Medical Equipment Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

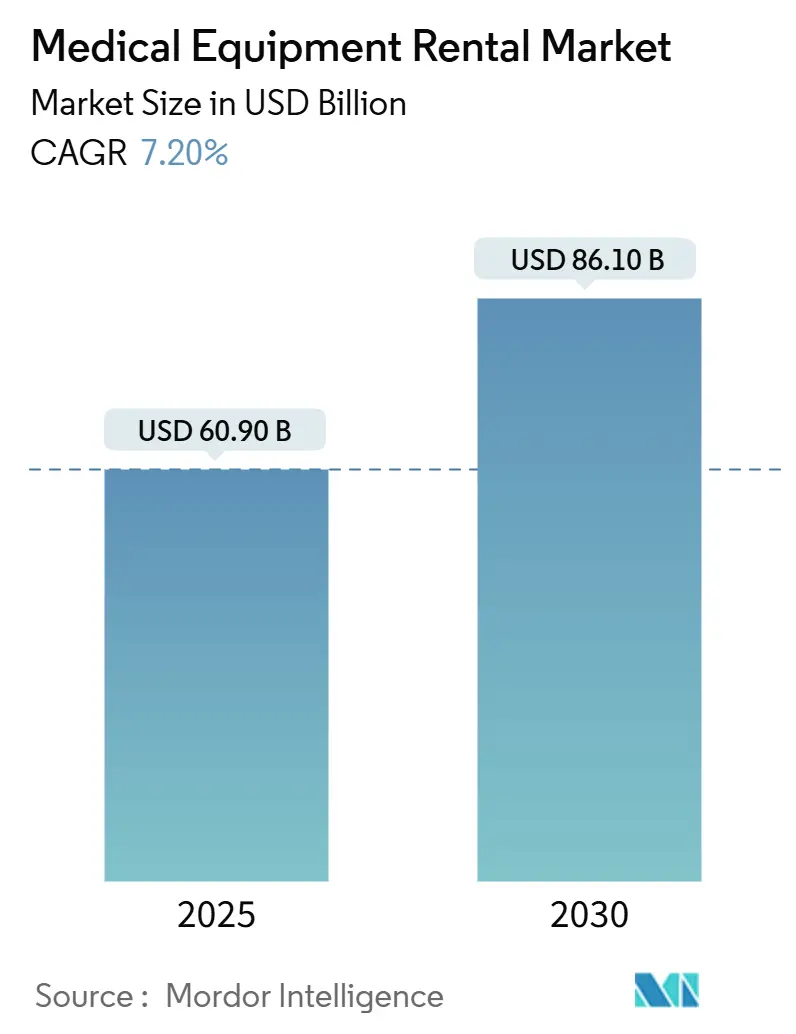

| Market Size (2025) | USD 60.90 Billion |

| Market Size (2030) | USD 86.10 Billion |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

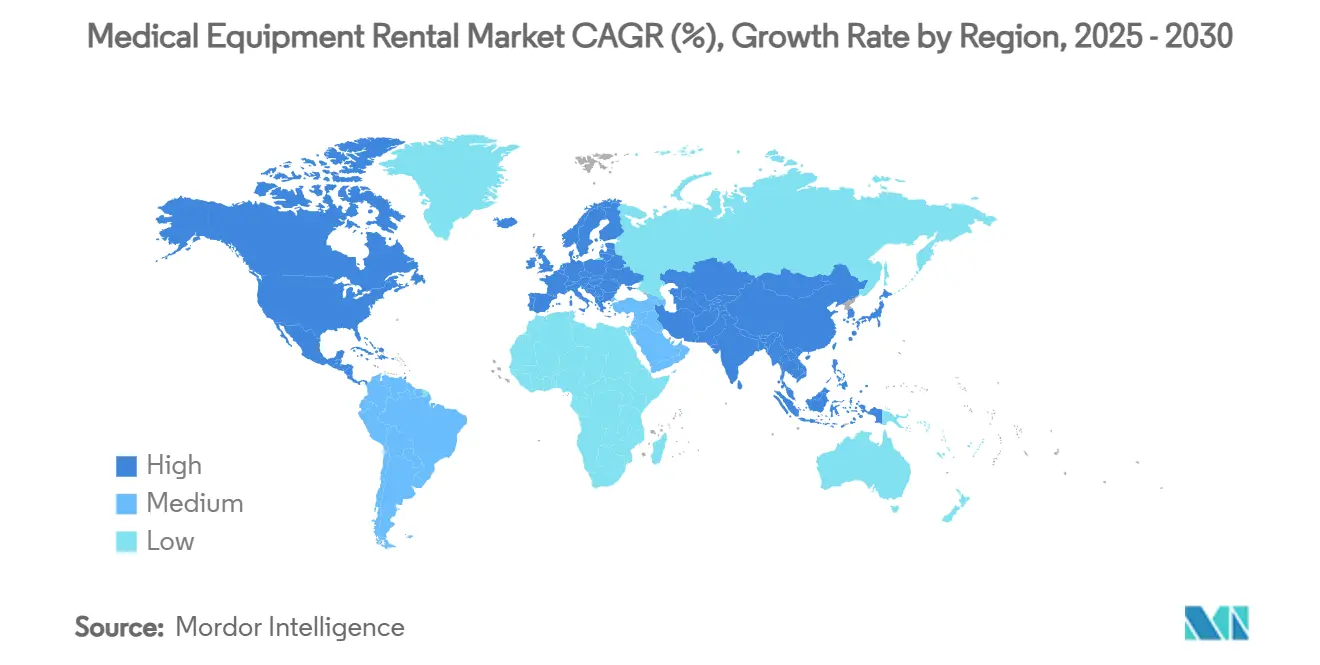

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Equipment Rental Market Analysis by Mordor Intelligence

The Medical Equipment Rental Market size is estimated at USD 60.90 billion in 2025, and is expected to reach USD 86.10 billion by 2030, at a CAGR of 7.20% during the forecast period (2025-2030).

The medical equipment rental market is expanding as hospitals, long-term care facilities and home-care providers pivot toward asset-light models that cushion capital budgets, enable rapid capacity scaling and shorten the technology refresh cycle. Growing chronic disease prevalence, surging demand for hospital-at-home programs and the increased adoption of AI-enabled fleet analytics are together accelerating uptake across every region. Europe’s entrenched reimbursement frameworks, Asia Pacific’s sweeping infrastructure investments and North America’s emphasis on operational flexibility offer distinct regional growth pathways. Competitive momentum is shifting toward integrated service platforms that bundle rental, maintenance, logistics and connected-device cybersecurity under a single contract.

Key Report Takeaways

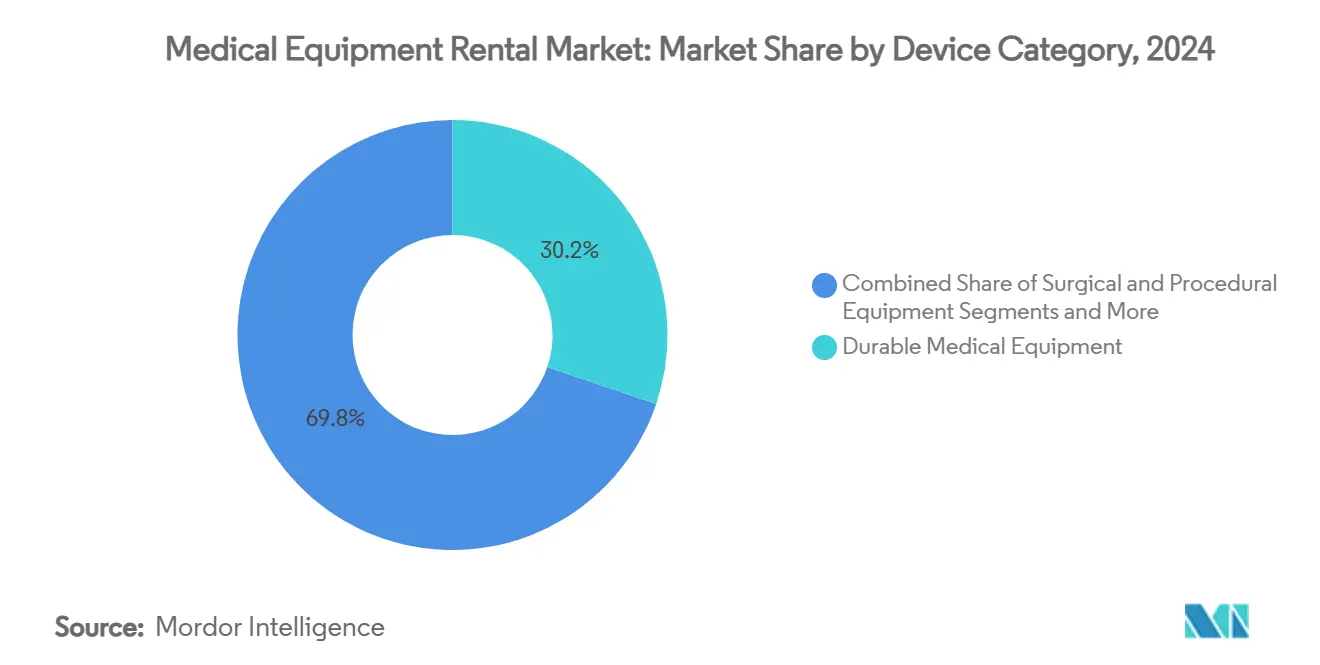

- By device category, Durable Medical Equipment led with 30.2% of medical equipment rental market share in 2024, while Home-care & Personal-use Equipment is forecast to expand at a 7.3% CAGR through 2030.

- By end user, Hospitals & Acute-Care Centers held 24.3% revenue share in 2024, whereas Home-care Patients are advancing at a 7.8% CAGR to 2030.

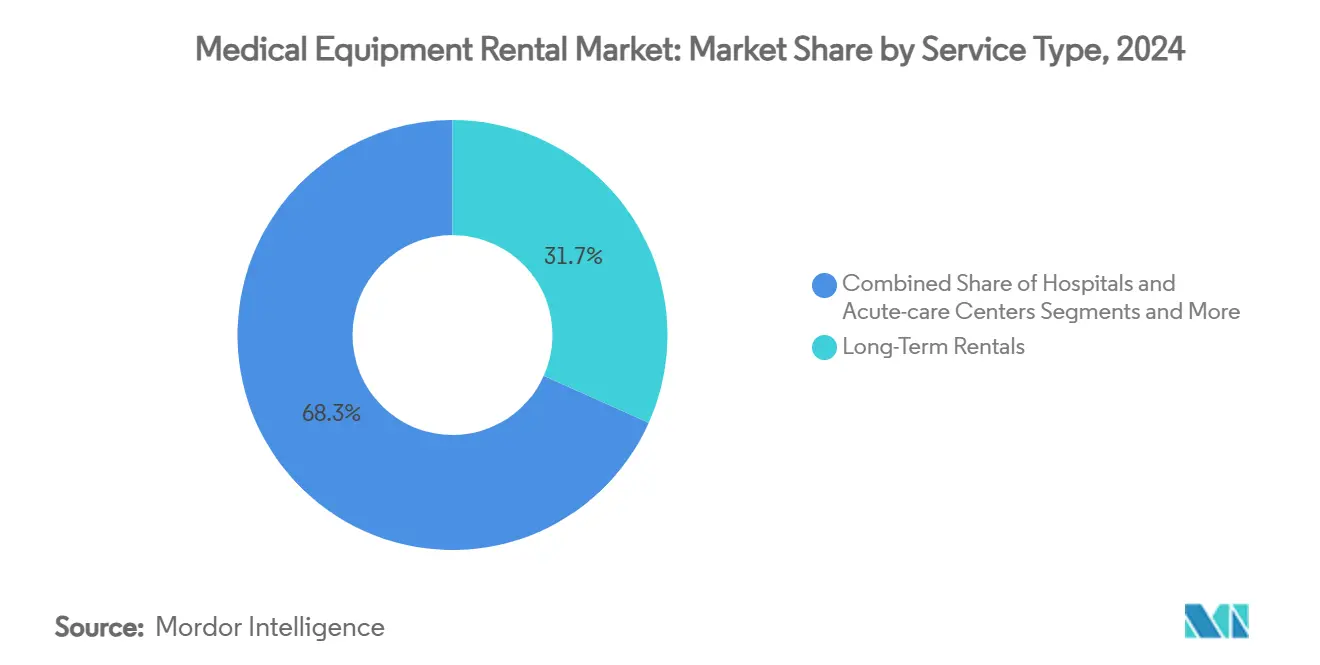

- By service type, Long-Term Rentals captured 31.7% share in 2024, and Short-Term Rentals are projected to register the highest 8.2% CAGR through 2030.

- By geography, Europe commanded a 29.1% share of the medical equipment rental market in 2024; Asia Pacific is poised for a 6.6% CAGR to 2030.

Global Medical Equipment Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & chronic disease burden | +1.50% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Shift to cost-efficient home-care models | +1.20% | North America & Europe leading, Asia Pacific following | Medium term (2-4 years) |

| Hospital CAPEX constraints favouring asset-light rentals | +0.80% | Global, acute in developed markets | Short term (≤ 2 years) |

| Growing demand for ICU surge/peak-need equipment | +0.60% | Global, episodic spikes | Short term (≤ 2 years) |

| AI-enabled utilisation analytics for fleet optimisation | +0.40% | North America & Europe early uptake, Asia Pacific emerging | Medium term (2-4 years) |

| Circular-economy & ESG mandates lengthening asset life | +0.30% | Europe leading, others following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Chronic Disease Burden

A steadily older demographic profile is reshaping utilization patterns across the medical equipment rental market. Medicare’s 2025 rollout of new HCPCS codes for dynamic stretching and pneumatic compression devices broadened reimbursable rental categories, acknowledging that ownership-based supply chains cannot flex fast enough to meet complex, multi-morbidity needs.[1]Centers for Medicare & Medicaid Services, “HCPCS Quarterly Update,” cms.gov Providers now rely on rental contracts to obtain bariatric beds, pressure-relief mattresses, and oxygen therapy systems without tying up scarce capital. Patients benefit from access to the latest devices, upgraded as therapy protocols evolve, while payers curb upfront spending. Rental operators equally gain longer average contract terms that stabilize revenue streams and justify investments in predictive maintenance.

Shift to Cost-Efficient Home-Care Models

Institutional care’s high fixed cost structure is prompting health systems to push treatment out of the ward and into the living room. Government-backed hospital-at-home pilots in Australia and Singapore are fueling demand for portable infusion pumps, remotely monitored CPAP units, and lightweight patient lifts. The medical equipment rental market thus finds itself at the nexus of telehealth expansion and patient-centric design. Providers that master just-in-time delivery, doorstep training, and cloud-enabled device monitoring are carving out a durable advantage. Equipment formats are also evolving: battery life is extending, user interfaces are becoming touchscreen-intuitive, and ruggedised casings support cross-country logistics in diverse climates.

Hospital CAPEX Constraints Favoring Asset-Light Rentals

Operating margins remain tight as labor, pharmaceutical, and cybersecurity costs climb. Hospitals now scrutinize every dollar locked into depreciating hardware, preferring multi-year rental agreements that roll service, software upgrades, and compliance certification into a single monthly line item. The medical equipment rental market thereby becomes the conduit through which hospitals access robotic surgery towers, hybrid OR imaging suites, and specialty ventilators without facing write-down risk when technology leapfrogs. As one Midwest health network renegotiated MRI ownership into a seven-year pay-per-use contract, it unlocked USD 12 million for workforce development while ensuring annual coil upgrades.

Growing Demand for ICU Surge/Peak-Need Equipment

COVID-19 exposed rigid capacity planning. To hedge against future pandemics and climate-related mass-casualty events, governments are underwriting regional surge pools of critical care devices. Rental firms now stock modular ventilator fleets, negative-pressure transport pods, and portable monitors that can be dispatched to hot spots within 24 hours. Container-based mobile ICU pods validated during 2024 hurricane responses cut deployment time by 70% versus fixed builds.[2]Health Management.org Editorial Team, “Shipping-Container ICUs: Rapid Surge Capacity,” healthmanagement.orgThe medical equipment rental market benefits from recurring readiness fees layered atop usage-based charges.

AI-Enabled Utilization Analytics for Fleet Optimization

Predictive analytics platforms mine device telemetry to forecast maintenance, rotate underused assets, and right-size fleet composition. Early adopters have trimmed unplanned downtime by 18% while extending asset life by two cycles. Hospitals gain real-time dashboards that flag idle units, prompting intra-system transfers instead of new rentals. Vendors capture higher EBITDA margins by squeezing more billable days per device. The medical equipment rental market thereby shifts from logistics-first to data-first, rewarding firms with the deepest algorithmic insights.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex reimbursement & capped-rental rules | −0.9% | North America primarily | Medium term (2-4 years) |

| High maintenance/calibration cost of hi-tech devices | −0.7% | Global, higher impact in emerging markets | Long term (≥ 4 years) |

| Cyber-security & data-privacy risks for connected rentals | −0.5% | North America & Europe | Short term (≤ 2 years) |

| Refurbishment-parts supply bottlenecks | −0.4% | Global, specialised segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Reimbursement & Capped-Rental Rules

Medicare’s declining fee schedule—beginning at 10% of average purchase price for month one and sliding to 7.5% by month four—limits revenue headroom for US-based rental providers. Paperwork intensity further forces investment in clearinghouse software that smaller firms cannot afford. Consolidation may accelerate as niche operators struggle to remain compliant across divergent state Medicaid codes.

High Maintenance / Calibration Cost of Hi-Tech Devices

PET-CT scanners, surgical robotics, and hybrid cath lab equipment require OEM technicians, proprietary parts, and ISO-13485 audit trails. Service can consume 15-20% of rental OPEX, squeezing gross margins unless scale economies exist. Data-driven predictive maintenance trims truck rolls, yet cannot fully offset sensor costs and specialized labor.[3]E. Cheng, “Predictive Maintenance Adoption in Imaging,” Journal of Clinical Engineering, journals.lww.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Durable Lead, Home-Care Momentum

Durable Medical Equipment held 30.2% of the medical equipment rental market share in 2024 and remains the backbone for post-acute and chronic disease pathways. Wheelchairs, hospital beds, and oxygen concentrators occupy long-duration contracts that underpin consistent cash flows. Rental companies optimise asset yield through refurbishment cycles that extend unit life to seven years, well beyond the original depreciation benchmark. DME utilization peaks in regions with high Medicare penetration, while emerging-market growth is buoyed by expanding private insurance plans that reimburse rental periods longer than 90 days.

Homecare and personal-use Equipment, while presently a more minor revenue contributor, is projected to post the fastest 7.3% CAGR by 2030. Policymakers pushing de-institutionalization favor devices that combine medical-grade performance with consumer-level ergonomics. The medical equipment rental market size for this segment is set to climb as Bluetooth connectivity, voice-assisted controls, and remote clinical dashboards become standard. Suppliers that pair devices with wrap-around patient coaching generate lower return rates and higher Net Promoter Scores, reinforcing brand preference.

Surgical & Procedural Equipment rides the outpatient migration wave. Ambulatory surgical centre (ASC) procedure volumes are forecast to jump 21% by 2034, bolstered by private equity-funded site expansion. Rental agreements bridge capital gaps as ASCs scale capacity for orthopaedics and ophthalmology. Diagnostic & Imaging Equipment grapples with steep service-agreement pricing but benefits from bundled-payment imaging contracts that cushion reimbursement volatility. Storage & Transport Systems, though niche, deliver mission-critical value during emergency deployments and draw premium rates for turnkey logistics bundles.

By End User: Hospital Anchor, Home-Care Lift

Hospitals & Acute-Care Centers dominated revenue with a 24.3% share in 2024. Multi-year framework agreements cover broad equipment categories, from infusion devices to mobile X-ray units, embedding rental as a strategic lever for capital stewardship. However, growth prospects remain modest, tethered to stagnant inpatient admissions and capacity rationalization drives in urban catchments.

Home-care Patients constitute the fastest-expanding cohort at a 7.8% CAGR, reflecting the upsurge in hospital-at-home, remote rehabilitation, and chronic disease self-management programs. The medical equipment rental market size allocated to this end user is projected to widen as insurers authorize longer rental durations for negative pressure wound therapy pumps and insulin delivery systems. Vendors that integrate tele-monitoring portals and 24/7 helplines convert one-time device shipments into high-touch service relationships.

Long-term Care Facilities navigate strict infection-control codes that mandate routine device swap-outs. Rental programs tailored to mobility aids and pressure ulcer prevention beds help facilities comply without ballooning inventories. Ambulatory Surgical Centers look to the medical equipment rental market for ophthalmic microscopes, arthroscopy towers, and patient positioning systems on a per-procedure or capped monthly basis, allowing flexible case-mix expansion.

By Service Type: Stability Meets Flexibility

Long-Term Rentals captured 31.7% revenue in 2024, underscoring the steady need for continuous therapy devices supporting COPD, congestive heart failure and ALS management. Contracts span 12-36 months and often include mid-term upgrades, consumables supply and preventive maintenance clauses. Providers secure annuity-like revenue, while payers gain pricing certainty.

Short-Term Rentals, though smaller today, are projected to grow at an 8.2% CAGR as hospitals sharpen demand forecasting. The medical equipment rental market increasingly segments short-term packages by clinical pathway—cardiac cath week, bariatric surgery season or winter respiratory surge—rather than by calendar duration. Kaiser Permanente’s equipment sharing programme, which reduced system-wide rental expenditure by USD 8.6 million over two years, exemplifies how collaborative pooling maximizes asset utilization. Future models may blend subscription-style readiness fees with pay-per-use billing, blurring traditional service-type boundaries.

Geography Analysis

Europe retained 29.1% of the medical equipment rental market in 2024, underpinned by statutory insurance frameworks that reimburse rentals of mobility aids, respiratory therapy devices, and imaging platforms. Germany’s EUR 40 billion MedTech ecosystem nurtures refurbishing clusters that funnel pre-owned equipment into secondary and tertiary hospitals. The EU Medical Device Regulation, although stringent, has catalyzed quality-assurance investments that elevate renter confidence. NHS England’s shift to reusable laparoscopic instruments—a move expected to save GBP 11 million (USD 14.7 million) annually further embeds sustainability metrics into tender criteria.

North America forms the historical nucleus of the medical equipment rental market, yet growth remains tethered by Medicare’s capped rental policy. Rising cyber-vulnerability disclosures—up 59% year on year—now feature prominently in contract negotiations, pushing vendors to certify SOC2-compliant data pipelines. Domestic sourcing urgency amplified during 2024-2025 tariff negotiations, funneling demand toward US-based depots that hold validated safety stock.

Asia Pacific is the fastest-growing region, tracking a 6.6% CAGR through 2030. National health-tech blueprints in China, Japan, and India earmark subsidies for tele-ICU and remote diagnostic rollouts. The medical equipment rental market therein benefits from public-private partnerships that fund device fleets for underserved rural clinics. Manufacturers are setting up refurbishment hubs within ASEAN special economic zones to circumvent import duties and reduce last-mile delivery lead times by 25%.

Competitive Landscape

The medical equipment rental market is moderately fragmented: the top 10 players control under 40% of global revenue. Consolidation momentum is accelerating, illustrated by THL’s USD 2.5 billion acquisition of Agiliti in February 2025, Reuters, and Owens & Minor’s USD 1.36 billion purchase of Rotech Healthcare in July 2024. These moves pool logistics networks, harmonize contract management, and unlock bulk-purchase discounts from OEMs.

Technology now ranks alongside fleet size as a competitive separator. Leading providers deploy AI-driven command centers that visualize asset location, predictive maintenance windows, and consumable stock in real time. IoT-connected ventilators alert technicians ahead of filter expiration, cutting emergency service calls by 30%. Cybersecurity proficiency is emerging as table stakes, with vendors investing in device-level encryption and zero-trust architectures to satisfy tightening FDA and EMA guidance.

Circular-economy capability is the third battleground. Philips has demonstrated that refurbished cath lab systems cut carbon footprints by 28% without compromising uptime, winning ESG-minded tenders across Benelux. Smaller challengers are carving niches by specializing: one Mid-Atlantic firm focuses solely on mobile ICU pods, while a Tokyo-based start-up rents AI-ready ultrasound scanners calibrated for low-band 5G hospital networks.

Medical Equipment Rental Industry Leaders

Agiliti

Baxter

US Med-Equip

Arjo

Med One Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Philips launched its circular-economy initiative for Azurion 7 C20 cath lab systems, achieving a 28% carbon footprint reduction through refurbishment.

- February 2025: THL finalized a USD 2.5 billion acquisition of Agiliti, creating a top-tier multi-service equipment rental platform.

- December 2024: Care Synergy and RCC Medical Equipment formed a joint venture to supply hospice organizations across Colorado.

- November 2024: Henry Schein acquired Acentus, bolstering its home-care equipment rental reach within decentralized care models.

Global Medical Equipment Rental Market Report Scope

| Durable Medical Equipment (DME) |

| Surgical & Procedural Equipment |

| Home-care & Personal-use Equipment |

| Diagnostic & Imaging Equipment |

| Storage & Transport Systems |

| Hospitals & Acute-care Centers |

| Long-term Care Facilities |

| Home-care Patients |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Category | Durable Medical Equipment (DME) | |

| Surgical & Procedural Equipment | ||

| Home-care & Personal-use Equipment | ||

| Diagnostic & Imaging Equipment | ||

| Storage & Transport Systems | ||

| By End User | Hospitals & Acute-care Centers | |

| Long-term Care Facilities | ||

| Home-care Patients | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical equipment rental market?

The medical equipment rental market size is USD 60.9 billion in 2025.

How fast is the medical equipment rental market expected to grow?

It is forecast to register a 7.2% CAGR, reaching USD 86.1 billion by 2030.

Which region leads the medical equipment rental market?

Europe holds the largest regional share at 29.0% in 2024, thanks to robust reimbursement systems and circular-economy policies.

What device category is expanding the fastest?

Home-care & Personal-use Equipment is projected to grow at a 7.3% CAGR through 2030 as care shifts toward patient homes.

How are hospitals managing capital constraints?

Many hospitals prefer long-term rental agreements that bundle service and upgrades, preserving cash flow and allowing technology refresh flexibility.

Why is cybersecurity important for rental providers?

A 59% rise in reported medical-device vulnerabilities has made SOC2-compliant encryption and zero-trust frameworks essential to win contracts, especially in North America and Europe.

Page last updated on: