Medical Cyclotron Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

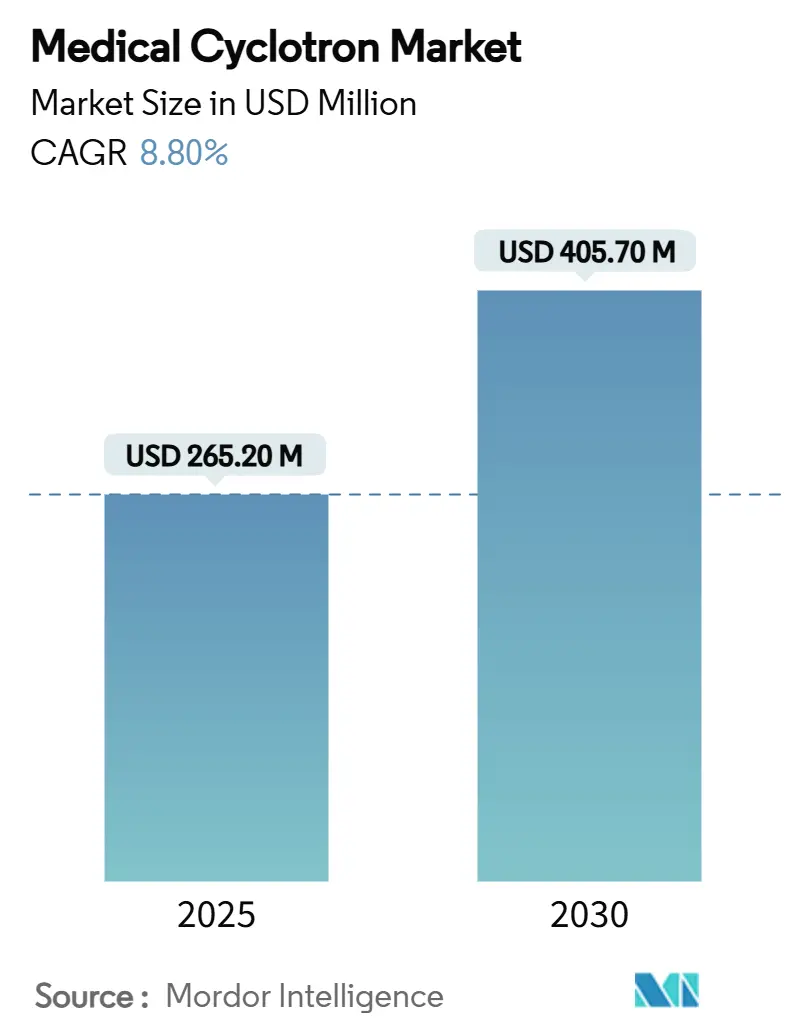

| Market Size (2025) | USD 265.20 Million |

| Market Size (2030) | USD 405.70 Million |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

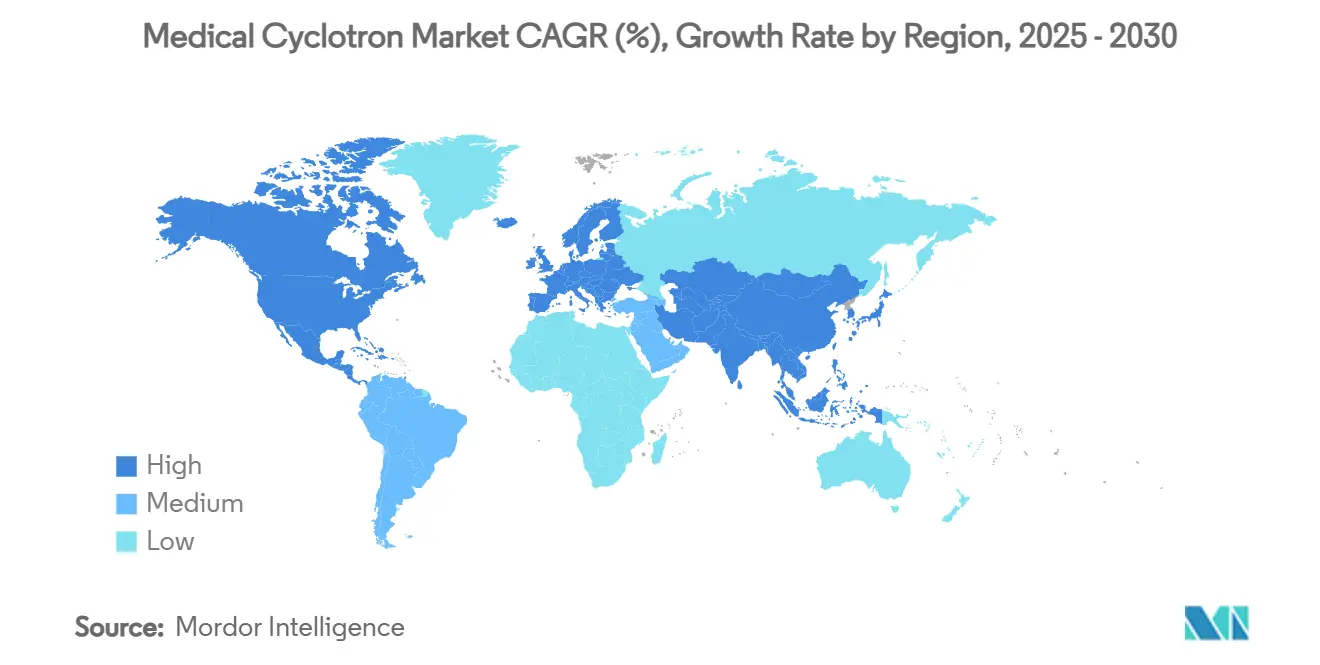

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

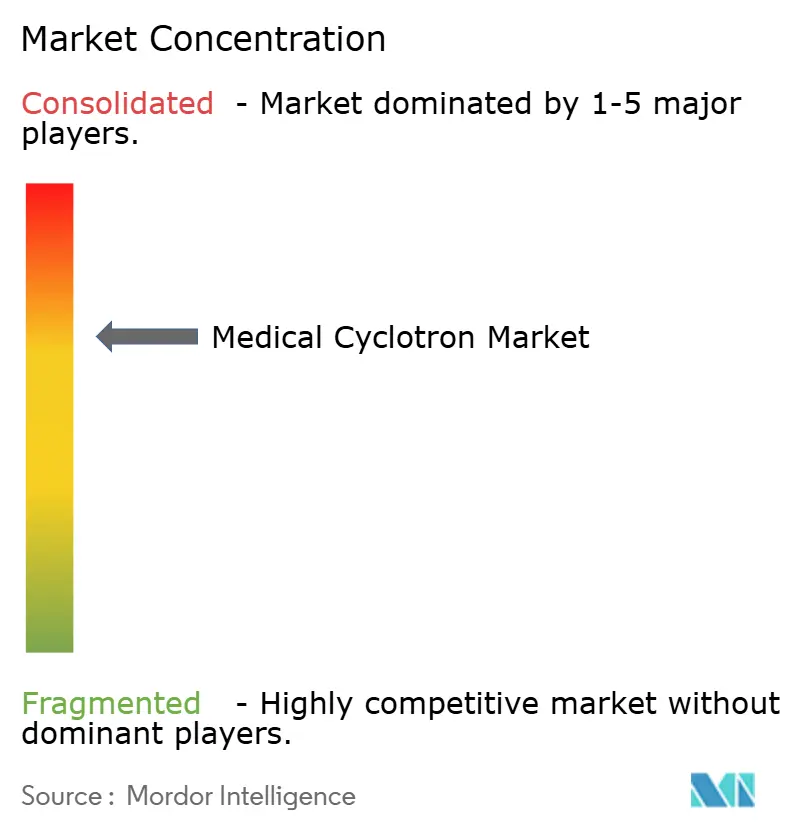

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Cyclotron Market Analysis by Mordor Intelligence

The medical cyclotron market size stood at USD 265.2 million in 2025 and is forecast to reach USD 405.7 million by 2030, expanding to an 8.8% CAGR. Demand is underpinned by rising cancer prevalence, broader adoption of precision medicine, and the growing need for on-site production of short-lived radioisotopes that support both diagnostic and therapeutic applications. Medium-energy cyclotrons remain a workhorse segment because they efficiently generate core PET tracers such as fluorine-18, while very-high-energy systems are gaining traction as hospitals and contract manufacturers pivot toward alpha- and beta-emitting isotopes for targeted radiotherapy. Established vendors are responding with more compact, GMP-compliant machines that lower site-prep costs and automate quality control. Government funding programs across North America, Europe, and Asia Pacific are also sustaining purchase pipelines, although there is a persistent shortage of trained radiochemists and operators tempers installation rates in some regions.

Key Report Takeaways

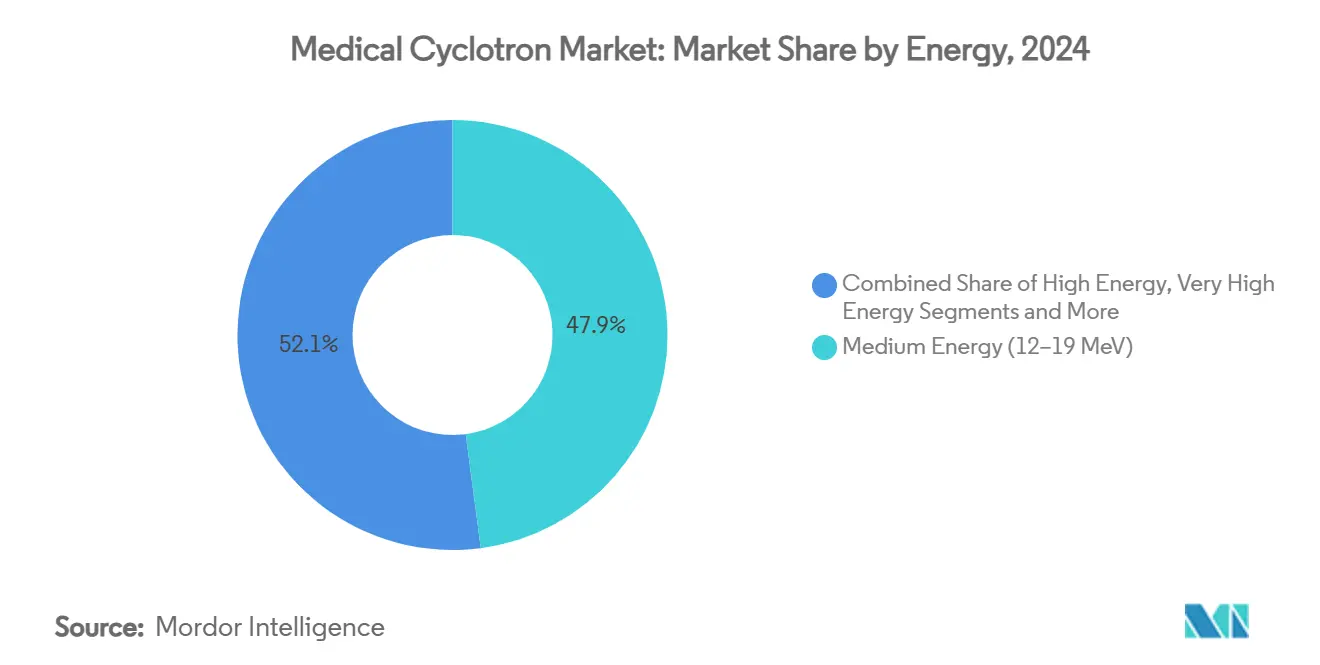

- By energy, medium energy systems held 47.9% of medical cyclotron market share in 2024; very-high-energy cyclotrons are projected to post the fastest 12.4% CAGR through 2030.

- By application, diagnostic imaging accounted for 83.1% revenue share in 2024, whereas therapeutic isotope production is forecast to advance at a 15.1% CAGR to 2030.

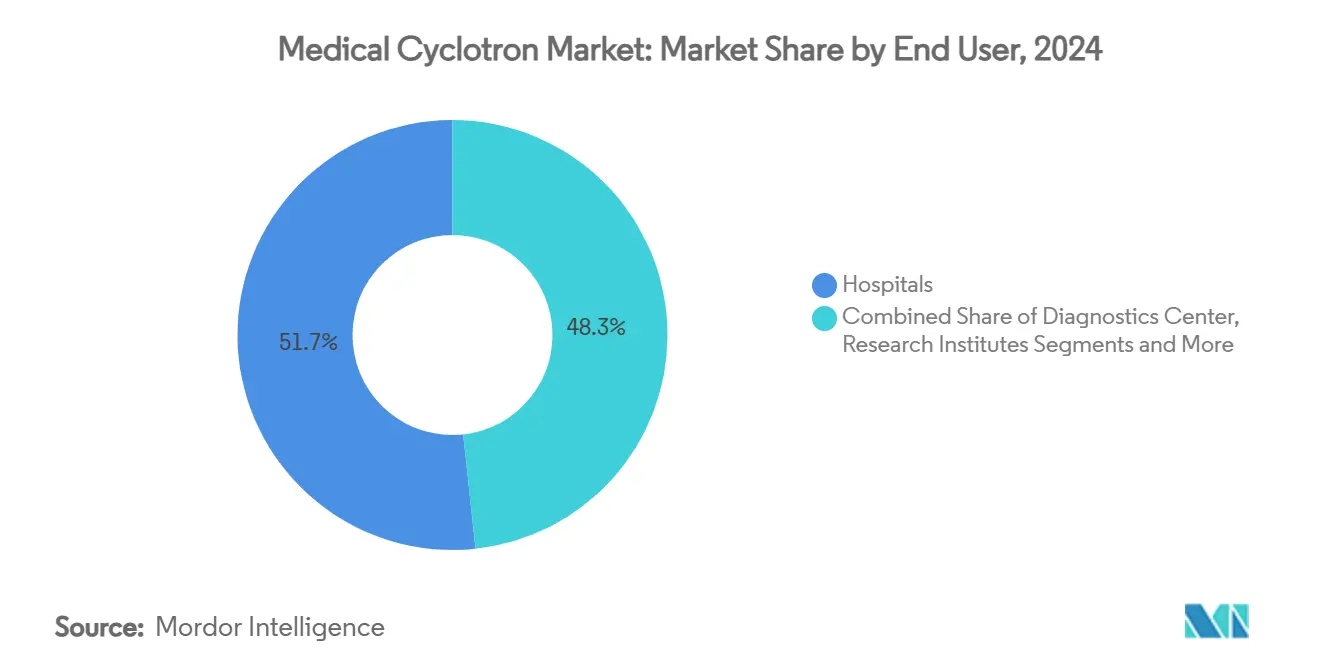

- By end user, hospitals commanded 51.7% share of the medical cyclotron market size in 2024, while pharmaceutical & CDMOs are set to grow at 14.3% CAGR over the outlook period.

- By geography, North America led with 34.8% market share in 2024; Asia Pacific is expected to register the quickest 9.3% CAGR through 2030.

Global Medical Cyclotron Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Of PET Imaging In Oncology | +2.10% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Government Funding For Nuclear Medicine Infrastructure | +1.80% | Asia Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Rapid Expansion Of GMP-Compliant Compact Cyclotrons | +1.50% | Global, with early gains in North America & EU | Short term (≤ 2 years) |

| Shift Toward Theranostic Radio-Isotopes (Alpha & Beta Emitters) | +2.30% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| On-Site Production To Mitigate Global Mo-99 Supply Risk | +1.20% | Global, particularly North America | Short term (≤ 2 years) |

| Rising Collaborations Between Cyclotron Vendors & Pharma CDMOs | +1.60% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of PET Imaging in Oncology

PET is now embedded in mainstream oncology pathways, and the FDA approval of flurpiridaz F-18 in 2024 illustrates the trend toward tracers with half-lives long enough for regional distribution as per the Society of Nuclear Medicine and Molecular Imaging. Health systems value PET’s superior sensitivity, especially for high-BMI patients, which reinforces orders for medium energy cyclotrons that make fluorine-18 and gallium-68. Precision oncology protocols require broader tracer portfolios, nudging sites toward higher-energy machines capable of copper-64 production. As reimbursement rules favor early, accurate diagnoses, procedure volumes keep rising and strengthen the investment case for on-site cyclotrons. Vendor service models that guarantee uptime further de-risk ownership for hospitals.[1]Society of Nuclear Medicine and Molecular Imaging, “FDA Approves Flurpiridaz F-18 for CAD Imaging,” snmmi.org

Government Funding for Nuclear Medicine Infrastructure

Large public programs are anchoring demand in both mature and emerging economies. Canada’s USD 35 million Canadian Medical Isotope Ecosystem targets domestic isotope self-sufficiency. Bolivia’s USD 300 million nuclear research complex exemplifies a similar push in developing markets. The U.S. Department of Energy requested USD 183.9 million for isotope production in FY 2025, with Brookhaven slated for cyclotron upgrades.[2]U.S. Department of Energy, “FY 2025 Congressional Budget Request for Isotope Production and Distribution Program,” energy.gov Funds typically cover buildings, shielding, training, and regulatory support, which lowers entry barriers for hospitals. Regional hub strategies further optimize capital by serving multiple institutions from one facility.

Rapid Expansion of GMP-Compliant Compact Cyclotrons

Next-generation compact cyclotrons combine superconducting magnets, automated target handling, and self-shielded vaults. IBA’s Cyclone KIUBE 180 roll-out with Jubilant Radiopharma, involving five U.S. installations for USD 50 million, signals strong appetite for distributed networks. Smaller footprints reduce site construction costs and fit urban hospitals with limited space. Built-in quality modules align with FDA and EU GMP guidelines, minimizing manual interventions and mitigating personnel shortages. Modular designs also let owners add targets as throughput grows, keeping initial spending manageable. Early adopters report faster time-to-revenue because commissioning timelines are shorter than those for legacy vault systems.

Shift Toward Theranostic Radio-Isotopes (Alpha & Beta Emitters)

Theranostics combine diagnostic scans and therapy within a single patient workflow, driving demand for high-energy, high-current cyclotrons. Lutetium-177 agents such as Pluvicto and Lutathera proved survival benefits in prostate and neuroendocrine tumors, stimulating hospital interest in co-located therapeutic isotope lines. Actinium-225 programs are also scaling, with Actinium Pharmaceuticals advancing proprietary cyclotron production technology. High-current machines like IsoDAR can deliver 5 mA H2+ beams, producing enough activity to serve national therapy markets. As regulatory approvals expand, sites that run both imaging and therapy see improved asset utilization and better return on invested capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operational Costs | -1.90% | Global, particularly in developing markets | Long term (≥ 4 years) |

| Complex Multi-Agency Licensing Requirements | -1.40% | Global, with varying intensity by region | Medium term (2-4 years) |

| Shortage Of Qualified Radiochemists & Operators | -1.20% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| Helium Supply Volatility Raising Operating Costs | -0.80% | Global, with concentration in regions dependent on helium imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Operational Costs

Purchasing a cyclotron entails USD 2.5–6.6 million for the accelerator and another outlay for shielding, HVAC, and hot-lab build-outs, often doubling the project budget. Annual running costs can reach USD 1.9 million, with wages making up two-thirds of expenses. Break-even volumes hinge on reimbursement rates, which vary widely across markets. Spare-parts contracts and helium for cooling add to the bill; recent helium price spikes raise operating risk in import-dependent regions. These economics can delay procurement in lower-income countries unless supported by public grants or multilateral loans.

Complex Multi-Agency Licensing Requirements

Cyclotron sites must satisfy pharmaceutical GMP rules, radiation safety laws, and often separate state or provincial codes. In the United States, NRC amendments simplified some processes in 2024, yet facilities still need detailed safety analysis reports and periodic inspections.[3]U.S. Nuclear Regulatory Commission, “Amendments to 10 CFR Part 50 for Non-Power Accelerators,” nrc.gov The FDA’s stability testing rule for PET drugs is projected to add USD 3 million in annual compliance costs per site, as per the Society of Nuclear Medicine and Molecular Imaging. Europe lacks harmonized small-scale radiopharmaceutical guidelines, which forces operators to navigate divergent national rules and complicates cross-border supply. This regulatory patchwork discourages smaller hospitals from entering the medical cyclotron market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Energy: Medium Systems Dominate While High-Energy Lines Accelerate

Medium energy cyclotrons captured 47.9% of the medical cyclotron market share in 2024, producing routine PET isotopes that underpin day-to-day imaging volumes. Their proven workflows, moderate shielding needs, and established regulatory pathways make them the default choice for many hospitals. Capital payback is achievable within five years when centers run high-throughput FDG programs. Low-energy models serve niche cardiac and neurology tracers, whereas 20–30 MeV machines appeal to academic labs that require broader isotope menus.

Very-high-energy systems above 30 MeV are expected to post a 12.4% CAGR, the quickest among energy classes, as targeted radiotherapy demand ramps up. The arrival of a 230-tonne unit at Argentina’s Proton Therapy Centre shows hospitals’ willingness to invest in multipurpose high-current equipment. MIT’s latest 60 MeV, 5 mA H2+ prototypes highlight the engineering push toward compact superconducting models that fit urban campuses. As production economics improve, these units will support decentralized actinium-225 and lutetium-177 supply chains and strengthen the medical cyclotron market.

By Application: Imaging Remains Anchor as Therapy Gains Momentum

Diagnostic imaging dominated the medical cyclotron market size with an 83.1% revenue contribution in 2024, thanks to entrenched PET/CT procedures in oncology, neurology, and cardiology. Fluorine-18 FDG continues to account for most scans, and Bangladesh’s NINMAS facility illustrates how a single medium-energy machine can supply more than 100 regional FDG batches annually, according to the Bangladesh Journal of Nuclear Medicine. Reimbursement stability and mature logistics networks keep imaging volumes steady, preserving medium energy cyclotron demand.

Therapeutic isotope production is set for a 15.1% CAGR through 2030, fueled by regulatory endorsements for beta and alpha emitters. Telix Pharma’s USD 82.5 million acquisition of ARTMS underscores corporate bets on distributed lutetium-177 manufacturing. Higher-energy cyclotrons paired with automated radiochemistry modules shorten end-to-end lead times and ensure GMP compliance. As new therapies secure coverage, the therapy segment will account for a rising slice of the medical cyclotron market size.

By End User: Hospitals Lead While CDMOs Expand

Hospitals held 51.7% of the medical cyclotron market size in 2024 by leveraging on-site production to reduce radiotracer decay losses and align scan schedules with patient workflows. The ARRONAX hospital radiopharmacy shows how clinical centers now support early-phase trials with internally produced agents. Integrated service contracts from vendors further simplify lifecycle management.

Pharmaceutical companies and CDMOs are forecast to grow at 14.3% CAGR as biopharma firms outsource both imaging and therapy isotope production. Partnerships such as IBA–Jubilant indicate a shift toward nationwide PET networks that guarantee same-day deliveries. University and research institutes retain a specialized role in method development, reinforcing innovation within the medical cyclotron industry.

Geography Analysis

North America retained 34.8% of the medical cyclotron market in 2024, supported by advanced reimbursement policies and a robust installed base. Canada’s TRIUMF operates multiple units and supplies 15% of the nation’s isotopes, displaying the region’s commitment to domestic capacity. CMS reimbursement reforms that cover tracers priced above USD 630 enhance site economics and encourage replacement sales. Mexico’s first ABT BG-75 self-shielded cyclotron also widened North American access to PET services.

Europe counted more than 348 operational cyclotrons by 2024, underpinning a well-distributed supply grid. D-A-CH nations operate 42 units, mainly within university campuses, and collaborate with industry for commercial output. The Institute for Radioelements’ new 30 MeV line in Belgium highlights regional capacity upgrades aimed at germanium-68 generators for gallium-68 PET agents. Yet differing GMP interpretations across member states still lengthen project timelines.

Asia Pacific is projected to register the fastest 9.3% CAGR by 2030. China already runs more than 120 cyclotrons and has a national plan to double its isotope services by 2035. India counts 24 medical cyclotrons and leverages international partnerships to expand access. Bangladesh and the Philippines have recently commissioned their first medium-energy machines, demonstrating how governmental cancer agendas are boosting the medical cyclotron market in emerging economies.

Competitive Landscape

The medical cyclotron market is moderately consolidated. IBA, GE Healthcare, and Siemens Healthineers anchor the field, bundling accelerators, targets, and maintenance into turnkey propositions. IBA posted EUR 498.2 million revenue in 2024, with its Other Accelerators business up 18%. Siemens Healthineers’ PETNET delivers 1.4 million doses annually from its cyclotron network, ensuring same-day radiotracer supply to 2,800 sites.

New entrants focus on specialty isotopes. Actinium Pharmaceuticals is scaling proprietary actinium-225 production backed by 54 patents, positioning itself for alpha-therapy expansion. IsoDAR’s high-current concept illustrates how beam innovations can lower the cost-per-curie for therapeutic nuclides. Service-heavy models that handle regulatory filings and staffing are becoming a key differentiator as operator shortages persist. Acquisitions such as Lantheus–Life Molecular Imaging and Telix–ARTMS show incumbents expanding portfolios to cover diagnostics and therapy in a single platform.

Medical Cyclotron Industry Leaders

-

Ion Beam Applications SA (IBA)

-

GE Healthcare Technologies Inc.

-

Siemens Healthineers AG

-

Sumitomo Heavy Industries, Ltd.

-

Advanced Cyclotron Systems Inc. (ACSI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lantheus Holdings agreed to acquire Life Molecular Imaging for up to USD 750 million to broaden its PET tracer pipeline.

- December 2024: Institute for Radioelements installed a 30 MeV IBA cyclotron in Belgium to scale germanium-68 output.

- November 2024: Oklo Inc. announced plans to acquire Atomic Alchemy to enter the isotope market using fast-reactor tech.

- October 2024: IBA sold five Cyclone KIUBE 180 units to Jubilant Radiopharma for USD 50 million, expanding U.S. PET capacity.

Global Medical Cyclotron Market Report Scope

| Low Energy (<12 MeV) |

| Medium Energy (12–19 MeV) |

| High Energy (20–30 MeV) |

| Very High Energy (>30 MeV) |

| Diagnostic Imaging | Positron Emission Tomography (PET) |

| Single Photon Emission CT (SPECT) | |

| Therapeutic Isotope Production | Beta Emitters (e.g., Lu-177) |

| Alpha Emitters (e.g., Ac-225) |

| Hospitals |

| Diagnostic Imaging Centers |

| Research Institutes & Universities |

| Pharmaceutical & CMOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Energy | Low Energy (<12 MeV) | |

| Medium Energy (12–19 MeV) | ||

| High Energy (20–30 MeV) | ||

| Very High Energy (>30 MeV) | ||

| By Application | Diagnostic Imaging | Positron Emission Tomography (PET) |

| Single Photon Emission CT (SPECT) | ||

| Therapeutic Isotope Production | Beta Emitters (e.g., Lu-177) | |

| Alpha Emitters (e.g., Ac-225) | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Research Institutes & Universities | ||

| Pharmaceutical & CMOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical cyclotron market?

The medical cyclotron market size reached USD 265.2 million in 2025 and is projected to climb to USD 405 million by 2030.

Which energy class of cyclotrons holds the largest market share?

Medium energy cyclotrons (12–19 MeV) led with 47.9% market share in 2024 because they efficiently produce core PET tracers such as fluorine-18.

Why are very-high-energy cyclotrons (>30 MeV) growing faster than other segments?

Hospitals and contract manufacturers need higher-energy machines to generate therapeutic isotopes like actinium-225 and lutetium-177, driving a 12.4% CAGR through 2030.

Which geographic region is expanding the quickest?

Asia Pacific is expected to log the fastest 9.3% CAGR to 2030, propelled by increased healthcare access, government funding, and rising cancer incidence.

What is the biggest operational challenge facing new cyclotron facilities?

High capital and running costs—often topping USD 2.5 million for the machine plus matching infrastructure—combined with a shortage of qualified radiochemists and operators.

How concentrated is the competitive landscape?

The market concentration score is 6, indicating the top five vendors control roughly 60% of global revenue while niche producers keep emerging.

Page last updated on: