Medical Cold Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

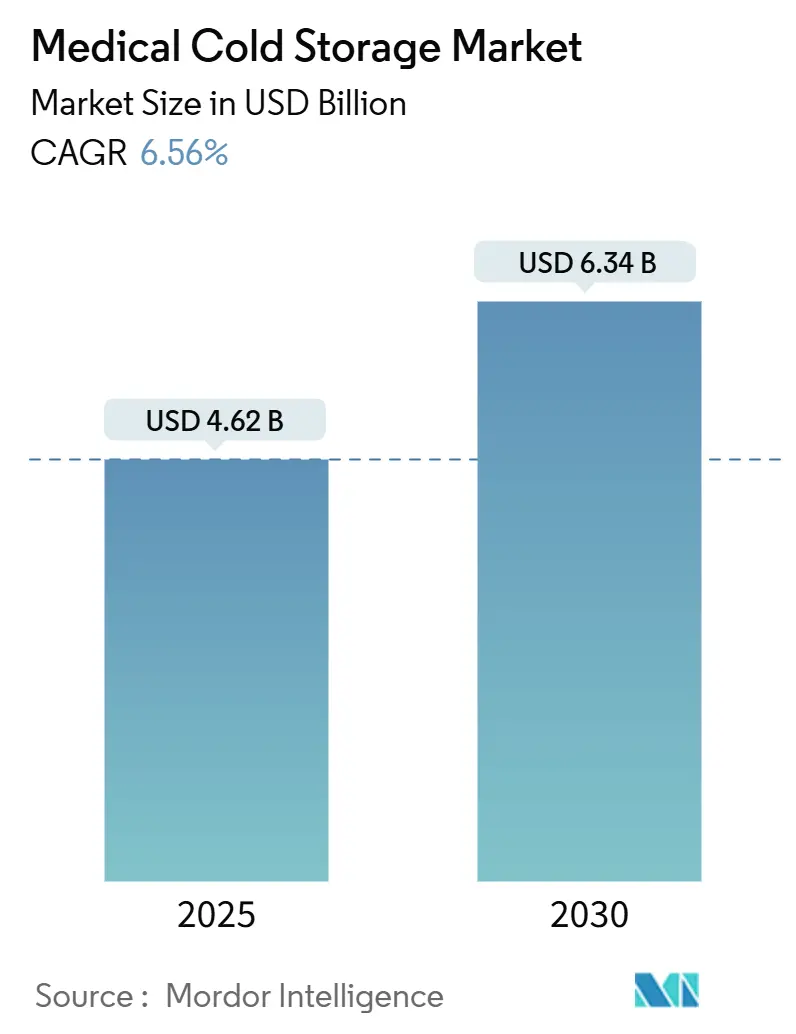

| Market Size (2025) | USD 4.62 Billion |

| Market Size (2030) | USD 6.34 Billion |

| Growth Rate (2025 - 2030) | 6.56% CAGR |

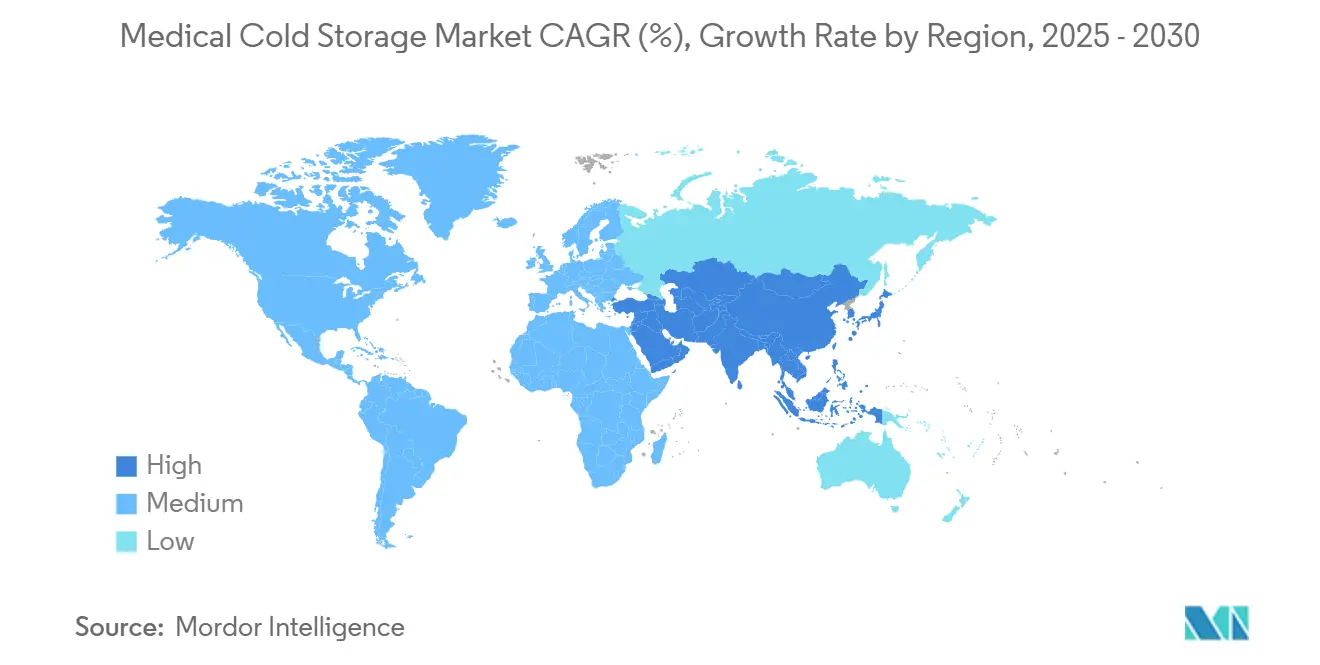

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Cold Storage Market Analysis by Mordor Intelligence

The medical cold storage market size stands at USD 4.62 billion in 2025 and is projected to reach USD 6.34 billion by 2030, advancing at a 6.56% CAGR during the forecast period. Continuous expansion comes from biologics that need ultra-low and cryogenic conditions, tight regulatory oversight that punishes temperature excursions, and the widening reach of precision medicine into mainstream care. Capital is flowing into connected freezers, real-time sensors, and green-refrigerant retrofits as hospitals, research sites, and logistics firms race to comply with evolving quality guidelines. Consolidation among third-party logistics providers is reshaping bargaining power, while regional public–private partnerships keep pushing distributed cold hubs closer to point-of-care delivery. Together, these developments accentuate the structural shift toward specialized infrastructure that shields sensitive therapies from thermal risk, even in resource-constrained environments.

Key Report Takeaways

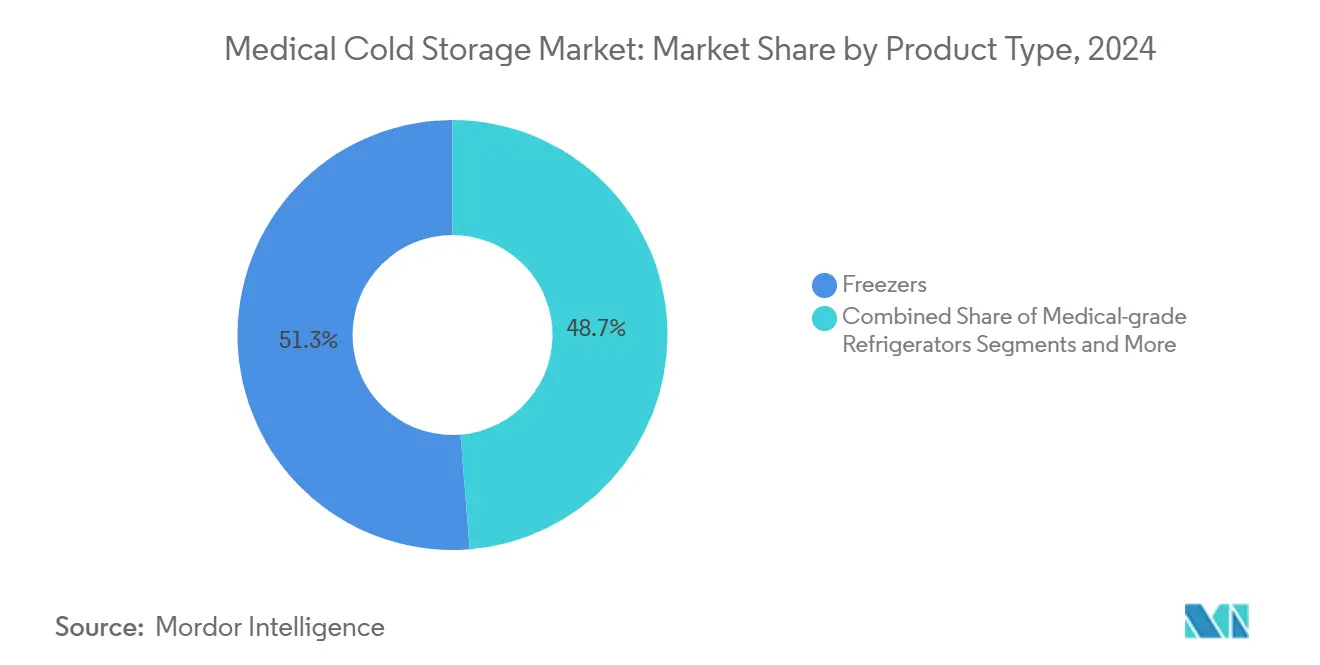

- By product type, freezers led with 51.27% revenue share in 2024, while monitoring systems and accessories are set to grow at a 10.37% CAGR through 2030.

- By application, vaccines accounted for 38.27% of the medical cold storage market share in 2024; cell and gene therapies are forecast to post a 9.37% CAGR to 2030.

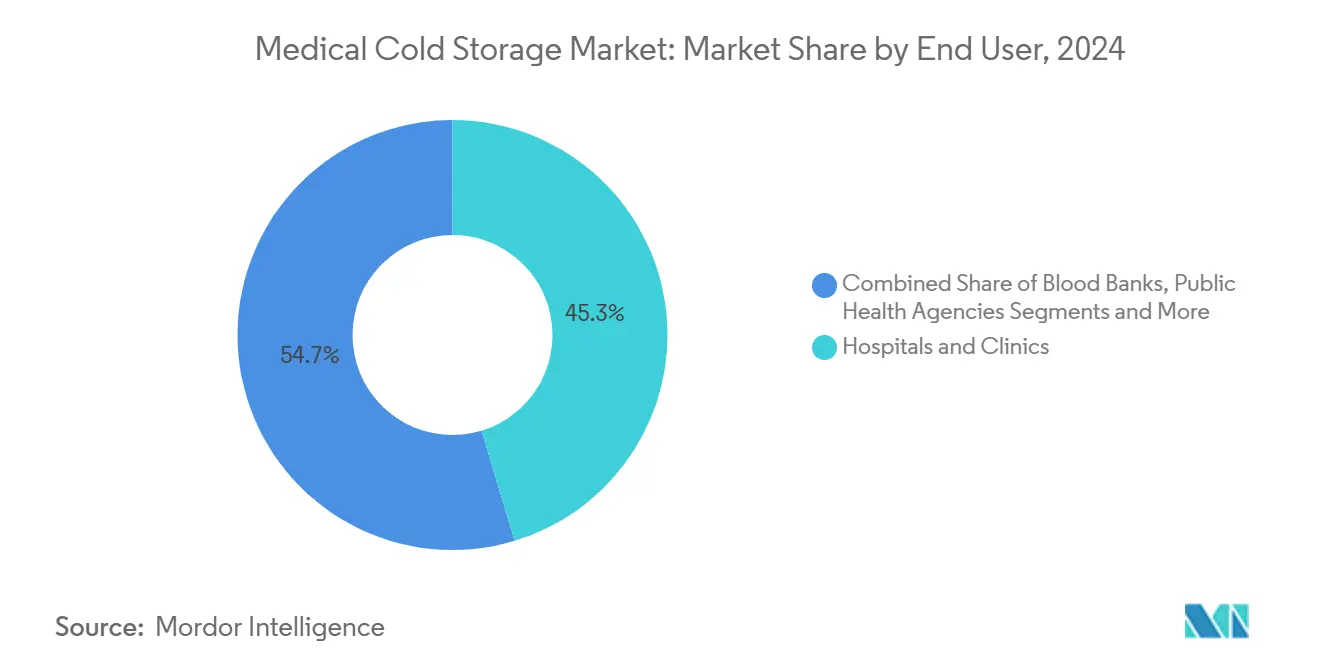

- By end user, hospitals and clinics dominated with 45.33% share of the medical cold storage market size in 2024, whereas CROs and CMOs are primed for 9.66% CAGR through 2030.

- By storage temperature, the ultra-low band controlled 43.54% of 2024 value; cryogenic storage below −150 °C is projected to expand at a 10.24% CAGR between 2025 and 2030.

- By geography, North America held 32.47% share in 2024, but Asia-Pacific is on track for the fastest 9.23% CAGR over the outlook period.

Global Medical Cold Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In Biologics & Cell-Gene Therapies | 2.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Global Vaccine Initiatives & Boosters | 1.8% | Global, with emphasis on emerging markets | Medium term (2-4 years) |

| Expansion Of Decentralized Clinical Trials | 1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising Blood & Organ-Storage Demand | 0.9% | Global, with advanced markets leading adoption | Long term (≥ 4 years) |

| AI-Driven Predictive Maintenance Adoption | 0.7% | North America & EU, with APAC following | Short term (≤ 2 years) |

| Green-Refrigerant Retrofit Wave | 0.5% | EU leading, North America & APAC following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Biologics & Cell-Gene Therapies

Ever-larger pipelines of monoclonal antibodies, RNA platforms, and autologous cell products push storage needs deep into the ultra-low and cryogenic range. Hospitals now integrate liquid-nitrogen vapor tanks that hold material at around −196 °C, while specialty couriers add vacuum-insulated shippers that maintain those conditions for multiple days. Coordinated labeling, validated loading protocols, and chain-of-identity safeguards accompany each batch, turning every freezer rack into a regulated space. Thermo Fisher Scientific alone earmarked USD 2 billion for new U.S. manufacturing and R&D capacity between 2024 and 2028 to keep pace with this wave. Premium pricing for cryogenic systems is increasingly accepted because the therapy value per vial far outweighs equipment cost.

Global Vaccine Initiatives & Boosters

Multilateral agencies intensified financing for refrigerators, freezers, and last-mile data loggers after the covid emergency but kept the momentum as routine immunization rebounded. UNICEF delivered more than 6,600 temperature-controlled units worldwide in 2024, including 1,400 high-specification appliances in Ukraine outfitted with three-day power backup.[1]UNICEF, “To aid effective vaccine storage, UNICEF equips 1,000 vaccination points in Ukraine with refrigerators meeting global standards,” unicef.org WHO prequalification of the MVA-BN mpox vaccine triggered immediate procurement of chilled cabinets that can switch between 2-8 °C holding and ultra-low staging. Solar-direct units rolled out by PAHO allow jab programs in off-grid clinics to operate without diesel generators.[2]Pan American Health Organization, “No power, no problem – Preserving the cold chain in Trinidad and Tobago,” paho.orgRegional manufacturing goals, such as Africa CDC’s plan to supply 60% of continental demand by 2040, guarantee a long runway for distributed capacity expansion.

Expansion of Decentralized Clinical Trials

Remote first-in-human studies now ship investigational products straight to participants’ homes. That shift multiplies unit shipments and forces sponsors to validate parcel-sized coolers with active cooling elements. The Journal of Immunotherapy and Precision Oncology outlines frameworks in which trial monitors rely on continuous telemetry rather than site visits. Blockchain-enabled platforms under evaluation on medRxiv promise automated release of temperature data to regulators, cutting manual paperwork. CROs respond with mobile freezers, self-charging data loggers, and 24/7 control-tower services, turning the model into a competitive necessity.

Rising Blood & Organ-Storage Demand

Transplant programs now test isochoric supercooling chambers that hold livers at −2 °C without ice formation for 48 hours, doubling traditional viability windows.[3]Erik L. Toth, “Isochoric Supercooling Organ Preservation System,” Bioengineering, mdpi.comSupercooled red blood cells survive 63 days at −8 °C, trimming wastage at large blood banks. Platelet additives from AABB research extend cold storage to 14 days, reducing logistics stress. These breakthroughs create traction for multi-temperature modular rooms within single facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & OPEX Of ULT Freezers | -1.4% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

| Stringent Refrigerant Phase-Out Rules | -1.1% | EU leading, North America & APAC following | Medium term (2-4 years) |

| Cold-Chain Talent Shortage In Ems | -0.8% | Emerging markets, particularly Africa & Latin America | Medium term (2-4 years) |

| Cyber-Security Risks To Iot Freezers | -0.6% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX & OPEX of ULT Freezers

A single −80 °C cabinet can draw five times the electricity of a standard pharmacy refrigerator, eroding limited hospital budgets. Hybrid Peltier-compressor prototypes now in feasibility testing show promise, yet market price remains beyond reach for smaller clinics. NIST found retrofitting existing lab fridges with optimized condensers could save U.S. facilities USD 30 million in annual power costs. Until those solutions scale, many emerging-market buyers restrict installations to regional hubs, limiting penetration.

Stringent Refrigerant Phase-Out Rules

Compliance deadlines push operators to invest before assets reach full depreciation. Carrier Transicold levied surcharges in early 2025 to recoup rising R452A costs while launching prototypes that cut refrigerant impact by 89%. Even with grants, labor scarcity for certified A2L technicians inflates retrofit budgets. Cross-border fleets must manage dual inventories of spare parts until global convergence arrives, adding logistical complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Freezers Lead While Monitoring Systems Accelerate

Freezers accounted for 51.27% of 2024 revenue in the medical cold storage market, reflecting widespread adoption of −60 °C to −90 °C cabinets for mRNA vaccines and expanding cell therapy lines. Upright formats dominate hospital corridors, while chest styles satisfy high-volume biobank demand. Energy-efficient compressors, advanced vacuum insulation panels, and variable-speed drives are lowering lifetime costs, but procurement teams still scrutinize total cost of ownership before authorizing expansion. Growth continues as biopharma sponsors install backup units to safeguard trial supplies, pushing urban facilities toward space-saving designs.

Connected monitoring systems, currently the fastest-growing category at a 10.37% CAGR, integrate edge analytics that alert staff to minor deviations long before thresholds are breached. Barcode-matched probes and drug-specific alert profiles improve compliance documentation, a feature increasingly mandatory for regulatory audits. Medical-grade refrigerators retain importance for routine pharmacy stock yet face commoditization pressures that compress margins. Cold rooms, walk-ins, and off-site warehouses add capacity for wholesalers, while smart transportation containers maintain integrity across third-party links in global supply chains.

By Application: Vaccines Dominate as Cell Therapies Surge

Vaccines retained 38.27% of 2024 value in the medical cold storage market, sustained by routine childhood programs, booster schedules, and strategic stockpiles for outbreak response. Shipments fluctuated after the covid emergency yet never returned to pre-pandemic baselines, indicating structurally higher demand for chilled infrastructure. Many public agencies now deploy multi-temperature holding suites, staging mRNA inventory in −80 °C freezers before thawing doses in 2-8 °C pharmacies. Blood and blood components form a mature segment with stable revenues, yet supercooling technology promises to lengthen storage windows and free up transport flexibility.

Cell and gene therapies rise fastest at a 9.37% CAGR, elevating cryogenic shippers, redundant liquid-nitrogen dewars, and chain-of-identity barcoding to mission-critical status. Diagnostic samples benefit from growth in molecular testing and home-collection kits that require multi-day stability during transit. Organ and tissue programs invest in dual-chamber systems that let teams pre-condition grafts at near-freezing temperatures, enhancing post-transplant viability.

By End User: Hospitals Lead While CROs Expand Rapidly

Hospitals and clinics commanded 45.33% of medical cold storage market share in 2024 owing to their role as the first touchpoint for vaccination, oncology infusions, and emergency transfusions. Most tertiary centers operate tiered temperature zones within central pharmacies plus satellite units nearer point of care to minimize walk time. Blood banks remain critical nodes, often colocated with transfusion services and research institutes that rely on −30 °C plasma freezers and platelet agitators. Research and academic laboratories purchase smaller yet highly specialized cabinets to house experimental reagents, while large pharmaceutical and biotech companies run campus-wide freezer farms with automated picking robots for sample management.

CROs and CMOs, scaling at 9.66% CAGR, add overflow capacity for sponsors wary of capital lock-in, offering pay-as-you-go racks, compliance software, and white-glove logistics. Public health agencies bolster emergency stockpiles, and logistics providers integrate temperature-controlled cross-docks to streamline downstream distribution.

By Storage Temperature Range: Ultra-Low Dominates While Cryogenic Accelerates

Ultra-low cabinets between −60 °C and −90 °C captured 43.54% of 2024 revenue within the medical cold storage market, buoyed by vaccine and cell therapy volumes that require precise temperature holds. Manufacturers deploy cascade compressors and thin-wall insulation to reduce energy intensity, a must as electricity tariffs rise. Conventional 2-8 °C refrigeration persists in absolute volume leadership for oral vaccines and insulin analogs but contributes less margin per cubic foot. Frozen storage at −20 °C backs blood product logistics, while controlled room-temperature bays equipped with passive monitors ensure tablet stability in hot climates.

Cryogenic capacity below −150 °C logs the fastest 10.24% CAGR, with demand fueled by CAR-T therapies, induced pluripotent stem cell lines, and organ preservation research. Smart LN₂ feeders, oxygen-deficiency alarms, and vacuum-insulated transfer hoses are now standard features, reflecting operational learning curves. Future growth hinges on modular systems that combine multiple temperature zones under a single monitoring dashboard.

Geography Analysis

North America held 32.47% share of the medical cold storage market in 2024 thanks to a robust biopharmaceutical ecosystem, stringent FDA temperature-control guidance, and heavy federal funding for pandemic readiness. The United States concentrates advanced GMP freezer farms around Boston, Philadelphia, and the San Francisco Bay Area, while Canada builds out ultra-low depots to support its expanding mRNA vaccine manufacturing hubs. Mexico’s public-sector modernization programs focus on solar-backed refrigerators in rural clinics and new cross-dock freezers near the U.S. border, improving regional vaccine coverage.

Asia-Pacific is poised for a swift 9.23% CAGR through 2030 as China scales national cold-chain regulations and invests in AI-enabled warehousing for biologics. Japanese universities partner with industry to commercialize artificial blood substitutes that could reshape plasma logistics once approved, a development that may add niche temperature requirements. India’s governmental emphasis on extended immunization programs stimulates demand for village-level refrigerators, while private vaccine exporters install high-density freezer racks in Hyderabad and Pune. South Korea and Australia keep upgrading ultra-low fleets to back cell therapy clinical trials, further reinforcing regional momentum.

Europe remains a mature yet technologically evolving arena where F-gas reductions force accelerated adoption of propane and CO₂ systems. Germany leads installations of energy-recovering ultra-low compressors, France pilots blockchain traceability for pharmacy fridges, and the United Kingdom tests autonomous mobile freezers for intra-hospital transfers. In Southern Europe, stimulus funding targets replacement of aging vaccine coolers with lockable, networked units. The Middle East and Africa benefit from Global Alliance for Vaccines and Immunization grants that finance solar direct-drive refrigerators and technician training, while South America accelerates modernization of blood bank infrastructure in Brazil and Argentina to meet rising elective procedure volumes.

Competitive Landscape

Competition in the medical cold storage market centers on technological capabilities, geographic reach, and environmental compliance. Lineage Logistics and Americold collectively control a majority of North American refrigerated warehouse capacity, using scale to negotiate long-term contracts with vaccine producers and plasma fractionators. UPS Healthcare added European depth by purchasing Frigo-Trans and BPL, and bolstered North American reach through the CAD 2.2 billion acquisition of Andlauer Healthcare Group in 2025, aiming to double healthcare revenue by 2026. DHL’s takeover of CRYOPDP extends its network to 15 countries and more than 600,000 specialty shipments each year, sharpening rivalry for clinical-trial logistics contracts.

Equipment manufacturers jockey to launch propane-charged freezers that match legacy performance yet remain within tightening GWP caps. Innovation skews toward energy-efficient compressors, vacuum-insulated panels, and integrated IoT gateways that feed live metrics into AI dashboards. Component vendors experiment with phase-change eutectic plates that can stabilize temperatures during grid outages, a feature popular in emerging markets. Service providers layer value by bundling validation, monitoring software, and emergency response teams into multi-year subscriptions, locking in clients and smoothing revenue.

New entrants focus on region-specific pain points. African startups deploy solar-powered mini cold rooms for rural vaccine programs, while Latin American firms assemble locally to bypass import duties and shorten lead times. Chinese automation suppliers offer robotic handling modules that retrofit into existing freezer farms, appealing to labs grappling with manpower shortages. With specialist skill sets becoming scarce, mergers and acquisitions continue as incumbents secure technician pools and proprietary software to protect competitive positions.

Medical Cold Storage Industry Leaders

PHC Holdings Corp.

Thermo Fisher Scientific Inc.

Merck KGaA

Haier Biomedical

Helmer Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Almac Clinical Services tripled −15 °C to −25 °C secondary packaging capacity and doubled ultra-low storage space at its Craigavon headquarters.

- March 2025: DHL acquired CRYOPDP, bringing 15-country coverage and 600,000 annual life-science shipments into its network.

- January 2025: UPS completed acquisitions of Frigo-Trans and BPL, adding six temperature zones of warehousing and Pan-European transportation solutions.

Global Medical Cold Storage Market Report Scope

| Medical-grade Refrigerators | Pharmacy / Vaccine Refrigerators |

| Blood-Bank Refrigerators | |

| Laboratory / General-Purpose Refrigerators | |

| Freezers | Ultra-Low Temperature Freezers (-60 °C to -90 °C) |

| Low-Temperature Freezers (-20 °C to -40 °C) | |

| Cryogenic Freezers (≤-150 °C) | |

| Chest & Upright Freezers | |

| Cold Rooms & Walk-in Chambers | |

| Transportation Containers | Passive Containers |

| Active / Refrigerated Containers | |

| Cold-Storage Warehouses | |

| Monitoring Systems & Accessories |

| Vaccines |

| Blood & Blood Components |

| Cell & Gene Therapies |

| Biologics & Biopharmaceuticals |

| Diagnostic Samples |

| Organs & Tissues |

| Other Applications |

| Hospitals & Clinics |

| Blood Banks |

| Research & Academic Laboratories |

| Pharmaceutical & Biotech Companies |

| CROs & CMOs |

| Public Health Agencies |

| Logistics Providers & 3PL |

| Controlled Room Temperature (20–25 °C) |

| Cold (+2 °C to +8 °C) |

| Frozen (-20 °C) |

| Ultra-Low (-60 °C to -90 °C) |

| Cryogenic (≤-150 °C) |

| LN₂ Vapor (≈-196 °C) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Medical-grade Refrigerators | Pharmacy / Vaccine Refrigerators |

| Blood-Bank Refrigerators | ||

| Laboratory / General-Purpose Refrigerators | ||

| Freezers | Ultra-Low Temperature Freezers (-60 °C to -90 °C) | |

| Low-Temperature Freezers (-20 °C to -40 °C) | ||

| Cryogenic Freezers (≤-150 °C) | ||

| Chest & Upright Freezers | ||

| Cold Rooms & Walk-in Chambers | ||

| Transportation Containers | Passive Containers | |

| Active / Refrigerated Containers | ||

| Cold-Storage Warehouses | ||

| Monitoring Systems & Accessories | ||

| By Application | Vaccines | |

| Blood & Blood Components | ||

| Cell & Gene Therapies | ||

| Biologics & Biopharmaceuticals | ||

| Diagnostic Samples | ||

| Organs & Tissues | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Blood Banks | ||

| Research & Academic Laboratories | ||

| Pharmaceutical & Biotech Companies | ||

| CROs & CMOs | ||

| Public Health Agencies | ||

| Logistics Providers & 3PL | ||

| By Storage Temperature Range | Controlled Room Temperature (20–25 °C) | |

| Cold (+2 °C to +8 °C) | ||

| Frozen (-20 °C) | ||

| Ultra-Low (-60 °C to -90 °C) | ||

| Cryogenic (≤-150 °C) | ||

| LN₂ Vapor (≈-196 °C) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the medical cold storage market in 2030?

Forecasts place the market at USD 6.34 billion by 2030, reflecting a 6.56% CAGR from 2025.

Which segment is expected to grow fastest through 2030?

Cryogenic storage below −150 °C leads growth with a projected 10.24% CAGR, driven by cell and gene therapies.

How are refrigerant regulations influencing equipment choices?

Phase-out mandates push buyers toward natural refrigerants such as propane and CO₂, spurring accelerated freezer retrofits.

Why are CROs and CMOs increasing cold-chain investments?

Sponsors outsource clinical trials and manufacturing, prompting service providers to add ultra-low capacity and integrated monitoring.

Which region is set to record the highest growth rate?

Asia-Pacific is forecast to post a 9.23% CAGR through 2030 on expanding healthcare infrastructure and vaccine programs.

Page last updated on: