Thawing System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

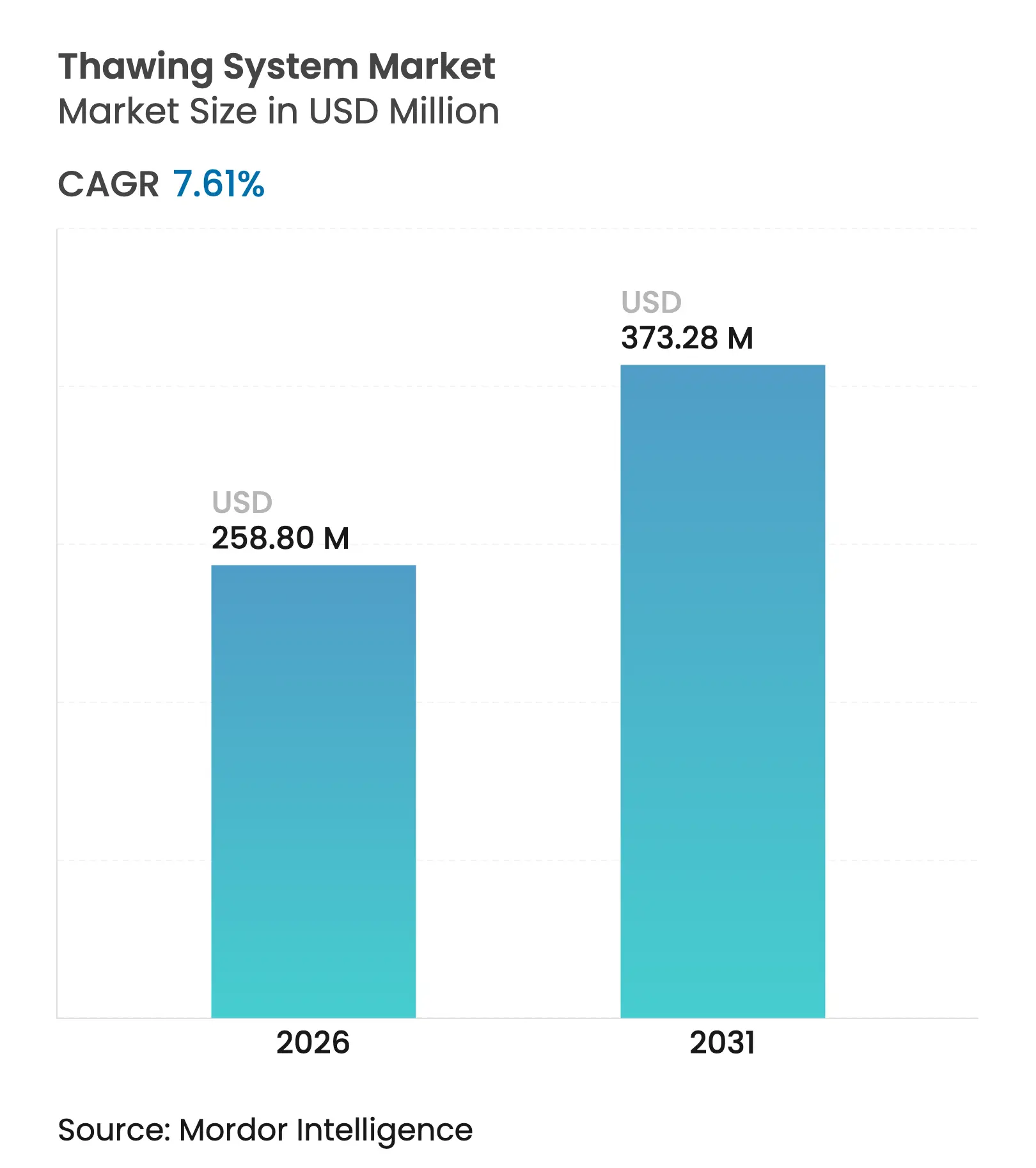

| Market Size (2026) | USD 258.8 Million |

| Market Size (2031) | USD 373.28 Million |

| Growth Rate (2026 - 2031) | 7.61 % CAGR |

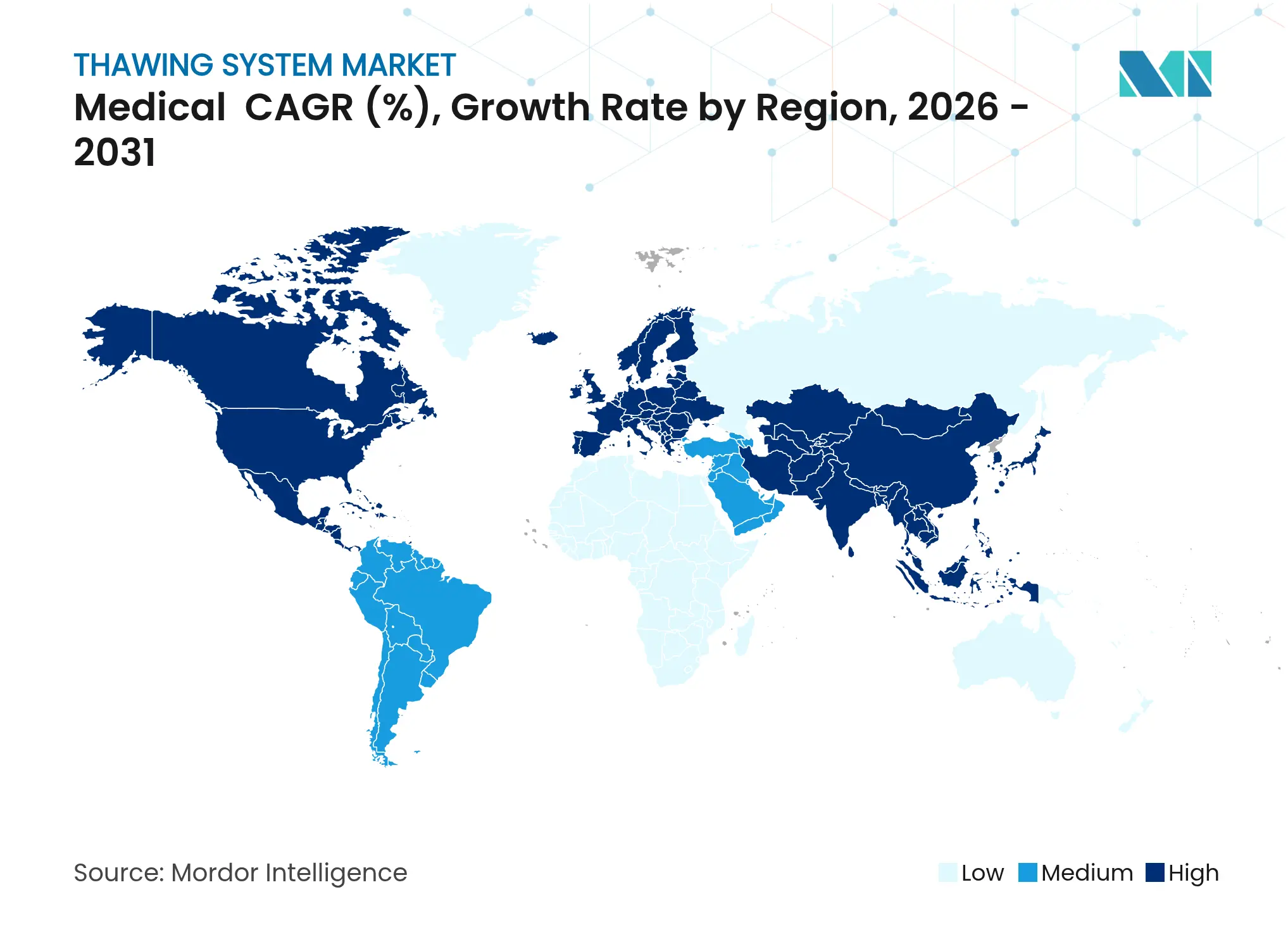

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Thawing System Market Analysis by Mordor Intelligence

Thawing system market size in 2026 is estimated at USD 258.8 million, growing from 2025 value of USD 240.5 million with 2031 projections showing USD 373.28 million, growing at 7.61% CAGR over 2026-2031. Investment in cell and gene therapies, tighter GMP expectations, and the shift toward single-use closed consumables accelerate demand for rapid and uniform thawing platforms. Regulatory momentum, including multiple FDA cell-therapy approvals in 2024–2025 and targeted device guidance on thermal effects issued in March 2024, is catalyzing the adoption of automated solutions that eradicate operator variability. North America retains leadership owing to its mature cell-therapy pipeline, yet Asia-Pacific’s expansion of biomanufacturing capacity and regulatory harmonization drives the fastest regional growth. Technology preferences are in transition: manual plate warmers still dominate, but dielectric radio-frequency (RF) systems and dry conduction platforms gain traction, especially for organ recovery and high-value biologics. End-users increasingly demand IoT-enabled units with native data-logging that streamline GMP record-keeping and create ancillary service revenues.

Key Report Takeaways

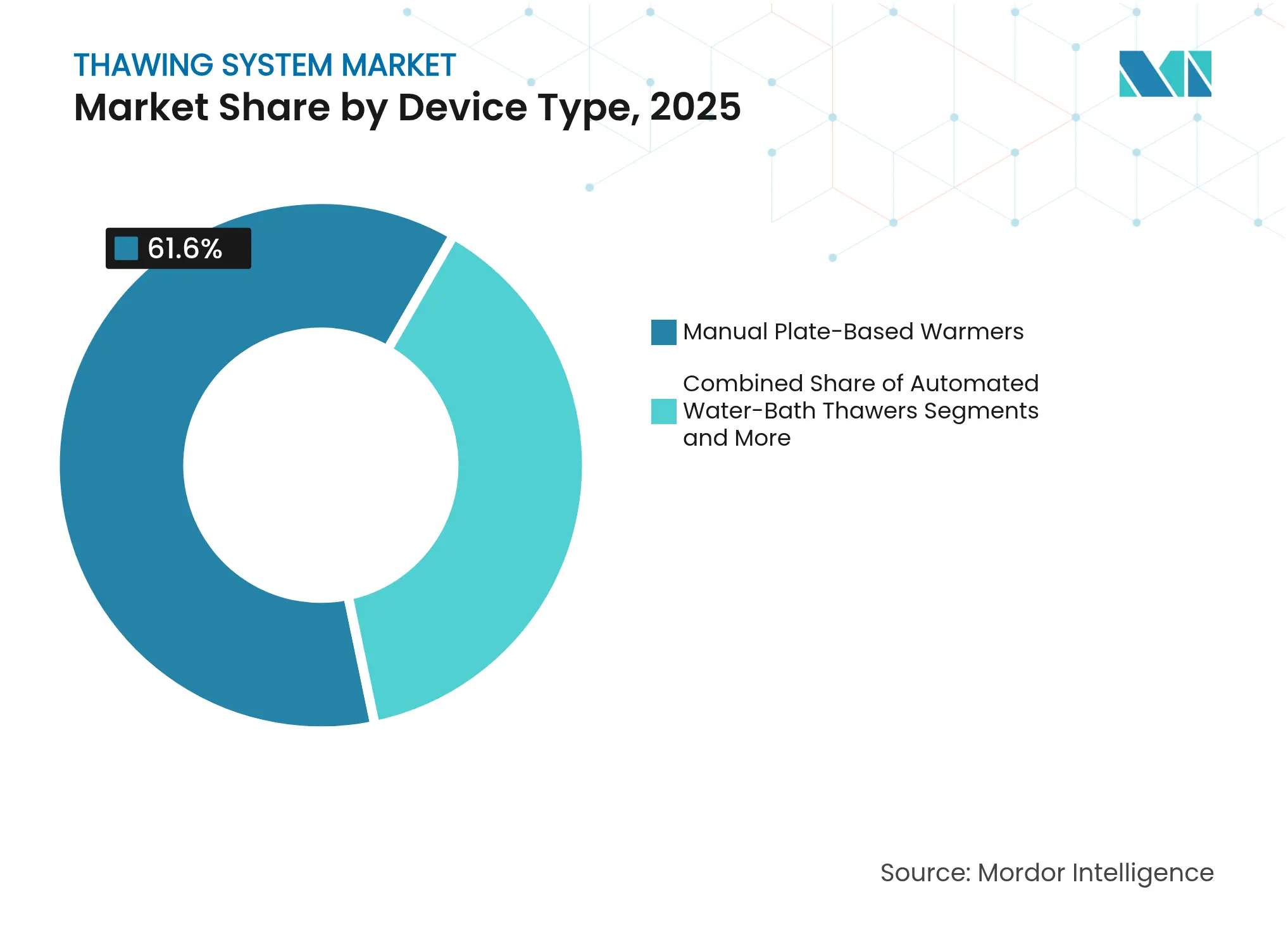

- By device type, manual plate-based warmers led with 61.60% of the thawing system market share in 2025, whereas dielectric RF thawers are projected to advance at an 7.95% CAGR through 2031.

- By sample type, blood samples accounted for 56.10% of the thawing system market size in 2025, while tissues & organs are poised for the fastest growth at a 10.02% CAGR to 2031.

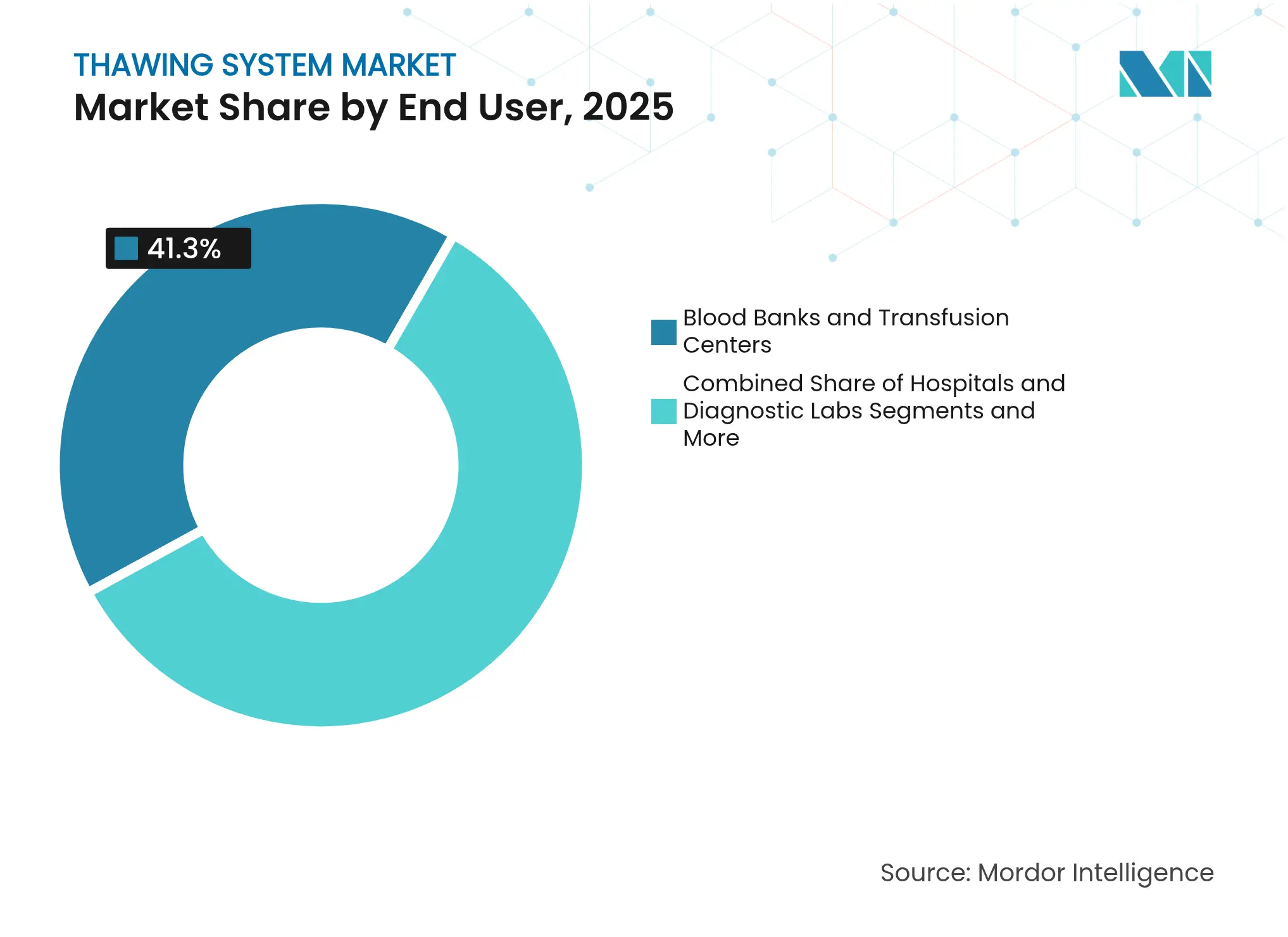

- By end-user, blood banks & transfusion centers held 41.30% revenue share in 2025; cell-therapy & biopharma manufacturers are expected to register a 9.3% CAGR over the same period.

- By thawing technology, conduction plate heating commanded 63.80% of the thawing system market share in 2025; dielectric RF warming exhibits the highest forecast CAGR at 7.95%.

- By geography, North America captured 37.80% revenue in 2025, whereas Asia-Pacific is projected to expand at an 10.68% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thawing System Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expanding cell & gene-therapy volumes require GMP-grade thawing solutions Expanding cell & gene-therapy volumes require GMP-grade thawing solutions | +2.10% | Global, concentrated in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.10% | Geographic Relevance:Global, concentrated in North America & EU | Impact Timeline:Medium term (2-4 years) |

Rising blood-component transfusions mandate standardized fast thawers Rising blood-component transfusions mandate standardized fast thawers | +1.80% | Global, higher impact in APAC & MEA | Short term (≤ 2 years) | |||

Automation reduces contamination & operator variability Automation reduces contamination & operator variability | +1.50% | North America & EU core, spill-over to APAC | Medium term (2-4 years) | |||

Dielectric RF organ-warming unlocks frozen-organ banking Dielectric RF organ-warming unlocks frozen-organ banking | +1.20% | North America & EU research centers | Long term (≥ 4 years) | |||

Single-use closed thaw bags accelerate equipment replacement Single-use closed thaw bags accelerate equipment replacement | +0.90% | Global biopharmaceutical hubs | Short term (≤ 2 years) | |||

IoT-enabled cryochain analytics create service-revenue streams IoT-enabled cryochain analytics create service-revenue streams | +0.60% | Developed markets initially, expanding globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Expanding Cell & Gene-Therapy Volumes Require GMP-Grade Thawing Solutions

FDA approvals for products such as Casgevy and Lyfgenia have locked in strict temperature windows—typically 37 °C for ≤ 20 minutes—forcing manufacturers to adopt functionally closed, automated devices that guarantee repeatability. Transfusion services increasingly manage thawing for autologous therapies because of their legacy competence in cold-chain handling. Partnerships like Cell and Gene Therapy Catapult with Asymptote demonstrate how benchtop equipment now comes with barcode traceability, audit logs, and disposable inserts to reduce contamination risk.[1]Cell and Gene Therapy Catapult, “Automated Benchtop Thawing Project Overview,” ct.catapult.org.uk Investment in these systems is further justified as accelerated review pathways reward facilities that show robust GMP controls.

Rising Blood-Component Transfusions Mandate Standardized Fast Thawers

Blockchain, RFID, and AI have modernized blood-bank logistics, creating throughput bottlenecks at thaw steps. Terumo’s Reveos automated processing platform, launched in February 2025, cuts manual touchpoints from over 20 to a handful, demanding equally swift thawing modules. High-capacity blast freezers now cool plasma to −90 °C within minutes, so downstream thawers must keep pace to sustain eight-fold productivity gains. Integration with digital inventory systems enables real-time temperature event alerts that support hemovigilance programs.

Automation Reduces Contamination & Operator Variability

Water-bath units risk cross-contamination and inconsistent warming curves. GE HealthCare’s dry VIA Thaw CB1000 offers programmable profiles and built-in data capture to ease validation burdens. STEMCELL Technologies’ ThawSTAR CFT2 posted improved recovery for peripheral blood mononuclear and pluripotent stem cells relative to baths, underscoring the viability benefits of closed, dry thawing. Robotic fill-finish lines such as Finia integrate thaw, dilution, and cryo-fill into a single module, trimming human error and aligning with continuous-manufacturing philosophies.

Dielectric RF Organ-Warming Unlocks Frozen-Organ Banking

Electromagnetic warming at 27 MHz has demonstrated kidney heating rates of 150 °C per minute, limiting devitrification and preserving tissue architecture. X-Therma’s GMP-ready XT-Thrive platform attracted USD 22.4 million in Series B funding, signalling commercial confidence in RF-driven organ revival. Novel three-phase electrode layouts now deliver 91.9% field uniformity, addressing hot-spot risk and supporting regulatory submissions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital cost of fully automated platforms High capital cost of fully automated platforms | -1.40% | Global, with higher impact in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.40% | Geographic Relevance:Global, with higher impact in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Container–device incompatibility limits workflow flexibility Container–device incompatibility limits workflow flexibility | -0.80% | Global biopharmaceutical manufacturing | Medium term (2-4 years) | |||

Uneven temperature gradients risk viability in large bags Uneven temperature gradients risk viability in large bags | -0.70% | Global, with higher impact in cell therapy manufacturing | Medium term (2-4 years) | |||

Regulatory uncertainty for dielectric organ warming Regulatory uncertainty for dielectric organ warming | -0.50% | North America & EU regulatory jurisdictions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital Cost of Fully Automated Platforms

Comprehensive units that include HEPA-filtered enclosures, IoT telemetry, and GMP-tier audit trails demand sizeable upfront budgets. Although Single Use Support’s scalable RoSS.pFTU line ranges from benchtop to 500 L, capital outlays still deter smaller clinics. Economic models indicate automated thawers shave nearly four minutes per therapeutic dose and cut medication errors by 54%, offsetting costs over time. Investor activity, such as Novo Holdings buying 60% of Single Use Support in 2024, suggests hardware prices will decline as production volumes rise.

Container–Device Incompatibility Limits Workflow Flexibility

Heterogeneous bag sizes and rigid vials often require different inserts or adapters, complicating validation. Cross-platform alliances such as Sartorius with HOF Sonderanlagenbau aim to standardize freeze-thaw consumables, yet progress remains incremental. Some innovators avoid the issue by removing freezing from the workflow altogether: DefiniGEN and Atelerix have commercialized room-temperature preservation matrices that bypass the thaw step entirely. Until standards converge, end-users must stock multiple fixtures, curbing economies of scale.

Segment Analysis

By Device Type: Automation Gains Ground Despite Manual Dominance

Manual plate warmers delivered 61.60% of 2025 revenue, underscoring entrenched use within blood centers that favor low complexity and familiar upkeep. However, dielectric RF thawers lead growth with an 7.95% CAGR as transplant programs pilot organ-banking concepts. Automated plate units and water-bath replacements serve laboratories looking for consistent run-to-run performance while keeping costs below RF platforms. The thawing system market now provides dry conduction chambers that appeal to facilities prioritizing contamination avoidance.

Adoption trends mirror tighter GMP oversight. Facilities preparing for late-stage commercial cell therapies increasingly replace manual warmers with PLC-driven devices that log every temperature excursion. The thawing system industry also experiments with magnetic nanoparticle nanowarming, which uses dispersed iron oxide particles to create volumetric heating under alternating magnetic fields. In peer-reviewed trials, the two-stage protocol maintained high post-thaw viability, pointing to future disruption once scale and regulatory hurdles are resolved.

Note: Segment shares of all individual segments available upon report purchase

By Sample Type: Tissue Applications Drive Innovation

Blood components accounted for 56.10% of 2025 sales, given the sheer volume of global transfusions and established thaw procedures. Yet tissues & organs segment posts a 10.02% CAGR, reflecting research breakthroughs that extend cold-storage horizons and enable centralized organ banks. Cell- and gene-therapy vials also expand quickly as the therapy pipeline widens, demanding precise, repeatable thawing to protect potency. Embryos and oocytes remain niche but vital, and modified rehydration protocols now improve oocyte survival to 89.8% post-thaw.

Sample diversity pushes vendors to diversify formats. Supercooling extends red-blood-cell storage to 63 days at −8 °C, which means thaw workflows must ensure gentle re-warming to avoid hemolysis. Isochoric preservation, applying constant-volume pressure rather than ice formation, may eliminate classical thaw steps for organs, upending established device design. Such paradigm shifts create incremental demand as laboratories invest in hybrid systems that can thaw traditional bags today yet evolve for next-generation protocols tomorrow.

By End-User: Biopharmaceutical Manufacturing Accelerates

Blood banks and transfusion centers controlled 41.30% of 2025 turnover because of routine plasma and cellular-component workflows. Hospitals and diagnostic laboratories follow, using thawers for point-of-care applications from trauma resuscitation to stem-cell infusions. Research institutes serve as early adopters of novel technologies such as nanowarming, validating their performance in controlled environments. IVF clinics rely on small-batch units tuned for gamete and embryo handling.

Cell-therapy and biopharma manufacturers present the steepest curve, growing at 9.3% CAGR. Their multi-lot commercial processes mandate GMP recording and full electronic batch records. Thermo Fisher’s 2025 Wisconsin lab expansion focusing on biologic characterization illustrates the infrastructure wave that underpins new demand. Century Therapeutics’ iPSC-based allogeneic pipeline likewise calls for high-throughput, closed thawers that dovetail with robotic fill-finish systems. As more therapies shift from clinical to commercial scale, equipment refresh cycles shorten, reinforcing replacement revenues.

Note: Segment shares of all individual segments available upon report purchase

By Thawing Technology: Electromagnetic Methods Gain Momentum

Conduction plate heating supplied 63.80% of 2025 revenue due to its low risk profile and simple validation path. Water-bath circulation persists where legacy infrastructure remains. Convective air warming and infrared systems occupy specialized niches demanding uniform gradients. Dielectric RF warming, however, is growing at an 7.95% CAGR as organ-banking studies confirm rapid, homogeneous heating with minimal thermal stress.

Recent work improved field uniformity to over 90%, using three-phase circular electrodes that diminish edge effects. The thawing system market size for dielectric RF applications in organ preservation is forecast to expand materially once FDA pathways clarify performance testing expectations. Meanwhile microwave systems have demonstrated 300–500 °C per minute tissue warming but still require sophisticated real-time control to manage hotspots. Vendors racing to combine RF and microwave elements may eventually deliver hybrid platforms for broad specimen categories.

Geography Analysis

North America contributed 37.80% revenue in 2025. The region benefits from concentrated cell-therapy innovators, abundant GMP-grade contract manufacturing, and clear agency guidance on device thermal profiles. Temporary FDA staffing reductions in late 2024 raised review times, yet rigorous submissions also enhance equipment credibility once cleared. Canada’s public health¬care networks continue to pilot portable thawers for rural transfusion hubs, further reinforcing regional uptake.

Europe ranks second in value, aided by stringent Medical Device Regulation that rewards manufacturers with mature quality systems. Initiatives such as the Cell and Gene Therapy Catapult’s collaboration with Asymptote demonstrate public-private efforts to accelerate compliant automation. Getinge’s 2024 Paragonix acquisition adds an organ transport portfolio, tightening integration between storage, shipping, and thaw steps. Energy-saving policies also spur interest in isochoric refrigeration, which lowers facility operating costs by up to 70% while aligning with EU sustainability targets.

Asia-Pacific is the fastest climber, projected at 10.68% CAGR for 2026–2031. China’s device market, expected to hit EUR 30 billion, is buoyed by refreshed NMPA regulations that shorten foreign-device registration cycles. Japan is tackling its approval lag through accelerated pathways, opening earlier windows for advanced thawers. Regional cell-therapy centers in South Korea and Singapore anchor demand for fully automated, humidity-controlled equipment connected to national traceability platforms. The thawing system market thus faces its richest growth opportunity across Asia-Pacific’s upgraded biomanufacturing corridors.

Competitive Landscape

Market Concentration

The competitive field is moderately fragmented. Established incumbent portfolios dominate blood-bank lines, while specialist entrants compete in cell-therapy and organ-banking niches. Consolidation among full-line life-science suppliers continues: Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification and filtration assets broadens its end-to-end offering and pulls thawing equipment into a wider single-use ecosystem. BioLife Solutions, already strong in cryogenic freezers, has expanded through acquisitions of Stirling Ultracold and PanTHERA CryoSolutions, targeting an integrated chain from freeze to final thaw.

Automation and digital integration drive competition. GE HealthCare, Terumo BCT, and Single Use Support embed track-and-trace software layers that feed directly into electronic batch-record systems. Start-ups like X-Therma and Pluristyx differentiate through RF warming and cryoprotective media that reduce DMSO residuals, carving high-margin niches.

White-space opportunities remain around IoT software service contracts that monetize temperature-trace datasets, and within dielectric RF organ-warming where clinical validation is early but strategic interest high.

Thawing System Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Abeona Therapeutics received FDA approval for ZEVASKYN (prademagene zamikeracel), the first cell-based gene therapy for recessive dystrophic epidermolysis bullosa, requiring specialized thawing protocols for genetically modified patient skin cells.

- March 2025: DHL Group acquired CRYOPDP from Cryoport to strengthen pharma logistics, handling over 600,000 temperature-controlled shipments annually across 15 countries.

- March 2025: Teknova and Pluristyx launched the PluriFreeze cryopreservation system to accelerate cell-therapy development and support high-viability thaw outcomes.

- February 2025: Terumo Blood and Cell Technologies introduced the Reveos Automated Blood Processing System in the United States, reducing processing steps and improving blood-center efficiency.

Table of Contents for Thawing System Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Expanding Cell & Gene-Therapy Volumes Require GMP-Grade Thawing Solutions

- 4.2.2Rising Blood-Component Transfusions Mandate Standardized Fast Thawers

- 4.2.3Automation Reduces Contamination & Operator Variability

- 4.2.4Dielectric RF Organ-Warming Unlocks Frozen-Organ Banking

- 4.2.5Single-Use Closed Thaw Bags Accelerate Equipment Replacement

- 4.2.6IoT-Enabled Cryochain Analytics Create Service-Revenue Streams

- 4.3Market Restraints

- 4.3.1High Capital Cost Of Fully Automated Platforms

- 4.3.2Container-Device Incompatibility Limits Workflow Flexibility

- 4.3.3Uneven Temperature Gradients Risk Viability In Large Bags

- 4.3.4Regulatory Uncertainty For Dielectric Organ Warming

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Device Type

- 5.1.1Manual Plate-Based Warmers

- 5.1.2Automated Plate-Based Warmers

- 5.1.3Automated Water-Bath Thawers

- 5.1.4Dry-Conduction Thawers

- 5.1.5Dielectric RF Thawers

- 5.1.6Others

- 5.2By Sample Type

- 5.2.1Blood

- 5.2.2Cell & Gene-Therapy Vials

- 5.2.3Embryos & Oocytes

- 5.2.4Tissues & Organs

- 5.2.5Others

- 5.3By End-User

- 5.3.1Hospitals & Diagnostic Labs

- 5.3.2Blood Banks & Transfusion Centers

- 5.3.3Cell-Therapy & Biopharma Manufacturers

- 5.3.4IVF & Fertility Centers

- 5.3.5Research Institutes

- 5.3.6Others

- 5.4By Thawing Technology

- 5.4.1Conduction Plate Heating

- 5.4.2Water-Bath Circulation

- 5.4.3Dielectric RF Warming

- 5.4.4Convective Air Warming

- 5.4.5Microwave / Infra-Red

- 5.4.6Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Helmer Scientific

- 6.3.2Sartorius AG

- 6.3.3Boekel Scientific

- 6.3.4Barkey GmbH & Co. KG

- 6.3.5BioLife Solutions

- 6.3.6Terumo Corporation

- 6.3.7Cardinal Health

- 6.3.8Sarstedt AG & Co. KG

- 6.3.9CytoTherm

- 6.3.10Single Use Support

- 6.3.11Thermo Fisher Scientific

- 6.3.12GE HealthCare

- 6.3.13MedCision LLC

- 6.3.14Plasma Solutions

- 6.3.15REM? Group

- 6.3.16Stericox India

- 6.3.173M Company

- 6.3.18Drägerwerk AG & Co. KGaA

- 6.3.19Eppendorf SE

- 6.3.20Praxair Cryogenics

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical thawing system market as electrically powered table-top or floor-standing equipment that gently raises frozen biological materials (blood components, cell-therapy vials, embryos, tissues, and organs) to a uniform, ice-free condition suitable for immediate downstream use.

Scope exclusion: we deliberately omit large-scale industrial food thawing lines and generic laboratory hot plates to maintain clinical relevance.

Segmentation Overview

- By Device Type

- Manual Plate-Based Warmers

- Automated Plate-Based Warmers

- Automated Water-Bath Thawers

- Dry-Conduction Thawers

- Dielectric RF Thawers

- Others

- Manual Plate-Based Warmers

- By Sample Type

- Blood

- Cell & Gene-Therapy Vials

- Embryos & Oocytes

- Tissues & Organs

- Others

- Blood

- By End-User

- Hospitals & Diagnostic Labs

- Blood Banks & Transfusion Centers

- Cell-Therapy & Biopharma Manufacturers

- IVF & Fertility Centers

- Research Institutes

- Others

- Hospitals & Diagnostic Labs

- By Thawing Technology

- Conduction Plate Heating

- Water-Bath Circulation

- Dielectric RF Warming

- Convective Air Warming

- Microwave / Infra-Red

- Others

- Conduction Plate Heating

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

To close gaps, we spoke with biomedical engineers, transfusion supervisors, and cell-therapy process owners across North America, Europe, and Asia. Their feedback on average thaw cycles, device replacement intervals, and emerging dielectric designs sharpened assumptions and anchored price bands.

Desk Research

In desk research, our analysts drew foundational figures from trusted, non-paywalled sources such as the WHO Blood Safety database, AABB transfusion statistics, FDA 510(k) clearances, Eurostat trade codes, and peer-reviewed cryobiology journals that quantify failure modes and thaw times.

Mordor analysts enrich those public insights with subscription intelligence from D&B Hoovers and Factiva, manufacturer filings, investor decks, regional blood-bank portals, and shipment traces from Volza, ensuring every variable sits on multiple data pillars. The examples cited are illustrative, and many other documents informed data validation.

Market-Sizing & Forecasting

Mordor's model begins with a top-down reconstruction of demand using global blood collection volumes, hematology lab counts, cord-blood bank capacity, and reimbursement penetration. These pools are pressure-tested through selective bottom-up supplier roll-ups and sample ASP × unit checks to fine-tune totals. Forecasts employ multivariate regression that links device shipments to elective-surgery growth, stem-cell trial starts, and capital-equipment budgets, producing an 8.1% CAGR our expert panel judged realistic.

Data Validation & Update Cycle

Before publication, we run variance scans, reroute anomalies for senior review, and update the spreadsheet if fresh regulatory alerts or recall notices surface. Only after these independent checks are cleared do we release the final dataset, and Mordor refreshes every twelve months while issuing interim bulletins for material events.

Why Mordor's Thawing System Baseline Inspires Global Confidence

Benchmark comparison

Published estimates often diverge because firms adopt different sample universes, device categories, and year-end conversions. We acknowledge these realities up front and show how each choice nudges the final dollar value.

Key gaps arise when other publishers restrict scope to manual warmers, omit emerging dielectric RF units, rely solely on manufacturer revenue reports, or freeze exchange rates at survey launch. Mordor includes the full device spectrum, adjusts for local currency swings, and benefits from an annual refresh cadence.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 240.5 M (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 221.9 M (2024) | Global Consultancy A | Excludes dielectric RF and tissue thawers; uses manufacturer revenue only | ||

USD 111.98 M (2024) | Trade Journal B | Focuses on blood products and high-income regions only | ||

USD 97.51 M (2024) | Industry Portal C | Counts manual devices and omits advanced sample types |