Healthcare Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

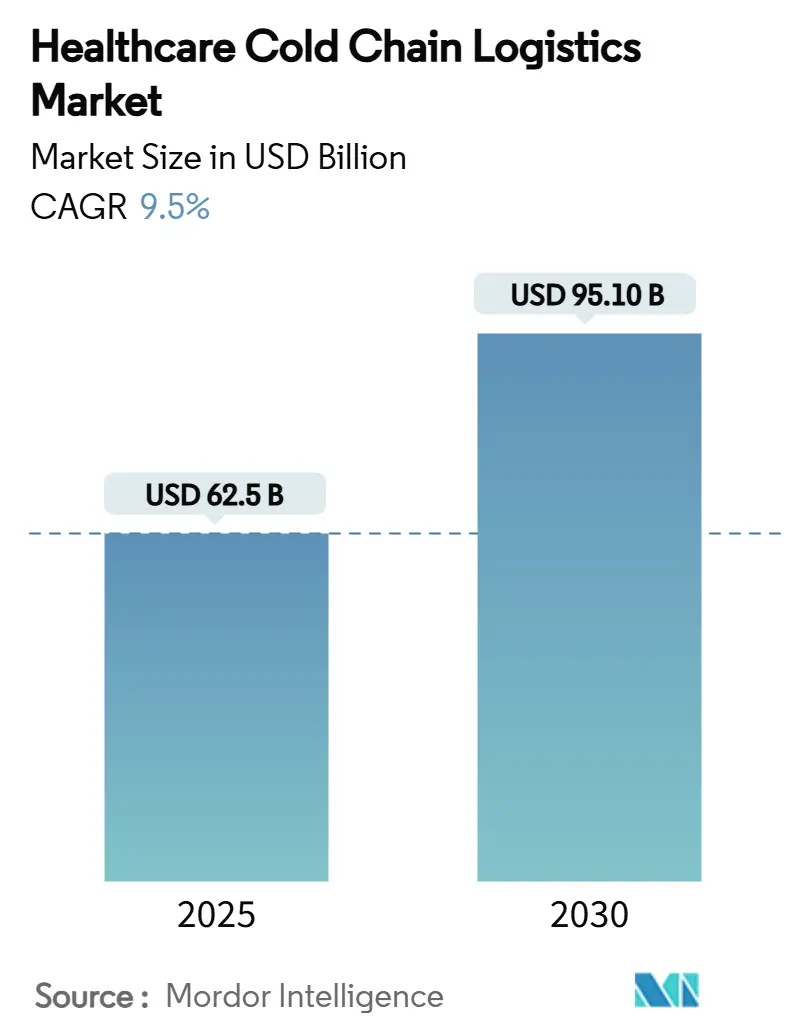

| Market Size (2025) | USD 62.5 Billion |

| Market Size (2030) | USD 95.10 Billion |

| Growth Rate (2025 - 2030) | 9.50% CAGR |

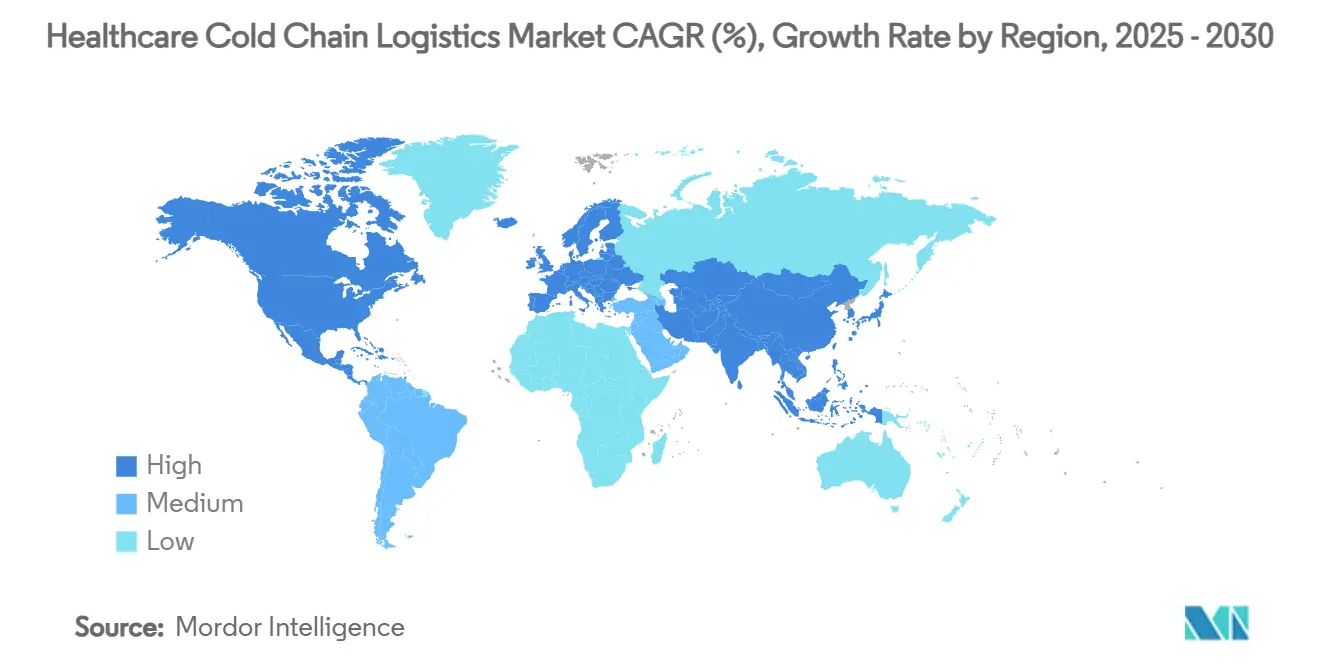

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Cold Chain Logistics Market Analysis by Mordor Intelligence

The healthcare cold chain logistics market reached USD 62.5 billion in 2025 and is forecast to hit USD 95.1 billion by 2030, translating into a robust 9.5% CAGR and cementing its position as a strategic pillar of global health supply chains. This expansion is propelled by the rapid adoption of biologics, cell and gene therapies, and personalized medicines that demand stringent temperature management throughout distribution. Pandemic-driven vaccination drives, rising regulatory scrutiny, and decentralized clinical trials that bypass traditional depot models are redefining service design. Capital commitments by leading third-party logistics (3PL) providers and government infrastructure programs are accelerating network modernization, while technology investments in IoT monitoring and blockchain documentation improve shipment visibility and compliance. However, escalating energy prices, workforce shortages in validated operations, and a rising frequency of temperature excursions add cost and risk pressures that market participants must mitigate.

Key Report Takeaways

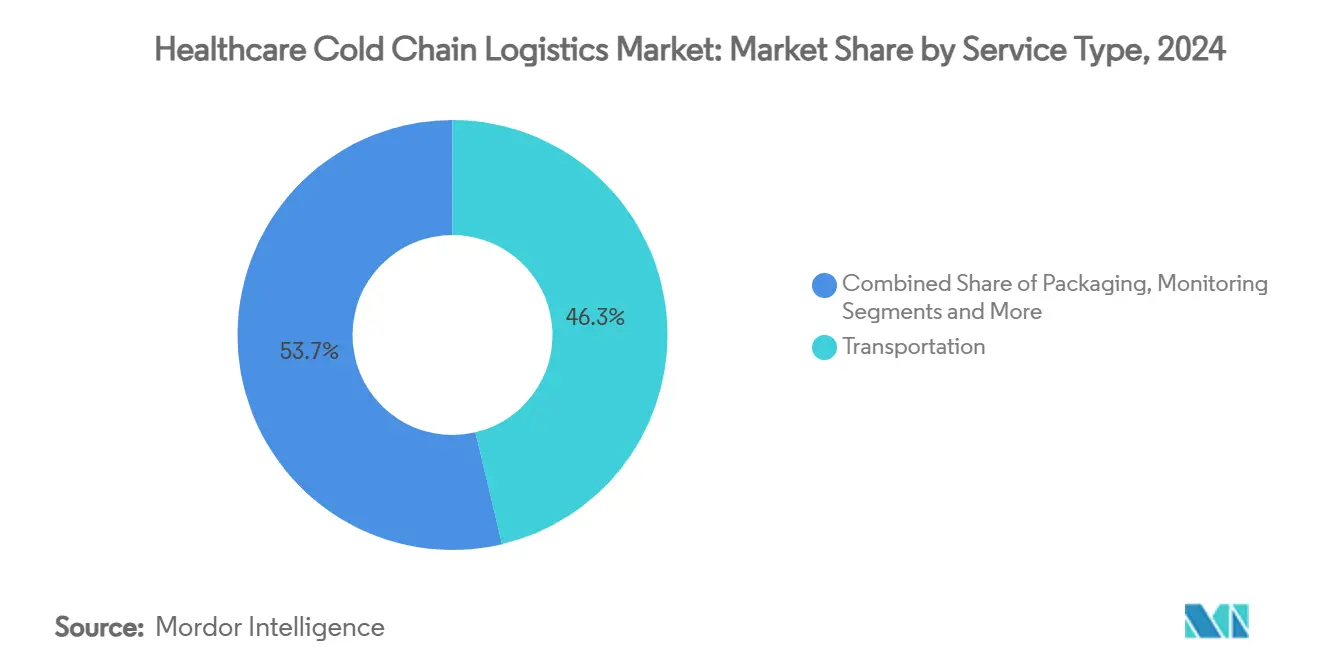

- By service type, transportation services held 46.3% of the healthcare cold chain logistics market share in 2024, whereas monitoring and data-logging services are advancing at a 12.4% CAGR through 2030.

- By product type, vaccines accounted for 38.2% of the healthcare cold chain logistics market size in 2024; cell and gene therapies are projected to expand at an 18.9% CAGR to 2030.

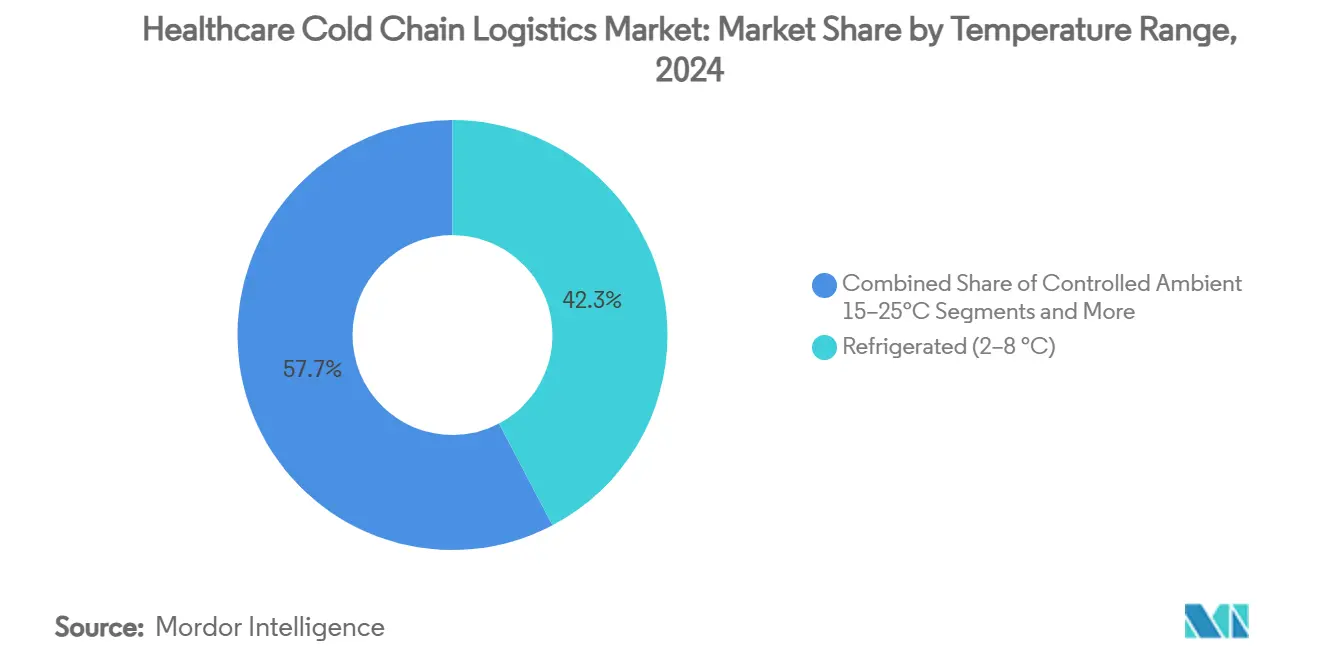

- By temperature range, refrigerated storage captured 42.3% share of the healthcare cold chain logistics market size in 2024, while cryogenic applications are growing at 21.3% CAGR through 2030.

- By transportation mode, air freight held 41.0% of the healthcare cold chain logistics market share in 2024 and is forecast to rise at a 13.7% CAGR through 2030.

- By end user, pharmaceutical and biotech manufacturers dominated with 55.7% share of the healthcare cold chain logistics market size in 2024, whereas CROs record the highest projected growth at an 11.2% CAGR through 2030.

- By geography, North America dominated with 39.6% market share in 2024, but Asia Pacific is forecast to record the highest CAGR at 9.3% through 2030.

Global Healthcare Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising biologics & specialty-pharma volumes | +2.10% | North America & EU core, emerging APAC | Medium term (2-4 years) |

| Global vaccination campaigns & pandemic stockpiles | +1.80% | Global, emphasis on emerging markets | Short term (≤ 2 years) |

| Stricter GDP/GMP regulatory enforcement | +1.20% | EU & North America core, expanding APAC | Long term (≥ 4 years) |

| Infrastructure investments by 3PL majors & governments | +1.50% | North America & APAC, selective EU | Medium term (2-4 years) |

| Decentralised clinical trials and direct-to-patient shipments | +1.30% | North America & EU, pilot APAC | Medium term (2-4 years) |

| Cell & gene therapy boom needing cryogenic logistics | +1.60% | North America & EU, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Biologics & Specialty-Pharma Volumes

Accelerated biologics approvals are increasing shipment complexity because more than 85% of these products require tight temperature control across multiple zones. Pharmaceutical firms are localizing production in Asia Pacific, where government-funded mRNA facilities underpin regional distribution hubs. Each biologic launch multiplies demand for validated storage and multi-modal transport, prompting 3PLs to expand dedicated capacity. Continuous validation across an extended supply chain has shifted investments toward end-to-end monitoring solutions that guarantee compliance. The healthcare cold chain logistics market is consequently pivoting from bulk efficiency to high-precision handling capabilities built around biologics.

Global Vaccination Campaigns & Pandemic Stockpiles

National stockpiling strategies require networks that can triple capacity within weeks, elevating cold chain assets to critical infrastructure. Thermostable formulations and agile labelling systems support the WHO 100 Days Mission, enabling near real-time adjustment of expiry dates.[1]MDPI Vaccines, “Stability Preparedness: The Not-So-Cold Case for Innovations in Vaccine Stability Modelling and Product Release,” Vaccines, mdpi.com Distributed vaccine manufacturing in Africa and Asia reduces reliance on legacy hub-and-spoke models and shortens transport legs. Operators are installing predictive maintenance and redundant power to avert costly excursions in strategic reserves. These developments collectively enlarge the addressable healthcare cold chain logistics market, especially in underserved regions.

Stricter GDP/GMP Regulatory Enforcement

Enhanced EU GDP guidelines mandate transport validation under representative climatic conditions, embedding continuous monitoring into every shipment stage. Regulators in emerging markets are aligning with these standards to attract pharmaceutical investments, tightening entry barriers for uncertified carriers. Blockchain documentation and risk-based audit trails are becoming baseline, favouring logistics providers with global compliance credentials. Regulatory convergence is also spurring consolidation, as smaller entities struggle with the capital burden of multi-jurisdictional validation.

Infrastructure Investments by 3PL Majors & Governments

DHL has earmarked EUR 2 billion through 2030 to build GDP-certified Pharma Hubs and expand ultra-low temperature storage. Parallel government efforts, such as the U.S. Zero-Emission Freight Corridor Strategy, incentivize low-carbon vehicles and renewable energy cold stores.[2]U.S. Department of Energy, “National Zero-Emission Freight Corridor Strategy,” driveelectric.gov These capital flows de-risk capacity constraints, reduce single-point failure exposure, and enable modal diversification into rail and ocean lanes. Resultant redundancy and flexibility reinforce the healthcare cold chain logistics market’s growth trajectory.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy & operating costs of cold assets | -1.40% | Global, acute in energy-intensive regions | Short term (≤ 2 years) |

| Temperature-excursion risk & product losses | -0.90% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| Skilled-labour shortages in validated cold chains | -0.80% | North America & EU, emerging APAC | Long term (≥ 4 years) |

| Costly refrigerant phase-outs for sustainability goals | -0.60% | EU & North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy & Operating Costs of Cold Assets

Electricity accounts for the largest controllable expense in cold storage, and ultra-low systems for cell therapies consume several multiples of standard refrigeration. The U.S. Department of Energy highlights geothermal and solar integration pathways that can curb power intensity in new builds.[3]U.S. Department of Energy, “Pathways to Commercial Liftoff: Geothermal Heating and Cooling,” liftoff.energy.gov Carbon-reduction mandates accelerate the shift to efficient compressors and natural refrigerants, yet they demand upfront capital that smaller operators find prohibitive. Automation offers partial relief by optimizing airflow and reducing door openings, but the payback periods remain sensitive to regional energy tariffs.

Temperature-Excursion Risk & Product Losses

Annual excursion-related wastage stands near USD 35 billion, a figure magnified by the high unit value of biologics. IoT sensors and blockchain platforms now offer real-time notifications and immutable logs; Wiliot’s pixel-sized tags even harvest ambient radio-frequency energy for power-free tracking. Extreme weather events linked to climate change are increasing disruption probability, compelling stakeholders to invest in redundant refrigeration and alternate routing. Yet smaller regional carriers often lack the resources to deploy such technologies comprehensively, sustaining an industry-wide risk overhang.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates While Monitoring Accelerates

Transportation services retained 46.3% of the healthcare cold chain logistics market share in 2024, reflecting the indispensable need to move sensitive cargo across complex multimodal corridors. Air freight, road, sea, and increasingly rail require purpose-built units, validated processes, and cross-hand-off integrity, underpinning sustained demand. Monitoring and data-logging solutions are registering a 12.4% CAGR through 2030 as regulators intensify documentation requirements and shippers seek excursion prevention. Continuous visibility platforms from Cognizant and others furnish granular data, supporting proactive risk management. Storage retains a foundational role, while packaging is evolving toward fibre-based, sensor-enabled configurations that extend protection windows to 96 hours.

E-commerce-driven direct-to-patient models push logistics providers to fuse transportation, packaging, and monitoring into single, outcome-based contracts. DHL’s specialty pharma offering now bundles home delivery, passive packaging, and data analytics to support decentralized trials. As therapies advance, boundaries between traditional service categories blur, positioning integrated operators for outsized gains within the healthcare cold chain logistics market.

By Product Type: Vaccines Hold Sway but Cell Therapies Surge

Vaccines commanded 38.2% of the healthcare cold chain logistics market size in 2024, buoyed by ongoing immunization programs and replenishment of pandemic reserves. Cell and gene therapies, though starting from a smaller base, are scaling at an 18.9% CAGR as approvals broaden and manufacturing capacity ramps. Biopharmaceuticals—especially monoclonal antibodies- continue to enlarge their share, reinforcing the need for 2-8 °C storage across supply chains. Clinical-trial materials rise in tandem with R&D spending, while medical devices that require temperature stability for calibration broaden the service matrix.

McKesson’s InspiroGene initiative illustrates how distributors are building specialized networks to handle personalized therapies, shortening vein-to-vein timelines. The diversity of cargo demands pushes operators to maintain multi-range, multi-format capabilities, fueling mergers that combine cryogenic expertise with standard cold chain assets.

By Temperature Range: Refrigerated Leads, Cryogenic Expands Rapidly

Refrigerated storage (2-8 °C) represented 42.3% share of the healthcare cold chain logistics market size in 2024, supported by broad vaccine and biologic volumes. Cryogenic solutions below −150 °C, critical for cell and gene therapies, are expanding at 21.3% CAGR, prompting sizable capital outlays in liquid-nitrogen shippers and dedicated freezers. Controlled ambient (15-25 °C) and frozen (-20 °C) categories fill niche requirements for select diagnostics and legacy pharmaceuticals. Deep-frozen (-80 °C) niches support research specimens and certain advanced therapies.

Infrastructure specialization is emerging as providers create separate nodes for varied ranges to optimize asset utilization. Cryoport’s HV3 container exemplifies innovation tailored for extended cryogenic holds, improving reliability for international lanes. Regulatory recognition of 2-15 °C “controlled cold” windows under USP <659> introduces flexibility without compromising safety.

By Transportation Mode: Air Freight Leads Despite Modal Shifts

Air freight captured 41.0% share in 2024, reflecting its time-critical advantage for high-value pharmaceuticals and emergency supplies. The segment continues to grow at 13.7% CAGR through 2030, even as sustainability imperatives encourage modal revaluation. CEVA Logistics reports a rising share of ocean freight for non-urgent biologics, delivering up to 80% CO₂ savings. Road transport dominates regional distribution and last-mile fulfilment, while rail gains traction on continental routes that balance speed and emissions.

FedEx’s expansion of healthcare capabilities in Asia Pacific underscores ongoing investment in temperature-controlled air capacity despite carbon concerns. Electric trucks and hydrogen-powered reefers are emerging solutions for urban deliveries, aligning environmental goals with reliability standards in the healthcare cold chain logistics market.

By End User: Pharma Manufacturers Remain Core While CROs Ascend

Pharmaceutical and biotech manufacturers accounted for 55.7% of 2024 revenues as they retain direct oversight of compliant distribution. Contract Research and Manufacturing Organizations (CROs) are the quickest-growing cohort at 11.2% CAGR, propelled by outsourced clinical trial logistics and specialized manufacturing. Hospitals and clinics, blood banks and diagnostic labs form steady demand pools for routine replenishment and emergency supply.

Increasing adoption of home-infusion therapies and specialty pharmacies adds new touchpoints that require finely tuned last-mile services. Logistics providers are deploying patient-centric platforms that schedule deliveries, provide real-time temperature status to caregivers, and manage returns. Consequently, the healthcare cold chain logistics market is expanding both vertically—into advanced therapy support—and horizontally—across diverse care settings.

Geography Analysis

North America commanded 39.6% of global revenues in 2024, underpinned by dense pharmaceutical manufacturing clusters, rigorous FDA oversight, and sustained 3PL investment. DHL’s USD 1.1 billion allocation over five years and Americold’s Kansas City expansion illustrate capital depth aimed at fortifying capacity. Rising energy tariffs and labour shortages in certified operations are near-term challenges, pushing operators to automate processes and adopt renewable power.

Asia Pacific is projected to record a 9.3% CAGR through 2030, the fastest among regions, driven by government-funded production hubs and rapidly expanding healthcare access. China’s deployment of autonomous forklifts in sub-zero warehouses signals technology-led efficiency gains. Singapore’s DHL Pharma Hub strengthens regional connectivity and underscores the healthcare cold chain logistics market’s escalating strategic relevance in Southeast Asia.

Europe remains a cornerstone, leveraging stringent GDP frameworks that shape global compliance norms. UPS’s acquisitions of Frigo-Trans and BPL extend integrated, GDP-accredited transport and warehousing across key European corridors. Sustainability policies champion natural refrigerants and reusable packaging, nudging the market toward circular models. In parallel, Middle East and Africa corridors are gaining traction as public-private partnerships, such as the Africa Finance Corporation’s USD 40 million medical centre investment, drive network build-outs.

Mordor Intelligence provides coverage of the healthcare cold chain logistics market across other key regional markets, including Asia and Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Global integrators, specialized cryogenic providers and regional entrants contest a moderately fragmented field. DHL’s EUR 2 billion plan and the acquisition of CRYOPDP extend its reach across clinical trials and advanced therapy logistics, reinforcing scale and capability. UPS mirrors this trajectory by absorbing Andlauer Healthcare, Frigo-Trans, and BPL, building end-to-end cold chain coverage in key markets. FedEx is enhancing healthcare service layers in Asia Pacific, while Lineage’s USD 5 billion IPO funds capacity growth and technology upgrades.

Technology is the chief battleground. Players integrate IoT sensors, AI analytics, and blockchain to verify compliance, reduce spoilage, and differentiate on reliability. Cryoport leads in cryogenic hardware innovation, whereas Wiliot’s energy-harvesting tags exemplify emerging data-centric solutions. Partnerships between logistics firms and packaging innovators, such as DS Smith’s TailorTemp fibre systems, broaden sustainability credentials. Regional specialists, though nimble, must either niche down or align with larger networks to remain competitive in the fast-scaling healthcare cold chain logistics market.

Healthcare Cold Chain Logistics Industry Leaders

DHL Group (DHL Supply Chain & Global Forwarding)

UPS Healthcare

FedEx Logistics

Kuehne + Nagel International AG

DB Schenker

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: UPS completed acquisition of Andlauer Healthcare Group for CAD 2.2 billion (USD 1.6 billion), increasing North American capacity.

- April 2025: HL committed EUR 2 billion (USD 2.34 billion) by 2030 for new GDP-certified Pharma Hubs and expanded cold chain infrastructure.

- March 2025: DHL acquired CRYOPDP, adding 600,000+ annual temperature-controlled shipments across 15 countries.

- January 2025: Cryoport launched HV3 cryogenic shipping system for advanced therapies.

Global Healthcare Cold Chain Logistics Market Report Scope

| Storage |

| Transportation |

| Packaging |

| Monitoring & Data Logging |

| Vaccines |

| Biopharmaceuticals |

| Cell & Gene Therapies |

| Clinical Trial Materials |

| Medical Devices & Diagnostics |

| Controlled Ambient (15–25 °C) |

| Refrigerated (2–8 °C) |

| Frozen (-20 °C) |

| Deep-Frozen (-80 °C) |

| Cryogenic (<-150 °C) |

| Air Freight |

| Sea Freight |

| Road Transport |

| Rail Transport |

| Pharmaceutical & Biotech Manufacturers |

| Contract Research & Manufacturing Orgs. |

| Hospitals & Clinics |

| Blood Banks & Transfusion Centers |

| Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Storage | |

| Transportation | ||

| Packaging | ||

| Monitoring & Data Logging | ||

| By Product Type | Vaccines | |

| Biopharmaceuticals | ||

| Cell & Gene Therapies | ||

| Clinical Trial Materials | ||

| Medical Devices & Diagnostics | ||

| By Temperature Range | Controlled Ambient (15–25 °C) | |

| Refrigerated (2–8 °C) | ||

| Frozen (-20 °C) | ||

| Deep-Frozen (-80 °C) | ||

| Cryogenic (<-150 °C) | ||

| By Mode of Transportation | Air Freight | |

| Sea Freight | ||

| Road Transport | ||

| Rail Transport | ||

| By End User | Pharmaceutical & Biotech Manufacturers | |

| Contract Research & Manufacturing Orgs. | ||

| Hospitals & Clinics | ||

| Blood Banks & Transfusion Centers | ||

| Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the healthcare cold chain logistics market by 2030?

The market is expected to reach USD 95.1 billion by 2030, expanding at a 9.5% CAGR.

Which service segment is growing the fastest?

Monitoring and data-logging services are advancing at a 12.4% CAGR through 2030, outpacing transportation and storage demand.

Why are cell and gene therapies influencing cold chain design?

These advanced therapies require cryogenic conditions below −150 °C, strict chain-of-custody verification and rapid administration, driving specialised equipment and premium services.

Which region offers the highest growth potential?

Asia Pacific exhibits the fastest regional CAGR at 9.3% through 2030 thanks to large-scale manufacturing investments and expanding healthcare access.

How significant are temperature excursions in terms of financial impact?

Excursions cost the pharmaceutical sector an estimated USD 35 billion each year, underscoring the importance of real-time monitoring and predictive analytics.

What sustainability actions are logistics providers undertaking?

Firms are adopting electric vehicles, natural refrigerants, fibre-based packaging and renewable-powered warehouses to lower carbon footprints while maintaining compliance.

Page last updated on: