Medical Linear Accelerator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

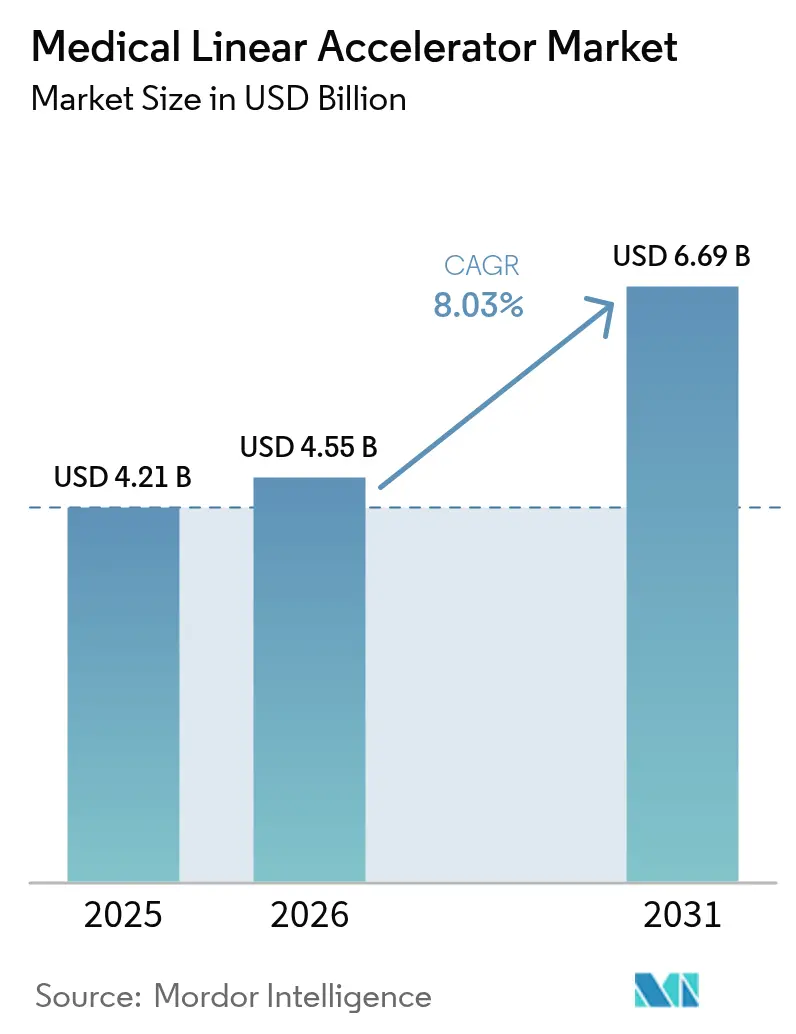

| Market Size (2026) | USD 4.55 Billion |

| Market Size (2031) | USD 6.69 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Linear Accelerator Market Analysis by Mordor Intelligence

The medical linear accelerator market size was valued at USD 4.21 billion in 2025 and estimated to grow from USD 4.55 billion in 2026 to reach USD 6.69 billion by 2031, at a CAGR of 8.03% during the forecast period (2026-2031). Accelerated adoption of FLASH-RT, AI-driven adaptive systems and MRI-guided platforms is redefining treatment precision, shortening care pathways and broadening the addressable patient pool. Rising global cancer incidence, structured government replacement programs and the commercialization of next-generation LINACs continue to draw capital into the medical linear accelerator market, while disruptive entrants such as biology-guided radiotherapy vendors create competitive tension. At the same time, component-level supply constraints and workforce shortages temper near-term installation rates, pushing vendors to automate workflows and integrate service resiliency. Growth opportunities surface most visibly in Asia-Pacific, where greenfield installations outpace mature-market replacement cycles, and in decentralized care networks where compact LINACs bring high-end therapy into community settings.

Key Report Takeaways

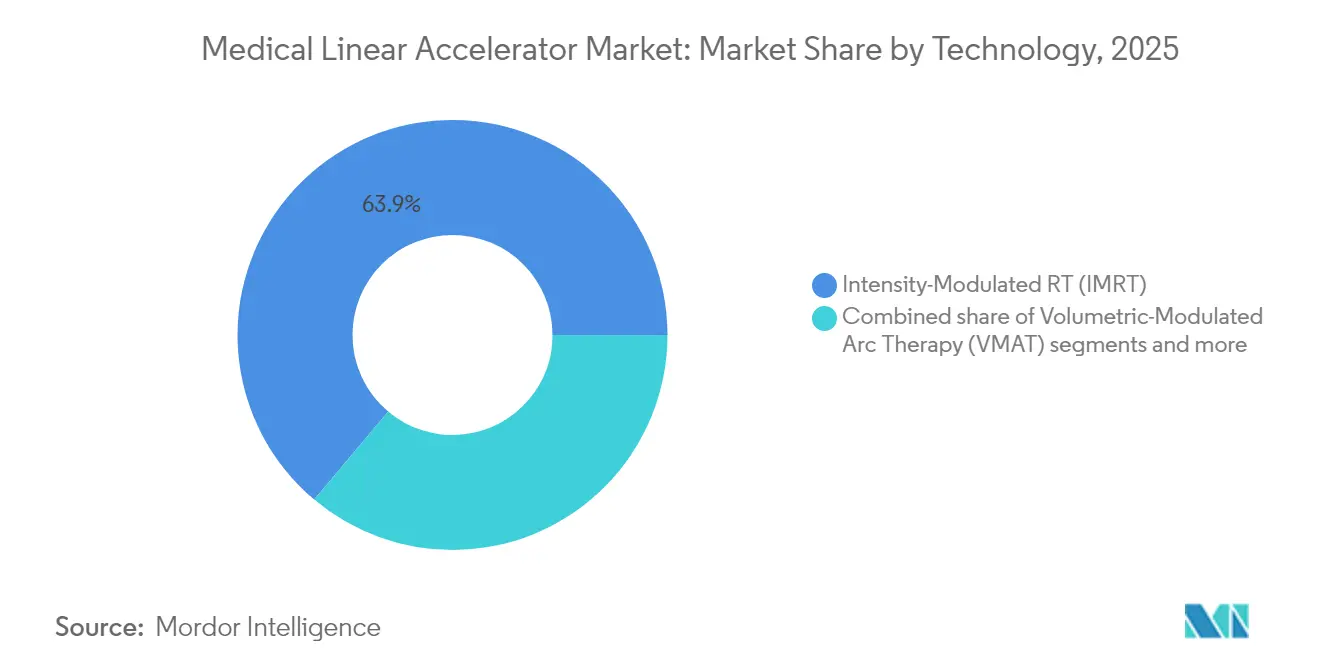

By technology, Intensity-Modulated RT held 64.53% of medical linear accelerator market share in 2024, whereas Volumetric-Modulated Arc Therapy is advancing at an 8.19% CAGR through 2030.

By application, breast cancer captured 83.12% share of the medical linear accelerator market size in 2024, while lung cancer is projected to expand at an 8.78% CAGR between 2025 and 2030.

By energy type, High-Energy systems (6-15 MeV) commanded 72.56% share of the medical linear accelerator market size in 2024; Very-High Energy platforms are set to grow at a 9.01% CAGR to 2030.

By modality, Photon-based LINACs accounted for 71.23% medical linear accelerator market share in 2024, while MRI-guided systems pace ahead at an 8.96% CAGR through 2030.

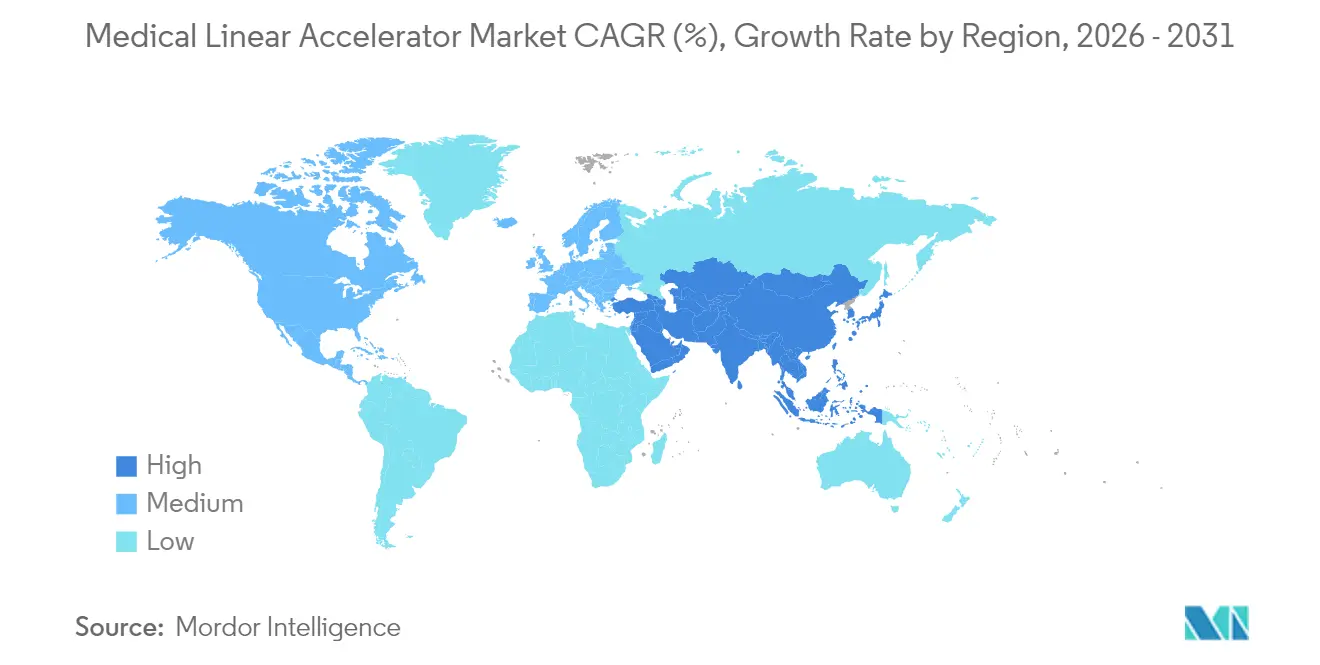

North America led with 39.23% revenue contribution in 2024; Asia-Pacific registers the fastest regional CAGR at 9.23% to 2030

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Linear Accelerator Market Trends and Insights

Driver Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global cancer incidence | +1.8% | Global, with highest impact in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Rapid adoption of AI-enabled adaptive radiotherapy | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Government funding & equipment replacement cycles | +1.5% | Global, with concentrated impact in UK, Australia, Canada | Short term (≤ 2 years) |

| Expansion of radiotherapy capacity in emerging economies | +1.0% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Commercialization of FLASH-RT-ready LINAC platforms | +0.9% | North America & EU, early adoption centers | Medium term (2-4 years) |

| Growth of compact LINACs for decentralized cancer care | +0.7% | Global, with emphasis on rural and underserved regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Incidence

Global cancer cases are forecast to rise 42% by 2040, with 70% occurring in low- and middle-income nations where radiotherapy access remains severely constrained. Current penetration stands at roughly 380 LINACs for 1.2 billion Africans versus nearly 4,000 units for 331 million Americans, underscoring the inequity driving sustained demand in the medical linear accelerator market. International agencies now frame radiotherapy equipment as a core intervention, pivoting investment priorities in emerging economies from replacement to greenfield installation. This demographic pressure underpins the long-term expansion profile of the medical linear accelerator market.

Rapid Adoption of AI-Enabled Adaptive Radiotherapy

AI now automates contouring, planning and on-table adaptation, cutting planning times by up to 70% and helping offset workforce gaps. Systems such as Elekta’s adaptive CT-LINAC adjust beam parameters in real time to anatomical change, boosting dose conformity and sparing healthy tissue. These performance gains fuel premium-priced upgrades and reinforce the value proposition of next-generation platforms within the medical linear accelerator market.

Government Funding & Equipment Replacement Cycles

Targeted funding programs accelerate modernization. The UK’s GBP 130 million Radiotherapy Modernisation Fund replaced more than 100 aging systems and shaved GBP 17.1 million via bulk purchasing. Australia’s scheme reimburses up to USD 3 million per LINAC over 8-10 years, ensuring predictable market pull. These policies stabilize ordering cycles and stimulate early adoption of capabilities such as MRI guidance and FLASH readiness.

Expansion of Radiotherapy Capacity in Emerging Economies

China’s 2021–2035 medical isotope plan aims to double domestic scale, channeling budget toward LINAC procurement and isotope production. Taiwan now hosts eight proton-therapy centers for 23 million residents, illustrating advanced technology uptake yet highlighting residual wait-list pressures. Similar deficits in India and sub-Saharan Africa propel multi-year growth prospects for the medical linear accelerator market

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs | -1.4% | Global, with highest impact in emerging markets and smaller facilities | Long term (≥ 4 years) |

| Shortage of trained radiation-oncology workforce | -1.1% | Global, with acute shortages in North America and Europe | Medium term (2-4 years) |

| Lengthy regulatory & reimbursement approval timelines | -0.8% | North America & EU, with spillover effects globally | Medium term (2-4 years) |

| RF-component supply-chain disruptions for klystrons | -0.6% | Global, with concentrated impact on high-energy systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs

Purchase prices exceed USD 4 million and annual service can top 10% of capital outlay, peaking near year seven. These economics limit early replacement appetite and complicate uptake in low-resource settings, restraining the medical linear accelerator market despite demonstrable clinical need.

Shortage of Trained Radiation-Oncology Workforce

Vacancy rates among radiation therapists climbed to 10.7% in 2022 and are projected to worsen, while dosimetrist shortfalls may reach 50 per year by 2035. Skills scarcity creates bottlenecks even where capital equipment is available, capping capacity expansion within the medical linear accelerator marke

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: IMRT Dominance Faces VMAT Acceleration

Intensity-Modulated RT led the medical linear accelerator market size with USD 2.69 billion in 2025. The segment benefits from entrenched reimbursement frameworks and robust clinical evidence, securing routine use across breast, prostate and head-and-neck protocols. Yet IMRT’s position is gradually eroded by VMAT, whose rotational dose delivery cuts treatment time to 2–4 minutes, easing throughput pressures. VMAT posted an 8.10% CAGR outlook to 2031, outpacing the overall medical linear accelerator market.

Emerging sub-technologies, including image-guided RT and stereotactic SRS/SBRT, grow on the strength of hypo-fractionated regimens that align with patient convenience and workforce optimization. Rapid progress in FLASH-RT and biology-guided systems represents the next curve, but regulatory and evidence hurdles keep their aggregate revenue share below 3% through 2025. Vendor portfolios thus straddle legacy volumes from IMRT while investing in VMAT software upgrades and adaptive workflows.

By Application: Breast Cancer Leadership Challenged by Lung Innovation

Breast cancer therapy represented USD 3.46 billion of the medical linear accelerator market size in 2025, fueled by high disease prevalence and standardized fractionation schedules. Deep-inspiration breath-hold techniques, now integrated into LINAC software, further entrench adoption. Nonetheless, lung cancer revenues climb fastest at an 8.69% CAGR, propelled by the need for ultra-precise dose sculpting around mobile thoracic structures.

Biology-guided radiotherapy, cleared for lung and bone applications, synchronizes beam delivery to tumor PET emissions, expanding re-irradiation and Stage IV indications. Prostate workflows leverage MRI guidance to spare surrounding organs, with adaptive planning reducing toxicity. Colorectal and head-and-neck treatments continue steady uptake as hypofractionation models gain payor acceptance. Across categories, reimbursement alignment increasingly prizes technologies that reduce total fractions, a trend that benefits the medical linear accelerator market.

By Energy Type: High-Energy Systems Face Very-High Disruption

High-Energy (6-15 MeV) configurations retain 72.02% of the medical linear accelerator market share, preferred for their versatility across deep-seated tumors without excessive neutron contamination. Yet Very-High Energy Electron (VHEE) research demonstrates superior depth-dose profiles for FLASH, and commercial prototypes above 15 MeV project a 8.88% CAGR.

Manufacturers now offer multi-energy heads within single gantries, providing institutions a future-proof path as treatment protocols evolve. Low-Energy units (<6 MeV) persist for superficial lesions and intra-operative settings, though their revenue share inches downward. Overall, energy flexibility becomes a selling point, especially in capital-constrained health systems seeking long asset lifetimes inside the medical linear accelerator market.

By Modality: Photon Dominance Meets MRI-Guided Innovation

Photon-based systems commanded 70.75% of 2025 revenue, covering the broadest spectrum of treatment sites and supporting established quality-assurance processes. MRI-guided LINACs, however, delivered an 8.84% CAGR, building momentum via real-time imaging that eliminates CT setup margins and enables daily adaptation.

Electron machines address niche uses such as total-skin therapy, while adaptive RT suites integrate AI engines with cone-beam CT to approximate MRI performance at lower cost. FLASH-ready designs emerge as vendors retrofit gun assemblies and beamlines to achieve dose-rates above 40 Gy/s. Institutions now weigh the incremental cost of MRI coils and shielding against toxicity reductions, shaping procurement criteria across the medical linear accelerator market.

Geography Analysis

North America maintains 38.88% market share in 2025, supported by robust healthcare infrastructure, favorable reimbursement frameworks, and early adoption of breakthrough technologies including AI-powered adaptive systems and biology-guided radiotherapy. The region benefits from substantial government investments, exemplified by the UK's £70 million radiotherapy equipment program and Canada's equipment replacement initiatives that modernize aging LINAC fleets while expanding treatment capacity. However, Asia-Pacific emerges as the fastest-growing region at 9.08% CAGR through 2031, driven by healthcare infrastructure expansion, rising cancer incidence, and government-supported technology adoption programs.

Europe demonstrates steady growth through coordinated healthcare modernization programs and regulatory harmonization initiatives that facilitate technology adoption across member states. The region's emphasis on MRI-guided systems and adaptive radiotherapy reflects its leadership in precision oncology research and clinical implementation. South America shows emerging potential through targeted investments in cancer care infrastructure, while Middle East and Africa regions experience growth driven by healthcare system development and international technology transfer programs. China's nuclear medicine expansion, supported by the 2021-2035 development plan targeting industry scale doubling, exemplifies Asia-Pacific's commitment to advanced cancer treatment capabilities. Taiwan's achievement of the world's highest particle therapy facility density demonstrates the region's technological sophistication, though operational challenges including patient waitlists highlight the need for continued capacity expansion to meet growing demand.

Competitive Landscape

The top five vendors account for half of of global revenue, yielding a moderate concentration profile within the medical linear accelerator market. Siemens Healthineers’ 2024 acquisition of Varian created a portfolio spanning conventional LINACs to proton therapy, unlocking EUR 300 million in annual synergies and strengthening integrated service offerings. Elekta answers via AI-powered adaptive CT-LINAC innovations and sizable emerging-market tenders, while Accuray exploits a focused strategy around precision SRS platforms.

RefleXion introduces biology-guided radiotherapy, winning FDA clearance and raising USD 105 million to scale production. The start-up’s SCINTIX mode challenges legacy paradigms by tethering dose delivery to tumor biology rather than anatomy. ViewRay’s bankruptcy illustrates capital intensity hurdles; yet its IP may catalyze consolidation as larger players seek MRI competencies. Supply-chain resilience, especially for klystrons and high-precision bearings, increasingly influences vendor selection, with dual-sourcing and predictive maintenance emerging as differentiators.

Customer buying criteria coalesce around adaptability, AI automation and service uptime. Vendors bundle software licenses and training to offset workforce gaps, while managed-equipment services convert capex to opex. In developing markets, compact units paired with turnkey bunker solutions appeal to hospital networks expanding outside tier-one cities. Overall, competition centers on delivering clinical efficacy, operational efficiency and economic flexibility inside the medical linear accelerator market.

Medical Linear Accelerator Industry Leaders

-

Accuray Inc.

-

Shinva Medical Instruments Co. Ltd.

-

Elekta

-

ViewRay, Inc.

-

Panacea Medical Technologies Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Salem Health filed a lawsuit against RefleXion over a USD 6.4 million radiation machine that allegedly performed worse than older equipment, with the company admitting in December 2024 that the technology was not ready for clinical deployment.

- May 2025: Hartford HealthCare opened the Fairfield Cancer Center featuring Connecticut's first Varian Ethos Radiation Therapy System with Adaptive Intelligence capabilities, demonstrating continued expansion of AI-powered adaptive radiotherapy platforms in clinical practice

Global Medical Linear Accelerator Market Report Scope

As per the report's scope, a medical linear accelerator uses high-energy X-rays and takes the shape of a tumor to destroy it while leaving healthy cells. It is commonly used in external radiotherapy.

The Medical Linear Accelerator Market is Segmented by Product Type, Treatment Type, and Geography. The market is segmented as dedicated linear accelerator and non-dedicated linear accelerator based on product type. Based on treatment type the market is segmented into, intensity-modulated radiation therapy, volumetric modulated arc therapy, image-guided radiation therapy, and stereotactic radiosurgery/stereotactic body radiotherapy. The report also covers the market sizes and forecasts for the medical linear accelerator market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Intensity-Modulated RT (IMRT) |

| Volumetric-Modulated Arc Therapy (VMAT) |

| Image-Guided RT (IGRT) |

| Stereotactic SRS/SBRT |

| Others |

| Breast Cancer |

| Lung Cancer |

| Prostate Cancer |

| Colorectal Cancer |

| Head & Neck Cancer |

| Other Cancers |

| Low-Energy (<6 MeV) |

| High-Energy (6–15 MeV) |

| Very-High Energy (>15 MeV) |

| Photon-based LINAC |

| Electron-based LINAC |

| MRI-guided LINAC |

| Adaptive RT Systems |

| FLASH-ready LINAC |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology (Value, USD Million) | Intensity-Modulated RT (IMRT) | |

| Volumetric-Modulated Arc Therapy (VMAT) | ||

| Image-Guided RT (IGRT) | ||

| Stereotactic SRS/SBRT | ||

| Others | ||

| By Application (Value, USD Million) | Breast Cancer | |

| Lung Cancer | ||

| Prostate Cancer | ||

| Colorectal Cancer | ||

| Head & Neck Cancer | ||

| Other Cancers | ||

| By Energy Type (Value, USD Million) | Low-Energy (<6 MeV) | |

| High-Energy (6–15 MeV) | ||

| Very-High Energy (>15 MeV) | ||

| By Modality (Value, USD Million) | Photon-based LINAC | |

| Electron-based LINAC | ||

| MRI-guided LINAC | ||

| Adaptive RT Systems | ||

| FLASH-ready LINAC | ||

| By Geography (Value, USD Million) | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the medical linear accelerator market?

The medical linear accelerator market size is USD 4.55 billion in 2026.

How fast is the market expected to grow through 2031?

Revenue is projected to rise at an 8.03% CAGR, reaching USD 6.69 billion by 2031.

Which technology segment is growing the quickest?

Volumetric-Modulated Arc Therapy is forecast to expand at an 8.10% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Rising cancer incidence, government investment in treatment infrastructure and bulk procurement programs drive a 9.08% CAGR in Asia-Pacific installations.

What bottlenecks could limit adoption of new LINACs?

High capital costs, klystron supply-chain constraints and shortages of trained radiation-oncology professionals can slow deployment despite strong demand.

How are vendors addressing workforce shortages?

Vendors integrate AI-enabled adaptive planning and service bundles that automate routine tasks, reduce planning time and provide remote support to offset staffing gaps.

Page last updated on: