Healthcare Bioconvergence Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 153.21 Billion |

| Market Size (2030) | USD 220.56 Billion |

| Growth Rate (2025 - 2030) | 7.56% CAGR |

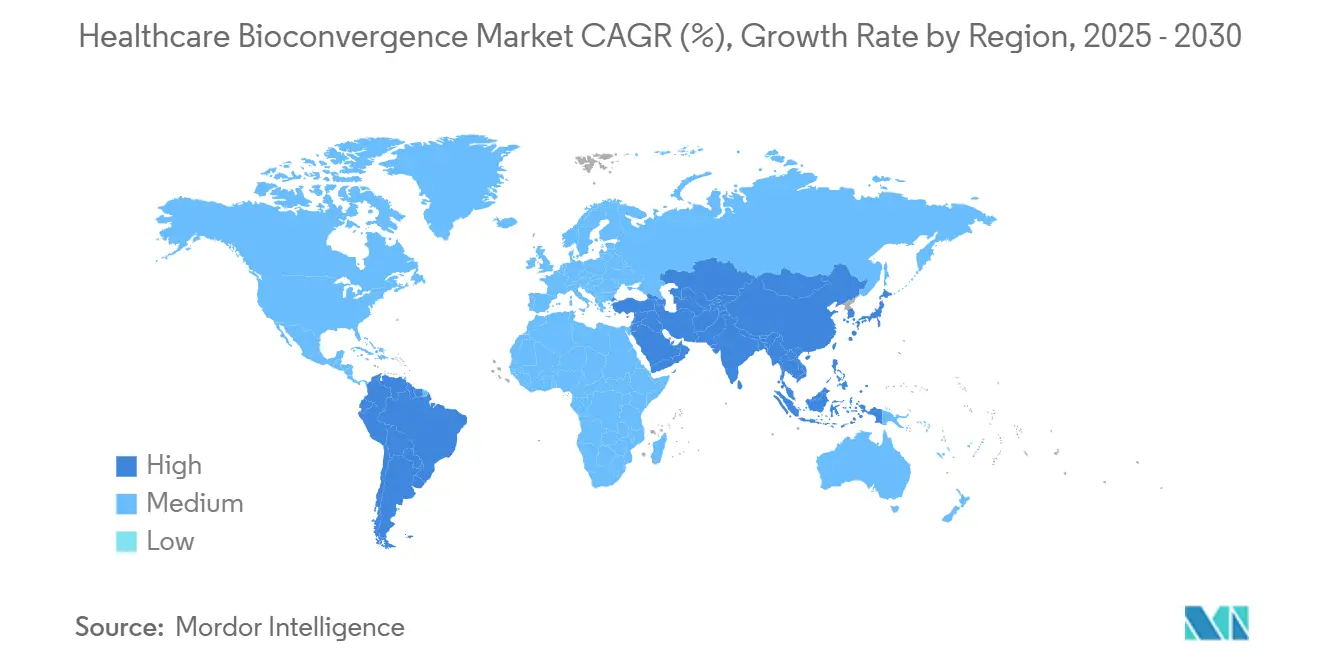

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

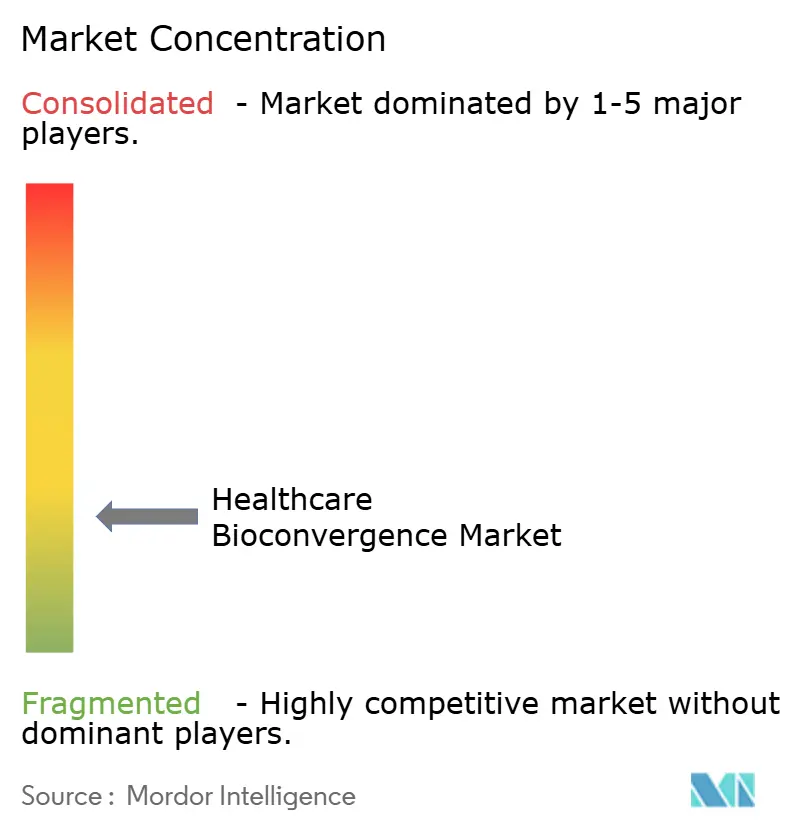

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Bioconvergence Market Analysis by Mordor Intelligence

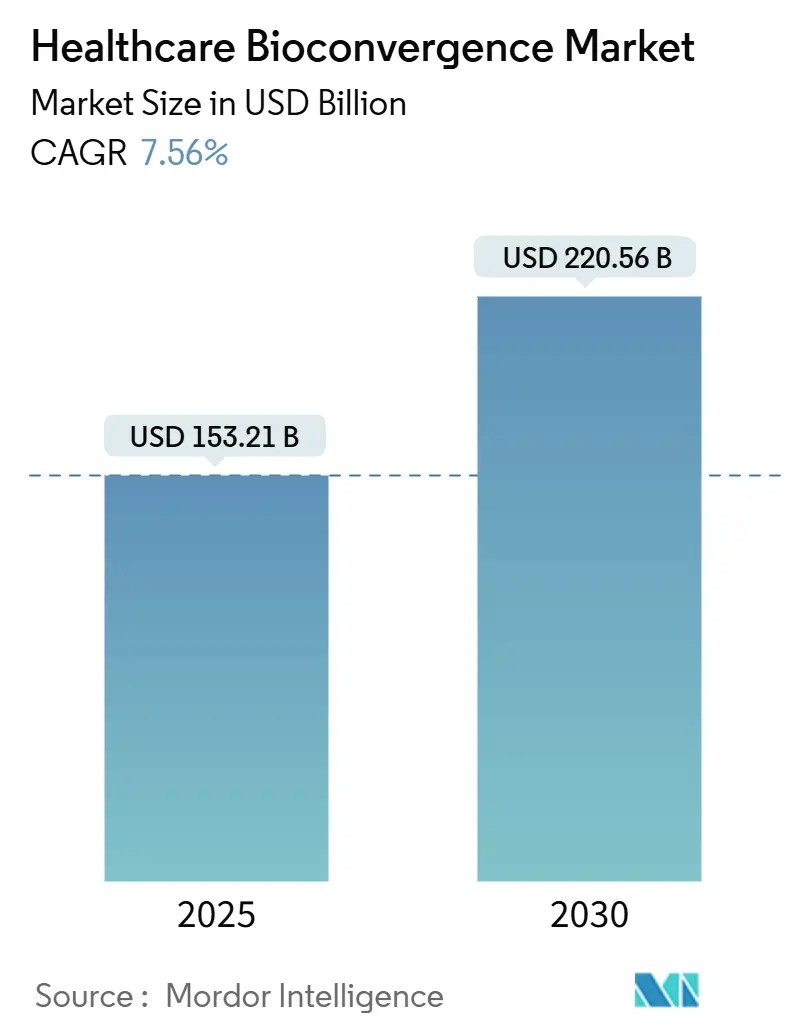

The Healthcare Bioconvergence Market size is estimated at USD 153.21 billion in 2025, and is expected to reach USD 220.56 billion by 2030, at a CAGR of 7.56% during the forecast period (2025-2030).

Rising integration of biological systems with artificial intelligence, nanotechnology, and semiconductor platforms is shortening drug-development timelines and expanding remote-care capabilities. Cross-sector alliances between chipmakers and drug developers are enabling miniature diagnostics, implantable therapeutics, and adaptive software that personalizes dosing in real time. Early regulatory frameworks for combination products, falling costs of 3D bioprinting consumables, and maturing venture-capital support for synthetic biology further strengthen demand. Taken together, these forces position the healthcare bioconvergence market for sustained double-digit annual spending gains in advanced analytics, bioelectronics, and precision medicine infrastructure.

Key Report Takeaways

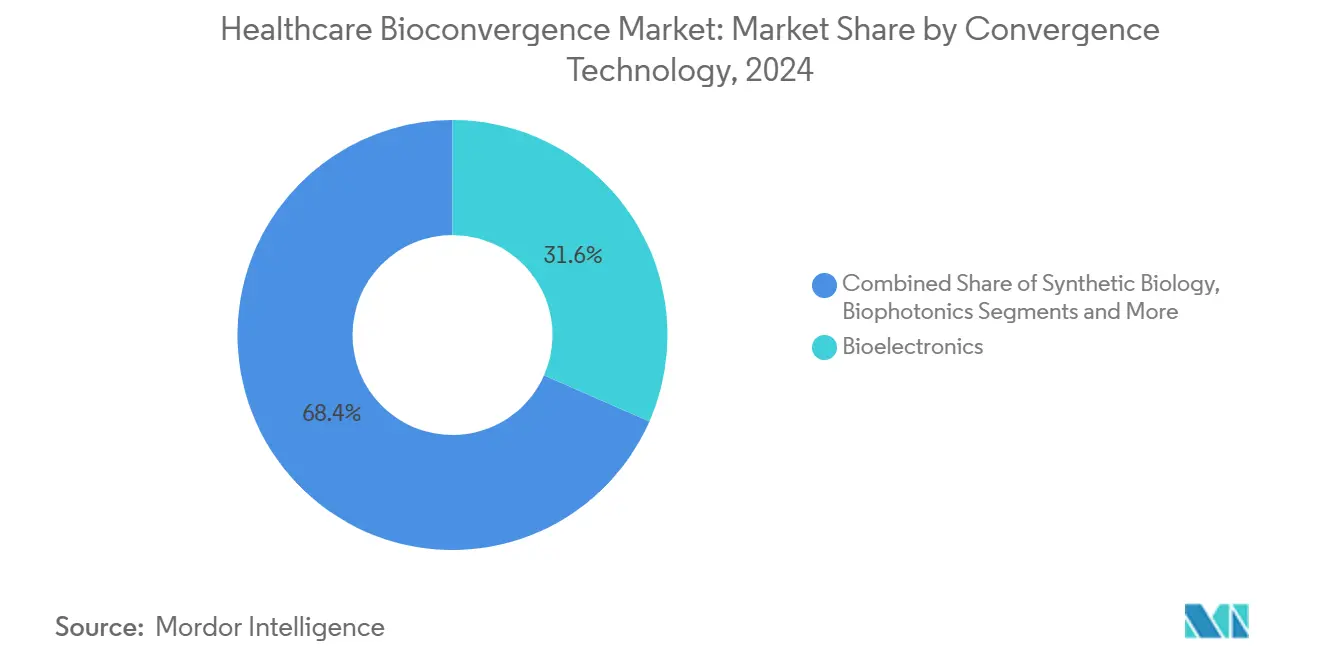

- By convergence technology, bioelectronics held 31.58% of healthcare bioconvergence market share in 2024; 3D bioprinting and tissue engineering are expanding at a 10.37% CAGR through 2030.

- By application, diagnostics and imaging captured 27.88% of the healthcare bioconvergence market size in 2024, while regenerative medicine and tissue engineering lead growth at an 11.38% CAGR to 2030.

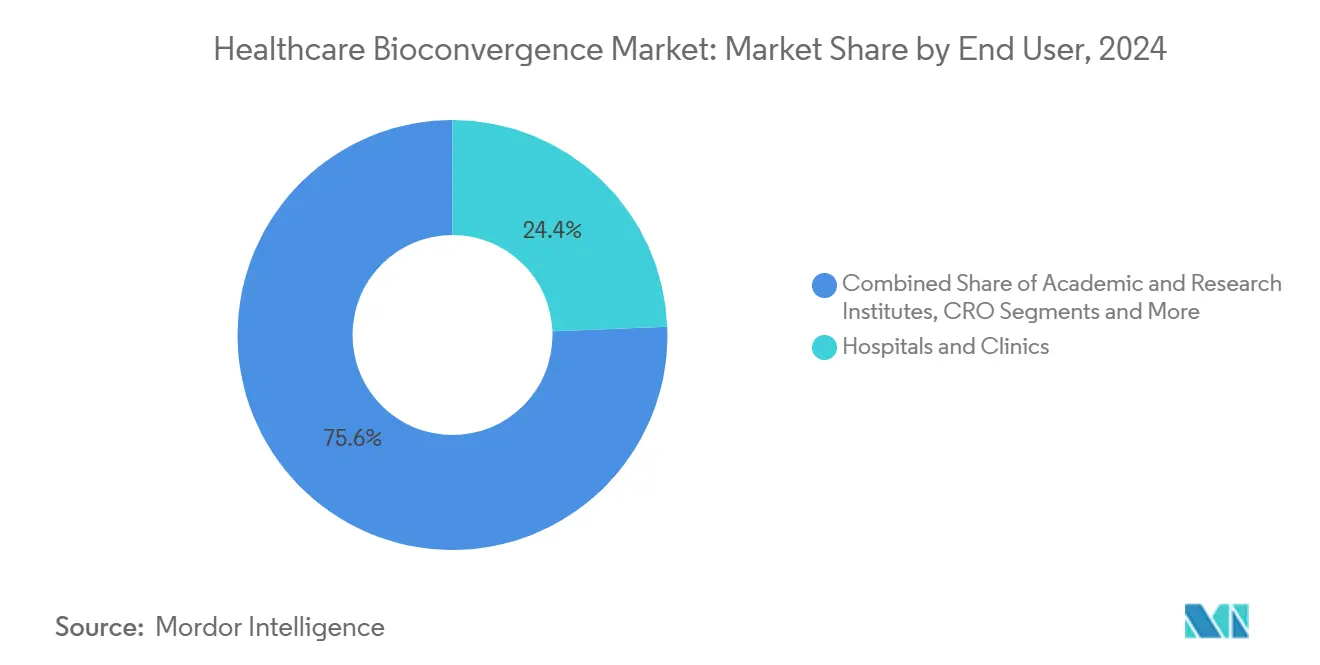

- By end user, hospitals and clinics commanded 24.39% revenue share of the healthcare bioconvergence market size in 2024; digital health and MedTech firms are advancing at an 11.88% CAGR through 2030.

- By therapeutic area, oncology dominated with 41.22% share of the healthcare bioconvergence market size in 2024, whereas neurology registers the fastest expansion at a 9.49% CAGR to 2030.

- By geography, North America accounted for 38.35% of the healthcare bioconvergence market in 2024; Asia-Pacific is projected to post the highest 9.72% CAGR between 2025 and 2030.

Global Healthcare Bioconvergence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic-disease burden | +1.2% | North America, Europe | Long term (≥ 4 years) |

| AI/ML advances for multi-omics analytics | +1.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Scaling precision-medicine programs | +1.1% | North America, Western Europe | Medium term (2-4 years) |

| Increased funding for synthetic biology | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Adoption of organ-on-chip platforms | +0.7% | North America | Medium term (2-4 years) |

| Semiconductor–pharma consortia formation | +0.5% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic-Disease Burden

Greater life expectancy has pushed multimorbidity into mainstream care delivery, and the healthcare bioconvergence market is responding with continuous monitoring integrated to AI therapy engines. Dexcom’s USD 75 million equity in ŌURA brings metabolic data and glucose curves together, allowing physicians to pre-empt acute episodes rather than treat them after presentation.[1]Dexcom Communications, “Dexcom and ŌURA Announce Strategic Partnership,” investors.dexcom.com The U.S. Centers for Disease Control and Prevention stresses that genomic, behavioral, and environmental insights must converge to contain escalating chronic-care costs.[2]Centers for Disease Control and Prevention Staff, “Precision Health: Predict and Prevent Disease,” cdc.gov Bioconvergent platforms coordinate those datasets in real time, unlocking actionable care pathways that single-discipline systems miss.

AI/ML Advances for Multi-Omics Analytics

Drug developers now embed high-performance GPUs into discovery lines so that RNA, protein, and clinical streams can be parsed simultaneously. NVIDIA’s joint work with Illumina and Mayo Clinic illustrates how concurrent analysis uncovers disease signatures invisible to legacy pipelines.[3]NVIDIA, “NVIDIA Partners With Industry Leaders to Advance Genomics, Drug Discovery and Healthcare,” investor.nvidia.com Adaptive dosing software refines protocols during therapy rather than after trials conclude, cutting attrition and cost. Brain–computer interface research under the same architecture informs neurology implants, illustrating the spill-over benefits of shared compute infrastructure.

Scaling Precision-Medicine Programs

Ohio State’s 100,000-participant exome initiative shows that whole-genome projects no longer sit only in research wards.[4]Wexner Medical Center, “Wexner Medical Center and Helix Launch the Largest Precision Health Initiative in Ohio,” wexnermedical.osu.edu Declining sequencing costs and cloud-based decision support extend personalized treatment into community clinics. Illumina and Tempus are broadening panels beyond oncology so that a single assay can triage cardiology, endocrine, and immunology risks simultaneously. Health-system savings arise because disease onset is delayed or avoided, realigning spend from end-stage intervention to prevention.

Increased Funding for Synthetic Biology

Large-ticket mergers signal investor confidence that algorithm-driven cell engineering will outperform legacy R&D. Flagship Pioneering joined with Analog Devices to digitize cellular read-outs using semiconductor sensors, merging biofoundry and fabrication disciplines in one clean-room workflow. Funding now targets multi-modality platforms rather than single-asset biotech, giving them the scale needed to industrialize rapid prototyping of candidate molecules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and infrastructure spend | –0.8% | Global (acute in emerging markets) | Long term (≥ 4 years) |

| Multi-agency regulatory hurdles | –0.6% | North America, Europe | Medium term (2-4 years) |

| Data silos across bio-tech interfaces | –0.4% | Global | Short term (≤ 2 years) |

| Shortage of interdisciplinary talent | –0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High R&D and Infrastructure Spend

A single national bio-convergence lab in Israel cost USD 35.5 million, underscoring the capital intensity of facilities that must meet both sterile-biological and semiconductor-clean-room specifications. Small firms often cannot shoulder dual-discipline payrolls that include molecular biologists, software architects, and MEMS engineers. As a result, incumbents with prior fabrication or biologics footprint enjoy cost advantages that deter greenfield entrants.

Complex Regulatory Pathways

Products that embed living cells with firmware must satisfy drug, device, and often software oversight. The U.S. Food and Drug Administration’s harmonization pilot with European regulators for AI-enabled devices illustrates the multi-agency choreography required before launch. Filing costs escalate, extending break-even points and tempering venture appetite for early-stage convergence ventures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Convergence Technology: Bioelectronics Lead, 3D Bioprinting Rising

Bioelectronics accounted for 31.58% of healthcare bioconvergence market share in 2024 after neuromodulation and continuous-glucose systems secured landmark FDA clearances. SetPoint Medical’s neuro-immune modulator and Carnegie Mellon’s wireless pain implants highlight clinical traction. The healthcare bioconvergence market size for bioelectronics is set to widen as cloud-connected firmware upgrades extend installed-base life cycles. Meanwhile, 3D bioprinting and tissue engineering post a 10.37% CAGR through 2030. Falling hydrogel prices and automated multi-nozzle printers allow batch production of vascularized constructs, which accelerates their transition from lab benches to operating theaters.

Synthetic-biology foundries benefi t from standardized DNA-writing and microfluidic assembly lines, while biophotonics now branches into optogenetic therapy and intraoperative fluorescence-guided surgery. Nano-bio interfaces deliver chemistries across the blood-brain barrier, and smart biomaterials adapt stiffness or drug-release rates in response to local pH. Bio-AI platforms remain the fastest-growing niche as cloud inference motors every data-rich workflow from assay design to post-market vigilance.

By Application: Diagnostics Retain Scale, Regenerative Medicine Surges

Diagnostics and imaging held 27.88% of the healthcare bioconvergence market size in 2024 as AI layering on CT, MRI, and point-of-care devices improved triage accuracy. Regenerative medicine, however, expands at 11.38% CAGR as printed cartilage, liver patches, and cardiac scaffolds move from compassionate-use to standard-of-care pathways. Therapeutic segments—drug delivery and implants—leverage nanocarriers that localize payloads, trimming systemic toxicity.

Precision-medicine services integrate multi-omics dashboards, giving clinicians compendiums of variants, expression signatures, and environmental exposures in one digest. Drug discovery workflows shift toward self-driving labs that iterate compound libraries faster than human cycle times. Wearable and point-of-care devices connect to telehealth nodes, allowing population-scale observation while maintaining individual granularity. Healthcare analytics platforms turn raw streams into risk scores that trigger automated outreach, closing the feedback loop between patient behavior and care plans.

By End User: Hospitals Lead While Digital Health Scales Up

Hospitals and clinics captured 24.39% of healthcare bioconvergence market share in 2024, reflecting their capacity to fund capital-intensive convergence platforms such as AI-assisted robotic surgery suites and multi-omics sequencing pipelines. Their early adoption is reinforced by established surgical workflows, reimbursement familiarity, and in-house clinical-trial infrastructure that validate new devices quickly. Pharmaceutical and biotechnology companies follow as major purchasers, channeling convergence tools into faster drug-candidate screening and adaptive trial designs that improve success rates. Academic and research institutes remain core innovation nodes where interdisciplinary collaborations de-risk proof-of-concept studies before industry uptake. Contract research organizations expand specialized wet-lab and computational services so smaller firms can outsource convergence expertise without buying laboratories outright.

Digital health and MedTech firms post the fastest 11.88% CAGR through 2030 as direct-to-consumer subscription models deliver clinical-grade diagnostics without hospital gatekeeping. Cloud architecture lets these firms iterate firmware and analytics remotely, converting installed wearables into recurring-revenue ecosystems. Cross-licensing deals with established providers grant access to longitudinal electronic-medical-record data, sharpening algorithm accuracy and easing regulatory review. Venture investors favor this asset-light path, pushing capital toward platforms that bundle hardware, software, and continuous coaching in a single monthly fee. As competitive lines blur, hospitals increasingly partner with digital entrants to extend care beyond the facility and to defend share against non-traditional providers.

By Therapeutic Area: Oncology Dominates as Neurology Accelerates

Oncology accounted for 41.22% of healthcare bioconvergence market share in 2024, powered by tumor-agnostic genomic panels, adaptive immunotherapies, and AI-guided radiology that personalize regimens in real time. Real-world outcome data feed learning systems that refine dosing between treatment cycles, raising response rates and reducing adverse events. The segment benefits from rich funding, clear biomarker endpoints, and accelerated approval pathways that recognize convergence innovations such as bioelectronic drug-delivery implants. Commercial momentum in oncology also seeds technology spill-over into adjacent disease areas, creating economies of scope that reinforce scale advantages.

Neurology records the quickest 9.49% CAGR to 2030 as closed-loop brain-computer interfaces, AI-scored electroencephalograms, and targeted neuro-stimulation move from experimental use to routine clinical deployment. Early detection platforms identify neurodegenerative changes years before symptom onset, expanding therapeutic windows and shifting spend toward prevention. Cardiovascular programs integrate continuous hemodynamic monitoring with dose-adjusting pumps, while metabolic applications pair glucose data with behavioral nudges to curb disease progression. Infectious disease analytics leverage rapid diagnostics and cloud epidemiology for outbreak containment, and immunology harnesses vagus-nerve modulation to manage systemic inflammation. Collectively, these advances diversify revenue streams and cushion the market against volatility in any single therapeutic field.

Geography Analysis

North America’s 38.35% share of the healthcare bioconvergence market reflects a virtuous circle of venture capital, academic-industry consortia, and the FDA’s agile review pathways. NVIDIA’s collaborations with life-science majors exemplify how Silicon Valley compute joins East-Coast pharma to prototype AI-guided therapeutics inside a single jurisdiction. Mayo Clinic pilots bring these prototypes into frontline care, creating a feedback loop that fine-tunes algorithms in real time. High compliance costs, however, inhibit smaller entrants, tilting innovation weight toward well-funded incumbents.

Asia-Pacific records the fastest 9.72% CAGR through 2030. National precision-medicine roadmaps in China, semiconductor-biomedical programs in Taiwan, and Japan’s elder-care needs all converge to drive adoption. The region’s contract-manufacturing base in electronics supplies cost-effective biosensor chips, and rising healthcare budgets allow tier-one hospitals to install convergence platforms. India’s software talent underpins a burgeoning export sector in AI diagnostics, widening the global footprint of Asia-born solutions.

Europe blends medical-device heritage with avant-garde genomics. Cross-border data-sharing frameworks ease multicenter trials; Sweden’s PROMISE program sets a template for nationwide omics repositories. Fragmented payer systems slow uniform rollout, yet stable reimbursement rules in Northern Europe provide predictable cash flows for capital equipment. Local champions in precision engineering supply nano-patterned scaffolds and photonics components for continental projects.

Competitive Landscape

The healthcare bioconvergence industry shows moderate concentration. Top players pair computational heft with wet-lab assets, locking in know-how that startups struggle to replicate. Johnson & Johnson’s VIRTUGUIDE AI for spine surgery exemplifies an incumbent blending robotics, imaging, and cloud inference into a platform suite. Dexcom’s minority stake in ŌURA shows device specialists broadening into holistic monitoring ecosystems.

Analog Devices and Flagship’s venture into digitized biology demonstrates how component suppliers move upstream to capture value in therapeutic decision loops. M&A remains the mechanism of choice to bolt deep-tech onto pharma pipelines, suggesting that deal flow will stay active as valuations favor acquirers with balance-sheet firepower.

Healthcare Bioconvergence Industry Leaders

Johnson & Johnson

Medtronic plc

Siemens Healthineers AG

GE Healthcare Technologies Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: iRhythm and Lucem Health partnered to enhance arrhythmia detection through predictive AI technology, demonstrating the integration of cardiovascular monitoring with machine learning algorithms for improved diagnostic accuracy.

- July 2025: Progyny partnered with ŌURA to empower women's health through wearable data and personalized insights, expanding bioconvergence applications into reproductive health monitoring and management.

- July 2025: Trinity Biotech unveiled CGM+, an AI-native wearable biosensor for holistic health monitoring, representing advancement in continuous glucose monitoring integrated with artificial intelligence capabilities.

- June 2025: NVIDIA partnered with Novo Nordisk and DCAI to advance drug discovery through AI, utilizing the Gefion supercomputer for creating customized AI models to support early research and clinical development, representing a significant convergence of semiconductor and pharmaceutical capabilities.

Global Healthcare Bioconvergence Market Report Scope

| Bioelectronics |

| Synthetic Biology |

| Biophotonics |

| Nano-bio Interfaces |

| 3D Bioprinting & Tissue Engineering |

| Smart Biomaterials |

| Bio-AI Platforms |

| Diagnostics & Imaging |

| Therapeutics (Drug Delivery & Implants) |

| Precision & Personalized Medicine |

| Regenerative Medicine & Tissue Engineering |

| Drug Discovery & Development |

| Wearable & Point-of-Care Devices |

| Healthcare Analytics & Decision Support |

| Hospitals & Clinics |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Digital Health & MedTech Firms |

| Contract Research Organizations (CROs) |

| Oncology |

| Neurology |

| Cardiovascular Diseases |

| Metabolic Disorders (Diabetes & Obesity) |

| Infectious Diseases |

| Immunology & Inflammation |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Convergence Technology | Bioelectronics | |

| Synthetic Biology | ||

| Biophotonics | ||

| Nano-bio Interfaces | ||

| 3D Bioprinting & Tissue Engineering | ||

| Smart Biomaterials | ||

| Bio-AI Platforms | ||

| By Application | Diagnostics & Imaging | |

| Therapeutics (Drug Delivery & Implants) | ||

| Precision & Personalized Medicine | ||

| Regenerative Medicine & Tissue Engineering | ||

| Drug Discovery & Development | ||

| Wearable & Point-of-Care Devices | ||

| Healthcare Analytics & Decision Support | ||

| By End User | Hospitals & Clinics | |

| Pharmaceutical & Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Digital Health & MedTech Firms | ||

| Contract Research Organizations (CROs) | ||

| By Therapeutic Area | Oncology | |

| Neurology | ||

| Cardiovascular Diseases | ||

| Metabolic Disorders (Diabetes & Obesity) | ||

| Infectious Diseases | ||

| Immunology & Inflammation | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the healthcare bioconvergence market in 2025?

The healthcare bioconvergence market size is valued at USD 153.21 billion in 2025.

Which convergence technology leads current revenues?

Bioelectronics leads, accounting for 31.58% of healthcare bioconvergence market share in 2024.

Which region is growing the fastest through 2030?

Asia-Pacific posts the highest CAGR at 9.72% thanks to policy support and semiconductor capacity.

What segment is projected to expand the most by application?

Regenerative medicine and tissue engineering show the fastest application-level CAGR at 11.38% to 2030.

What is the main barrier to wider adoption?

High dual-discipline R&D and facility costs remain the primary restraint, subtracting an estimated 0.8% from CAGR forecasts.

Page last updated on: