Banking Maintenance Support And Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

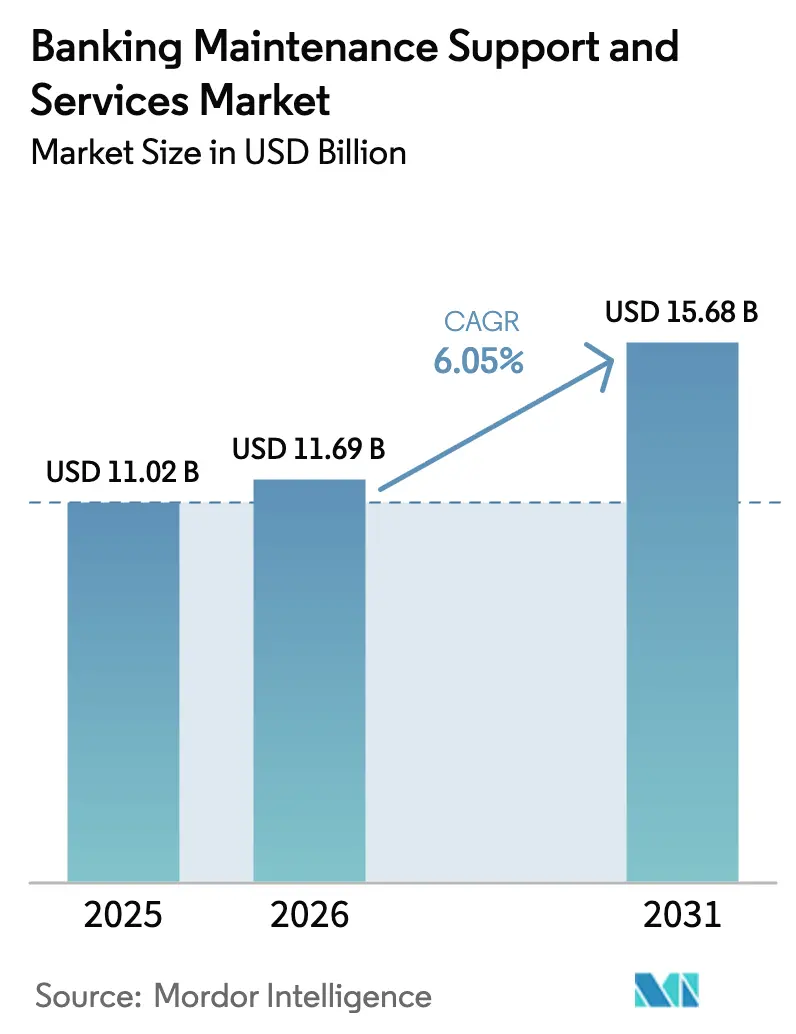

| Market Size (2026) | USD 11.69 Billion |

| Market Size (2031) | USD 15.68 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

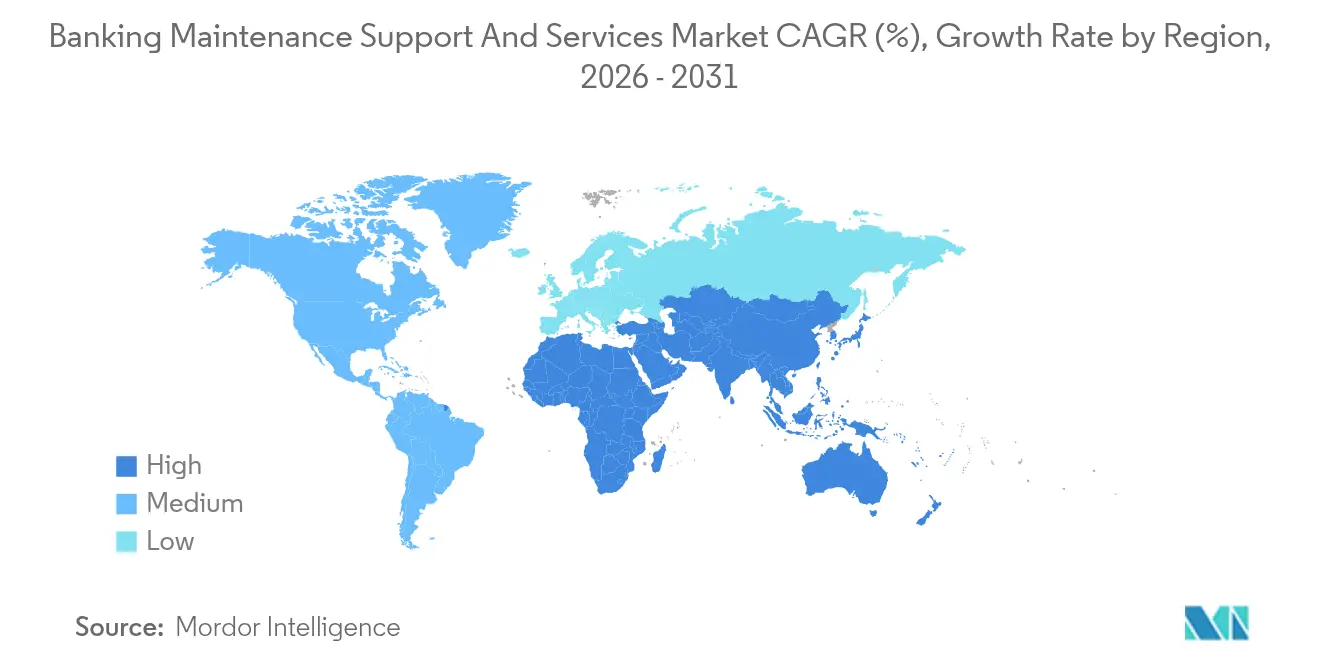

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Banking Maintenance Support And Services Market Analysis by Mordor Intelligence

The Banking Maintenance Support and Services market size is expected to grow from USD 11.02 billion in 2025 to USD 11.69 billion in 2026 and is forecast to reach USD 15.68 billion by 2031 at 6.05% CAGR over 2026-2031. Greater spending on incident-response contracts, rapid core-platform refresh cycles and tighter uptime regulations are the primary demand catalysts. Vendors are fusing corrective maintenance with cyber-threat monitoring, while banks are bundling observability, patch management and regulatory-reporting support into single, outcome-based agreements. Cloud elasticity, consumption-based pricing and API-driven architectures are steering workloads toward hybrid arrangements that still retain mission-critical ledgers on-premises. Regional specialists are gaining share by offering sovereign-cloud services and ISO 20022 migration expertise as compliance deadlines approach.

Key Report Takeaways

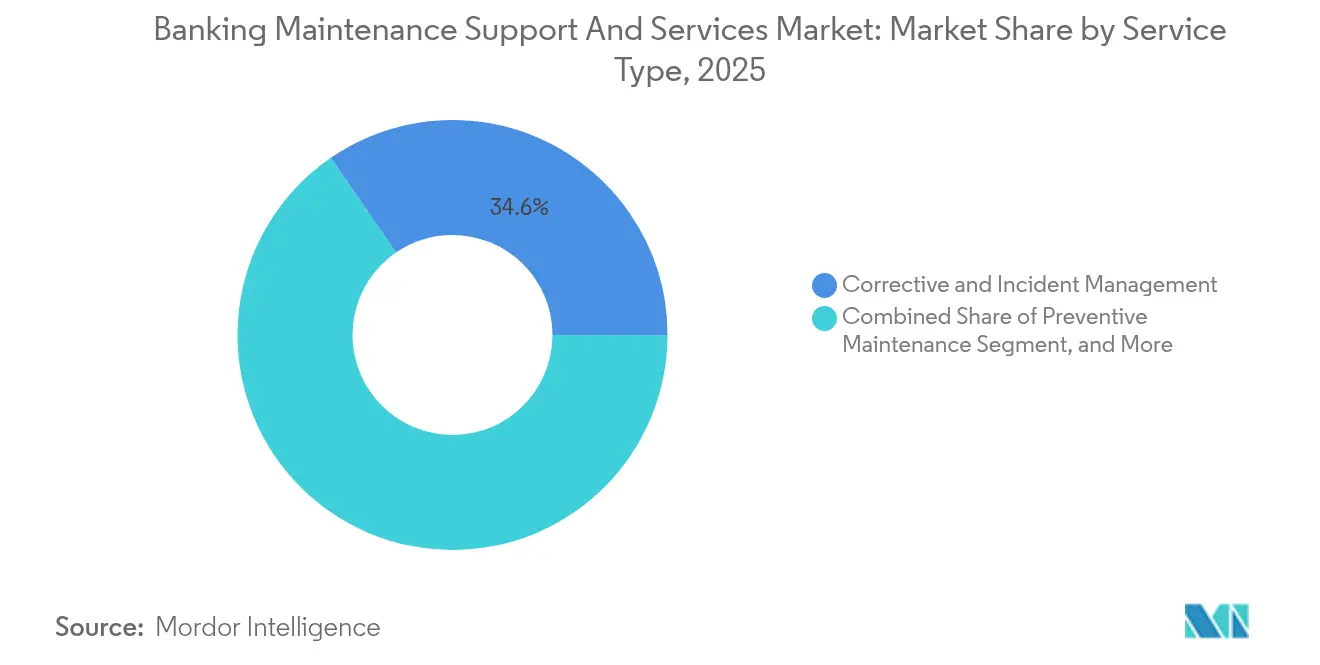

- By service type, corrective and incident management services held 34.58% of the Banking Maintenance Support and Services market share in 2025, while cloud-based managed services are projected to expand at a 6.58% CAGR through 2031.

- By deployment model, on-premises contracts accounted for 59.10% of 2025 revenue; however, cloud-based engagements are projected to grow at a 7.12% CAGR through 2031.

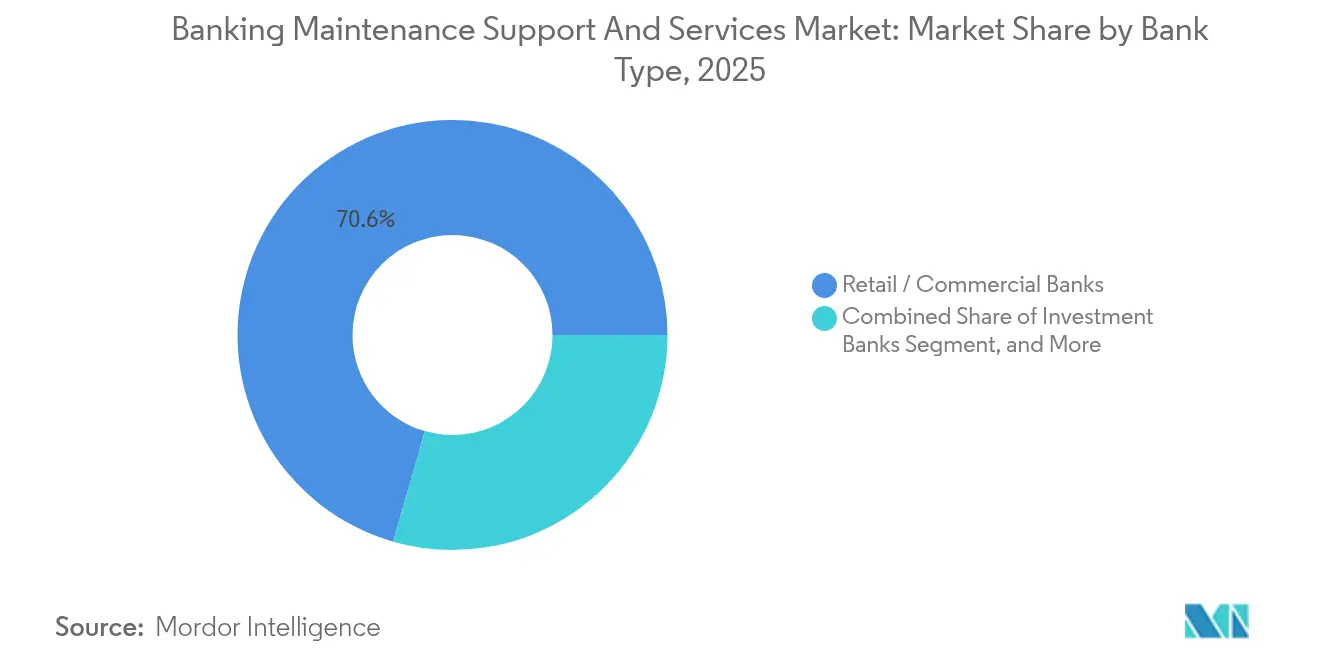

- By bank type, retail and commercial institutions accounted for 70.55% of 2025 spending, whereas digital-only and neo-banks represented the fastest-growing client segment, with a 6.52% CAGR.

- By component, core banking platforms accounted for 39.88% of the 2025 outlays, while channel systems, ATMs, point-of-sale, online, and mobile systems are projected to rise at a 6.32% CAGR to 2031.

- By geography, Asia-Pacific captured 33.05% of global revenue in 2025 and is expanding at a 6.61% CAGR on the back of surging UPI and digital-yuan volumes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Banking Maintenance Support And Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Core-Banking System Obsolescence | +1.2% | North America, Europe, Global Tier-1s | Medium term (2-4 years) |

| Intensifying Cyber-Threat Landscape | +1.1% | APAC, North America, Global | Short term (≤ 2 years) |

| Regulatory Mandates for 24/7 Uptime | +0.9% | Europe, North America, APAC | Medium term (2-4 years) |

| Shift to X-as-a-Service Operating Models | +0.8% | North America, Western Europe, Global | Long term (≥ 4 years) |

| Cloud-Native Observability Toolchains | +0.7% | North America, Europe, APAC Tier-1 banks | Medium term (2-4 years) |

| ESG-Driven Decommissioning of Legacy Hardware | +0.5% | Europe, North America, Japan, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Core-Banking System Obsolescence

End-of-life notices for mainframe operating systems are bringing forward refresh timelines. IBM ended extended support for z/OS 2.4 in September 2024, prompting 340 banks to migrate or accept 40% higher maintenance costs.[1] IBM Corporation, “z/OS Lifecycle Announcement,” ibm.com Temenos stated that 58% of its new-license bookings in 2024 originated from replacements of systems older than 15 years, with migrations averaging 18 months in parallel-run mode. FIS logged a 29% jump in core-modernization consulting engagements as banks seek ISO 20022-compliant platforms ahead of the November 2025 deadline. Hybrid support models are emerging, pairing mainframe JCL specialists with Kubernetes engineers to ensure data integrity during staged cut-overs. The result is steady demand for dual-skilled maintenance teams able to manage legacy and cloud-native platforms in tandem.

Intensifying Cyber-Threat Landscape

Ransomware assaults on core-banking environments reached 127 recorded events in 2024, with average demands of USD 4.2 million per incident. API exposure for open-banking has heightened vulnerability, as regulators flagged 2,300 inadequate-authentication cases during supervisory reviews. Zero-trust architecture adoption doubled year-over-year to 41%, fueling growth in bundled security-operations-center retainers. Cognizant noted that 68% of its banking clients now combine infrastructure and cybersecurity support under a single SLA, blurring maintenance and defense boundaries. Continuous configuration audits and rapid patch cycles have consequently become baseline contract inclusions.

Regulatory Mandates for 24/7 Uptime

The European Union’s Digital Operational Resilience Act (DORA) took effect in January 2025, compelling banks to classify ICT providers as critical and run annual penetration tests. Singapore’s revised Technology Risk Management rules require 99.95% channel availability and 2-hour regulatory access to incident logs. In the United States, the Federal Reserve mandates resumption of critical operations within 2 hours, formalizing restoration expectations. These benchmarks are driving premium-tier support contracts with 15-minute response times, as evidenced by 73% of Jack Henry’s community-bank clients upgrading in 2024. Vendor accountability for uptime is now contractual rather than aspirational.

Shift to X-as-a-Service Operating Models

Consumption-based pricing is displacing fixed-fee frameworks. Infosys’ pay-per-transaction plan charges USD 0.0012 per API call, aligning costs with actual workload volumes. Fiserv reported that 34% of its core-banking customers transferred infrastructure and application support risk to the vendor in exchange for revenue-share models. Capgemini’s predictive staffing algorithms cut labor expenses by 19% while raising first-call resolution to 82%. Such models favor automation and AIOps to protect vendor margins. Banks benefit from elastic pricing, while providers capture recurring, usage-linked revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Vendor-Lock-In Switching Costs | -0.8% | North America, Europe, Global | Medium term (2-4 years) |

| Scarcity of L3 Talent for COBOL and Mainframes | -0.6% | North America, Western Europe, Global | Long term (≥ 4 years) |

| Capital Spending Freeze in Tier-2/3 Banks | -0.5% | North America, Europe, some APAC | Short term (≤ 2 years) |

| Rising Open-Source Support Reducing Contracts | -0.4% | APAC, Latin America, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Vendor-Lock-In Switching Costs

Oracle disclosures show exit fees of 18–22% of remaining contract value for early termination, dissuading migrations. A mid-tier European bank spent EUR 3.8 million(USD 4.42 million) extracting 18 years of data, extending its cloud timeline by 14 months. FIS retained 94% of top-100 clients in 2024, crediting renewal success to elevated switching friction rather than functionality. Proprietary data formats and IP restrictions force costly redevelopment of customized modules during platform shifts. Consequently, incumbent vendors maintain pricing power despite rising open-source alternatives.

Capital Spending Freeze in Tier-2/3 Banks

Community banks’ net-interest margins shrank 42 basis points in 2024, resulting in a 16% reduction in discretionary tech budgets.[2]Federal Deposit Insurance Corporation, “Quarterly Banking Profile Q4 2024,” fdic.gov Thirty-eight percent of Jack Henry’s Tier-3 clients postponed core migrations, opting for patch-only coverage. Cooperative banks in Europe trimmed IT capex to maintain Tier-1 capital ratios. The result is a bifurcated market in which Tier-1 institutions modernize aggressively, while smaller peers struggle with legacy assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Incident Management Remains the Revenue Anchor

Corrective and incident-management contracts produced the largest stream of revenue, accounting for 34.58% of Banking Maintenance Support and Services market size in 2025. Banks confront concurrent failures across legacy monoliths and microservices, resulting in high headcounts for break-fix and ticket-triage. Cloud-based managed services, however, are expected to grow at a 6.58% CAGR to 2031, reflecting the migration to subscription bundles that combine monitoring, patching, and response capabilities.

Preventive maintenance is being replaced by predictive analytics, which curtails scheduled downtime. Infosys clients trimmed maintenance windows by 34% after deploying failure-forecast models. ATM service contracts now integrate cash-optimization algorithms; NCR cut replenishment runs by 28%, adding software renewals to hardware deals. Compliance-driven patch management demand intensified with the release of PCI DSS 4.0, which halves the permissible patch windows, creating new revenue opportunities for automation-centric vendors.

By Deployment Model: Hybrid Structures Balance Control and Elasticity

On-premises setups commanded 59.10% of 2025 spending, but cloud contracts will log the fastest 7.12% CAGR, aided by scalable consumption and freed capex. The Banking Maintenance Support and Services market share for on-premises models will erode as auditors gain comfort with sovereign-cloud controls.

Hybrid models dominate new projects. Two-thirds of Fiserv’s clients split customer-facing channels between AWS and Azure, while retaining batch settlement on mainframes. IBM’s mainframe support now includes migration road maps, embedding vendors early in lift-and-shift journeys. Dual-skilled engineers certified in z/OS and Kubernetes are in high demand, and ECB cloud guidelines clarify hybrid-support needs by allowing banks to park non-critical workloads in public clouds.

By Bank Type: Neo-Banks Redefine Velocity

Retail and commercial banks generated 70.55% of 2025 expenditure, underpinned by branch networks and ATM fleets that necessitate 24/7 support. Yet digital-only and neo-banks will post a 6.52% CAGR to 2031, reshaping the Banking Maintenance Support and Services market with CI/CD pipelines that need near-real-time rollback.

Chime averaged 47 daily code pushes in 2024, mandating automated monitoring frameworks that legacy quarterly release cadences cannot match. Nubank’s 180-person SRE organization maintains 18,000 TPS across Kubernetes clusters. Cooperative banks share sectoral bureaus to offset talent gaps, while investment banks pay premiums for sub-5-minute response on trading systems.

By Component Supported: Core Platforms Dominate Spend, Channels Accelerate

Core platforms absorbed 39.88% of 2025 budgets, as they process deposits, loans, and general ledger entries that define systemic resilience. Nevertheless, channel components are expected to grow at a 6.32% CAGR, driven by biometric ATMs, QR-code POS terminals, and increasing mobile traffic.

FedNow’s adoption by 850 U.S. banks illustrates how real-time settlement extends support scopes to 24/7 operations. Diebold Nixdorf observed an 18% increase in per-unit ATM maintenance costs due to the use of advanced hardware. Risk and compliance engines increase patch cycles, with a European Tier-1 bank operating 14 AML engines that require quarterly sanctions updates. Neglecting ancillary systems can lead to cascading failures, as a regional U.S. bank learned after an HR-system credential theft compromised core ledgers.

Geography Analysis

Asia-Pacific posted the highest growth trajectory, reflecting transaction-volume surges from India’s UPI and China’s digital-currency pilots. Banks in India are negotiating outcome-based contracts tied to transaction throughput, compelling vendors to guarantee sub-second response across heterogeneous stacks. Chinese institutions, as they roll out e-CNY wallets, require simultaneous support for blockchain nodes and legacy core platforms, resulting in dual-skill hiring waves. Southeast Asian regulators, including Singapore’s MAS, mandate 99.95% channel availability, driving the uptake of premium support tiers among newly licensed digital banks.

North America remains a technology bellwether as FedNow instant payments migrate from overnight settlement to real-time. U.S. Tier-1 banks are accelerating the retirement of COBOL; early adopters report 12% operational cost savings after shifting to cloud-native cores. Canadian banks, governed by OSFI resilience frameworks, request unified observability across mainframes and public clouds. Vendor competition intensifies as hyperscalers co-sell managed-services bundles with partners specializing in financial-grade compliance.

Europe’s agenda centers on DORA enforcement and ISO 20022 standardization. Banks face overlapping GDPR, PSD2 and Basel III obligations, creating a labyrinth of audit trails that must be maintained within two hours for regulators. Managed-services providers bundle compliance templates, automated incident-reports and third-party risk registers into SLA-backed offerings. Nordic banks pioneer green-data-center migrations, aided by abundant hydroelectric power, linking ESG metrics to maintenance KPIs.

Competitive Landscape

The Banking Maintenance Support and Services market is moderately fragmented, with the top 10 vendors controlling roughly 48% of the 2024 revenue, allowing specialized regional firms to flourish. Tata Consultancy Services leverages 12,000-seat hubs in India and Eastern Europe to deliver ISO 20022 migration and 24/7 incident management at 40–55% labor-cost savings. Temenos vertically integrated by purchasing a cloud consultancy for EUR 85 million (USD 98.93 million), enabling bundled software and migration engagements that curb reliance on third-party integrators. Revolut insourced 320 platform engineers to safeguard customer experience, highlighting how neo-banks prioritize in-house SRE talent.

DXC’s pending patent aggregates telemetry from mainframes and hyperscalers to cut incident resolution times. Intellect Design Arena’s DORA compliance module automatically generates incident reports, targeting mid-tier banks in Europe. Open-source ecosystems pressure price points; Apache Fineract deployments enable cost reductions, which commercial vendors respond to with lower-tiered subscription models.

Traditional hardware suppliers pivot toward software and managed services to offset declining ATM shipments. Diebold Nixdorf bundles biometric upgrade paths with predictive-maintenance analytics, while IBM offers cloud-transition assessments within mainframe support contracts. The result is convergence between systems integrators, software providers and hardware OEMs vying for the same recurring-revenue pools.

Banking Maintenance Support And Services Industry Leaders

NCR Corporation

Diebold Nixdorf, Incorporated

Fidelity National Information Services, Inc. (FIS)

Fiserv, Inc.

Temenos AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The European Banking Authority released final DORA technical standards, forcing banks to classify ICT providers as critical and run annual penetration tests.

- November 2024: Tata Consultancy Services opened a 12,000-seat banking-support hub in Pune, focused on ISO 20022 migrations for European banks.

- October 2024: Fiserv earmarked USD 240 million for its cloud-native core platform, adding real-time fraud detection and automated regulatory reporting.

- September 2024: IBM ceased extended support for z/OS 2.4, triggering higher maintenance fees and accelerating cloud migration plans for 340 banks.

Global Banking Maintenance Support And Services Market Report Scope

The Banking Maintenance Support and Services Market comprises solutions and services that ensure the continuous performance, reliability, and security of banking IT systems. It encompasses a wide range of service types, including preventive maintenance, incident management, ATM managed services, software upgrades, compliance support, and IT infrastructure operations, delivered via cloud, on-premises, or hybrid models. The market serves a diverse range of bank types, including retail/commercial banks, cooperative and mutual institutions, investment banks, and digital-only/neo-banks, supporting components such as core banking platforms, channels, payment systems, risk and compliance tools, and ancillary systems.

The Banking Maintenance Support and Services Market Report is Segmented by Service Type (Preventive Maintenance, Corrective & Incident Management, ATM Managed Services, Software Upgrade and Patch Management, Regulatory Compliance and Audit Support, IT Infrastructure Support), Deployment Model (Cloud, On-Premises, Hybrid), Bank Type (Retail/Commercial, Cooperative & Mutual, Investment, Digital-only/Neo-banks), Component Supported (Core Banking Platforms, Channels, Payment Processing, Risk and Compliance, Ancillary Systems), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Preventive Maintenance |

| Corrective and Incident Management |

| ATM Managed Services |

| Software Upgrade and Patch Management |

| Regulatory Compliance and Audit Support |

| IT Infrastructure Support |

| Cloud |

| On-Premises |

| Hybrid |

| Retail / Commercial Banks |

| Cooperative and Mutual Banks |

| Investment Banks |

| Digital-only / Neo-banks |

| Supported Core Banking Platforms |

| Channels (ATM / POS / Online / Mobile) |

| Payment Processing Systems |

| Risk and Compliance Systems |

| Ancillary Systems (CRM, Treasury, HR) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Preventive Maintenance | ||

| Corrective and Incident Management | |||

| ATM Managed Services | |||

| Software Upgrade and Patch Management | |||

| Regulatory Compliance and Audit Support | |||

| IT Infrastructure Support | |||

| By Deployment Model | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Bank Type | Retail / Commercial Banks | ||

| Cooperative and Mutual Banks | |||

| Investment Banks | |||

| Digital-only / Neo-banks | |||

| By Component | Supported Core Banking Platforms | ||

| Channels (ATM / POS / Online / Mobile) | |||

| Payment Processing Systems | |||

| Risk and Compliance Systems | |||

| Ancillary Systems (CRM, Treasury, HR) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Banking Maintenance Support and Services market today?

The market stood at USD 11.69 billion in 2026 and is on track to reach USD 15.68 billion by 2031.

Which service type attracts the most spending?

Corrective and incident management services held 34.58% of global revenue in 2025.

What is driving faster growth in cloud deployments?

Consumption-based pricing and elastic capacity needs are propelling cloud contracts at a 7.12% CAGR through 2031.

Why is Asia-Pacific growing the fastest?

Massive transaction volumes from systems such as Indias UPI and Chinas digital-yuan pilots are pushing demand for 24/7 support.

How are regulations influencing maintenance contracts?

Frameworks like the EUs DORA and Singapores TRM guidelines impose strict uptime and audit-trail requirements, prompting banks to sign premium SLAs with rapid incident-response times.

Are open-source platforms affecting vendor revenues?

Yes, community-supported cores such as Apache Fineract enable cost-conscious banks to cut annual maintenance fees, applying price pressure on proprietary vendors.

Page last updated on: