Interstitial Cystitis Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.46 Billion |

| Market Size (2030) | USD 1.92 Billion |

| Growth Rate (2025 - 2030) | 5.59% CAGR |

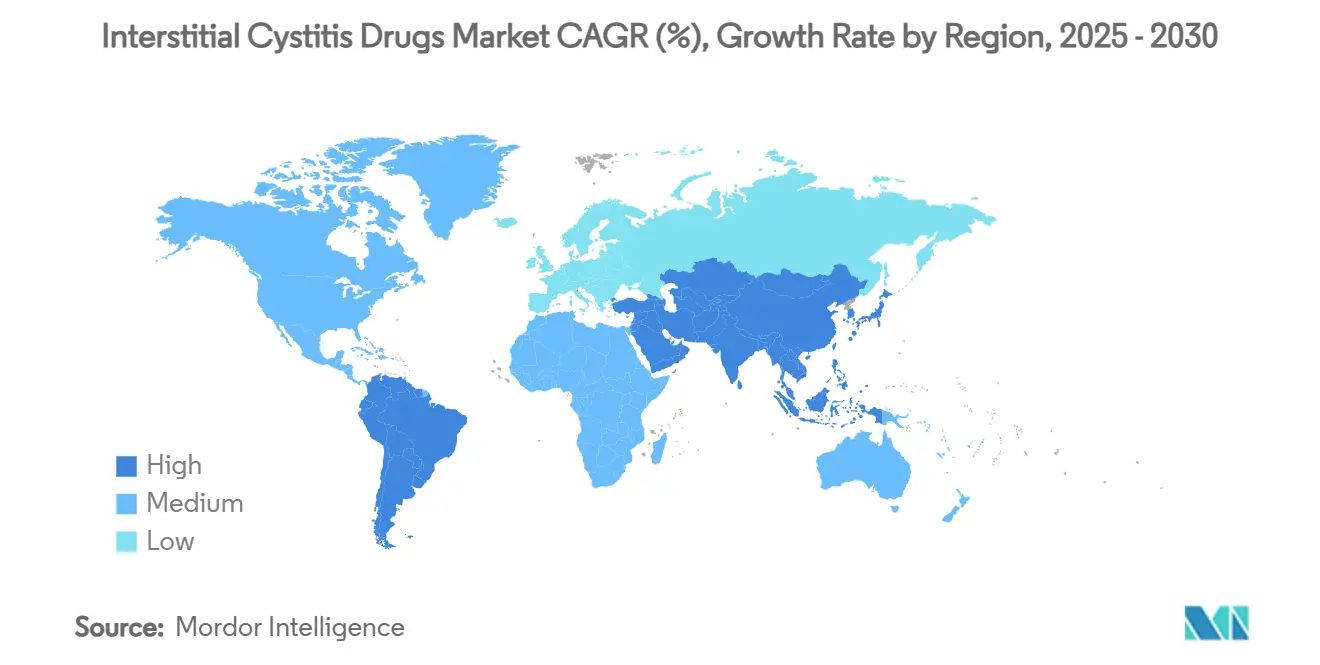

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

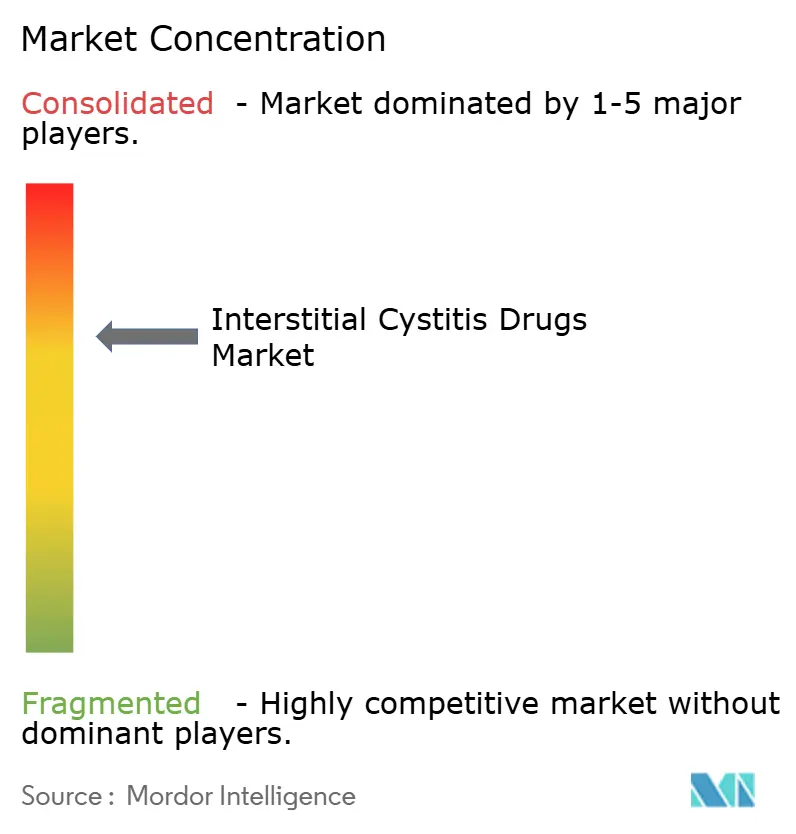

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interstitial Cystitis Drugs Market Analysis by Mordor Intelligence

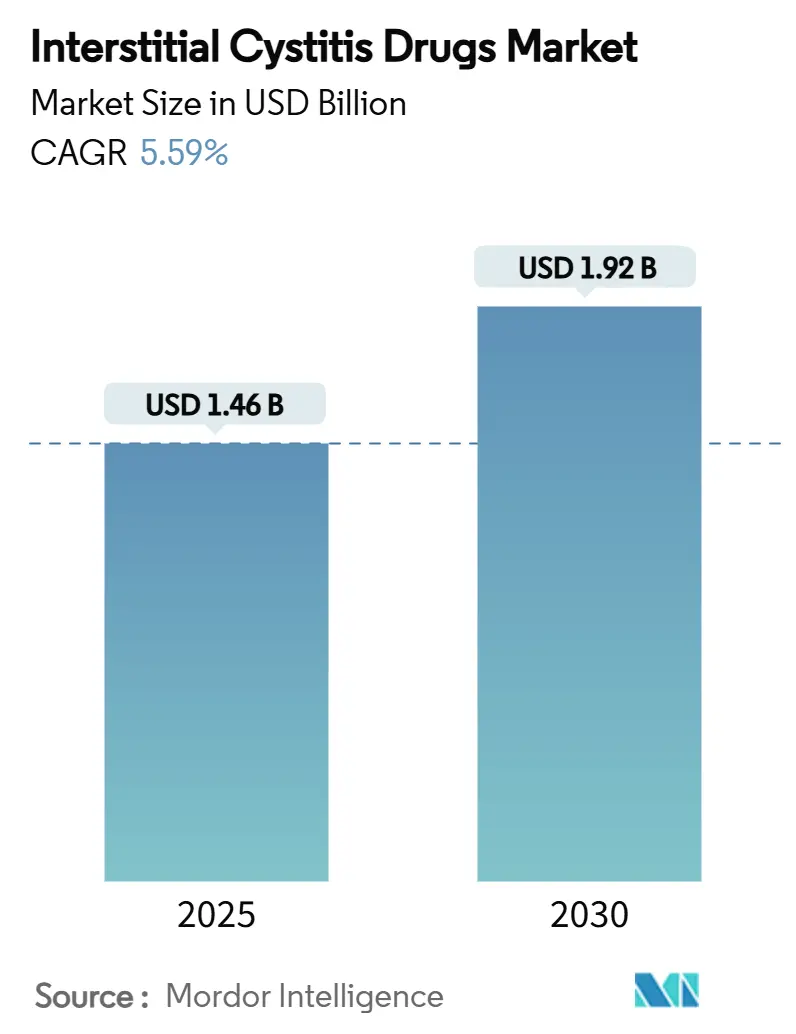

The interstitial cystitis drugs market size is USD 1.46 billion in 2025 and is forecast to reach USD 1.92 billion in 2030, advancing at a 5.59% CAGR over the period. The expansion reflects broader diagnostic recognition of interstitial cystitis/bladder pain syndrome (IC/BPS), deeper penetration of biomarker-guided protocols, and steadily improving reimbursement for novel intravesical formulations. Oral therapies remain the first-line option for most patients, yet mounting safety alerts around pentosan polysulfate are accelerating clinical interest in alternatives that deliver agents directly to the bladder. Neuromodulator research demonstrates meaningful pain reduction, encouraging a shift away from sole symptom suppression toward therapies that correct urothelial barrier failure and dysregulated neural signaling.[1]Tadeja Kuret, “Matched Serum- and Urine-Derived Biomarkers of Interstitial Cystitis/Bladder Pain Syndrome,” PLoS ONE, journals.plos.org Regionally, North America leads adoption thanks to early-stage clinical infrastructure, while Asia-Pacific is moving fastest as Japan and South Korea approve intravesical dimethyl sulfoxide and expand urology specialty capacity. The competitive field remains fragmented; however, large pharmaceutical companies are scouting acquisitions that provide proprietary devices or polymer platforms able to prolong drug residence time in the bladder.

Key Report Takeaways

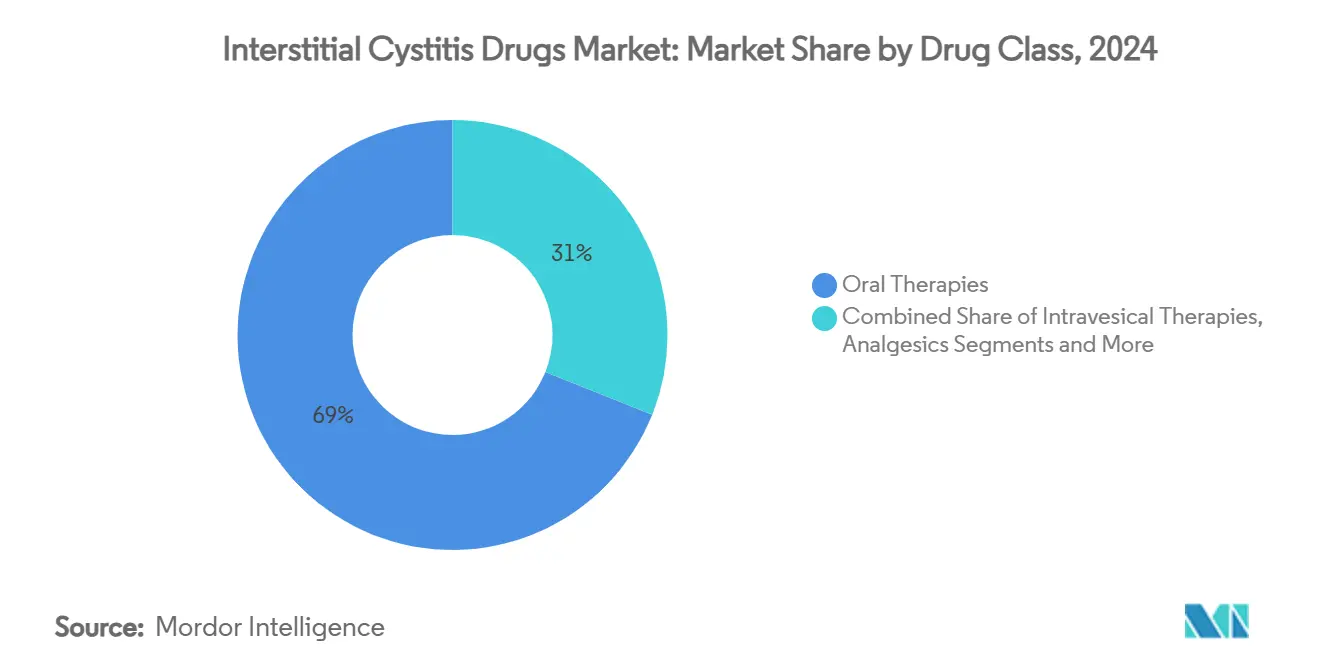

- By drug class, oral therapies held 68.96% of interstitial cystitis drugs market share in 2024, whereas intravesical therapies are projected to post the fastest 8.48% CAGR to 2030.

- By route of administration, oral products captured 72.34% revenue in 2024, while intravesical systems are forecast to expand at 8.62% CAGR through 2030.

- By formulation type, capsules and tablets accounted for 63.54% of the interstitial cystitis drugs market size in 2024; gel and liposomal formats are anticipated to grow 7.89% annually to 2030.

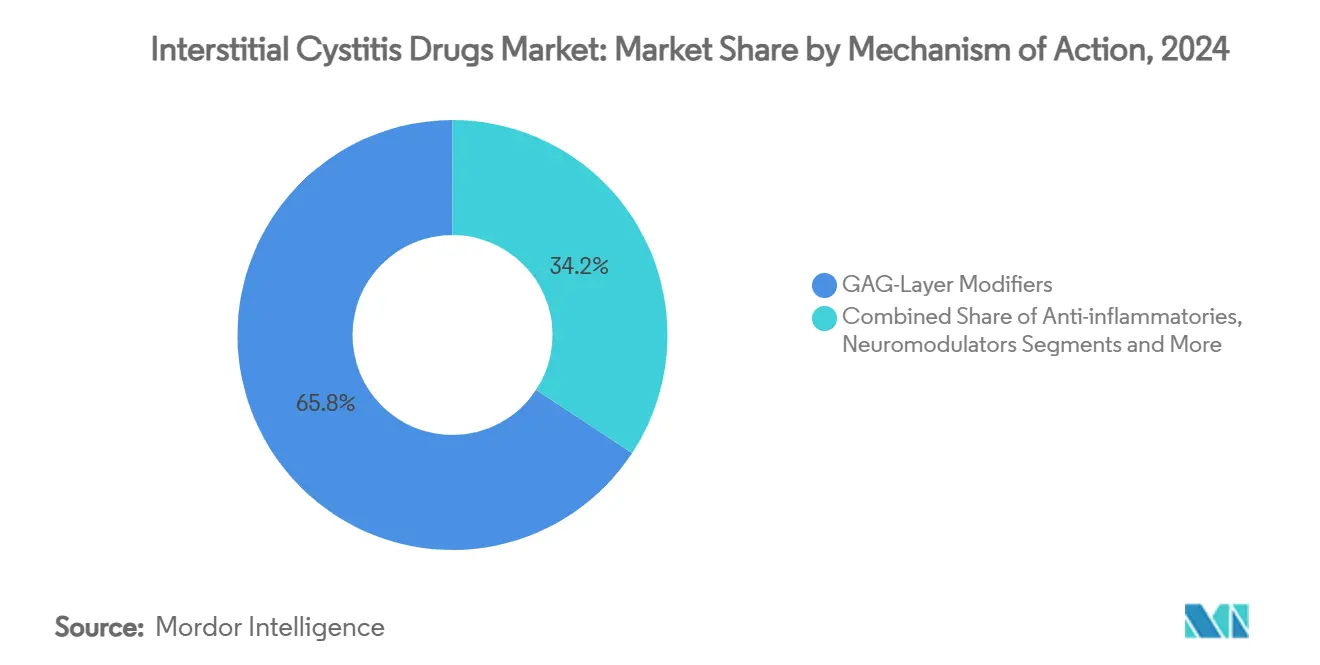

- By mechanism of action, GAG-layer modifiers controlled 65.76% of interstitial cystitis drugs market share in 2024, while neuromodulators are on track for an 8.13% CAGR over the outlook period.

- By distribution channel, hospital pharmacies held 42.36% of revenue in 2024; online pharmacies are projected to climb at 9.72% CAGR to 2030.

- By geography, North America represented 47.61% of 2024 sales, whereas Asia-Pacific is poised for a 7.86% CAGR through 2030.

Global Interstitial Cystitis Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of IC/BPS | +1.2% | Global, higher in North America & Europe | Long term (≥ 4 years) |

| FDA approvals & expanded indications | +0.8% | North America core; spill-over to EU & APAC | Medium term (2-4 years) |

| Increasing female geriatric population | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Growing adoption of intravesical techniques | +1.1% | North America & EU core; expanding in APAC | Medium term (2-4 years) |

| Nanocarrier intravesical formulations | +0.7% | Global; early uptake in academic centers | Long term (≥ 4 years) |

| Digital bladder-diary reimbursement pathways | +0.4% | North America & select EU markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Interstitial Cystitis & Bladder Pain Syndrome

Growing disease recognition is swelling the treated population as urologists deploy biomarker panels that distinguish Hunner-type from non-Hunner disease early in the diagnostic journey. Recent work shows serum and urine MMP9 tracks directly with symptom severity and therapy response, allowing physicians to initiate targeted interventions sooner. Health systems that once treated IC/BPS as a diagnosis of exclusion now introduce dedicated care pathways staffed by pelvic-pain specialists, lifting prescription volumes for oral and intravesical agents alike. Earlier diagnosis also raises the share of newly identified cases among younger cohorts, bolstering lifetime treatment value per patient. These shifts collectively underpin a structural rise in baseline demand for all classes of interstitial cystitis drugs market therapies.

FDA Approvals & Expanded Indications for PPS & Pipeline Drugs

Regulatory clarity is shortening development timelines. The US FDA’s 2024 guidance on BCG-unresponsive bladder disease outlines study endpoints that translate well to IC/BPS trials, easing the route for intravesical systems entering Phase II. Breakthrough designation for Johnson & Johnson’s TAR-200 gemcitabine platform illustrates agency appetite for innovative delivery mechanisms, while NIDDK’s broadened funding for microbiome-driven research fuels exploratory programs targeting neuro-immune pathways.[2]National Institute of Diabetes and Digestive and Kidney Diseases, “Clinical Trials for Interstitial Cystitis,” niddk.nih.gov Clearer guidance and expedited reviews lower commercial risk and encourage investment across the interstitial cystitis drugs market landscape.

Increasing Female Geriatric Population

Aging demographics in developed economies cause a steady rise in estrogen-deficient urothelial dysfunction that precipitates IC/BPS. Epidemiological analyses indicate women over 65 present the highest incidence, reinforcing long-run demand for GAG-layer replenishment agents. Longer life expectancy translates into decades-long treatment horizons, making adherence and safety paramount. Expanded Medicare coverage for urological conditions helps offset cost barriers, although reimbursement for premium formulations remains uneven. The demographic surge reinforces baseline volumes for the interstitial cystitis drugs market well into the forecast window.

Growing Adoption of Intravesical Drug-Delivery Techniques

Sustained-release intravesical platforms now demonstrate superior bladder tissue exposure and symptom relief compared with systemic therapy. Crosslinked glycosaminoglycan GLX-100 adheres to the bladder wall and maintains longer residence time than traditional solutions, with Phase 1b data showing meaningful reductions in pain and urgency. Systematic reviews confirm intravesical dimethyl sulfoxide and hyaluronic acid deliver higher response rates than oral agents in refractory IC/BPS cases. Training programs for urology nurses and investment in catheter-friendly outpatient suites lower procedural hurdles, accelerating uptake across tertiary centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PPS-linked pigmentary maculopathy warnings | -0.6% | Global; highest visibility in US & EU | Short term (≤ 2 years) |

| High therapy cost & limited coverage | -0.9% | Global; most severe in US | Medium term (2-4 years) |

| Product-liability litigation risks | -0.4% | Primarily North America | Medium term (2-4 years) |

| Diagnostic heterogeneity across providers | -0.7% | Global; pronounced in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PPS-Linked Pigmentary Maculopathy Safety Warnings

Long-term pentosan polysulfate exposure has been associated with irreversible retinal pigmentary changes, prompting the FDA to mandate baseline and periodic ophthalmic exams for all patients on Elmiron. Clinicians increasingly switch chronic users to intravesical hyaluronic acid or DMSO, reducing oral PPS volumes during the guideline-driven monitoring period. The heightened safety oversight adds testing costs that weigh on payer willingness to reimburse, curbing short-term growth in the dominant oral therapy segment.

High Therapy Cost & Limited Insurance Coverage

Out-of-pocket costs for oral PPS still exceed USD 400 per month when plans exclude or tier-shift the medicine, a barrier for many chronic-pain patients. Intravesical instillations incur procedure fees plus catheter supplies, stretching total cost above USD 2,000 for a six-week course in the United States. Prior-authorization hurdles prolong untreated periods and fuel patient attrition. Without broader generic entry the interstitial cystitis drugs market faces moderate demand suppression through mid-decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Intravesical Innovation Challenges Oral Dominance

Oral pentosan polysulfate drove 68.96% of interstitial cystitis drugs market revenue in 2024, benefiting from its unique FDA indication and convenient once-daily dosing. Safety-linked discontinuations, however, are steering physicians toward intravesical dimethyl sulfoxide and hyaluronic acid, which together are forecast to record an 8.48% CAGR through 2030. The interstitial cystitis drugs market size for intravesical solutions is projected to advance as Japanese real-world data confirm 70% response rates in refractory Hunner-type cases. Combination gels blending amitriptyline, baclofen, and gabapentin exemplify multi-mechanism products designed to prolong remission and limit narcotic reliance. The pursuit of oral alternatives continues, yet clinical momentum now favors bladder-directed approaches that deliver higher local concentrations while curtailing systemic exposure.

Second-line analgesics and NSAIDs remain widely prescribed off-label, yet their contribution to overall revenue is modest because of low unit prices and short treatment cycles. Immune-targeted investigational agents such as tipelukast are contributing to a late-stage pipeline targeting fibrotic pathways implicated in chronic bladder inflammation. Investors expect that integrating oral and intravesical regimens will allow step-up therapy algorithms that improve quality-of-life scores while limiting cumulative steroid exposure.

By Route of Administration: Intravesical Systems Gain Clinical Acceptance

The oral route captured 72.34% of 2024 spending, anchored by Elmiron and widespread patient familiarity. Yet mounting evidence shows direct bladder instillation produces quicker symptom relief and superior long-term control, giving intravesical systems the fastest growth trajectory at 8.62% through 2030. Injectable triamcinolone has demonstrated 92.9% pain improvement among Hunner lesion patients, carving out a niche for patients who fail traditional options. Transdermal programs leverage permeation enhancers to circumvent first-pass metabolism, though limited data restrict uptake for now.

Expanding ambulatory urology networks accommodate catheter-based therapies, while home-based self-instillation programs piloted in Sweden and Canada suggest future opportunities to decentralize care. As experience accumulates, practicing urologists increasingly situate intravesical agents earlier in the patient journey, eroding the historical dominance of oral monotherapy across the interstitial cystitis drugs market.

By Formulation Type: Advanced Delivery Systems Drive Innovation

Capsules and tablets accounted for 63.54% share in 2024, reflecting the entrenchment of oral PPS alongside adjunctive NSAIDs. Yet gel and liposomal vehicles are advancing at 7.89% CAGR thanks to bladder-surface adhesion and controlled release that extend dosing intervals to monthly or quarterly schedules.[3]Y. Huang, “Intravesical Liposome Treatment,” ncbi.nlm.nih.gov The interstitial cystitis drugs market share of device-based instillations, including TAR-200 style drug-eluting inserts, is small today but is projected to exceed 5% by 2030 as pivotal trials complete.

Solution formats dominate hospital usage because they are easy to compound and administer. Nonetheless, crosslinked GAG polymers such as GLX-100 show superior adherence under hydrodynamic stress, and early human data reveal durable symptom reductions after just two instillations. Nanotechnology is spurring entirely new classes of particles that combine anti-inflammatory, antimicrobial, and antioxidant properties in a single carrier system, setting the stage for multi-modal formulations that could reshape therapeutic expectations.

By Mechanism of Action: Neuromodulation Emerges as Growth Driver

GAG-layer modifiers earned 65.76% of 2024 revenue, confirming the centrality of barrier repair in disease management. However, neuromodulators are advancing fastest, supported by data showing median pain score drops from 8 to 3 after sacral neuromodulation in refractory cohorts. Anti-inflammatory biologics trail behind due to administration complexity and lack of validated targets, though elevated BAFF and IL-17 suggest avenues for future immune-directed drugs.

Sunobinop’s nociceptin/orphanin-FQ receptor engagement exemplifies a new wave of small-molecule neuromodulators in Phase Ib studies that aim to combine oral convenience with central pain pathway rebalancing. As mechanistic diversity broadens, combination regimens pairing barrier repair with neural or immune modulation may become the norm, positioning the segment for sustained leadership within the interstitial cystitis drugs market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies generated 42.36% of sales in 2024, owing to procedure-linked dispensing of intravesical agents and injectable corticosteroids. Retail outlets handle stable chronic prescriptions but face share erosion as patients gravitate online for discreet ordering and subscription discounts. Online pharmacies are forecast to post 9.72% CAGR, the highest among distribution tiers, as telehealth platforms bundle e-consultation, e-prescribing, and doorstep delivery into integrated chronic-care offerings.

Digital refill reminders and automated insurance adjudication mitigate abandonment, raising adherence above 80% in pilot programs. Regulators are moving to standardize cold-chain validation and identity checks, paving the way for biologics and specialty formulations to flow through direct-to-patient channels. As e-commerce norms mature, the interstitial cystitis drugs market will likely mirror broader retail medicine trends in shifting sizable volumes away from traditional bricks-and-mortar dispensaries.

Geography Analysis

North America commanded 47.61% of 2024 revenue on the strength of established reimbursement, dense urology networks, and high awareness among primary-care providers. The United States alone accounted for more than three-quarters of regional demand, and its payer landscape heavily influences product launch sequencing. Canada’s 2025 national guideline endorses early intravesical therapy for Hunner lesions, which should further widen adoption. Despite its maturity, the region still contributes significant absolute growth as biologic and neuromodulator launches carry premium pricing.

Europe follows with sizable if slower-moving uptake. Country-level heterogeneity in reimbursement rules creates a patchwork of access; nevertheless, EMA’s progressive stance on novel urological drugs, evidenced by vibegron’s OAB approval, signals receptivity to additional IC/BPS filings. Germany and the Nordic countries lead prescription density, whereas Central and Eastern Europe lag amid budget constraints. Ongoing alignment of treatment guidelines under EAU is expected to narrow access gaps post-2027.

Asia-Pacific is the fastest-growing territory at 7.86% CAGR. Japan’s 2024 endorsement of intravesical DMSO catalyzed a surge in hospital procedures and prompted domestic firms to license Western GAG formulations. South Korea is expanding insurance coverage for sacral neuromodulation, improving uptake. China, while starting from a lower base, is rolling out urology specialty clinics in top-tier cities, creating fertile ground for multinationals once regulatory clarity around combination gels improves. India’s private-hospital chains are piloting tele-urology services that integrate online pharmacy fulfillment, illustrating how leapfrog digital models can bypass brick-and-mortar constraints.

Latin America and the Middle East & Africa collectively hold a smaller share but offer niche potential. Brazil’s ANVISA is assessing hyaluronic acid instillation dossiers, and regional distributors are gearing up for private-market introductions. Gulf Cooperation Council states, led by Saudi Arabia and the UAE, show growing demand for premium neuromodulation as part of broader investment in tertiary women’s health services. Conversely, diagnostic heterogeneity and limited payer budgets dampen immediate prospects across Sub-Saharan Africa, meaning penetration will likely trail until multilateral aid programs prioritize pelvic pain management.

Competitive Landscape

The interstitial cystitis drugs market remains moderately fragmented. Janssen’s Elmiron enjoys brand recognition but is vulnerable to declining use because of ocular safety concerns. As a countermeasure, Janssen is exploring next-generation capsule coatings to reduce systemic exposure. Johnson & Johnson leverages device know-how from TAR-200 to diversify beyond oncology into chronic bladder pain, signaling large-cap interest in mechanical drug delivery.

Biotechnology entrants such as Glycologix and Vaneltix pursue crosslinked polymers and muco-adhesive gels that challenge traditional GAG solutions. Imbrium Therapeutics’ sunobinop exemplifies neuro-centric pipelines attempting to redefine first-line therapy. Academic spin-outs are harnessing cerium oxide nanoparticles to combine anti-oxidative stress and anti-inflammatory effects in single agents, though IP portfolios remain early stage. Meanwhile, digital health firms partner with pharmacy benefit managers to capture data exhaust from bladder-diary apps, aiming to create value-add adherence platforms rather than selling drugs directly.

M&A already hints at consolidation: over the past 18 months two midsize specialty pharma firms acquired urology-focused start-ups with nanocarrier delivery patents. Large generic houses watch closely, anticipating eventual PPS patent expiry to enter with price-volume plays. Overall, the interplay between device-enabled delivery and molecular innovation is redefining competitive stakes, suggesting meaningful reshuffling of share positions through the forecast horizon.

Interstitial Cystitis Drugs Industry Leaders

Johnson & Johnson

Teva Pharmaceutical Industries

Endo Inc

Viatris

Kyorin Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Glycologix announced Phase 1b data for GLX-100 will be presented at the AUA 2025 Annual Meeting.

- March 2025: Imbrium Therapeutics completed last-patient visits in its Phase 1b trial evaluating sunobinop for IC/BPS.

- December 2024: Vaneltix Pharma initiated the VNX001-110 trial to study Alenura in IC/BPS treatment.

Global Interstitial Cystitis Drugs Market Report Scope

| Oral Therapies |

| Intravesical Therapies |

| Analgesics/NSAIDs |

| Others |

| Oral Route |

| Intravesical Route |

| Others (injectable, transdermal) |

| Capsule/Tablet |

| Solution |

| Gel / Liposomal |

| Device-Based Instillations |

| GAG-Layer Modifiers |

| Anti-inflammatories |

| Neuromodulators |

| Immunotherapies / Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Oral Therapies | |

| Intravesical Therapies | ||

| Analgesics/NSAIDs | ||

| Others | ||

| By Route of Administration | Oral Route | |

| Intravesical Route | ||

| Others (injectable, transdermal) | ||

| By Formulation Type | Capsule/Tablet | |

| Solution | ||

| Gel / Liposomal | ||

| Device-Based Instillations | ||

| By Mechanism of Action | GAG-Layer Modifiers | |

| Anti-inflammatories | ||

| Neuromodulators | ||

| Immunotherapies / Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current interstitial cystitis drugs market size?

The market is valued at USD 1.46 billion in 2025 and is projected to reach USD 1.92 billion by 2030.

2. Which drug class leads revenue today?

Oral therapies, dominated by pentosan polysulfate, held 68.96% of 2024 revenue.

3. Why are intravesical therapies growing faster than oral drugs?

They deliver higher bladder concentrations, show better symptom relief, and bypass systemic side-effects, driving an 8.48% CAGR outlook.

4. Which region shows the highest growth potential?

Asia-Pacific is forecast to expand at 7.86% CAGR as Japan and South Korea broaden reimbursement for intravesical agents.

Page last updated on: