pressure on supply chains, most visibly the US Biosecure Act and China’s ban on Illumina products, is steering procurement toward multiple regional manufacturing hubs, while high-value enzyme engineering continues to differentiate premium suppliers. Manufacturers that can combine scale, clinical-grade compliance and application-specific performance are best positioned to accelerate revenue through the forecast horizon.

Key Report Takeaways

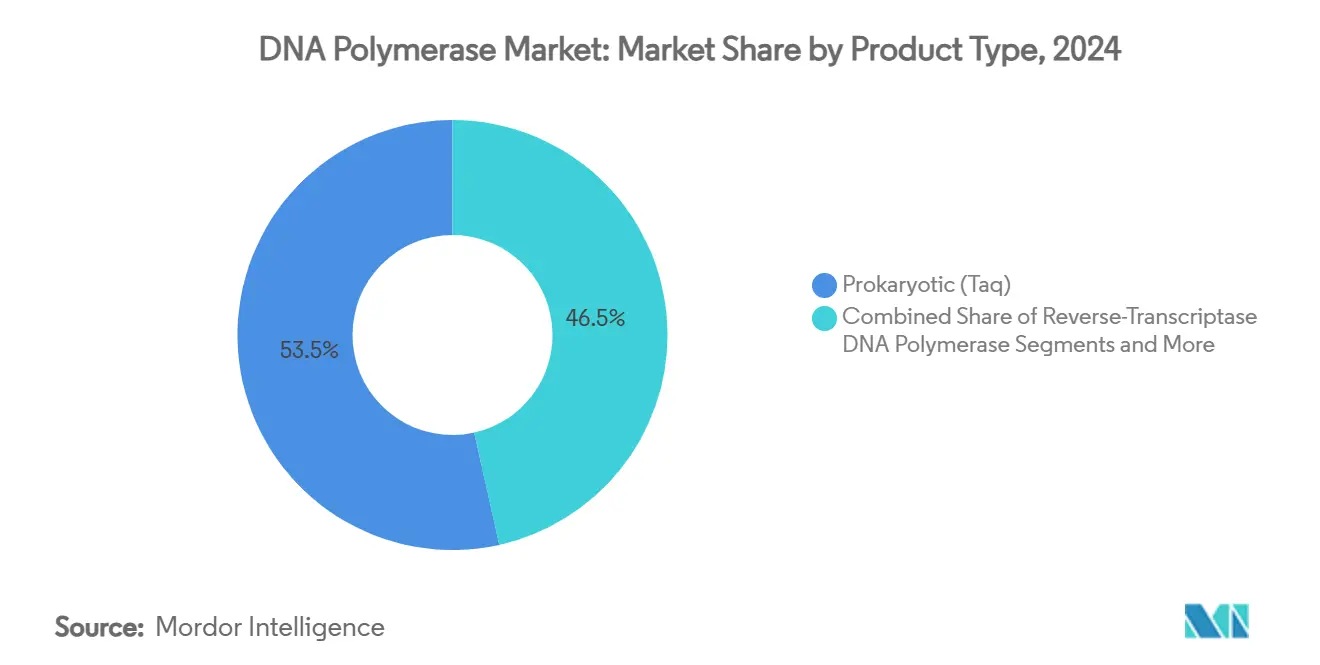

- By product type, prokaryotic Taq enzymes led with 53.48% of DNA polymerase market share in 2024, while high-fidelity variants are advancing at a 7.34% CAGR to 2030.

- By application, standard PCR commanded 64.58% share of the DNA polymerase market size in 2024; DNA sequencing and library preparation are expanding at an 8.53% CAGR through 2030.

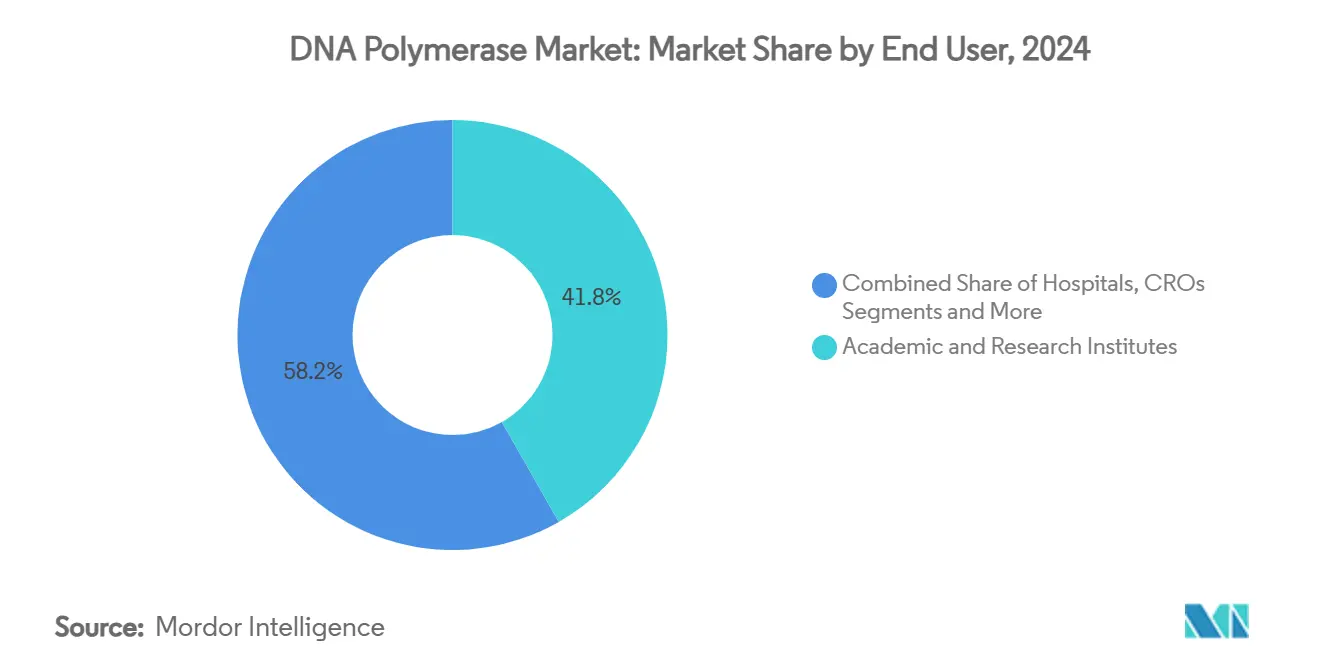

- By end user, academic and research institutes held 41.77% share in 2024, yet clinical diagnostic laboratories are the fastest-growing segment at 6.81% CAGR to 2030.

- By formulation, liquid enzymes maintained 78.64% share in 2024, whereas lyophilized products are increasing at a 7.69% CAGR on the back of POC deployment.

- By geography, North America contributed 36.73% of 2024 revenue; Asia-Pacific shows the highest regional growth at 7.04% CAGR to 2030.

Global DNA Polymerase Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID expansion of PCR diagnostics | +1.2% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| NGS labs’ demand for high-fidelity enzymes | +0.8% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| APAC R&D funding surge for genomics | +0.6% | Asia-Pacific | Long term (≥ 4 years) |

| CRISPR-POC assays need polymerase variants | +0.4% | Early adoption in North America & Europe | Medium term (2-4 years) |

| Synthetic-biology demand for mutagenic enzymes | +0.3% | North America & Europe; emerging in APAC | Long term (≥ 4 years) |

| Lyophilized field-kits for on-site DNA tests | +0.5% | Resource-limited regions worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-COVID expansion of PCR diagnostics

Clinical laboratories keep automating PCR platforms to handle routine pathogen testing and pandemic-era respiratory panels that remain in high demand. The FDA’s 2024 emergency authorization for Labcorp’s monkeypox home-collection PCR kit set a precedent for rapid polymerase-based approvals, encouraging vendors to tailor enzymes to newly emergent pathogens.[1]Food and Drug Administration, “Authorization of Emergency Use of Monkeypox PCR Test Home Collection Kit,” federalregister.gov Takara Bio’s 2024 launch of the PrimeCap T7 RNA Polymerase highlights manufacturers’ pivot toward mRNA therapy support, while lyophilized reagents enable reliable transport to lower-resource settings. These shifts sustain above-trend polymerase consumption beyond academic labs.

NGS labs’ demand for high-fidelity enzymes

Element Biosciences’ Cloudbreak UltraQ achieved Q50 reads for 70% of sequences in 2024, pushing library-prep error tolerance below 0.001%. New England Biolabs’ Q5 enzyme delivers error rates 280-fold lower than standard Taq, demonstrating how protein engineering secures premium price points. Research into psychrophilic polymerase fusions for nanopore platforms widens the innovation pipeline and raises barriers for smaller rivals lacking R&D depth.[2]Sun Yaping et al., “Engineering Psychrophilic Polymerase for Nanopore Sequencing,” frontiersin.org

APAC R&D funding surge for genomics

China recorded more than 40 companies pursuing small-nucleic-acid therapeutics in 2024, backed by dedicated state and private capital flows. Japan’s Whole Genome Analysis initiative further institutionalizes clinical sequencing demand. Meanwhile, India’s contract development and manufacturing organizations (CDMOs) benefit from multinationals’ drive to diversify away from Chinese suppliers after the US Biosecure Act.

CRISPR-POC assays need polymerase variants

Cas13a-based monkeypox assays delivered 100% sensitivity using multienzyme isothermal amplification, underscoring the requirement for polymerases that remain active under low-temperature, rapid-cycle conditions.[3]Zhang Qin et al., “CRISPR-Cas13a Point-of-Care Assay for Monkeypox,” idpjournal.biomedcentral.comEngineered FnCas9 systems widen target selection and create downstream demand for equally precise amplification enzymes. Portable LAMP solutions such as the Dragonfly platform prove the commercial relevance of thermostable, lyophilized enzyme kits for decentralized testing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price erosion from generic suppliers | -0.7% | Global; pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Patent cliff for key polymerase variants | -0.5% | Developed markets | Medium term (2-4 years) |

| Fermentation-capacity bottlenecks | -0.4% | Global; supply-chain dependent | Short term (≤ 2 years) |

| Bio-security scrutiny on extremophile strains | -0.3% | Regulatory dependent worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price erosion from generic suppliers

Yeast-derived Taq expression systems cut production costs, enabling low-price competition that erodes margins on standard enzymes. Chinese and Indian vendors increasingly match ISO-compliant quality, challenging incumbents to defend share through application-specific value rather than price.

Patent cliff for key polymerase variants

Pending expirations across Thermo Fisher’s portfolio are set to open the door to copycat formulations, prompting innovators to accelerate platform-tied enzyme launches such as Roche’s sequencing-by-expansion technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Precision enzymes rise within a Taq-dominated baseline

Prokaryotic Taq still underpins 53.48% of the DNA polymerase market share in 2024 owing to cost efficiency and robust standard-PCR performance. Yet proof-reading high-fidelity variants are advancing at 7.34% CAGR as NGS and oncology sequencing prioritize near-error-free amplification. Reverse-transcriptase enzymes gain prominence in RNA diagnostics, while long-range polymerases serve structural-variant studies. Engineered mutagenic variants, tailored for directed evolution, carve out a premium niche that commands above-average pricing. Master-mixes simplify workflow by bundling buffers and co-factors, trading higher unit cost for throughput efficiency. Suppliers differentiate through hot-start chemistry, inhibitor tolerance and formulation breadth, positioning high-fidelity and specialty enzymes for outsized contribution to future revenue.

Demand dynamics will maintain Taq’s revenue lead, but its unit-price trajectory softens as generic offerings proliferate. Conversely, IP-protected proofreading enzymes sustain higher ASPs and margin contribution, cushioning suppliers against commoditization. As synthetic-biology workflows mature, mutagenic and orthogonal polymerases could become mainstream, further diversifying product revenue streams within the DNA polymerase market.

By Application: Sequencing workflows close the gap on entrenched PCR usage

Standard PCR’s 64.58% share of the DNA polymerase market size attests to its ubiquity across research, QC and diagnostic protocols. However, DNA sequencing and library-prep applications showcase an 8.53% CAGR that outpaces the baseline, propelled by population genomics and precision oncology initiatives. qPCR and digital PCR expand via MRD and liquid-biopsy testing, demanding enzymes that maintain quantitative linearity across nine logarithmic orders. Molecular diagnostics benefit from FDA reclassification of DNA-based MRD tests to Class II status, accelerating commercial adoption.

Cloning, mutagenesis and whole-genome amplification sustain specialized demand for processive, low-bias enzymes that minimize allelic dropout. Suppliers that provide kit-level solutions tied to targeted oncology panels or cfDNA workflows secure predictable, reagent-driven revenue over the forecast window.

By End User: Clinical adoption narrows the gap with research leadership

Academic and research institutes retained 41.77% of DNA polymerase market share in 2024, reflecting decades of grant-funded genomics projects and basic-science exploration that favor performance-driven enzyme selection over price constraints. Funding initiatives such as Japan’s Whole Genome Analysis plan and China’s national precision-medicine programs ensure laboratories continue acquiring high-fidelity and specialty variants for complex workflows. These institutions also pilot emerging methods—single-cell sequencing, orthogonal replication and CRISPR screening—that require tailored polymerases capable of ultra-low error rates or engineered mutagenesis. In parallel, pharmaceutical and biotech firms scale enzyme consumption for gene-therapy vector QC and companion-diagnostic development, choosing suppliers that can certify GMP-grade production and traceability. Contract research organizations expand their orders as drug sponsors outsource molecular assays, while hospitals widen in-house molecular labs to speed oncologic and infectious-disease decisions.

Clinical diagnostic laboratories represent the fastest-growing end-user cohort, advancing at a 6.81% CAGR through 2030 as post-pandemic PCR capacity becomes routine infrastructure in respiratory, sexually transmitted and antimicrobial-resistance testing. Regulatory streamlining, illustrated by the FDA’s 2025 reclassification of DNA-based MRD assays to Class II devices, lowers commercialization hurdles and stimulates uptake of validated polymerases that guarantee batch-to-batch consistency. Point-of-care workflows further boost demand for lyophilized reagents that survive transit without refrigeration, allowing smaller community clinics to run molecular panels. With reimbursement increasingly tied to rapid, precise results, enzyme providers that bundle assay-specific protocols and robust technical support win preferred-supplier status across expanding clinical networks.

By Formulation: Lyophilized formats outpace but do not overturn liquid dominance

Liquid preparations accounted for 78.64% of 2024 revenue as most core research and hospital labs favor ready-to-use master mixes that integrate buffers, cofactors and hot-start antibodies to minimize setup time and contamination risk. Suppliers differentiate these liquids through inhibitor tolerance, shortened elongation times and compatibility with automation, keeping them the default choice for high-throughput thermal cyclers. The sustained volume also anchors scale economies that support aggressive pricing on commodity Taq variants while subsidizing R&D for premium high-fidelity lines. Yet dependence on cold-chain logistics exposes vulnerability in field settings, disaster zones and emerging markets where reliable refrigeration is scarce.

Lyophilized, freeze-dried formulations expand at a 7.69% CAGR, driven by portable molecular platforms and public-health programs that prioritize ambient-temperature stability. Studies show complete qPCR reagent kits can retain performance for three days at 4 °C and primer–probe mixes remain stable for five months at –20 °C, validating shelf-life claims essential for resource-limited deployments. Tablet and bead formats—essentially pre-aliquoted lyophilizates—offer similar robustness with simplified handling, though higher production costs and instrument-compatibility checks limit rapid scale-up. The DNA polymerase market size for lyophilized products therefore remains a minority portion but commands premium margins, especially when integrated into pathogen-specific kits for decentralized diagnostics. Vendors that master dual manufacturing streams—large-volume liquid for core labs and ambient-stable formulations for field use—build resilience against supply disruptions while tapping parallel growth curves.

Geography Analysis

North America held 36.73% of 2024 revenue owing to deep research funding pools, routine clinical sequencing and vertically integrated biomanufacturing. Large-scale investments, such as Roche’s USD 50 billion commitment to expand US manufacturing through 2030, reinforce regional supply resilience. Canada and Mexico add incremental demand through expanding diagnostic infrastructure and pharmaceutical contract services. FDA oversight raises compliance thresholds, steering buyers toward clinically validated, premium-priced enzymes.

Asia-Pacific, advancing at a 7.04% CAGR, draws momentum from China’s nucleic-acid drug push and Japan’s nationwide genome-analysis framework. China’s 2025 ban on Illumina sequencing platforms shifts procurement toward domestic alternatives, sparking local polymerase development. India’s CDMOs capture volume as Western firms diversify post-Biosecure-Act, while Southeast Asia expands infectious-disease testing capacity, demanding lyophilized formats suitable for tropical climates.

Europe presents a mature, regulation-driven market with stringent CE-IVD and MDR requirements. High-fidelity enzymes see strong uptake in clinical diagnostics under Europe’s precision-medicine programs. The Middle East and Africa grow from a small base as governments prioritize POC testing to combat endemic diseases, creating opportunity for ambient-temperature stable kits. South America, led by Brazil and Argentina, leverages public-sector Genomics initiatives but remains constrained by currency volatility and import dependencies. Collectively, emerging regions offer double-digit growth pockets that vendors can unlock through localized distribution and technical-support footprints.

Competitive Landscape

The DNA polymerase market features moderate concentration as a handful of global suppliers combine proprietary engineering with large-scale GMP production. New England Biolabs, Qiagen, Takara Bio, Thermo Fisher Scientific, Roche, Promega and a short list of specialty challengers anchor premium niches by demonstrating disciplined innovation cycles. Q5 high-fidelity chemistry, sequencing-by-expansion reagents and lyophilized field kits exemplify portfolio differentiation that sustains price premiums. Supply-chain realignment away from single-country dependence also favors companies with dual-continent manufacturing.

Generic pressure intensifies as ISO-13485-certified Asian producers close quality gaps, undercutting pricing on legacy Taq formulations. Patent expirations accelerate biosimilar entry, compelling incumbents to bundle reagents with instrumentation and bioinformatics to protect share. Strategic collaborations, such as Qiagen-Incyte’s panel development and Agilent-SeqOne’s liquid-biopsy analytics tie-ins, embed reagents within broader clinical ecosystems, raising customer switching costs. Capital investment in fermentation capacity remains a critical entry barrier, with multiyear build cycles limiting rapid share capture by newcomers.

Over the forecast window, the strongest growth accrues to players that align enzyme portfolios with oncology NGS, CRISPR diagnostics and synthetic-biology workflows while offering multiple formulation options. Partnerships with CDMOs and decentralized diagnostic platforms further tilt competitive advantage toward firms delivering both scale and specialized performance.

DNA Polymerase Industry Leaders

Thermo Fisher Scientific Inc

New England Biolabs

Qiagen N.V.

Merck KGaA

Takara Bio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: QIAGEN and Incyte agreed to co-develop a diagnostic panel supporting investigational myeloproliferative neoplasm therapies.

- June 2025: Acurx Pharmaceuticals presented Phase 3-ready DNA pol IIIC inhibitor data targeting Gram-positive pathogens.

- June 2025: SeqOne partnered with Agilent to optimize multiomic liquid-biopsy analytics for the Avida Cancer panel suite.

Global DNA Polymerase Market Report Scope

| Prokaryotic (Taq) |

| Proof-reading / High-fidelity |

| Reverse-Transcriptase DNA Polymerase |

| High-processivity / Long-range |

| Engineered Mutagenic Variants |

| Polymerase Master-Mixes |

| Standard PCR |

| qPCR / Real-time PCR |

| Digital PCR |

| DNA Sequencing & Library Prep |

| Molecular Diagnostics |

| Cloning & Mutagenesis |

| Whole-Genome / WGA |

| Academic & Research Institutes |

| Clinical Diagnostic Laboratories |

| Pharmaceutical & Biotech Companies |

| Hospitals |

| Contract Research Organisations |

| Liquid Enzymes |

| Lyophilised (Freeze-dried) |

| Bead / Tablet Format |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Prokaryotic (Taq) | |

| Proof-reading / High-fidelity | ||

| Reverse-Transcriptase DNA Polymerase | ||

| High-processivity / Long-range | ||

| Engineered Mutagenic Variants | ||

| Polymerase Master-Mixes | ||

| By Application | Standard PCR | |

| qPCR / Real-time PCR | ||

| Digital PCR | ||

| DNA Sequencing & Library Prep | ||

| Molecular Diagnostics | ||

| Cloning & Mutagenesis | ||

| Whole-Genome / WGA | ||

| By End User | Academic & Research Institutes | |

| Clinical Diagnostic Laboratories | ||

| Pharmaceutical & Biotech Companies | ||

| Hospitals | ||

| Contract Research Organisations | ||

| By Formulation | Liquid Enzymes | |

| Lyophilised (Freeze-dried) | ||

| Bead / Tablet Format | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the DNA polymerase market and its growth outlook?

The DNA polymerase market size reached USD 331.13 million in 2025 and is projected to climb to USD 417.91 million by 2030, reflecting a 4.77% CAGR.

2. Which product segment is expanding the fastest?

Proof-reading high-fidelity enzymes are the fastest-rising segment, advancing at a 7.34% CAGR as NGS labs demand ultra-low error rates.

3. What regional market shows the highest growth potential?

Asia-Pacific leads regional momentum with a 7.04% CAGR to 2030, fueled by large-scale genomics funding in China, Japan and India.

4. How do recent geopolitical measures affect supply chains for DNA polymerases?

The US Biosecure Act and China’s 2025 ban on Illumina products are prompting pharmaceutical and diagnostic firms to diversify suppliers toward India, Europe and the United States.

5. Why is demand rising in clinical diagnostic laboratories?

Post-pandemic PCR infrastructure, rapid regulatory clearances and automation investments are driving a 6.81% CAGR for clinical labs through 2030.

Page last updated on: