Hypertonic Drinks Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

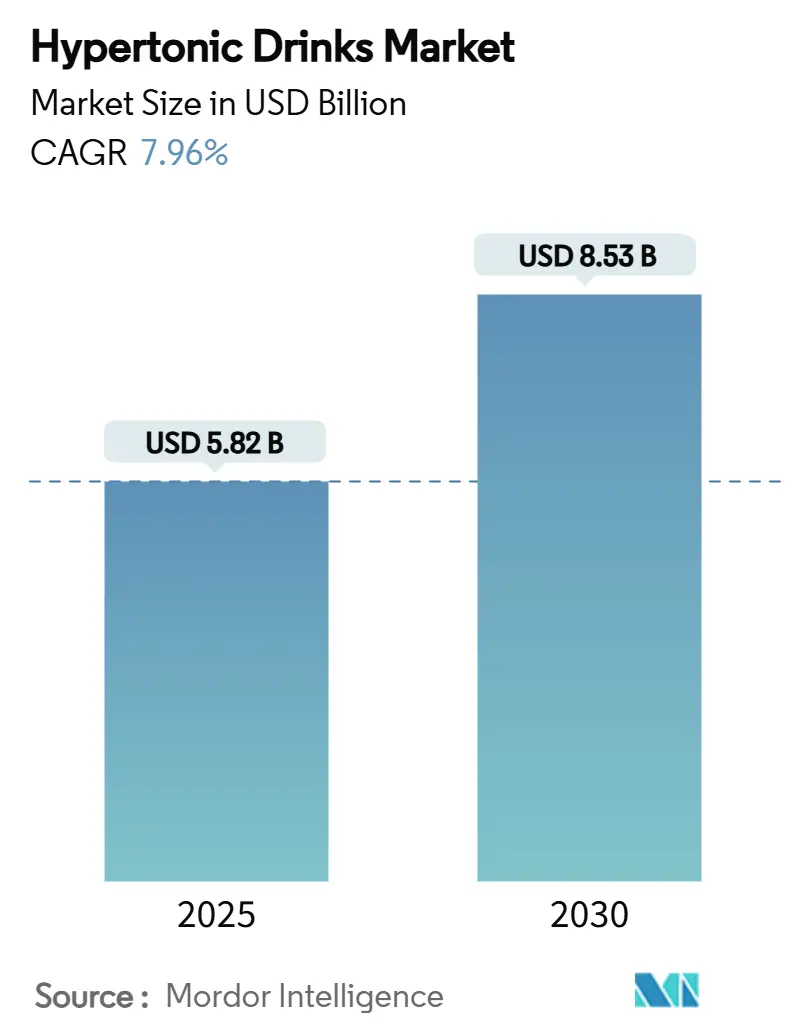

| Market Size (2025) | USD 5.82 Billion |

| Market Size (2030) | USD 8.53 Billion |

| Growth Rate (2025 - 2030) | 7.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hypertonic Drinks Market Analysis by Mordor Intelligence

The hypertonic drinks market size reached USD 5.82 billion in 2025 and is on track to attain USD 8.53 billion by 2030, advancing at a 7.96% CAGR during the forecast period. Current growth rests on accelerated adoption in mainstream wellness, improvements in carbohydrate-loading science, and wider availability of wearable sweat-testing devices that translate laboratory hydration protocols into day-to-day consumption. The market benefits from resilient demand at the intersection of endurance sports, tactical nutrition, and emerging personalized hydration platforms that encourage higher carbohydrate throughput than isotonic alternatives can supply. Rapid innovation in hydrogel and multi-electrolyte delivery systems mitigates gastrointestinal side effects, opening the way for broader consumer segments that once viewed hypertonic beverages as niche athletic aids. Competitive intensity remains moderate, allowing global beverage leaders and agile direct-to-consumer brands alike to capture share through flavor innovation, transparent labeling, and targeted digital outreach.

Key Report Takeaways

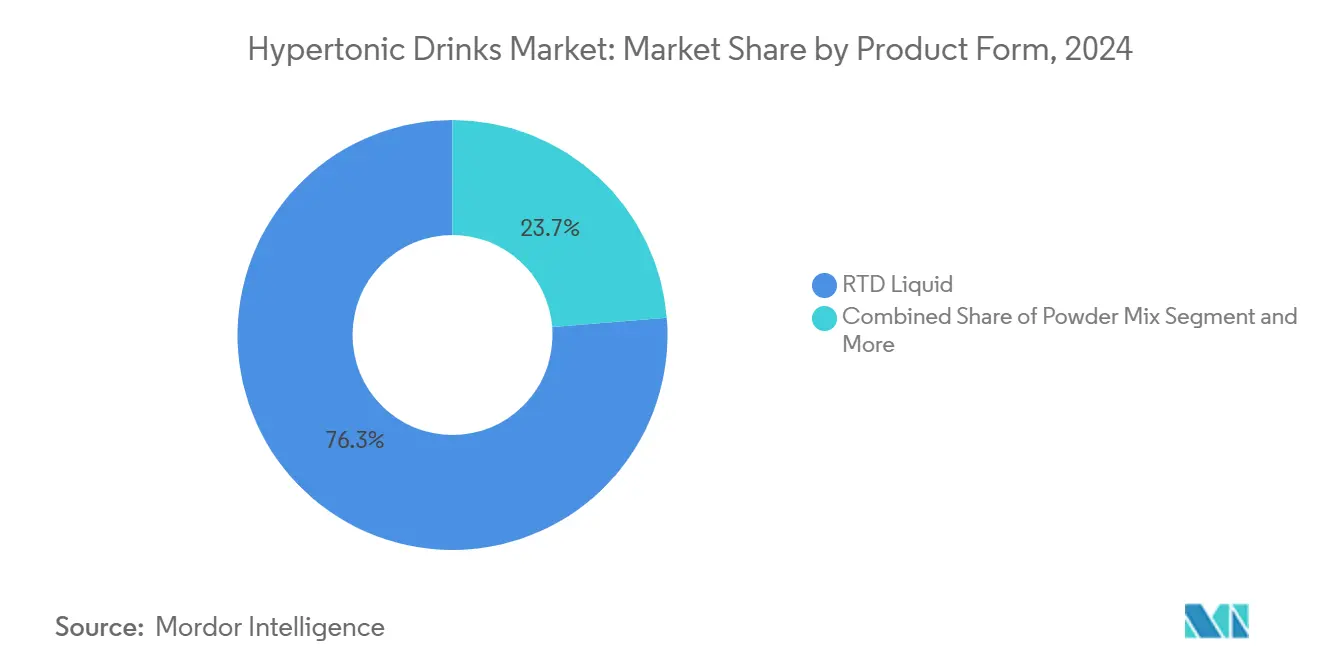

- By product form, ready-to-drink (RTD) liquids led with 76.27% of the hypertonic drinks market share in 2024; effervescent tablets are projected to register the highest 8.69% CAGR to 2030.

- By distribution channel, supermarkets and hypermarkets accounted for 37.14% of the hypertonic drinks market size in 2024, while online retail is accelerating at a 9.21% CAGR through 2030.

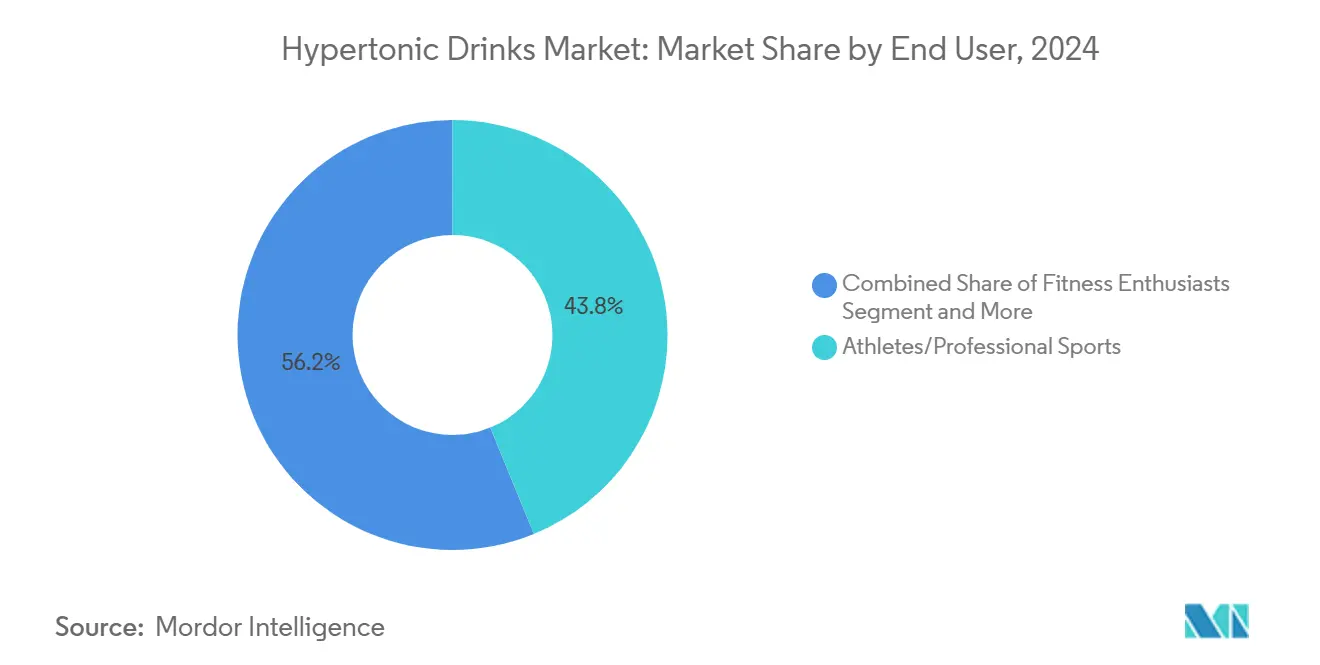

- By end user, athletes and professional sports represented 44.26% of the hypertonic drinks market size in 2024; fitness enthusiasts constitute the fastest-growing consumer group with a 10.87% CAGR to 2030.

- By geography, North America held the largest regional share at 41.74% in 2024; Asia-Pacific is forecast to expand at a 6.25% CAGR toward 2030.

Global Hypertonic Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of intra-workout carbohydrate loading for endurance sports | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Proliferation of multi-electrolyte + carbohydrate formulations | +0.8% | Global | Short term (≤ 2 years) |

| Rapid growth of e-commerce native sports-nutrition brands | +1.5% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Inclusion of hypertonic drinks in mainstream athletic training protocols | +0.9% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Wearable sweat-testing enabling personalized hypertonic prescriptions | +0.6% | North America & Europe initially | Long term (≥ 4 years) |

| Military procurement for hot-climate deployments | +0.4% | North America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Intra-Workout Carbohydrate Loading for Endurance Sports

Endurance athletes are increasingly exceeding the traditional recommendation of 30-60 grams of carbohydrates per hour during workouts. Elite athletes are now targeting an impressive 90-120+ grams hourly for prolonged events[1]Matthew Kadey, “The Best High-Carb Drink Mixes for Endurance Athletes,” Triathlete, triathlete.com. This shift is backed by emerging sports science research, which shows that a higher carbohydrate intake not only stabilizes blood glucose levels but also spares muscle glycogen. This enables athletes to sustain their performance during ultra-endurance activities. The trend gained traction after professional cycling teams and marathon runners reported reduced fatigue and enhanced power output when they consumed hypertonic formulations during competitions. In response, sports dietitians are now emphasizing "gut training" protocols. These protocols help athletes' digestive systems adapt to higher carbohydrate concentrations, fueling a growing demand for specialized hypertonic products meant for prolonged consumption. The edge lies in hypertonic drinks, which provide concentrated energy without the need for large fluid volumes. This innovation effectively tackles the challenges of fuel delivery and hydration management during extended physical exertion.

Proliferation of Multi-Electrolyte + Carbohydrate Formulations

Formulation innovation focuses on blending various electrolyte sources with optimized carbohydrate ratios. This not only boosts absorption efficiency but also reduces osmotic stress on the gastrointestinal system. Today's advanced products draw sodium from diverse sources, such as sea salt, sodium citrate, and sodium alginate. These are combined with potassium, magnesium, and calcium, achieving a closer match to sweat composition than traditional single-electrolyte formulations. A significant breakthrough is the use of hydrogel technology. This method encapsulates high carbohydrate concentrations in alginate-pectin matrices, facilitating rapid gastric emptying without compromising energy density. This innovation effectively tackles the primary drawback of conventional hypertonic drinks, which frequently led to gastric distress due to elevated osmolality. To cater to clean-label preferences without sacrificing efficacy, manufacturers are blending natural ingredients like coconut water and watermelon juice with synthetic compounds, ensuring a balanced electrolyte profile.

Rapid Growth of E-commerce Native Sports-Nutrition Brands

Digital channels empower direct-to-consumer sports nutrition brands to sidestep traditional retail gatekeepers, forging direct ties with consumers focused on performance and specialized formulations. Leveraging targeted social media marketing, partnerships with elite athlete influencers, and subscription-based delivery models, these brands swiftly scale, ensuring their products remain consistently available. Their competitive edge lies in the ability to rapidly adjust product formulations based on customer feedback and the latest in sports science research, a nimbleness that sets them apart from established brands with lengthier development cycles. E-commerce platforms play a pivotal role, using content marketing to educate consumers, especially on the nuanced applications of hypertonic drinks, bridging a knowledge gap. This approach resonates especially well with younger demographics, who value ingredient transparency and are ready to invest in products that support their performance aspirations.

Inclusion of Hypertonic Drinks in Mainstream Athletic Training Protocols

Sports performance coaches and registered dietitians are increasingly incorporating hypertonic drinks into structured training regimens for athletes across various disciplines. This shift marks a move from sporadic use to a more systematic approach known as nutritional periodization. The growing adoption underscores a heightened awareness: the availability of carbohydrates plays a crucial role in determining the quality of training and the body's adaptive responses. This is especially true during high-intensity interval training and extended endurance sessions. In response, professional sports organizations have begun to enforce specific hydration protocols, emphasizing hypertonic formulations during designated training phases. This has led to standardized demand patterns, bolstering market growth. Moreover, this trend isn't limited to the pros; collegiate and amateur sports programs are also on board, with coaches leveraging these nutritional strategies for a competitive edge. To further this understanding, sports science institutes are rolling out educational initiatives, enlightening practitioners on the physiological benefits of hypertonic drinks. This effort aims to diminish the previous reliance on trial-and-error methods, which had hindered broader adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gastro-intestinal distress concerns from high sugar concentration | -1.3% | Global | Short term (≤ 2 years) |

| Sugar-tax regulations on sweetened beverages | -1.2% | Europe, select APAC markets | Medium term (2-4 years) |

| Competition from isotonic/hypotonic alternatives | -0.8% | Global | Medium term (2-4 years) |

| Supply-chain volatility for specialty carbohydrates | -0.7% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gastro-Intestinal Distress Concerns from High Sugar Concentration

Hypertonic drinks, laden with high carbohydrate concentrations, can upset the body's osmotic balance. This disruption often leads to nausea, cramping, and digestive discomfort, especially when these drinks are consumed during intense physical activity. During such exertion, blood flow is redirected away from the gastrointestinal tract. Research highlights that beverages with carbohydrate concentrations surpassing 8% notably heighten the risk of gastric distress. This risk is further pronounced during high-intensity exercise, a time when the body's gastric emptying rates naturally slow down. The core issue with hypertonic solutions lies in their need for dilution before absorption. This requirement can inadvertently pull fluids into the intestinal tract, worsening dehydration instead of alleviating it. Athletes, especially during competitions, report heightened sensitivity to these effects. This sensitivity is compounded by stress hormones, which can further hinder digestive function. As a result, many performance-focused consumers, who value reliability over sheer energy density, remain cautious about adopting such products. In response to these challenges, manufacturers are innovating formulations. Techniques like hydrogel technology and the use of highly branched cyclic dextrin are being employed. These advancements aim to lower osmotic pressure while ensuring consistent carbohydrate delivery rates.

Sugar-tax Regulations on Sweetened Beverages

Government levies on sugary drinks are putting a squeeze on hypertonic beverages, which naturally contain higher carbohydrate levels. The UK's Soft Drinks Industry Levy is setting a precedent for similar initiatives worldwide[2]HM Revenue and Customs. "Strengthening the Soft Drinks Industry Levy consultation." April 28, 2025. www.gov.uk. Specifically, the UK regulation zeroes in on drinks with over 5 grams of sugar per 100ml. This move hits hypertonic drinks hard, as they usually pack in 8-12 grams per 100ml to deliver their desired effects. There's talk of tightening these regulations further, with suggestions to drop the sugar limit to 4 grams per 100ml. Additionally, there's a push to eliminate current exemptions for certain sports nutrition products. Such changes could compel manufacturers to either alter their formulations or hike prices, potentially making these drinks less accessible to consumers. This regulatory movement underscores a broader public health goal: curbing sugar consumption at the population level[3]Kerry. "The State of Sugar and Health Taxes in 2021." February 6, 2023. www.kerry.com. However, this goal clashes with the needs of sports nutrition, where a higher carbohydrate density is crucial for performance. In response, the industry is innovating with new sweetening systems and advocating for exemptions in sports nutrition, emphasizing the functional benefits over mere recreational use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: RTD Liquids Consolidate Leadership as Effervescent Tablets Accelerate

RTD liquids accounted for 76.27% of the hypertonic drinks market in 2024, highlighting consumers’ preference for immediate consumption that sidesteps mixing inaccuracies and safeguards on-the-go convenience. The format’s scale economies enable precision engineering of carbohydrate-to-electrolyte ratios, translating laboratory recipes into mass-market reliability. Shelf stability widens placement opportunities across grocery, convenience, and sporting goods channels, supporting impulse purchases before training sessions or competitions. Cross-merchandising with protein bars and recovery powders further entrenches RTD share by framing the beverage as a complete performance system. Manufacturers invest in eco-lightweight bottles and post-consumer resin to mitigate packaging concerns while point-of-sale displays emphasize science-backed dosing simplicity.

Effervescent tablets, though representing a small base, are forecast to grow at 8.69% CAGR because rapid dissolution technology now delivers full carbohydrate payloads within 30 seconds, eliminating earlier preparation delays. Consumers value pocket-sized tubes that fit easily into race belts or travel kits, resolving luggage and spill worries linked to liquid options. The hypertonic drinks market size for tablets expands as brands integrate probiotics, B-vitamins, and collagen peptides unstable in aqueous RTDs, offering functional layering that differentiates beyond basic energy delivery. Interactive fizzing also signals “activation,” creating a sensory cue tied to efficacy. Price-per-serving advantages and reduced freight emissions resonate with environmentally conscious shoppers, positioning tablets as a sustainable alternate within an increasingly diversified product portfolio.

By Distribution Channel: Online Retail Outpaces Modern Grocery Stronghold

Supermarkets and hypermarkets retained 37.14% of the hypertonic drinks market in 2024 by leveraging broad physical footprints, panoramic shelf sets, and cross-category promotions that introduce hypertonic SKUs alongside isotonic and protein beverages. In-store sampling programs demystify usage occasions, while loyalty-card data guides planogram placement near pre-workout snacks. Retailers negotiate end-cap visibility in exchange for volume commitments, reinforcing entrenched supplier relationships that favor multinational beverage groups with extensive field marketing budgets. Still, physical retail faces rising inventory complexity as niche flavor variants and personalization trends escalate SKU counts.

Online retail, registering a 9.21% CAGR through 2030, absorbs consumers gravitating toward data-rich shopping experiences that clarify carbohydrate ratios, osmolality metrics, and sweat-rate calculators inside product pages. Subscription models guarantee training-cycle continuity and reward brand loyalty with tiered discounts, bridging the gap between performance planning and supply certainty. Algorithm-driven recommendation engines upsell customizable starter kits that match patch-based sweat analytics, increasing average order values. Direct-to-consumer brands reinvest margin savings into athlete sponsorship content that mainstream grocery banners seldom match. As younger athletes normalize mobile commerce, the hypertonic drinks market increasingly relies on omnichannel plays that synchronize brick-and-mortar education with online replenishment ease.

By End User: Fitness Enthusiasts Expand Demand Beyond Elite Athletics

Athletes and professional sports consumed 44.26% of the hypertonic drinks market in 2024, reflecting high-frequency intake patterns rooted in rigorous training volumes and evidence-based nutrition regimes. Teams deploy performance dietitians who prescribe servings by session type, making demand relatively price-inelastic but highly sensitive to consistency and scientific validation. Athlete endorsement remains a primary credibility lever that migrates product perception into mass channels. Purchase surges cluster around competitive calendars, requiring manufacturers to navigate peak production cycles that coincide with major marathons and triathlon seasons.

Fitness enthusiasts, projected to advance at 10.87% CAGR, exemplify the sportification of everyday wellness as recreational runners, cyclists, and functional fitness practitioners pursue marginal gains once reserved for elites. Social media challenge groups turn carbohydrate fueling into a gamified lifestyle motif, while wearables deliver real-time caloric expenditure that rationalizes hypertonic intake on short weekday workouts. Lower total mileage means smaller absolute volumes per user, yet rapid segment expansion offsets intake gaps. The hypertonic drinks market share among enthusiasts strengthens as brands reposition messaging from athletic peak performance toward “energy confidence” for demanding work-life schedules, broadening addressable demographics to busy professionals and active parents.

Geography Analysis

In 2024, North America secured a dominant 41.74% share of the hypertonic drinks market. This stronghold is bolstered by a vibrant sports nutrition research ecosystem, a deep-rooted culture of collegiate athletics, and extensive military procurement programs that have institutionalized the use of hypertonic drinks. The region's growth is further fueled by high discretionary incomes, which facilitate the adoption of premium beverages, and a sophisticated e-commerce infrastructure that enhances direct-to-consumer outreach. The workforce's emphasis on measurable performance metrics has heightened the appeal of hydration science, especially as it's communicated through apps and wearables. Moreover, the U.S. Food and Drug Administration's clear regulatory stance distinguishes specialized sports drinks from regular soft drinks, minimizing compliance uncertainties and spurring innovation in formulations.

Asia-Pacific, projected to grow at a 6.25% CAGR through 2030, is witnessing a surge in sports participation. Urban middle-class consumers are increasingly viewing marathons, triathlons, and cycling events as lifestyle milestones. Local brands are attuning their sweetness profiles and fruit flavorings to regional tastes, all while ensuring the drinks' functional density. In China, India, and Southeast Asia, rising gym memberships are forging distribution partnerships with national fitness chains. These chains are strategically placing hypertonic ready-to-drinks (RTDs) near workout zones, encouraging immediate trials. Government-backed sports festivals and corporate wellness initiatives are further embedding the importance of hydration. Despite logistical challenges in emerging markets, mobile commerce is bridging infrastructure gaps, driving digital subscription models even in tier-two cities.

Europe's steady adoption of hypertonic drinks is anchored in its rich culture of endurance sports, particularly within cycling clubs and long-distance running communities. However, the region grapples with challenges posed by sugar-tax policies that inflate retail prices. In response, brands are navigating these regulatory waters by underscoring the functional benefits of their products in athletic settings and experimenting with lower-sugar variants, often enhanced with hydrogel technology. Meanwhile, the Middle East and Africa, though still in nascent stages, see promise in the market. With extreme heat leading to heightened electrolyte loss, hypertonic solutions are gaining traction for both recreational sports and occupational hydration. Yet, establishing a robust market demands significant investments in consumer education and a reliable cold-chain distribution system to ensure product stability. South America, with its football-centric culture, is gradually pivoting towards marathon and Ironman events. This shift presents a lucrative opportunity, but the region's macro-economic volatility poses challenges to discretionary spending.

Competitive Landscape

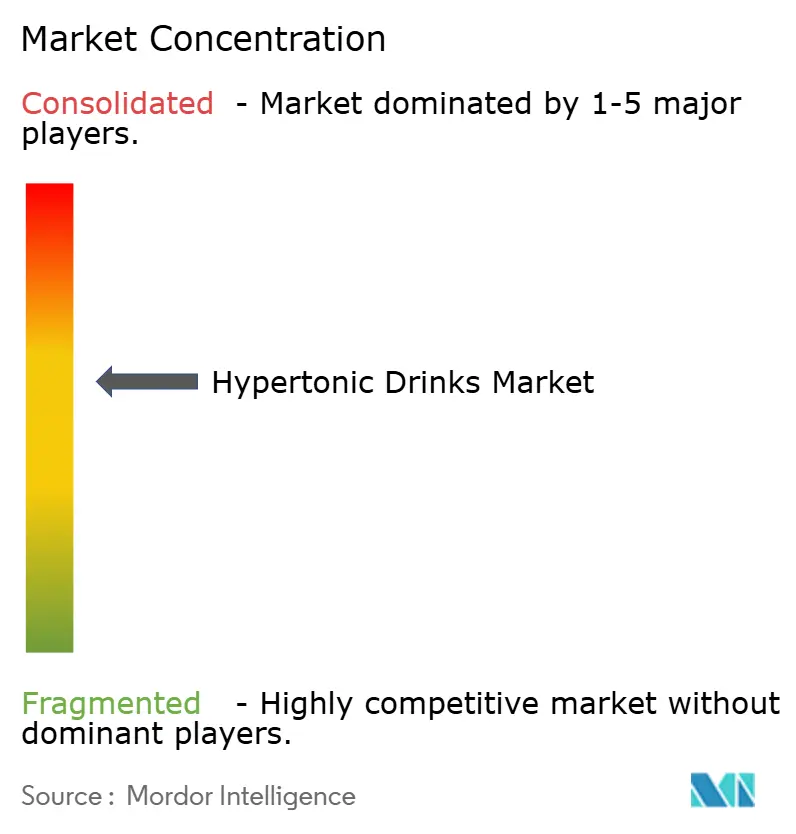

The hypertonic drinks market exhibits a moderate fragmentation, yielding a concentration score of 6 out of 10. Multinational beverage houses such as PepsiCo and Coca-Cola leverage manufacturing scale, ubiquitous distribution, and multi-category brand equity to secure shelf prominence. Their flagship lines integrate incremental carbohydrate increases and functional electrolyte blends, translating research advances into mass-market formats. Meanwhile, innovation-oriented specialists like Maurten and Science in Sport prioritize proprietary hydrogel encapsulation and elite athlete validation, commanding premium pricing among performance purists.

Hydrogel patents exemplify technology-led differentiation; Maurten’s alginate-pectin matrix gels in stomach acid, enabling 90 g carbohydrate per hour with reduced gastric stress, a feature widely publicized through world-record marathon fueling strategies. Competitive response includes PepsiCo’s Gatorade Hydration Booster powder that expands beyond event usage into daily hydration with watermelon and sea-salt electrolytes, signaling a push to reclaim innovator status. Acquisition remains a strategic lever; Keurig Dr Pepper’s USD 990 million majority stake in Ghost illustrates convergence between energy drinks and specialized sports hydration as conglomerates seek authentic brand voices and digital community reach.

Direct-to-consumer insurgents gain momentum through rapid formulation cycles, data-driven subscription curation, and transparent supply chains that resonate with millennial and Gen Z demographics. They offset small-scale manufacturing by partnering with co-packers specializing in aseptic filling and by maintaining tight ingredient portfolios that facilitate quick compliance adjustments across markets. As wearable analytics mainstream, co-branding between sensor manufacturers and beverage labels creates new defensible moats around locked-in recipe algorithms. Competitive intensity is poised to escalate around personalization, flavor depth, and digestive comfort claims, while regulatory shifts in sugar taxation and labeling transparency may recalibrate cost structures across company sizes.

Hypertonic Drinks Industry Leaders

-

The Coca-Cola Company

-

GU Energy Labs

-

Torq Ltd.

-

Etixx Sports Nutrition

-

Science in Sport plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Unlikely hero Merrick Watts has reimagined Posca, infusing it with contemporary flavors and bolstering it with 2000 years of sports science insights, resulting in Australia's inaugural sugar-free sparkling hypertonic drink. Boasting zero sugar, all-natural components, and devoid of stimulants, this drink amplifies hydration and electrolyte retention through its distinctive formulation.

- October 2024: Keurig Dr Pepper acquired 60% stake in Ghost for USD 990 million, marking significant consolidation in the energy drink and sports nutrition sector. The acquisition enhances KDP's position in performance beverages and provides Ghost access to extensive distribution networks for market expansion

- September 2024: PepsiCo launched Gatorade Hydration Booster electrolyte powder targeting everyday hydration needs beyond traditional athletic applications. The product features electrolytes from watermelon juice and sea salt, representing expansion into mainstream wellness markets

Global Hypertonic Drinks Market Report Scope

| RTD Liquid |

| Powder Mix |

| Effervescent Tablets |

| Concentrates |

| Supermarkets & Hypermarkets |

| Convenience Stores |

| Online Retail |

| Specialty Stores |

| Others |

| Athletes/Professional Sports |

| Fitness Enthusiasts |

| Defense & Tactical Personnel |

| Medical/Recovery Patients |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-pacific | |

| South America | Brazil |

| Argentina | |

| Columbia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Turkey | |

| Egypt | |

| Rest of Africa |

| Product Form | RTD Liquid | |

| Powder Mix | ||

| Effervescent Tablets | ||

| Concentrates | ||

| Distribution Channel | Supermarkets & Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Specialty Stores | ||

| Others | ||

| End User | Athletes/Professional Sports | |

| Fitness Enthusiasts | ||

| Defense & Tactical Personnel | ||

| Medical/Recovery Patients | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-pacific | ||

| South America | Brazil | |

| Argentina | ||

| Columbia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Turkey | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for hypertonic drinks in 2030?

Market value is expected to reach USD 8.53 billion by 2030 supported by a 7.96% CAGR.

Which region currently leads in sales of hypertonic beverages?

North America held 41.74% of global sales in 2024 thanks to mature sports nutrition infrastructure and military contracts.

Which product form dominates retail shelves?

Ready-to-drink liquids captured 76.27% share in 2024 because consumers value grab-and-go convenience and dose accuracy.

Who are the fastest-growing consumers of high-carb hydration?

Fitness enthusiasts show a 10.87% projected CAGR as mainstream exercisers adopt elite fueling practices.

Page last updated on: