Cystatin C Assay Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 430.67 Million |

| Market Size (2030) | USD 619.58 Million |

| Growth Rate (2025 - 2030) | 7.55% CAGR |

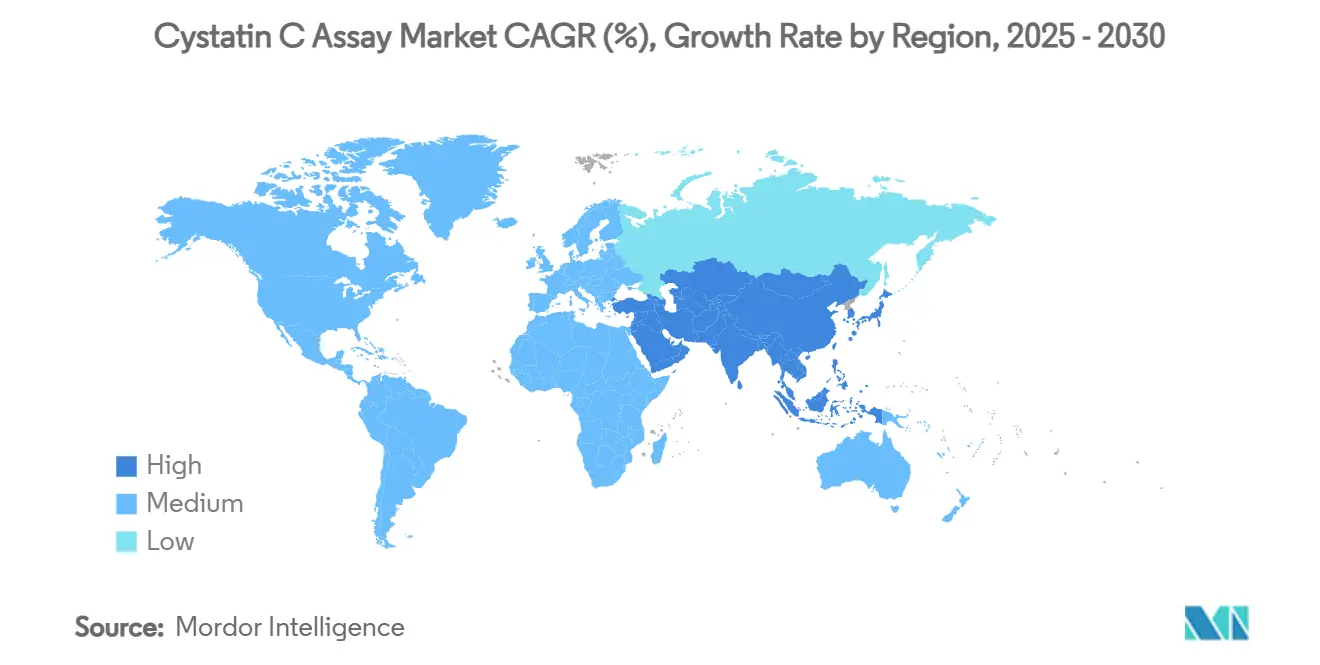

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

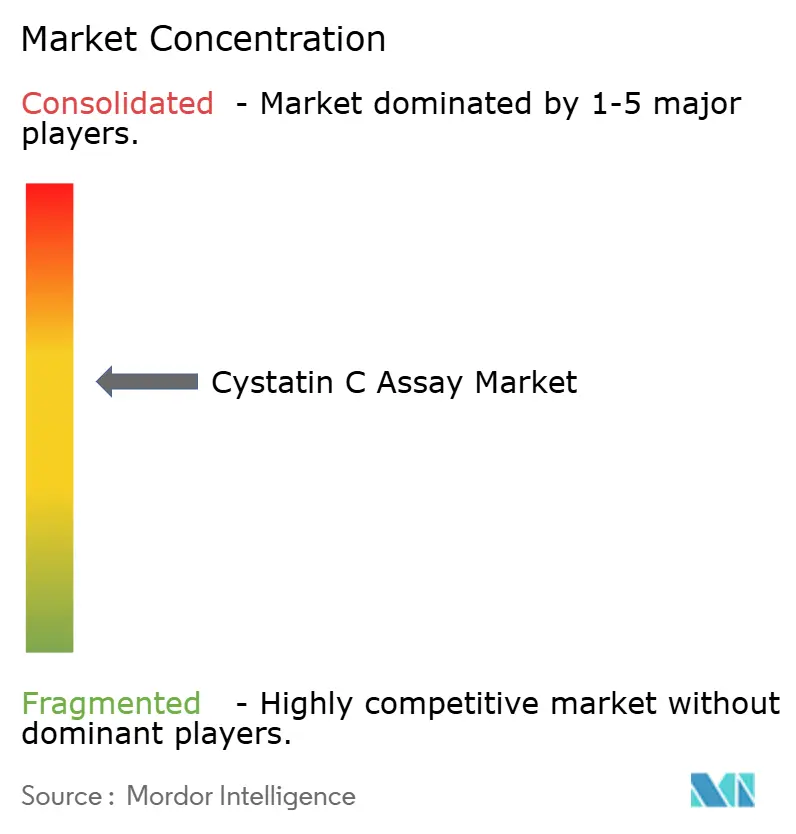

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cystatin C Assay Market Analysis by Mordor Intelligence

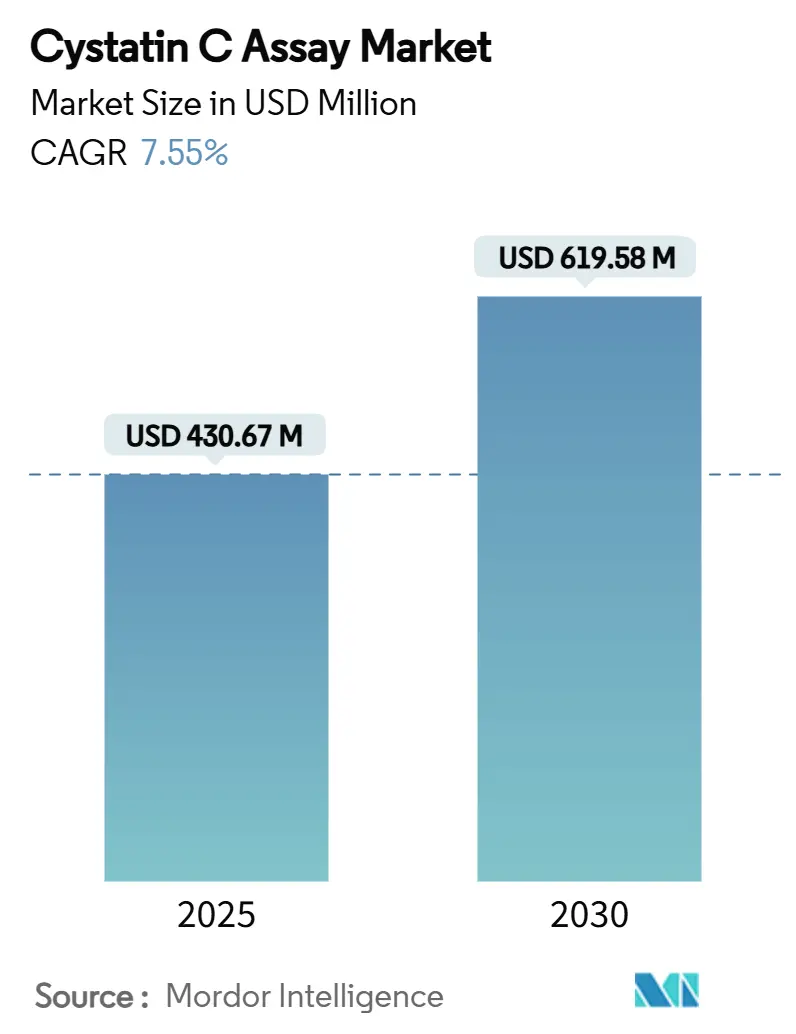

In 2025, the Cystatin C assay market size reached USD 430.67 million and is forecast to advance to USD 619.58 million by 2030, translating into a 7.55% CAGR over the period under review. Growing clinical confidence that Cystatin C offers a more precise estimate of glomerular filtration rate than creatinine in numerous patient groups, combined with the 2024 KDIGO guideline that now recommends routine dual-marker testing, sets a clear direction for laboratories worldwide.[1]Kidney Disease: Improving Global Outcomes, “KDIGO 2024 Clinical Practice Guideline for the Evaluation and Management of Chronic Kidney Disease,” kdigo.org Rising chronic kidney disease (CKD) prevalence, surging diabetes incidence, and aging demographics collectively enlarge the pool of individuals who require accurate kidney function checks, while emergency departments increasingly rely on Cystatin C to detect acute kidney injury (AKI) 6-48 hours ahead of creatinine readings. Diagnostic manufacturers respond by integrating high-throughput immunoturbidimetric assays and point-of-care cartridges into existing analyzers, thereby reducing turnaround time and supporting workflow automation. Together, these demand and technology factors keep the Cystatin C assay market on a firmly upward trajectory.

Key Report Takeaways

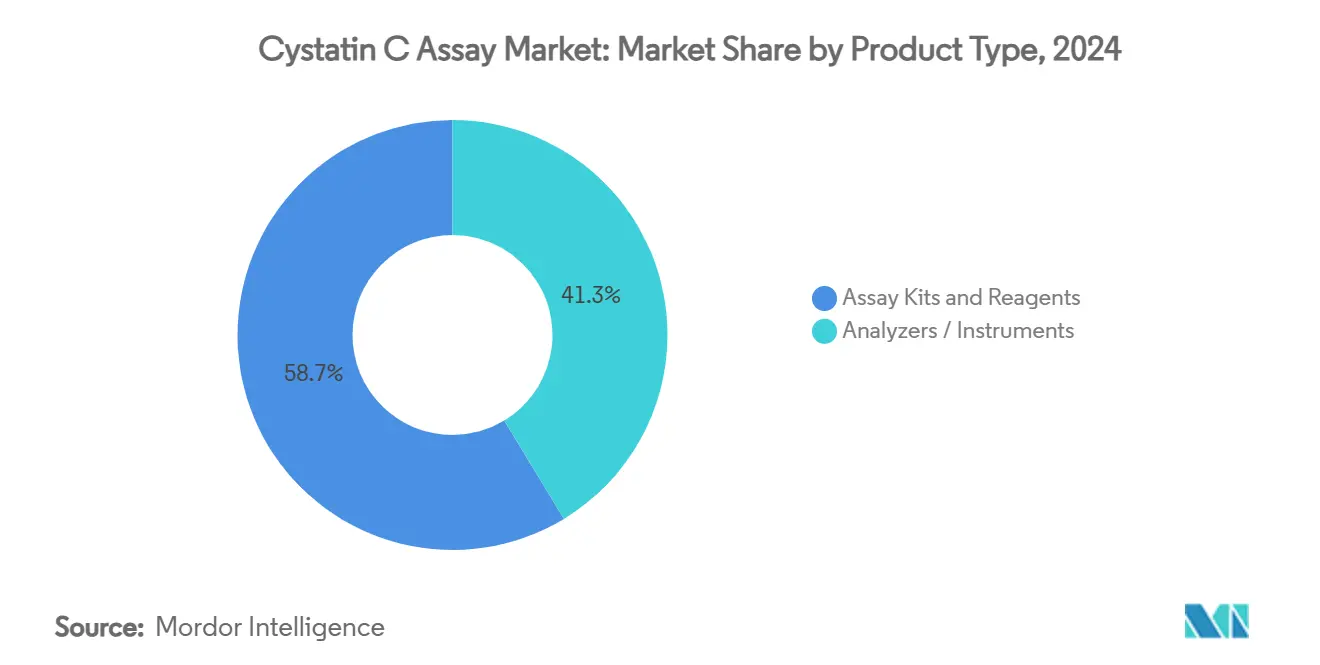

- By product type, assay kits and reagents captured 58.67% of the Cystatin C assay market share in 2024, while analyzers and instruments are projected to post the fastest 9.36% CAGR through 2030.

- By methodology, immunoturbidimetric assays commanded 46.23% of the Cystatin C assay market size in 2024, whereas ELISA and other emerging formats lead growth with a 10.23% CAGR over the forecast.

- By sample type, serum and plasma testing accounted for 82.36% share of the Cystatin C assay market size in 2024, and urine-based assays exhibit the highest 11.71% CAGR outlook to 2030.

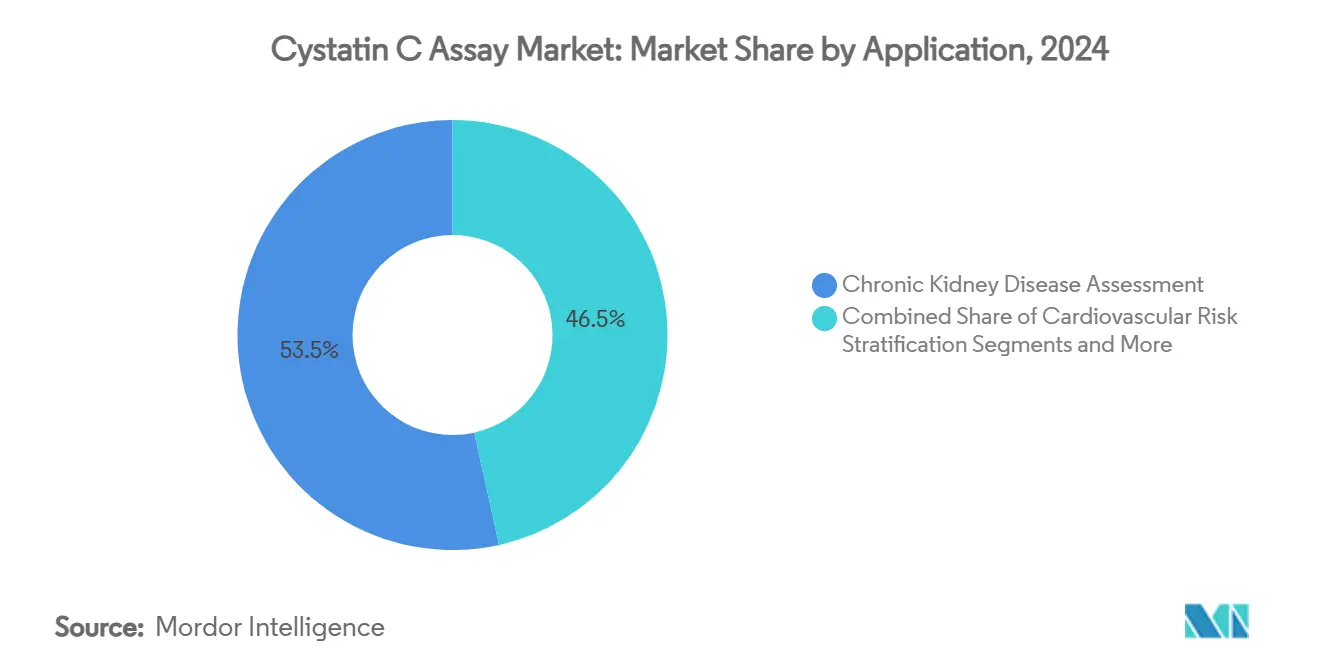

- By application, chronic kidney disease assessment represented 53.47% of the Cystatin C assay market size in 2024, but acute kidney injury detection advances at a 9.79% CAGR as the fastest-growing application.

- By end user, hospital laboratories held 51.28% share of the Cystatin C assay market size in 2024, while academic and research institutes are expected to expand quickest with a 9.47% CAGR to 2030.

- By geography, North America led with 31.26% of the Cystatin C assay market share in 2024, whereas Asia-Pacific is projected to deliver the highest 10.14% CAGR during the forecast period.

Global Cystatin C Assay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CKD prevalence worldwide | +1.8% | Global, highest in APAC and MEA | Long term (≥ 4 years) |

| Guideline endorsements for Cystatin C-based eGFR | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Superior accuracy in pediatrics & geriatrics | +1.2% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Growing use in acute kidney injury detection | +1.4% | Global, led by North America and EU | Short term (≤ 2 years) |

| Multi-analyte cardiovascular risk panels | +0.9% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Monitoring nephrotoxicity in oncology care | +0.7% | Global, concentrated in oncology centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising CKD Prevalence Worldwide

Chronic kidney disease has climbed the global mortality rankings, with the latest burden-of-disease analysis underscoring a steady rise in incident cases since 2024.[2]Levi Hooper et al., “The Kinetics of Cystatin C and Serum Creatinine in AKI,” Clinical Journal of the American Society of Nephrology, cjasn.asnonline.orgTraditional creatinine measurements often miss early dysfunction, so clinicians now view Cystatin C as a practical avenue for earlier identification and risk stratification. Diabetes remains the leading CKD driver, and high-risk diabetic cohorts show hazard ratios above 3.4 when serum Cystatin C trajectories accelerate.[3]Nana Wang et al., “Serum Cystatin C Trajectory Is a Marker Associated With Diabetic Kidney Disease,” Frontiers in Endocrinology, frontiersin.org Low- and middle-income countries feel the financial strain of dialysis, prompting health ministries to prioritize affordable biomarkers that might postpone renal replacement therapy. The demographic wave of older adults in developed economies keeps test volumes high, while lifestyle shifts in emerging markets feed incremental demand. Consequently, CKD epidemiology adds consistent momentum to the Cystatin C assay market.

Guideline Endorsements for Cystatin C-Based eGFR

Publication of the 2024 KDIGO guideline represents a pivotal regulatory nod; it now recommends combined creatinine-Cystatin C eGFR equations wherever Cystatin C testing is available. Because KDIGO recommendations inform protocols in roughly 180 nations, hospital labs in North America and Europe quickly updated chemistry panels, and Asia-Pacific nephrology societies are following suit. The document pinpoints frail patients, individuals with abnormal muscle mass, and those requiring drug-dosing precision as key beneficiaries of dual-marker models. By clarifying analytical performance targets, the guideline propels investments in standardization materials and calibrators. Coupled with laboratory automation, this endorsement widens the installed base of Cystatin C-capable analyzers, advancing the Cystatin C assay market.

Superior Accuracy in Pediatrics & Geriatrics

Children and seniors share a diagnostic blind spot: fluctuating or diminished muscle mass skews creatinine-based eGFR. Peer-reviewed studies confirm that serum Cystatin C provides reliable kidney function readings across pediatric age bands irrespective of growth stage or gender. In geriatric clinics, the marker mitigates under-recognition of CKD that stems from sarcopenia-related creatinine suppression, though some academics caution about potential over-diagnosis when Cystatin C increases alone are interpreted without measured GFR confirmation. Surgical teams employ Cystatin C for pre-operative assessments to fine-tune anesthesia plans and contrast dosing. Transplant centers likewise rely on the biomarker to monitor graft function, recognizing its independence from muscle catabolism. This broad clinical relevance elevates demand among age-extreme cohorts, reinforcing revenue for the Cystatin C assay market.

Growing Use in Acute Kidney Injury Detection

Emergency physicians value time; detecting AKI nearly two days sooner than creatinine translates to quicker fluid resuscitation and nephrotoxin avoidance. Prospective trials in critical care reveal that pairing NT-proBNP with Cystatin C achieves an AUC of 0.859, comfortably outperforming single-analyte approaches. Cardiologists exploit the marker when managing contrast-induced nephropathy risk, particularly during percutaneous interventions. Oncologists use Cystatin C to distinguish true renal injury from creatinine bumps caused by CDK4/6 inhibitors, thereby avoiding unnecessary chemotherapy delays. Hospitals integrating Cystatin C into electronic order sets report shorter diagnostic timelines and lower rates of dialysis initiation. Such outcome data fuel rapid AKI-related growth within the Cystatin C assay market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher per-test cost vs. creatinine | -1.1% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Limited reimbursement in emerging markets | -0.8% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Clinical inertia toward creatinine testing | -0.6% | Global, stronger in established systems | Long term (≥ 4 years) |

| Absence of global calibrator standardization | -0.4% | Global, affects inter-lab comparability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Per-Test Cost vs. Creatinine

A Cystatin C run can cost USD 75-100 in low-volume settings, whereas creatinine assays often cost less than USD 1. Budget-constrained hospitals in Africa, South Asia, and parts of Latin America ration usage to high-risk patients rather than routine screening. Gentian Diagnostics projects that reagent costs could drop to USD 5-10 once global volumes crest a meaningful threshold, a projection that rests on scaling production and broader analyzer compatibility. Until then, labs must justify the premium by linking earlier diagnosis to avoided dialysis or shorter ICU stays, a case that resonates more easily with payers in high-income countries than in emerging economies. Consequently, cost remains a drag on short-term uptake and tempers CAGR for the Cystatin C assay market.

Limited Reimbursement in Emerging Markets

Many national insurance schemes in APAC and Africa still classify Cystatin C as an out-of-pocket test, discouraging physicians from ordering it except in complex cases. Where coverage exists, reimbursement often applies only to transplant follow-up or oncology drug monitoring, not routine CKD staging. Ministries of Health demand local health-economic data showing that early detection offsets downstream dialysis costs, but such real-world studies take time to mature. Diagnostic manufacturers partner with teaching hospitals to generate pilot evidence in India, Thailand, and Kenya, aiming to nudge payers toward full tariff codes. In the interim, reimbursement gaps hamper equitable access and slow the Cystatin C assay market’s penetration rate in high-population territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Dominate, Instruments Drive Value

Assay kits and reagents generated 58.67% of the Cystatin C assay market share in 2024, confirming that recurring consumables underpin revenue stability for suppliers. Reagent demand scales in direct proportion to test volume, creating a virtuous loop as guideline adoption expands. Vendors bundle calibrators and controls with reagent cartridges, ensuring that quality-control requirements translate into steady pull-through. On the opposite side, analyzers and instruments represent a smaller revenue slice yet command a 9.36% CAGR to 2030, thanks to laboratory automation and the search for high-throughput solutions. As health systems consolidate laboratories into regional hubs, managers invest in integrated chemistry-immunoassay platforms that host Cystatin C alongside routine analytes, favoring vendors that provide closed-loop ecosystems.

Point-of-care devices start occupying a middle ground between central lab analyzers and bedside strips. Designs that combine Cystatin C with creatinine in a single cartridge allow emergency physicians to obtain eGFR within minutes, closing therapy gaps for septic or trauma patients. Instrument makers tap open-channel architectures so regional reagent brands can load Cystatin C assays without extensive validation, accelerating geographic reach. These product-segment developments underpin momentum for the broader Cystatin C assay market.

By Methodology: Immunoturbidimetric Leads, ELISA Picks Up Pace

Immunoturbidimetric assays held 46.23% share of the Cystatin C assay market size in 2024 because they run seamlessly on widely installed clinical chemistry analyzers. Laboratories appreciate the minimal manual steps, automated calibration, and stable reagent shelf life. Particle-enhanced nephelometry has niche use in certain European centers that value its linearity at low concentrations, but growth remains moderate. ELISA and other high-sensitivity modalities log the fastest 10.23% CAGR because academic groups deploy them in exploratory research and specialized settings such as neonatal units. These platforms also host multiplex kits where Cystatin C shares a microplate with cytokines or cardiac markers, saving sample volume.

Standardization bodies encourage method-to-method convergence by promoting common calibrators and uniform reporting units, which reduce physician confusion and facilitate pooled outcome analytics across trials. Automation vendors incorporate middleware that translates ELISA output into lab information systems, therefore narrowing operational differences with core chemistry lanes. Such methodological evolution keeps the Cystatin C assay market on a consolidation path.

By Sample Type: Serum Dominates, Urine Gains Momentum

Serum and plasma specimens accounted for 82.36% of all Cystatin C tests in 2024, reflecting entrenched workflows where phlebotomy and chemistry processing already exist for complete metabolic panels. Clinicians prefer blood-based eGFR because it ties neatly into dosing calculators embedded in electronic health records. Yet urine testing posts an 11.71% CAGR, largely fueled by cardiac-surgery units that monitor tubular injury early in the postoperative window. Researchers document that urinary Cystatin C spikes sooner than serum changes after cardiopulmonary bypass, letting physicians initiate renal-protective regimens swiftly.

Pediatricians also explore urine assays to sidestep venipuncture in infants, while nephrologists investigate combined urinary Cystatin C and albumin-creatinine ratios for nuanced tubulo-glomerular profiling. Nevertheless, confounders such as smoking and ethanol intake can alter excretion rates, so societies still recommend serum testing for standardized CKD staging. The sample-type mix therefore diversifies, contributing incremental revenue streams to the Cystatin C assay market.

By Application: CKD Leads, AKI Expands Rapidly

Chronic kidney disease assessment generated 53.47% of global demand in 2024, anchored in guideline-mandated staging protocols that now favor creatinine-Cystatin C dual equations. Longitudinal monitoring in diabetes clinics and hypertension programs sustains baseline volumes. Acute kidney injury detection grows faster at 9.79% CAGR, thanks to ICUs and emergency departments that value the biomarker’s earlier kinetic response. Clinical algorithms integrate Cystatin C thresholds with urine output and hemodynamic parameters for bundled AKI alerts, cutting ICU length of stay and improving prognoses.

Cardiovascular and oncology niches add diversification. Elevated Cystatin C joins NT-proBNP in composite cardiac risk scores, while oncology centers deploy the marker to fine-tune nephrotoxic drug regimens. Epidemiology studies link high Cystatin C to mortality in lung, hematologic, brain, and liver cancers, broadening its prognostic role. These application vectors collectively reinforce the Cystatin C assay market.

By End User: Hospitals Anchor Demand, Academia Fuels Innovation

Hospital laboratories held 51.28% share in 2024, supported by 24-hour operations and integrated IT infrastructure that push high daily throughput. Bundling Cystatin C with creatinine and urea nitrogen on comprehensive renal panels allows hospitals to generate eGFR automatically for every patient above a certain age threshold. Reference labs supply community clinics with send-out testing, acting as bridging channels for institutions that lack immunochemistry analyzers.

Academic and research institutes, though smaller, chart a 9.47% CAGR because they investigate multi-omics and artificial-intelligence algorithms that combine Cystatin C with genomic or proteomic data for individualized medicine. These centers often pilot novel sample matrices, sensor technologies, and assay formats. Their proof-of-concept studies frequently transition into commercial kits, feeding the product pipeline that sustains the Cystatin C assay market.

Geography Analysis

North America held 31.26% of the Cystatin C assay market share in 2024 on the back of broad reimbursement and robust analyzer fleets. Implementation of the 2024 KDIGO dual-marker guideline was swift, aided by Medicare coverage that treats Cystatin C on par with creatinine for CKD staging. Academic medical centers contribute a steady flow of high-impact publications that reinforce clinical trust, while integrated delivery networks adopt middleware that automatically reports combined eGFR values. These factors stabilize growth at mid-single digits even as the region matures.

Asia-Pacific charts a 10.14% CAGR to 2030, the fastest globally, as governments upgrade tertiary hospitals and encourage in-country manufacturing to cut reagent import costs. Sysmex’s new Indian reagent plant illustrates localization designed to support high-volume laboratories while keeping price points accessible. Rising incidence of diabetes and hypertension broadens the at-risk population, prompting nephrology societies in China and Japan to draft local guidance that echoes KDIGO recommendations.

Europe enjoys steady growth driven by regulatory harmony and evidence from Sweden, where nationwide adoption has demonstrated practical workflow benefits. Laboratories in Germany and France leverage centralized purchasing contracts to adopt large-batch reagent programs, thereby shrinking per-test expense. Meanwhile, Middle East and Africa markets gain traction as new tertiary centers open in the Gulf and North Africa, though reimbursement gaps and analyzer scarcity temper uptake. Collectively, these regional currents anchor expansion prospects for the global Cystatin C assay market.

Competitive Landscape

The Cystatin C assay market shows moderate concentration, with multinational diagnostics leaders defending share through platform breadth and service networks. Roche, Siemens Healthineers, and Abbott embed Cystatin C into analyzer menus that also include troponin, NT-proBNP, and hormonal assays, creating sticky customer relationships. Service contracts, remote system diagnostics, and reagent rental models make switching costly for laboratories that prize uptime and quality metrics. Roche’s introduction of the Elecsys PRO-C3 liver fibrosis test in 2025 exemplifies a strategy of continuous menu expansion that leverages established immunochemistry hardware.

Emerging firms focus on targeted pain points. Gentian commercializes a particle-enhanced turbidimetric assay calibrated for multiple open analyzers, emphasizing inter-instrument concordance. Point-of-care developers work on handheld cartridges that can generate Cystatin C in tandem with creatinine, positioning themselves for ambulances and rural clinics. The IFCC reference material standard accelerates analytical comparability, giving newcomers a level playing field on traceability claims.

Mergers and acquisitions shape competitive contours; Thermo Fisher’s USD 3.1 billion Olink purchase adds proximity-extension assays that complement high-plex proteomics and can surface new Cystatin C-adjacent biomarkers. As healthcare shifts toward value-based purchasing, vendors differentiate not only on assay precision but also on clinical decision-support software, supply-chain resiliency, and sustainability credentials. These elements collectively define rivalry in the Cystatin C assay market.

Cystatin C Assay Industry Leaders

F. Hoffmann-La Roche Ltd

Siemens Healthineers

Abbott Laboratories

Danaher

Gentian Diagnostics ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Gentian Diagnostics showcased its fully automated Cystatin C immunoassay at ADLM, highlighting broad chemistry-analyzer compatibility.

- December 2024: Gentian Diagnostics projected per-test cost reductions from USD 75-100 to USD 5-10 as volumes scale.

- July 2024: Thermo Fisher Scientific closed its USD 3.1 billion Olink acquisition, expanding high-throughput proteomics that support biomarker validation.

Global Cystatin C Assay Market Report Scope

| Assay Kits & Reagents |

| Analyzers / Instruments |

| Immunoturbidimetric |

| Particle-Enhanced Nephelometric |

| ELISA & Others |

| Serum / Plasma |

| Urine |

| Chronic Kidney Disease Assessment |

| Acute Kidney Injury Detection |

| Cardiovascular Risk Stratification |

| Oncology Therapy Monitoring |

| Hospital Laboratories |

| Reference & Diagnostic Labs |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Assay Kits & Reagents | |

| Analyzers / Instruments | ||

| By Methodology | Immunoturbidimetric | |

| Particle-Enhanced Nephelometric | ||

| ELISA & Others | ||

| By Sample Type | Serum / Plasma | |

| Urine | ||

| By Application | Chronic Kidney Disease Assessment | |

| Acute Kidney Injury Detection | ||

| Cardiovascular Risk Stratification | ||

| Oncology Therapy Monitoring | ||

| By End User | Hospital Laboratories | |

| Reference & Diagnostic Labs | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Cystatin C assay market?

The market posted USD 430.67 million in 2025 and is projected to reach USD 619.58 million by 2030 at a 7.55% CAGR.

How do updated KDIGO guidelines influence Cystatin C testing?

The 2024 guideline now recommends combined creatinine-Cystatin C eGFR equations, accelerating laboratory adoption worldwide and boosting test volumes.

Why is Cystatin C preferred over creatinine in acute kidney injury detection?

Cystatin C rises 6-48 hours before creatinine, enabling earlier intervention and potentially avoiding dialysis in critical care settings.

Which region is growing fastest for Cystatin C assays?

Asia-Pacific logs the highest growth, with a 10.14% CAGR through 2030 due to healthcare modernization and rising chronic disease prevalence.

What limits broader Cystatin C uptake in emerging markets?

Higher per-test costs and limited reimbursement frameworks remain key barriers, although projected reagent price drops may ease constraints.

Which application segment shows the strongest growth?

Acute kidney injury detection leads with a 9.79% CAGR as emergency and intensive care units adopt rapid Cystatin C protocols.

Page last updated on: