Gene Amplification Technologies Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

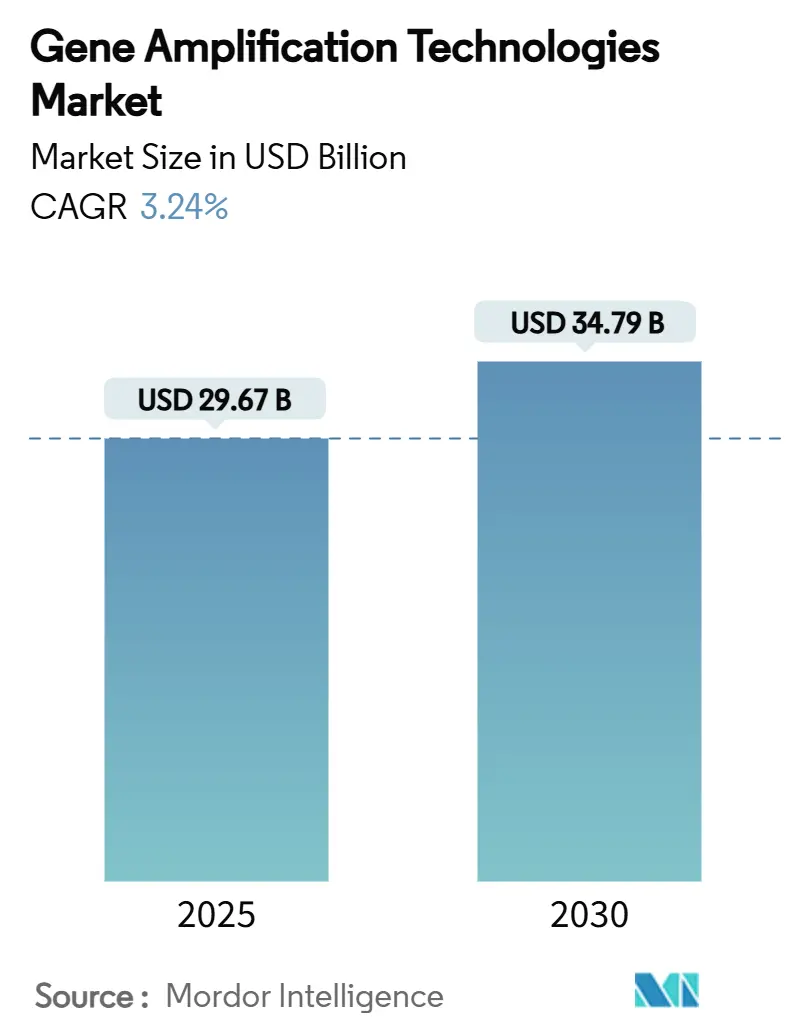

| Market Size (2025) | USD 29.67 Billion |

| Market Size (2030) | USD 34.79 Billion |

| Growth Rate (2025 - 2030) | 3.24% CAGR |

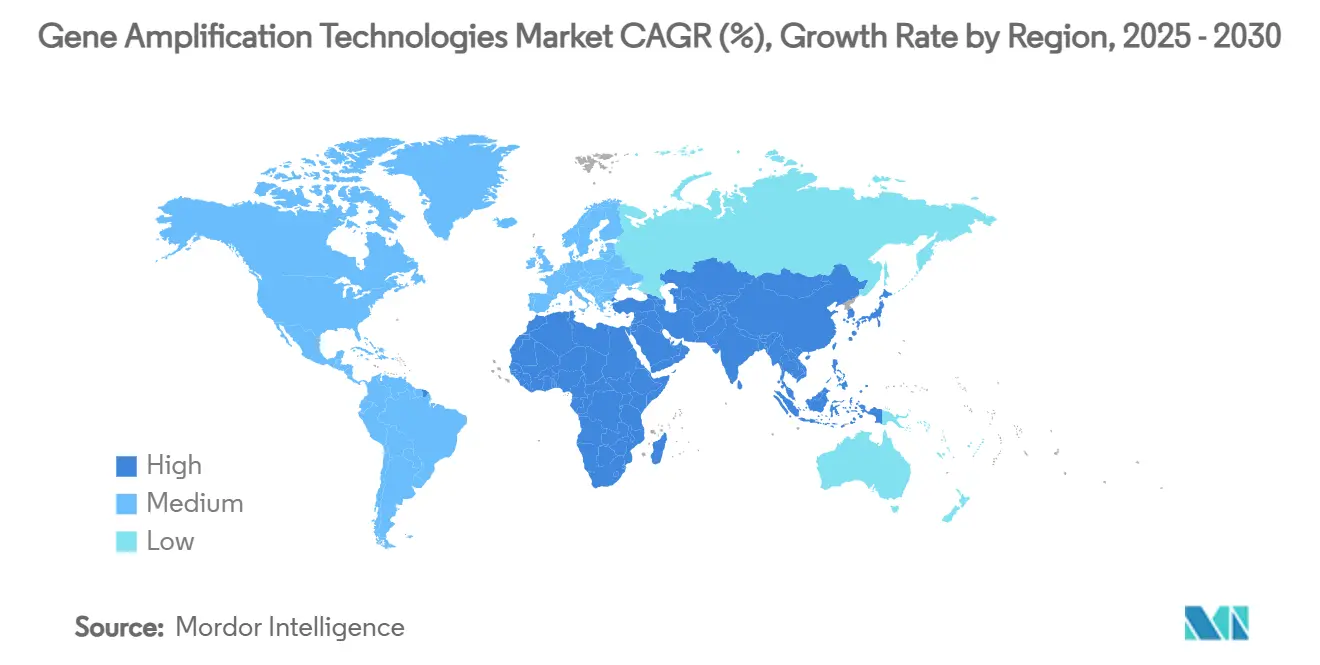

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

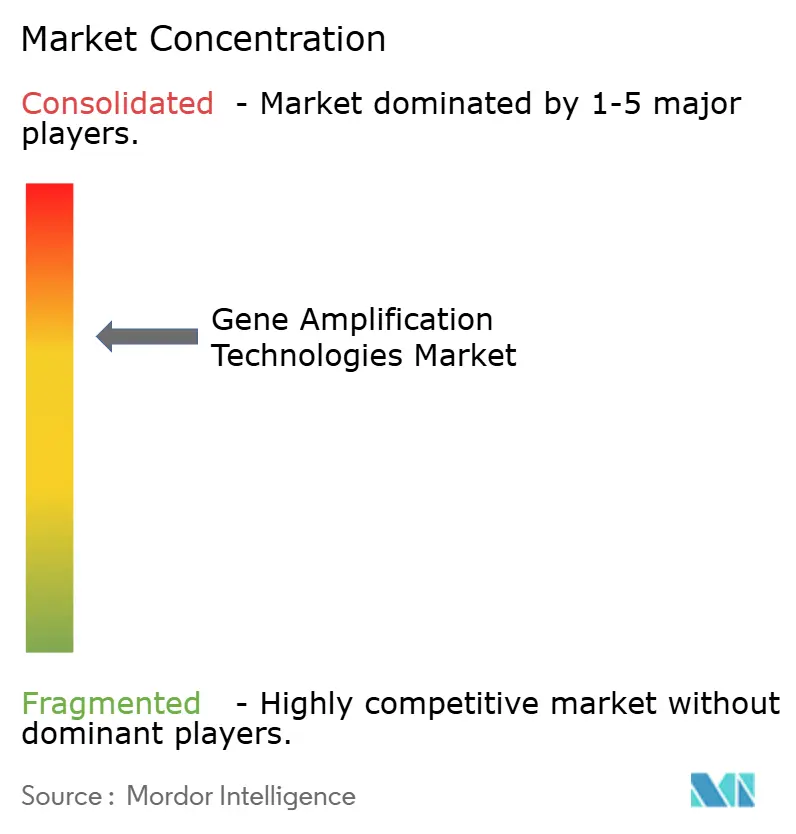

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gene Amplification Technologies Market Analysis by Mordor Intelligence

The gene amplification technologies market size reached USD 29.67 billion in 2025 and is on track to hit USD 34.79 billion by 2030, translating into a 3.24% CAGR during the forecast period; this steady trajectory reflects a shift from pandemic-era volume testing toward precision-focused applications. Redeployment of COVID-driven PCR capacity, falling next-generation sequencing (NGS) costs, and a wave of companion-diagnostic approvals are the primary growth levers, while stringent IVDR and FDA rules temper near-term expansion. Incumbents are responding by bundling instruments, reagents, software, and services into integrated offerings that lock in customers and create recurring revenue streams. Government programs such as ARPA-H’s USD 1.5 billion budget allocation are de-risking breakthrough platforms, especially those geared toward liquid biopsy and cell-free gene therapy workflows. Asia-Pacific’s cost-competitive manufacturing of micro-reactor chips and roll-to-roll fluidics is forecast to accelerate technology diffusion beyond high-income economies, widening the addressable base for the gene amplification technologies market.

Key Report Takeaways

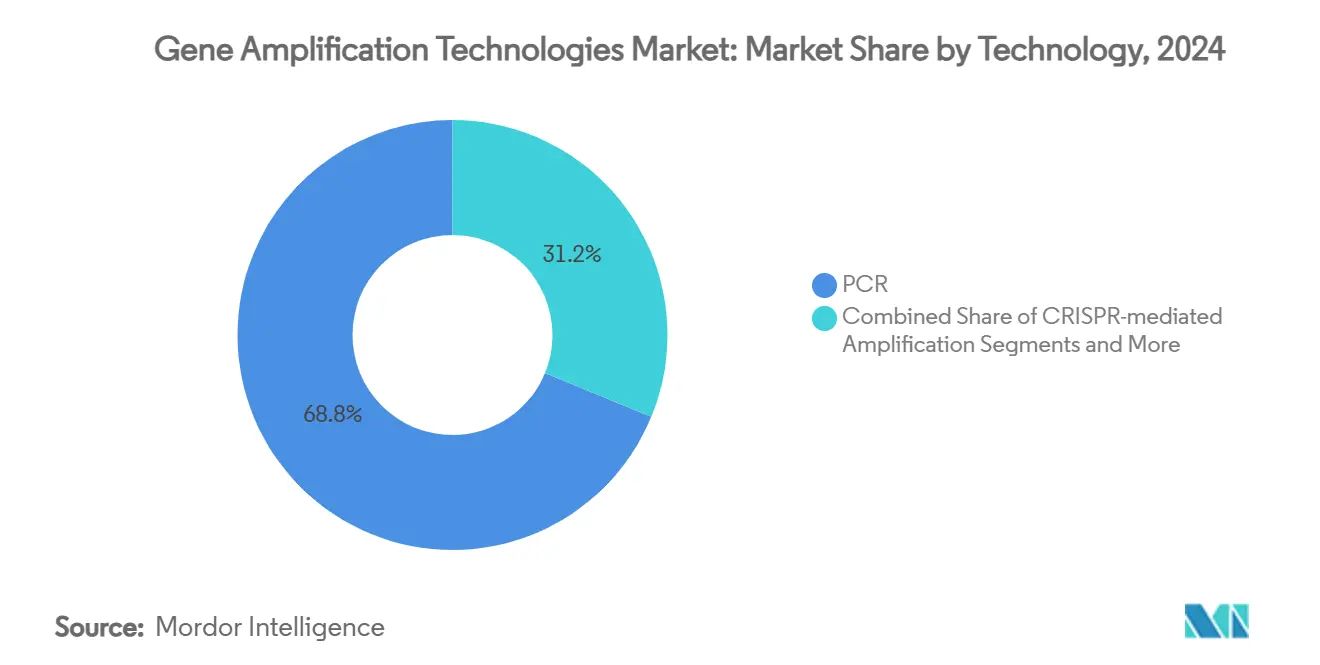

- By technology, PCR led with 68.79% of the gene amplification technologies market share in 2024; CRISPR-mediated amplification is projected to expand at a 6.44% CAGR through 2030.

- By product, reagents and consumables accounted for 54.32% of the 2024 gene amplification technologies market size, while software and services registered the fastest forecast CAGR at 7.69%.

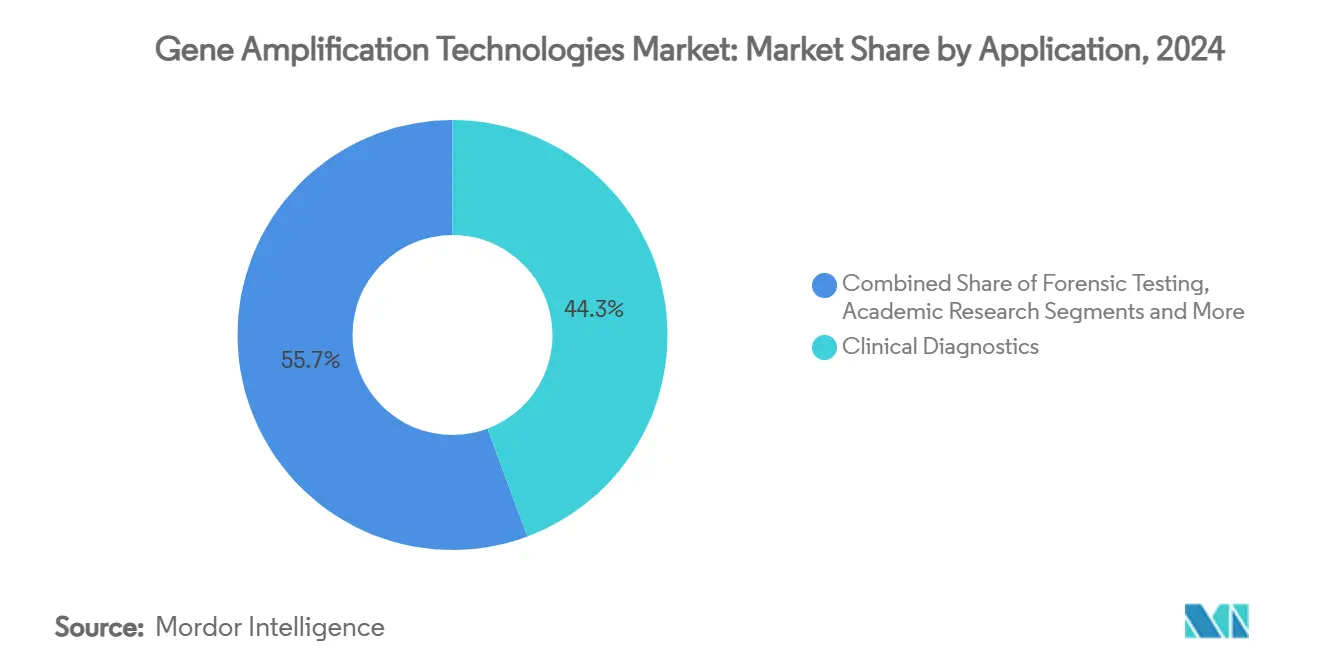

- By application, clinical diagnostics captured 44.33% revenue share in 2024; forensic testing is poised to rise at a 6.89% CAGR to 2030.

- By end-user, hospitals and diagnostic centers held 38.67% of the 2024 gene amplification technologies market share, whereas contract research organizations are advancing at a 5.78% CAGR over the same period.

- By geography, North America dominated with 38.52% share in 2024; Asia-Pacific is expected to deliver the highest regional CAGR of 5.89% through 2030.

Global Gene Amplification Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In PCR-Based COVID Legacy Capacity Redeployed For Oncology & Rare-Disease Testing | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Falling NGS Cost Per Gb Enabling Ultra-High Multiplex Amplicon Panels | +0.6% | Global, with early adoption in APAC and North America | Long term (≥ 4 years) |

| Expansion Of Companion-Diagnostic Approvals That Mandate Nucleic-Acid Amplification Tests | +0.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Government Genomics Moonshots (E.G., U.S. ARPA-H) Funding Core Amplification Platforms | +0.4% | North America, with spillover to allied nations | Long term (≥ 4 years) |

| Integration Of Roll-To-Roll Fluidics Micro-Reactors Boosting Throughput 10× | +0.3% | Global, with manufacturing hubs in APAC | Long term (≥ 4 years) |

| AI-Optimised Thermal-Cycling Algorithms Cutting Run-Time By 40% In Forensic Kits | +0.2% | Global, with early adoption in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in PCR Capacity Redeployed for Oncology & Rare-Disease Testing

Pandemic-era investment in thermal cyclers and nucleic-acid labs created surplus infrastructure now channelled into liquid biopsy and minimal-residual-disease workflows, allowing community hospitals to run assays once limited to reference centres. Liquid biopsy protocols for circulating tumour DNA can be completed in three days versus nine days for whole-genome sequencing, giving laboratories a competitive turnaround advantage.[1]Charlotte Houldcroft, “RT-PCR genotyping assays to identify SARS-CoV-2 variants in England in 2021,” The Lancet Microbe, thelancet.comThe ability to pivot high-throughput lines toward oncology raises entry barriers for newcomers that lack installed PCR fleets. Reimbursement incentives tied to companion diagnostics further cement PCR as a frontline tool for precision medicine. Laboratories with scalable PCR assets can unlock new revenue streams without additional capital spend, improving return on COVID-era investments.

Falling NGS Cost per Gigabase Enabling Ultra-High Multiplex Panels

Benchmarked studies on Element’s AVITI sequencer show per-sample cost reductions near 60% since July 2024, making 500-gene panels financially viable for routine tumour profiling.[2]Jeff Verdoorn, “Another AVITI sequencing price drop for a happier new year,” University of Minnesota Genomics Center, genomics.umn.edu Economic parity with single-gene PCR sparks a strategic shift toward comprehensive genomic profiling, especially in cancers with heterogeneous driver mutations. Roll-to-roll fluidics reduces reagent waste and supports continuous flow processing, dropping consumable expense to USD 9.5 per test. Hospitals in Asia-Pacific have begun to leapfrog single-gene testing by installing amplicon-based NGS suites directly, accelerating regional adoption curves. Lower sequencing outlay also benefits antimicrobial resistance surveillance, where multiplex amplicon panels can detect resistance genes and pathogen species in a single run.

Expansion of Companion-Diagnostic Approvals Mandating Nucleic-Acid Tests

The FDA’s green light for Illumina’s TruSight Oncology Comprehensive assay, covering more than 500 genes, underscores regulatory momentum that converts amplification platforms from optional tools into standard of care. Pharmaceutical sponsors now build pivotal trials around biomarker stratification, which hard-codes gene testing into drug labels and reimbursement pathways. QIAGEN’s QIAstat-Dx has secured partnerships in chronic diseases, illustrating how platform providers ride the companion-diagnostic wave to lock in reagent revenue and software subscriptions. Heightened validation demands reward companies with robust quality systems, giving incumbents a defensible moat.

Government Genomics Moonshots Funding Core Amplification Platforms

ARPA-H has earmarked USD 1.5 billion for projects that lower gene therapy production costs and democratise access, including EMBODY and ADAPT initiatives that rely on high-throughput amplification backbones.[3]Jocelyn Kaiser, “ARPA-H FY 2025 Budget,” Advanced Research Projects Agency for Health, arpa-h.gov The agency’s SBIR/STTR calls for “Process Analytical Technology for Cell and Gene Therapies” direct grant dollars toward assay development, reducing private R&D risk. National institutes in Japan, China, and Australia have mirrored this strategy, seeding domestic suppliers and bolstering regional self-sufficiency. Funding cushions early commercialisation hurdles and accelerates time‐to‐market for novel chemistries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost Of Digital-PCR & NGS Instruments For Mid-Tier Labs | -0.7% | Global, with particular impact in emerging markets | Medium term (2-4 years) |

| Stringent IVDR / FDA Compliance Delays For Multiplex Assays | -0.5% | North America & EU, with regulatory spillover effects | Long term (≥ 4 years) |

| Patent Thickets Around CRISPR-Powered Amplification Chemistries | -0.3% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Data-Sovereignty Rules Limiting Cross-Border Cloud Analysis Of Amplified Genomes | -0.2% | EU core, with spillover to APAC and other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Digital PCR & NGS Instruments

Acquiring a single digital PCR platform can exceed USD 200,000, and full NGS suites demand similar investment plus bioinformatics workstations. Ongoing maintenance and consumable expenses consume up to 70% of lifetime outlay, challenging mid-tier labs with limited throughput. Capital hurdles are most acute in Latin America, the Middle East, and parts of Southeast Asia where reimbursement lags technology adoption. Leasing models and reagent rental agreements ease entry barriers but still hinge on predictable sample volumes that small centres often lack.

Stringent IVDR / FDA Compliance Delays for Multiplex Assays

The FDA’s phased removal of enforcement discretion for laboratory-developed tests adds 12-18 months to commercial timelines and elevates validation budgets. Europe’s IVDR reclassifies many multiplex assays as high risk, triggering third-party certification costs that can top USD 1 million per panel. Regulatory uncertainty stalls investor confidence in start-ups, curtailing innovation velocity. Established manufacturers absorb the cost but pass expenses downstream through higher kit prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: CRISPR Disruption Accelerates Beyond Traditional PCR

The gene amplification technologies market size for PCR still dwarfs competitors, yet CRISPR-mediated assays are advancing with a 6.44% CAGR that outpaces the overall market. PCR platforms offered 68.79% gene amplification technologies market share in 2024, but programmable detection and attomolar limits of detection make CRISPR attractive for rapid sepsis and point-of-care viral testing. Rolling-circle amplification serves niche single-cell protocols, whereas NGS-driven target enrichment dominates comprehensive tumour profiling thanks to falling sequencing costs. Patent disputes may temper CRISPR’s speed, though licensing clarity will unlock broader deployment.

Adoption patterns diverge by setting. Community hospitals favour real-time PCR for its installed base and reimbursement familiarity, while reference labs integrate CRISPR-Cas13 to screen RNA viruses without thermal cycling. Academic centres deploy hybrid methods that combine LAMP pre-enrichment with NGS readouts to overcome GC-rich regions. The competitive landscape is fluid, with AI-optimised thermal cycling extending PCR’s utility even as next-gen chemistries gain mindshare.

By Product: Software Integration Drives Service Revenue Growth

Reagents and consumables commanded 54.32% of 2024 revenues, underscoring their recurrent cash-flow appeal. Yet software and services are expanding at a 7.69% CAGR, the quickest of all product categories, as labs seek AI engines that fine-tune reaction conditions and automate compliance logs. Instruments have edged toward commoditisation, pressuring manufacturers to differentiate through cloud dashboards and proactive maintenance analytics.

Subscription models charge by sample or report, smoothing revenue and embedding vendors deeper into laboratory workflows. Reagent makers now bundle lyophilised master mixes with barcode-linked software that verifies lot integrity, enhancing traceability for IVDR audits. Continuous-flow cartridge production supports private-label strategies, allowing service bureaus to outsource manufacturing and focus on informatics.

By Application: Forensic Testing Emerges as High-Growth Segment

Clinical diagnostics contributed 44.33% of market turnover in 2024 and retains volume leadership due to reimbursed oncology and infectious-disease panels. Forensic testing is climbing at 6.89% CAGR as AI-enhanced PCR shortens backlog clearance times, particularly for degraded samples from cold cases.

Drug discovery labs integrate CRISPR amplification in biomarker verification stages, compressing timelines for precision oncology trials. Agriculture and veterinary sectors adopt LAMP assays for field-ready Salmonella detection, broadening the use of gene amplification technologies market solutions beyond human health. Academic research absorbs spillover capacity but faces flat funding, reinforcing the pivot toward revenue-linked applications.

By End-User: CROs Capitalise on Outsourcing Trend

Hospitals and diagnostic centres maintained a 38.67% stake in 2024, yet contract research organisations are leading growth at 5.78% CAGR as pharmaceutical sponsors offload companion-diagnostic development. CROs leverage specialised staff and quality systems to satisfy rising regulatory claims, making them indispensable to late-stage trials.

Academic and research institutes remain innovation hubs but collaborate increasingly with CROs for scale-up and regulatory filings. Forensic laboratories benefit from direct grants that upgrade digital PCR fleets to process sexual-assault kit backlogs rapidly. Point-of-care platforms, such as PCB-based disposable chips, enable decentralised testing in rural clinics, redefining service delivery models.

Geography Analysis

North America held 38.52% of the gene amplification technologies market in 2024, driven by early adoption of AI-optimised workflows and robust federal funding pipelines. FDA scrutiny raises compliance costs, steering hospital labs toward vendor-supplied turnkey assays that bundle reagents, software, and validation files. Canada’s Precision Medicine Initiative mirrors US incentives, keeping regional growth resilient despite reimbursement pressure.

Asia-Pacific is forecast to produce the fastest CAGR at 5.89% through 2030. State-backed genomics corridors in China and India subsidise instrument purchases, while Japanese firms pioneer continuous-flow micro-reactor cartridges. Local manufacturing lifts availability of low-cost disposables, lowering entry thresholds for community hospitals and agriculture labs. The region increasingly exports OEM components to US and EU system integrators, embedding itself in global supply chains.

Europe balances stringent IVDR demands with a mature academic network. Germany and the Nordics channel Horizon Europe grants into companion-diagnostic projects, fuelling incremental uptake despite certification bottlenecks. Data localisation rules slow full-cloud adoption, yet on-premise AI appliances fill the gap, sustaining momentum without breaching GDPR [NATUREMEDICINE.COM]. Southern European countries prioritise food-safety monitoring platforms, broadening revenue beyond clinical niches.

Competitive Landscape

The market remains moderately fragmented. Thermo Fisher Scientific’s purchase of Olink added proximity extension assays that dovetail with quantitative PCR and NGS demand, reinforcing cross-selling potential. QIAGEN teams with Gencurix to load oncology assays onto its QIAcuityDx digital PCR line, exemplifying platform-centric expansion. Roche’s acquisition of LumiraDx’s technology signals large players’ interest in over-the-counter molecular tests, extending reach beyond central labs.

Emerging challengers focus on niche differentiation. Metagenomi licenses metagenomics-derived nucleases that boost editing specificity, a feature valued in personalised cell therapies. Start-ups commercialise AI-native laboratories where robotic pipettors and machine-vision thermocyclers run unattended, driving labour savings in high-throughput settings. Nonetheless, capital intensity and regulatory hurdles sustain entry barriers, keeping bargaining power with incumbents that possess service networks and validated workflows.

Growth strategies revolve around integrated ecosystems. Vendors bundle cloud software, reagent rental, and compliance consulting into multi-year contracts, reducing churn. Partnerships with pharmaceutical firms for companion diagnostics anchor long-term reagent consumption and create co-marketing synergies. Players unable to offer a full-stack proposition risk commoditisation and margin erosion.

Gene Amplification Technologies Industry Leaders

Thermo Fisher Scientific

QIAGEN

Bio-Rad Laboratories

Agilent Technologies

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Bio-Rad Laboratories introduced four new Droplet Digital PCR platforms, including the QX Continuum system, following its acquisition of Stilla Technologies.

- June 2025: QIAGEN and GENCURIX agreed to co-develop oncology assays for the QIAcuityDx digital PCR platform.

- June 2025: Visby Medical raised up to USD 65 million to accelerate the launch of its FDA-authorised at-home Women’s Sexual Health Test, cementing its position in rapid PCR diagnostics.

Global Gene Amplification Technologies Market Report Scope

| PCR |

| Isothermal Amplification |

| NGS-based Target Enrichment & Amplification |

| Rolling-Circle & RCA-derived Methods |

| CRISPR-mediated Amplification |

| Other / Hybrid Technologies |

| Instruments and Analyzers |

| Reagents and Consumables |

| Software and Services |

| Clinical Diagnostics |

| Drug Discovery & Development |

| Forensic Testing |

| Agriculture & Veterinary |

| Environmental & Food Safety Monitoring |

| Academic Research |

| Hospitals & Diagnostic Centers |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| Forensic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | PCR | |

| Isothermal Amplification | ||

| NGS-based Target Enrichment & Amplification | ||

| Rolling-Circle & RCA-derived Methods | ||

| CRISPR-mediated Amplification | ||

| Other / Hybrid Technologies | ||

| By Product | Instruments and Analyzers | |

| Reagents and Consumables | ||

| Software and Services | ||

| By Application | Clinical Diagnostics | |

| Drug Discovery & Development | ||

| Forensic Testing | ||

| Agriculture & Veterinary | ||

| Environmental & Food Safety Monitoring | ||

| Academic Research | ||

| By End-User | Hospitals & Diagnostic Centers | |

| Pharmaceutical & Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Contract Research Organizations (CROs) | ||

| Forensic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the gene amplification technologies market?

The gene amplification technologies market size stood at USD 29.67 billion in 2025 and is forecast to reach USD 34.79 billion by 2030.

2. Which technology segment is growing fastest?

CRISPR-mediated amplification is the fastest-growing segment with a projected 6.44% CAGR between 2025 and 2030.

3. Why are contract research organisations gaining share?

Pharmaceutical companies increasingly outsource companion-diagnostic and biomarker validation projects, driving CRO revenue at a 5.78% CAGR.

4. How are falling NGS costs influencing market dynamics?

Lower sequencing costs enable ultra-high multiplex panels, shifting testing from single-gene PCR to comprehensive genomic profiling at competitive prices.

5. What regulatory factors restrain growth?

Stringent IVDR rules in Europe and the FDA’s new oversight of laboratory-developed tests add 12-18 months to assay approval timelines and increase compliance costs.

6. Which region will register the highest growth rate?

Asia-Pacific is expected to deliver the highest regional CAGR of 5.89% through 2030, buoyed by government genomics initiatives and local manufacturing strength.

Page last updated on: