Medical Pendant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

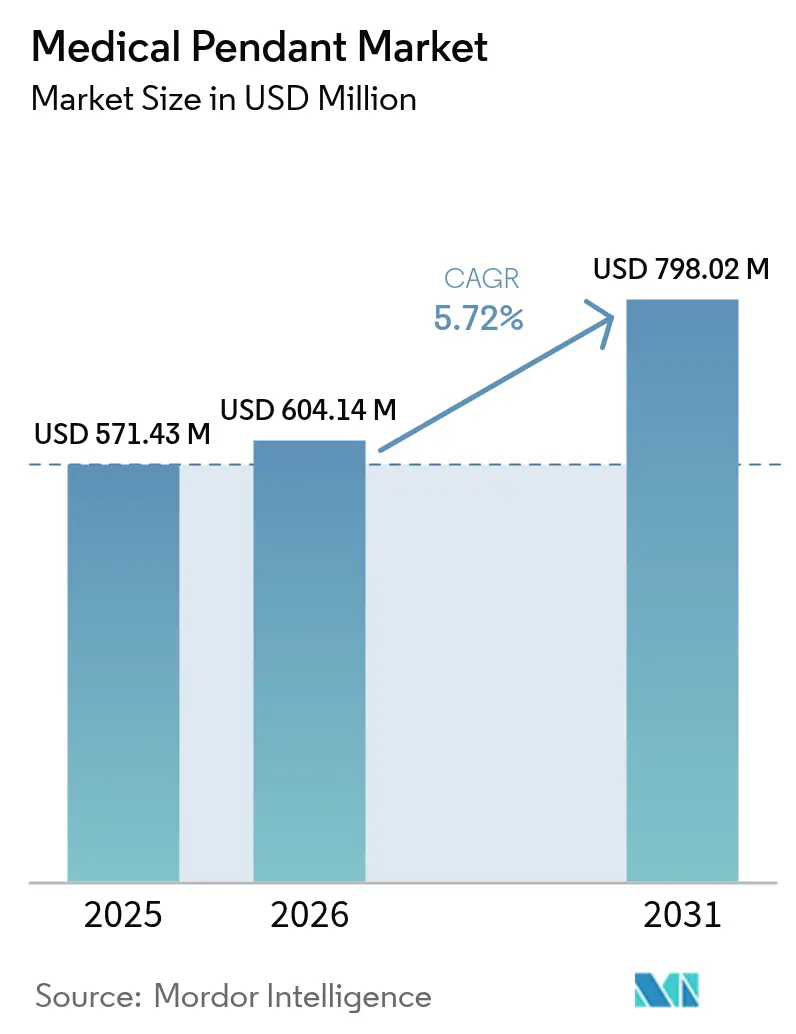

| Market Size (2026) | USD 604.14 Million |

| Market Size (2031) | USD 798.02 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

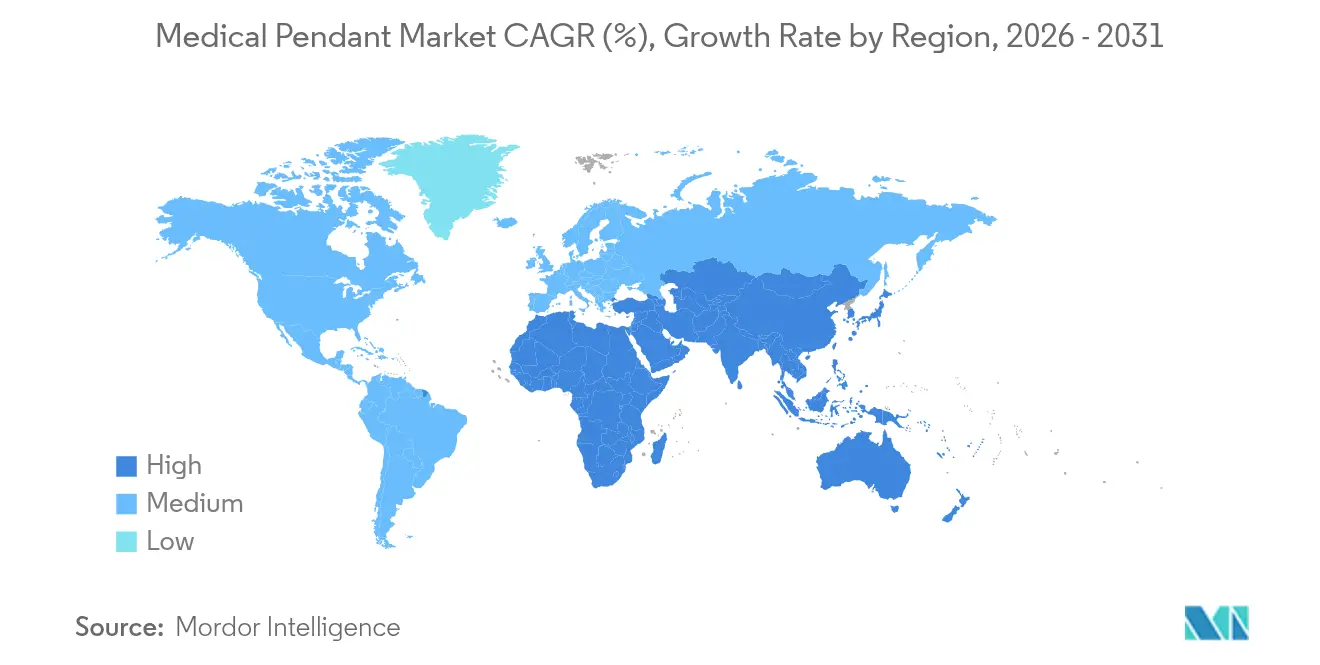

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Pendant Market Analysis by Mordor Intelligence

The Medical Pendant Market size was valued at USD 571.43 million in 2025 and estimated to grow from USD 604.14 million in 2026 to reach USD 798.02 million by 2031, at a CAGR of 5.72% during the forecast period (2026-2031).

This performance reflects the sector’s shift from static ceiling booms to digitally enabled clinical infrastructure that supports image-guided, minimally invasive, and hybrid procedures. Hybrid operating room installations, higher surgical volumes, and sustained demand for modular critical-care spaces continue to shape purchasing priorities. Hospitals in mature economies are retrofitting existing suites to meet ESG mandates and workflow digitalization goals, while new facilities in developing regions specify pendant systems at the architectural design stage. Vendors compete on automation, data integration, and infection-control features rather than on mechanical design alone, resulting in a steady pipeline of AI-ready pendant platforms. Intensifying biomedical engineer shortages remain a structural risk because unserved maintenance needs can slow unit deployment and lengthen replacement cycles.

Key Report Takeaways

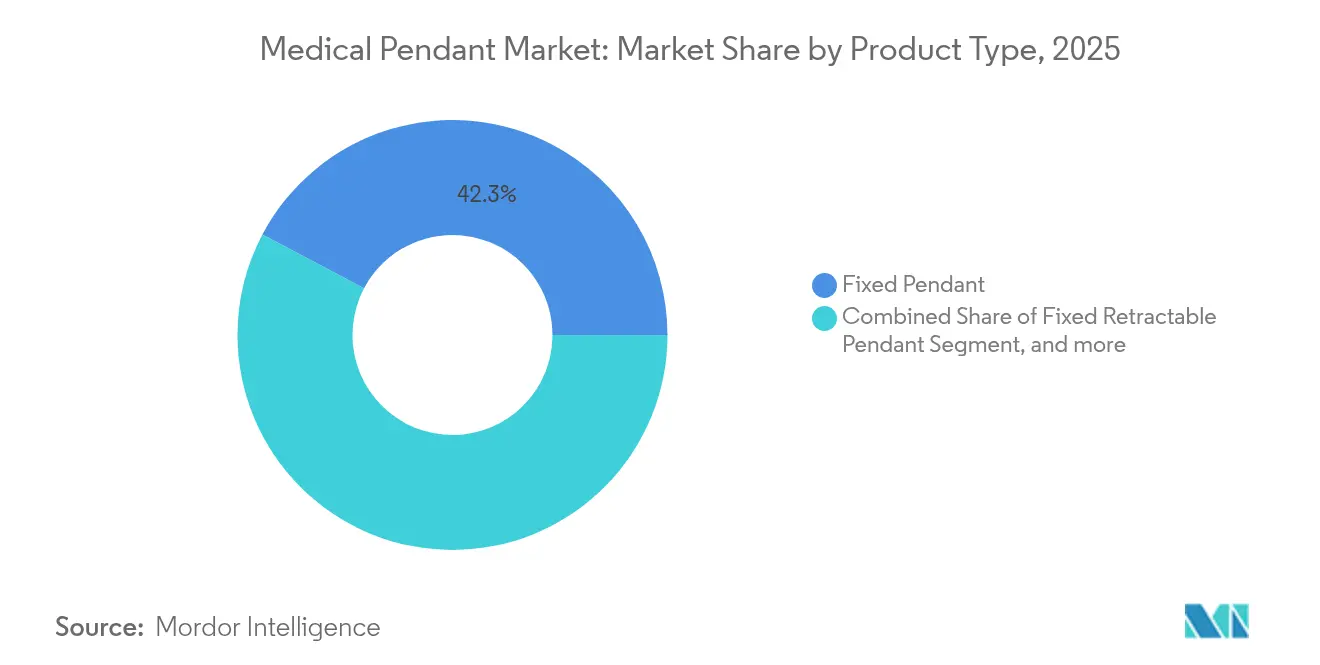

- By product type, fixed pendant systems led with 42.26% of medical pendant market share in 2025; motorized pendant systems are projected to grow at 7.78% CAGR to 2031.

- By application, surgery accounted for 33.88% of the medical pendant market size in 2025, while emergency & trauma is set to expand at a 8.61% CAGR through 2031.

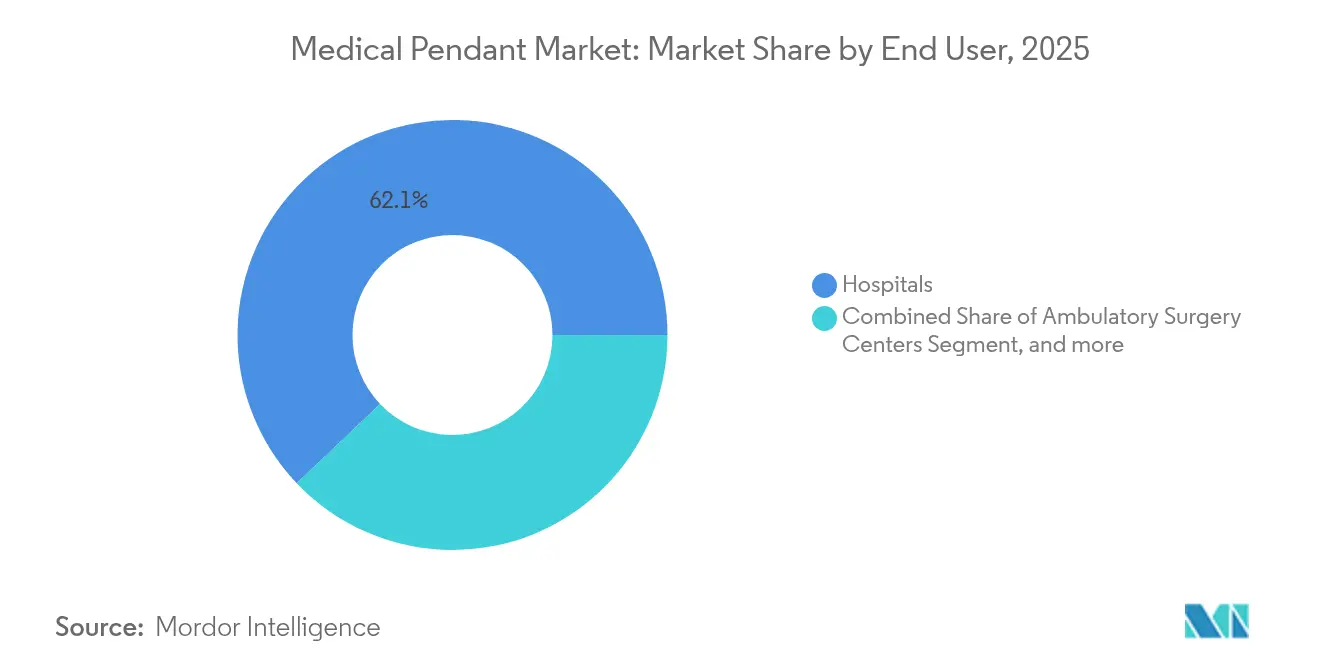

- By end user, hospitals held 62.10% revenue share in 2025; ambulatory surgery centers record the highest forecast CAGR at 8.83% through 2031.

- By geography, North America commanded 31.84% of market revenue in 2025; Asia is expected to grow at 10.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Pendant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Number of Surgical Procedures Globally | +1.5% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Expansion of Healthcare Infrastructure in Tier-2 And Tier-3 Cities | +0.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Growing Adoption of Hybrid Operating Rooms Integrating Imaging | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increased Deployment of Ceiling-Mounted Robotic Systems | +0.9% | Global, led by North America | Short term (≤ 2 years) |

| Surge In Demand for Modular ICU and Critical Care | +1.1% | Global, accelerated in post-pandemic recovery regions | Short term (≤ 2 years) |

| ESG-Driven Hospital Retrofitting Initiatives | +0.6% | EU & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Surgical Procedures Globally

Global procedure counts are climbing as minimally invasive techniques broaden eligibility for complex interventions. Ambulatory surgery centers alone expect 44 million procedures by 2034, a 21% rise over current levels.[1]American Surgery Center Association, “Outlook 2025: Ambulatory Surgery Demand,” ascfocus.org Higher case volumes intensify demand for pendant platforms that can reposition quickly, carry heavier imaging payloads, and interlock with robotic arms. Multi-arm motorized models therefore gain preference over traditional single-arm booms that restrict room turnover. Vendors position modular designs that accept specialty attachments so hospitals can shift between orthopedics, cardiovascular, and trauma workflows without purchasing separate pendant sets. This driver is most visible in high-throughput centers where procedure delays carry direct reimbursement penalties.

Expansion of Healthcare Infrastructure in Tier-2 and Tier-3 Cities

Government investment programs in secondary urban clusters fund new build hospitals that leapfrog legacy infrastructure. India’s state health authorities, for example, allocated INR 255 billion (USD 3.1 billion) for district hospital upgrades in 2025. Because these facilities start with greenfield layouts, planners specify digital pendant networks from the outset, avoiding costly retrofits later. Manufacturers active in these markets bundle gas, data, and power channels into standardized rails that shorten installation time by up to 30%. The approach balances budget sensitivity with room for later upgrades, ensuring compliance with evolving accreditation norms.

Growing Adoption of Hybrid Operating Rooms Integrating Imaging

Hybrid suites combining surgical and imaging technologies now represent close to 15% of new OR projects in North America.[2]Applied Sciences Editorial Board, “Hybrid Operating Room Design Paradigms,” mdpi.com Every ceiling node must support C-arm clearance, light contamination control, and multi-modality data distribution. Pendant suppliers respond with low-profile multi-arm frames and shielded cable trunks that prevent electromagnetic interference during real-time imaging. Neurosurgical and cardiovascular teams gain the ability to switch between diagnostic scans and intervention without patient transfer, which has reduced average procedure time by 18% at early-adopting centers. The medical pendant market captures incremental revenue through high-capacity load cells and integrated touchscreen controllers tailored to hybrid workflows.

Increased Deployment of Ceiling-Mounted Robotic Systems

Hospitals deploying ceiling-guided robots such as Siemens Ciartic Move cut imaging reposition times by 50%.[3]Siemens Healthineers, “Ciartic Move Robotic C-Arm: Product Brief 2024,” siemens-healthineers.com These installations require pendants that communicate with robotic motion sensors and stop arms automatically to avoid collisions. Leading suppliers embed LiDAR-based spatial mapping and software APIs that sync robot and pendant trajectories. Early results from orthopedic centers in the United States show 12% faster case turnover after pairing robotic imaging with smart pendants. Automated boom control also reduces musculoskeletal strain on surgical staff, aligning with workplace safety metrics that factor into reimbursement calculations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Required for Pendant Systems | -0.7% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Budgetary Constraints and Procurement Delays in Public and Government Hospitals | -0.4% | Global, concentrated in public healthcare systems | Short term (≤ 2 years) |

| Shortage of Trained Biomedical Engineers | -0.5% | Global, acute in North America & EU | Long term (≥ 4 years) |

| Structural Limitations in Older Healthcare Facilities | -0.3% | North America & EU, legacy infrastructure regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Required for Pendant Systems

Equipment budgets account for up to 20% of hospital revenue, and pendant projects often compete with imaging or digital records upgrades for the same funds. Installation can require structural reinforcement costing USD 110,000 per room, raising total project outlays. Flexible financing models help, but emerging facilities still postpone advanced features. To lower barriers, manufacturers now offer subscription-based hardware assurance plans that bundle maintenance, software, and periodic upgrades over five-year terms. Early pilot programs cut upfront cash needs by 50% while locking vendors into long-term partnerships that stabilize revenue projections.

Budgetary Constraints and Procurement Delays in Public and Government Hospitals

Supply chain disruptions left 90% of United States hospitals facing core product shortages in 2024, generating average losses of USD 350,000 for mid-scale systems. Public sector tenders can stretch 18 months beyond private sector timelines because of layered approvals and local content rules. Pendant suppliers reduce sales-cycle risk by pre-configuring product bundles that align with national procurement codes and by setting up regional service depots that satisfy local‐maintenance clauses. Some vendors also partner with multilateral development banks to channel concessional finance toward infrastructure-starved districts, thereby mitigating delay-related revenue erosion in the medical pendant market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Redefines Ceiling Infrastructure

Motorized Pendant systems will expand at 7.78% CAGR to 2031, outpacing fixed-arm models. Demand accelerates as surgical teams prioritize precision and ergonomics that manual units cannot match. Integrated motor drives allow joystick and voice command control, cutting arm reposition time by 70% compared with manual adjustment. The medical pendant market size for Motorized systems reflecting automated workflow adoption across high-acuity procedure rooms.

Fixed Pendant platforms still dominate with 42.26% medical pendant market share in 2025 because legacy hospitals deploy them widely during earlier buildouts. Upgrades focus on retractable gas outlets and modular accessory rails that extend installed life. Single-arm movable units remain popular in emergency bays that handle rapid patient turnover, while double-arm and multi-arm frames gain traction in hybrid ORs managing concurrent imaging and surgical tasks. Accessories such as articulated monitors, surgical light holders, and integrated suction modules constitute a fast-growing revenue pool because health systems can add them without new structural work.

By Application: Emergency & Trauma Outpaces Traditional Surgery

Surgery retained the largest share of application revenues at 33.88% in 2025. Cardiac, neuro, and oncologic surgeries rely on pendant-mounted imaging and anesthesia rails that support complex instrumentation. Even so, Emergency & Trauma lines are poised for 8.61% CAGR as trauma centers upgrade to rapidly configurable ceiling booms.

Endoscopy segments also post solid gains because outpatient GI centers invest in flush-mounted gas outlets and cable management trays that keep hazardous fluids off the floor. Anesthesia stations benefit from pendants with digitally metered gas flow control, improving dosage precision during complex cases. ICUs expand pendant installations to accommodate negative pressure modules and multi-parameter monitors, an approach that reduces nosocomial infection risk by keeping pumps and cables off mobile trolleys.

By End User: Outpatient Models Realign Demand Horizons

Hospitals accounted for 62.10% of global revenues in 2025, due to their scale and procedural diversity. Retrofits dominate this channel as institutions phase out 1990s‐era pendants that lack data ports and automation. Nevertheless, Ambulatory Surgery Centers are projected to log 8.83% CAGR, the fastest within the medical pendant market. Developers of new ASC campuses embed pendants from the blueprint stage, ensuring optimized ceiling clearances and minimal build-out disruption. Medical pendant industry suppliers provide space-saving single-arm motorized units that support orthopedic and ophthalmic procedures within compact theaters.

Specialty clinics focusing on spine, fertility, and pain management display growing interest in modular pendants that can convert consultation rooms into minor procedure suites during peak demand. Other healthcare facilities, including urgent care and diagnostic imaging centers, deploy lightweight pendants to carry 4K monitors and contrast-injector pumps. This spread of users underscores how distributed care models expand overall unit volumes despite slower sales cycles in traditional hospital channels.

Geography Analysis

North America remains the largest regional revenue pool with 31.84% of the medical pendant market in 2025. Hospitals upgrade existing suites to accommodate robotics, advanced visualization, and ESG retrofits that target reduced gas leakage. Federal infrastructure funds under the United States CHIPS and Science Act earmark USD 158 million for medical-device-related facility modernization, a portion of which finances ceiling-mounted systems. Canadian provinces add procurement preferences for antimicrobial finishes and low-carbon materials, prompting suppliers to switch coating chemistry and component sourcing.

Asia-Pacific leads the growth race with a 10.25% CAGR expected through 2031. China’s Healthy China 2030 blueprint mandates smart hospital standards that include IoT-ready ceiling booms in new ORs, driving large tender volumes. Provincial grant schemes reimburse up to 35% of pendant system outlays if units meet domestic content thresholds, encouraging local assembly partnerships. In India, federal tax incentives for tier-2 city health projects accelerate adoption. Southeast Asia follows, as Indonesia and Vietnam push public‐private hospital expansion that specifies integrated pendant rails for imaging and robotic systems.

Europe posts steady but lower single-digit growth as mature markets replace aging stock rather than expand footprint. EU taxonomy rules on sustainable buildings create pull for energy-monitored pendants that integrate consumption dashboards into hospital management systems. Hospitals in Germany and the Nordics sign multi-year service contracts covering remote predictive maintenance, ensuring pendant uptime meets exacting care standards. Southern Europe adopts cost-shared leasing arrangements mediated by regional development banks, enabling resource-limited hospitals to access advanced pendants.

The Middle East & Africa medical pendant market adds capacity as GCC nations build flagship academic medical centers. Qatar’s Sidra and Saudi Arabia’s Vision 2030 health pillars allocate funding for hybrid OR clusters that demand high-load multi-arm pendants. African growth remains modest but accelerates where regional manufacturing hubs in Egypt and South Africa shorten lead times. South America’s modernization trajectory is gaining momentum; Brazil’s health ministry approved USD 2.4 billion for surgical infrastructure upgrades in 2025, which includes pendant retrofits.

Competitive Landscape

The industry remains moderately fragmented. Drägerwerk leverages its EUR 331.1 million R&D expenditure to integrate AI diagnostics into pendant dashboards, offering predictive fault detection that alerts hospital technicians before mechanical failures draeger.com. STERIS bundles decontamination services with pendant sales, closing multi-year service contracts that lock in annuity revenue. Hillrom (now part of Baxter) focuses on ASC-specific motorized booms that support touchless controls, catering to outpatient ergonomic demands.

Regional challengers in China and India deliver cost-optimized pendants priced 25% below global brands but increasingly embed imported sensors to match performance specs. Technology firms like Oxipit and Brainlab integrate imaging analytics and augmented reality overlays that display on pendant-mounted 4K screens, creating software-driven differentiation. Component suppliers add Bluetooth Low Energy modules so pendant arms can broadcast usage data to centralized dashboards. Strategic partnerships dominate over mergers; in late 2024, a leading pendant maker teamed with a cloud analytics firm to co-develop a remote asset-management platform, enabling dashboard consolidation across an entire hospital network within six weeks.

Service capability is emerging as a deciding factor because biomedical engineer shortages threaten uptime. Vendors open regional training academies to certify hospital staff and to streamline maintenance. International tender documents now score bids on remote diagnostic response time, further encouraging telemaintenance. Intensifying competition coupled with rising product complexity is expected to hold average selling prices steady, but higher software subscription fees will lift overall dollar-value per installed arm. The medical pendant market therefore shifts from hardware margin reliance toward blended hardware-software-service models.

Medical Pendant Industry Leaders

Drägerwerk AG & Co. KGaA

Steris Plc

Shenzhen Mindray Bio-Medical Electronics Co., Ltd

BeaconMedaes

Novair Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PieX AI has announced the upcoming launch of a personalised AI-powered mental health pendant, marking a strategic expansion into the digital wellness and wearable healthtech space. The innovative pendant is designed to support users in managing their mental well-being through real-time emotional sensing and adaptive support features. It leverages PieX AI’s proprietary Sensing Technology and advanced foundational AI models to monitor biometric signals and contextual data, enabling discreet, personalized feedback and mental health interventions.

- October 2024: Vocodia has officially expanded its portfolio by entering the medical alert industry with the launch of a cutting-edge emergency response pendant. This strategic move marks a significant milestone in the company’s mission to leverage its artificial intelligence and communication expertise to enhance personal safety technologies. The newly launched pendant offers 24/7 emergency connectivity at the press of a button, enabling instant access to support services during health or safety emergencies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We assess the medical pendant market as all ceiling, wall, or boom-mounted utility supply systems installed in operating rooms, intensive-care units, endoscopy suites, and emergency bays to organize medical gases, electrical power, data, lights, and ancillary equipment. These units are treated as capital equipment and valued in USD at factory gate.

Scope exclusion: Hand-held nurse-call pendants and patient-worn alarm buttons are not counted.

Segmentation Overview

- By Product Type

- Fixed Pendant

- Fixed Retractable Pendant

- Single Arm Movable Pendant

- Double & Multi-Arm Movable Pendant

- Motorized Pendant

- Accessories & Attachments

- By Application

- Surgery

- Endoscopy

- Anesthesia

- Intensive Care Unit

- Emergency & Trauma

- Imaging / Radiology

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Specialty Clinics

- Other Healthcare Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed biomedical engineers, OR managers, ICU directors, and procurement chiefs across North America, Europe, and five key Asia-Pacific economies. These conversations clarified real-world replacement cycles, average selling prices, ceiling-load constraints, and adoption hurdles, allowing us to refine model assumptions and close data gaps flagged during desk work.

Desk Research

Our analysts first gathered baseline signals from open sources such as the World Health Organization's Global Health Expenditure database, OECD hospital bed statistics, U.S. FDA device registrations, Eurostat building permits for hospitals, and national surgical volume registries. Complementary insights flowed from annual reports and 10-Ks of leading pendant manufacturers, tender notices on Tenders Info, import shipment traces on Volza, and trade association briefs (ECRI, JRC). Paid databases, D&B Hoovers for company revenues and Dow Jones Factiva for press flow, helped size vendor footprints and verify pricing bands. This list is illustrative; many other public records and industry notes were mined to cross-check facts.

Market-Sizing & Forecasting

A top-down build starts with surgical and critical-care bed counts by country, multiplies them by pendant penetration rates and replacement intervals, and is then benchmarked against selective bottom-up roll-ups of manufacturer shipments and sampled ASP × volume checks. Key variables include: 1) annual surgical procedures, 2) ICU bed additions, 3) public-hospital capital budgets, 4) hybrid OR installations, and 5) median pendant lifespan. Forecasts to 2030 use a multivariate regression that links unit demand to healthcare CAPEX growth, surgical volume CAGR, and regulatory mandates on medical gas safety. Where bottom-up subtotals deviate beyond ±5%, values are adjusted to the blended mean.

Data Validation & Update Cycle

Before sign-off, results undergo variance scans, peer review, and anomaly resolution. Models refresh every twelve months, with interim updates triggered by material events, such as large tenders and regulatory shifts. A final analyst pass ensures clients receive the most current view.

Why Our Medical Pendant Baseline Commands Reliability

Published numbers often diverge because firms pick different device families, price points, and refresh cadences.

Readers deserve to know these levers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 571.4 M (2025) | Mordor Intelligence | - |

| USD 586 M (2024) | Global Consultancy A | Uses mid-2023 exchange rates and bundles ceiling service booms sold without gas outlets |

| USD 568.9 M (2024) | Industry Association B | Relies on hospital starts but omits ICU retrofits, leading to trimmed base |

| USD 2.02 B (2024) | Trade Journal C | Counts home-care pendant alarms and mobile carts, dramatically widening scope |

The comparison shows that once scope creep and pricing differences are stripped away, our disciplined variable selection and annual refresh yield a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the medical pendant market?

The market is valued at USD 604.14 million in 2026 and is projected to reach USD 798.02 million by 2031 as demand rises for digitally integrated ceiling booms.

Which region leads the medical pendant market and which one grows fastest?

North America holds the largest regional share at 31.84% in 2025, while Asia-Pacific is the fastest-growing region with a 10.25% CAGR expected through 2031.

What segment within the medical pendant market shows the highest growth?

Motorized Pendant systems post the highest product-level CAGR at 7.78% because they support automated, image-guided workflows.

How are outpatient facilities influencing product development?

Ambulatory Surgery Centers grow at 8.83% CAGR and favor compact, motorized designs that fit tight theater spaces and enable rapid turnover.

Why are hybrid operating rooms important for pendant manufacturers?

Hybrid ORs require pendants that integrate imaging, robotics, and data distribution, leading suppliers to launch low-profile multi-arm systems with EMI shielding.

What challenges could slow market expansion?

High capital costs and lengthy public-sector procurement cycles restrain adoption, particularly in emerging economies, although leasing and subscription models are easing this barrier.

Page last updated on: