Medical Cameras Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

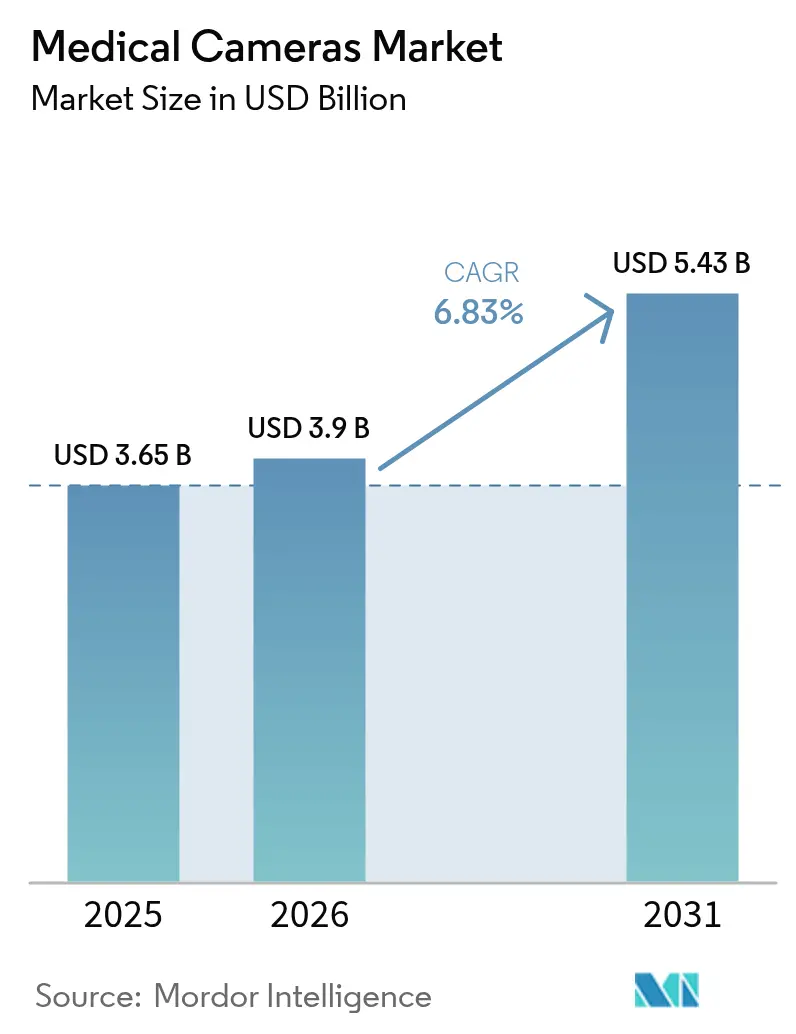

| Market Size (2026) | USD 3.9 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

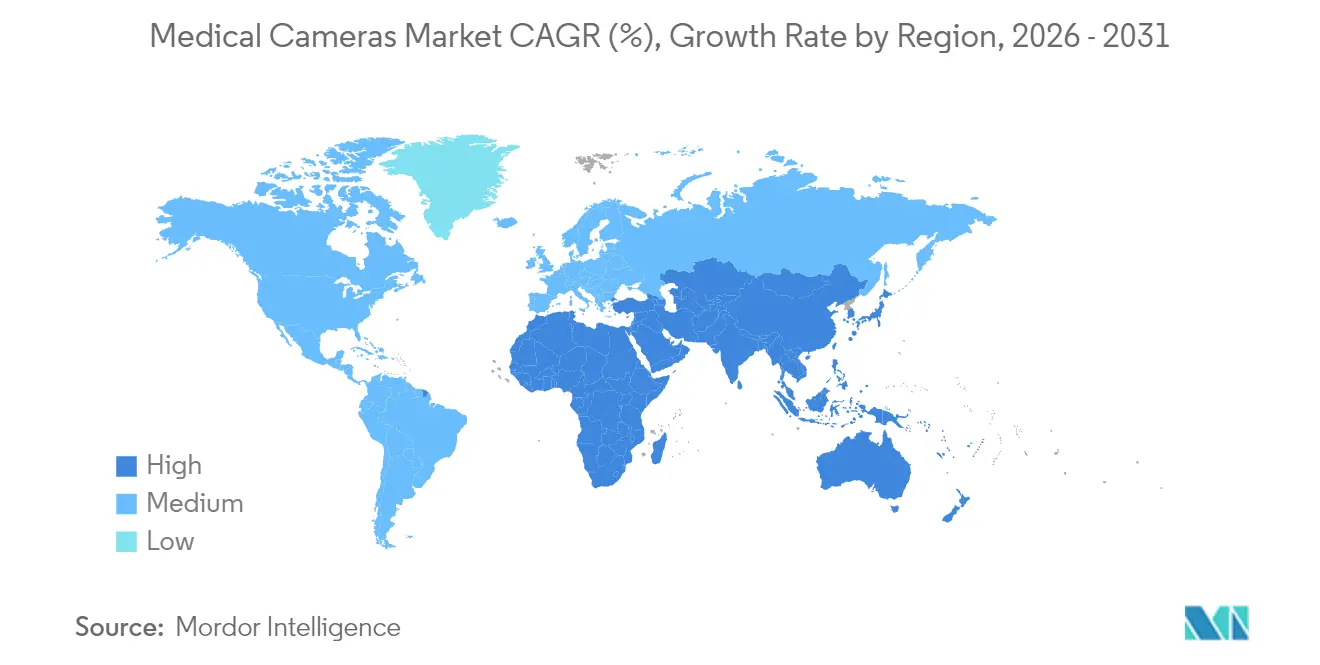

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

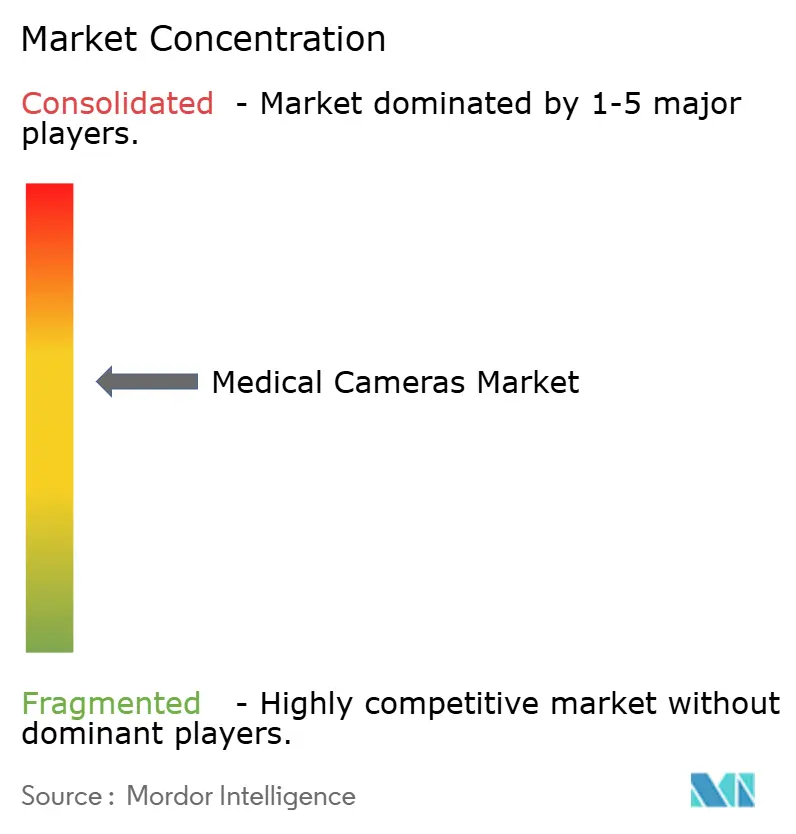

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Cameras Market Analysis by Mordor Intelligence

The Medical Cameras Market size market is expected to grow from USD 3.65 billion in 2025 to USD 3.9 billion in 2026 and is forecast to reach USD 5.43 billion by 2031 at 6.83% CAGR over 2026-2031.

This expansion is propelled by the transition from standard-definition to ultra-high-definition 4K and 8K visualization, the rise of minimally invasive surgery, and steady procedure growth in oncology, cardiology, and gastroenterology. Demand for single-use and capsule endoscopes is rising as infection-control protocols tighten, while hospitals pursue technology upgrades that shorten operating times and speed patient recovery. Asia-Pacific is gaining prominence as government programs foster domestic medical-device manufacturing, yet North America retains the largest installed base because of early adoption of premium imaging platforms. Competitive momentum centers on integrating artificial intelligence (AI) into camera ecosystems to deliver automated lesion detection and real-time tissue characterization.

Key Report Takeaways

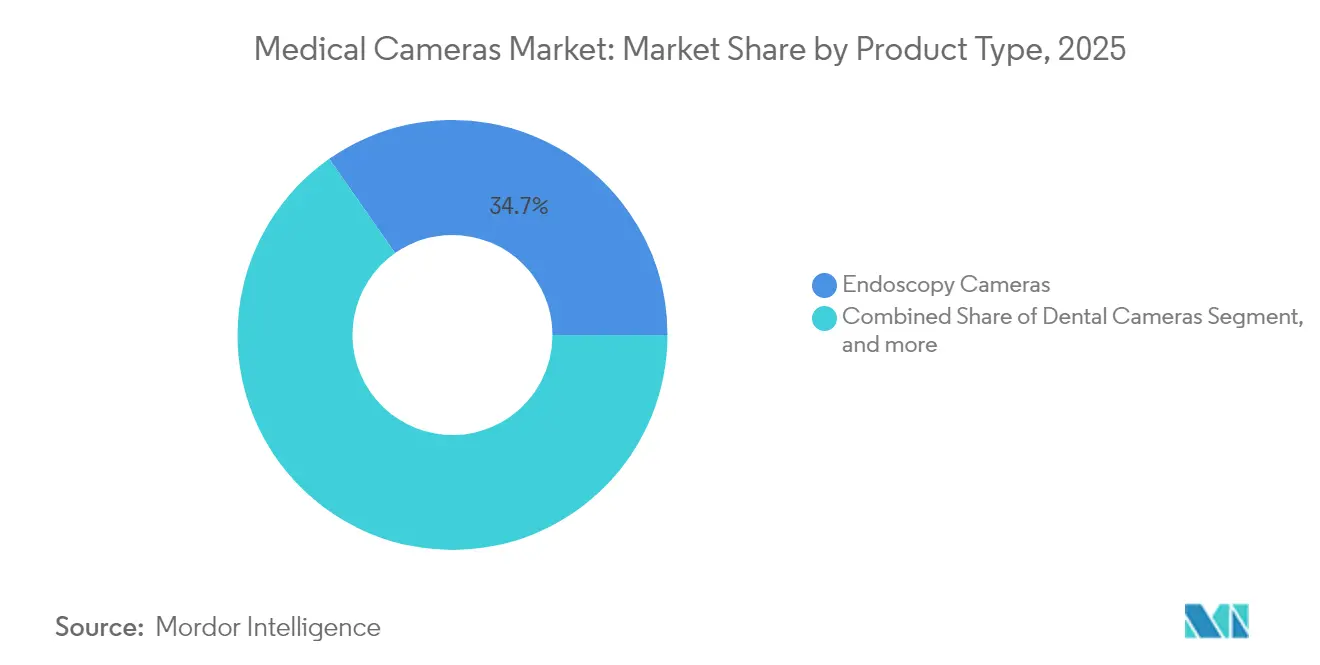

- By product type, endoscopy cameras held 34.72% of the medical cameras market share in 2025; capsule and disposable endoscopic cameras are advancing at an 7.76% CAGR through 2031.

- By resolution, high-definition systems accounted for 48.21% of the medical cameras market size in 2025, whereas 4K/8K platforms are expanding at an 8.34% CAGR to 2031.

- By sensor technology, CMOS led with a 63.84% share of the medical cameras market size in 2025, while sCMOS is registering the fastest 9.05% CAGR.

- By end user, hospitals commanded 54.21% revenue share in 2025; ambulatory surgery centers are growing at an 7.9% CAGR through 2031.

- By geography, North America captured 34.85% of the global total in 2025, yet Asia-Pacific is projected to log a 9.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Cameras Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for 4K/8K ultra-HD visualization in minimally invasive surgeries | +1.8% | North America, Europe, expanding globally | Medium term (2-4 years) |

| Growing adoption of endoscopy procedures worldwide | +1.5% | Accelerated growth in Asia-Pacific | Long term (≥ 4 years) |

| Increasing prevalence of chronic diseases requiring surgical interventions | +1.2% | Highest impact where populations are aging | Long term (≥ 4 years) |

| Integration of AI-powered real-time tissue characterization | +1.0% | North America & Europe lead | Medium term (2-4 years) |

| Surge in demand for wireless, capsule & nano-cameras | +0.9% | Strong uptake in developed markets | Short term (≤ 2 years) |

| Shift toward hybrid operating rooms and integrated imaging workflows | +0.8% | North America & Europe core, Asia-Pacific adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for 4K/8K Ultra-HD Visualization in Minimally Invasive Surgeries

Surgeons report that four-fold pixel density relative to HD exposes microvascular patterns and subtle tumor margins that previously went unnoticed, enabling earlier resection and reducing the need for repeat procedures.[1]Olympus Corporation, “4K Camera Head CH-S700-08-LB Launch Announcement,” olympus-global.com Specialty imaging modes such as Narrow Band Imaging and Blue Light are bundled with these 4K cameras, further sharpening discrimination between malignant and benign tissue. Academic centers are documenting shorter operating times because clearer visualization lessens reliance on adjunct imaging. Capital budgets remain a hurdle because a full 4K stack costs upward of USD 200,000, yet leasing schemes and proof-of-outcome data are easing procurement decisions. As component prices fall, community hospitals are forecast to upgrade legacy HD systems during scheduled replacement cycles.

Growing Adoption of Endoscopy Procedures Worldwide

Global procedure volumes for gastrointestinal and pulmonary endoscopy are rising alongside screening programs and a preference for day-case interventions. The availability of AI-enabled camera heads that elevate adenoma detection by double-digit percentages is encouraging payers to extend reimbursement, driving equipment refreshes across Europe and North America.[2]Fujifilm Medical Systems, “FDA Clears CAD EYE Functionality,” fujifilm.com Single-use scopes eliminate re-processing labor and reduce cross-contamination risk an imperative solidified after the COVID-19 pandemic. Ambulatory surgery centers (ASCs) are expanding capacity to absorb overflow from hospitals, compelling manufacturers to fine-tune pricing for these cost-sensitive buyers. Market entrants offering disposable, wireless camera modules are well positioned to capture ASC demand.

Increasing Prevalence of Chronic Diseases Requiring Surgical Interventions

Cardiovascular disease, diabetes, and cancer collectively raise the number of diagnostic and therapeutic endoscopic procedures needed over a patient’s lifetime. Elderly patients benefit from smaller incisions and faster recovery associated with camera-guided minimally invasive techniques, translating into lower total cost of care for providers. Real-time tissue analytics powered by AI reduce the need for multiple interventions, boosting surgeon productivity and minimizing patient exposure to anesthesia.[3]MDPI, “Real-Time Tissue Characterization Using AI in Minimally Invasive Surgery,” mdpi.com Health-system planners in Asia-Pacific are prioritizing camera-equipped surgical suites in newly built facilities, driving multi-year purchase commitments that stabilize manufacturer order books. These secular factors underpin steady demand growth regardless of short-term economic cycles.

Integration of AI-Powered Real-Time Tissue Characterization

Deep-learning algorithms trained on large pathological datasets now identify lesions and flag bleeding sites in milliseconds, transforming cameras into decision-support tools. Automated annotation of suspicious areas shortens learning curves for junior surgeons and standardizes outcomes across institutions. Regulatory pathways are lengthening as agencies demand substantial validation datasets; typical 510(k) clearance timelines now stretch to six months for AI-enabled devices. Companies are mitigating risk through modular software updates that allow algorithms to evolve post-approval under predetermined change-control plans. Partnership with cloud vendors facilitates off-board processing, enabling lighter camera heads that improve ergonomics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and maintenance of camera systems | -1.5% | Most severe in emerging economies | Short term (≤ 2 years) |

| Stringent FDA / CE approval timelines | -0.8% | United States & European Union | Medium term (2-4 years) |

| Cyber-security risks in network-connected imaging devices | -0.6% | Developed markets adopting connectivity | Short term (≤ 2 years) |

| Supply-chain fragility for sensor-grade semiconductors | -0.5% | Global with regional variability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Maintenance of Camera Systems

A premium 4K tower couples high-grade optics, processors, and monitors that together exceed USD 200,000 per operating room. Annual service contracts and sensor re-calibration amplify lifetime cost, deterring budget-constrained facilities from rapid adoption. Emerging-market hospitals often postpone upgrades until multi-year equipment funds are approved, lengthening replacement cycles. Manufacturers are introducing tiered product lines and pay-per-procedure financing to lower upfront barriers. Meanwhile, disposable camera formats eliminate sterilization expense but require proof that per-case economics remain favorable beyond the break-even utilization threshold.

Stringent FDA / CE Approval Timelines

Designers integrating AI or wireless functions into medical cameras must navigate evolving guidance on software validation and radio-frequency safety testing. 510(k) submissions can exceed 180 days when device claims differ from predicates, delaying revenue recognition and extending R&D payback periods. European CE certification entails separate assessments for hardware and embedded software under the Medical Device Regulation, imposing documentation loads that small companies struggle to meet. Collaborative pre-submission meetings with regulators and phased modular approvals are emerging tactics to compress time-to-market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Endoscopy Cameras Anchor Demand

Endoscopy cameras contributed 34.72% to the medical cameras market in 2025 as they remain indispensable across gastroenterology, urology, and pulmonology suites. Capsule and single-use models are escalating at an 7.76% CAGR, reflecting infection-control imperatives that align with post-pandemic sterilization standards. Manufacturers are miniaturizing optics to sub-millimeter diameters, enabling swallowable devices that wirelessly transmit images for eight hours, expanding reach to remote screening programs. Intraoperative microscopy cameras, exemplified by 4K robotic systems for neurosurgery, are attracting neurosurgeons seeking stereoscopic depth. Dental and dermatology cameras hold niche positions, with AI-enhanced skin-lesion imaging poised for tele-dermatology expansion.

The shift toward single-use formats challenges established re-processing workflows in hospitals yet offers supply-chain efficiencies by removing sterilization equipment. Camera makers that bundle scopes, processors, and AI analytics into integrated kits are achieving higher recurring revenue per procedure. As capsule and disposable adoption rises, vendors must ensure secure data transmission and battery longevity to satisfy clinical reliability standards.

By Resolution: 4K/8K Systems Gain Momentum

High-definition remained the dominant resolution in 2025, capturing 48.21% revenue as legacy fleets continue to serve routine cases. Nevertheless, 4K/8K units are advancing at 8.34% CAGR, driven by surgeon preference for enhanced clarity and depth perception. The medical cameras market size for ultra-high-definition equipment is expanding fastest in ophthalmology and neurosurgery where sub-millimeter accuracy is critical. Hospitals upgrading to 4K realize workflow gains when larger displays permit team visualization without repeated positioning.

Upgrading, however, requires compatible recorders and network bandwidth to handle quadrupled data throughput. To ease transition, suppliers offer hybrid control units that auto-scale between HD and 4K feeds, preserving compatibility with existing monitors. Demonstrable gains in lesion detection and reduced operating-time metrics are accelerating procurement approvals, particularly when return-on-investment models document payback within four years.

By Sensor Technology: sCMOS Raises Performance Bar

CMOS arrays delivered cost leadership and 63.84% market share in 2025 as consumer-electronics capacity keeps unit prices low. sCMOS, with its sub-2-electron read noise and 25,000:1 dynamic range, is the fastest-growing category at 9.05% CAGR, excelling in low-light and fluorescence-guided surgery. Early adopters in oncology are pairing sCMOS with near-infrared fluorophores to distinguish tumor margins intraoperatively. Though component cost is higher, hospitals value image quality gains when procedures shorten and follow-up interventions decline.

CCD demand continues to wane because slower readout and higher power draw elevate heat generation, complicating sterilization. Vendors are phasing out CCD from new platforms, concentrating R&D on sCMOS packaging that withstands repeated autoclave cycles. Over the forecast window, sCMOS penetration is expected to approach 30% of total camera shipments as economies of scale improve.

By End User: ASC Growth Redefines Procurement

Hospitals controlled 54.21% of 2025 shipments thanks to multi-specialty usage and robust capital budgets. Still, ambulatory surgery centers are expanding case volumes at an 7.9% CAGR, propelled by payer incentives that favor outpatient settings for cost containment. The medical cameras market size allocated to ASCs is rising as these centers equip procedure rooms with lightweight, modular camera towers optimized for rapid turnover.

ASCs place a premium on infection-control disposable scopes and service contracts that guarantee uptime without on-site biomedical staff. Specialty clinics dermatology, ophthalmology, gastroenterology leverage dedicated cameras to expedite high-throughput diagnostic workflows. Meanwhile, mobile imaging services and veterinary hospitals form a nascent but growing customer base as miniaturized cameras reach sub-USD 1,000 price points.

Geography Analysis

North America remained the largest regional buyer with 34.85% revenue share in 2025 as hospitals upgraded to AI-ready 4K stacks and reimbursement supports minimally invasive surgery. The United States leads global procedure volumes, assisted by favorable billing codes and established surgeon preference for endoscopic interventions. Canada follows with province-level funding that prioritizes infection-control enhancements such as single-use imaging.

Asia-Pacific is expanding at a 9.78% CAGR, fuelled by public-sector investment in surgical infrastructure, rapid adoption of capsule endoscopy, and domestic manufacturing encouragement in China and India. China’s hospitals are retrofitting operating rooms to meet Tier-3 accreditation, often specifying 4K readiness in tenders. India’s MedTech incentive scheme is lowering import duties on optical components, improving affordability for secondary-tier facilities.

Europe posts steady demand as German and French hospitals transition to integrated operating rooms, though budget constraints temper replacement speed. Scandinavian countries are early adopters of wireless capsule cameras for colorectal screening, reflecting high tele-health penetration. In the Middle East, flagship medical cities in Saudi Arabia and the United Arab Emirates are specifying hybrid ORs with built-in 3D endoscopy suites, creating pockets of high-value demand. Latin America and Africa are smaller contributors but are witnessing procurement financed by multilateral development banks focused on infection-control upgrades.

Regulatory Landscape

Medical cameras used in endoscopy, surgical microscopy, dermatology, and connected imaging workflows are regulated as medical devices, with requirements covering electrical safety, quality systems, cybersecurity, and (increasingly) software and AI lifecycle controls. In the United States, products commonly use the FDA 510(k) pathway and quality system requirements under 21 CFR Part 820, while in Europe, market access is governed by the EU Medical Device Regulation (EU MDR 2017/745), with heightened expectations for clinical evidence and post-market obligations.

AI-enabled camera ecosystems face a tighter dual-compliance environment in Europe as the EU AI Act adds risk-based requirements alongside EU MDR conformity assessment, increasing the focus on transparency, robustness, and documentation. In the United States, FDA actions in 2024-2025 around imaging-related software classifications and guidance reinforce the direction toward clearer special controls and validation expectations for acquisition and optimization tools, expanding compliance attention from optics and sensors into algorithm performance management and post-market surveillance.

Competitive Landscape

The medical cameras market exhibits moderate consolidation: the top five vendors control significant global revenue. Olympus Corporation retains a leading installed base in flexible endoscopy, leveraging a broad consumables pipeline that anchors customer loyalty. Stryker Corporation is expanding into visualization + analytics platforms through acquisitions of Nico Corporation and Care.ai, embedding AI in surgical workflows. Sony Corporation is cross-pollinating consumer-imaging innovation into surgical robotics, debuting 8K 3D camera heads that interface with microscopes.

Carl Zeiss Meditec AG focuses on neuro- and ophthalmic microscopy where premium optics command high margins, while Fujifilm targets gastroenterology with AI-assisted lesion detection. Emerging companies pursue nano-camera chips smaller than 1 mm³ for vascular and pediatric applications. Competitive differentiation is shifting from sheer image resolution toward the breadth of AI apps, ergonomic design, and cybersecurity robustness. Patent filings on wireless video compression and edge-AI inference are climbing, signaling sustained innovation intensity.

Mergers and alliances revolve around filling software gaps or securing sensor supply. Camera makers are inking long-term wafer agreements with semiconductor fabs to insulate against supply disruptions first exposed. Service-as-a-subscription bundles that wrap hardware, software updates, and analytics dashboards are gaining traction, aligning vendor revenue with procedure growth.

Medical Cameras Industry Leaders

Canfield Scientific, Inc.

Olympus Corporation

Richard Wolf GmbH

Stryker Corporation

Carestream Dental LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Platform upgrades that standardize visualization across operating rooms and procedure suites remain a visible whitespace as providers move away from mixed HD components toward integrated stacks that support 4K/3D and fluorescence-guided surgery. Olympus Corporation’s March 2026 U.S. launch of the VISERA ELITE III surgical imaging platform is a concrete signal of that shift, as it packages 4K, 3D, and IR/ICG fluorescence capabilities for multispecialty use, consistent with hospitals pursuing hybrid operating rooms and integrated imaging workflows.

Interoperability and color-fidelity needs also open an opportunity for camera vendors that offer standards-ready connectivity and consistent image reproduction across sites, including outpatient and telemedicine-linked workflows. The publication of ISO 12052:2026 (DICOM) supports standardized image and metadata exchange across medical disciplines, while ITU-T Recommendation F.780.6 (2025) addresses UHD telemedicine color and measurement methods, shaping procurement criteria that favor systems built for data exchange, documentation, and reproducible imaging performance rather than standalone camera heads.

Recent Industry Developments

- March 2026: Olympus Corporation launched the VISERA ELITE III surgical imaging platform in the United States, adding 4K, 3D, and fluorescence-guided surgery capabilities. The launch supports multispecialty standardization strategies in operating rooms where hospitals are consolidating visualization stacks and prioritizing upgradeable ecosystems.

- September 2025: Olympus announced the U.S. launch of its newest imaging platform for ENT and urological procedures. The introduction broadened Olympus's visualization footprint beyond core GI endoscopy and reinforced competitive focus on procedure-specific imaging workflows that can be bundled with scopes and service.

- August 2024: Richard Wolf GmbH partnered with Photocure to develop a new flexible, reusable cystoscope designed for photodynamic diagnostics (PDD) in bladder cancer screening and surveillance. The collaboration links camera-enabled cystoscopy hardware with a targeted clinical application, expanding differentiation around imaging modes and disease-focused pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the medical cameras market covers camera systems used to capture still images or video for clinical diagnosis, surgery, and procedure guidance, along with their core camera heads, control units, and essential imaging accessories.

Scope exclusions: We exclude general consumer cameras and non-medical imaging devices that are not designed, certified, and sold for clinical use.

Segmentation Overview

- By Product Type

- Dental Cameras

- Dermatology Cameras

- Endoscopy Cameras

- Ophthalmology Cameras

- Surgical Microscopy Cameras

- Capsule & Disposable Endoscopic Cameras

- Other Cameras

- By Resolution

- Standard-Definition Cameras

- High-Definition Cameras

- Ultra-High-Definition (4K/8K) Cameras

- By Sensor Technology

- CCD

- CMOS

- sCMOS

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgery Centers

- Diagnostic Imaging Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with understanding how medical cameras move through healthcare systems, and what drives replacement, upgrades, and new installations. We used public, non-paywalled sources such as the US FDA device databases and safety notices, Centers for Medicare and Medicaid Services references for procedure volumes and care settings, World Health Organization health indicators, and OECD health statistics for hospital capacity and utilization signals.

Next, the inputs were sharpened using public company filings, investor presentations, hospital procurement disclosures, association publications, and reputed press to map typical price bands and adoption timing. In parallel, our analysts used paid subscriptions for company financials and intelligence, a patent database to track imaging-related innovation activity, and an import-export shipment-level database where trade flows helped validate supply availability. The sources listed here are illustrative, and we also reviewed other public documents for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what desk sources cannot show clearly, mainly the mix of camera types used in endoscopy, microscopy, ophthalmology, and dental workflows, plus how budgets and upgrade cycles are changing. We spoke with manufacturers and channel partners, along with hospital and clinic stakeholders involved in clinical engineering, procurement, and specialty departments, to validate price ranges, installed base behavior, and the pace of technology shifts across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 47% |

| Mid tier: 57% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 14% | Managers: 48% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that reconstructs demand from procedure volumes and care setting capacity, and then applies realistic camera-per-room and camera-per-suite intensity levels by specialty. Once that demand pool is constructed, average selling prices are applied using price bands that reflect typical configurations (including camera head, control unit, and required accessories) and regional procurement patterns.

To keep the totals practical, we corroborate the result with selective bottom-up approximations, such as sampled supplier revenues for medical camera lines, channel feedback on unit shipments, and a simple ASP multiplied by volume check for a few high-visibility camera categories. Key inputs that steer the model include endoscopy and minimally invasive surgery volumes, ophthalmic exam and retinal screening activity, operating room and endoscopy suite counts, replacement and service life cycles, and observed ASP movement tied to sensor shifts and resolution upgrades.

For forecasting, scenario analysis is used so the model can handle different adoption speeds in ambulatory settings and different hospital capex conditions. These scenarios are then anchored back to primary feedback on procurement timing, lead times, and expected upgrade triggers, and gaps in bottom-up checks are handled by conservative ranges that are narrowed after follow-up calls where variance is high.

Data Validation & Update Cycle

Results are validated through triangulation across independent signals, including procedure trends, facility capacity growth, and typical replacement timing shared by interviewees. If a region or specialty shows an unusual jump, the assumptions are rechecked first, and then the underlying inputs are revisited for unit intensity, price bands, or timing issues.

Before sign-off, the model goes through multi-step analyst review so calculations, conversions, and scope boundaries are consistently applied. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, supply disruptions, or sharp pricing moves. Right before delivery, a final pass is done so clients receive the most current view based on newly available public information and any necessary re-contacts.

Mordor Intelligence's Medical Cameras Market Size Versus Other Published Estimates

Published market sizes for medical cameras often vary, and the differences usually come from what is counted as a medical camera system, which year is treated as the base, and how prices are handled when product mixes are changing.

Procedure volume trends in endoscopy and surgery, along with cross-checks against facility capacity and replacement cycles, are used to keep Mordor Intelligence's estimate anchored to an addressable demand pool rather than broad imaging spend assumptions. Gaps typically show up when adjacent devices are included, when aggressive adoption is assumed in ambulatory settings without checks, or when currency timing and inflation treatment are not stated clearly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.65 B (2025) | |

| Global Consultancy A | USD 4.44 B (2025) | This figure appears to sit on a wider product and application boundary, and it may count broader imaging camera categories beyond clinical procedure cameras, which lifts the 2025 value. |

| Trade Journal B | USD 3.40 B (2024) | This estimate is anchored to 2024 and can read lower because it reflects an earlier pricing mix, and it may treat upgrades and accessory content more lightly in the average system value. |

The comparison shows that the spread is mainly explained by boundary choices and base-year timing, not by a single growth disagreement. By keeping inputs traceable to procedure demand, care setting capacity, and realistic price bands, the final number stays repeatable and easier to reconcile when new data arrives.

Key Questions Answered in the Report

What is the current size of the Medical Cameras Market?

The Medical Cameras Market size is USD 3.9 billion in 2026, with revenue projected to reach USD 5.43 billion by 2031.

Which camera type holds the largest market share today?

Endoscopy cameras contribute 34.72% of global revenue, making them the leading product category.

Why are 4K and 8K medical cameras growing so fast?

Surgeons report clearer visualization, higher lesion-detection rates, and shorter operating times, resulting in an 8.34% CAGR for 4K/8K systems.

Which region is expanding the quickest?

Asia-Pacific is forecast to grow at a 9.78% CAGR to 2031, driven by infrastructure investments and increasing procedure volumes.

How is artificial intelligence changing medical camera usage?

AI algorithms embedded in new cameras provide real-time lesion detection and tissue classification, elevating diagnostic accuracy and standardizing surgical outcomes.

What challenges could slow market growth?

High capital costs, lengthy regulatory approvals, cybersecurity vulnerabilities, and semiconductor supply disruptions could moderate adoption rates over the next two years.

Page last updated on: