Enzymatic DNA Synthesis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

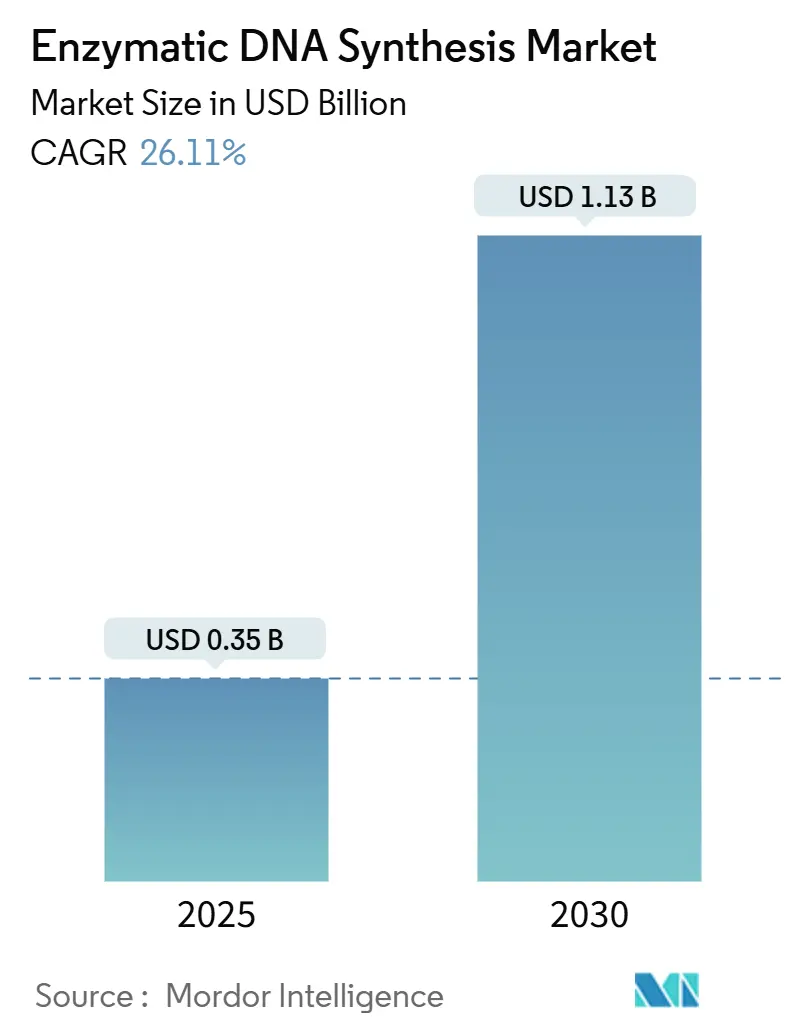

| Market Size (2025) | USD 0.35 Billion |

| Market Size (2030) | USD 1.13 Billion |

| Growth Rate (2025 - 2030) | 26.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Enzymatic DNA Synthesis Market Analysis by Mordor Intelligence

The enzymatic DNA synthesis market size reached USD 355.82 million in 2025 and is forecast to grow to USD 1.134 billion by 2030, advancing at a 26.11% CAGR. Venture-capital investments topping USD 1 billion since 2023, AI-designed polymerases that push error rates below 0.05% per kilobase, and defense-funded distributed biomanufacturing mandates collectively accelerate adoption across research and therapeutic pipelines. Corporations pursuing net-zero targets increasingly favor solvent-free workflows that cut solvent use by 90% and shrink environmental impacts. North America holds leadership with 43.56% revenue share, yet the Asia-Pacific region is expanding fastest on the back of regulatory harmonization and new biopharmaceutical capacity. Gene and cell therapy remain the largest application area, while DNA data storage records the most rapid gains as cloud providers test terabyte-scale prototypes.

Key Report Takeaways

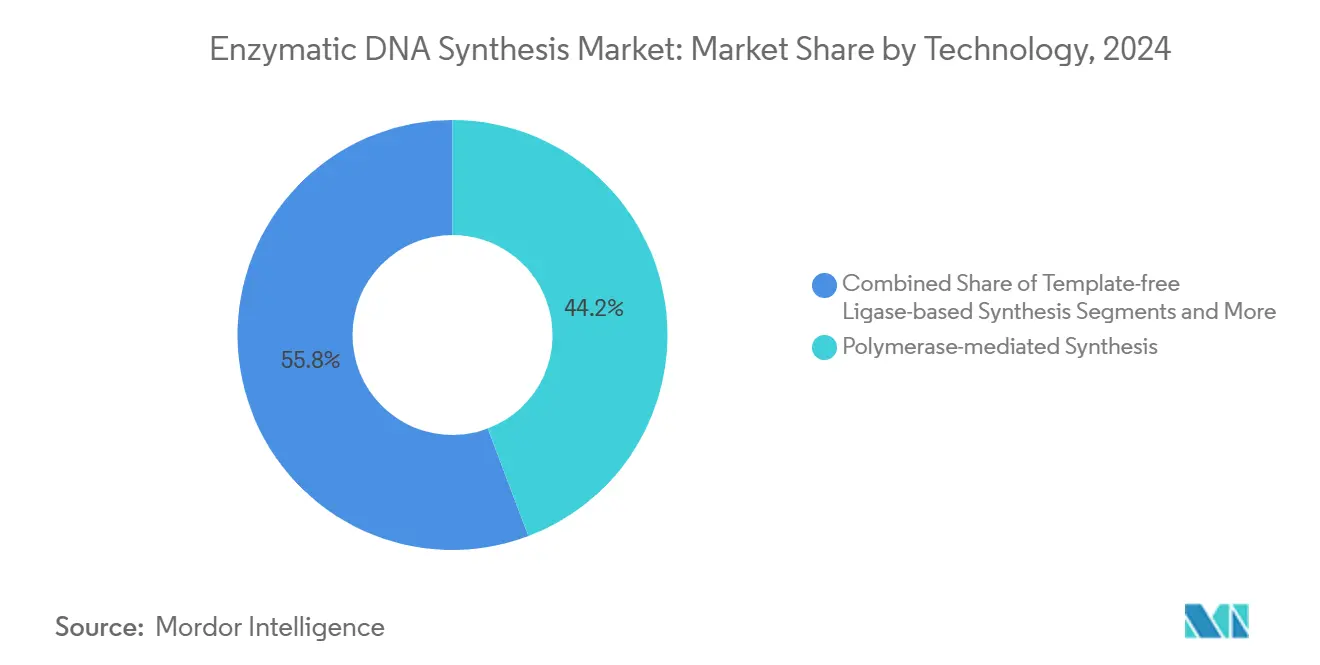

- By technology, polymerase-based platforms led with 44.25% of the enzymatic DNA synthesis market share in 2024, while TdT systems are projected to climb at a 30.42% CAGR through 2030.

- By application, gene and cell therapy held 36.73% of revenue in 2024; DNA data storage is forecast to expand at a 39.58% CAGR to 2030.

- By fragment length, short oligos accounted for 53.47% share of the enzymatic DNA synthesis market size in 2024 and long constructs are advancing at a 28.41% CAGR through 2030.

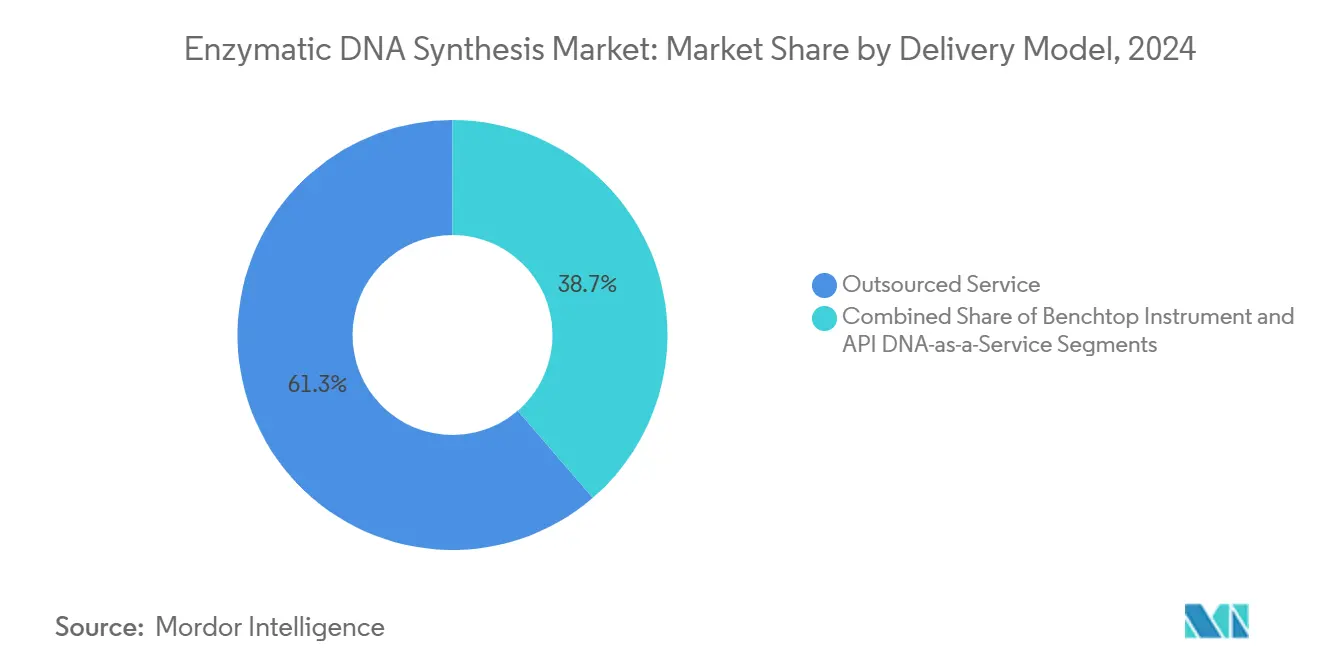

- By delivery model, outsourced services commanded 61.32% of revenue in 2024; benchtop instruments are rising at a 29.66% CAGR to 2030.

- By end user, pharmaceutical and biotechnology companies controlled 51.74% of 2024 demand, whereas synthetic-biology start-ups show the fastest growth at 29.39% CAGR through 2030.

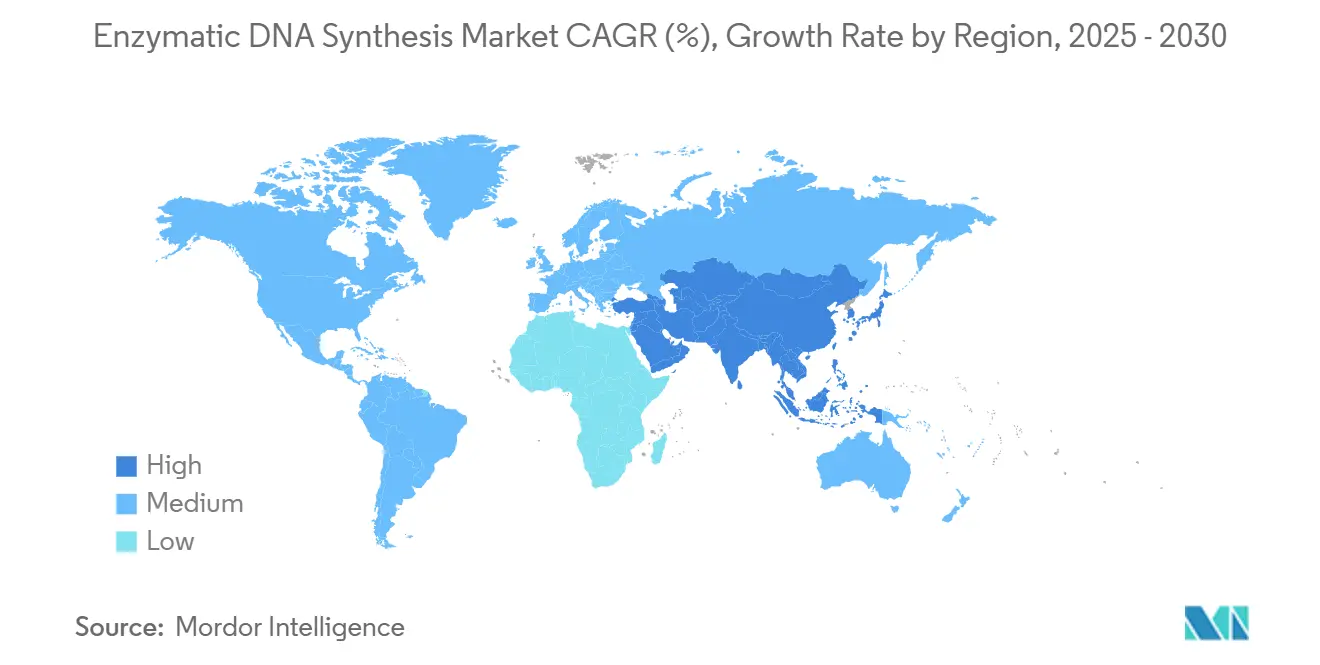

- By geography, North America led with 43.56% revenue share in 2024, but Asia-Pacific is on track for a 28.79% CAGR to 2030.

Global Enzymatic DNA Synthesis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling oligo synthesis costs below USD 0.01 per base in benchtop instruments | +4.2% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Accelerating demand for long (>5 kb) gene fragments in cell- and gene-therapy pipelines | +5.8% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Venture-capital inflow topping USD 1 billion since 2023 for benchtop enzymatic platforms | +3.9% | Global, concentrated in United States, United Kingdom, Germany | Short term (≤ 2 years) |

| AI-designed polymerases cutting error rates to <0.05% per kilobase | +4.7% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Defense-funded distributed biomanufacturing mandates for rapid DNA-on-demand | +3.1% | United States first, expanding to allied nations | Long term (≥ 4 years) |

| Corporate net-zero targets favoring solvent-free synthesis workflows | +2.8% | Global, strongest traction in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling Oligo Synthesis Costs Below USD 0.01 per Base in Benchtop Instruments

Array-based production now delivers bases at USD 0.00001 to 0.001, slashing research costs and opening access for smaller laboratories.[1]R. Tromans, “Synthesis of Short DNA and RNA Fragments by Resonant Acoustic Mixing,” Royal Society of Chemistry, pubs.rsc.org Benchtop enzymatic devices remove phosphoramidite reagents and cut hands-on time by 85%, while resonant acoustic mixing lowers solvent use by 90% at comparable yields.[2]M. Edmonds, “Sequence Preference and Initiator Promiscuity for De Novo DNA Synthesis by TdT,” National Institutes of Health, ncbi.nlm.nih.gov The cost plunge accelerates synthetic-biology prototyping and de-risks large gene orders. ISO 9001 quality systems underpin manufacturing consistency, and the FDA’s Advanced Manufacturing Technologies program offers regulatory clarity for innovators. Capital-equipment vendors report rising install bases in academic settings, pointing to durable demand over the next two years.

Accelerating Demand for Long (>5 kb) Gene Fragments in Cell- and Gene-Therapy Pipelines

Therapies such as Casgevy confirm clinical utility for long DNA constructs, with 29 of 31 patients experiencing pain relief. Enzymatic platforms surpass chemical methods by delivering full antibody variable regions in weeks rather than months. Engineered TdT reaches 98.7% stepwise yields for extended sequences, and AI-guided enzyme design further boosts performance. Regulators have updated genome-editing guidance, streamlining pre-IND discussions and accelerating approvals. Demand for bigger payloads underpins strong medium-term tailwinds, especially in North America and Europe, before spreading to Asia-Pacific by 2028.

Venture-Capital Inflow Topping USD 1 Billion Since 2023 for Benchtop Enzymatic Platforms

Investors view enzymatic synthesis as a keystone of distributed biomanufacturing. Funding rounds such as Constructive Bio’s USD 58 million Series A, Elegen’s USD 35 million Series B, and Molecular Assemblies’ USD 12.2 million Series A highlight momentum. AI-based enzyme design firms attract additional capital, proven by Biomatter’s EUR 6.5 million seed round. Strategic alliances with pharmaceutical majors, such as GSK’s licensing agreement with Elegen, further validate commercial potential. Institutional investors cite clear FDA and GMP frameworks as risk mitigants, supporting near-term deployment of new benchtop systems.

AI-Designed Polymerases Cutting Error Rates to <0.05% per Kilobase

Machine-learning algorithms now iterate polymerase variants in weeks, not years, achieving fidelity that eclipses phosphoramidite chemistry. University of California researchers engineered the 10-92 TNA polymerase, boosting efficiency for synthetic genetic materials. Biomatter’s Intelligent Architecture platform designs de novo enzymes without natural templates, serving partners such as Thermo Fisher Scientific. DARPA’s Living Foundries program integrates AI and automation to accelerate prototyping. Improved fidelity unlocks regulatory confidence and propels medium-term adoption across therapeutics and data storage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| In-house phosphoramidite capacity still cheaper at ≥10 g scale | -2.8% | Global, especially established pharma in North America and EU | Medium term (2-4 years) |

| IP thickets around TdT blocking freedom-to-operate for newcomers | -1.9% | United States and European patent jurisdictions | Long term (≥ 4 years) |

| Enzyme batch-to-batch variability causing QC failures | -2.1% | Global manufacturing hubs, regulated markets | Short term (≤ 2 years) |

| Low availability of modified nucleotides for enzymatic routes | -1.7% | Asia-Pacific supply chains, spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

In-House Phosphoramidite Capacity Still Cheaper at ≥10 g Scale

Large pharmaceutical plants already amortized solid-phase equipment that delivers DNA at lower unit costs when runs exceed 10 grams. Chemical platforms also manage hundreds of sequences in parallel, exploiting scale economies. Enzymatic methods currently face throughput limitations and higher enzyme costs. Some manufacturers therefore keep chemical synthetic lines for bulk production while reserving enzymatic systems for specialty constructs. As enzyme prices fall and reactor designs mature, the cost disadvantage should narrow by 2029, yet near-term headwinds persist.

IP Thickets Around TdT Blocking Freedom-to-Operate for Newcomers

A dense patent landscape surrounds TdT engineering and template-free extension chemistries, raising litigation risks for start-ups.[3]James Field, “DNA Synthesis and Sequencing Costs and Productivity for 2025,” Synthesis, synthesis.cc Licensing negotiations can slow product launches and deter investors. Companies are responding by engineering alternate polymerases or pursuing hybrid approaches to sidestep protected claims. Regulatory agencies remain technology-agnostic, but filings must carefully detail intellectual-property positions to secure approvals. The restraint is most pronounced in the United States and Europe, where enforcement is strict.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Polymerase-Based Platforms Sustain Leadership

Polymerase-mediated systems held a 44.25% share of the enzymatic DNA synthesis market in 2024, anchored by familiar workflows and broad reagent availability. TdT platforms, though newer, are projected to post a 30.42% CAGR, propelled by template-free extension that accommodates complex or repetitive motifs. The enzymatic DNA synthesis market size for polymerase platforms is expected to surpass USD 500 million by 2030, while TdT revenues climb even faster on a smaller base. Ligase-based and hybrid chemistries address niche requirements for precise sequence control or modified bases, and XNA synthesis is gaining interest for gene-editing applications that demand novel backbones.

A competitive race focuses on read length, fidelity, and automation. Ansa Biotechnologies already delivers 600-bp direct syntheses and targets 5,000 bp by year-end 2025. Camena Bioscience promotes a TdT-free strategy to curb sequence bias. Regulatory designations under the FDA Advanced Manufacturing Technologies umbrella streamline adoption, giving compliant vendors a marketing edge. Over the forecast horizon, the enzymatic DNA synthesis market will feature coexistence of multiple chemistries, each optimized for distinct end-user goals.

By Application: Therapeutic Uses Dominate Revenue

Gene and cell therapy retained 36.73% of 2024 turnover, driven by approvals such as Casgevy for sickle-cell disease. The enzymatic DNA synthesis market size serving therapeutic developers is forecast to exceed USD 400 million by 2030 as pipeline assets multiply. DNA data storage, while nascent, shows the fastest rise at 39.58% CAGR as Microsoft and Twist prove terabyte-scale prototypes. CRISPR guide-RNA libraries, synthetic-biology circuit construction, and diagnostics remain steady contributors, benefitting from faster turnaround times.

Partnerships illustrate momentum: GSK licensed Elegen’s ENFINIA DNA to accelerate RNA-based vaccines. Twist Bioscience extended gene fragments to 5 kb with two-day delivery, courting protein-engineering and mRNA customers. Regulators have issued plasmid DNA vaccine guidelines, offering clear submission paths in the European Union. Overall, therapeutic and storage segments will continue to pull the enzymatic DNA synthesis market forward with divergent but complementary growth arcs.

By Fragment Length: Long Constructs Gain Traction

Short oligos under 200 nt dominated 53.47% of revenue in 2024 due to pervasive use in PCR and sequencing. Yet demand for multi-kilobase fragments is escalating, with long constructs forecast to grow at 28.41% CAGR. The enzymatic DNA synthesis market share for long fragments will expand as TdT and polymerase hybrids push reliable synthesis past 1,000 bp. Gene fragments between 200 nt and 5 kb bridge research and therapeutic needs, representing the largest incremental revenue pool through 2030.

Ansa demonstrated 1,005-base yields at 99.9%, underscoring technical feasibility. DNA Script and Evonetix compete on turnaround times and automation for benchtop users. As downstream applications require ever-longer templates, suppliers that combine high-fidelity enzymes with scalable instrumentation will capture outsized value.

By Delivery Model: Benchtop Systems Reshape Access

Outsourced synthesis services captured 61.32% of 2024 revenue, reflecting long-standing customer relationships and capacity. Nevertheless, benchtop instruments are projected to post a 29.66% CAGR, aided by falling capital costs and IP-sensitive programs. The enzymatic DNA synthesis market size for benchtop solutions could top USD 300 million by 2030. Cloud-linked ordering portals and API integration facilitate automated design-to-build workflows, while biosecurity policies are homing in on mandatory sequence screening.

Kilobaser offers personal synthesizers priced below EUR 50,000, completing cycles in 2.5 minutes. Telesis Bio secured USD 21 million to accelerate Gibson SOLA platform uptake, enabling overnight mRNA transcription. Governance frameworks, including export controls for dual-use equipment, will shape market penetration, yet the flexibility of on-site manufacturing supports strong growth across industry and defense settings.

By End User: Pharma Leads, Start-ups Accelerate

Pharmaceutical and biotechnology companies accounted for 51.74% of sales during 2024, relying on enzymatic synthesis for vaccine and gene-therapy pipelines. Synthetic-biology start-ups represent the fastest-growing cohort at 29.39% CAGR, buoyed by venture capital and sustainability-driven products. Academic institutes, CROs, and CDMOs maintain steady demand, while defense labs procure systems for rapid countermeasure development.

GSK’s multi-year pact with Elegen underscores big-pharma engagement. DARPA’s awards support prototype factories aimed at producing 1,000 molecules for field use. Funding constraints within academia pose minor headwinds, but overall, user diversity strengthens the resilience of the enzymatic DNA synthesis market.

Geography Analysis

North America retained leadership with 43.56% revenue share in 2024, anchored by venture funding clusters in California and Massachusetts and by clear FDA guidance on advanced manufacturing. The United States Department of Defense invested heavily in distributed biomanufacturing, accelerating domestic capacity. Canada’s university consortia and Mexico’s contract-manufacturing hubs complement regional demand.

Asia-Pacific shows the fastest expansion at a 28.79% CAGR to 2030 as China green-lights gene-edited crops and scales mRNA facilities. Japan, South Korea, and Singapore leverage precision-engineering strengths to develop compact instruments, while India’s pharmaceutical sector pursues in-house DNA production. Australia’s academic network drives fundamental enzyme research, fostering regional innovation.

Europe maintains steady momentum through clusters in Germany, the United Kingdom, and France, where EMA guidance supports plasmid DNA vaccines. Sustainability regulations create demand for solvent-free methods, positioning enzymatic synthesis as a compliance tool. Middle East and Africa are in early adoption phases, focusing on healthcare infrastructure, while South America, led by Brazil and Argentina, invests in biotech parks that will gradually lift regional uptake. Collectively, geographic diversification cushions the enzymatic DNA synthesis market against localized slowdowns.

Competitive Landscape

The market remains fragmented, with no single firm holding more than 20% share, leaving room for innovation and alliances. Twist Bioscience combines proprietary high-fidelity polymerases with vertical manufacturing to streamline costs. DNA Script advances benchtop instruments using TdT chemistry, while Ansa and Camena differentiate through sequence length or bias mitigation. Elegen’s collaboration with GSK worth USD 35 million confirms appetite for strategic partnerships.

Acquisitions signal consolidation: Maravai LifeSciences bought Officinae Bio’s DNA/RNA unit to boost AI-enabled mRNA manufacturing. Large suppliers strengthen supply-chain control by developing in-house enzymes, reducing dependency on external vendors. Patent constraints drive some start-ups toward hybrid or novel chemistries to avoid litigation. Quality-assurance capabilities and GMP certifications serve as key purchasing criteria, particularly for therapeutics.

Market players increasingly join policy initiatives such as the U.S. Department of Commerce AI Safety Consortium, advocating responsible bio-automation. Competitive intensity will likely rise as academic spin-outs mature and as electronics firms enter instrument manufacturing. Overall, collaboration, vertical integration, and regulatory readiness will determine long-term winners in the enzymatic DNA synthesis market.

Enzymatic DNA Synthesis Industry Leaders

-

Ansa Biotechnologies

-

Twist Bioscience

-

Telesis Bio

-

DNA Script

-

Molecular Assemblies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Telesis Bio secured up to USD 21 million to advance Gibson SOLA for rapid on-site DNA and mRNA synthesis.

- February 2025: Twist Bioscience reported record quarterly revenue and expanded its enzymatic DNA synthesis platform.

- February 2025: Maravai LifeSciences finalized its acquisition of Officinae Bio’s DNA/RNA business to deepen AI-enabled mRNA production.

Global Enzymatic DNA Synthesis Market Report Scope

| Polymerase-mediated synthesis |

| Terminal deoxynucleotidyl transferase (TdT) |

| Template-free ligase-based synthesis |

| Hybrid chemical-enzymatic workflows |

| Xeno-nucleic-acid (XNA) synthesis platforms |

| Gene & Cell Therapy |

| CRISPR Genome Editing |

| Synthetic Biology & Metabolic Engineering |

| Diagnostics (PCR / NGS Library Prep) |

| DNA Data Storage |

| Vaccine & mRNA Production |

| Short Oligos (<200 nt) |

| Gene Fragments (200 nt – 5 kb) |

| Long Constructs (>5 kb) |

| Benchtop Instrument |

| Outsourced Service |

| Cloud-based / API DNA-as-a-Service |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| CROs / CDMOs |

| Synthetic-Biology Start-ups |

| Government & Defense Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Polymerase-mediated synthesis | |

| Terminal deoxynucleotidyl transferase (TdT) | ||

| Template-free ligase-based synthesis | ||

| Hybrid chemical-enzymatic workflows | ||

| Xeno-nucleic-acid (XNA) synthesis platforms | ||

| By Application | Gene & Cell Therapy | |

| CRISPR Genome Editing | ||

| Synthetic Biology & Metabolic Engineering | ||

| Diagnostics (PCR / NGS Library Prep) | ||

| DNA Data Storage | ||

| Vaccine & mRNA Production | ||

| By Fragment Length | Short Oligos (<200 nt) | |

| Gene Fragments (200 nt – 5 kb) | ||

| Long Constructs (>5 kb) | ||

| By Delivery Model | Benchtop Instrument | |

| Outsourced Service | ||

| Cloud-based / API DNA-as-a-Service | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| CROs / CDMOs | ||

| Synthetic-Biology Start-ups | ||

| Government & Defense Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the enzymatic DNA synthesis market?

The market was valued at USD 355.82 million in 2025 and is projected to grow rapidly.

Which region is expanding fastest?

Asia-Pacific is forecast to post the highest CAGR of 28.79% through 2030.

Which application area leads revenue?

Gene and cell therapy holds the largest share at 36.73% of 2024 revenue.

What technology segment is gaining momentum?

TdT-based platforms are expected to expand at a 30.42% CAGR to 2030.

Why are benchtop instruments important?

They provide rapid, on-site synthesis, protecting intellectual property and reducing lead times.

How will sustainability affect adoption?

Solvent-free enzymatic methods align with corporate net-zero goals, accelerating uptake.

Page last updated on: