In-vitro Diagnostics Enzymes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

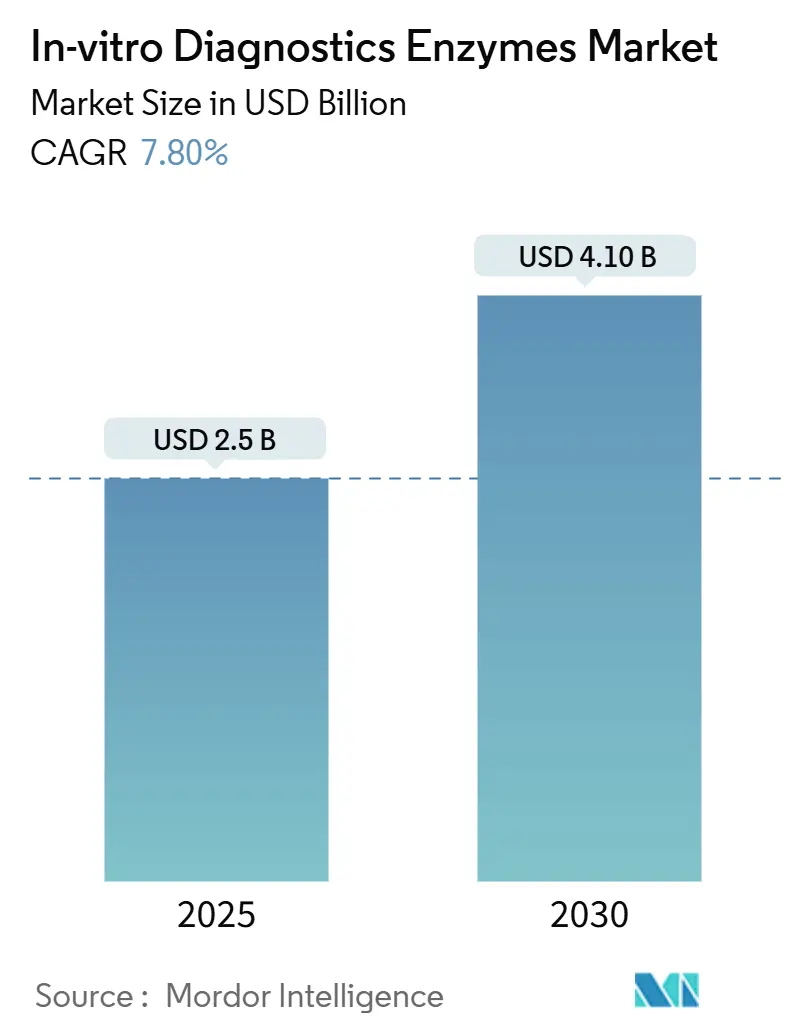

| Market Size (2025) | USD 2.5 Billion |

| Market Size (2030) | USD 4.10 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

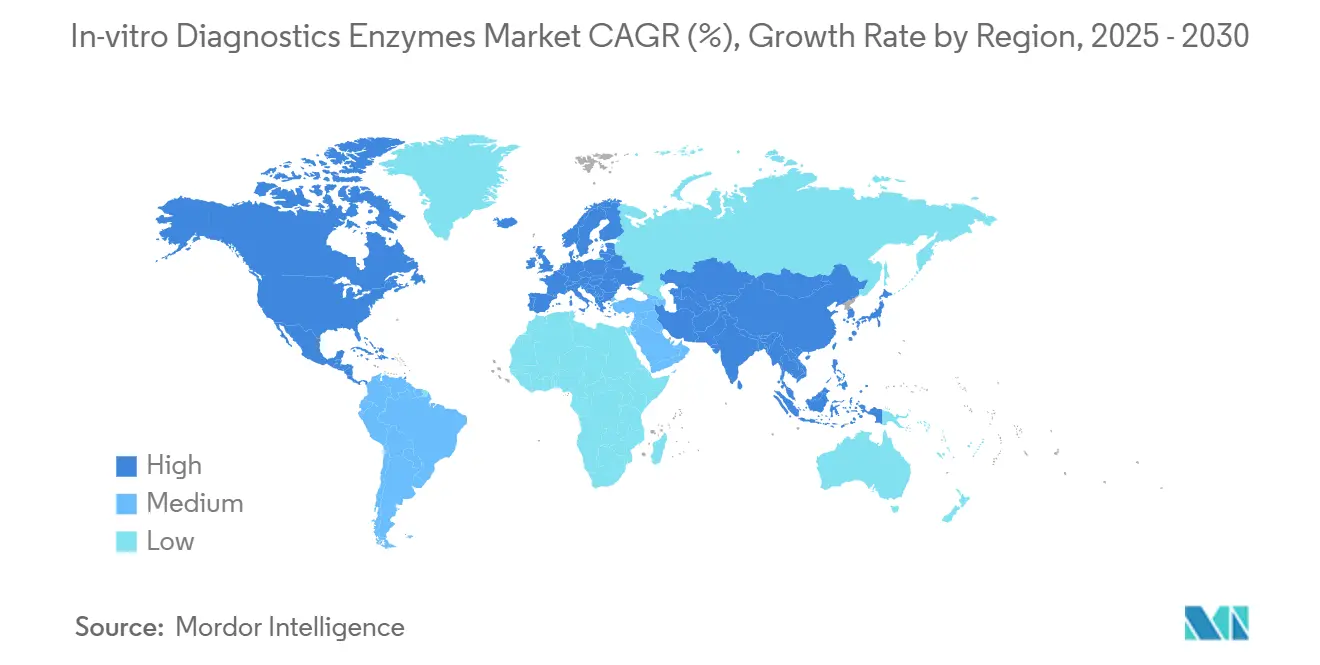

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-vitro Diagnostics Enzymes Market Analysis by Mordor Intelligence

The in-vitro diagnostics enzymes market size stood at USD 2.5 billion in 2025 and is forecast to reach USD 4.1 billion by 2030, advancing at a 7.8% CAGR during 2025-2030. This trajectory rests on high-fidelity enzyme engineering, automation-ready formulations, and the rapid adoption of companion diagnostics that rely on specialized enzymatic workflows. The in-vitro diagnostics enzymes market benefits from expanding next-generation sequencing (NGS) pipelines that demand polymerases with error rates below 1 in 10^6 nucleotides. Laboratories continue to embed lyophilized reagents into automated systems, cutting protocol time by up to 30% and lowering cold-chain dependence. In the short term, syndromic infectious-disease panels and point-of-care (POC) molecular tests are raising enzyme consumption, while vertical integration across reagent and instrument supply chains mitigates the price volatility exposed during recent global disruptions.

Key Report Takeaways

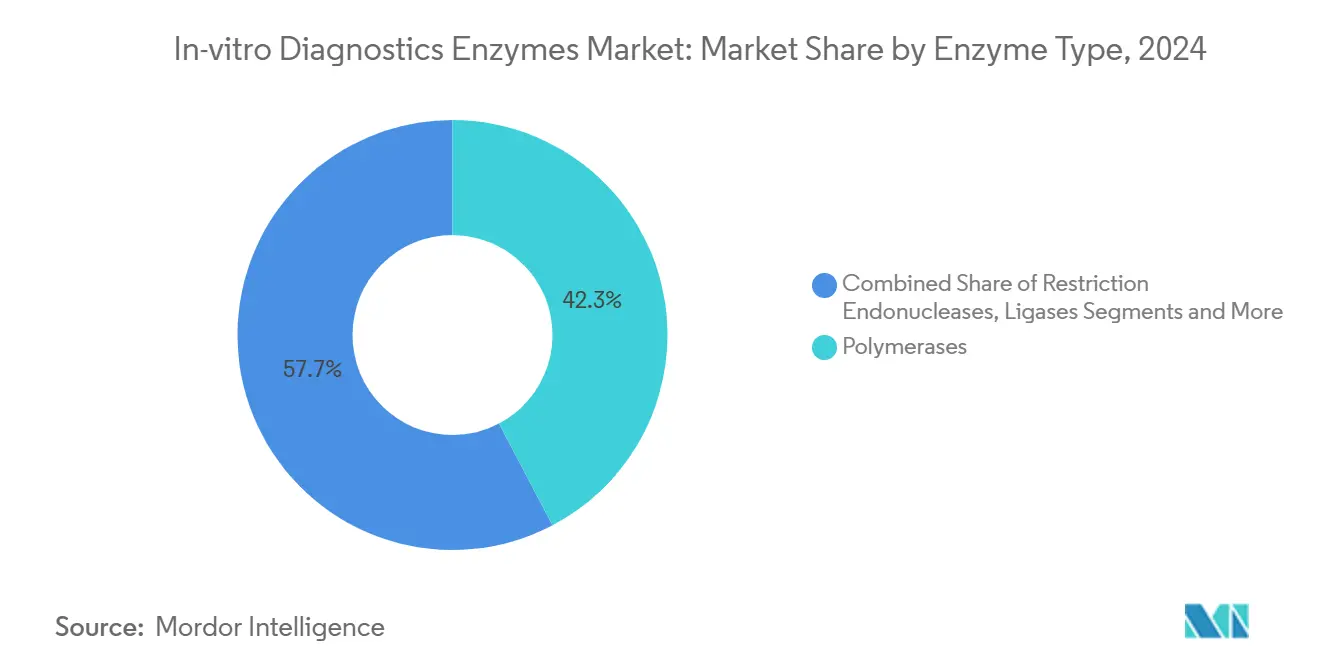

- By enzyme type, polymerases led with 42.3% of the in-vitro diagnostics enzymes market share in 2024, whereas ligases are projected to grow at an 8.8% CAGR through 2030.

- By diagnostic technique, PCR/qPCR retained 55.1% revenue share in 2024; isothermal amplification platforms are set to expand at a 7.2% CAGR to 2030.

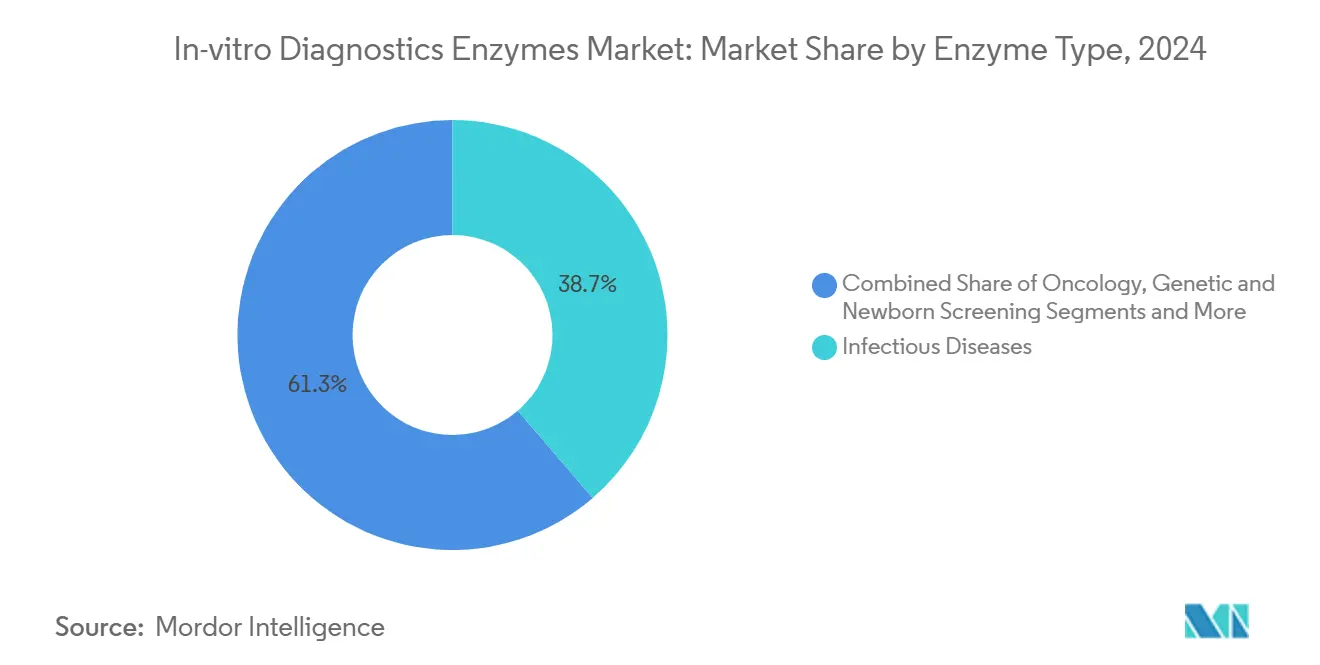

- By disease application, infectious diseases accounted for 38.7% of the in-vitro diagnostics enzymes market size in 2024, while oncology solutions are advancing at an 8.5% CAGR during the forecast window.

- By end user, diagnostic reference laboratories held 46.9% share of the in-vitro diagnostics enzymes market size in 2024, whereas POC sites are pacing at a 9.6% CAGR through 2030.

- By region, North America captured 43.8% revenue share in 2024, while Asia Pacific is forecast to grow the fastest at a 7.1% CAGR to 2030.

Global In-vitro Diagnostics Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-fidelity & hot-start polymerases | +1.20% | North America & EU | Medium term (2-4 years) |

| Expansion of point-of-care molecular testing platforms | +1.80% | APAC core; spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Growth of companion diagnostics in oncology | +1.50% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Surge in syndromic infectious-disease panels | +1.10% | Global, faster in emerging markets | Short term (≤ 2 years) |

| Automation-ready lyophilized reagent formats | +0.90% | Global, high utility in emerging economies | Medium term (2-4 years) |

| Government funding for pandemic-preparedness bio-banks | +0.70% | North America, EU, select APAC nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Fidelity & Hot-Start Polymerases

The in-vitro diagnostics enzymes market rests on a core requirement for ultra-low error rates in PCR and qPCR assays. Aptamer-based hot-start systems now enable room-temperature storage, eliminating time-consuming thermal activation steps and shortening assay cycles by up to 30%. These advances free automated platforms from temperature constraints and boost throughput. New RNA polymerases such as PrimeCap T7 lower double-stranded RNA formation to <10%, refining mRNA workflows that feed into emerging diagnostics.[1]PrimeCap™ Product Note, “Mutant T7 RNA Polymerase,” clinicalresearchnewsonline.com The shift from qualitative to quantitative biomarker detection depends on enzymes that preserve template integrity even in multiplexed reactions. Collectively, these innovations reinforce the competitive positioning of suppliers capable of delivering high-fidelity variants across bulk and bespoke formats within the in-vitro diagnostics enzymes market.

Expansion of Point-of-Care Molecular Testing Platforms

Portable instruments integrate lyophilized RT-LAMP and RT-PCR chemistries to deliver laboratory-grade results in under 60 minutes without refrigerated storage.[2]Getchell et al., “Pathogen Genomic Surveillance in Asia,” nature.com Cepheid’s Mpox assay illustrates how enclosed cartridges couple sample prep with enzymatic amplification to yield answers in 36 minutes, supporting decentralized outbreak control. Multiplex platforms such as the RespiDisk panel process 19 respiratory pathogens with only 5 minutes of hands-on time, affirming that automation and enzyme stability jointly underpin POC reliability. As health systems pivot toward distributed diagnostics, the in-vitro diagnostics enzymes market will penetrate settings ranging from retail clinics to home testing, provided formulations withstand wide temperature swings.

Growth of Companion Diagnostics in Oncology

NGS-based companion diagnostics rely on high-performance polymerases and ligases to interrogate low-abundance tumor DNA from liquid biopsies. Collaborations such as Takeda–Foundation Medicine emphasize the need for fully validated enzymatic kits supporting regulatory-cleared genomic panels. QIAGEN’s QIAstat-Dx partnerships broaden multiplex real-time PCR into chronic disease genotyping, reflecting clinician demand for near-patient genomic insight. Digital PCR systems with droplet partitioning sharpen detection thresholds, enabling transplant monitoring and minimal residual disease assessments at sensitivities previously considered impractical. The in-vitro diagnostics enzymes market, therefore, intersects directly with therapeutic decision pathways, securing price premiums for GMP-grade, companion-diagnostic-ready reagents.

Surge in Syndromic Infectious-Disease Panels

FilmArray-style panels condense nucleic acid extraction and multiplex PCR into a single workflow, identifying up to 19 pathogens and elevating clinical sensitivity to 82%-97.1% across specimen types.[3]Armstrong et al., “SARS-CoV-2 Supply Shortages,” asm.org Hospitals adopting such panels have trimmed time to optimal therapy for bloodstream infections from 14.68 hours to 4.65 hours. Molecular multiplex tests under development at Cue Health demonstrate how in-house enzyme production guards against supply disruptions and supports rapid iteration. In aggregate, syndromic testing fortifies antimicrobial stewardship and outbreak containment, cementing enzymes as indispensable components of modern infection control strategies within the in-vitro diagnostics enzymes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply bottlenecks for recombinant enzyme expression systems | −0.8% | Global, larger effect in EMs | Short term (≤ 2 years) |

| Stringent EU IVDR validation costs for OEM enzyme suppliers | −1.1% | Primarily EU | Medium term (2-4 years) |

| Pricing pressure from integrated cartridge-based platforms | −0.9% | Worldwide, highest in developed | Medium term (2-4 years) |

| Cold-chain vulnerabilities in emerging economies | −0.6% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Bottlenecks for Recombinant Enzyme Expression Systems

Pandemic-era shortages highlighted how centralized manufacturing left critical diagnostics without core reagents for tuberculosis and SARS-CoV-2 testing. Academic initiatives such as Stanford’s Open Bioeconomy Lab catalog now disseminate expression cassettes for reverse transcriptase and Bst polymerase, yet scale-out remains limited. To close capacity gaps, Takara Bio expanded its Gothenburg plant to 600,000 reactions per week, although full ramp-up takes 18-24 months. Until regional production matures, supply fragility may temper near-term growth in the in-vitro diagnostics enzymes market.

Stringent EU IVDR Validation Costs for OEM Enzyme Suppliers

The IVDR classifies most laboratory-developed tests as high-risk devices, compelling exhaustive clinical validation and post-market surveillance. Compliance outlays can top EUR 500,000 per enzyme line and strain smaller vendors’ resources. Diagnostic centers report dedicating entire teams to inventory mapping and dossier submission, sometimes discontinuing niche assays when commercial alternatives surface. The regulation, therefore, accelerates consolidation inside the in-vitro diagnostic enzymes market as scale becomes a prerequisite for European market access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enzyme Type: Ligases Accelerate, While Polymerases Dominate

Polymerases captured 42.3% revenue in 2024, cementing their role in amplification workflows that underpin clinical PCR and qPCR. The in-vitro diagnostics enzymes market size for polymerases reached USD 1.1 billion that year, reflecting sustained test volumes in respiratory and sexually transmitted infection screening. Ligases, though smaller, are projected to expand at an 8.8% CAGR, driven by NGS library preparation, where precise fragment joining governs read accuracy. Advanced DNA ligation chemistries now deliver >95% efficiency across GC-rich regions, lowering duplicate reads and saving sequencing costs. Restriction enzymes and nucleases address contamination control and sample prep, holding stable shares amid rising throughput automation. As assays intertwine multiple enzymatic steps, suppliers bundle polymerase-ligase cocktails, reinforcing switching costs and deepening client lock-in within the in-vitro diagnostics enzymes market.

Emerging innovations such as magnetic bead-enabled extraction kits incorporate proteinase and nuclease activities to streamline viral nucleic acid recovery for low-abundance pathogens. Case Western Reserve University’s AMPLON method halves amplification time by skipping extreme temperatures, signaling a potential pivot toward novel enzyme formats that eclipse legacy Taq variants. Collectively, these shifts position ligases as the fastest-growing component while ensuring polymerases remain the revenue anchor of the in-vitro diagnostics enzymes market.

By Diagnostic Technique: PCR Holds Ground as Isothermal Methods Scale

PCR/qPCR generated 55.1% of total sales in 2024, translating into an in-vitro diagnostics enzymes market size of approximately USD 1.3 billion that year. Widespread instrument installations and entrenched clinical protocols preserve PCR’s dominance. Yet isothermal amplification platforms are registering a 7.2% CAGR, propelled by Loop-Mediated Isothermal Amplification (LAMP) and Recombinase Polymerase Amplification (RPA) protocols that thrive without thermal cycling. LAMP produces up to 10^9 copies at 65 °C within an hour, while RPA delivers answers under 30 minutes at ambient temperatures. These characteristics dovetail with POC devices, making isothermal chemistry a critical frontier for the in-vitro diagnostics enzymes market.

Digital PCR technologies such as the QX600 ddPCR system enhance absolute quantification for minimal residual disease, compelling labs to upgrade reagent portfolios. Meanwhile, NGS library prep sustains double-digit growth as oncologists mandate comprehensive genomic profiling for therapy selection. With instrument vendors embedding proprietary enzyme kits, incumbents and new entrants alike fight to secure OEM positions, further intensifying competition in the in-vitro diagnostics enzymes market.

By Disease Application: Infectious Diseases Anchor, Oncology Gains Pace

Infectious-disease assays accounted for 38.7% of 2024 revenue, equating to an in-vitro diagnostics enzymes market size of roughly USD 970 million. Governments stockpiled influenza and coronavirus panels, while hospitals enforced syndromic testing for sepsis and respiratory illnesses. Oncology workflows are projected to climb at an 8.5% CAGR, expanding the segment’s share as liquid biopsy and tumor mutational burden assays enter routine care. Enzymatic fidelity is paramount for detecting allelic fractions below 0.5%, driving premium-priced reagents.

Genetic and newborn screening add steady volumes through centralized programs, whereas cardiometabolic biomarker assays transition from immunoassay to molecular readouts that exploit enzyme-mediated amplification for higher specificity. Novel mitochondrial disorder panels using long-range PCR showcase the breadth of clinical questions addressed by the in-vitro diagnostics enzymes market.

By End User: Reference Labs Lead, POC Sites Accelerate

Reference laboratories processed 46.9% of global test volumes in 2024, benefiting from high-throughput automation platforms that require bulk enzyme procurement. Their scale yields vendor leverage but also heightens demand for performance guarantees and compliant documentation. POC venues—retail clinics, urgent-care centers, and home testing—represent the fastest-growing outlet, posting a 9.6% CAGR as decentralized care gains payer endorsement. Hospital labs preserve critical capacity for inpatient diagnosis, while academic centers drive early-stage assay proof-of-concepts feeding commercial pipelines. Automation advances such as QIAsymphony Connect and SmartChip ND raise throughput efficiency, sustaining enzyme demand across all user classes.

Geography Analysis

North America retained 43.80% share of the in-vitro diagnostics enzymes market in 2024, underpinned by USD 5 billion in federal Project NextGen funding for advanced COVID-19 countermeasures. BARDA’s Accelerator Network further subsidizes early-stage diagnostics, ensuring continuous reagent innovation and uptake. Mature payor systems absorb the premium of validated enzymes by offsetting downstream treatment savings through faster, more precise diagnoses.

Asia Pacific is the fastest-expanding arena, progressing at a 7.1% CAGR to 2030. China leverages extensive biomanufacturing capacity, while Japan’s microfluidics expertise fosters portable, enzyme-laden chips. India scales molecular surveillance for tuberculosis and vector-borne diseases, albeit hampered by cold-chain gaps that can degrade reagent potency during transport. Regional collaborations on pathogen genomic surveillance across 13 nations further enlarge the demand for robust enzyme supply.

Europe exhibits stable growth as laboratories navigate IVDR complexities. Germany, France, and the United Kingdom capitalize on strong biotech ecosystems but incur higher validation expenses that tilt procurement toward large, compliant suppliers. The Middle East & Africa and South America add incremental volumes, driven by Gulf-state hospital expansions and Brazilian public-health investments, respectively. Nonetheless, currency fluctuations and infrastructure limits temper enzyme adoption in price-sensitive settings, nudging vendors to offer smaller, lyophilized pack sizes within the in-vitro diagnostics enzymes market.

Competitive Landscape

The in-vitro diagnostics enzymes market remains moderately fragmented, with the top five companies estimated to control roughly 45% of global revenue. Thermo Fisher Scientific, New England Biolabs, QIAGEN, Takara Bio, and Bio-Rad Laboratories leverage proprietary enzyme engineering platforms and layered patent estates to sustain moats. Strategic integrations—such as Thermo Fisher’s multibillion-dollar M&A war-chest targeting point-of-care innovators—signal ongoing consolidation. Vertical plays bundle cartridges, instruments, and cloud analytics, locking customers into reagent subscription models that offset razor-thin hardware margins.

Collaborations expand technological breadth: Danaher’s partnership with the Innovative Genomics Institute embeds CRISPR nucleases into diagnostic kits, opening adjacent revenue in gene-editing quality control. Takara Bio’s Shasta™ system pushes single-cell NGS throughput to 1,500 cells per run, aligning enzyme development with emerging precision-oncology workflows. Price pressure arises where cartridge vendors internalize the enzyme supply, compressing third-party opportunities. Still, specialty niches like digital PCR, single-cell analysis, and cell-free DNA monitoring leave room for agile entrants, ensuring vibrant competition across the in-vitro diagnostics enzymes market.

In-vitro Diagnostics Enzymes Industry Leaders

Thermo Fisher Scientific

QIAGEN

New England Biolabs

Merck KGaA

Takara Bio

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Takara Bio Europe expanded its Gothenburg site with a custom enzyme plant able to turn out 600,000 PCR and qPCR reactions a week, cutting prototyping cycles from months to weeks while meeting diagnostic-grade quality standards.

- May 2024: Takara Bio Europe launched PrimeCap T7 RNA polymerase, a mutant enzyme that keeps double-stranded RNA below 10% while achieving 95% capping efficiency. This allows mRNA developers to cut cap-analog use fourfold and lower immunogenicity risks.

- April 2024: Bio-Rad Laboratories and Oncocyte partnered to refine droplet digital-PCR enzymes that can more sensitively spot donor-derived cell-free DNA for transplant monitoring.

- March 2024: New England Biolabs debuted LyoPrime freeze-dried enzyme formats—high-fidelity polymerases, reverse transcriptases, and nucleases—that keep full activity without refrigeration, easing global shipping and supporting field diagnostics.

Global In-vitro Diagnostics Enzymes Market Report Scope

| Polymerases |

| Restriction Endonucleases |

| Ligases |

| Proteases (e.g., Proteinase K) |

| Nucleases (DNase/RNase) |

| PCR / qPCR / dPCR |

| Isothermal Amplification (LAMP, RPA) |

| NGS Library Preparation |

| Immunoassay / ELISA |

| Clinical Chemistry Workflows |

| Infectious Diseases |

| Oncology |

| Genetic & Newborn Screening |

| Cardiometabolic Disorders |

| Blood-bank & Transfusion Safety |

| Diagnostic Reference Laboratories |

| Hospital & Clinical Laboratories |

| Point-of-Care Testing Sites |

| Academic & Research Institutes |

| Pharma & Biotech Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Enzyme Type | Polymerases | |

| Restriction Endonucleases | ||

| Ligases | ||

| Proteases (e.g., Proteinase K) | ||

| Nucleases (DNase/RNase) | ||

| By Diagnostic Technique | PCR / qPCR / dPCR | |

| Isothermal Amplification (LAMP, RPA) | ||

| NGS Library Preparation | ||

| Immunoassay / ELISA | ||

| Clinical Chemistry Workflows | ||

| By Disease Application | Infectious Diseases | |

| Oncology | ||

| Genetic & Newborn Screening | ||

| Cardiometabolic Disorders | ||

| Blood-bank & Transfusion Safety | ||

| By End User | Diagnostic Reference Laboratories | |

| Hospital & Clinical Laboratories | ||

| Point-of-Care Testing Sites | ||

| Academic & Research Institutes | ||

| Pharma & Biotech Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is expected for the in-vitro diagnostics enzymes market between 2025 and 2030?

The market is projected to advance at a 7.8% CAGR during 2025-2030.

Which enzyme class is forecast to grow fastest through 2030?

Ligases are set to register the quickest rise, at an 8.8% CAGR, thanks to their expanding role in NGS library preparation.

Why are isothermal amplification techniques gaining momentum?

They remove thermal cycling, enabling portable devices that deliver results in under an hour at constant temperatures.

Which region will witness the highest growth rate in enzyme demand?

Asia Pacific is anticipated to expand at a 7.1% CAGR, fueled by widespread investments in molecular testing infrastructure.

How is EU IVDR affecting enzyme suppliers?

The regulation increases validation costs, prompting consolidation as only well-capitalized firms can meet stringent compliance requirements.

What recent acquisition strengthens Bio-Rads digital PCR portfolio?

The companys February 2025 offer to acquire Stilla Technologies adds the Nio® digital PCR systems to its diagnostics lineup.

Page last updated on: