Disposable Medical Supplies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

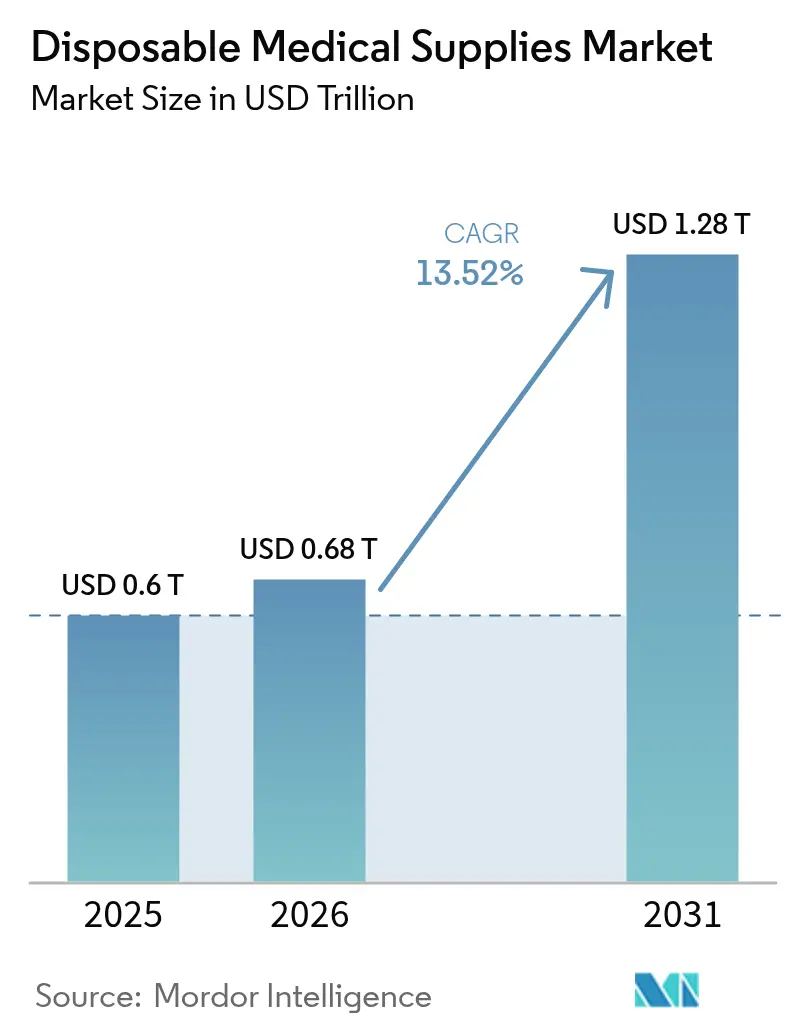

| Market Size (2026) | USD 0.68 Trillion |

| Market Size (2031) | USD 1.28 Trillion |

| Growth Rate (2026 - 2031) | 13.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Medical Supplies Market Analysis by Mordor Intelligence

The disposable medical supplies market size was valued at USD 0.60 trillion in 2025 and estimated to grow from USD 0.68 trillion in 2026 to reach USD 1.28 trillion by 2031, at a CAGR of 13.52% during the forecast period (2026-2031). Growth is fueled by stringent infection-control requirements introduced after COVID-19, accelerating a long-term pivot from reusable to single-use products. Revised Joint Commission standards that took effect in July 2024 shifted procurement decisions toward infection prevention rather than unit price. Hospital decision-makers now weigh total cost of ownership, including sterilization labor, equipment depreciation, and liability when favoring disposables. Simultaneously, Extended Producer Responsibility (EPR) rules in major regions reward biopolymers and recyclable formats, pushing manufacturers to overhaul material portfolios. On the supply side, tariffs on Chinese gloves and masks rising to 100% and 50% respectively by 2026 are prompting the United States to reshore investments that reinforce regional supply assurance.

Key Report Takeaways

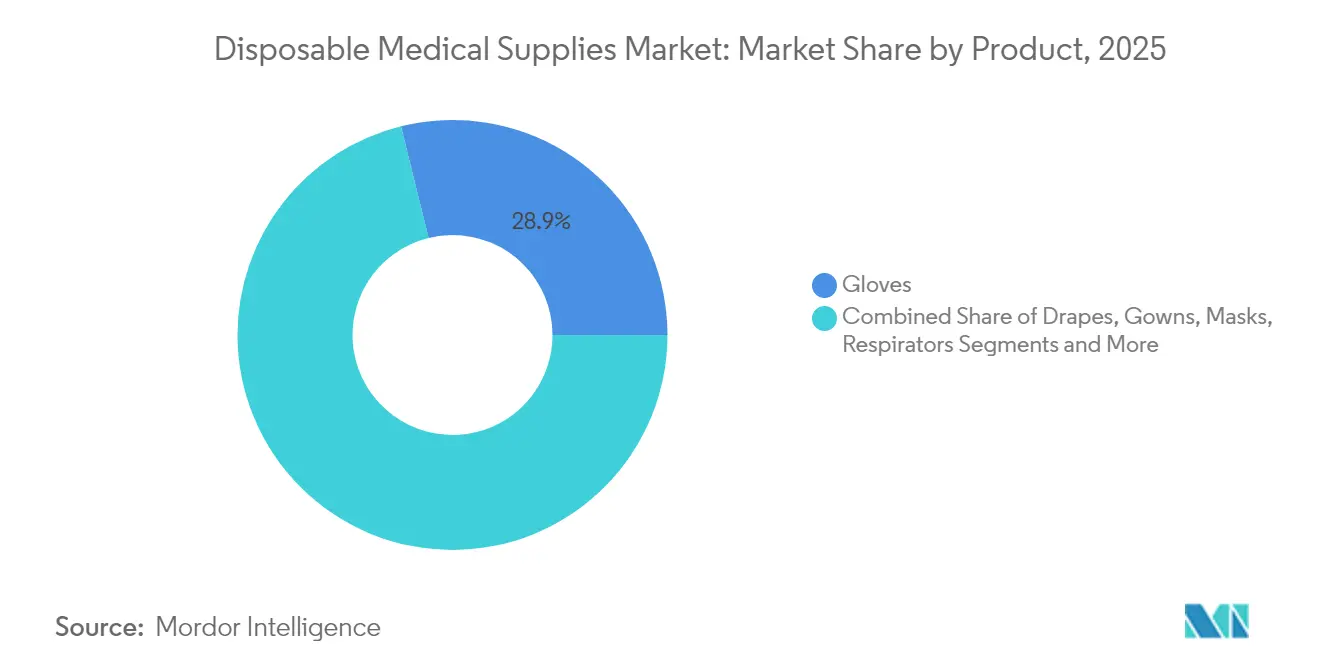

- By product type, gloves led the disposable medical supplies market with 28.85% share in 2025, while biodegradable gloves are on track for an 11.52% CAGR to 2031.

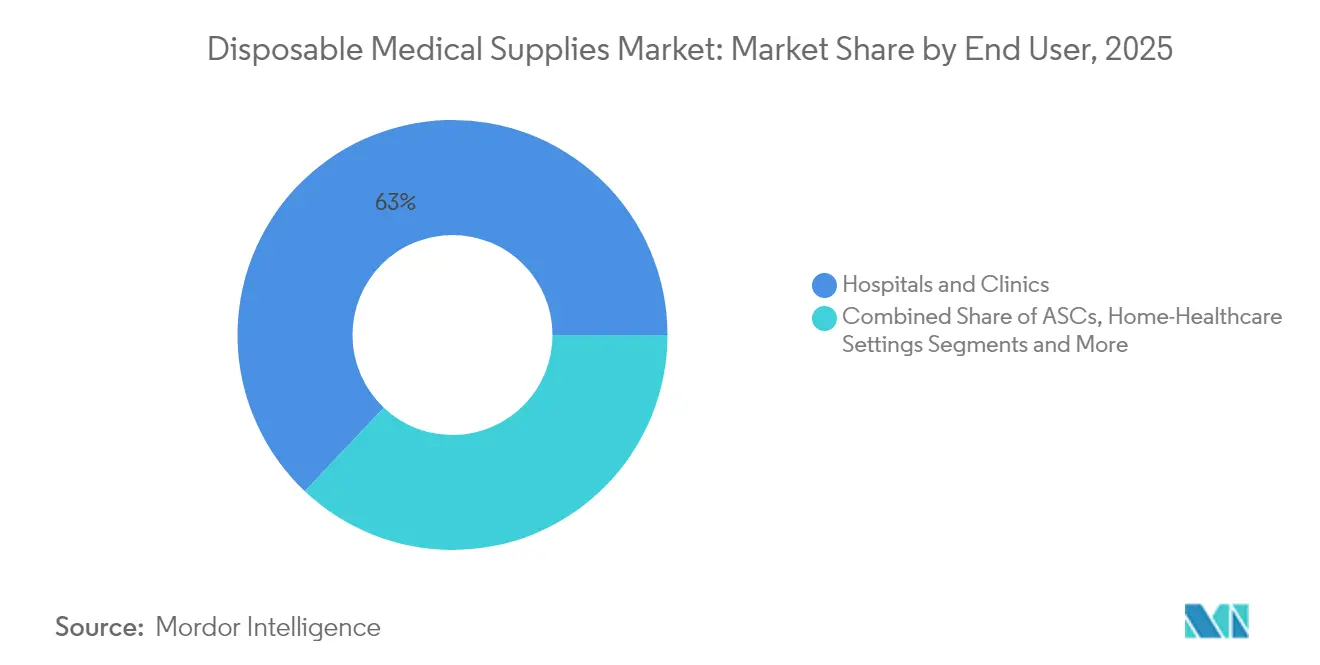

- By end user, hospitals and clinics accounted for 62.95% of the disposable medical supplies market in 2025; home health care is expanding at 9.38% CAGR through 2031.

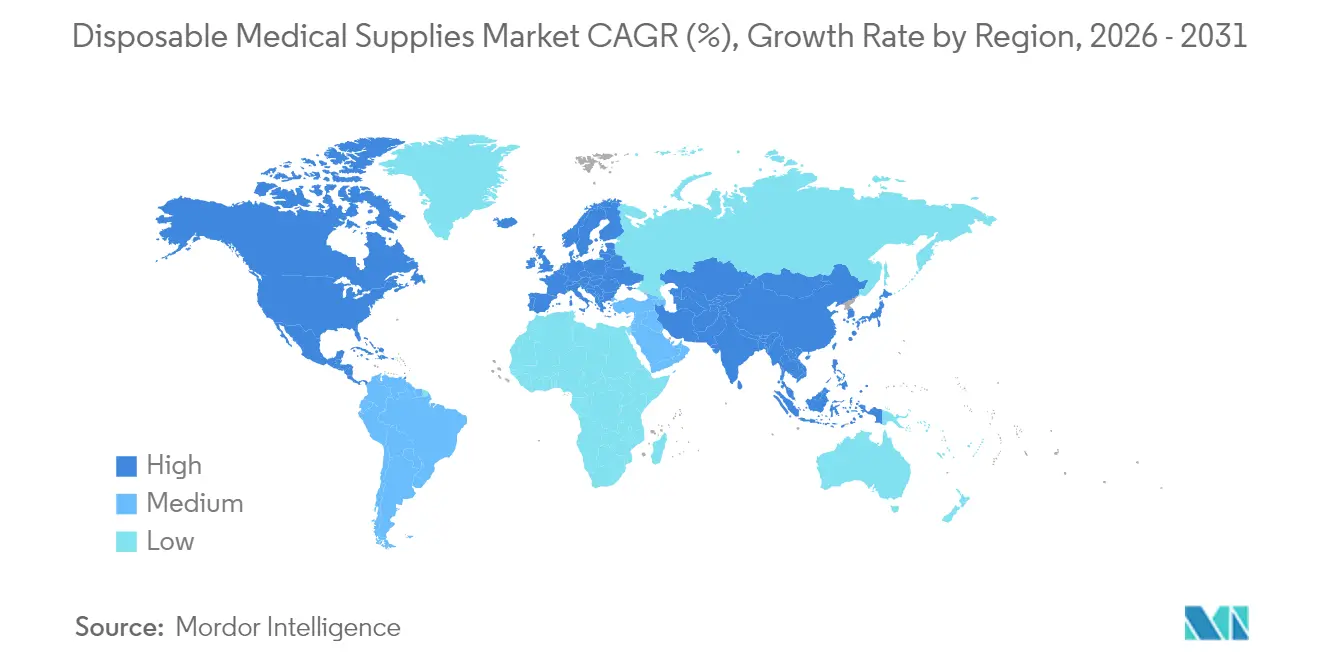

- By region, North America commanded 37.05% revenue share in 2025, whereas Asia-Pacific is forecasting a 7.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Disposable Medical Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Infection-Control Norms In Post-COVID Healthcare Systems | +2.80% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Rapid ASC (Ambulatory Surgery Center) Expansion In OECD Countries | +2.10% | OECD countries, particularly North America | Medium term (2-4 years) |

| Home-Based Chronic-Care Boom Driving Single-Use Kits | +1.90% | Global, with emphasis on developed markets | Long term (≥ 4 years) |

| Growth Of Point-Of-Care Diagnostics Using Disposable Sensors | +1.40% | Global, with early adoption in North America & Europe | Long term (≥ 4 years) |

| Biodegradable Bio-Polymer Breakthroughs Lowering Eco-Concerns | +1.20% | Europe leading, expanding to North America & APAC | Long term (≥ 4 years) |

| Reshoring Of Med-Tech Manufacturing In US & EU Boosting Demand For Sterile Packaging | +0.90% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Infection-Control Norms

Healthcare organizations have locked in post-pandemic protocols that prioritize disposable supplies to curb cross-contamination. The Joint Commission cut 70% of process checks but tightened surface-cleaning outcomes, driving hospitals to replace reusable items with single-use equivalents.[1]Frontiers in Nanotechnology, “Nanobiosensors for Point-of-Care Diagnostics,” frontiersin.orgThe shift now extends to general wards where disposable gowns, drapes, and diagnostics are routine. Budget holders factor avoidance of sterilization downtime and litigation costs when justifying higher per-unit spending. Compliance scores tied to patient satisfaction further anchor demand for disposables across the disposable medical supplies market.

Rapid ASC Expansion

Ambulatory surgery centers continue to gain payer support for orthopedics and cardiology procedures. Lean staffing and rapid case turnover require pre-sterile kits that eliminate reprocessing delays. ASCs typically lack in-house sterilizers, so disposable kits speed room turnover and minimize overhead. Reimbursement shifts that incentivize outpatient care strengthen volume, boosting specialized packs containing drapes, catheters, and single-use instruments. The disposable medical supplies market gains a lasting tailwind as ASC footprints widen across OECD nations.

Home-based Chronic-Care Boom

Home settings lack sterile processing, so caregivers favor single-use wound dressings, injection devices, and monitoring kits. “Hospital at Home” programs extend the complexity of services delivered in residences, demanding ready-to-use disposable kits. Caregiver shortages boost demand for intuitive devices that reduce training time. This migration underpins long-term growth across the disposable medical supplies market.

Growth of Point-Of-Care Diagnostics

Miniaturized sensors now deliver laboratory-quality tests bedside through single-use cartridges.[2]AAMI News, “Medical Plastic Waste in Acute Care,” aami.org BD’s MiniDraw capillary collection system matches venous-draw accuracy, letting pharmacies and clinics deploy rapid diagnostics. Eliminating transport and batching delays justifies per-test disposable costs. Retail clinics and home users are adopting these devices, expanding the disposable medical supplies market into new care venues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-Fill Taxes & EPR Laws Escalating Disposal Costs | -1.80% | Europe leading, expanding to North America | Medium term (2-4 years) |

| Price Compression From Bulk GPO Tenders In North America | -1.20% | North America, with spillover to other regions | Short term (≤ 2 years) |

| Sterilization Capacity Bottlenecks Delaying Product Launches | -1.50% | Global, with highest impact in North America & Europe | Short term (≤ 2 years) |

| Volatility In Nitrile & Latex Prices Impacting Margins | -1.10% | Global, with manufacturing concentration in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Landfill Taxes & EPR Laws Escalating Disposal Costs

The EU Packaging and Packaging Waste Regulation mandates recyclability by 2030 and shifts disposal fees to producers from August 2026. Healthcare already generates nearly 6 million tons of waste annually, of which fewer than 1% of plastics are recycled.[3]Joint Commission, “New Infection Prevention and Control Standards Effective July 2024,” jointcommission.orgManufacturers of traditional PVC gloves face rising levies that erode margins. Providers add waste charges into purchasing decisions, tempering the adoption of non-sustainable disposables in cost-sensitive segments of the disposable medical supplies market.

Price Compression from Bulk GPO Tenders in North America

Group Purchasing Organizations handle more than 85% of U.S. hospital procurement and deliver 13.1% average savings that are extracted directly from supplier pricing. Contracts often lock prices for up to three years, limiting inflation pass-through. This environment favors incumbents with scale while raising barriers for innovative newcomers who lack volume discounts. Margin pressure can slow R&D spending and dampen premium product uptake within the disposable medical supplies market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gloves Sustain Leadership While Bio-Based Variants Surge

The gloves segment generated 28.85% of the disposable medical supplies market revenue in 2025 and remains central to everyday clinical routines. Usage frequency rose sharply after COVID-19, and elevated volumes have normalized at higher baselines. Biodegradable gloves are scaling quickly, registering an 11.52% CAGR that outpaces all other sub-categories. Their momentum reflects imminent EPR fees on traditional nitrile and latex waste. Procedure kits and trays also benefit from ambulatory surgery center growth, as pre-pack builds streamline room turnover. Drapes and gowns ride the same efficiency trend, whereas masks and respirators, though moderating from pandemic peaks, still post healthy demand given occupational safety standards. Needles and syringes post stable gains, tied to chronic-care injections migrating into homes. Catheter makers face PTFE supply constraints, prompting capacity investments and alternative materials development.

Innovators are advancing nanofiber wound dressings and connected single-use sensors that report data to electronic records, broadening the category. Evonik’s RESOMER polymer platform illustrates how material science responds to dual performance and sustainability targets. As more hospitals link purchasing to waste disclosure, bio-based lines gain shelf space. Consequently, the disposable medical supplies market size for biodegradable gloves is projected to log visible share gains by 2031.

By End User: Institutional Volume Dominates, but Home-Care Races Ahead

Hospitals and clinics accounted for 62.95% of 2025 sales across the disposable medical supplies market. Procedure intensity, combined with stringent compliance audits, drives constant restocking cycles. Providers absorb higher unit prices, citing savings from avoided reprocessing labor and infection-related penalties. Ambulatory surgery centers run leaner but fast-growing platforms that require turnkey kits and have been expanding at a 6.72% CAGR. Diagnostic laboratories depend on bulk consumables and now integrate point-of-care devices to decentralize testing.

Home-healthcare stands out with a 9.38% CAGR to 2031 as an aging population and payer policies shift chronic care delivery into residences. Limited sterile infrastructure in homes raises reliance on pre-sterile packs. Retail drugstores and urgent clinics represent further nodes that boost distributed consumption. These channels collectively expand the disposable medical supplies market footprint outside hospital walls. In turn, suppliers must adjust packaging sizes and distribution models to support small-batch, rapid-replenishment orders.

Geography Analysis

North America retained a 37.05% share of the disposable medical supplies market in 2025, thanks to strict infection-control oversight and fresh capital investments in local manufacturing. Tariffs that climb to 100% on certain Chinese gloves by 2026 spur companies such as Kimberly-Clark to pump USD 2 billion into Ohio and South Carolina plants, creating more than 900 skilled roles. Group Purchasing Organizations standardize specifications, accelerating product turnover and ensuring steady volume across the network.

Europe remains committed to sustainable healthcare procurement. EPR legislation that compels recyclable packaging by 2030 has amplified interest in bio-polymer disposable lines. Hospitals in Germany and the Nordics publish annual waste metrics, and suppliers able to lower disposal fees gain bidding advantages. While the continent’s population growth is muted, aging demographics sustain procedural volumes and drive continuous demand within the disposable medical supplies market.

Asia Pacific is expected to chart a 7.62% CAGR up to 2031, the fastest among all regions. Urbanization and rising healthcare funding expand bed capacity across China, India, Indonesia, and Vietnam. Although trade tensions redirect some export orders away from China, regional manufacturers in Malaysia and Thailand seize glove contracts to backfill U.S. demand. Meanwhile, emerging private hospitals in India adopt Western infection-control norms, boosting average per-patient disposable consumption.

Middle East and Africa, along with South America, contribute modest but rising demand as governments invest in hospital infrastructure and seek to reduce healthcare-acquired infections. Multilateral funding programs often include clauses for single-use kits to meet global accreditation benchmarks. Collectively, these developing territories add incremental volume and diversify revenue streams for suppliers active in the disposable medical supplies market.

Competitive Landscape

The disposable medical supplies market shows moderate fragmentation. Cardinal Health, Medtronic, and 3M continue to exploit scale and GPO relationships, yet none commands more than 10% individual share. BD earmarked USD 2.5 billion for U.S. expansion, underscoring the pivot toward domestic capacity. Ansell’s USD 640 million buyout of Kimberly-Clark’s PPE unit highlights ongoing consolidation aimed at portfolio breadth.

Technology is emerging as a separator. Medline collaborates with Microsoft to infuse AI into inventory platforms that predict stock-outs and automatically reorder, helping hospitals minimize emergency buys. Medtronic is paring its supplier list from 65,000 to a few strategic partners and shuttering older plants, positioning for leaner operations. Sustainability is another battleground. Only 1% of medical plastics today derive from bio-based feedstocks, giving first movers reputational currency and bidding leverage, especially in Europe.

Regulatory science is shaping product pipelines. The U.S. FDA confirmed vaporized hydrogen peroxide as a validated sterilant, opening doors for suppliers that can package devices in materials compatible with that process. Meanwhile, uncertainty over ethylene oxide restrictions poses launch risks for catheter and kit lines that still rely on legacy sterilization—firms hedge by qualifying multiple modalities to secure uninterrupted supply to the disposable medical supplies market.

Disposable Medical Supplies Industry Leaders

Cardinal Health, Inc.

3M

Molnlycke Health Care AB

Medtronic

Owens and Minor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BD confirmed USD 2.5 billion U.S. capacity investments over five years.

- April 2025: Owens & Minor arranged USD 1 billion in secured notes to acquire Rotech Healthcare Holdings, broadening home-care distribution reach.

- February 2025: Teleflex agreed to purchase BIOTRONIK’s vascular intervention unit for EUR 760 million to enhance coronary and peripheral offerings.

- January 2025: Kimberly-Clark committed USD 2 billion to expand North American manufacturing, adding a new Ohio facility and upgrading South Carolina capacity, creating 900 jobs.

Global Disposable Medical Supplies Market Report Scope

As per the scope of the report, disposable medical supplies include products that are used to prevent cross-contamination between doctors and caregivers and doctors and patients during diagnosis and treatment procedures.

The disposable medical supplies market is segmented by type, end users, and geography. By type, the market is segmented into gloves, drapes and gowns, masks, needles and syringes, procedure kits and trays, and other types. By end users, the market is segmented into hospitals and clinics, ambulatory surgery centers, and other end users. By geography, the market is segmented into North America, Europe, Asia Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Gloves |

| Drapes & Gowns |

| Masks & Respirators |

| Needles & Syringes |

| Procedure Kits & Trays |

| Catheters |

| Wound Dressings |

| Diagnostic & Sampling Disposables |

| Other Types |

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Home-Healthcare Settings |

| Diagnostic Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Gloves | |

| Drapes & Gowns | ||

| Masks & Respirators | ||

| Needles & Syringes | ||

| Procedure Kits & Trays | ||

| Catheters | ||

| Wound Dressings | ||

| Diagnostic & Sampling Disposables | ||

| Other Types | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgery Centers | ||

| Home-Healthcare Settings | ||

| Diagnostic Laboratories | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the disposable medical supplies market?

The market is valued at USD 0.68 trillion in 2026 and is projected to reach USD 1.28 trillion by 2031.

Which product category holds the largest disposable medical supplies market share?

Gloves dominate with 28.85% share in 2025, reflecting universal clinical use and strict infection-control norms.

How quickly is the home-healthcare segment growing?

Home-healthcare demand for disposables is expanding at a 9.38% CAGR through 2031 as chronic care shifts into residences.

What region is growing the fastest?

Asia-Pacific is forecast to record a 7.62% CAGR to 2031 on the back of infrastructure expansion and rising care standards.

How are sustainability regulations affecting the market?

EPR laws such as the EU Packaging and Packaging Waste Regulation effective in 2026 are driving investment into biodegradable materials and recyclable packaging, influencing product design and procurement decisions.

Why are manufacturers reshoring production?

Escalating tariffs on Chinese gloves and masks alongside pandemic-era supply shocks have spurred U.S. and European firms to build domestic plants, improving resilience despite higher operating costs.

Page last updated on: