Medical Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

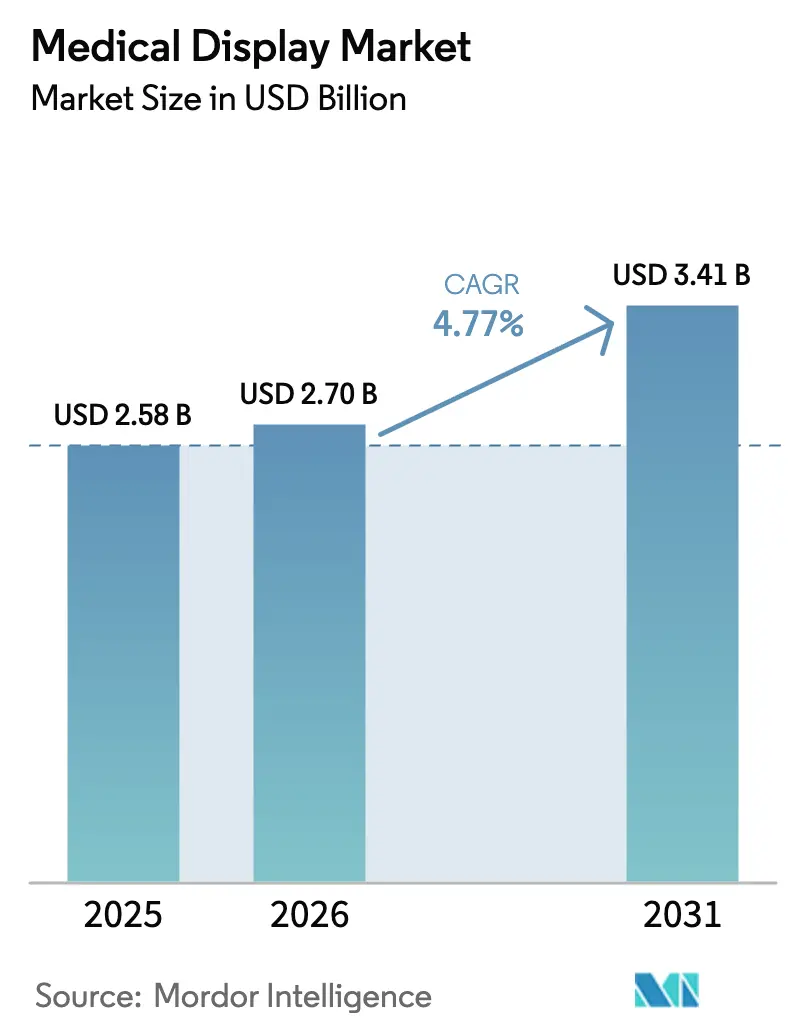

| Market Size (2026) | USD 2.7 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 4.77% CAGR |

| Fastest Growing Market | Middle East and Africa |

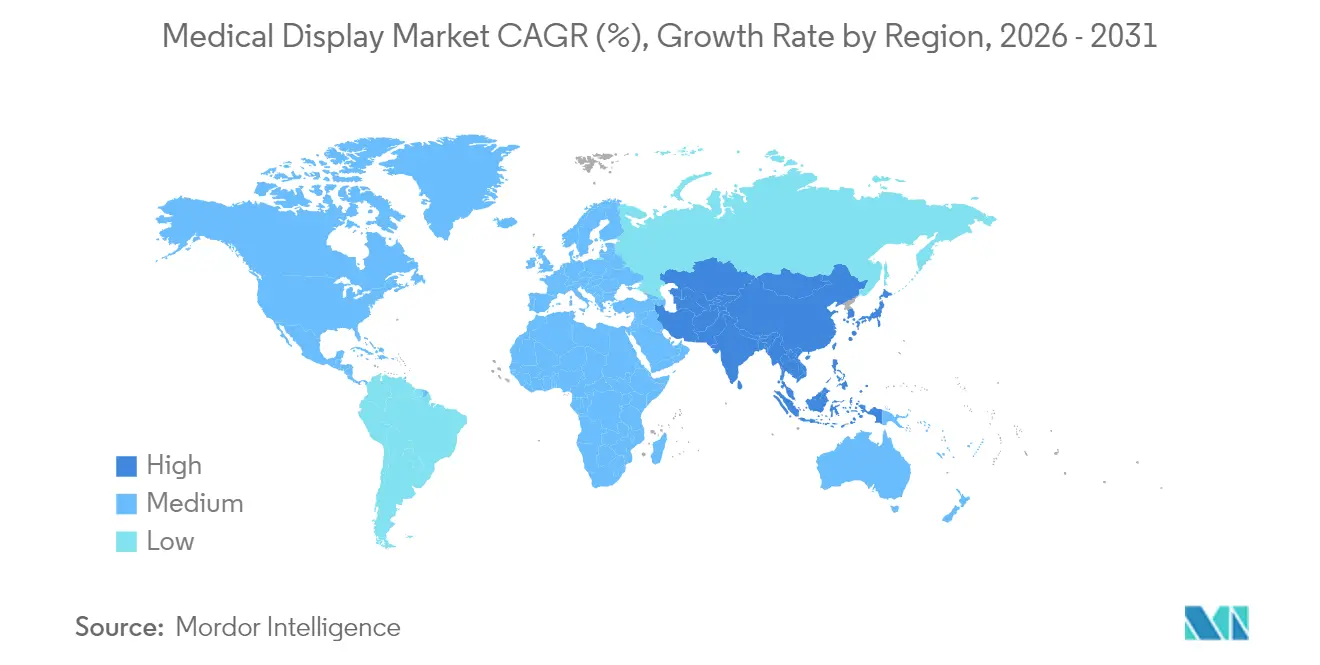

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Display Market Analysis by Mordor Intelligence

The medical display market size in 2026 is estimated at USD 2.7 billion, growing from 2025 value of USD 2.58 billion with 2031 projections showing USD 3.41 billion, growing at 4.77% CAGR over 2026-2031. The shift from cold-cathode fluorescent lamp panels to LED-backlit, OLED, and emerging micro-LED architectures continues to reshape procurement strategies, as hospitals seek brighter screens, longer lifecycles, and embedded AI capabilities that lower reading-room latency. Regulatory pushes—most notably the U.S. FDA’s Section 524B cybersecurity mandate—force quicker replacement cycles, while hybrid OR build-outs call for 4K-over-IP surgical panels that stream uncompressed video across hospital IP networks. The Asia-Pacific region leads in value, supported by extensive hospital infrastructure programs in China and India, whereas the Gulf Cooperation Council and South Africa are investing aggressively despite smaller installed bases. Trade tensions, phosphorus shortages, and fragmented calibration support moderate the headline growth rate; yet, value-based care and precision-medicine workflows continue to anchor capital spending.

Key Report Takeaways

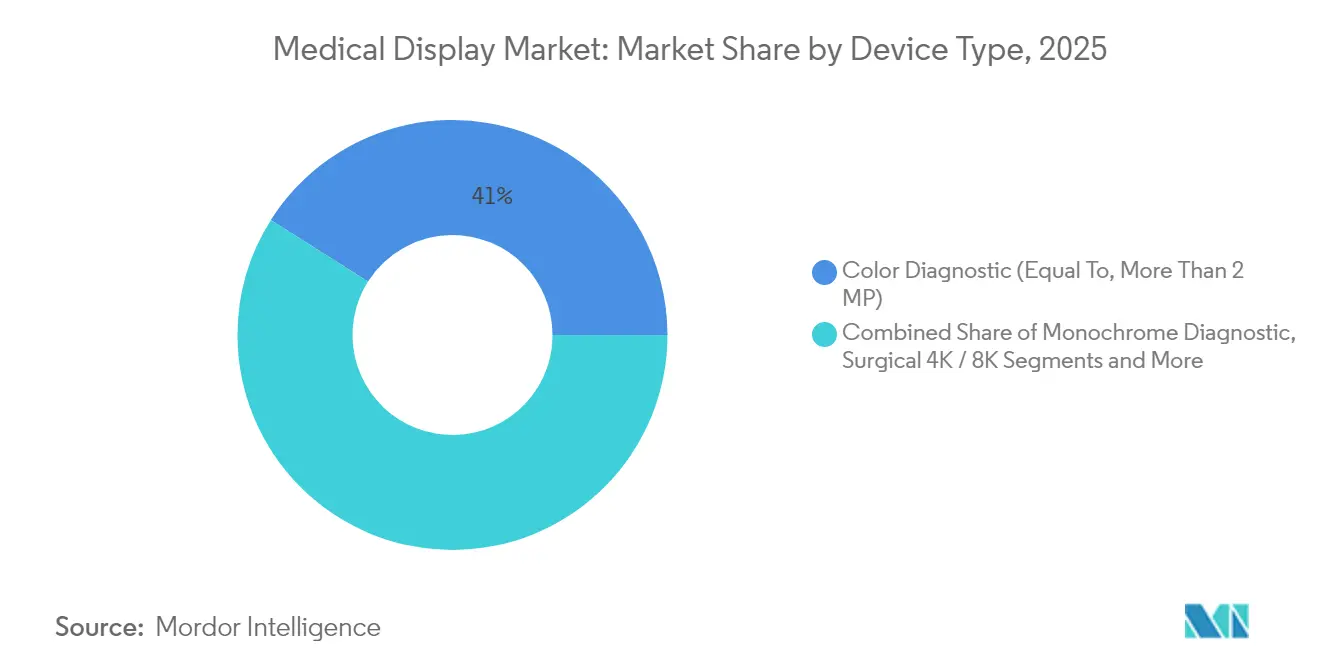

- By display type, color diagnostic panels above 2 megapixels led with 41.02% of the medical display market size in 2025; flexible OLED displays are advancing at an 7.91% CAGR to 2031.

- By panel size, 27.0–41.9 inch formats accounted for 39.55% of the medical display market size in 2025, whereas panels 42 inches and above are rising at a 6.91% CAGR.

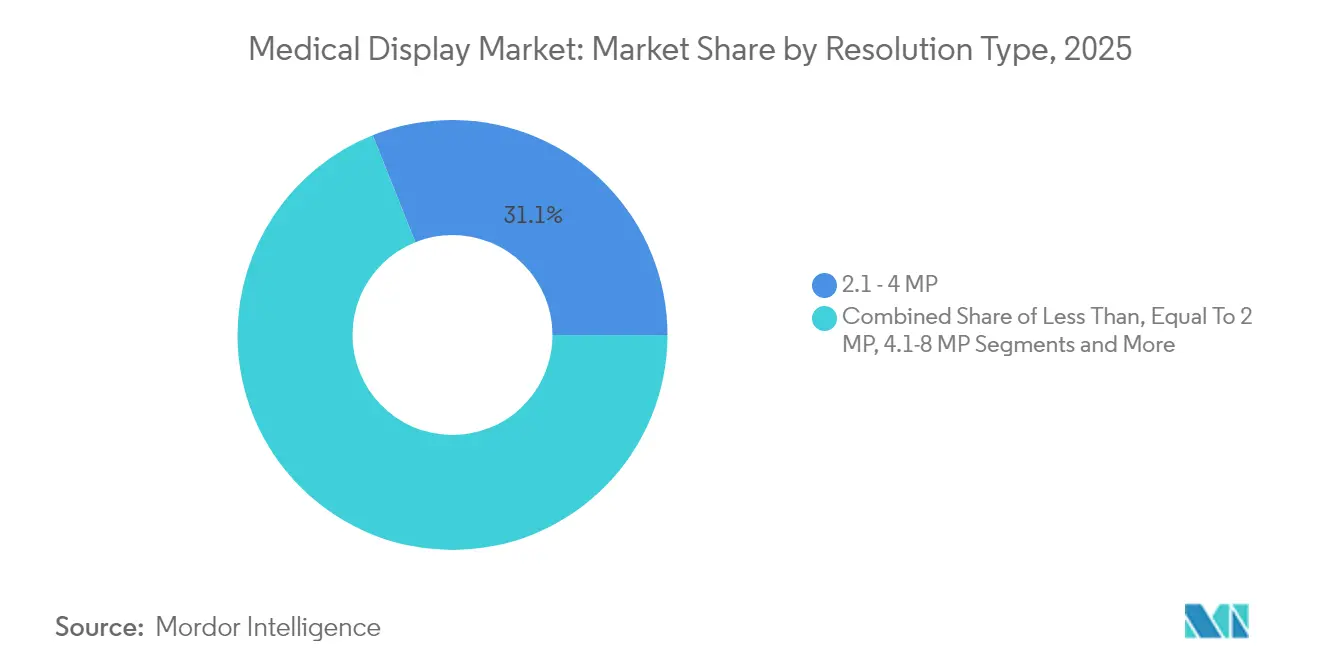

- By resolution, 2.1–4 megapixel screens held 31.05% share of the medical display market size in 2025, while panels above 8 megapixels are projected to grow at a 6.05% CAGR.

- By technology, LED-backlit LCDs dominated with 64.05% of the medical display market size in 2025; micro-LED solutions exhibit a 6.98% CAGR.

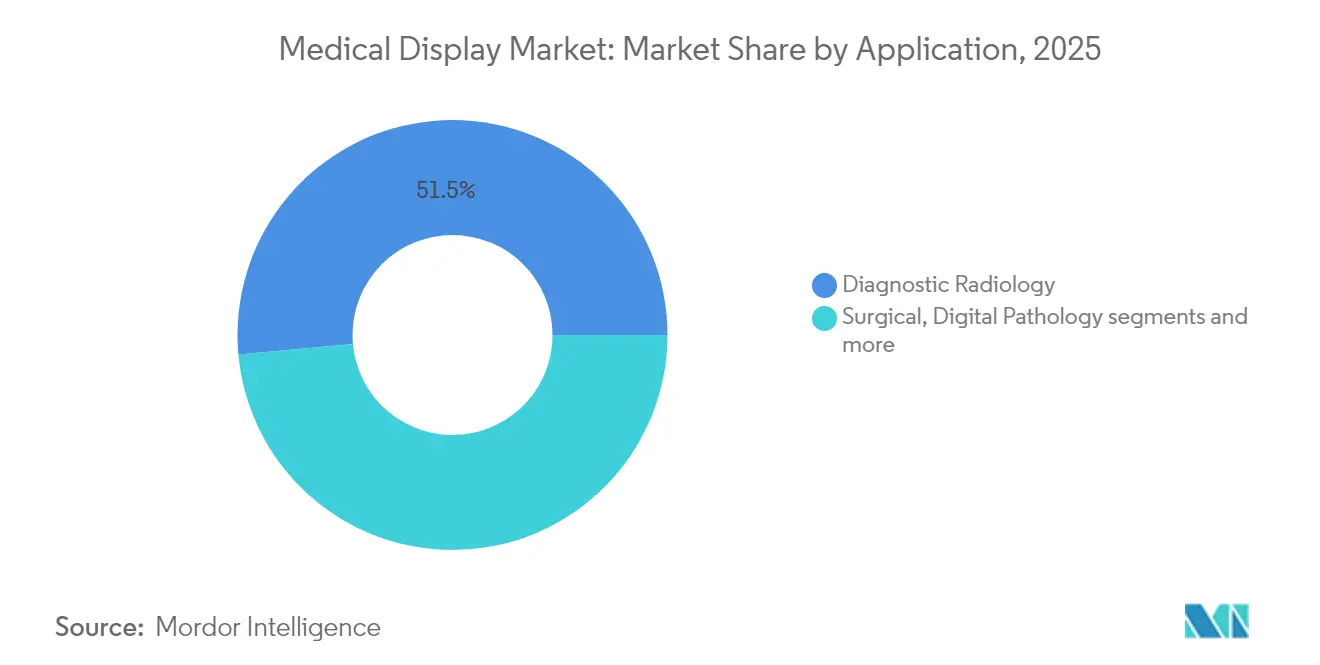

- By application, surgical and endoscopy displays led with a 24.62% revenue share in 2025; digital pathology is the fastest-growing use case, growing at an 8.45% CAGR through 2031.

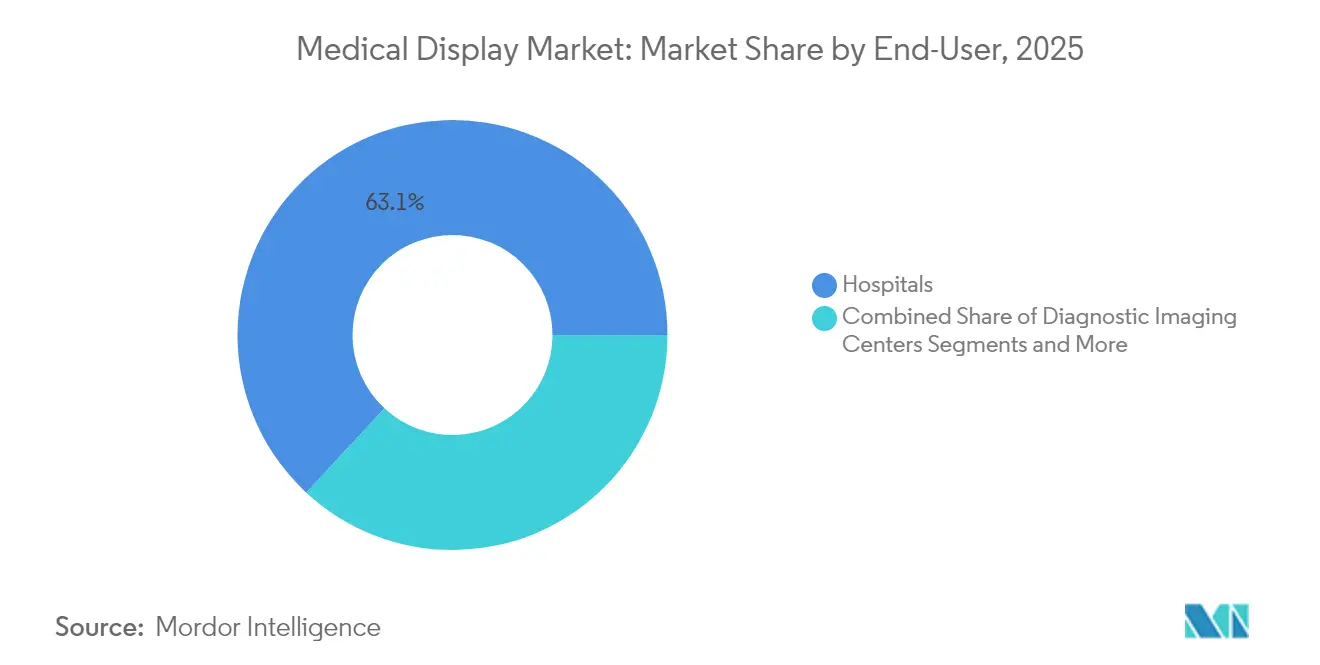

- By end user, hospitals captured 63.10% of the medical display market share in 2025, while ambulatory surgical centers are expanding at a 6.01% CAGR through 2031.

- By geography, Asia-pacific captured 37.15% of the medical display market share in 2025, while middle-east and africa are expanding at a 6.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Display Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of AI-Ready 4–8 K Diagnostic Workstations | +1.2% | Global, North America & EU core | Medium term (2-4 years) |

| Regulatory Mandates for DICOM Calibration & Cybersecurity Hardening | +0.9% | North America & EU, spillover to APAC | Short term (≤ 2 years) |

| Proliferation of Hybrid ORs Requiring 4K-Over-IP Surgical Panels | +0.8% | Global, led by North America & APAC | Medium term (2-4 years) |

| APAC Hospital-Build Boom with Local Manufacturing Incentives | +1.1% | APAC core, spillover to MEA | Long term (≥ 4 years) |

| Micro-LED Backlight Breakthroughs Lowering Ownership Cost | +0.7% | Global | Long term (≥ 4 years) |

| Flexible OLED Glass Enabling Wearable & Curved Clinician Displays | +0.5% | North America & EU, early APAC adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI-Ready 4–8K Diagnostic Workstations

Radiologists now embed convolutional neural networks directly into diagnostic consoles, enabling chest X-ray triage and lung nodule flagging without sending images to external servers. In 2024, the FDA cleared more than 600 AI-enabled radiology algorithms, each requiring displays of at least 4 megapixels to visualize heatmaps alongside source images. Barco’s 2024 Coronis Uniti paired a tensor-core GPU with dual 12-megapixel panels to serve high-volume academic centers.[1]Barco NV, “Coronis Uniti Launch Press Release,” Barco, barco.com GE Healthcare upgraded its Centricity viewer in 2025 to stream 8K surgical video, requiring HDMI 2.1 and DisplayPort 2.0 interfaces. These capabilities lift productivity and shorten time-to-diagnosis, contributing 1.2 percentage points to the overall CAGR. Hospitals expect to see peak benefits in three to four years as they align display purchases with workstation refresh cycles.

Regulatory Mandates for DICOM Calibration & Cybersecurity Hardening

Section 524B, finalized in October 2024, requires software bills of materials and quarterly firmware updates for every networked diagnostic display. Institutions that cannot prove DICOM calibration risk facing Joint Commission penalties that result in reduced Medicare reimbursements. EIZO’s RadiCS software automates monthly checks and logs results across 4,500 U.S. hospitals. Siemens Healthineers introduced a zero-trust network design for its Atellica line in 2025, safeguarding display traffic against ransomware. The combined effect adds 0.9 percentage points to the CAGR, especially in the first two years of enforcement.

Proliferation of Hybrid ORs Requiring 4K-Over-IP Surgical Panels

Hybrid operating suites combine fixed imaging, navigation, and robotic systems, all of which depend on low-latency 4K feeds. Olympus launched EasySuite 4K in 2024, routing uncompressed video over 10-gigabit Ethernet to 55-inch monitors. Barco’s 2025 Nexxis update supports SMPTE ST 2110, letting surgeons annotate live images for remote consultation. The American College of Surgeons found that 18% of U.S. hospitals already house at least one hybrid OR. The trend lifts the growth rate by 0.8 percentage points with a material impact in the medium term.

APAC Hospital-Build Boom with Local Manufacturing Incentives

China’s 14th Five-Year Plan earmarks CNY 300 billion for 1,200 county-level hospitals by 2026, each requiring extensive diagnostic display fleets. India’s Ayushman Bharat program finances 157 new medical colleges, creating orders for up to 25,000 PACS workstations. Domestic content rules spur local fabs, such as Jusha’s 500,000-unit Nanjing plant, which opened in 2024. Japan offers 30% tax credits for OLED and micro-LED pilot lines to encourage onshore manufacturing.[3]Ministry of Health, Labour and Welfare, “Medical Equipment Development Support Program Guidelines,” MHLW, mhlw.go.jp These forces add roughly 1.1 percentage points to long-term CAGR.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-Ex & Short Refresh Cycles in Cost-Constrained Facilities | -0.6% | Global, acute in South America & sub-Saharan Africa | Short term (≤ 2 years) |

| Global Shortage of Rare-Earth Phosphors for High-Brightness Panels | -0.4% | Global | Medium term (2-4 years) |

| Fragmented Post-Sale Calibration Service Networks in Emerging Markets | -0.3% | APAC emerging, MEA, South America | Medium term (2-4 years) |

| Trade-War Tariffs on LED Drivers & Glass Substrates | -0.5% | North America, spillover to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex & Short Refresh Cycles in Cost-Constrained Facilities

Public hospitals in South America and sub-Saharan Africa allocate under 12% of capital budgets to imaging, leaving only 2–3% for displays. A 5-megapixel color monitor costs USD 8,000–12,000, or about 15% of a mid-tier ultrasound unit, prompting buyers to extend refresh cycles by two to three years. Brazil’s Sistema Único de Saúde froze reimbursement in 2023, and 40% of radiology workstations ran non-DICOM screens in early 2025. South Africa’s National Health Insurance pilot caps equipment funding at ZAR 50 million per facility, limiting display upgrades. The constraint subtracts 0.6 percentage points from global growth.[2]South Africa Department of Health, “National Health Insurance Pilot Framework,” Health SA, health.gov.za

Global Shortage of Rare-Earth Phosphors for High-Brightness Panels

China’s 2024 Critical Minerals Export Control curbed europium and terbium exports, doubling lead times to 20 weeks in 2025. Substitutes reduce DICOM compliance, and alternative refining in Australia or the United States is still years away. NEC Display noted 28% higher phosphor costs in 2024, while Totoku dual-sourced from Lynas and Shenghe at a premium. The shortfall trims CAGR by 0.4 percentage points through mid-decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Type: Surgical Displays Lead, OLED Variants Surge

Color diagnostic screens above 2 megapixels commanded 41.02% of the medical display market in 2025. Surgical 4 K and 8 K panels covered 24.62%, fueled by minimally invasive procedures that rely on endoscopic images. Flexible OLED units, though smaller in share, register an 7.91% CAGR as curved clinician monitors and wearables gain traction. Regulatory compliance under IEC 60601-1 adds up to nine months in design testing, while OLED burn-in concerns spur pixel-shift algorithms. Barco’s Nexxis OLED panel promises service life parity with LED models, and touch-enabled bedside monitors carry antimicrobial coatings certified for 10,000 alcohol-wipe cycles.

Monochrome diagnostic screens keep footholds in mammography-focused sites, but digital breast tomosynthesis now overlays microcalcifications in color, accelerating the color shift. Clinical-review monitors serve emergency and intensive-care units, favoring thin bezels and single-cable USB-C connectivity as seen in Dell’s P2423DE. Surgical displays face splash-proof and sterilization challenges, raising enclosure costs. Vendors differentiate via built-in calibration engines and IEC 62304-compliant firmware that logs luminance drift for audits. As hybrid OR adoption widens, multi-input 55-inch models with picture-in-picture features replace analog matrices, making surgical displays the visible growth engine of the medical display market.

By Panel Size: Mid-Range Dominates, Large Formats Accelerate

Screens between 27.0 and 41.9 inches held 39.55% of the medical display market in 2025, reflecting the ergonomic sweet spot for dual-monitor radiology desks. Larger units of 42 inches or more are growing at 6.91% CAGR, driven by multi-modality reading rooms and ceiling-mounted hybrid-OR installations. ISO 9241 guidelines dictate a 50–70 cm viewing distance, favoring mid-range panels for routine diagnostic work. Large screens must meet IEC 60068 seismic-stress tests, adding both bracket costs and installation planning to capital budgets.

Small formats under 23 inches remain in mobile carts and field clinics, yet tablets encroach on their territory. Mid-range displays benefit from narrower bezels that cut eye travel in comparative reading. Large formats integrate picture-in-picture overlays of vitals, a time-saving feature validated by EIZO’s 43-inch EX4342. While touch functionality is rare on ceiling-mounted OR screens, voice-controlled overlays gain acceptance, reducing contamination risk. Hospitals reviewing PACS replacement cycles therefore weigh mid-range panel refreshes against new large-format investments, a balance that keeps both segments vital to medical display market growth. Surgeons benefit from a single large screen that reduces head movement and streamlines team communication. Ceiling-suspended 4 K panels with low-latency video routing eliminate bezel gaps and preserve sterile lines of sight. Meanwhile, displays under 23 inches stay relevant for dental chairs and ophthalmic microscopes where space constraints persist.

By Resolution: Mid-Range Prevails, Ultra-High Density Climbs

Panels delivering 2.1–4 megapixels secured 31.05% of the medical display market in 2025 by balancing cost and clarity for general radiology. Displays at or below 2 megapixels linger in point-of-care settings, while 4.1–8 megapixel units support mammography and digital pathology. Ultra-high-density screens beyond 8 megapixels advance at 6.05% CAGR, propelled by augmented-reality surgery and virtual-reality training. Barco’s Fusion 12-megapixel panel surpasses American College of Radiology brightness guidelines by 20%.

Bandwidth constraints loom: 12-megapixel video at 60 fps demands DisplayPort 2.0 or HDMI 2.1. Many workstations still rely on older ports, capping motion-cine loops at 30 Hz. BenQ Medical’s hardware scaler sidesteps the gap by downsampling whole-slide images in real time. Lower-resolution displays below 2 megapixels risk obsolescence as electronic medical-record tablets standardize Full-HD. Nonetheless, they remain inexpensive tools for bedside verification and mobile ultrasound carts, sustaining a niche footprint in the wider medical display market.

By Technology: LED-Backlit LCD Dominates, Micro-LED Gains Momentum

LED-backlit LCD panels held 64.05% of the medical display market in 2025 thanks to mature supply chains and proven calibration software. OLED offers infinite contrast but still trails in longevity and cost, while micro-LED combines both advantages yet sits in pilot production. Mini- and micro-LED backlights post a 6.98% CAGR, promising double-length lifespans that lower service calls. Mercury-based CCFL backlights are exiting under the Minamata Convention, though refurbished equipment extends their tail in lower-income regions.

IPS technology dominates color diagnostic displays for 178-degree viewing angles. VA panels, with higher contrast, serve monochrome needs. LG’s 31-inch IPS module meets DICOM Part 14 without uniformity issues, cementing IPS in mainstream adoption. Micro-LED remains premium, at USD 20,000 for a 27-inch unit, but Sony’s Crystal LED shows the performance ceiling. As yields climb and tariffs shift, technology mix will continue to rebalance, keeping competitive tension high and reinforcing multi-vendor procurement policies across the medical display market.

By Application: Surgical Endoscopy Leads, Digital Pathology Surges

Surgical and endoscopy uses held 24.62% of 2025 revenue as minimally invasive procedures rely on high-resolution visualization. Radiology PACS remain foundational, though growth plateaus in saturated geographies. Digital pathology expands at 8.45% CAGR: Philips’ IntelliSite 5.0 now lets U.S. hospitals record primary diagnoses using 8-megapixel calibrated screens. Mammography retains strict 5-megapixel baselines and semi-annual calibration, raising total cost of ownership to USD 30,000 per workstation.

Hybrid ORs blend fluoroscopy, navigation, and endoscopy feeds on shared 4 K overlays, cutting procedure times by up to 12 minutes. Pathology labs demand gigapixel slide rendering without tiling artifacts, and color-accuracy Delta-E below 2.0 ensures reliable stain differentiation. Multi-modality reading combines CT, MRI, and ultrasound on large displays, lowering context-switch fatigue. Each workflow adds fresh replacement demand, extending growth momentum across the medical display market.

By End User: Hospitals Dominate, Ambulatory Centers Accelerate

Hospitals held 63.10% of the medical display market in 2025, driven by comprehensive imaging suites and hybrid ORs. Ambulatory surgical centers grow at 6.01% CAGR as insurers shift cataract and orthopedic cases to lower-cost environments. Imaging centers rely on dual 5-megapixel PACS workstations for diagnostics, while clinics deploy lower-resolution screens for point-of-care ultrasound. Academic institutions pilot ultra-high-resolution and AR-enabled monitors for training.

Centers for Medicare & Medicaid Services lists more than 6,000 U.S. ambulatory centers as of 2024 CMS.GOV. GE’s OEC Elite mobile C-arm pairs with a 27-inch touchscreen that stores fluoroscopic images locally. Diagnostic centers face reimbursement pressure yet must keep American College of Radiology accreditation. Rural clinics lean on teleradiology, shifting display spend upstream to centralized reading hubs. Nonetheless, all settings must meet rising cybersecurity and calibration standards, anchoring a broad base of recurring demand within the medical display market.

Geography Analysis

Asia-Pacific captured 37.15% of the medical display market in 2025. China’s CNY 300 billion hospital-build drive and India’s Ayushman Bharat college program feed continuous demand, while Jusha’s Nanjing fab and Shenzhen Beacon’s surgical panels satisfy local-content rules. Japan’s 30% tax credit encourages OLED and micro-LED pilots, and South Korea now reimburses digital pathology consultations nationwide. Middle East and Africa, although smaller, post the fastest 6.28% CAGR through 2031, buoyed by Saudi Arabia’s King Salman Medical City and South Africa’s National Health Insurance roll-out.

North America and Europe are transitioning from volume growth to refresh-driven upgrades, prioritizing AI-ready, cybersecurity-hardened panels. Section 524B forces early replacements, and Germany’s 2025 calibration directive adds quarterly audits. The U.K.’s NHS lengthens refresh cycles yet upgrades surgical rooms first. South American hospitals struggle with frozen reimbursement and tariff-inflated component costs; Brazil reports that 40% of workstations are non-compliant, and Argentina’s modernization funds are stretched thin under 18–22% import surcharges. Despite regional disparities, each geography faces its own blend of regulatory drivers and fiscal challenges that shape localized procurement for the medical display market.

Competitive Landscape

The top five suppliers—Barco, EIZO, Sony, LG Display, and Siemens Healthineers—major share in 2024, signalling moderate concentration. Imaging-equipment vendors bundle monitors with modalities, a practice drawing European antitrust scrutiny. Pure-play specialists defend premium niches using quality-assurance suites and 80-country service coverage, while Chinese entrants such as Jusha and Beacon undercut prices by up to 40% in Asia-Pacific tiers two and three.

Sony and LG Display redeploy consumer OLED fabs for medical-grade production, compressing margins yet widening volume. Patent filings in mini- and micro-LED backlighting rose 40% in 2024, enabling semiconductor players like Nichia to seek footholds. Software-defined calibration startups threaten incumbent recurring revenue by certifying commodity displays through the cloud. Advantech and Dell extend enterprise IT channels into clinics and physician offices. Regulatory barriers under IEC 62304 and ISO 13485 slow newcomers but ensure safety, sustaining the current balance of power in the medical display market.

Medical Display Industry Leaders

Novanta Inc. (NDS Surgical Imaging)

Barco NV

Sony Corporation

LG Display Co., Ltd.

EIZO Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Barco will integrate NVIDIA IGX Thor robotics processors into NexxisCompute for edge AI in operating rooms and interventional radiology labs.

- July 2024: Philips won FDA 510(k) clearance for IntelliSite Pathology Solution 5.0, adding calibrated 8-megapixel displays for primary diagnosis.

- March 2024: Barco and NVIDIA partnered to embed AI image processing in the dual 12-megapixel Coronis Uniti workstation for high-volume radiology environments

Global Medical Display Market Report Scope

As per the scope of the report, a medical display is a specialized monitor for viewing diagnostic images in healthcare settings, meeting strict quality and calibration standards. The medical display market is segmented into display type, panel size, resolution, technology, application, end-user and geography. By display type, the market is segmented into Color Diagnostic (≥2 MP), Monochrome Diagnostic, Surgical 4K/8K, Clinical Review & Point-of-Care, and Touch-enabled Patient Monitoring. By panel size, the market is segmented into up to 22.9 inches, 23.0–26.9 inches, 27.0–41.9 inches, and ≥ 42 inches (Large Format). By resolution, the market is segmented into ≤2 MP, 2.1–4 MP, 4.1–8 MP, and >8 MP & 3D / AR-ready. By technology, the market is segmented into LED-backlit LCD (IPS / VA), OLED, Mini- / Micro-LED, and CCFL Legacy (phase-out). By application, the market is segmented into Radiology & PACS, Mammography & Tomosynthesis, Surgical & Endoscopy, Digital Pathology, and Multi-modality. By end user, the market is segmented into Hospitals, Diagnostic Imaging Centers, Ambulatory Surgical Centers, clinics and physician offices, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (in USD) for the above segments.

| Color Diagnostic (≥2 MP) |

| Monochrome Diagnostic |

| Surgical 4K / 8K |

| Clinical Review & Point-of-Care |

| Touch-enabled Patient Monitoring |

| Up to 22.9-inch |

| 23.0–26.9-inch |

| 27.0–41.9-inch |

| ≥42-inch Large Format |

| Less than Equal To 2 MP |

| 2.1–4 MP |

| 4.1–8 MP |

| More Than 8 MP & 3D / AR-ready |

| LED-backlit LCD (IPS / VA) |

| OLED |

| Mini- / Micro-LED |

| CCFL Legacy (phase-out) |

| Radiology & PACS |

| Mammography & Tomosynthesis |

| Surgical & Endoscopy |

| Digital Pathology |

| Multi-modality |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Clinics & Physician Offices |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Display Type | Color Diagnostic (≥2 MP) | |

| Monochrome Diagnostic | ||

| Surgical 4K / 8K | ||

| Clinical Review & Point-of-Care | ||

| Touch-enabled Patient Monitoring | ||

| By Panel Size | Up to 22.9-inch | |

| 23.0–26.9-inch | ||

| 27.0–41.9-inch | ||

| ≥42-inch Large Format | ||

| By Resolution | Less than Equal To 2 MP | |

| 2.1–4 MP | ||

| 4.1–8 MP | ||

| More Than 8 MP & 3D / AR-ready | ||

| By Technology | LED-backlit LCD (IPS / VA) | |

| OLED | ||

| Mini- / Micro-LED | ||

| CCFL Legacy (phase-out) | ||

| By Application | Radiology & PACS | |

| Mammography & Tomosynthesis | ||

| Surgical & Endoscopy | ||

| Digital Pathology | ||

| Multi-modality | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Clinics & Physician Offices | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical display market?

The medical display market size is valued at USD 2.7 billion in 2026 and is forecast to reach USD 3.41 billion by 2031.

Which display technology is growing the fastest?

Micro-LED backlit panels post the highest growth, advancing at 6.98% CAGR as brightness and lifespan advantages improve total cost of ownership.

Why are hybrid operating rooms influencing display demand?

Hybrid ORs require 4 K-over-IP video distribution and large surgical monitors, which accelerate refresh cycles and lift unit volumes, especially in North America and Asia-Pacific.

How do new FDA cybersecurity rules affect hospital purchasing?

Section 524B forces hospitals to replace non-compliant displays sooner and to document quarterly firmware and calibration updates, increasing near-term procurement.

What challenges limit adoption in emerging markets?

High upfront costs, rare-earth phosphor shortages, fragmented calibration services, and tariff-driven price increases constrain uptake, particularly in South America and sub-Saharan Africa.

Which application segment is expanding the quickest?

Digital pathology shows the fastest growth at an 8.45% CAGR, reflecting wider whole-slide imaging adoption and FDA clearance for primary diagnoses using calibrated 8-megapixel monitors.

Page last updated on: