Medical Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

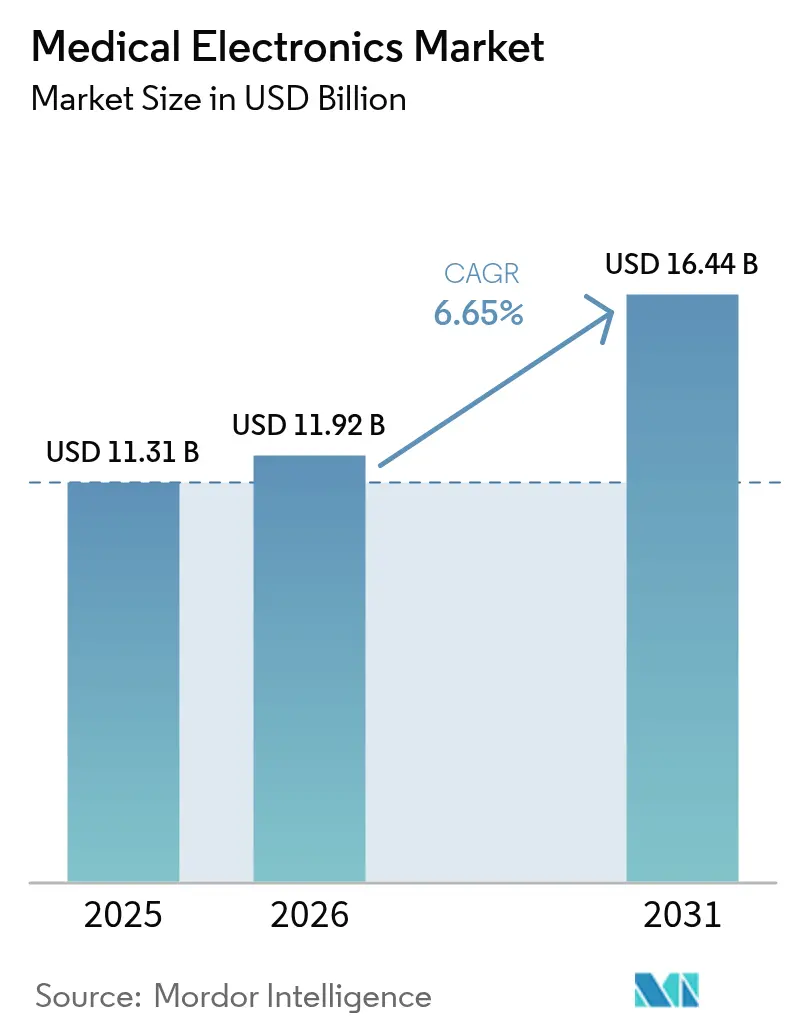

| Market Size (2026) | USD 11.92 Billion |

| Market Size (2031) | USD 16.44 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

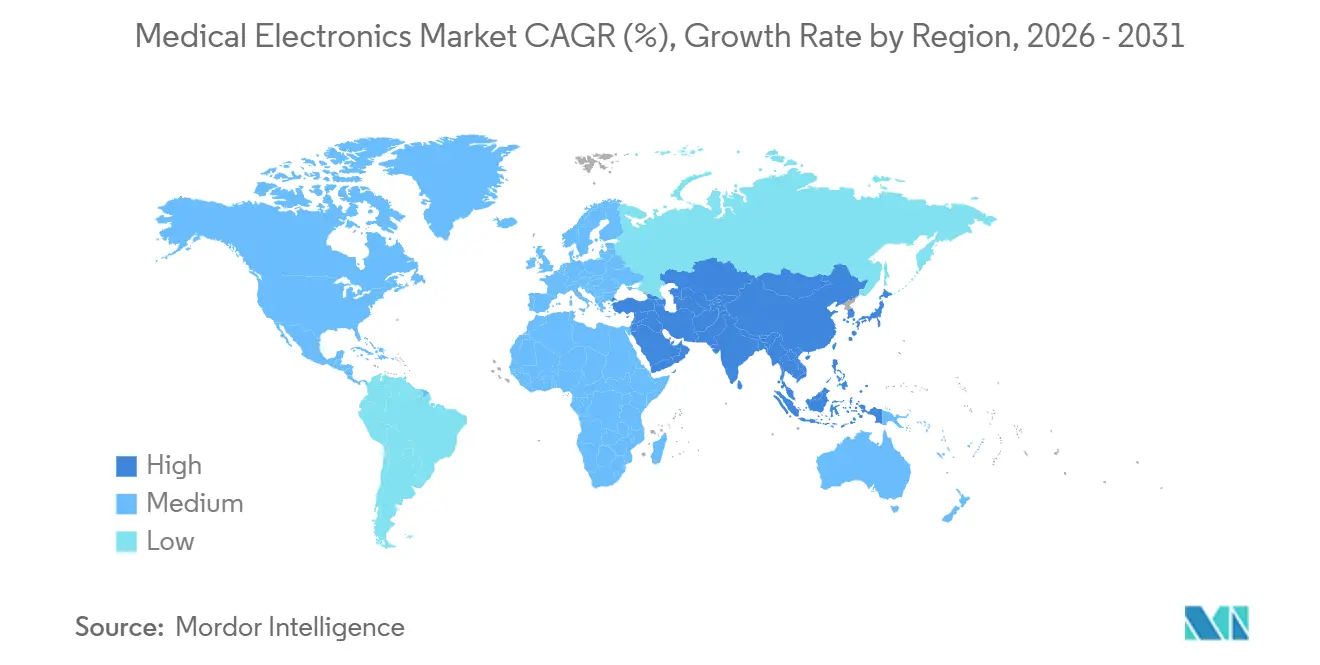

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

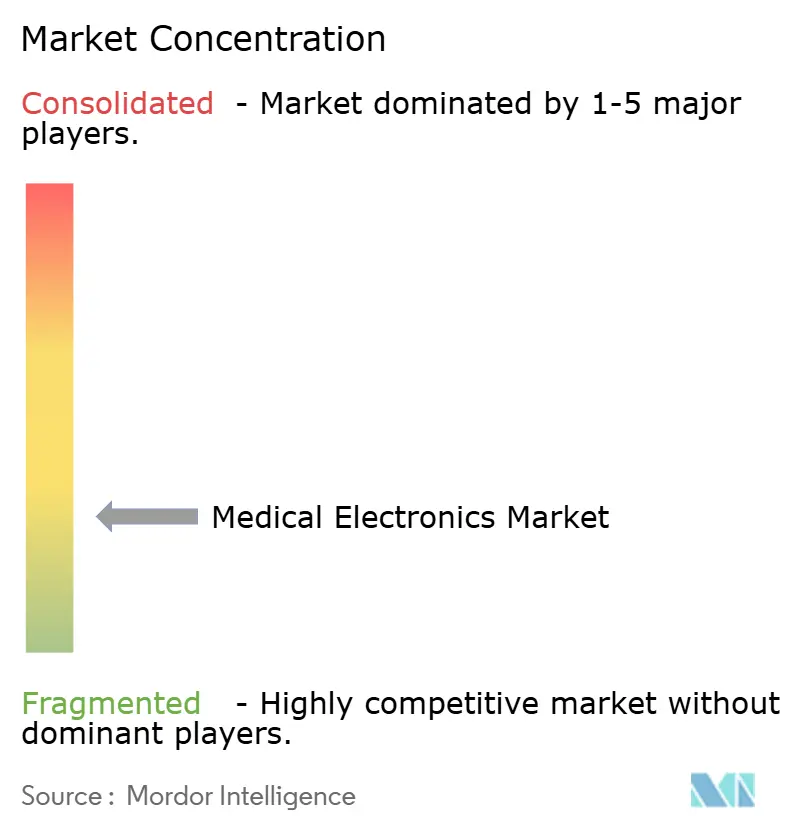

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Electronics Market Analysis by Mordor Intelligence

The Medical Electronics Market size is projected to be USD 11.31 billion in 2025, USD 11.92 billion in 2026, and reach USD 16.44 billion by 2031, growing at a CAGR of 6.65% from 2026 to 2031.

A reimbursement shift toward outcome-linked payments is steering capital from episodic imaging toward continuous monitoring, accelerating demand for AI-enabled wearables and implantables. Semiconductor shortages are easing, yet component dual-sourcing remains a standard design discipline as manufacturers hedge against any return of foundry bottlenecks. Cybersecurity compliance has become a front-end design criterion after the FDA’s 2024 guidance, prompting OEMs to build software bills of materials into every connected asset.[1]U.S. Food and Drug Administration, “Cybersecurity in Medical Devices: Quality System Considerations and Content of Premarket Submissions,” FDA.gov Meanwhile, helium scarcity is nudging radiology budgets toward low-cryogen MRI platforms, opening disruptive lanes for zero-boil-off magnet developers. Market leaders are pivoting from one-time hardware sales to recurring digital-service subscriptions, pairing equipment uptime guarantees with analytics that prove value under emerging value-based contracts.

Key Report Takeaways

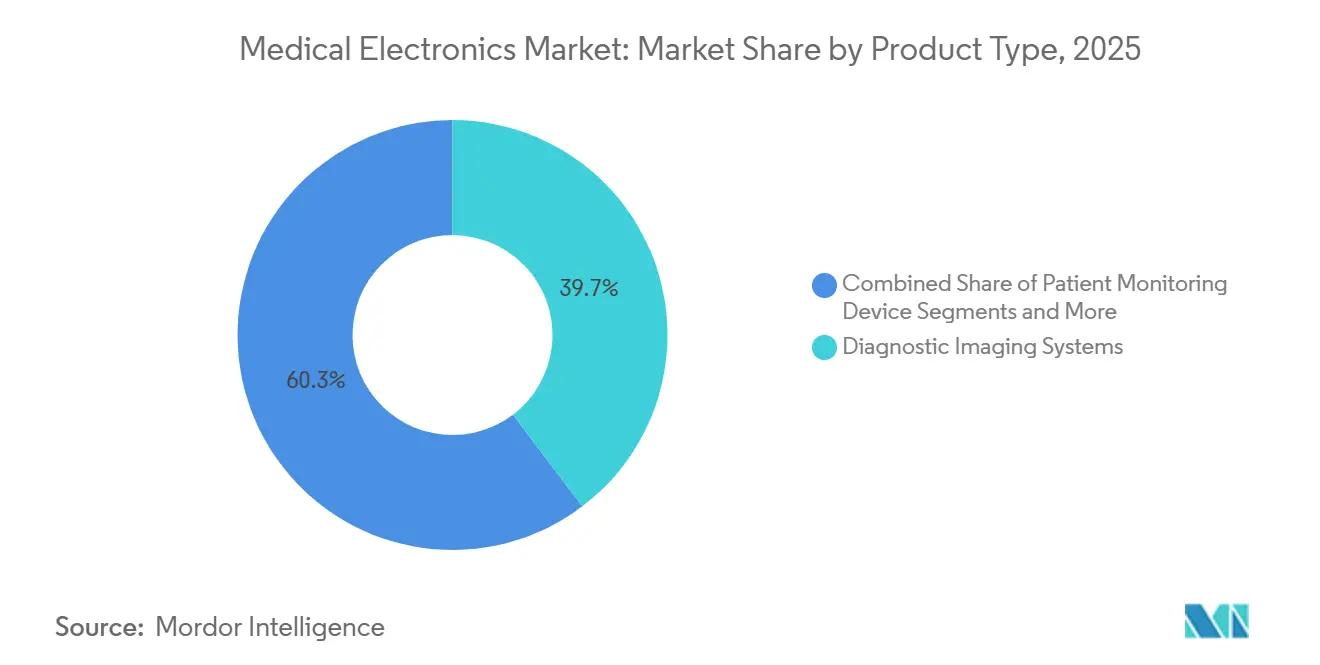

- By product type, diagnostic imaging led with 39.68% of medical electronics market share in 2025 while wearables and implantables are advancing at a 10.73% CAGR through 2031.

- By component, sensors and MEMS commanded 32.33% share of the medical electronics market size in 2025 and are forecast to expand at 9.43% CAGR over 2026-2031.

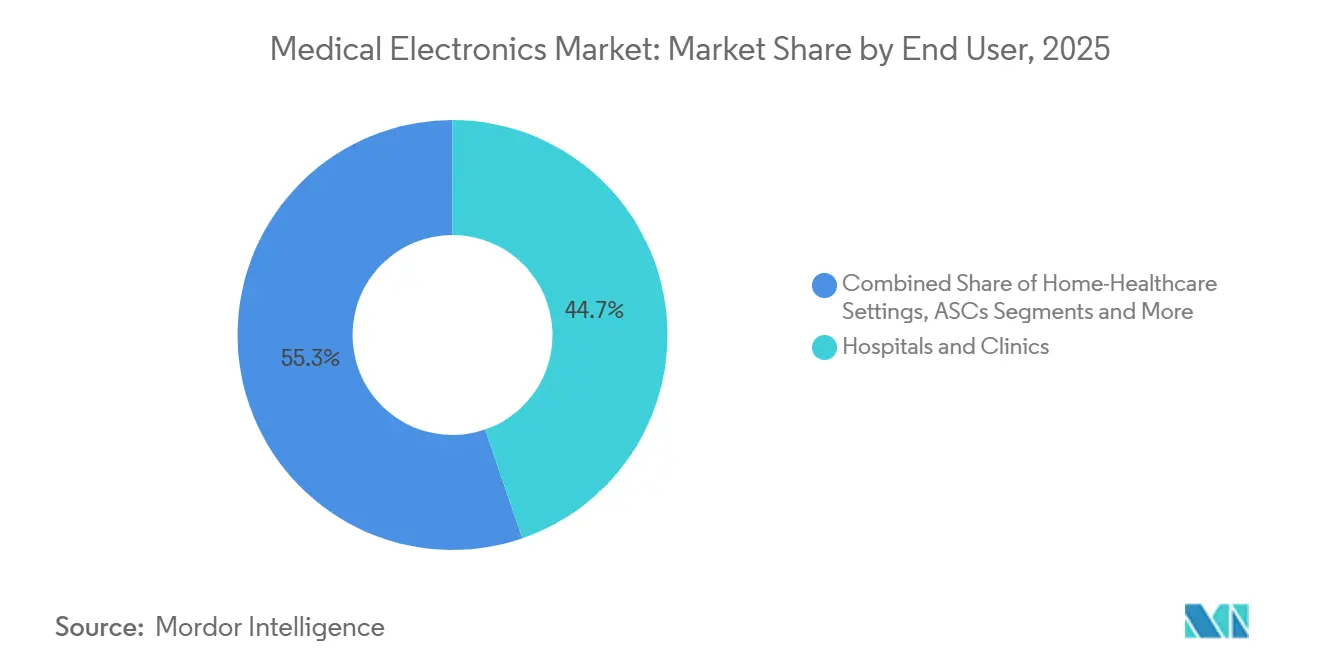

- By end-user, hospitals and clinics held 44.72% of 2025 spending, whereas home-healthcare settings are projected to post a 9.01% CAGR to 2031.

- By clinical application, cardiology captured 29.44% share of the medical electronics market size in 2025; oncology is set to record a 10.33% CAGR during 2026-2031.

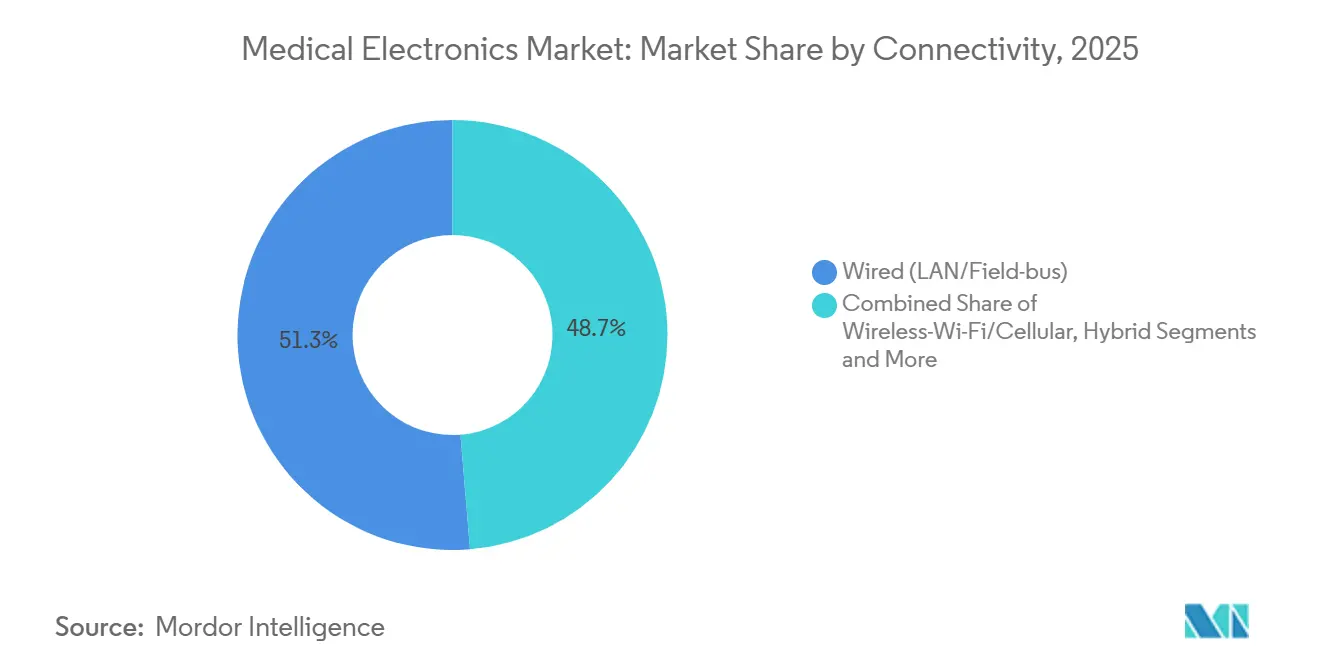

- By connectivity, wired LAN and field-bus links accounted for 51.29% of 2025 revenues, but Bluetooth Low Energy is rising at an 8.24% CAGR through 2031.

- By geography, North America led with 33.46% revenue share in 2025, whereas Asia-Pacific is forecast to advance at an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of AI-Enabled Imaging Modalities | +1.4% | North America, Europe | Medium term (2-4 years) |

| Shift Toward Home-Based and Wearable Diagnostics | +1.6% | North America, Europe, APAC | Short term (≤ 2 years) |

| Regulatory Push for IEC 60601-1 4th Edition Compliance | +0.8% | Global | Long term (≥ 4 years) |

| Emergence of Printable & Flexible Bioelectronics | +0.7% | North America, APAC | Long term (≥ 4 years) |

| Growing Demand for Radiation-Hard Semiconductors in Proton Therapy | +0.5% | North America, Europe, China | Medium term (2-4 years) |

| Expansion of Telehealth Reimbursement for Remote Monitoring | +1.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of AI-Enabled Imaging Modalities

More than 600 AI-enabled devices cleared by the FDA by mid-2024 have turned image-analysis tasks into near-real-time workflows, trimming MRI scan times by up to 50% and cutting interpretation backlogs.[2]U.S. Food and Drug Administration, “Artificial Intelligence and Machine Learning (AI/ML)-Enabled Medical Devices,” FDA.gov Providers recoup investments swiftly because Medicare Advantage and several European payers reimburse AI-assisted reads at premium rates, enhancing ROI while creating defensible upgrade cycles.

Shift Toward Home-Based and Wearable Diagnostics

Expanded U.S. remote patient-monitoring codes that came into force in 2026 pay physicians for reviewing patient-generated data, turning connected wearables into reimbursable assets.[3]U.S. Centers for Medicare & Medicaid Services, “Calendar Year 2026 Physician Fee Schedule Final Rule,” CMS.gov Continuous glucose monitors and cuff-less blood-pressure devices are embedding multi-parameter sensing and mobile links, allowing clinicians to titrate therapies without office visits.

Regulatory Push for IEC 60601-1 4th Edition Compliance

Draft revisions fortify cyber-safety and software lifecycle rigor, effectively raising design-verification workloads, yet offering market access advantages to firms with mature quality systems. Procurement teams in group-purchasing organizations increasingly stipulate 60601-1 compliance, turning certification into a sales gatekeeper.

Emergence of Printable & Flexible Bioelectronics

Stretchable, ultra-thin circuits demonstrated by Stanford and University of Tokyo labs in 2024 deliver artifact-free signals even under 50% strain, paving the way for skin-conformal ECG patches that could retail below USD 1 per sensor once roll-to-roll yields mature. First-wave commercial pilots focus on wound-healing monitors where disposability offsets higher unit cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicon Supply-Chain Volatility Post-2025 | −0.9% | Global | Short term (≤ 2 years) |

| Stringent Post-Market Surveillance Under EU MDR | −0.7% | Europe | Medium term (2-4 years) |

| Cybersecurity Certification Bottlenecks for Connected Implants | −0.6% | North America, Europe | Medium term (2-4 years) |

| Helium Shortage Elevating MRI Magnet Costs | −0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicon Supply-Chain Volatility Post-2025

Lead-times for power semiconductors peaked at 52 weeks in 2024, forcing many device OEMs into expensive redesigns or spot-market buys that eroded margins. New fabs funded by the CHIPS Acts will not ease constraints until after 2027.

Stringent Post-Market Surveillance Under EU MDR

Mandatory periodic safety-update reporting and clinical-evidence updates add USD 0.5-1 million in annual compliance overhead for mid-size firms, prompting some niche suppliers to exit the EU or merge with better-capitalized partners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Imaging Anchors Revenue, Wearables Drive Growth

Diagnostic imaging platforms generated 39.68% of 2025 revenue, underpinning the medical electronics market through multiyear service contracts and upgrade bundles. Imaging OEMs now embed on-device AI to automate reconstruction and annotate scans, recapturing value that once flowed to stand-alone software vendors.

Wearables and implantables, while smaller in absolute revenue, are forecast to expand at a 10.73% CAGR through 2031. Reimbursement for continuous glucose and blood-pressure monitoring plus smartphone tethering is lifting average selling prices. This double-digit trajectory will steadily lift the medical electronics market as capital-light home devices supplement hospital imaging budgets.

By Component: Sensors and MEMS Lead, Power ICs Trail

Sensors and MEMS accounted for 32.33% of 2025 sales and will rise at 9.43% per year, a pace that outstrips every other chip class. Miniaturized inertial and biochemical sensors allow single-use adhesive patches that stream multi-vital data over Bluetooth or Wi-Fi. Power-management ICs lag on growth yet remain essential for battery-operated form factors. Early adoption of solid-state batteries in cochlear and cardiac implants promises longer replacement cycles, reinforcing aftermarket parts revenue in the medical electronics market.

By End-User: Hospitals Hold Share, Home Settings Surge

Hospital procurement represented 44.72% of 2025 revenue, reflecting capital-equipment lifecycles and in-house biomedical engineering support. Home-healthcare, however, is climbing at a 9.01% CAGR, converting disease-management workflows into reimbursable RPM service lines. Retail pharmacies and e-commerce storefronts extend distribution reach, broadening the medical electronics market to an audience once served almost exclusively by institutional buyers.

By Clinical Application: Cardiology Dominates, Oncology Accelerates

Cardiology’s entrenched 29.44% revenue share is underpinned by chronic-disease prevalence and well-established reimbursement. Oncology platforms, growing at 10.33% CAGR, benefit from proton therapy’s higher payment rates and the push for adaptive radiation planning, expanding the overall medical electronics market size allocated to cancer care technologies.

By Connectivity: Wired Dominates, Wireless Gains Traction

Wired LAN and field-bus architectures still claimed 51.29% of 2025 connectivity revenue owing to deterministic performance in critical care. Bluetooth Low Energy and Wi-Fi nodes are advancing at 8.24% CAGR, especially in wearables. FDA-mandated SBOMs elevate the cost of wireless certification, yet interoperability gains and Wi-Fi 6E deployments are narrowing latency gaps, expanding wireless’s footprint inside the medical electronics market.

Geography Analysis

North America generated 33.46% of 2025 revenue, buoyed by CMS reimbursement expansion and the FDA’s fast-track pathways for AI-based devices. Robust venture funding channels accelerate commercialization, sealing the region’s leadership in both imaging and wearable pipelines.

Europe trails in share but boasts harmonized market access under EU MDR, simplifying multi-country launches once conformity is achieved. Germany’s Digital Healthcare Act offers structured coding for digital therapeutics, turning the bloc into a proving ground for outcome-based payment models.

Asia-Pacific is the fastest-growing region at 8.02% CAGR. China’s localization push for high-end ultrasound and MRI components and India’s Production-Linked Incentive scheme draw OEM assembly and R&D footprints into the region, lifting the medical electronics market across APAC.

Competitive Landscape

Top-tier OEMs such as Siemens Healthineers, GE HealthCare, Philips, and Medtronic leverage installed bases and global service to defend high-ticket imaging and therapy franchises. Semiconductor specialists—Texas Instruments, Analog Devices, STMicroelectronics—differentiate on low-power performance and pre-certified wireless stacks, securing sockets inside next-generation wearables. Start-ups occupy remote-monitoring niches, selling direct to consumers or partnering with telehealth platforms to unlock reimbursement swiftly. Edge-AI capability, regulatory readiness, and cybersecurity posture define competitive advantage as the medical electronics market shifts from hardware margin capture to software-subscription annuities.

Medical Electronics Industry Leaders

Koninklijke Philips N.V.

Siemens Healthcare GmbH

Medtronic

GE Healthcare

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Olympus published the EAGLE Trial validating the cloud-based CADDIE polyp detection platform, the first FDA-cleared and CE-marked CADe tool within its OLYSENSE ecosystem.

- January 2026: ZEISS Medical Technology rolled out Collaborative Care, a browser application that lets eye-care professionals exchange data and referrals in real time.

- January 2026: Polymatech Electronics received CDSCO registration to begin domestic manufacture of vein-finder devices under India’s Medical Devices Rules.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the medical electronics market as the aggregate value of active electronic components and embedded circuits that power diagnostic imaging systems, patient-monitoring platforms, therapeutic devices, and portable or home-care equipment used for human healthcare worldwide. The valuation reflects factory-gate revenues recorded in the base year 2025, expressed in current USD.

Scope exclusions include non-electronic consumables, standalone software sold without bundled hardware, contract manufacturing revenues, and veterinary devices, which are not included.

Segmentation Overview

- By Product Type

- Diagnostic Imaging Systems

- Patient Monitoring Devices

- Therapeutic & Surgical Devices

- Wearables & Implantables

- By Component

- Sensors & MEMS

- Power Management ICs & Batteries

- MCUs/MPUs & DSPs

- Displays & Optoelectronics

- By End-user

- Hospitals & Clinics

- Home-Healthcare Settings

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- By Clinical Application

- Cardiology

- Neurology

- Oncology

- Orthopedics

- Others

- By Connectivity

- Wired (LAN/Field-bus)

- Wireless—Bluetooth/BLE

- Wireless—Wi-Fi/Cellular

- Hybrid (Wired + Wireless)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys were conducted with biomedical engineers at hospitals, procurement heads at group purchasing organizations, component vendors, and regional regulators across North America, Europe, Asia-Pacific, and Latin America. Their insights validated utilization rates, service-contract attach ratios, and upcoming regulatory milestones, which were then folded back into our model to tighten assumptions.

Desk Research

Our analysts first mapped the universe through public datasets such as US FDA 510(k) clearances, WHO Global Health Expenditure, OECD Health Stats, UN population tables, and International Trade Center shipment codes that isolate HS-level flows for imaging and monitoring equipment. Company 10-Ks, investor decks, and selected peer-reviewed journals furnished average selling prices and replacement cycles, while D&B Hoovers and Dow Jones Factiva supplied supplemental financials and deal news. These sources establish the structural demand pool and price corridors that anchor the model. The list above is illustrative; numerous other credible publications were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down reconstruction layers national procedure volumes, installed-base audits, and import-export tallies, which are then reconciled with selective bottom-up snapshots such as supplier roll-ups and sampled ASP × unit flows for MRI, CT, and multiparameter monitors. Key variables like aging-population share, chronic disease prevalence, hospital capital-expenditure cycles, component price erosion, and device approval pipelines drive yearly estimates. Multivariate regression links these indicators to historical revenue to project 2026-2030 growth, while scenario analysis stresses high inflation or delayed procurement cases. Where bottom-up evidence is thin, variance caps derived from component cost trends limit over or under-statement.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, with automated anomaly flags for outliers beyond ±8%. Material deviations trigger re-contact with sources. Reports refresh annually, and an interim scan is run when major recalls, reimbursement shifts, or geopolitical events could sway demand.

Why Mordor's Medical Electronics Baseline Earns Decision-Maker Confidence

Published market values often diverge because firms differ in scope choices, pricing assumptions, and update cadence.

Key gap drivers include whether implantables and semiconductor revenues are folded in, how currency conversions handle recent volatility, and if service contracts are recognized alongside hardware. Mordor's model sticks to end-device electronics only, applies transaction-date FX rates, and refreshes every twelve months, producing a balanced, transparent baseline that buyers can readily trace.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.33 B (2025) | Mordor Intelligence | - |

| USD 172.4 B (2024) | Global Consultancy A | Counts semiconductor and contract manufacturing revenue; broad component scope inflates total |

| USD 6.0 B (2023) | Research Firm B | Narrow component set; older base year and constant-dollar forecast dampen value |

| USD 8.25 B (2024) | Trade Journal C | Excludes implantables and therapeutic devices; reliance on limited hospital spend surveys |

These comparisons show that our disciplined scope definition, variable selection, and rolling validation give stakeholders a dependable starting point for strategy and budgeting decisions.

Key Questions Answered in the Report

What is the projected value of the medical electronics market in 2031?

Forecasts indicate USD 16.44 billion by 2031, reflecting a 6.65% CAGR over 2026-2031.

Which product category is expected to grow fastest toward 2031?

Wearables and implantables are on track for a 10.73% CAGR, outpacing all other categories as remote monitoring scales under new reimbursement codes.

How large is cardiology’s revenue contribution?

Cardiology devices accounted for 29.44% of 2025 sales and remain the largest clinical application slice.

Why is helium scarcity a concern for imaging centers?

Rising helium prices lengthen MRI magnet lead-times and push providers toward zero-boil-off or alternative imaging modalities.

Which region will expand quickest through 2031?

Asia-Pacific leads with an 8.02% CAGR, propelled by China’s localization drive and India’s PLI incentives for local manufacturing.

What compliance changes will most impact new device launches?

The forthcoming IEC 60601-1 4th Edition and tougher cybersecurity rules will demand deeper design verification and post-market surveillance.

Page last updated on: