Automated External Defibrillator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

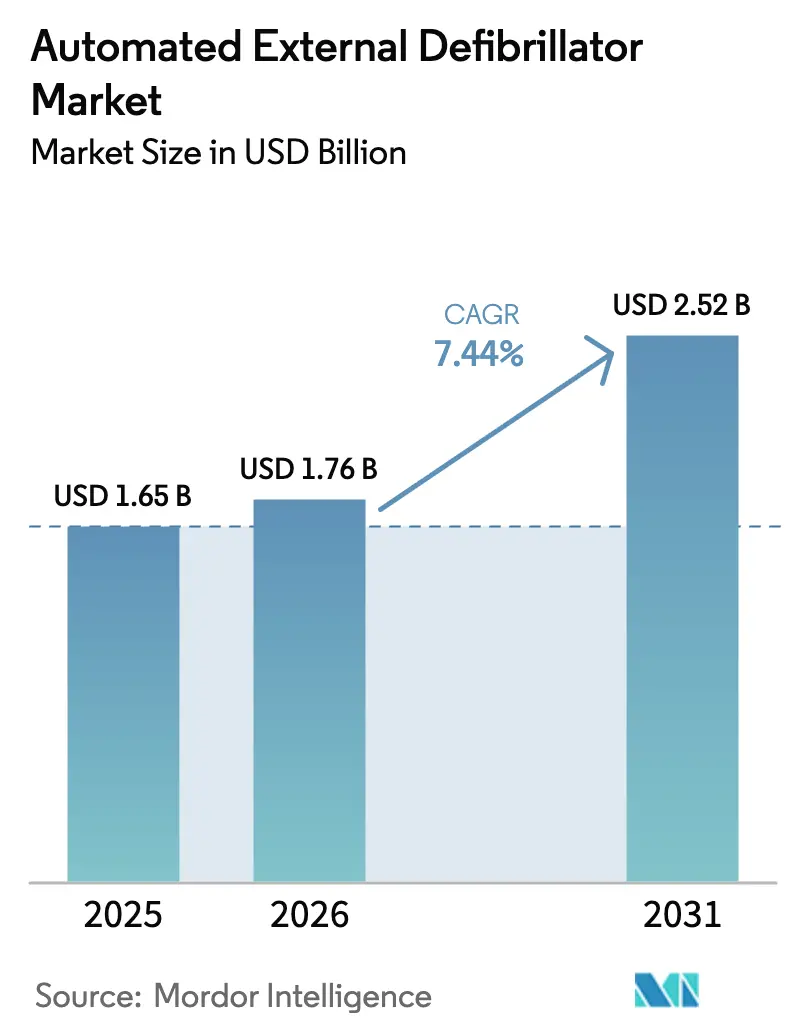

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

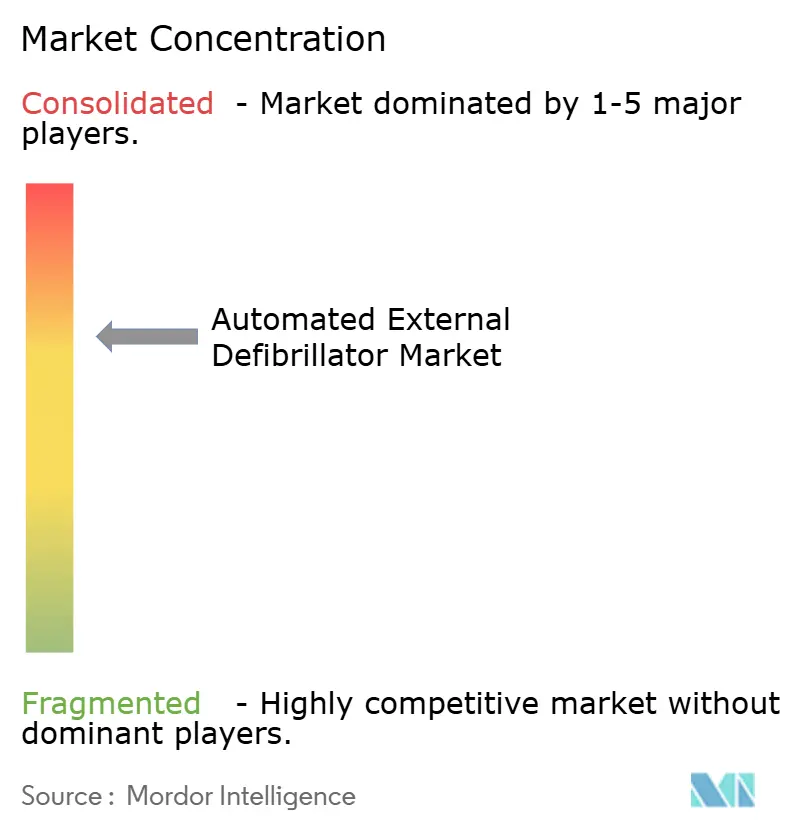

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated External Defibrillator Market Analysis by Mordor Intelligence

The Automated External Defibrillator Market size is expected to grow from USD 1.65 billion in 2025 to USD 1.76 billion in 2026 and is forecast to reach USD 2.52 billion by 2031 at 7.44% CAGR over 2026-2031.

Rising public-access programs, integration with smart-city platforms and expanding corporate ESG mandates are narrowing the life-saving gap between collapse and first shock. Vendors amplify demand by bundling training, consumables and cloud software into subscription contracts, which convert large cash purchases into manageable operating fees. Regulators on both sides of the Atlantic now favor biphasic, impedance-compensated waveforms, a shift that pushes hospitals and emergency medical services to replace older monophasic devices. Supply-chain reforms under the EU Battery Directive and U.S. reshoring policies reconfigure lithium sourcing, yet they also incentivize higher-density batteries that extend service intervals. Competitive intensity grows as connected-device start-ups and Chinese manufacturers vie with entrenched multinationals for hospital, workplace and community accounts.

Key Report Takeaways

- By product type, semi-automatic units held 58.24% of automated external defibrillator market share in 2025, whereas fully-automatic devices are forecast to expand at a 9.78% CAGR through 2031.

- By technology, biphasic waveform platforms commanded 91.11% share of the automated external defibrillator market size in 2025 and will progress at a 9.45% CAGR during the forecast window.

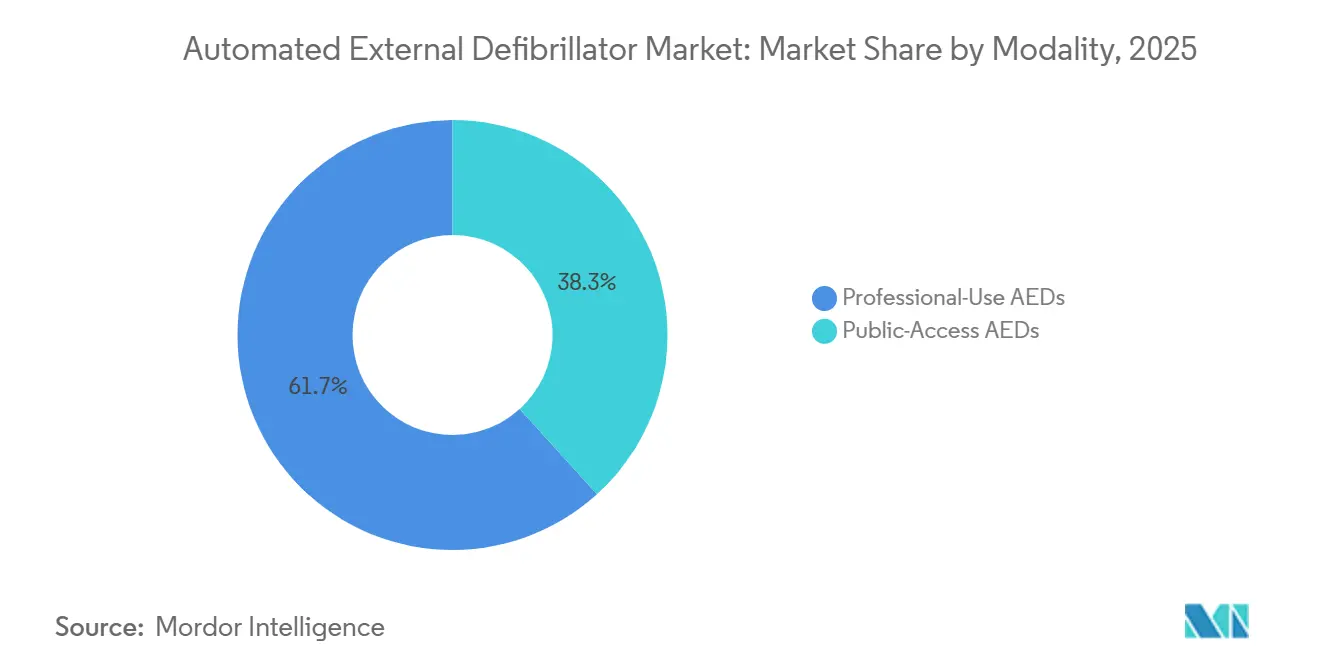

- By modality, professional-use models accounted for 61.73% revenue share in 2025, while public-access devices are projected to grow 10.25% annually to 2031.

- By end user, hospitals and clinics captured 58.34% share of the automated external defibrillator market size in 2025, yet public-access locations are advancing at a 10.64% CAGR.

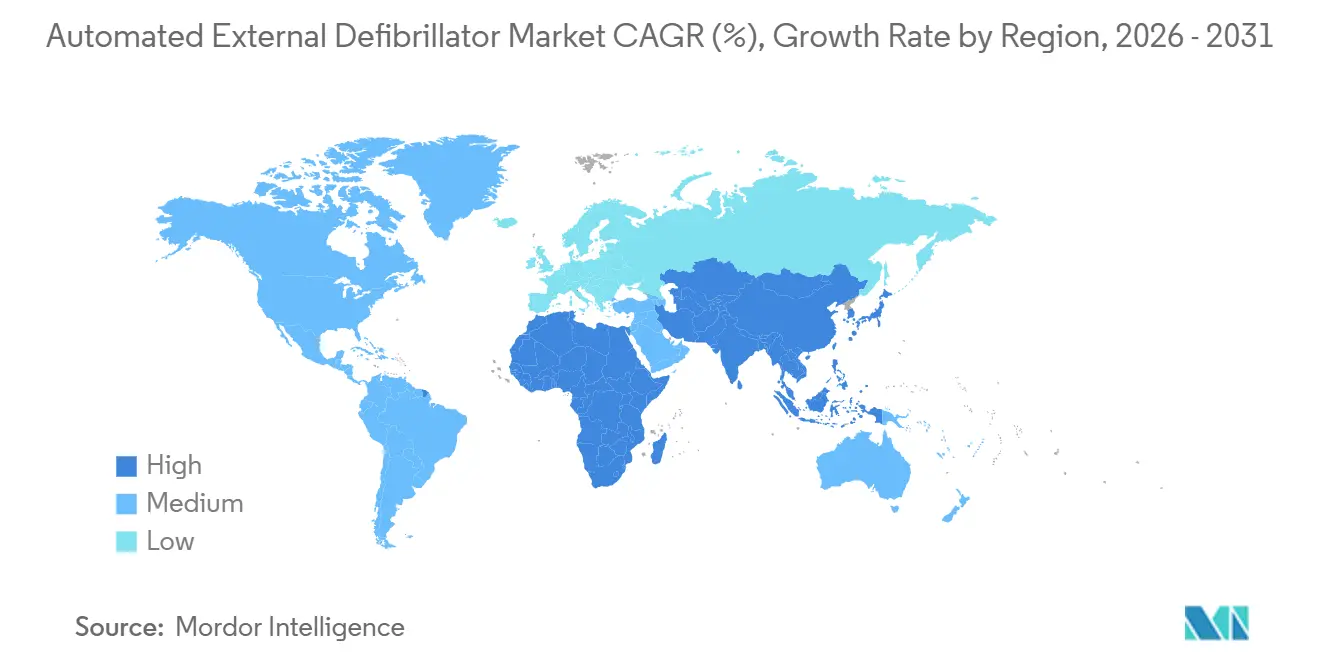

- By geography, North America led with 44.22% revenue share in 2025; Asia-Pacific is poised for the fastest 9.34% regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automated External Defibrillator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of sudden cardiac arrest (SCA) | 1.8% | Global, with acute burden in North America, Europe and urbanizing Asia-Pacific | Long term (≥ 4 years) |

| Government-funded Public Access Defibrillation (PAD) programs | 2.1% | North America & EU lead; APAC core (China, Japan, India) accelerating; spill-over to MEA | Medium term (2-4 years) |

| Technological shift to biphasic & impedance-compensated waveforms | 1.2% | Global, with regulatory emphasis in FDA and EU MDR jurisdictions | Medium term (2-4 years) |

| Integration of AEDs into smart-city IoT emergency networks | 0.9% | APAC core (China, South Korea), North America pilot cities, EU smart-city initiatives | Long term (≥ 4 years) |

| Corporate ESG mandates adding AED coverage to workplace HSE KPIs | 0.8% | North America & EU multinational headquarters; expanding to APAC subsidiaries | Short term (≤ 2 years) |

| Subscription-based "AED-as-a-Service" lowering CAPEX barriers | 0.6% | National, with early gains in United States, United Kingdom, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Sudden Cardiac Arrest (SCA)

Out-of-hospital SCA reached 350,000 U.S. events annually, and survival drops roughly 10% with every minute’s delay to defibrillation.[1]Samya Madhukar and Gina Peattie, “Latest Statistics,” Sudden Cardiac Arrest Foundation, sca-aware.org New American Heart Association 2025 guidelines shorten recommended response intervals and broaden pediatric protocols, prompting higher device densities in schools and sports venues.[2]American Heart Association, “2025 American Heart Association Guidelines for CPR and ECC,” American Heart Association, cpr.heart.org Municipal planners now map four-minute walk radii for AED placement, while during the CPR Awareness Week, India's Ministry of Health engaged over 747,000 citizens, providing physical training to more than 606,374 participants nationwide.[3]Press Information Bureau Staff, “Pan-India CPR Awareness Week Organized by Ministry of Health and Family Welfare to Strengthen Community Response Capacity,” Press Information Bureau, pib.gov.in Aging populations intensify baseline risk in Japan and Europe, but middle-income Asia-Pacific nations record the steepest absolute growth because lifestyle diseases are outpacing emergency-response build-outs.

Government-Funded Public-Access Defibrillation (PAD) Programs

China installed more than 64,000 public-access units in 2024, and Beijing committed to 2,000 networked cabinets with GPS telemetry. The United Kingdom set aside GBP 1 million (USD 1.27 million) in 2025 to place 2,000 devices in underserved areas. U.S. jurisdictions such as New York City and New Hampshire translate policy into bulk-buy contracts that quote Philips HeartStart OnSite at USD 898.79 and ZOLL AED Plus at USD 1,070. European decrees in France, Germany and Italy similarly mandate defibrillators in public buildings, creating predictable replacement cycles.

Technological Shift to Biphasic & Impedance-Compensated Waveforms

Biphasic shocks deliver higher first-shock success and less myocardial injury than legacy monophasic energy, an advantage embedded in FDA 510(k) clearances. ZOLL’s rectilinear biphasic waveform, validated in trials of 11,500 patients, underpins the AED 3 and AED Plus lines. Stryker’s LIFEPAK CR2 analyses rhythm during compressions, while Philips and Nihon Kohden add real-time impedance adjustment. Regulators harmonize dossiers under EU MDR, accelerating global rollouts and driving a replacement wave away from monophasic stock.

Integration into Smart-City IoT Emergency Networks

Daily self-test telemetry from Nihon Kohden’s Cardiolife AED-3100 flows via Bluetooth to cloud dashboards, alerting managers to expiring pads. ZOLL’s PlusTrac software links Wi-Fi equipped AED 3 units to dispatch centers, and Beijing pilots route the nearest trained bystander through WeChat when a 911-equivalent call falls within 300 meters of a registered cabinet. South Korea’s Emergency Medical Service Act encourages similar telemetry ties to its national 119 system. These integrations cut median time-to-shock by two to three minutes in early studies, justifying higher upfront device costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & maintenance cost for small institutions | -0.9% | Global, acute in rural North America, emerging APAC, MEA, South America | Medium term (2-4 years) |

| Limited reimbursement & liability concerns in emerging markets | -0.7% | APAC emerging (India, Indonesia, Philippines), MEA, South America | Long term (≥ 4 years) |

| Supply-chain dependence on lithium cells facing EU/US sourcing rules | -0.5% | Global, with regulatory pressure in EU (Battery Directive) and US (IRA, CHIPS Act reshoring) | Short term (≤ 2 years) |

| End-of-life environmental compliance (battery & pad waste) | -0.3% | EU (WEEE Directive), California, select APAC jurisdictions (Japan, South Korea) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Maintenance Cost for Small Institutions

A basic AED sells for USD 849-1,795, but five-year ownership doubles after pad, battery, cabinet and training expenses. Small nonprofits often depend on donated, non-connected devices, leaving one in five units unusable when needed. Grants exist yet administrative burdens deter the smallest clinics and volunteer fire departments, perpetuating geographic inequity.

Limited Reimbursement & Liability Concerns in Emerging Markets

National insurance schemes in India and Indonesia do not reimburse AED purchases, and Good Samaritan protections remain untested in courts, suppressing bystander willingness to intervene. China’s installations vary by province, and insurance carriers in many emerging markets exclude AED-related claims, forcing institutions to self-insure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Semi-Automatic Dominance Yields to Full-Auto Simplicity

Semi-automatic units controlled 58.24% automated external defibrillator market share in 2025, reflecting decades of training that tells rescuers to press a button only after confirming safety. Fully-automatic devices will compound at 9.78% through 2031 as public venues prefer hardware that fires without hesitation. ZOLL’s AED 3 and Stryker’s LIFEPAK CR2 come in both modes, letting buyers match user profiles. Airports and stadiums lean toward full-auto for untrained crowds, whereas hospitals still favor semi-auto for clinical oversight. Pricing parity—it often costs less than USD 100 to switch modes—removes cost as a barrier, leaving policies and confidence to steer adoption.

Fully-automatic gains feed the automated external defibrillator market by shortening pause time, which studies link to higher return-of-spontaneous-circulation rates. Regulatory frameworks in Japan and South Korea allow both modes, though their training curricula still echo semi-auto norms, slowing transition. As more public-access networks go live, familiarity with hands-free operation should accelerate replacement demand for semi-auto stock, nudging the automated external defibrillator industry toward simplicity.

By Technology: Biphasic Waveforms Cement Preference

Biphasic platforms captured 91.11% share of automated external defibrillator market size in 2025 and will rise 9.45% annually. FDA registrants now use biphasic comparators for substantial equivalence, effectively making monophasic filings obsolete. ZOLL’s rectilinear waveform adjusts energy to patient impedance, while Stryker’s cprINSIGHT analyzes rhythm without stopping compressions, removing one to two minutes of idle time per case.

Monophasic devices linger in older hospital inventories and low-income markets, but Chinese exporters are also adopting biphasic designs, cutting price gaps and speeding global phase-out. These advances align with studies showing higher first-shock efficacy and lower tissue damage, guaranteeing that future automated external defibrillator market replacements gravitate to biphasic hardware.

By Modality: Public-Access Surge Challenges Professional-Use Incumbency

Professional-use models owned 61.73% of revenue in 2025 because hospitals and EMS fleets value manual overrides and ECG integration. Yet public-access units are set to outgrow them at 10.25% CAGR as municipalities, schools and corporations follow updated building codes. China’s Red Cross placed 64,000 devices in 2024, and the U.K. funded another 2,000 for underserved areas, adding momentum.

Public-access buyers seek three-step voice-prompt simplicity, multilingual support and Wi-Fi self-tests, all while keeping prices between USD 849 and USD 1,795. EMS agencies will still buy rugged units with IP55 housing and longer-life batteries, but the volume story for the automated external defibrillator market clearly tilts toward public venues.

By End User: Public Access Locations Outpace Hospital Incumbents

Hospitals and clinics held 58.34% share in 2025, anchored by mandatory crash-cart stocking and data-system integration. Public-access sites, however, are expanding fastest at 10.64% CAGR, driven by building mandates and liability mitigation at sports arenas, transit hubs and office towers. New York City’s Local Law 20 and France’s Decree 2018-1186 crystallize these obligations.

Emergency medical services equip transport-grade models that survive temperature extremes, while home-care uptake remains low because consumer units still exceed USD 1,000. Venture-backed platforms like Avive aim to lower thresholds with connected home devices and subscription monitoring, foreshadowing another wave of automated external defibrillator market growth once payers and regulators catch up.

Geography Analysis

North America contributed 44.22% of 2025 revenue thanks to mature public-access legislation in all 50 U.S. states and federal grants under the Rural Access to Emergency Devices Act. New American Heart Association guidelines published in 2025 adjust device specs for schools and childcare centers. Canada and Mexico trail the U.S. in per-capita deployment but offer catch-up opportunity as provinces and private employers fund new placements.

Asia-Pacific is on track for the fastest 9.34% regional CAGR through 2031. China’s Red Cross installed 64,000 devices in 2024 and Beijing ordered 2,000 smart cabinets with live GPS feeds. Japan’s Fire and Disaster Management Agency continues to push devices into public facilities, and South Korea’s EMS Act requires units in schools and large commercial buildings. India’s CPR Awareness Week trains 606,374, yet federal AED mandates and liability clarity remain pending, limiting immediate conversion.

Europe balances moderate growth with stringent environmental rules. The United Kingdom has earmarked GBP 1 million for community placements, and France, Germany and Italy enforce location-specific mandates. The EU Battery and WEEE Directives raise compliance costs but also motivate upgrades to longer-life batteries and pad recycling programs. Middle East-Africa and South America remain nascent, although GCC nations and Brazil’s metro health secretariats are piloting public-access programs that could scale on positive survival data.

Regulatory Landscape

Automated external defibrillators (AEDs) are regulated as high-scrutiny medical devices in major markets, which influences product design, documentation, and lifecycle obligations. In the United States, AEDs fall under FDA device classification (21 CFR 870.5310) as Class III devices and are tied to Premarket Approval (PMA) expectations alongside ongoing postmarket oversight (including FDA Total Product Life Cycle reporting for the relevant product code). A key compliance inflection is the FDA Quality Management System Regulation (QMSR), which became effective on February 2, 2026, requiring manufacturers and critical suppliers to align quality systems to the updated framework and audit expectations.

In Europe, AED market access is governed by the Medical Device Regulation (EU) 2017/745 (EU MDR), with conformity assessment performed via Notified Bodies and supported by technical documentation, EU Declarations of Conformity, and UDI requirements (including Basic UDI-DI). The MDR transition window for certain legacy devices extends into 2027-2028 under the MDR transitional provisions, creating near-term pressure to maintain certificates while completing MDR upgrades. In the United Kingdom, the post-Brexit framework continues to evolve, and strengthened post-market surveillance provisions enacted in 2024 increase reporting and vigilance expectations for manufacturers and importers placing AEDs on the UK market.

Value Chain Analysis

The AED value chain begins with specialized upstream inputs, including high-reliability electronics (processors, sensors, and energy-storage components such as capacitors), lithium-based batteries, and single-use consumables such as electrode pads that rely on conductive hydrogels and engineered backing films. Because AEDs are FDA Class III devices, manufacturing and supplier controls are closely tied to regulated quality systems (commonly aligned to ISO 13485), design controls, and traceability for safety-critical parts. Electrode pad production is also a distinct sub-chain, using cleanroom-oriented steps such as film handling, hydrogel application, lamination, die-cutting, and sealed packaging to preserve shelf-life and performance.

Midstream, OEMs integrate hardware, embedded software, and increasingly connectivity modules for self-test telemetry and fleet-management dashboards, expanding requirements beyond assembly into software validation, cybersecurity processes, and cloud integration. Downstream, routes to market bifurcate between institutional sales (hospitals, EMS, and enterprise workplace deployments), public tenders linked to PAD programs, and distributor-led or e-commerce-led placements for schools, small businesses, and community sites. Service layers such as training, readiness monitoring, pad and battery replenishment, and compliance documentation are frequently bundled into subscription models, shifting some value capture from one-time device sales to recurring program management across installed fleets.

Competitive Landscape

The top five suppliers, ZOLL Medical, Stryker, Bridgefield-owned Philips Emergency Care, Cardiac Science, and Nihon Kohden, together control more than half of the revenue, giving the automated external defibrillator market a moderate level of concentration. ZOLL monetizes Real CPR Help and See-Thru algorithms at premium prices in EMS and hospital channels, while Stryker’s LIFEPAK CR2 targets buyers seeking minimal pause time. Philips’ January 2025 divestiture signals a pivot away from hardware, inviting rivals and Chinese entrants such as Mindray to chase freed share.

IoT-centric challengers intensify rivalry. Avive raised USD 56.5 million in 2024 to commercialize cloud-connected devices that stream event data directly to 911 dispatch. Distributors like Safe Life, valued at EUR 500 million by Bridgepoint in 2025, aggregate multibrand offerings and overlay compliance software, capturing margin via service rather than hardware.

White-space opportunities include home-use devices and full-stack program-management platforms that bundle training, consumables and telemetry into recurring subscriptions. Regulatory harmonization under EU MDR and streamlined FDA 510(k) pathways lower barriers for newcomers, while smart-city pilots normalize Wi-Fi and cellular connectivity, shifting competition from hardware specs to data ecosystems and service quality.

Automated External Defibrillator Industry Leaders

Stryker Corporation

Nihon Kohden Corporation

Koninklijke Philips NV

Asahi Kasei (ZOLL Medical)

Shenzhen Mindray Bio-Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public-access mandates and program refresh cycles are creating whitespace in community and retail footprints where coverage remains uneven, while connectivity and compliance tooling are increasingly used as procurement differentiators. In the United States, state-level program updates provide a visible trigger for new placements and formalized compliance requirements: Maryland enacted Chapter 92 (Senate Bill 24) in April 2026 to revise its Public Access Automated External Defibrillator Program, including specific certification requirements for grocery stores and restaurants, with provisions taking effect October 1, 2026. These rules increase demand not only for devices, but also for documentation, inspection automation, and staff training packages that reduce the compliance burden for multi-site operators.

A second opportunity area is the shift from standalone devices to connected AED ecosystems that reduce inspection burden and improve readiness. FDA review activity around connected AEDs points in this direction, including the May 2026 status that HeartHero had an FDA premarket application under review for a connected AED paired with a mobile app for readiness monitoring and device status reporting. For incumbents, incremental PMA supplements support differentiation and refresh purchases within existing fleets, as shown by ZOLL Medicals PMA supplement approval (P160015/S025) in December 2025 for AED 3 labeling updates that incorporate post-approval study results. Together, these developments support demand for IoT-enabled fleet management, subscription-based AED-as-a-Service offerings, and replacement of older non-connected or legacy platforms in schools, workplaces, and public-access networks.

Recent Industry Developments

- January 2026: Nihon Kohden Corporation approved the acquisition of a 90.3% stake in DOWELL Co., Ltd. to make it a consolidated subsidiary. The move supports Nihon Kohdens scale in adjacent medical-technology capabilities and can support broader commercialization reach across its resuscitation and monitoring portfolio.

- April 2025: Canon Marketing Japan began supplying fully automated AED models from Nihon Kohden (AED-3250) and Asahi Kasei ZOLL Medical (ZOLL AED 3 Autoshock). The channel expansion increases availability of fully automatic AED options in Japan and supports faster deployment in public-access and workplace settings that prioritize minimal user intervention.

- October 2024: ZOLL Medical received EU MDR certification for the ZOLL AED Plus defibrillator. The certification helps sustain European market access under MDR and supports continuity for replacements and new public-access placements tied to local mandates and procurement cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the sales value of automated external defibrillators (AEDs) that analyze heart rhythm and deliver a shock when needed, across major regions and end-use settings, within the defined study window.

Scope exclusions: Implantable cardioverter defibrillators, wearable cardioverter defibrillators, and standalone manual external defibrillators are excluded.

Segmentation Overview

- By Product Type

- Semi-Automatic AEDs

- Fully-Automatic AEDs

- By Technology

- Biphasic Waveform AEDs

- Monophasic Waveform AEDs

- By Modality

- Professional-Use AEDs

- Public-Access AEDs

- By End User

- Hospitals & Clinics

- Emergency Medical Services (EMS)

- Public Access Locations

- Home Care

- Others (Training Institutions, Corporate Wellness)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on sudden cardiac arrest incidence, emergency response norms, and AED access rules, and then mapping how these translate into device demand over time. We mainly rely on non-paywalled sources such as World Health Organization publications, national health agencies like the US CDC, OECD health statistics, the US FDA device databases and safety notices, and select peer-reviewed clinical and health-economics journals.

To ground the commercial side, public sources like annual reports, investor presentations, product brochures, tender notices, and reputable press are read to understand product positioning and typical replacement cycles for batteries and pads. In parallel, we use approved paid subscriptions for company financials and intelligence, news and financials, patent databases, and, where relevant, a global contracts and tenders view to sanity check where public access deployments are accelerating. These desk sources are illustrative rather than exhaustive, and several other public datasets and filings were also reviewed to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work focuses on checking what is really being purchased, and how buying decisions differ by public access programs, hospitals, EMS providers, and large workplaces. We interview and survey a mix of manufacturers, distributors, service partners, clinical users, and procurement teams across APAC, EMEA, and the Americas, which helps narrow gaps around pricing, installed base refresh timing, and compliance-driven demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 44% |

| Mid tier: 55% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 19% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using both top-down and bottom-up logic. The main build starts from a demand-pool view that links sudden cardiac arrest incidence, AED placement norms, and replacement cycles to annual unit needs by region. Once that structure is in place, totals are cross-checked using selective bottom-up approximations like sampled ASP times unit volumes, distributor channel checks, and partial supplier roll-ups where disclosure is available, and then the final numbers are adjusted only when the checks keep pointing in the same direction.

Inputs are kept practical and traceable, so the model leans on variables such as public access AED penetration trends, EMS adoption rates, typical battery and electrode pad change intervals, pricing differences between semi-automatic and fully-automatic units, and regulatory or guideline changes that affect placement requirements. Where unit data is thin for smaller countries, gaps are handled using proxy indicators like population, urbanization, healthcare spend, and observed procurement activity, followed by validation calls to avoid overstretching assumptions.

For forecasting, scenario analysis is used to reflect how AED deployment programs can ramp up quickly after policy moves, and how replacement demand behaves more steadily once an installed base is built. Scenarios are tied back to expert inputs on procurement budgets, training intensity, and expected price movements, so the forecast stays aligned with what buyers and channels indicate is realistic.

Data Validation & Update Cycle

Validation is done by triangulating model outputs against independent signals like procurement patterns, product-mix shifts, and country-level adoption narratives that show whether demand is expanding through new placements or mostly through replacement. When outliers appear, the drivers are rechecked, assumptions are revisited, and targeted re-contacts are triggered to confirm whether the variance is real or caused by timing, currency, or one-off purchasing.

Before sign-off, the full model goes through multi-step analyst review, including cross-checks of growth rates, regional shares, and implied unit volumes versus what stakeholders describe in the field. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so the published view reflects the latest available information.

Mordor Intelligence's Global Automated External Defibrillator Market Market Size Compared With Other Published Estimates

It is common to see different AED market values across publications, even when the same end-use wording is used, because boundaries and counting rules can change the total. The biggest drivers usually come from what products are included, whether recurring consumables are counted beyond the first sale, and how the current year is defined in currency terms.

By tracking bundled first-sale software and disposables and keeping implantable, wearable, and standalone manual defibrillators out of scope, Mordor Intelligence produces an AED-only number that typically differs from totals that blend in adjacent device categories or extend recurring revenue assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.76 B (2026) | |

| Global Consultancy A | USD 1.51 B (2024) | Uses a different base year and may emphasize hospital channels more than public-access programs, which can understate replacement-led demand when deployments broaden. |

| Trade Journal B | USD 1.99 B (2024) | Likely applies a wider revenue lens, where longer-run consumables or adjacent defibrillator offerings can be counted alongside AED device sales, lifting the reported value. |

The spread is mainly explained by scope boundaries and timing, followed by how replacement cycles are converted into yearly sales and priced across regions. When assumptions are tied back to placement activity, replacement intervals, and channel feedback, the steps stay repeatable and easier to reconcile with observed buying behavior.

Key Questions Answered in the Report

What is the current value of the automated external defibrillator market?

The market is valued at USD 1.76 billion in 2026 and is forecast to reach USD 2.52 billion by 2031.

How fast is demand for public-access AEDs growing?

Public-access units are projected to expand at a robust 10.25% CAGR through 2031, outpacing professional-use devices.

Which technology dominates new AED approvals?

Biphasic, impedance-compensated waveforms account for more than 90% of 2025 sales and remain the regulatory preference.

Why are subscription models becoming popular?

AED-as-a-Service spreads device, consumables and training costs into predictable annual fees, easing budgets for schools and small businesses.

Which region offers the fastest growth potential?

Asia-Pacific leads with a projected 9.34% CAGR as China, Japan and India scale national public-access programs.

What challenges limit wider deployment in emerging markets?

High upfront costs, limited reimbursement and uncertain Good Samaritan liability protections hamper adoption despite rising cardiac-arrest incidence.

Page last updated on: