Cystoscopes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

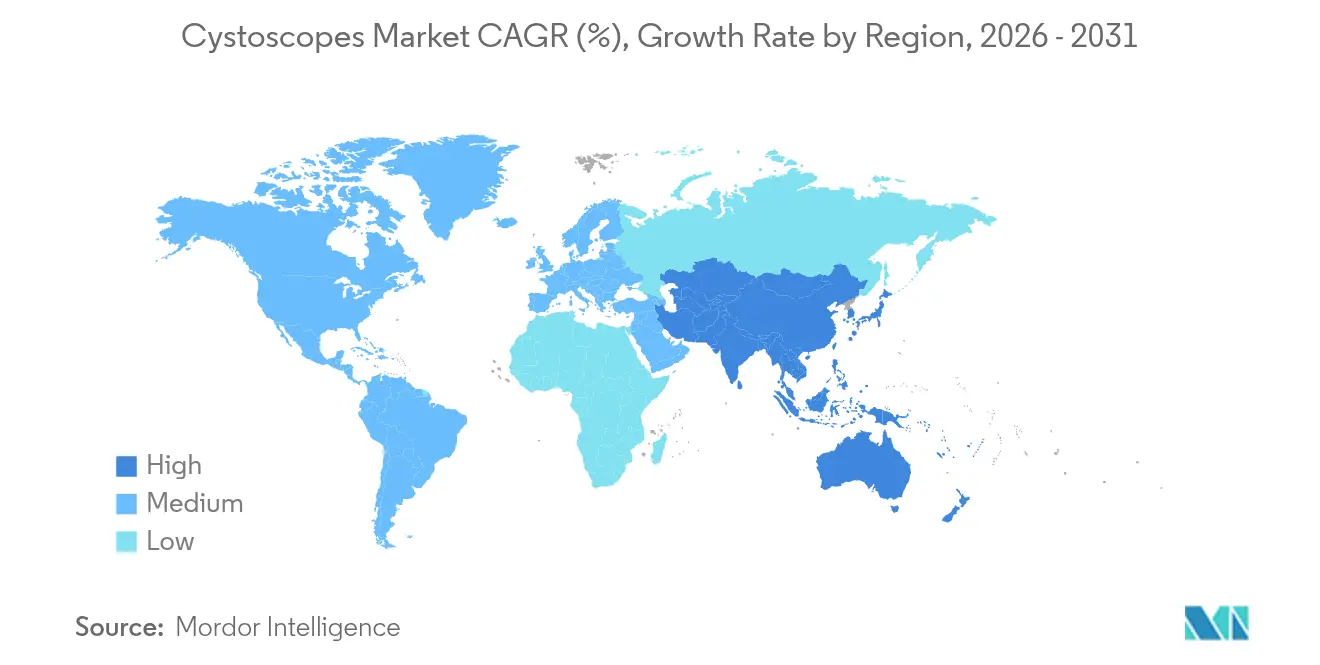

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

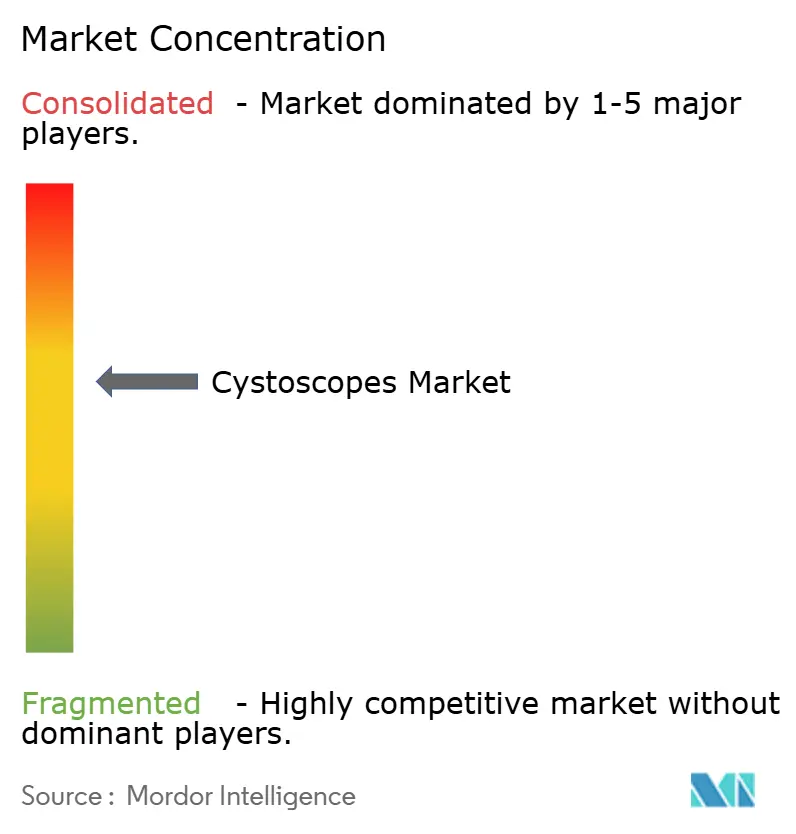

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cystoscopes Market Analysis by Mordor Intelligence

The cystoscopes market size in 2026 is estimated at USD 1.22 billion, growing from 2025 value of USD 1.14 billion with 2031 projections showing USD 1.67 billion, growing at 6.62% CAGR over 2026-2031. Continuous migration from reusable devices toward infection-controlled, single-use platforms, the roll-out of HD, 4K and Narrow Band Imaging (NBI) optics, and the growing use of artificial intelligence (AI) in lesion detection underpin this expansion. Incidence of bladder cancer is climbing in every major region, sustaining procedural volumes even as minimally invasive outpatient settings become the preferred care site. Hospitals, ambulatory surgical centers (ASCs) and office clinics are therefore prioritizing portable, AI-enabled cystoscopes that cut reprocessing time, raise diagnostic yield and align with emerging reimbursement codes. Further momentum comes from strategic acquisitions—for example, KARL STORZ integrating Asensus Surgical’s robotic assets—and procurement policies that elevate infection prevention over unit cost, accelerating single-use adoption.

Key Report Takeaways

- By product type, flexible devices led with 56.10% of cystoscopes market share in 2025, whereas single-use units within the product mix posted the fastest 7.48% CAGR through 2031.

- By usage, single-use cystoscopes accounted for 59.32% of the cystoscopes market size in 2025 and are advancing at 7.48% CAGR to 2031.

- By technology platform, fiber-optic systems captured 61.35% of cystoscopes market share in 2025; video (digital) units are growing quickest at 7.78% CAGR.

- By application, urology dominated with 69.10% revenue in 2025, while gynecology is set for the highest 7.15% CAGR to 2031.

- By end user, hospitals held 65.50% of cystoscopes market share in 2025; ASCs are expanding most rapidly at 7.65% CAGR.

- By geography, North America commanded 41.20% of the cystoscopes market size in 2025, whereas Asia-Pacific registers the top regional CAGR of 8.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cystoscopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in urinary tract & bladder cancer incidence | +1.2% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Technological leap to HD/4K & NBI imaging | +1.0% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Preference for minimally invasive outpatient cystoscopy | +0.8% | Global, led by developed markets | Medium term (2-4 years) |

| Hospital shift toward disposable, infection-free scopes | +1.1% | Global, accelerated in post-pandemic environment | Short term (≤ 2 years) |

| AI-assisted lesion detection boosting diagnostic yield | +0.7% | North America & Europe, gradual Asia-Pacific adoption | Long term (≥ 4 years) |

| Emerging reimbursement codes for office-based procedures | +0.6% | Primarily North America, selective European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Urinary Tract & Bladder Cancer Incidence

Incidence of bladder cancer has trended upward in every major demographic group, and five-year cystectomy rates now reach only 14% when chemoradiotherapy replaces radiotherapy alone, underscoring the need for precise diagnostic follow-up. Aging populations and exposure to smoking and industrial chemicals raise lifetime risk, prompting health systems to scale screening programs that rely heavily on cystoscopy. The cystoscopes market therefore benefits from uninterrupted demand across hospitals and outpatient clinics. Flexible optics remain central because they offer complete bladder visualization with minimal patient trauma. Manufacturers strengthening image quality and ergonomics are primed to capture additional share as providers standardize high-risk patient surveillance protocols.

Technological Leap to HD/4K & NBI Imaging

Olympus introduced 4K camera heads for urological use, quadrupling pixel density versus HD systems and bolstering NBI brightness by 20%.[1]Olympus Corp., “4K Imaging for Urology,” olympus-global.com Clinical evidence shows blue-light cystoscopy with 4K optics lifts carcinoma-in-situ detection to 95.2%, dwarfing the 42.9% rate of conventional white-light systems. Superior visualization lowers recurrence, supports premium pricing and drives faster replacement cycles as hospitals retire aging fiber bundles. These gains translate into a tangible +1.0% uplift to forecast CAGR for the cystoscopes market while anchoring differentiation strategies for vendors investing in digital platforms.

Preference for Minimally Invasive Outpatient Cystoscopy

Flexible cystoscopy typically requires only local anesthesia and less than 10 minutes, aligning with ASC and office-based models that cut total facility costs compared with hospital admission. Insurance payers increasingly reward site-neutral billing, and new CPT codes for outpatient procedures—such as Olympus’s iTind therapy—further legitimise office delivery. Ambulatory settings lack the reprocessing infrastructure of tertiary hospitals, making single-use solutions practical. This care shift encourages procurement of portable, infection-protected cystoscopes and supports scalable deployment where trained urologists are scarce.

Hospital Shift Toward Disposable, Infection-Free Scopes

FDA safety alerts highlight contamination risks tied to reprocessed endoscopes, accelerating interest in ready-to-use devices.[2]Ambu A/S, “Sustainability White Paper 2024,” ambu.com Studies reveal single-use cystoscopes abolish cross-infection and remove 42 minutes of reprocessing from each case, outweighing higher per-unit cost. A global survey of 415 procurement teams indicates willingness to convert 44.5% of cystoscopy workload to disposables, signalling deep penetration potential. As sustainability audits confirm lower life-cycle emissions than reusable alternatives, disposable adoption directly feeds a +1.1% CAGR contribution within the cystoscopes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & reprocessing cost of reusable scopes | -0.9% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Shortage of trained urologists in emerging markets | -0.7% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Environmental waste concerns over single-use products | -0.5% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Supply-chain crunch for CMOS/optical components | -0.8% | Global, with acute impact on manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Reprocessing Cost of Reusable Scopes

Lifetime cost auditing shows reusable flexible ureteroscopes carry per-procedure expenses of USD 1,212-1,743 once repairs, labor, consumables and downtime are included. For lower-income systems, that capital burden hampers equipment renewal and encourages reuse beyond manufacturer limits, raising infection risk. In parallel, single-use purchasing models with predictable case-based pricing appeal to finance officers seeking expense visibility. Consequently, emerging providers allocate cap-ex to digital single-use fleets, chipping away at residual reusable demand and restraining aggregate growth by 0.9 percentage points.

Shortage of Trained Urologists in Emerging Markets

Training pathways last between 5-9 years, and vacancy rates remain pronounced across Asia, Africa and Latin America. Task-shifting to physician associates grew 109% and nurse practitioners 156% between 2014-2024, yet procedural capacity remains tight. Manufacturers respond with AI-guided, plug-and-play cystoscopes that simplify orientation and documentation. Even so, specialist scarcity suppresses procedure volumes in high-burden geographies, trimming long-term cystoscopes market expansion by 0.7 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Devices Maintain Commanding Position

Flexible units contributed 56.10% of cystoscopes market share in 2025, a dominance owed to superior patient comfort and shaft maneuverability enabling 210° up-flexion and 120° down-flexion. The flexible cohort advances at 7.35% CAGR to 2031 as manufacturers add HD sensors, NBI, and variable stiffness features that widen adoption across outpatient clinics. Rigid scopes still serve pediatric and therapeutic tasks where instrument stability outweighs comfort, but incremental innovation flows mainly toward flexibles. The cystoscopes market continues to view flexible optics as the primary avenue for AI integration because stable digital feed is essential for algorithmic analysis.

Second-generation HD flexible cysto-nephroscopes illustrate the leap, integrating NBI that is 20% brighter than predecessor models. Early users report 95.2% carcinoma-in-situ detection with blue-light adjuncts versus 42.9% on legacy white light. Premium pricing remains defensible because lower recurrence rates avert costly reinterventions. As sustainability metrics improve—through recyclable packaging and lower energy use—flexible devices sustain their leadership in the cystoscopes industry, fortifying overall market resilience.

By Usage: Single-Use Surge Accelerates Infection Control

Single-use scopes delivered 59.32% to the cystoscopes market size in 2025 and are growing at 7.48% CAGR, propelled by hospital mandates that prioritize zero cross-infection and staff time savings. Evidence comparing carbon footprints shows reusable reprocessing outweighs the total life-cycle impact of disposables, reshaping perceptions of environmental cost. ASC administrators value the 42-minute time saving per procedure, which frees operating lists and raises throughput.

Ambu’s aScope 5 Cysto HD gained FDA clearance in January 2025, adding single-use HD imaging to percutaneous nephrolithotomy workflows and underscoring rapid innovation cadence. As price parity approaches and AI modules arrive on disposable platforms, the cystoscopes market anticipates tougher competition for legacy equipment. Nonetheless, high-volume centers may retain mixed fleets where reprocessing costs amortize efficiently, illustrating a nuanced transition rather than an outright replacement.

By Technology Platform: Digital Systems Gain Ground

Fiber-optic technology still controls 61.35% of cystoscopes market share in 2025 because of wide installed base and lower acquisition outlay, yet video systems are climbing at 7.78% CAGR. Digital feeds allow annotation, cloud storage and teleconsultation, aligning with electronic health record mandates. AI products require pixel-dense inputs, accelerating adoption of 4K and 8K sensors. The cystoscopes industry therefore regards video platforms as the gateway for decision-support analytics, fueling R&D investment.

Olympus’s latest 4K head quadruples pixel density over HD while embedding blue-light and AI hooks, meeting hospital demand for future-proof equipment. As depreciation cycles coincide with regulatory pushes for post-market surveillance data, administrators prefer upgradable digital stacks that maximize longevity. Market entrants differentiate on processing algorithms and intuitive user interfaces rather than on optics alone, making software a new battleground.

By Application: Urology Retains Core Role, Gynecology Climbs

Urology captured 69.10% share of the cystoscopes market size in 2025, underpinned by bladder cancer surveillance and therapeutic interventions such as transurethral resection, which sees 43.5% complication rates within 30 days. Hospitals seek scopes that integrate laser channels and irrigation control to tackle bleeding and resection debris. The high recurrence of non-muscle invasive bladder cancer ensures routine follow-up cystoscopies, locking in steady procedure flow.

Gynecology advances at 7.15% CAGR on rising awareness of female pelvic disorders and concomitant urinary issues. Clinicians increasingly employ cystoscopy during urogynecological repairs to check ureter patency, expanding addressable volume. Vendors offering slim, atraumatic tip designs tailored for female anatomy gain traction. While paediatric and research segments stay niche, AI-assisted image analysis promises to elevate adoption in training programs, extending the cystoscopes market footprint.

By End User: Hospitals Lead but ASCs Outpace

Hospitals held 65.50% of cystoscopes market share in 2025 thanks to comprehensive imaging suites, 24/7 staffing and proximity to intensive care for complex cases. Yet ASCs exhibit the highest 7.65% CAGR because they deliver lower facility costs and faster patient turnover. Reimbursement reforms that tie payments to site efficiency spur the shift, while portable HD disposables suit centers that lack sterile processing capacity.

Claims filed by physician associates and nurse practitioners for urological procedures grew 109% and 156% respectively from 2014-2024, signaling new operator groups entering outpatient delivery. Manufacturers now market turnkey cystoscopy kits with pre-loaded procedure packs, streamlining supply logistics for ASCs. As hospital outpatient departments adapt to competitive fee schedules, they may partner with standalone centers, potentially blending the lines between traditional end user categories within the cystoscopes market.

Geography Analysis

North America controlled 41.20% of the cystoscopes market size in 2025, buoyed by Medicare coverage, early AI trials and robust capital budgets. The Axonics acquisition by Boston Scientific for USD 3.7 billion underlines ongoing portfolio expansion in regional urology. Strong intellectual-property protections encourage R&D in AI-guided cystoscopy, maintaining technological leadership.

Europe follows closely, with regulatory reforms that extend CE-mark transition timelines to 2028, obligating deeper clinical evidence for existing devices. Sustainability drives purchasing, with the UK’s National Health Service evaluating circular economy pilots for medical equipment. These policies are amplifying demand for single-use scopes validated as lower-carbon alternatives, reshaping vendor scorecards across the cystoscopes market.

Asia-Pacific is the fastest-growing geography, tracking 8.05% CAGR through 2031. Infrastructure expansions in India, China and Southeast Asia open operating room capacity, while local suppliers pivot to export single-use devices amid tariff shifts. Poly Medicure projects 20% annual revenue growth and aims for USD 20-30 million in US cystoscopy sales by 2028, showcasing Asia’s ascending role in global supply chains. Regional governments also emphasise ESG compliance, which aligns with low-reprocessing, resource-efficient products that strengthen local adoption.

Competitive Landscape

Olympus, KARL STORZ, Boston Scientific and Ambu are among the major players in the cystoscopes market, underscoring a moderately fragmented structure where no single vendor dominates. Olympus reinforces its incumbency through sustained spending on 4 K and Narrow Band Imaging platforms, long equipment warranties and bundled service contracts that keep hospitals locked into its ecosystem. KARL STORZ has widened its scope by absorbing Asensus Surgical, a move that adds robotic assets and positions the firm to pair cystoscopy with digital surgery consoles.[3]KARL STORZ, “Asensus Surgical Acquisition Details,” karlstorz.comBoston Scientific strengthened its urology offering by purchasing Axonics, gaining sacral neuromodulation technology that complements its bladder management portfolio. These strategic moves illustrate how leading players rely on acquisitions and integrated service models to maintain share in the cystoscopes market.

Ambu leads the single-use wave after securing first-in-class FDA clearance for its disposable HD cysto-nephroscope in 2025, giving the company an infection-control narrative that resonates with outpatient facilities. BD amplifies disposable adoption through clinical studies that quantify a 42-minute reduction in reprocessing time per case, information that appeals to ambulatory surgical centers seeking higher throughput. Several Asian manufacturers compete on price by launching hybrid scopes that mix reusable housings with low-cost digital tips, creating budget-friendly alternatives for emerging markets. Western start-ups, meanwhile, channel investment into AI overlays that bolt onto installed video stacks, carving out niche positions without large capital footprints.

Software has become the newest battleground, with vendors racing to integrate decision-support algorithms trained on vast image libraries that improve lesion detection accuracy beyond expert urologist levels. Data-centric strategies encourage partnerships with hospitals willing to share de-identified procedural footage, giving developers the raw material needed to refine machine-learning models. Suppliers are also embedding cloud connectivity, remote diagnostics and automated reporting into next-generation platforms, heightening switching costs once facilities migrate to digital ecosystems. As a result, competitive rivalry is shifting from optics alone to a mix of hardware, software and service that determines total cost of ownership and clinical performance in the cystoscopes market.

Cystoscopes Industry Leaders

Olympus Corporation

KARL STORZ GmbH & Co. KG

Boston Scientific Corporation

Ambu A/S

Becton Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus announced two Category I CPT codes for the iTind procedure, easing reimbursement from January 2025.

- January 2025: Ambu secured FDA clearance for the aScope 5 Cysto HD, the first single-use flexible cysto-nephroscope approved in the United States.

- August 2024: KARL STORZ completed its USD 0.35-per-share acquisition of Asensus Surgical, integrating the LUNA digital surgery system.

- July 2024: Photocure and Richard Wolf formed a partnership to co-develop advanced cystoscopes, targeting improved visualization in bladder cancer procedures.

Global Cystoscopes Market Report Scope

As per the scope of the report, the cystoscope is a specialized medical instrument designed for examining the interior of the bladder and urethra. It is a type of endoscope that can be either flexible or rigid, equipped with a light and camera to provide a clear view of these areas. This tool is essential for diagnosing and treating various urinary tract conditions, such as infections, blockages, or tumors. By allowing direct visualization, it helps doctors perform procedures like biopsies or removing small stones. The primary cell culture market is segmented by product, application, end user, and geography. By product, the market is segmented into flexible cystoscope, and rigid cystoscope. By application, the market is segmented into urology, gynaecology, and others. By end user, the market is segmented into hospitals, ambulatory surgical centers, and diagnostic centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments

| Rigid Cystoscope |

| Flexible Cystoscope |

| Single-Use Cystoscope |

| Reusable Cystoscope |

| Fiber-optic |

| Video (Digital) |

| Urology |

| Gynecology |

| Others |

| Hospitals |

| Ambulatory Surgical Centers (ASC) |

| Diagnostic & Office-based Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Rigid Cystoscope | |

| Flexible Cystoscope | ||

| By Usage | Single-Use Cystoscope | |

| Reusable Cystoscope | ||

| By Technology Platform | Fiber-optic | |

| Video (Digital) | ||

| By Application | Urology | |

| Gynecology | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASC) | ||

| Diagnostic & Office-based Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cystoscopes market by 2031?

The cystoscopes market is forecast to reach USD 1.67 billion by 2031, expanding at a 6.62% CAGR.

Which product segment holds the largest share today?

Flexible devices lead with 56.10% cystoscopes market share in 2025, reflecting superior patient comfort and maneuverability.

Why are single-use cystoscopes gaining traction?

Growing infection-control mandates, elimination of reprocessing time and comparable life-cycle environmental impact are pushing single-use scopes to 7.48% CAGR growth.

Which region is expanding fastest?

Asia-Pacific records the highest 8.05% CAGR through 2031 owing to hospital infrastructure growth and rising bladder cancer incidence.

How does AI benefit cystoscopy procedures?

AI algorithms raise carcinoma-in-situ detection to 95.2% versus 42.9% with white light alone, improving diagnostic accuracy and enabling real-time decision support.

Page last updated on: