Canned Alcoholic Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

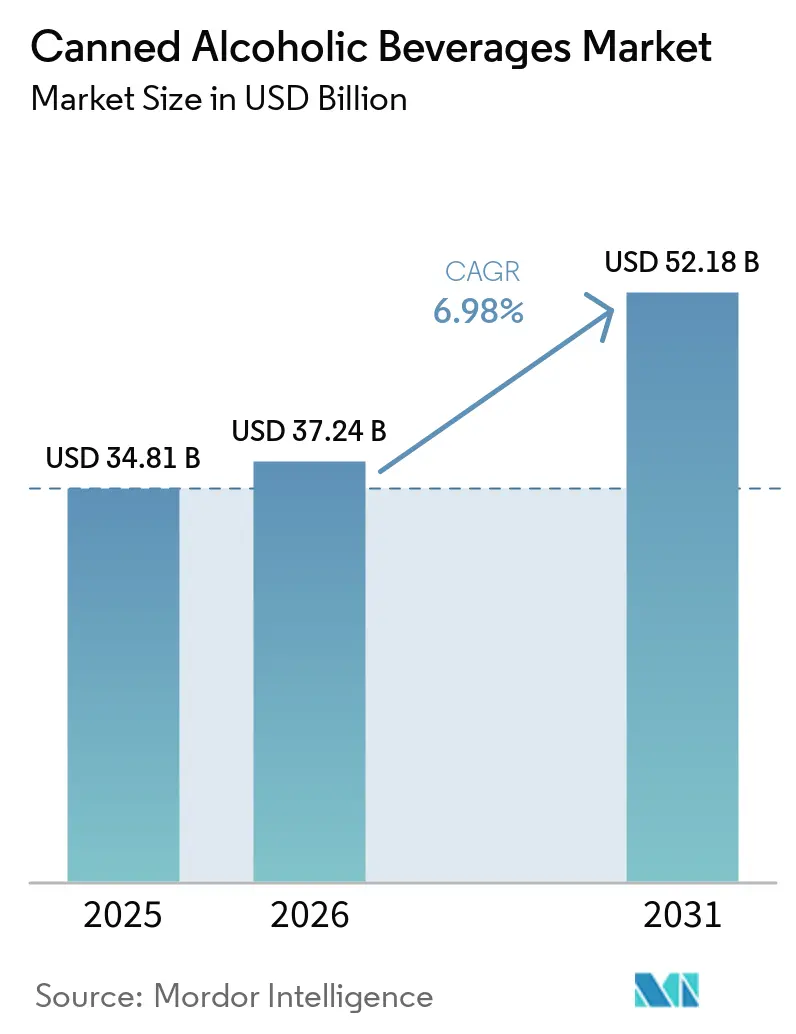

| Market Size (2026) | USD 37.24 Billion |

| Market Size (2031) | USD 52.18 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

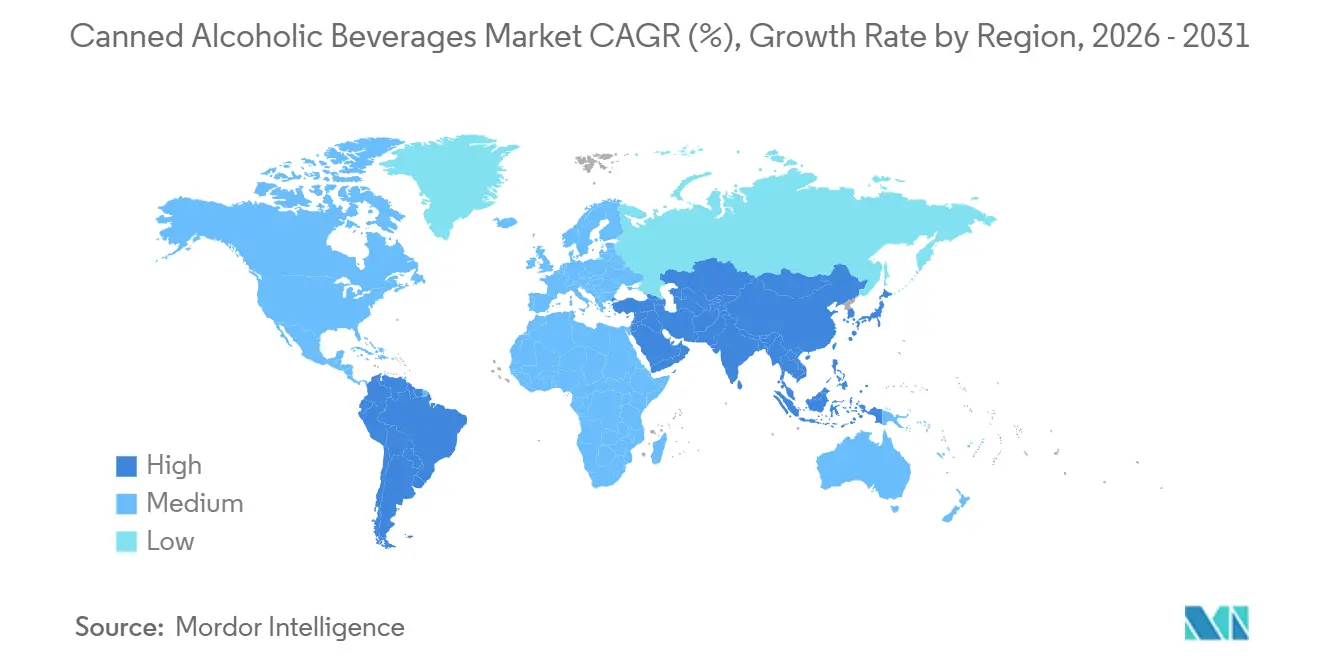

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Alcoholic Beverages Market Analysis by Mordor Intelligence

The canned alcoholic beverages market size was valued at USD 34.81 billion in 2025 and estimated to grow from USD 37.24 billion in 2026 to reach USD 52.18 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031). This growth is largely attributed to the increasing demand for convenient, ready-to-drink alcoholic options that offer premium quality and align with modern consumer lifestyles. Aluminum cans, known for their lightweight design and recyclability, are gaining popularity as they support sustainability efforts and meet environmental standards. Consumers are shifting their preferences toward spirit-based RTD cocktails, away from malt-based seltzers, driven by a desire for better taste and higher-quality beverages. To address environmental concerns, retailers are reorganizing their refrigerated sections to focus on fast-selling products, moving away from a reliance on brand loyalty. The market remains moderately consolidated, with leading companies such as Anheuser-Busch InBev, Mark Anthony Brands International, Constellation Brands Inc., and Boston Beer Company (Truly) dominating the competitive landscape and driving industry advancements.

Key Report Takeaways

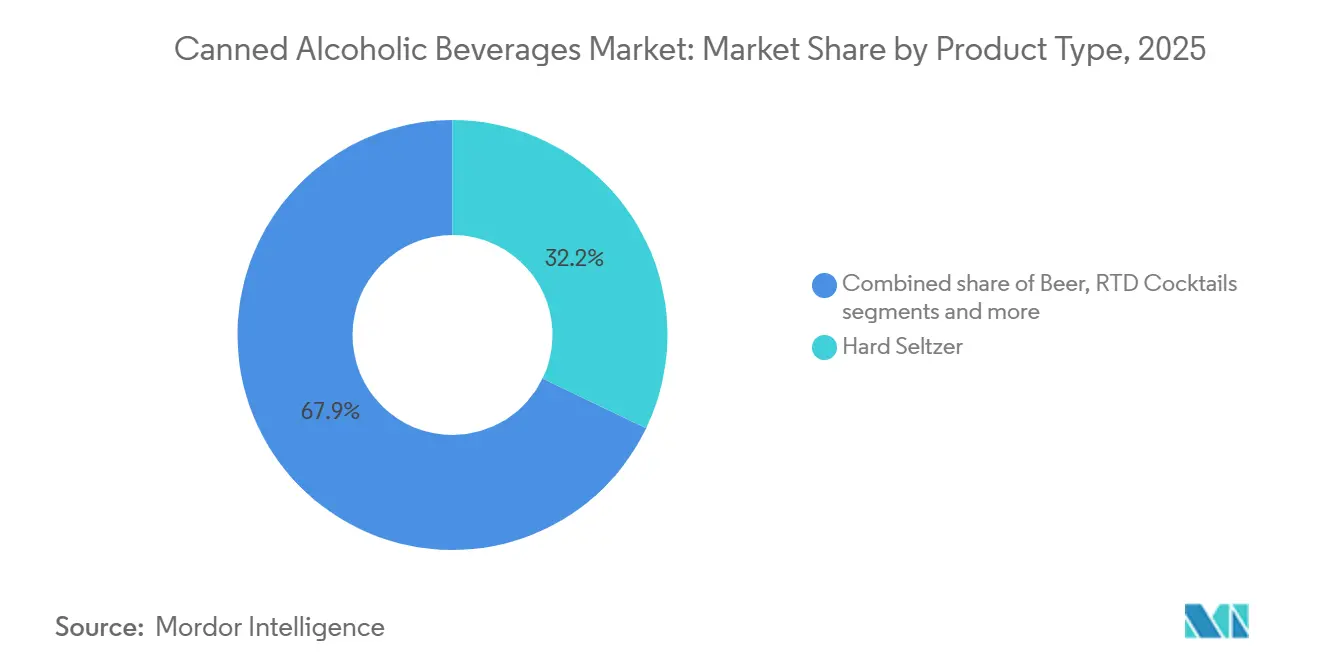

- By product type, hard seltzer led the canned alcoholic beverages market share at 32.15% revenue share in 2025, yet RTD cocktails are set to expand at an 8.58% CAGR to 2031.

- By alcohol content, 5-10% ABV SKUs commanded 57.21% of the canned alcoholic beverages market size in 2025, whereas sub-5% ABV offerings are projected to grow at a 7.37% CAGR to 2031.

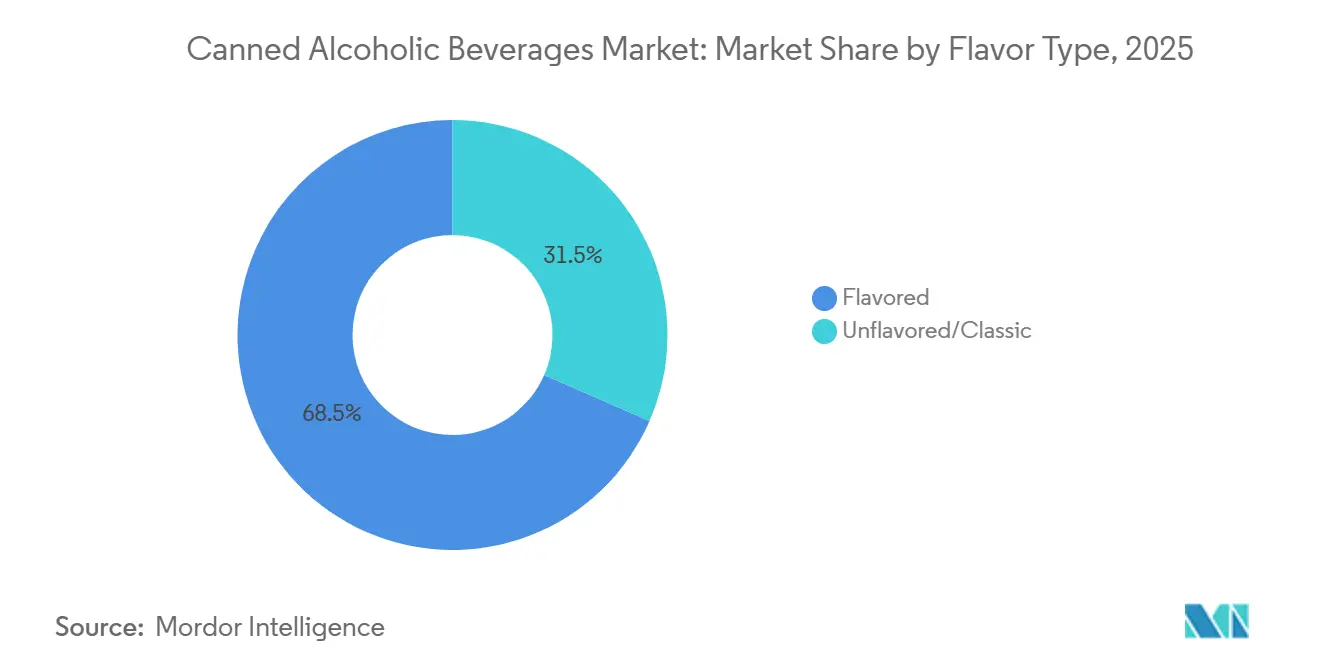

- By flavor, flavored variants held 68.46% revenue share in 2025; classic profiles are forecast to post a 7.04% CAGR through 2031 as flavor fatigue emerges.

- By channel, off-trade accounted for 62.83% sales in 2025, yet on-trade is set to expand at an 8.41% CAGR to 2031 as venues adopt portion-controlled canned cocktails.

- By geography, North America dominated with 54.17% revenue in 2025, while Asia-Pacific is poised for a 7.65% CAGR over 2026-2031, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Canned Alcoholic Beverages Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for convenient and portable alcoholic formats | +0.9% | Global, with early gains in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing popularity of ready-to-drink (RTD) beverages | +1.1% | North America, Europe, Asia-Pacific core markets | Short term (≤ 2 years) |

| Use of recyclable and lightweight aluminum cans aligning with sustainability trends | +0.7% | Europe, North America, Australia; spillover to urban South America and Middle East and Africa | Long term (≥ 4 years) |

| Growing cocktail culture and Western lifestyle influence encouraging consumption of canned cocktails | +0.8% | Asia-Pacific urban centers, South America metropolitan areas, Middle East and Africa expatriate hubs | Medium term (2-4 years) |

| Continuous product innovation, including premium offerings and unique flavor combinations | +1.0% | Global, with premium segments concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Advancements in can technology, including improved lining and sealing | +0.5% | Global manufacturing hubs; early adoption in North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for convenient and portable alcoholic formats

Consumer demand for portable and convenient alcoholic formats is driving growth in the global canned alcoholic beverages market. Single-serve cans are increasingly popular due to their ease of use, quick chilling, lightweight nature, and suitability for various occasions such as travel, outdoor events, and casual at-home consumption without requiring glassware or mixing. This trend aligns with a broader lifestyle shift where consumers prioritize hassle-free drinking experiences with consistent taste and portion control. In response, both emerging brands and established spirits companies are expanding their canned offerings to meet this demand. For example, in December 2025, Cointreau introduced its “Cocktail Twists” canned range, featuring pre-mixed, bar-quality Margarita options in slim cans. These products are designed to provide a premium cocktail experience in a ready-to-drink format, showcasing how established brands are embracing convenience-driven innovation to adapt to changing consumption habits.

Growing cocktail culture and Western lifestyle influence encouraging consumption of canned cocktails

The rising popularity of mixology and the adoption of Western drinking habits are driving the global canned alcoholic beverages market. This trend is particularly evident in emerging urban centers across Asia, where rising exposure to mixology trends on social media, the popularity of rooftop bars, and higher disposable incomes are motivating consumers to explore bar-style drinks. As a result, the demand for ready-to-drink (RTD) canned cocktails, which offer premium taste in a convenient, no-preparation format, is on the rise. In India, shifting consumption patterns among youth further highlight this change. A January 2026 study published on PubMed Central revealed that alcohol use among youth was 10.9% for males and 0.3% for females, indicating a gradually expanding consumer base[1]Source: PubMed Central, "Alcohol Consumption Among Youth of India: A Secondary Data Analysis of NFHS-5 Data", pmc.ncbi.nlm.nih.gov. To address this demand, global companies like Diageo and Heineken are launching flavored, moderate-ABV RTD products aimed at young, urban consumers.

Use of recyclable and lightweight aluminum cans is aligning with sustainability trends

The rising demand for recyclable aluminum cans is emerging as a crucial sustainability driver in the global canned alcoholic beverages market. According to Metal Packaging Europe, Europe recorded a 76.3% recycling rate for aluminum beverage cans, with the industry targeting 100% circularity by 2050, as reported in February 2026[2]Source: Metal Packaging Europe, "Aluminum Beverage Can Recycling Reaches a New Record", metalpackagingeurope.org. This impressive recycling rate is bolstered by the expansion of deposit-return systems and the adoption of closed-loop “can-to-can” processes, which significantly lower energy consumption and greenhouse gas emissions. Recycled aluminum requires up to 95% less energy compared to producing aluminum from virgin materials, making it a sustainable option. As global sustainability regulations become more stringent and companies face mounting pressure to meet carbon-reduction goals, alcoholic beverage manufacturers are increasingly turning to aluminum cans as an environmentally friendly packaging solution.

Advancements in can technology, including improved lining and sealing

Technological advancements in can manufacturing are playing a pivotal role in improving product quality, extending shelf life, and enhancing consumer engagement within the canned alcoholic beverages market. For instance, the introduction of BPA-NI (Bisphenol-A non-intent) liners and advanced seam designs has enabled spirit-based RTDs to maintain shelf lives exceeding 12 months without requiring heat pasteurization. This innovation helps preserve the delicate botanical flavors and overall product integrity, which are critical for premium offerings. Digital printing technologies are empowering brands to create limited-edition packaging and incorporate QR-based loyalty programs, catering to Gen Z's growing demand for interactive and personalized experiences. These features not only boost brand visibility but also foster stronger consumer connections. Industry leaders such as Ball Corporation are at the forefront of these developments.

Restraints Impact Analysis of Canned Alcoholic Beverages Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in excise duties and trade regulations | -0.8% | Global, with acute impact in United Kingdom, Australia, Canada, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Intense competition from traditional alcoholic beverages such as bottled beer, wine, and spirits | -0.9% | Global, particularly in mature markets with established bottle-format loyalty | Medium term (2-4 years) |

| Environmental concerns related to metal production and recycling inefficiencies | -0.4% | North America, emerging Asia-Pacific, and Middle East and Africa regions with weak collection infrastructure | Long term (≥ 4 years) |

| Social stigma and cultural resistance toward alcohol consumption in specific markets | -0.6% | Middle East, South Asia, Southeast Asia, and conservative regions within South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in excise duties and trade regulations

Fluctuations in excise duties and trade regulations continue to pose significant challenges for the global canned alcoholic beverages market, driving up costs and complicating operations for manufacturers. For instance, in early 2026, the implementation of the United States tariff measures led to a 25% retaliatory tariff from Canada[3]Source: Canada CA, "Canada's Response to U.S. Tariffs on Canadian Goods", canada.ca. This development disrupted well-established cross-border distribution networks, resulting in increased compliance burdens and higher logistics expenses for beverage companies. Countries like India and Indonesia impose steep import duties, making it more expensive for international players to penetrate these markets. Additional regulatory requirements, such as mandatory energy labeling in Australia and halal certification in Muslim-majority regions, further escalate localization costs. These combined factors create substantial barriers to market expansion and profitability, forcing companies to navigate a complex regulatory landscape.

Intense competition from traditional alcoholic beverages such as bottled beer, wine, and spirits

Intense competition from traditional beverage formats remains a notable challenge in the global canned alcoholic beverages market. Consumers in various regions continue to favor bottled beer, wine, and spirits, largely due to entrenched consumption habits and the perceived premium quality and heritage associated with these formats. On-premise consumption environments, such as bars, restaurants, and events, often prioritize bottled options over canned alternatives, further solidifying the dominance of traditional packaging. At the same time, the growing presence of private-label canned alcoholic beverages is amplifying price competition in retail channels. This surge in competition forces branded players to adopt pricing strategies that can limit their ability to expand profit margins and differentiate their offerings in an increasingly crowded market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Canned Alcoholic Beverages Market Segment Analysis

By Product Type:

Spirit-Led RTD Cocktails Surge AheadHard seltzers maintain their dominance in the canned alcoholic beverages market, contributing 32.15% of total revenue in 2025. This segment's success is largely due to consumers' growing inclination toward low-calorie, low-sugar alcoholic beverages that cater to health-conscious lifestyles. Younger consumers, in particular, favor hard seltzers as a lighter and more refreshing alternative to traditional beer and sugary cocktails. Additionally, the segment benefits from continuous flavor innovations, user-friendly packaging, and widespread availability across retail channels. These factors collectively ensure that hard seltzers remain the most widely consumed category in key global markets.

On the other hand, spirit-based ready-to-drink (RTD) cocktails are rapidly emerging as one of the fastest-growing segments, with a projected CAGR of 8.58% through 2031. This growth is fueled by increasing consumer demand for premium, bar-quality beverages in convenient, ready-to-consume formats. Consumers are increasingly drawn to authentic, bold flavors, higher alcohol content, and craft-inspired options that enhance the at-home drinking experience. To capitalize on this trend, brands are focusing on premiumization and product differentiation to stand out from beer-based RTDs. As a result, spirit-forward RTDs are gaining significant traction and are positioned as a high-growth segment within the market.

By Alcohol Content:

Sub-5% ABV Gains on ModerationProducts in the 5–10% ABV range continue to dominate the canned alcoholic beverages market, accounting for 57.21% of total revenue in 2025. This segment's success stems from its ability to offer a balanced alcohol content that caters to a broad consumer base seeking both flavor and moderate consumption. Popular categories such as hard seltzers, flavored beers, and spirit-based RTDs thrive in this range due to their appeal for casual and social drinking occasions. Furthermore, the versatility of this ABV range makes it suitable for both retail and on-premise channels, driving its widespread adoption across diverse consumer groups.

On the other hand, the sub-5% ABV segment is emerging as a rapidly growing category, projected to grow at a 7.37% CAGR through 2031. This growth is fueled by a rising preference for wellness-focused and low-alcohol lifestyles, particularly among younger consumers who prioritize moderation. Beverage manufacturers are addressing this demand by introducing innovative low-ABV products that retain flavor while reducing alcohol content. Additionally, the segment is gaining momentum in regions with stricter alcohol regulations and shifting consumption trends. As a result, sub-5% ABV beverages are becoming a significant growth driver within the market, offering opportunities for further expansion and innovation.

By Flavor:

Classic Profiles Stage a ComebackFlavored variants continue to dominate the global canned alcoholic beverages market, contributing 68.46% of total revenue in 2025. This dominance is attributed to the growing consumer demand for unique and innovative taste profiles, including fruity, citrus, exotic, and seasonal flavors. These offerings resonate particularly well with younger consumers who prioritize variety and experimentation in their beverage choices. Additionally, the segment benefits from ongoing flavor innovations, visually appealing packaging, and robust marketing strategies, which collectively enhance its appeal and maintain its leadership position across global markets.

On the other hand, unflavored or heritage mixes are steadily gaining traction, with the segment projected to grow at a CAGR of 7.04% through 2031. This growth is driven by consumers' rising preference for traditional, authentic taste profiles that emphasize simplicity and reduced sweetness. The premiumization trend further supports this category, as consumers increasingly value high-quality, spirit-forward beverages crafted with attention to detail. To capitalize on this demand, brands are introducing clean-label and minimalist formulations, positioning unflavored variants as a sophisticated and premium choice within the market. This shift highlights the evolving consumer interest in both heritage and quality-driven offerings.

By Distribution Channel:

On-Trade Accelerates Post-ShutdownOff-trade channels, such as grocery stores, liquor outlets, convenience stores, and e-commerce platforms, continued to dominate the canned alcoholic beverages market, contributing 62.83% of total revenue in 2025. This dominance stems from the convenience these channels offer for at-home consumption, coupled with their ability to provide a wide variety of products at competitive prices. The rapid expansion of online alcohol sales, supported by doorstep delivery services, has further bolstered this segment's growth. Moreover, promotional discounts and bulk purchasing options available in retail outlets attract cost-conscious consumers, solidifying the off-trade segment's leading position in the market.

On the other hand, on-trade channels are anticipated to experience a robust recovery, with a projected CAGR of 8.41% through 2031. This growth is fueled by the resurgence of social drinking occasions in bars, restaurants, and clubs, where consumers increasingly seek premium and experiential beverage options. The inclusion of canned alcoholic beverages in on-premise menus is gaining traction due to their convenience, consistent quality, and ease of service. Additionally, brands are utilizing on-trade channels to boost visibility and encourage product trials through curated events and experiences. Consequently, the on-trade segment is emerging as a significant growth driver within the market, complementing the dominance of off-trade channels.

Geography Analysis

North America Canned Alcoholic Beverages Market

North America continues to lead the global canned alcoholic beverages market, contributing 54.17% of total revenue in 2025. The region's dominance is attributed to a well-established RTD ecosystem, supportive labeling regulations, and high consumer purchasing power. The widespread availability of canned alcoholic beverages across off-trade channels, such as supermarkets and e-commerce platforms, further enhances market penetration. However, ongoing tariff disputes between the United States and Canada have disrupted cross-border supply chains, prompting manufacturers to adopt near-shoring strategies and invest in localized production to mitigate risks and control costs.

APAC Canned Alcoholic Beverages Market

Asia-Pacific is emerging as the fastest-growing region, with a projected CAGR of 7.65% through 2031. This growth is fueled by rapid urbanization, increasing disposable incomes, and the rising popularity of cocktail culture among younger demographics. Key markets, including China, India, and Southeast Asia, are experiencing heightened demand for convenient and premium RTD formats. Despite this growth, challenges such as high import duties in India and Indonesia, along with halal compliance requirements in certain countries, create regulatory hurdles. In Australia, evolving policies are influencing consumer preferences, but canned alcoholic beverages remain popular for outdoor and social occasions.

EMEA and South America Canned Alcoholic Beverages Market

Europe offers a balanced growth outlook, supported by strong sustainability initiatives but hindered by rising regulatory costs. The region's robust recycling practices encourage the adoption of aluminum cans, aligning with environmental goals. However, increasing excise duties and carbon-related regulations are impacting product pricing. Markets such as Spain and Poland are benefiting from the recovery of tourism and shifting consumption trends among younger consumers. Meanwhile, South America and the Middle East & Africa remain emerging markets, with Brazil showing potential for premium RTDs due to its preference for flavored beverages. In contrast, regulatory restrictions and informal market challenges in Saudi Arabia and parts of the GCC continue to limit market expansion.

Competitive Landscape

The global canned alcoholic beverages market is characterized by moderate consolidation, with major players such as Anheuser-Busch InBev, Diageo plc, and Mark Anthony Brands International dominating the competitive landscape. These companies benefit from extensive product portfolios that span beer, seltzers, and ready-to-drink (RTD) beverages, enabling them to cater to a wide range of consumer preferences. Their robust global distribution networks and ability to secure premium shelf space in refrigerated sections provide them with a significant competitive advantage. Furthermore, their economies of scale enable continuous product innovation and faster market penetration, thereby solidifying their market position.

To maintain their dominance, leading companies are increasingly collaborating with packaging firms like Ball Corporation to access advanced packaging solutions, such as lightweight and digitally printed cans. These innovations not only enhance operational efficiency and speed-to-market but also support limited-edition product launches and improve brand visibility on retail shelves. Large players are leveraging data analytics and category management strategies to strengthen their retail partnerships. By investing in co-marketing initiatives, they are securing long-term shelf space, even as retailers streamline their product assortments to optimize inventory management.

On the other hand, smaller and challenger brands are carving out their niche by emphasizing craft positioning, unique flavor profiles, and functional benefits to appeal to specific consumer segments. However, these brands often face challenges in scaling their distribution networks and sustaining innovation due to limited financial resources. As a result, they tend to avoid direct competition with larger incumbents, instead focusing on premium or specialized market segments. This dynamic allows major players to maintain their dominance while providing space for regional and craft brands to thrive in differentiated areas of the market.

Canned Alcoholic Beverages Industry Leaders

-

Anheuser-Busch InBev

-

Mark Anthony Brands International

-

Diageo plc

-

Constellation Brands Inc.

-

Boston Beer Company (Truly)

- *Disclaimer: Major Players sorted in no particular order

Canned Alcoholic Beverages Market Companies Covered in this Report

- Anheuser-Busch InBev

- Mark Anthony Brands International

- The Coca-Cola Company

- Diageo plc

- Constellation Brands Inc.

- Molson Coors Beverage Company

- Heineken N.V.

- Pernod Ricard S.A.

- Bacardi Limited

- Brown-Forman Corporation

- Boston Beer Company (Truly)

- Suntory Holdings Ltd.

- Campari Group

- Carlsberg Group

- Asahi Group Holdings

- Rémy Cointreau S.A.

- E.&J. Gallo Winery

- Treasury Wine Estates

- JuneShine Spirits Co.

- Flying Embers LLC

Recent Industry Developments in Canned Alcoholic Beverages Market

- August 2025: V Rum launched a new line of ready-to-drink canned cocktails, offering bar-quality flavors with the convenience modern consumers seek. The collection featured various flavor options and highlights premium ingredients and eco-friendly packaging, catering to the rising demand for high-quality, portable alcoholic beverages.

- July 2025: Casamigos has introduced its first ready-to-drink (RTD) margarita variety pack: Casamigos Margaritas. The non-carbonated beverages contain tequila, triple sec liqueur, natural flavors, and real juice. The product line features four flavors: Passionfruit & Prickly Pear, Strawberry & Colima Lime, Guava & Hibiscus, and Classic Lime. Each 200ml can contains 10% alcohol by volume (ABV), 135 calories, and is gluten-free.

- April 2025: South County Distillers (SCD) introduced three craft canned cocktails: Peach Lemonade, Blueberry Lemonade, and Limoncello Spritz. As Rhode Island's exclusive canned cocktail producer, SCD creates beverages using premium ingredients to deliver refreshing, approachable drinks. The diverse flavor range accommodates various consumer preferences.

- January 2025: Molson Coors Beverage Company announced a strategic partnership with Fever-Tree, acquiring exclusive U.S. commercialization rights and an 8.5% stake in Fever-Tree Drinks plc, making it the second-largest shareholder. The partnership leverages Molson Coors' distribution network to expand Fever-Tree's premium mixer portfolio in the U.S. market, where it leads the tonic and ginger beer categories.

Global Canned Alcoholic Beverages Market Report Scope

Canned alcoholic beverages are ready-to-drink (RTD) alcoholic drinks packaged in cans instead of bottles. They’re designed for convenience, portability, and quick consumption without mixing or preparation. The global canned alcoholic beverages market is classified into product type, alcohol content, flavor type, distribution channel, and geography. Based on product type, the market is segmented into beer, hard seltzers, RTD cocktails, wine, and others. Based on the alcohol content, the market is segmented into less than 5% ABV, 5-10% ABV, and more than 10% ABV. Based on the flavor type, the market is segmented into unflavored/classic and flavored. Based on distribution channel, the market is classified into on-trade and off-trade. Based on the geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD) and volume (Liters).

Segmentation Overview

| Beer |

| Hard Seltzer |

| RTD Cocktails |

| Wine |

| Others |

| Less than 5% ABV |

| 5-10% ABV |

| More than 10% ABV |

| Unflavored/Classic |

| Flavored |

| On-Trade | |

| Off-Trade | Specialty Liquor Stores |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Beer | |

| Hard Seltzer | ||

| RTD Cocktails | ||

| Wine | ||

| Others | ||

| By Alcohol Content | Less than 5% ABV | |

| 5-10% ABV | ||

| More than 10% ABV | ||

| By Flavor Type | Unflavored/Classic | |

| Flavored | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty Liquor Stores | |

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the Global canned alcoholic beverages market be by 2031?

It is forecast to reach USD 52.18 billion, reflecting a 6.98% CAGR from 2026-2031.

Which product segment is expanding fastest?

Spirit-based RTD cocktails show the quickest growth, overtaking malt-based seltzers in incremental revenue.

Which region offers the strongest growth prospects?

Asia-Pacific is projected for a 7.65% CAGR as urban cocktail culture spreads across China, India, and Southeast Asia.

What is driving on-trade recovery?

Bars and event venues value canned cocktails for speed of service and portion control, helping on-premise sales rebound at an 8.41% CAGR through 2031.

Page last updated on: