Biomedical Refrigerator And Freezer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomedical Refrigerator And Freezer Market Analysis by Mordor Intelligence

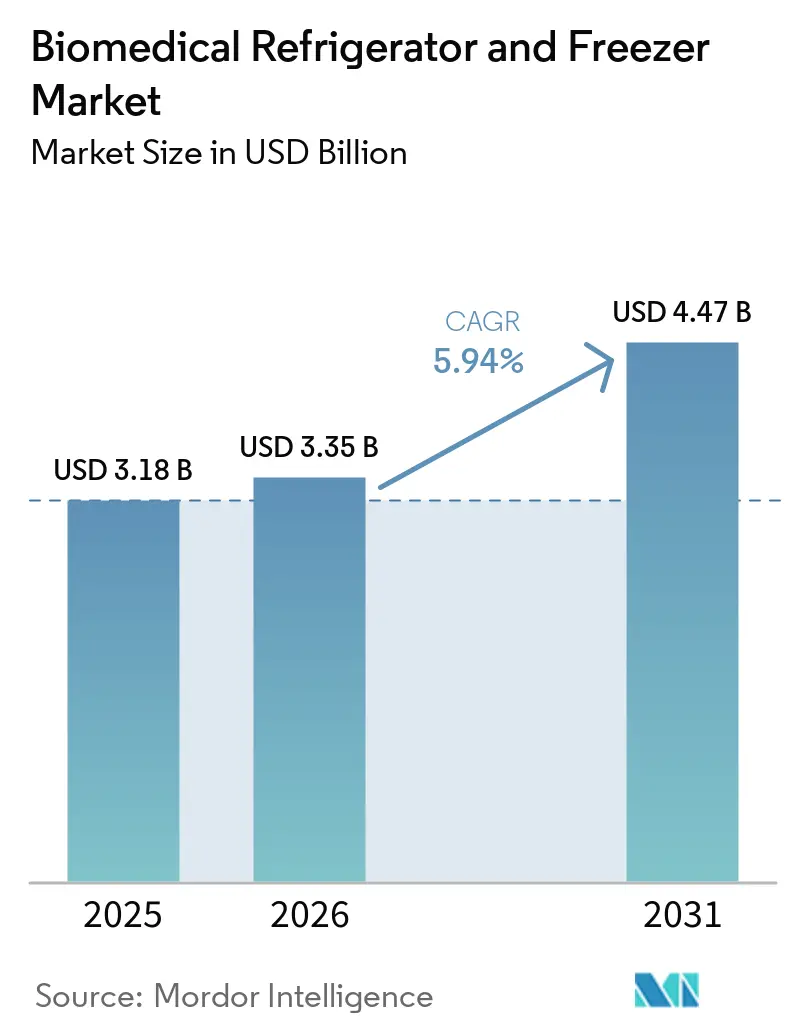

The Biomedical Refrigerator And Freezer Market size was valued at USD 3.18 billion in 2025 and is estimated to grow from USD 3.35 billion in 2026 to reach USD 4.47 billion by 2031, at a CAGR of 5.94% during the forecast period (2026-2031).

This growth reflects rising investments in cell and gene therapies that rely on ultra-precise temperature control, stricter global vaccine‐storage mandates, and an accelerating shift toward decentralized clinical trials that require portable, IoT-enabled cold-chain assets. Compressor technology still underpins most installed capacity, yet sustainability regulations are propelling rapid adoption of other refrigerant-free approaches. Supply-chain resilience is a recurring theme: helium scarcity constrains cryogenic capacity, while semiconductor shortages lengthen lead times for smart freezers. As a result, buyers now evaluate vendors not only on cooling performance but also on component traceability, remote monitoring, and predictive-maintenance features that limit downtime.

Key Report Takeaways

- By product type, laboratory refrigerators captured 21.63% of the Biomedical refrigerator & freezer market share in 2025, while cryogenic freezers are projected to expand at a 8.28% CAGR through 2031.

- By technology, compressor-based systems retained a 84.97% share, and the stirling engine is forecasted to expand at 8.08% CAGR over 2026-2031.

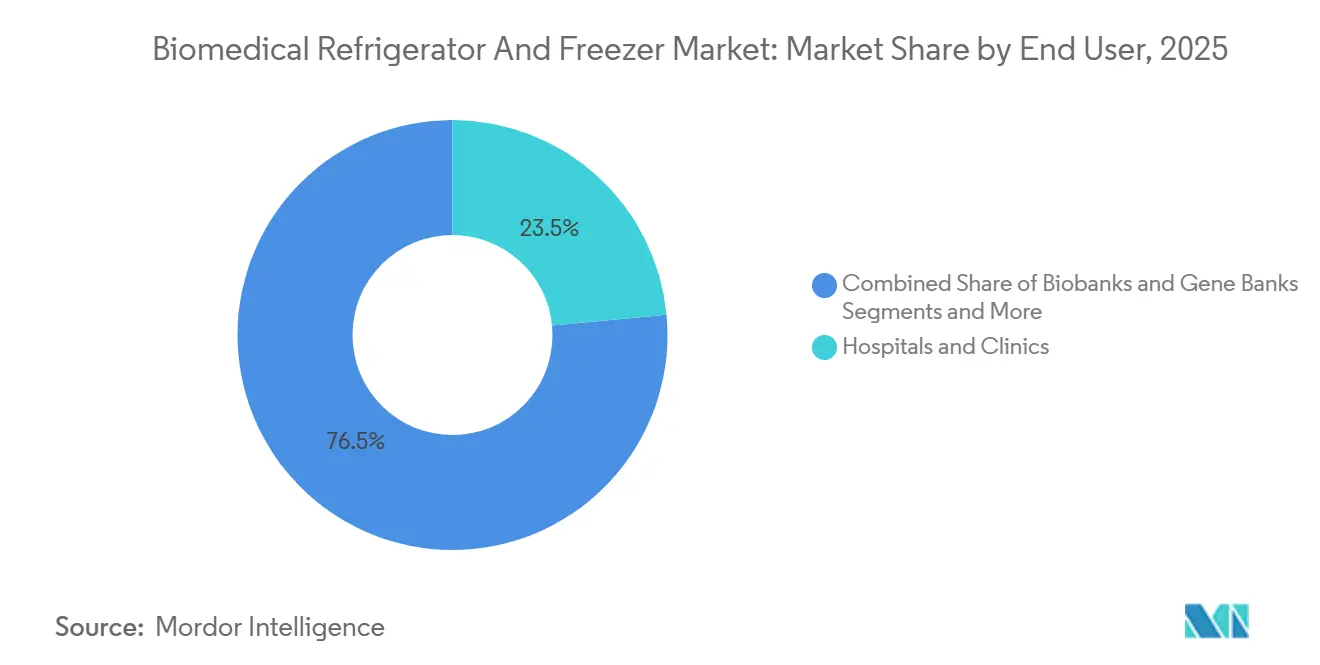

- By end user, hospitals & clinics led with 23.49% revenue share in 2025, whereas biobanks and gene banks are set to grow at a 8.81% CAGR to 2031.

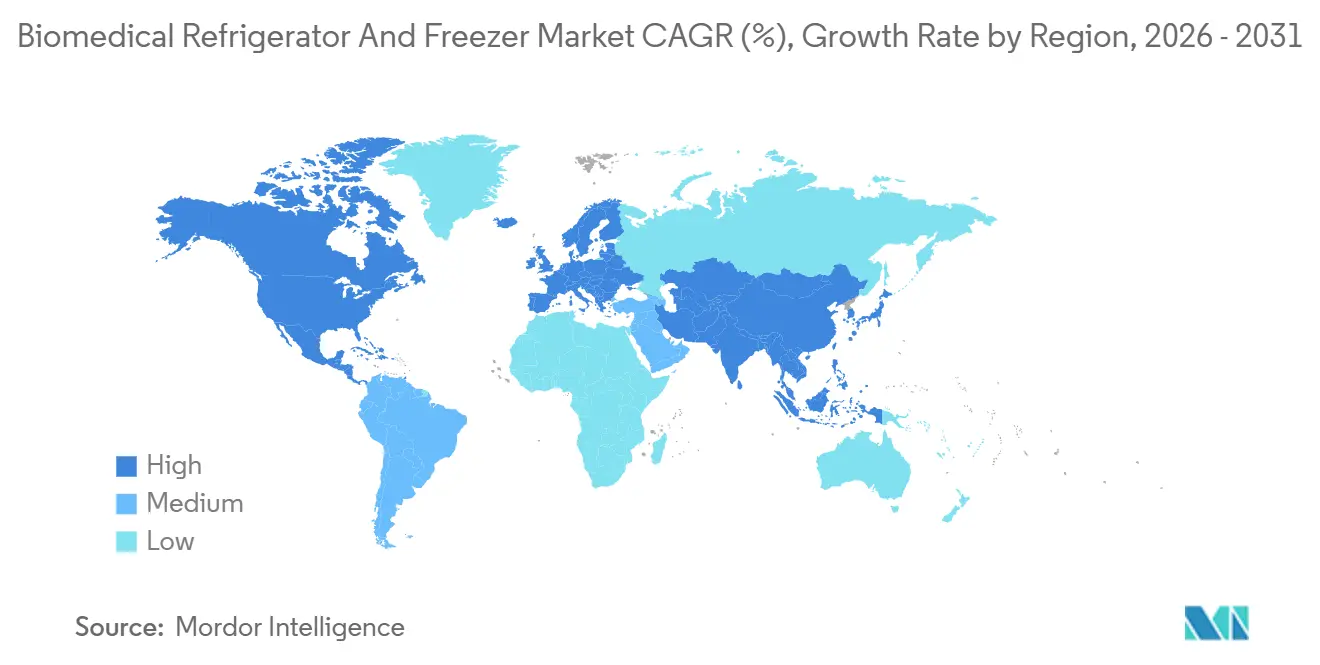

- By geography, North America held a 38.73% share of the biomedical refrigerator and freezer market in 2025, and Asia Pacific remains the fastest-growing region, with a 8.34% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomedical Refrigerator And Freezer Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing burden of chronic diseases and expanded immunization programs | 1.2% | Global, with concentration in APAC and Sub-Saharan Africa | Medium term (2-4 years) |

| Rising adoption of cell and gene therapies requiring ultra-low storage | 1.5% | North America, Europe, Japan | Long term (≥4 years) |

| Stringent blood-safety regulations necessitating advanced storage solutions | 0.9% | Global, led by EU and China | Short term (≤2 years) |

| Expansion of decentralized clinical trials boosting near-patient cold storage demand | 0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Expansion of blood banks and biobanks in emerging markets | 1.0% | APAC core, spill-over to MEA and South America | Long term (≥4 years) |

| Rising demand for pharmaceutical cold chain logistics | 0.6% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Diseases and Expanded Immunization Programs

More than 537 million adults live with diabetes, and many require insulin that must remain between 2 °C and 8 °C.[1]World Health Organization, “Diabetes,” who.int This single-therapy storage requirement alone keeps a continuous stream of orders flowing into the biomedical refrigerator & freezer market. Government-sponsored non-communicable disease programs are funding the installation of new pharmaceutical-grade cold rooms, particularly in India and Southeast Asia, while European hospitals are upgrading to multi-zone cabinets that can segregate biologics, vaccines, and blood products without requiring additional floor space. Oncology wards are another growth node; a single batch of temperature-excursion-sensitive monoclonal antibodies can exceed USD 70,000 in replacement cost, which heightens willingness to pay for redundant compressors, battery backups, and 24/7 cloud telemetry.

Rising Adoption of Cell and Gene Therapies Requiring Ultra-Low Storage

In 2024, the FDA approved 16 cell and gene therapies, including Vertex’s exa-cel and bluebird bio’s lovo-cel, both of which require storage at -150 °C. CAR-T pipelines depend on liquid-nitrogen vapor-phase freezers at -196 °C. However, facilities like the Children’s Hospital of Philadelphia’s Cell and Gene Therapy Laboratory are now using magnetically driven Stirling units, which eliminate the need for nitrogen logistics while reducing energy consumption by 70%. The European Medicines Agency’s 2024 guidance mandated validated temperature mapping for every storage zone. This has prompted hospitals to replace traditional chests with monitored uprights linked to electronic batch-release systems. Such regulatory mandates are driving double-digit growth in ultra-low storage solutions within the biomedical refrigerator and freezer market.

Stringent Blood-Safety Regulations Necessitating Advanced Storage Solutions

China’s Blood Safety Plan for 2024-2030 mandates RFID-enabled refrigerators in all provincial centers by 2026.[2]Department of Pharmaceuticals, “Pharmaceutical Industry in India,” Government of India, pharmaceuticals.gov.in The EU's Blood Directive for 2024 tightens the permissible temperature deviation from ±2 °C to ±1 °C, effective 2025. This change necessitates the use of units equipped with dual probes and microprocessor controls. In August 2024, India introduced a regulation mandating a 72-hour backup power clause, a feature that aligns well with solar-hybrid models from domestic suppliers. In the U.S., platelet-storage guidelines now allow a five-day shelf life if continuous bacterial detection is implemented. These synchronized regulations are accelerating replacement cycles in the biomedical refrigerator and freezer market.

Expansion of Decentralized Clinical Trials Boosting Near-Patient Cold Storage Demand

The FDA's decentralized-trial guidance in 2023, set to be widely adopted by 2025, permits home-based dosing, provided sponsors validate shipping and in-home storage.[3]FDA Staff, “Approved Drug Products with Therapeutic Equivalence Evaluations, Meclizine,” U.S. Food and Drug Administration, fda.gov In 2024, Pfizer's Phase III GLP-1 trial utilized 500 MediCool refrigerators equipped with 4G telemetry, delivering them to patient homes. According to industry data, 42% of oncology studies in North America and Europe employed at-home or near-site dosing in 2024. This trend has led to a 60% surge in orders for compact biomedical refrigerators and freezers. Australia’s regulatory body has equated remote temperature monitoring to on-site inspection, leading to a rise in IoT-enabled unit adoption in rural areas. As a result, near-patient storage nodes are emerging as a significant growth area.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital and maintenance costs | –0.7% | Global, acute in Sub-Saharan Africa and Southeast Asia | Short term (≤2 years) |

| Energy consumption and sustainability-compliance pressures | –0.5% | Europe, North America | Medium term (2-4 years) |

| Limited cold-chain infrastructure in emerging markets | –0.4% | Sub-Saharan Africa, Southeast Asia, parts of South America | Long term (≥4 years) |

| Semiconductor supply constraints delaying compressor/controller deliveries | –0.3% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs

Acquiring a cryogenic freezer operating at -150 °C involves a significant investment, with costs ranging from USD 35,000 to USD 50,000. Additionally, annual service contracts add USD 3,000 to USD 5,000, creating financial challenges, particularly in regions with per-capita health expenditures below USD 200. A 2024 survey of 46 low-income nations indicated that 62% of health ministries identified capital constraints as the primary obstacle to adopting solar-direct-drive units. Compressor failures account for nearly half of all service calls, with replacement costs ranging from USD 8,000 to USD 12,000, often exceeding the residual value of units older than seven years. Lease models, such as those introduced in Africa in 2024, have reduced upfront costs by 70%. However, adoption remains limited due to foreign-exchange volatility and insufficient local service support.

Energy Consumption and Sustainability-Compliance Pressures

Freezers operating at -86 °C consume 15-20 kWh daily, equivalent to the electricity usage of two to three average U.S. homes. Laboratories managing 50-100 units face annual energy expenses exceeding USD 100,000. Regulatory measures, such as the EU Energy Efficiency Directive mandating a 30% reduction in non-process energy consumption by 2030, are driving institutions to upgrade outdated equipment. A 2024 report highlighted that cold storage accounted for 18% of a university campus's power consumption, prompting a GBP 2 million retrofit that reduced energy usage by 25%. Similarly, in 2024, a major pharmaceutical company replaced 120 outdated ultra-low freezers with energy-efficient models, achieving a 35% reduction in energy consumption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cryogenic Growth Reshapes Portfolio Mix

Laboratory refrigerators captured the most significant share of the biomedical refrigerator & freezer market in 2025 at 21.63% because virtually every clinical, academic, and industrial healthcare facility must store reagents, vaccines, or patient samples within the 2 °C-8 °C temperature range. These units now ship with microprocessor controllers, door-opening sensors, and fan-assisted airflow, keeping temperature variance below ±1 °C. At the same time, the cryogenic freezers category is expected to grow at a 8.28% CAGR, driven by the rising adoption of advanced, self-sustaining ultra-low temperature storage systems in life sciences and clinical applications. In February 2026, Cryoport, Inc. introduced the MVE Fusion 800 Series, an advanced cryogenic freezer based on MVE Biological Solutions’ Fusion technology. The system eliminated the need for continuous liquid nitrogen supply, improving reliability, safety, and sustainability while offering a compact design suitable for space-constrained facilities.

Plasma freezers and blood bank refrigerators sustain mid-single-digit growth by replacing aging stock in transfusion centers, whereas shock freezers-niche devices that drop from ambient to -40 °C within 10 minutes-are finding new demand in advanced oncology research protocols. Manufacturers increasingly bundle cloud dashboards and service-level agreements that guarantee a 4-hour on-site technician response time, a feature especially valued by high-throughput COVID-19 genomic surveillance labs.

By Refrigeration Technology: Compressor-Based Dominance with Rising Stirling Engine

In 2025, compressor systems are expected to dominate the biomedical refrigerator and freezer market, holding a 84.97% share. Their versatility spans temperatures from 2 °C to -196 °C, supported by well-established service networks. The stirling engine segment, driven by advancements in next-generation cryogenic cooling technologies transitioning from pilot to commercial scale, is projected to grow at an annual rate of 8.08% through 2031, enabling laboratories to reduce electricity consumption by 20–30%. Stirling engines are gaining traction in ultra-low temperature storage applications, delivering up to 30% energy savings while eliminating the use of hydrocarbon refrigerants, as demonstrated by new product launches in 2025.

Absorption and adsorption cycles are primarily utilized in solar-powered vaccine programs, addressing reliability challenges in regions with unstable power grids. Initiatives have delivered thousands of solar-direct-drive units to countries in Africa by 2024. However, absorption models have captured less than 5% of the market due to efficiency limitations. In developed markets, sustainability targets are expected to drive the adoption of stirling solutions, although compressor cascades are anticipated to remain dominant in deep-cold applications through 2031.

By End User: Biobanks Outpace Hospitals on Precision-Medicine Tailwinds

In 2025, hospitals and clinics accounted for 23.49% of the biomedical refrigerator and freezer market demand, driven by their extensive installed bases for routine 2 °C-8 °C storage. However, growth is shifting towards biobanks and gene banks, which are forecast to expand at a compound annual growth rate of 8.81% through 2031, supported by the increasing scale of genomic programs in regions such as the European Union and Japan.

Pharmaceutical and biotechnology companies remain key consumers of cryogenic freezers, which are critical for drug-substance storage and stability testing. Leading firms have expanded ultra-low capacity at key facilities to support growing pipelines in specific therapeutic areas. Blood banks, while a mature segment, are experiencing a regulation-driven replacement cycle. As deviation tolerances become stricter in regions like China and the European Union, there is a growing demand for upgraded units equipped with dual sensors and power-failure alarms.

Geography Analysis

In 2025, North America accounted for 38.73% of the revenue in the biomedical refrigerator and freezer market. This growth was primarily driven by the enforcement of FDA regulations favoring IoT-enabled equipment with continuous logging. The United States fulfilled approximately 90% of the region's demand. In 2024, Canada enhanced its vaccine cold chains through provincial programs to support RSV campaigns. The decentralization of clinical trials in the United States has reshaped ordering patterns, leading to a significant increase in demand for compact, validated units under 100 liters to support at-home dosing requirements.

Asia-Pacific is projected to be the fastest-growing region, with a compound annual growth rate of 8.34% through 2031. India's National Digital Health Mission aims to connect 150,000 primary health centers by 2026, creating a substantial market opportunity for WHO-approved vaccine refrigerators. Additionally, countries such as Indonesia, Vietnam, and the Philippines are accelerating their immunization programs by incorporating ice-lined and solar-direct-drive units that meet WHO standards.

Europe is experiencing steady but slower growth due to market saturation and the implementation of advanced sustainability mandates. The EU's updated Blood Directive has tightened temperature tolerances, prompting the replacement of units across public blood services. Germany, the United Kingdom, France, Italy, and Spain collectively account for 65% of the region's demand, while Eastern Europe is expanding its biobank capacities with support from Horizon Europe grants. In the Middle East and Africa, demand is emerging rapidly. In South America, Brazil and Argentina have focused on expanding public blood networks, increasing storage capacities by 40% and adding 80 units, respectively, in 2024.

Competitive Landscape

The Biomedical refrigerator & freezer market is moderately fragmented. Thermo Fisher’s USD 2 billion US expansion and USD 4.1 billion filtration acquisition exemplify vertical integration moves that secure component supply and cross-sell synergies. PHC Holdings positions ENERGY STAR ULT models for sustainability-conscious buyers, while Envirotainer’s partnership with va-Q-tec extends cold-chain packaging options that dovetail with freezer fleets.

Disruptors focus on helium-free cooling or pay-per-use contracts. GCI Holdings’ purchase of Stirling Ultracold brings high-efficiency engines into its lineup, and multiple startups are designing blockchain-enabled inventory platforms that can be integrated with any freezer brand. Sustainability metrics, cybersecurity assurance, and 24/7 remote diagnostics are becoming as decisive as temperature uniformity specifications, reshaping buying criteria across the Biomedical refrigerator & freezer market.

Supply-chain challenges sharpen competitive edges. Firms with diversified semiconductor sources ship smart cabinets in six months versus rivals’ 12. Vendors that can retrofit older compressor models with magnetocaloric modules or swap helium coils for alternative cold heads will win replacement cycles. As green-procurement policies proliferate, providers offering cradle-to-grave refrigerant recovery gain preferential access to tenders, reinforcing differentiation in an otherwise hardware-intensive landscape.

Biomedical Refrigerator And Freezer Industry Leaders

Thermo Fisher Scientific Inc.

Haier Biomedical

PHC Holdings Corporation

Eppendorf AG

Helmer Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cold Chain Technologies partnered with Gobi Technologies to broaden temperature-controlled container choices for cell and gene therapies.

- February 2026: Hamilton Storage made all automated storage systems available with natural refrigerants.

- February 2026: Cryoport’s MVE Biological Solutions launched the Fusion 800 self-sustaining cryogenic freezer, eliminating continuous LN₂ supply.

- September 2025: Krish Biomedicals began operations at the Noida Medical Device Park, investing INR 6 crore (USD 0.72 million) in an –86 °C freezer line.

- May 2025: Liebherr USA added a combined refrigerator-freezer engineered for scientific environments.

- April 2025: Thermo Fisher Scientific committed USD 2 billion to United States manufacturing and R&D over four years.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the biomedical refrigerator and freezer market as all factory-built cold-storage units specifically certified to preserve blood, plasma, vaccines, cell and gene therapy payloads, or other temperature-sensitive biomedical specimens between +8 C and -86 C. Equipment installed in hospitals, blood banks, biobanks, pharmaceutical and research laboratories is counted at first sale value; refurbishments, household appliances, and generic food cold-chain systems are excluded from scope.

Scope Exclusion: Walk-in cold rooms and liquid-nitrogen cryogenic vessels fall outside this study.

Segmentation Overview

- By Product Type

- Plasma Freezers

- Blood Bank Refrigerators

- Laboratory Refrigerators

- Laboratory Freezers

- Cryogenic Freezers

- Shock Freezers

- Pharmaceutical Refrigerators

- Other Specialized Biomedical Cold Storage

- By Refrigeration Technology

- Compressor-based

- Absorption/Adsorption

- Magnetic Refrigeration

- Stirling Engine

- By End User

- Hospitals & Clinics

- Biobanks and Gene Banks

- Blood Banks

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Diagnostic Laboratories

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with hospital biomedical engineers, blood-bank operations heads, pharma cold-chain managers, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. These conversations validated utilization rates, service life, typical average selling prices, and technology preference shifts, filling gaps left by secondary data and fine-tuning our assumptions before modeling.

Desk Research

Our analysts screened freely accessible tier-1 datasets such as WHO Essential Medicines lists, American Association of Blood Banks annual statistics, Eurostat trade codes for HS 8418.50 equipment, and U.S. FDA 510(k) clearances for medical refrigerators. Broader demand signals were cross-checked through hospital-bed expansion data published by OECD, vaccine procurement releases on UNICEF Supply Portal, and peer-reviewed papers tracking biobank capacity additions. Paid platforms, D&B Hoovers for company financials and Dow Jones Factiva for deal flow, supplied revenue splits and shipment announcements. The sources cited above are illustrative; many additional public and subscription references informed the study.

Market-Sizing & Forecasting

A blended top-down model starts with global production and trade data for HS 8418.50 and 8418.69 codes, reconstructed into regional install bases, which are then sanity-checked through sampled supplier roll-ups (units × ASP). Key inputs include hospital bed growth, annual blood-transfusion volumes, funded biobank freezer racks, vaccine dose rollouts, and average price erosion for ultra-low-temperature units. Multivariate regression links these drivers to historical revenue, while scenario analysis accounts for energy-efficiency mandates and green refrigerant adoption. Where bottom-up samples under-represent smaller geographies, proportional scaling based on regional healthcare expenditure patches the gap.

Data Validation & Update Cycle

Outputs undergo variance checks against independent import statistics and public company guidance, followed by a two-level analyst review. Reports refresh yearly, with interim updates triggered by material events such as pandemic vaccination waves. A final pre-publication pass ensures clients receive the latest calibrated view.

Why Our Biomedical Refrigerator And Freezer Baseline Earns Trust

Published numbers often differ because firms apply unique scopes, price bases, or refresh cadences. Equipment counted for only vaccine storage, currency left unadjusted, or outdated install-base multipliers can all skew totals.

Key gap drivers here include whether ultra-low-temperature freezers are in scope, the cut-off year for COVID-related purchases, and if inflation-adjusted constant dollars are used. Mordor's disciplined variable selection, annual refresh, and dual-stage validation make its baseline dependable for planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.54 billion (2025) | Mordor Intelligence | - |

| USD 4.10 billion (2025) | Regional Consultancy A | Vaccine-only scope; excludes ULT units |

| USD 4.33 billion (2024) | Industry Journal B | Trend extrapolation from 2018; minimal primary checks |

| USD 4.92 billion (2024) | Global Consultancy C | Broader cold-chain equipment pool; nominal currency |

The comparison shows that when scope breadth, currency normalization, and primary validation differ, so do headline values. Mordor's balanced approach, traceable variables, repeatable steps, and timely updates, offers decision-makers a reliable anchor.

Key Questions Answered in the Report

What is driving the current growth of the Biomedical refrigerator & freezer market?

The strongest tailwinds are the surge of cell and gene therapies that need ultra-low temperatures, tighter global vaccine-storage rules, and hospital investments in IoT-enabled units for real-time monitoring-all combining to support a 5.94% CAGR through 2031.

How large is the Biomedical refrigerator & freezer market today, and what is its outlook?

The Biomedical refrigerator & freezer market stands at USD 3.35 billion in 2026 and is projected to reach USD 4.47 billion by 2031 as precision-medicine pipelines and decentralized clinical trials expand cold-chain nodes worldwide.

What factors are driving the dominance of compressor-based refrigeration systems?

Compressor-based refrigeration systems dominate due to their proven reliability, cost-effectiveness, wide availability, and ability to deliver precise and stable temperature control across biomedical storage applications such as vaccines, blood products, and laboratory samples.

Which end-user segment is growing fastest?

Biobanks and Gene Banks record a 8.81% CAGR to 2031, propelled by precision-medicine initiatives and pandemic-preparedness plans that require long-term, ultra-low-temperature storage for tissue, plasma, and genomic samples.

How are supply-chain disruptions affecting equipment availability?

Semiconductor shortages are extending lead times for smart cabinets to 12 months or more, while a global helium crunch limits the roll-out of -150 °C cryogenic freezers, pushing buyers to consider helium-free stirling or other alternatives.

Page last updated on: