Managed Database Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

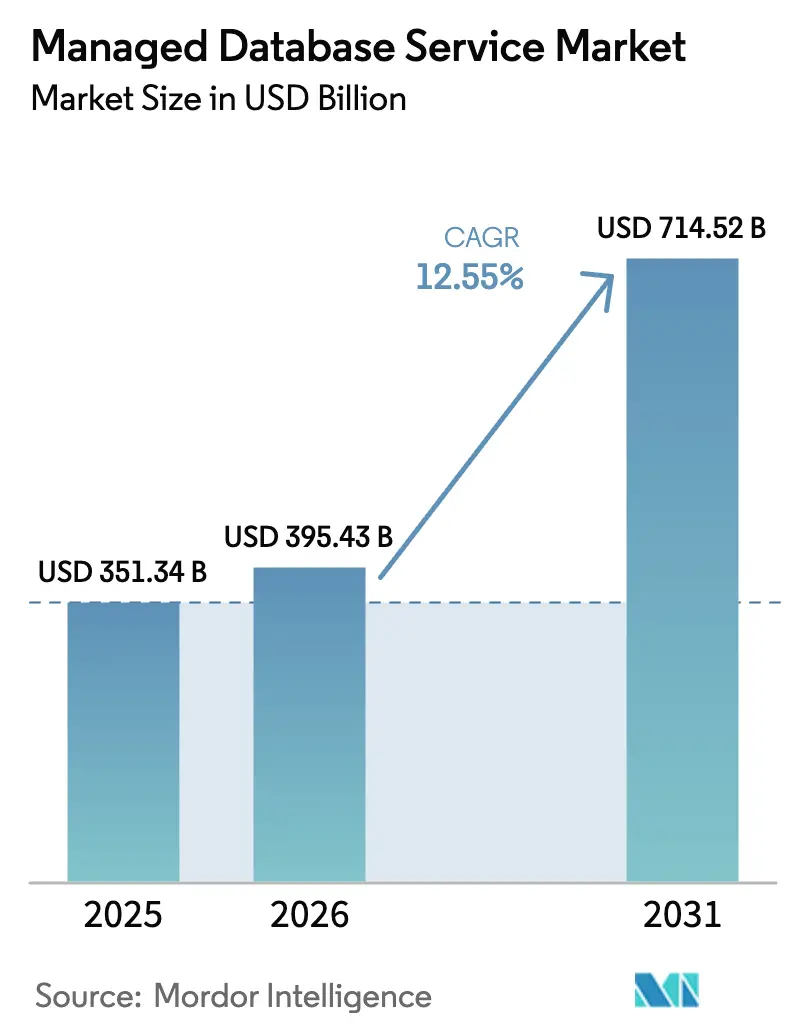

| Market Size (2026) | USD 395.43 Billion |

| Market Size (2031) | USD 714.52 Billion |

| Growth Rate (2026 - 2031) | 12.55% CAGR |

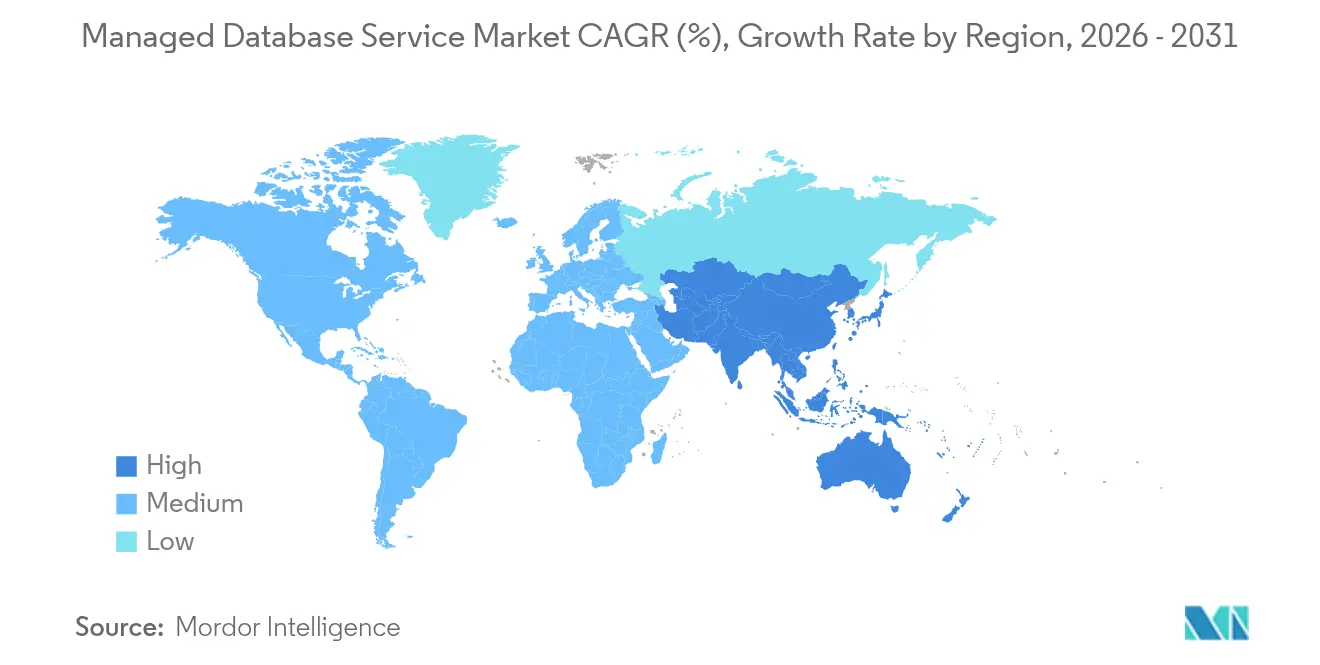

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Database Service Market Analysis by Mordor Intelligence

Managed database service market size in 2026 is estimated at USD 395.43 billion, growing from 2025 value of USD 351.34 billion with 2031 projections showing USD 714.52 billion, growing at 12.55% CAGR over 2026-2031. Rapid migration from on-premises databases to cloud-native, fully managed offerings underpins this expansion as enterprises off-load infrastructure tasks and scale AI workloads seamlessly. Heightened adoption of generative-AI tools is steering investment toward vector databases, while demand for serverless and autonomous capabilities is raising expectations around automatic capacity management. Vendor emphasis on multicloud deployments, interoperability, and data-sovereignty controls is widening competitive opportunities even as hyperscalers consolidate share. Momentum is strongest where regulated industries combine compliance obligations with real-time analytics objectives, notably in finance, healthcare, and manufacturing.

Key Report Takeaways

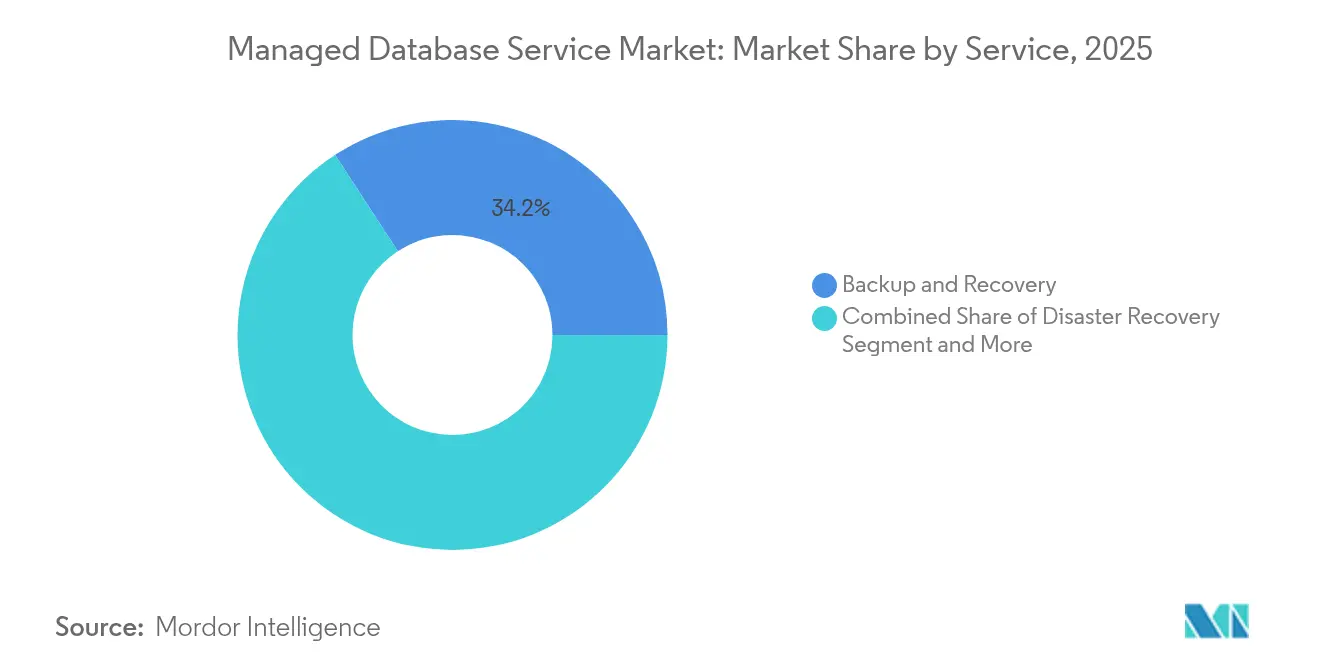

- By service, Backup & Recovery led with 34.19% revenue share in 2025, whereas Security & Compliance is expanding at a 22.65% CAGR through 2031.

- By deployment model, Public Cloud held 67.21% of the managed database service market share in 2025, while Hybrid/Multi-cloud usage is projected to climb at a 27.10% CAGR to 2031.

- By database type, traditional SQL engines commanded 57.96% of the managed database service market size in 2025; Vector/AI-ready platforms are set to rise at a 40.75% CAGR.

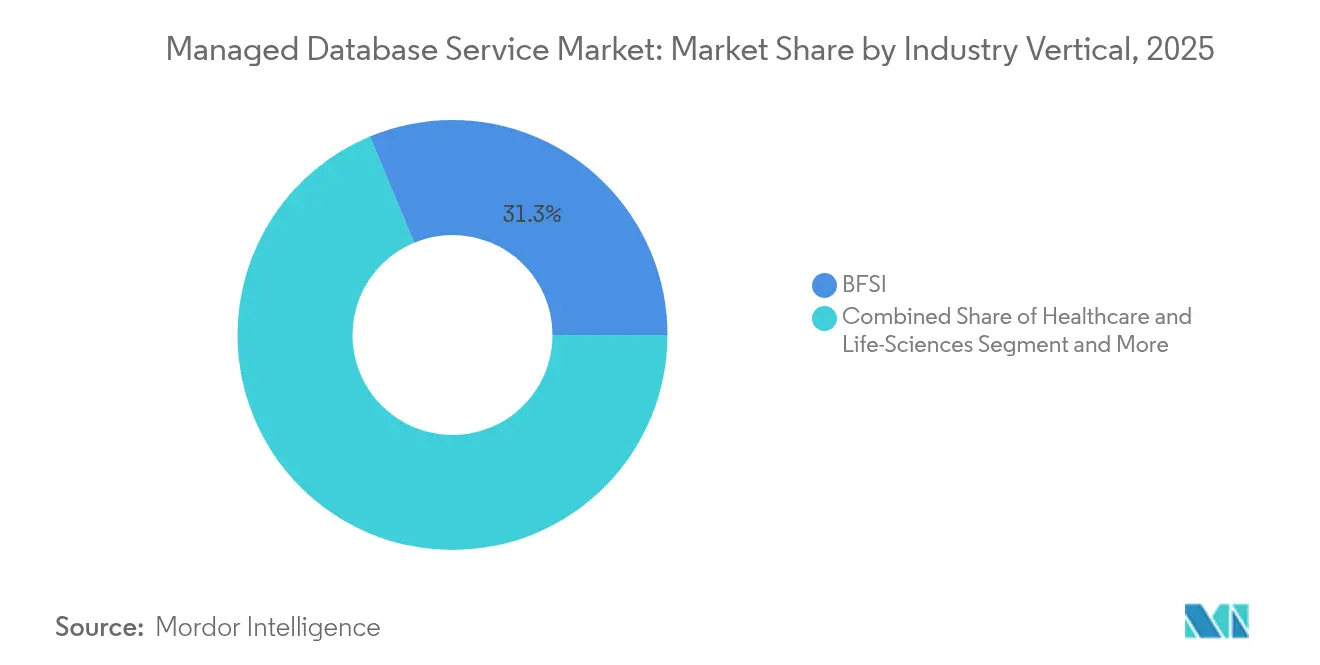

- By industry vertical, BFSI captured 31.28% revenue share in 2025, while healthcare is poised to accelerate at a 23.90% CAGR through 2031.

- By geography, North America accounted for 43.34% share of the managed database service market in 2025 and Asia-Pacific is advancing at a 24.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Managed Database Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native application boom | +2.8% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| SME shift to pay-as-you-go pricing | +1.9% | Global; notable in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| IoT/edge data growth | +2.1% | Asia-Pacific core; spill-over to Middle East, Africa, NA | Long term (≥ 4 years) |

| Generative-AI workloads | +3.2% | Global; led by North America | Medium term (2-4 years) |

| Public-cloud hyperscaler incentives | +1.4% | North America and Europe; emerging in Asia-Pacific | Short term (≤ 2 years) |

| Autonomous/serverless DB capabilities | +2.0% | Global; early uptake in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Application Boom Across Industries

Enterprises are rebuilding software into microservices that demand elastically scalable, API-driven data tiers. Fully managed databases remove configuration and patching chores, letting teams deliver new features faster while maintaining distributed-transaction integrity. Financial institutions are at the forefront as they refactor core banking into event-driven architectures, requiring real-time synchronization across hundreds of services. Digital-native firms likewise favor platforms that free engineers from low-value administration to focus on revenue-generating code. Resulting workload diversity keeps the managed database service market in the innovation spotlight.

SME Shift from Cap-Ex to Pay-As-You-Go DBaaS Pricing

Small and medium enterprises, once deterred by license fees and hardware outlays, now tap consumption-based tiers that map spend directly to usage. Hyperscalers have lowered entry barriers with permanent free allowances and graduated storage costs, making enterprise-grade durability attainable without specialist staff. In emerging economies, where cash preservation dominates budgeting decisions, the appeal is even sharper. As these firms adopt analytics and AI, automated backup, patching, and scaling become must-haves, reinforcing demand for managed services that compress total cost of ownership.

IoT/Edge Data Growth Demanding Elastic, Geo-Distributed Databases

Industrial automation, smart logistics, and connected vehicles push exabyte-scale telemetry to the edge, where sub-millisecond responsiveness is non-negotiable. Managed platforms supporting regional replicas and intelligent data placement solve latency and partitioning challenges while ensuring global visibility. Providers that enable auto-sharding, conflict resolution, and hot-standby failover are becoming strategic partners for manufacturing and telecom operators rolling out 5G and private-LTE networks.

Generative-AI Workloads Requiring Vector and Multimodal Databases

High-dimensional embeddings underpin retrieval-augmented generation, similarity search, and multimodal recommendation engines. Traditional SQL indexes cannot sustain the necessary throughput, driving uptake of vector-optimized engines that integrate seamlessly with large-language-model toolchains. Oracle added AI Vector Search directly inside its managed database portfolio to capture this demand. [1]Oracle Corporation, “Oracle Adds AI Vector Search to Oracle Database 23ai,” oracle.com Health-tech platforms, in particular, need combined imaging-plus-text queries to support diagnostic support systems, accelerating specialist-database adoption.

Restraints Impact Analysis*

| Restraint | ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and residency mandates | −1.8% | European Union, China, Russia; expanding in Asia-Pacific | Long term (≥ 4 years) |

| Vendor lock-in fears | −1.2% | Global; acute in large enterprises | Medium term (2-4 years) |

| Latency-critical workloads favoring on-prem | −0.9% | Global; concentrated in manufacturing and finance | Long term (≥ 4 years) |

| Skill-set gap in FinOps and observability | −0.7% | Global; higher in traditional enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Residency Mandates

Jurisdictions enforcing local data storage compel providers to build or lease in-country facilities, fragmenting capacity pools and raising costs. Enterprises operating across multiple regions must classify sensitive records and enforce geo-fencing at application level, complicating architecture and compliance verification. MongoDB’s regionalized clusters and FedRAMP-authorized offerings illustrate the engineering and certification investment required to satisfy overlapping regulations.[2]MongoDB Inc., “MongoDB Completes Acquisition of Voyage AI,” mongodb.com

Vendor Lock-In Concerns with Proprietary Cloud APIs

Organizations fear that bespoke extensions trap workloads, inflate future switching costs, and stifle negotiation leverage. Oracle’s multicloud pact places fully managed Oracle Database instances directly on AWS infrastructure, reflecting market pressure for portability.[3]Amazon Web Services, “Oracle Database@AWS Now Generally Available,” aws.amazon.com Even so, reconciling divergent IAM models, billing constructs, and monitoring stacks can dilute promised agility, sustaining interest in open-source engines and cross-cloud abstractions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Backup Foundations and Compliance Momentum

Backup & Recovery services underpinned 34.19% of the managed database service market in 2025, validating that data durability remains the baseline requirement for cloud migration. Enterprises rely on automated snapshots, point-in-time restore, and cross-region replication to meet disaster-recovery-ready SLAs. Cyber-resilience priorities keep this segment at the center of procurement checklists, ensuring steady absolute expansion even as relative share moderates.

Security & Compliance offerings, though smaller in 2025, are scaling fastest at 22.65% CAGR. Encryption key management, zero-trust access controls, and continuous audit trails speak directly to board-level risk mandates. Providers differentiate with fine-grained tokenization, bring-your-own-key support, and real-time anomaly detection. Heightened enforcement of privacy acts cements spending intent among healthcare and government tenants, injecting sustained energy into this high-growth niche.

By Deployment Model: Hybrid Becomes the New Default

Public-cloud residency generated 67.21% of managed database service market revenues in 2025, reflecting mature global footprints and elastic pricing. Enterprises gravitate to these platforms for global latency diversity, rich PaaS ecosystems, and seamless AI adjacency. Yet compliance-sensitive workloads and performance-critical applications often warrant alternative placement.

Hybrid and multi-cloud strategies are rising at a 27.10% CAGR as firms hedge against outages, price shocks, and lock-in. Tooling that provides unified management across on-prem, edge, and multiple public clouds is a decisive purchase criterion. Vendors that simplify network-attached replication, consistent IAM propagation, and cost telemetry gain notable mind-share among banks, insurers, and telecom operators charting phased modernization roadmaps.

By Database Type: Vector Acceleration Upsets the Hierarchy

SQL remained foundational with 57.96% revenue share in 2025. Financial-grade ACID guarantees, decades of ecosystem tooling, and broad developer familiarity keep relational paradigms indispensable for core transaction records. Providers reinforce relevance with automatic index management, self-tuning queries, and integration into serverless query fabrics.

Meanwhile, vector/AI-ready engines are compounding at 40.75% CAGR. Purpose-built similarity indexes, hybrid dense/sparse retrieval, and GPU acceleration solve memory-intensive inference patterns. Databricks’ acquisition of Neon brings serverless Postgres into an analytics-first platform, signaling convergence where OLTP and vector search co-exist in shared storage layers. NoSQL and multi-model variants fill use-case gaps where schema flexibility and horizontal sharding eclipse strict consistency.

By Application: Analytics and AI Steer Spend

Customer Relationship Management retained 28.91% share in 2025, underscoring the universal imperative to house unified customer profiles. Always-on availability and low-latency writes underpin this dominance. Yet analytics and AI workloads are the growth engine, surging at 28.91% CAGR as predictive customer insights, fraud detection, and supply-chain forecasting become board-level imperatives.

These analytics workloads increasingly blend unstructured logs, images, and sensor data, forcing databases to bridge OLTP and OLAP within a single fabric. Engines that offer columnar storage, materialized views, and embedded machine learning gain traction. Managed providers that align cost models to bursty query patterns win favor among finance and retail operators orchestrating nightly batch and daytime ad-hoc exploration in parallel.

By Industry Vertical: Healthcare Outpaces All Sectors

BFSI drove 31.28% of 2025 revenue, leveraging decades of digitization and heavy audit requirements. Managed database adoption now focuses on lowering operational expenditure and meeting 24×7 transaction-integrity imperatives. Providers emphasizing FIPS-compliant encryption and real-time reconciliation features defend market share.

Healthcare is advancing at a 23.90% CAGR as telemedicine, genomics, and imaging diagnostics bloom. Database services touting HIPAA eligibility, immutable audit logging, and data-masking APIs satisfy stringent clinical-data stewardship mandates. Multimodal AI pipelines—which require simultaneous access to images, text, and structured EHR data—cement the use of vector-enabled stores. Supply-chain traceability and digital twin initiatives in manufacturing, plus hyper-personalized recommendations in retail, deepen vertical diversification of the managed database service market.

By Organization Size: Democratized Sophistication

Large enterprises still dominate spend thanks to application sprawl and geographic reach. Yet they increasingly favor managed options to rationalize toolchains and redeploy talent toward higher-value engineering. Cross-border organizations emphasize federation, governance, and advanced observability, directing vendors to enrich policy-driven automation.

SMEs register the sharpest growth as simplified consoles and predictive scaling dissolve traditional DBA barriers. Free-tier entry points draw startups, while graduated storage classes accommodate seasonal retailers and regional logistics providers. Barclays’ 2024 CIO survey notes that database‐oriented optimizations remain a budget bright spot. Such findings indicate that parity of capability across company sizes is narrowing, fueling inclusive expansion of the managed database service industry.

Geography Analysis

North America remained the epicenter with 43.34% share in 2025, propelled by aggressive cloud migration in finance, technology, and media. The United States hosts all three hyperscalers at hyperscale, giving enterprises unmatched choice in compliance attestations, AI service adjacency, and inter-region latency management. Growth, however, is tempering as earlier movers shift attention from lift-and-shift to cost control and workload optimization, opening space for specialized providers offering cross-cloud governance toolsets.

Asia-Pacific is the sprint leader, advancing at a 24.85% CAGR to 2031. China’s state-backed digital infrastructure programs and India’s fintech surge fuel data-first business models that jump directly to serverless, fully managed back-ends. Regional cloud entrants mount competitive pricing and sovereign-cloud guarantees that resonate with public-sector and industrial customers wary of foreign jurisdiction. The managed database service market size for Asia-Pacific is forecast to more than triple over the period as 5G and IoT ecosystems mature.

Europe shows a complex mix of opportunity and constraint. GDPR and forthcoming AI legislation heighten demand for auditable, fine-grained data-control features. At the same time, energy-efficiency targets incentivize providers to site facilities in renewable-rich regions such as the Nordics, influencing capacity-planning strategies. Sovereign-cloud initiatives in France and Germany reinforce the strategic value of regional partnerships, ensuring sustained, if measured, expansion.

Competitive Landscape

Competition centers on the infrastructure scale and integrated tooling of AWS, Microsoft Azure, and Google Cloud Platform. These hyperscalers continue to deepen managed-database portfolios with serverless modes, multi-writer replication, and vector indexing, growing stickiness inside their broader ecosystems. AWS’s launch of Aurora DSQL, a globally distributed SQL service, underscores this cadence.

Specialist vendors differentiate through the breadth of data models or performance under niche workloads. MongoDB integrates document and vector search; Snowflake extends from warehouses into transactional lanes via its Crunchy Data acquisition. Cockroach Labs and PlanetScale court developers need globally consistent yet autonomously scaling relational stores, making them popular choices for consumer-grade SaaS firms.

Partnerships and acquisitions intensify as platforms converge. Oracle Database AWS provides full Oracle functionality on native AWS compute while retaining Oracle support guarantees. Databricks’ USD 1 billion Neon purchase folds serverless Postgres into its lakehouse, signaling that analytics-first vendors see operational data as strategic, not adjacent. Such moves indicate an industry marching toward unified data platforms that collapse transactional, analytical, and AI workloads into a seamless managed experience.

Managed Database Service Industry Leaders

Amazon Web Services (AWS)

Microsoft Azure

Google Cloud Platform (GCP)

Oracle Corporation

IBM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Oracle released Oracle Database@AWS for direct, fully managed Oracle deployments inside AWS regions, expanding multicloud options for joint customers.

- November 2024: Databricks acquired Neon for USD 1 billion to embed serverless PostgreSQL capabilities into its lakehouse platform.

- October 2024: Snowflake closed a USD 250 million deal for Crunchy Data, gaining PostgreSQL expertise and broadening its operational data services.

- September 2024: AWS introduced Aurora DSQL, a serverless distributed SQL engine delivering global consistency with local-region performance.

Global Managed Database Service Market Report Scope

In a managed database service, users pay a cloud provider for database access. With a growing emphasis on core business functions and customer needs, organizations increasingly turn to managed services to navigate the intricacies of database management. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The managed database service market is segmented by service (Data Administration, Database Backup & Recovery, Database Disaster Recovery, Database Security, and Database Optimization), by application (Customer Relationship Management, Enterprise Resource Planning. Supply Chain Management, Web Applications, and Big Data Analytics), by industry vertical (BFSI, Healthcare, IT & Telecom, Retail, Manufacturing and Other Industries) and by geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Data Administration |

| Backup and Recovery |

| Disaster Recovery |

| Security and Compliance |

| Performance Optimisation and Tuning |

| Public Cloud |

| Private Cloud |

| Hybrid / Multi-cloud |

| Relational (SQL) |

| NoSQL |

| Multimodel / NewSQL |

| Vector / AI-ready |

| Customer Relationship Management |

| Enterprise Resource Planning |

| Supply-Chain Management |

| Web and Mobile Applications |

| Big-Data / Analytics and AI |

| BFSI |

| Healthcare and Life-Sciences |

| IT and Telecom |

| Retail and E-commerce |

| Manufacturing |

| Government and Public Sector |

| Others (Media, Education, Energy) |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Service | Data Administration | ||

| Backup and Recovery | |||

| Disaster Recovery | |||

| Security and Compliance | |||

| Performance Optimisation and Tuning | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid / Multi-cloud | |||

| By Database Type | Relational (SQL) | ||

| NoSQL | |||

| Multimodel / NewSQL | |||

| Vector / AI-ready | |||

| By Application | Customer Relationship Management | ||

| Enterprise Resource Planning | |||

| Supply-Chain Management | |||

| Web and Mobile Applications | |||

| Big-Data / Analytics and AI | |||

| By Industry Vertical | BFSI | ||

| Healthcare and Life-Sciences | |||

| IT and Telecom | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Others (Media, Education, Energy) | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the managed database service market?

The market stands at USD 395.43 billion in 2026 and is projected to grow to USD 714.52 billion by 2031.

Which deployment model dominates spending?

Public-cloud deployments account for 67.21% of revenue, though hybrid and multi-cloud strategies are expanding at 27.10% CAGR.

Why are vector databases gaining traction?

Generative-AI workloads require high-dimensional similarity searches that traditional relational indexes cannot handle, driving 40.75% CAGR in vector/AI-ready engines.

Which region is growing the fastest?

Asia-Pacific leads with a 24.85% CAGR through 2031 due to accelerated digital transformation across manufacturing, e-commerce, and fintech.

Page last updated on: