Medical Batteries Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

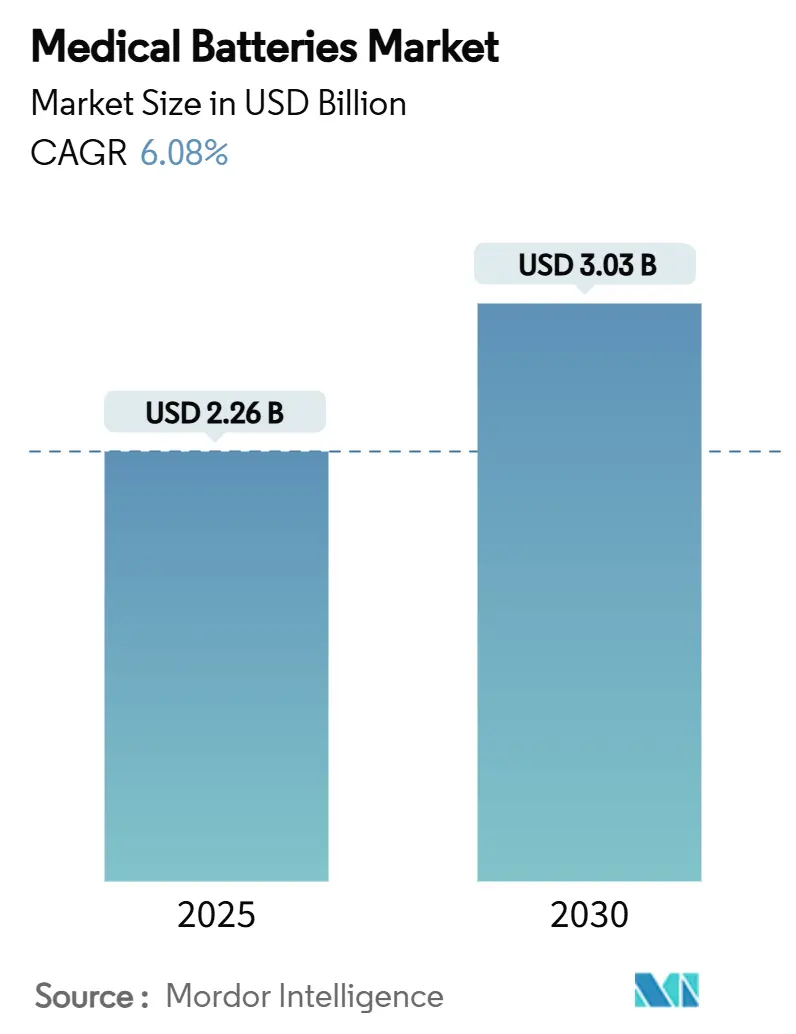

| Market Size (2025) | USD 2.26 Billion |

| Market Size (2030) | USD 3.03 Billion |

| Growth Rate (2025 - 2030) | 6.08% CAGR |

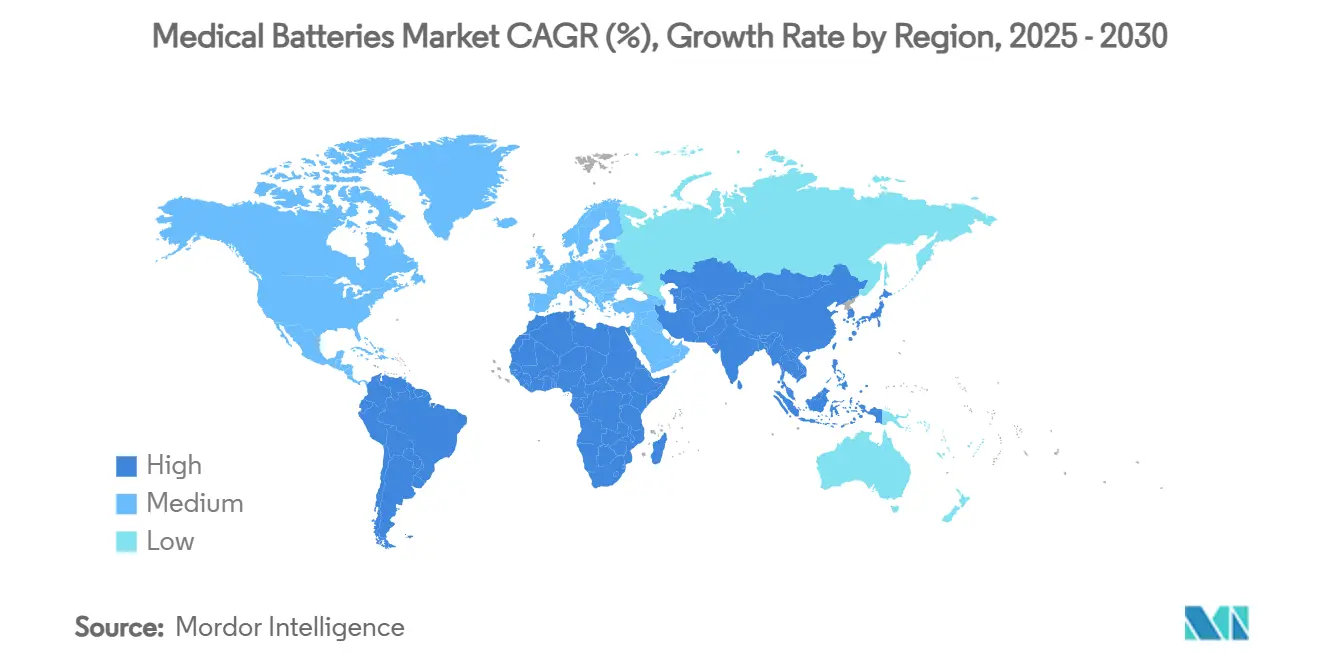

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Batteries Market Analysis by Mordor Intelligence

The medical batteries market size reached USD 2.26 billion in 2025 and is forecast to climb to USD 3.03 billion in 2030, translating into a 6.08% CAGR over the assessment period. Demand aligns with an aging world, rising chronic‐disease incidence and breakthroughs in battery chemistry that deliver longer life in smaller footprints. Lithium-ion cells remain the workhorse for implantables, yet aqueous chemistries such as silver-zinc gain momentum where safety is non-negotiable. Growth also reflects the rapid shift toward remote, home-based monitoring, where battery reliability directly affects clinical outcomes. Geographically, Asia-Pacific builds capacity fastest as local governments fund gigafactories and incentivize component supply while North America retains technology leadership through sustained R&D and predictable regulation. At the same time, critical-material shortages and multi-year regulatory qualification cycles temper near-term gains, favoring firms with deep supply-chain visibility and proven compliance records.

Key Report Takeaways

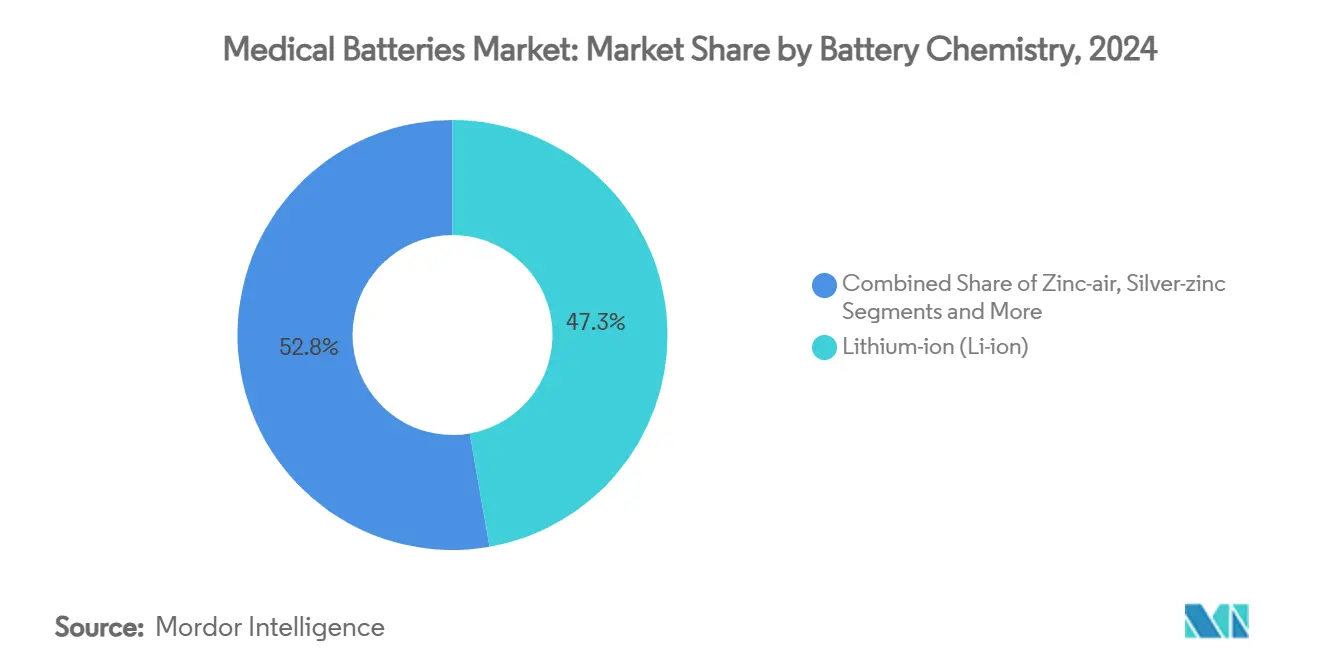

- By battery chemistry, lithium-ion commanded 47.25% of the medical batteries market share in 2024, while silver-zinc is projected to expand at a 10.01% CAGR to 2030.

- By application, implantable medical devices captured 39.34% revenue in 2024; portable and wearable devices are advancing at a 9.43% CAGR through 2030.

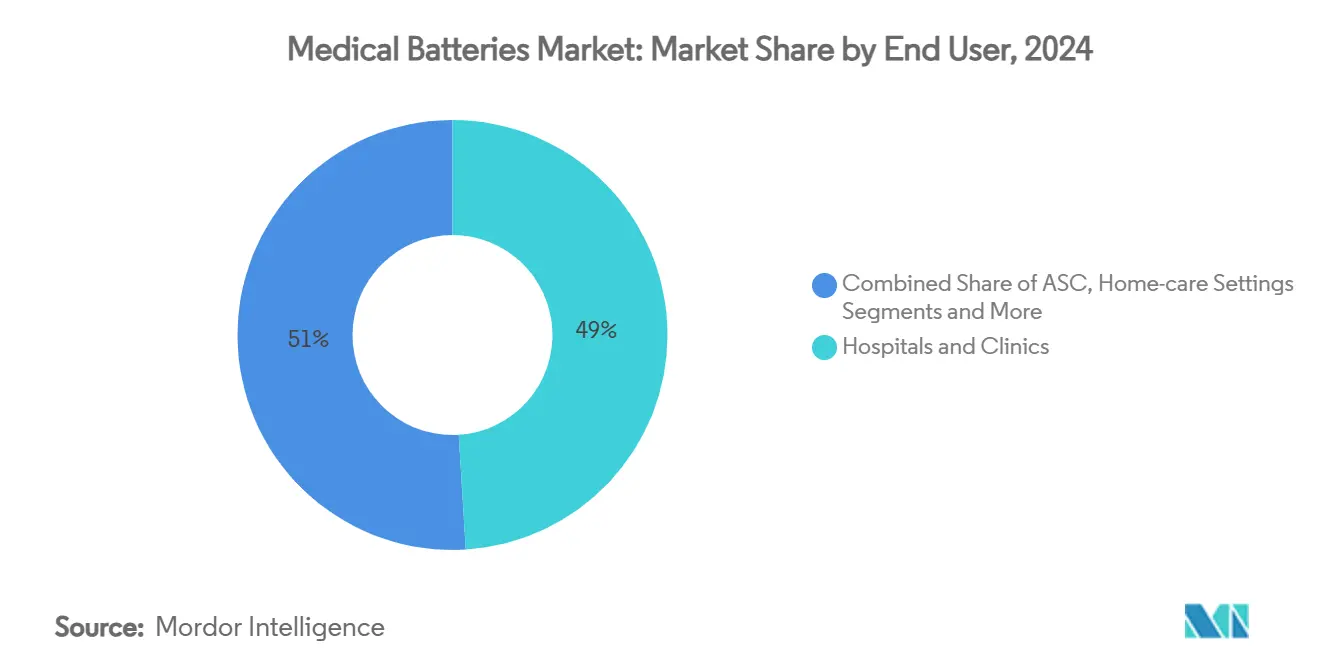

- By end user, hospitals and clinics held 49.01% of the medical batteries market size in 2024, whereas home-care settings are forecast to rise at an 8.56% CAGR to 2030.

- By capacity, the 1,000–10,000 mAh range accounted for 44.26% of the medical batteries market share in 2024; sub-100 mAh cells are expected to register the fastest 9.74% CAGR through 2030.

- By geography, North America led with 35.42% of 2024 revenue; Asia-Pacific is on track for an 8.66% CAGR up to 2030.

Global Medical Batteries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-Disease Prevalence Driving Implantables | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Shift Toward Home-Health Monitoring Devices | +1.8% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Advances In Li-Ion Micro- & Thin-Film Chemistries | +1.1% | Global, led by APAC manufacturing hubs | Medium term (2-4 years) |

| Regulatory Incentives For Safer Rechargeable Cells | +0.7% | North America & EU primarily | Short term (≤ 2 years) |

| Flexible Batteries Enabling Wearable Biosensors | +0.9% | Global, early adoption in developed markets | Medium term (2-4 years) |

| OEM "Battery-As-A-Service" Contracting Models | +0.5% | North America & Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic-disease prevalence driving implantables

Cardiovascular and neurological disorders continue to balloon, pushing implantable device volumes upward and creating repeat battery replacement cycles that compound demand. End-of-life surgeries decline when devices such as Boston Scientific’s EnduraLife ICDs deliver up to 17.5 years of service, yet aggregate cell shipments still rise as eligible patient counts climb.[1]Boston Scientific Communications, “VIGILANT EL Powered by EnduraLife,” Boston Scientific, bostonscientific.com Demographic aging in developed regions amplifies this predictable load, giving manufacturers confidence to invest heavily in next-generation chemistries. Neuro-stimulation and drug-delivery pumps broaden the addressable field beyond cardiac care, further supporting steady unit growth. Collectively, these factors raise baseline battery consumption independent of economic cycles.

Shift toward home-health monitoring devices

Permanent policy changes forged during the pandemic normalized remote care, embedding connected wearables into routine clinical workflows. Devices now process data at the edge, curbing transmission energy and allowing smaller batteries without shortening runtime. As reimbursement tilts toward preventive monitoring, home-care settings emerge as the fastest-growing customer group, encouraging designs that consumers can replace or recharge themselves. Retail and e-commerce channels widen distribution, while battery makers benefit from recurring sales tied to consumable power modules. This decentralized model requires ultra-reliable cells, since service interruptions directly affect patient safety outside clinical supervision.

Advances in Li-ion micro- & thin-film chemistries

Partnerships such as Murata-Stanford’s porous current collector cut internal resistance by 50% and boost power fourfold at unchanged energy density.[2]Corporate Communications, Murata Manufacturing Co., Ltd., “Murata and Stanford University Collaborate to Create the World’s First Porous Current Collector,” murata.com These gains permit smaller device footprints and lighter implantables, advancing patient comfort and surgical ease. Thin-film techniques integrate batteries onto semiconductor wafers, eliminating discrete packs in contact lenses or brain-computer interfaces. Emerging solid-state electrolytes promise leak-free safety, positioning Li-ion to defend share even as aqueous cells encroach. The blend of micro-fabrication and long production runs could lower costs when scaled through existing chip fabs.

Regulatory incentives for safer rechargeable cells

The FDA’s 2024 safety report introduced streamlined pathways for batteries that minimize thermal-runaway risk, accelerating reviews for aqueous chemistries such as silver-zinc.[3]Center for Devices and Radiological Health, “CDRH Issues 2024 Safety and Innovation Reports,” U.S. Food and Drug Administration, fda.gov These guidelines also emphasize recycling plans, nudging suppliers toward closed-loop programs that monetize recovered materials. Over time, regulators aim to shrink post-market surveillance incidents tied to power failures, rewarding brands with documented fault-tolerance. As legislation tightens, safer chemistries may secure premium pricing and faster clinic adoption relative to traditional Li-ion cells.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Regulatory Qualification Cycles | -0.8% | Global, most stringent in North America & EU | Long term (≥ 4 years) |

| High Cost Of High-Energy Chemistries | -1.1% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Critical-Material Supply-Chain Risks | -0.9% | Global, concentrated in lithium-dependent regions | Medium term (2-4 years) |

| End-Of-Life & E-Waste Compliance Costs | -0.4% | EU & North America primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long regulatory qualification cycles

Battery modules for implantables undergo 3-5 years of biocompatibility and clinical testing, imposing high entry barriers that weigh heavily on startups. Combined products that couple electronics with drugs or biologics encounter even more intricate review pathways. Recent recalls, such as Medtronic’s battery issue across seven cardiac models, heighten scrutiny and may add supplemental data requests. This environment locks in advantages for suppliers with established regulatory records and capital, slowing diffusion of disruptive chemistries.

High cost of high-energy chemistries

Silver-zinc cells cost 3-5 times comparable Li-ion units because of niche production volumes and medical-grade quality protocols. Price sensitivity in developing regions creates a two-tier market where premium batteries stay tethered to high-value applications. Economies of scale remain elusive: hundreds of device form factors each demand tailored packs, preventing the large-lot efficiencies seen in consumer electronics. Without concerted volume aggregation, advanced chemistries may struggle to cross cost thresholds needed for mass adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Safety-first chemistries unlock premium growth

Lithium-ion chemistry held 47.25% of the medical batteries market in 2024 due to its entrenched supply chain, predictable performance and competitive pricing. Silver-zinc, however, is projected to outpace all rivals with a 10.01% CAGR, buoyed by its aqueous electrolyte that eliminates thermal-runaway risk and extends operating temperatures from −40 °C to +70 °C. Zinc-air dominates hearing aids because atmospheric oxygen acts as a reactant, effectively freeing internal space for capacity. Nickel-metal hydride keeps a loyal, though shrinking, clientele where long-term reliability supersedes energy density. Specialty chemistries—lithium-CFx and lithium-SOCl₂—serve ultra-long-life sensors requiring 10–20 year service. During regulatory review, safer chemistries enjoy faster clearance, tilting investment toward aqueous systems despite higher cost.

The competitive landscape within chemistry is increasingly value-driven rather than solely capacity-driven. Manufacturers that document superior safety performance incur fewer post-market surveillance liabilities, a significant expense for implantables. Consequently, the medical batteries market size allocated to silver-zinc could widen beyond initial forecasts if regulatory agencies intensify flammability scrutiny. Meanwhile, incremental Li-ion gains from solid-state and thin-film designs aim to defend share by improving safety without sacrificing density. Firms leverage joint ventures with academia to speed discoveries from lab to production.

By Application: Wearables surge as implantable base holds steady

Implantable devices accounted for 39.34% of the 2024 revenue pool, anchored by pacemakers and defibrillators that rely on proven Li-ion packs. Yet portable and wearable devices are slated for a 9.43% CAGR through 2030 as decentralized care scales. The shift places a premium on ultra-low leakage currents and sealed housings able to withstand patient activity without degradation. Northwestern University’s dissolvable light-activated pacemaker exemplifies how micro-batteries create new procedure paradigms. Neuro-stimulation systems add complexity, demanding high-pulse precision and rechargeability; Boston Scientific’s Vercise Genus platform offers clinicians a choice between long-life primary cells and rechargeable variants for lifestyle fit.

As wearables move from fitness to regulated medical devices, compliance and data security raise the technical bar. Suppliers with medical-grade quality cultures are positioned to capture spillover volumes that consumer battery makers struggle to service. Integration of energy harvesting—piezoelectric, thermoelectric or biochemical—further reduces capacity requirements, aligning with sub-100 mAh growth themes. Over time, a higher proportion of the medical batteries market size will derive from ambulatory consumer devices prescribed for chronic-disease management.

By End User: Home-care reshapes procurement

Hospitals and clinics still controlled 49.01% of demand in 2024 thanks to large implantable rollouts and institutional purchasing clout. Home-care environments, however, are growing fastest at an 8.56% CAGR as payers reimburse remote patient monitoring. This shift prompts designs that patients can replace without clinical visits, thereby expanding unit volumes even if capacity per device falls. Ambulatory surgical centers bridge traditional and home settings, favoring rapid-charge packs that enable same-day discharges. Diagnostics and research labs require custom assemblies capable of rock-steady voltage for precision instrumentation, preserving a niche for high-reliability packs despite slower overall growth.

Decentralization changes service models: suppliers must now support logistics for direct-to-consumer channels while maintaining stringent traceability. Companies offering battery-as-a-service gain traction here, as they can predict replacement needs and dispatch fresh modules before failures occur, safeguarding patient outcomes and protecting brands.

By Capacity Range: Sub-100 mAh cells ride miniaturization wave

Cells rated 1,000–10,000 mAh retained 44.26% of 2024 revenue, powering pacemakers and neurostimulators that target multi-year autonomy. Yet devices optimized for ultra-low power and intermittent energy harvesting feed sub-100 mAh demand, which will accelerate at 9.74% CAGR to 2030. Medtronic’s next-gen leadless pacemaker shows how refined power management can stretch a small cell to nearly 17 years of service. The 100–1,000 mAh band supports wearables that balance continuous sensing with consumer-acceptable size and weight. Packs exceeding 10,000 mAh remain critical for portable imaging and emergency devices, though improvements in energy density could compress their share over time.

In parallel, solid-state and thin-film innovations raise gravimetric capacity without enlarging volume, potentially blurring historic capacity categories. Suppliers must, therefore, align production lines with demand variability, ensuring they can pivot between micro-cells and large modules without compromising medical-grade quality.

Geography Analysis

North America booked 35.42% of 2024 revenue courtesy of entrenched device OEMs, full reimbursement coverage and a robust regulatory framework that although strict, offers predictable pathways. Government grants, such as the DOE’s USD 199 million award to EnerSys for a South Carolina gigafactory, underscore policy support for local battery supply that mitigates geopolitical risk. Canada and Mexico complement the regional ecosystem through precision machining and component assembly that exploit USMCA tariff advantages. While high labor and environmental compliance costs persist, ongoing automation investments temper margin erosion.

Asia-Pacific is forecast to deliver the fastest regional CAGR at 8.66% through 2030, propelled by heavy manufacturing outlays and expanding healthcare access across populous nations. China drives scale with projects like Sunwoda’s USD 1 billion plant expansion across Southeast Asia. Japan and South Korea contribute advanced materials science, enabling high-precision micro-batteries that feed global implantable demand. India’s nascent device hubs focus on cost-optimized packs tailored to domestic purchasing power, while Australia ensures a steady pipeline of lithium. Regional governments layer incentives for domestic production, expediting technology transfer from multinational firms.

Europe presents a mature, regulation-intensive environment that prioritizes circular-economy principles. Recycling mandates sway buyers toward chemistries with easier metal recovery, giving zinc-based cells a policy tailwind. Germany leads in precision manufacturing while the United Kingdom, post-Brexit, leverages agile regulatory updates to stay attractive for clinical trials. France and Italy specialize in component fabrication and advanced clinical testing. Corporate restructurings such as VARTA’s capital reorganization highlight the pressure to scale and specialize amid tightening margins. Despite economic headwinds, Europe’s aging population secures a stable demand baseline, especially for implantables reimbursed under comprehensive healthcare systems.

Competitive Landscape

The medical batteries market reflects moderate fragmentation, with specialty implantable suppliers enjoying high entry barriers while portable-device segments invite broader participation. Intellectual property around chemistry formulation, hermetic sealing and biocompatible packaging underpins competitive advantage more than sheer production volume. Boston Scientific’s EnduraLife chemistry, delivering 17.5-year ICD longevity, illustrates how performance differentiation translates into physician preference and patient trust.

Partnerships between component giants and start-ups accelerate technology diffusion: Murata’s collaboration with QuantumScape to scale ceramic solid-state films typifies moves to leverage manufacturing muscle for next-generation designs. Funding flows into ultra-miniature battery developers such as Injectpower, whose EUR 6.5 million raise targets smart implant caps. At the same time, academic breakthroughs—implantable sodium-oxygen cells that use body fluids—introduce potential discontinuities that could supplant classical batteries in niche therapies.

Service innovation rivals chemistry innovation. Integer Holdings’ power-as-a-service model secures multi-year contracts across roughly 100 platforms, embedding the company deeper into OEM value chains and generating data-rich feedback loops for design iteration. As devices connect to the cloud, battery telemetry informs predictive maintenance, reinforcing vendor lock-in. Overall, suppliers able to combine safety validation, flexible manufacturing and service layer differentiation hold the edge in winning long-term implantable programs.

Medical Batteries Industry Leaders

-

EaglePicher Technologies

-

EnerSys (Medical)

-

Integer Holdings (Greatbatch)

-

Saft Groupe

-

PHC Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Abbott received FDA Breakthrough Device Designation for the AVEIR Conduction System Pacing leadless pacemaker and launched the ASCEND CSP pivotal trial.

- April 2025: Murata Manufacturing and QuantumScape began a collaboration to explore ceramic film manufacturing for solid-state batteries.

- January 2025: EnerSys finalized a USD 199 million DOE award to build a lithium-ion facility in Greenville, South Carolina.

Global Medical Batteries Market Report Scope

| Lithium-ion (Li-ion) |

| Nickel-metal Hydride (NiMH) |

| Zinc-air |

| Silver-zinc |

| Others (Li-CFx, Li-SOCl₂, etc.) |

| Implantable Medical Devices | Cardiac Rhythm Management (CRM) |

| Neuro-stimulation | |

| Drug-delivery Pumps | |

| Portable & Wearable Medical Devices | Patient Monitoring |

| Diagnostic Imaging | |

| Point-of-Care (POC) Devices | |

| Laboratory & Other Equipment |

| Hospitals & Clinics |

| Ambulatory Surgical Centers (ASC) |

| Home-care Settings |

| Diagnostics & Research Labs |

| <100 mAh |

| 100–1,000 mAh |

| 1,000–10,000 mAh |

| >10,000 mAh |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Battery Chemistry | Lithium-ion (Li-ion) | |

| Nickel-metal Hydride (NiMH) | ||

| Zinc-air | ||

| Silver-zinc | ||

| Others (Li-CFx, Li-SOCl₂, etc.) | ||

| By Application | Implantable Medical Devices | Cardiac Rhythm Management (CRM) |

| Neuro-stimulation | ||

| Drug-delivery Pumps | ||

| Portable & Wearable Medical Devices | Patient Monitoring | |

| Diagnostic Imaging | ||

| Point-of-Care (POC) Devices | ||

| Laboratory & Other Equipment | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers (ASC) | ||

| Home-care Settings | ||

| Diagnostics & Research Labs | ||

| By Capacity Range | <100 mAh | |

| 100–1,000 mAh | ||

| 1,000–10,000 mAh | ||

| >10,000 mAh | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the medical batteries market in 2025?

It stands at USD 2.26 billion and is projected to grow to USD 3.03 billion by 2030 at a 6.08% CAGR.

Which battery chemistry is growing fastest in medical devices?

Silver-zinc leads with a forecast 10.01% CAGR because its aqueous electrolyte eliminates thermal-runaway risk while delivering higher energy density.

Why are home-care settings important to medical battery suppliers?

Remote monitoring and preventive care have shifted procurement away from hospitals, driving an 8.56% CAGR for home-care demand and requiring longer-lasting, user-replaceable cells.

What capacity range will see the quickest growth?

Sub-100 mAh batteries will advance at 9.74% CAGR as miniaturized electronics and energy harvesting reduce power requirements.

Which region will expand fastest through 2030?

Asia-Pacific is expected to post an 8.66% CAGR, supported by large-scale manufacturing investments and broader healthcare access.

How are service models changing battery procurement?

Battery-as-a-service offerings convert upfront hardware costs into recurring fees, guaranteeing performance through predictive replacement and boosting supplier lock-in.

Page last updated on: