Data Center Managed Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 62.05 Billion |

| Market Size (2031) | USD 121.67 Billion |

| Growth Rate (2026 - 2031) | 14.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center Managed Services Market Analysis by Mordor Intelligence

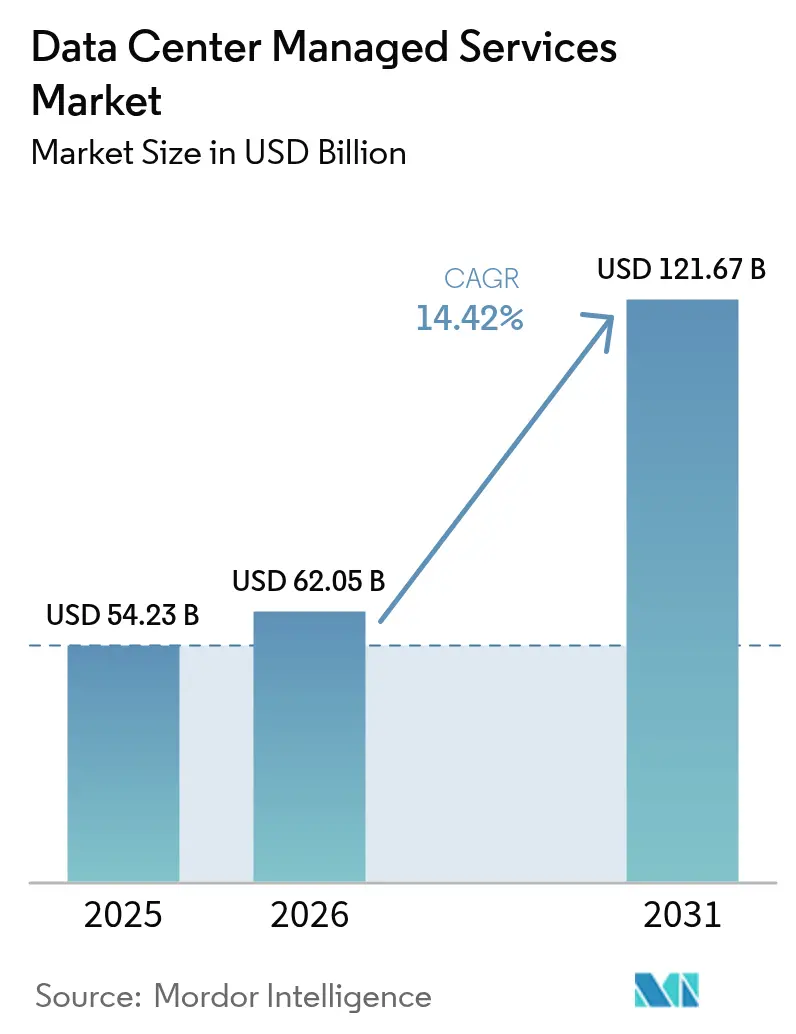

The data center managed services market size is expected to grow from USD 54.23 billion in 2025 to USD 62.05 billion in 2026 and is forecast to reach USD 121.67 billion by 2031 at 14.42% CAGR over 2026-2031. Rapid outsourcing of infrastructure complexity, escalating AI workload density, and the need to mitigate rising power constraints fuel this expansion. Enterprises are turning to managed service providers (MSPs) for cost-effective hybrid orchestration, compliance assurance, and round-the-clock operations coverage. Intensifying regulatory mandates, mounting sustainability targets, and widening skill gaps continue to steer budgets toward third-party operators. Competitive pressures are spurring strategic consolidation, deeper vertical specialization, and joint offerings with AI hardware vendors to sustain differentiation and margin resiliency.

Key Report Takeaways

- By service type, managed IT infrastructure led with 41.10% of data center managed services market share in 2025; managed security services are forecast to expand at a 15.52% CAGR through 2031.

- By deployment model, cloud deployments captured 62.30% of the data center managed services market in 2025, while hybrid architectures are advancing at a 15.21% CAGR to 2031.

- By data center type, colocation facilities accounted for 54.10% of the data center managed services market size in 2025; edge and micro data centers record the highest growth at 15.07% CAGR.

- By end-user industry, IT and telecommunications held 29.20% share of the data center managed services market in 2025, whereas healthcare is climbing fastest at a 15.12% CAGR.

- By geography, North America retained 41.20% share of the data center managed services market size in 2025, but Asia-Pacific is rising at a 15.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Center Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hyperscale-led colocation demand | +3.2% | Global, concentrated in North America, Asia-Pacific | Medium term (2-4 years) |

| Sustainability-linked SLA adoption | +1.8% | Europe, North America, Asia-Pacific tier-1 cities | Long term (≥ 4 years) |

| AI-driven predictive operations | +2.9% | Global, early adoption in North America, Europe | Short term (≤ 2 years) |

| Cloud cost-optimization outsourcing | +2.4% | North America, Europe, Asia-Pacific enterprise hubs | Medium term (2-4 years) |

| Edge data center roll-outs | +2.6% | Global, accelerated in Asia-Pacific, South America | Medium term (2-4 years) |

| Skill-gap outsourcing in operations and security | +2.1% | Global, acute in North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Hyperscale-Led Colocation Demand

Hyperscale operators secured more than 1,200 MW of colocation capacity in 2024 to circumvent the 24-to-36-month lead time of greenfield builds. Equinix reported 89% utilization across its global portfolio, while Digital Realty booked USD 1.2 billion in new contracts, underscoring urgency for immediately available space.[1]Equinix Inc., “Investor Relations,” equinix.com MSPs bundle remote operations, network optimization, and managed security into turnkey packages that reduce hyperscalers’ overhead and accelerate go-to-market cycles. The effect is pronounced in Asia-Pacific, where sovereign cloud mandates obligate partnerships with locally licensed providers.

AI-Driven Predictive Operations

AI-enabled monitoring platforms are lowering unplanned downtime by 30–40% through predictive failure analytics. IBM’s Maximo Application Suite trimmed mean-time-to-resolution by 35% in early data center rollouts during 2024, validating the economic case for AI-augmented operations.[2]IBM, “Maximo Application Suite,” ibm.com Providers that integrate telemetry from power, cooling, and network assets offer 15–20% premium SLA tiers, attracting enterprises seeking higher reliability without scaling head-count.

Edge Data Center Roll-Outs

Edge capacity is projected to triple between 2024 and 2028 as latency-sensitive retail, manufacturing, and telecom workloads shift closer to end users. Verizon extended its mobile edge footprint to 47 U.S. metros in 2024, enabling sub-10 millisecond round-trip performance for real-time analytics and AR training.[3]Verizon Business, “Mobile Edge Computing Solutions,” verizon.com MSPs are pivoting to hub-and-spoke management models that blend centralized AI orchestration with localized field support.

Sustainability-Linked SLA Adoption

Enterprises are now embedding carbon intensity requirements into contracts, demanding PUE figures below 1.3 and 75% renewable energy sourcing by 2027. Digital Realty earmarked USD 2 billion for renewable procurement and cooling upgrades, targeting carbon neutrality by 2030. Liquid cooling gains traction, reducing chiller energy by 20–30%, yet capital costs pose a challenge to mid-tier competitors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid capacity bottlenecks | -2.8% | North America (Northern Virginia, Phoenix), Europe (Frankfurt, Amsterdam), Asia-Pacific (Singapore) | Short term (≤ 2 years) |

| Vendor lock-in and repatriation risk | -1.9% | Global, acute in North America, Europe | Medium term (2-4 years) |

| Scarcity of specialist labor | -1.6% | Global, most severe in North America, Europe | Short term (≤ 2 years) |

| Heightened data-sovereignty rules | -1.4% | Europe (GDPR), China (PIPL), India (DPDPA) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Power-Grid Capacity Bottlenecks

Utility queues now stretch 18–36 months in Northern Virginia, Frankfurt, and Singapore. Dominion Energy flagged a 30-month interconnection backlog in 2024, forcing operators to evaluate secondary markets such as Ohio and Texas. AI clusters seeking contiguous 50–100 MW blocks feel the pinch most acutely, prompting some MSPs to add on-site gas turbines or fuel cells despite higher complexity.

Vendor Lock-In and Repatriation Risk

Cloud repatriation projects frequently overrun budgets by 2–3 times due to data egress fees and application refactoring. Enterprises therefore favor hybrid managed services that balance cost and control, yet rely on MSPs to orchestrate policies across on-premise, colocation, and public cloud estates. Maintaining dual infrastructure raises total cost of ownership but mitigates unilateral pricing shifts by hyperscalers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Outpace Infrastructure Management

Managed security services are registering a 15.52% CAGR to 2031, the fastest among all service layers. Zero-trust architecture mandates, with ransomware liabilities averaging USD 4.5 million per incident, and ISO 27001 adoption funnel budgets are directed toward continuous threat monitoring. Managed IT infrastructure still accounts for 41.10% of data center managed services market share, underscoring its role as the operational backbone.

Providers are expanding security operations centers to meet 24/7 coverage commitments while integrating immutable storage snapshots and AI-driven anomaly detection. The data center managed services market size for security services is poised to capture a larger share of enterprise spending as compliance penalties escalate. Mid-tier MSPs without in-house security expertise often pursue acquisitions to fill capability gaps, a trend that was mirrored by Rackspace’s 2024 deal, which broadened its managed detection and response portfolio.

By Deployment Model: Hybrid Architectures Gain Momentum

Cloud deployments captured 62.30% share in 2025, reflecting a decade of rapid migration; however, hybrid models are accelerating at a 15.21% CAGR. Enterprises see improved economics for predictable 24/7 workloads by retaining core compute on-premise while using cloud for burst capacity. Financial services institutions exemplify this balance, hosting transaction engines in compliant colocation cages and leveraging cloud analytics for customer-facing insights.

MSPs differentiate through orchestration layers that abstract infrastructure heterogeneity, enforcing uniform security and cost policies. The data center managed services market size tied to hybrid frameworks rises as sovereign data laws demand localized storage while maintaining global application responsiveness. Successful MSPs embed policy engines that trigger automated workload moves based on latency, cost, and compliance thresholds without service disruption.

By Data Center Type: Edge Facilities Challenge Colocation Dominance

Colocation remains dominant with 54.10% share, driven by hyperscalers leasing turnkey megawatt blocks. Yet edge and micro facilities are scaling at 15.07% CAGR as retail analytics, autonomous machinery, and mobile AR demand single-digit millisecond latency. Lumen added 120 U.S. edge data centers in 2024, underscoring the growth potential of distributed topologies.

The data center managed services market share held by edge deployments is widening as MSPs introduce hub-and-spoke control planes that push AI inference to local nodes while centralizing training workloads. Colocation leaders respond by pairing downtown interconnection hubs with suburban edge annexes, bundling single-contract managed services that span both tiers. Standardization hurdles persist due to vendor-specific hardware stacks, constraining economies of scale.

By End-User Industry: Healthcare Drives Fastest Expansion

The IT and telecommunications sectors still generate 29.20% of the 2025 revenue, while healthcare is accelerating at a 15.12% CAGR. Telehealth visits increased from 5% of U.S. consultations in 2019 to 38% in 2024, intensifying demand for HIPAA-compliant hosting and disaster recovery infrastructures. Electronic health record workloads require high-density storage, pushing providers to integrate GPU-powered analytics for imaging and diagnostics.

The data center managed services industry is expanding to include specialized healthcare business units staffed with HITRUST-certified personnel. BFSI, retail, and manufacturing also migrate critical systems to managed environments seeking 24/7 uptime guarantees and regulatory compliance. Energy, utilities, and government verticals emphasize operational technology convergence and air-gapped configurations, sustaining steady, though comparatively slower, uptake.

Geography Analysis

North America retained 41.20% share in 2025. Power constraints in Northern Virginia, Phoenix, and Silicon Valley push new capacity to Columbus, Dallas, and Atlanta, where utilities offer surplus load and land prices remain moderate. Canada leverages hydropower and cooler climates to attract latency-tolerant workloads, while Mexico hosts near-shore deployments targeting South America. A mature MSP ecosystem and deep enterprise outsourcing culture support continued regional leadership.

Asia-Pacific grows at a 15.14% CAGR to 2031, the fastest among regions. China’s Data Security Law and India’s Digital Personal Data Protection Act drive localized infrastructure mandates, boosting demand in Beijing, Mumbai, and Bangalore. Japan faces capacity challenges in Tokyo, shifting builds to Osaka. Singapore’s moratorium on new permits until 2027 channels investment to Malaysia and Indonesia. Sovereign cloud strategies and government subsidy programs underpin the region’s robust expansion.

Europe commands considerable revenue, anchored by Germany, the United Kingdom, and France. Frankfurt’s power backlog elongates approval cycles beyond 24 months. Brexit dynamics encourage dual-site footprints across EU and UK jurisdictions. Nordic countries offer 100% renewable grids and free cooling benefits, although added latency to central European populations limits adoption for real-time workloads. The Middle East, led by the United Arab Emirates and Saudi Arabia, invests heavily to diversify economies, while Africa’s progress remains uneven outside South Africa and Nigeria.

Regulatory Landscape

Regulation is tightening around sustainability reporting, data sovereignty, and security assurance, increasing the compliance burden for managed service providers (MSPs) and colocation partners. In the European Union, Commission Delegated Regulation (EU) 2024/1364 operationalizes energy-performance reporting for data centers, requiring operators at or above 500 kW IT power demand to report into a European database starting in September 2024 and on an annual cadence thereafter. Additional customer-facing energy performance indicator disclosure requirements apply to colocation and co-hosting operators by 15 May 2026, pushing MSPs to instrument energy, water, and utilization metrics across multi-tenant environments.

Security and sovereignty controls are also shaping service design and contracting. In the United States, federal-oriented managed services are aligning to evolving government security baselines, including OMB Memorandum M-25-04 (FY 2025 guidance on federal information security and privacy management requirements) and the FedRAMP Consolidated Rules for 2026, which raise expectations for continuous assessment and automation-friendly control evidence. In the Middle East, Dubai Electronic Security Center (part of Digital Dubai) rolled out Information Security Regulation (ISR) Version 3.0, adding data center security controls and restricting the processing of critical information outside the UAE, which increases demand for in-country operations, local staffing models, and tightly governed cross-border hybrid orchestration.

Value Chain Analysis

The value chain spans infrastructure OEMs (servers, networking, storage), power and thermal infrastructure suppliers (UPS, switchgear, cooling and liquid cooling), cloud and virtualization software, security tooling, connectivity and interconnection providers, and the systems integrators/MSPs that turn these components into design-build-operate and run-state service contracts. In this market, MSPs increasingly function as prime contractors and purchasing orchestrators for long-term managed operations, selecting hardware stacks, monitoring and AIOps platforms, and security controls, then binding them into SLAs across on-premise, colocation, and public cloud footprints.

Upstream constraints, particularly grid access and long-lead equipment, affect managed services scope and pricing. Supply-chain and delivery delays for critical equipment and multi-year power and interconnection timelines increase the value of providers that can secure capacity early or offer modular solutions. For example, SLB and Liberty Energy announced a July 2026 strategic alliance focused on modular infrastructure and integrated power generation for global data center projects. Downstream, partnerships that combine managed operations with governed AI platforms are gaining visibility among regulated buyers, including Rackspace Technology and Palantir Technologies launching a July 2026 operating framework that integrates Palantir Foundry and AIP with Rackspace managed operations for sovereign and regulated enterprise AI deployments.

Competitive Landscape

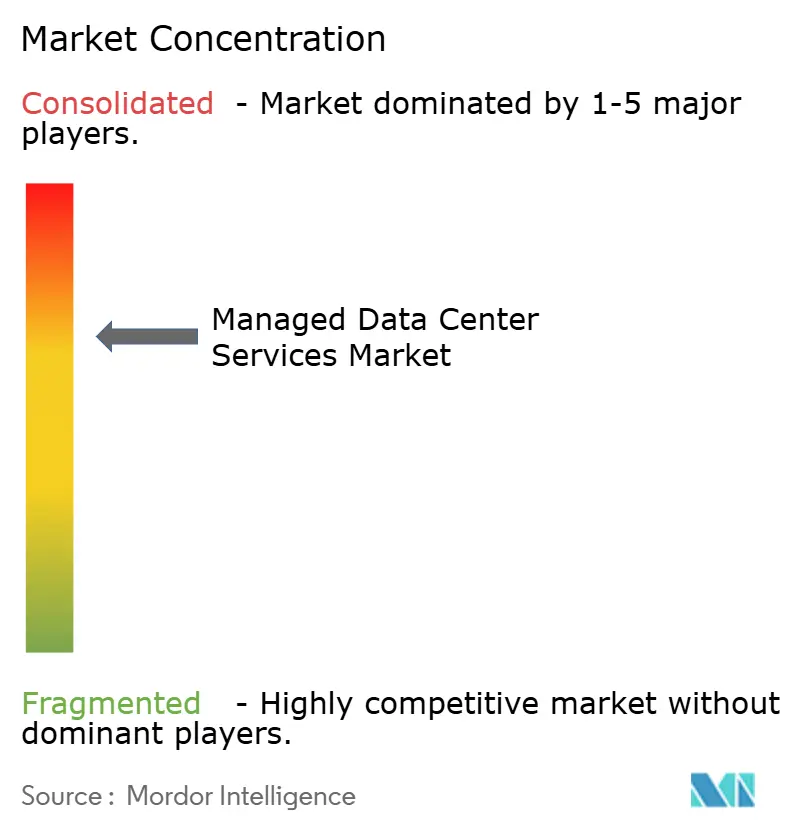

The data center managed services market features moderate fragmentation. The top 10 providers generate nearly half of the global revenue. Colocation leaders Equinix and Digital Realty expand up the stack, bundling security, network, and application management into single contracts. IT services majors IBM and NTT deepen infrastructure portfolios, merging application hosting with zero-trust security. Hyperscalers, such as Microsoft Azure and Alibaba Cloud, blur service lines by offering managed operations for hybrid environments, thereby intensifying price pressure.

Strategic alliances proliferate. Schneider Electric and NVIDIA formed a partnership in 2024 to support racks with thermal loads exceeding 100 kW. MSPs unable to finance specialized cooling or AI cluster orchestration face margin compression. Edge management emerges as white-space territory, with no clear leader yet able to manage thousands of micro-sites at scale. Acquisitions totaled 15 in 2024, reflecting consolidation as mid-tier firms seek scale or vertical depth.

Investment continues in AI-powered operations and sustainability differentiation. Providers deploying predictive maintenance platforms report churn rates 30% lower than peers still reliant on manual processes. Vertical specialization, particularly in healthcare and finance, secures premium pricing through compliance expertise. Operators with scale, renewable power commitments, and AI automation stand poised to capture outsized growth.

Data Center Managed Services Industry Leaders

Fujitsu Ltd

Cisco Systems Inc.

Dell EMC

IBM Corporation

AT&T Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AI-dense deployments and power constraints are shifting buyer priorities toward providers that can deliver end-to-end readiness, including high-density thermal management, faster access to power, and operating models that keep hybrid estates compliant across jurisdictions. Large-scale capacity programs and capital formation create room for MSPs to attach lifecycle services (design, migration, security operations, FinOps, and 24/7 facility and platform operations) to new builds and retrofits. This is supported by Meta's July 2026 announcement to expand its Hyperion campus in Richland Parish, Louisiana (raising total project investment to USD 50 billion and targeting 5 GW) and I Squared Capital's July 2026 agreement to acquire 10 data center facilities from Cogent Communications to form a new US operator platform.

Sovereign and regulated enterprise AI is also creating a more distinct managed-services lane that combines private infrastructure with governed data and model operations. Rackspace Technology's July 2026 operating framework with Palantir targets regulated enterprises seeking production-grade AI with tighter control over data locality, security evidence, and operational processes, reinforcing demand for managed services that go beyond infrastructure into policy-driven operations. In parallel, sustainability-linked SLAs and mandated energy-performance reporting in parts of Europe are increasing demand for instrumentation, reporting automation, and optimization services that connect facility telemetry to contract governance, particularly for colocation-heavy footprints where multiple customers require standardized indicator disclosure.

Recent Industry Developments

- July 2026: Rackspace Technology launched an operating framework with Palantir Technologies that integrates Palantir Foundry and AIP with Rackspace managed operations to help regulated enterprises move AI into production. The combined approach ties data and model governance to day-2 operations, strengthening managed services differentiation in sovereign and compliance-heavy environments.

- November 2025: Hewlett Packard Enterprise earmarked USD 650 million to extend its GreenLake managed services platform by deploying AI-ready infrastructure in eight data centers, including liquid-cooling designed for 200-kilowatt racks. The investment strengthens HPE's ability to attach managed operations to high-density AI deployments and supports hybrid delivery models where enterprises want predictable run-state costs.

- September 2024: Schneider Electric and NVIDIA formed a partnership to support data center racks with thermal loads exceeding 100 kW. The collaboration accelerates reference architectures for liquid-cooled, AI-dense infrastructure that MSPs and colocation operators can standardize around when delivering managed services for next-generation workloads.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers third-party services that run, monitor, secure, and optimize data center operations for customers. It includes IT infrastructure, network, security, storage and backup, and application hosting across cloud, on-premise, and hybrid setups.

Scope exclusions: We exclude customer-owned hardware capex, standalone software licensing, and pure connectivity services when they are sold without ongoing managed operations.

Segmentation Overview

- By Service Type

- Managed IT Infrastructure

- Managed Network Services

- Managed Security Services

- Managed Storage and Backup

- Managed Application Hosting

- By Deployment Model

- Cloud

- On-Premise

- Hybrid

- By Data Center Type

- Colocation Facilities

- Hyperscale-Owned Sites

- Enterprise On-Premise Sites

- Edge / Micro Data Centers

- By End-User Industry

- IT and Telecommunication

- BFSI

- Healthcare

- Retail and e-Commerce

- Manufacturing

- Government and Defense

- Energy and Utilities

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Mexico

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the outer guardrails for demand, pricing, and adoption. We pull consistent signals from public sources such as the U.S. Energy Information Administration for electricity pricing and reliability context, the International Energy Agency for efficiency and power-demand themes, the International Telecommunication Union for connectivity and traffic indicators, and the U.S. Bureau of Economic Analysis for IT services and cross-border services context.

We also review materials like public company annual reports, earnings call transcripts, and investor presentations from data center operators and service providers, followed by trade association releases and reputable press coverage to track contract terms and service bundling patterns. For quantitative checks, a paid subscription covering company financials and another covering patent and innovation activity are used selectively to confirm vendor exposure and service focus, and an import-export shipment-level database is referenced in limited cases to sanity-check infrastructure deployment momentum. The sources listed above are not exhaustive, and other public references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was used to pressure-test the model against real buying and delivery conditions. We spoke with managed service providers, colocation operators, enterprise IT teams, and channel partners across APAC, EMEA, and the Americas to confirm what is included in managed contracts, typical renewal cycles, and how spend is split across on-premise, cloud, and hybrid operations. When desk inputs showed wide ranges, especially for bundled monitoring, security, and backup, we tightened assumptions through follow-up checks so the sizing stays practical.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 21% | APAC: 45% |

| Mid tier: 50% | Functional/Unit leaders: 38% | EMEA: 33% |

| Smaller Players: 22% | Managers: 41% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing starts with a top-down demand pool build where regional data center activity is reconstructed and then filtered by the share of environments operated under managed service contracts. To keep totals grounded, we corroborate the outcome with selective bottom-up approximations, such as sampling typical monthly service fees, applying them to estimated managed footprints, and then running channel checks on pricing and attach rates.

Key inputs used in the model include data center capacity additions and utilization signals, workload migration intensity toward hybrid setups, security and compliance pressure that changes service scope, labor availability for 24x7 operations, and power and cooling constraints that push outsourcing decisions. Because pricing varies with what is bundled, we also track how often security, backup, and monitoring are packaged together to avoid double counting.

For forecasting, scenario analysis is applied around workload growth (including higher compute density) and outsourcing penetration by industry, and then the scenarios are blended into a central case. Assumptions are aligned to what practitioners expect for renewals, new builds, and price pass-through. Where bottom-up inputs are thin for smaller countries, we fill gaps using comparable-market ratios and then reconcile back to regional demand indicators.

Data Validation & Update Cycle

Outputs are triangulated through three lenses: demand signals, supply-side revenue exposure, and price-consistency checks across contract types. If a region shows an unusual jump, we re-check the drivers and follow up with primary contacts to confirm whether it came from a few large contracts, a pricing reset, or a change in what is being bundled.

Before sign-off, the model goes through multi-step review where assumptions, conversions, and split factors are checked by another analyst and then reconciled to the narrative. Reports are refreshed annually, with interim updates when material events occur, such as regulation changes, large capacity additions, or sharp power-price moves. Before delivery, an analyst completes a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Data Center Managed Services Market Estimate Compared With Other Published Estimates

Published market sizes for data center managed services often do not match because the service scope is not set the same way, and because pricing and contract bundling are treated differently. Differences also come from the base year chosen, how currency conversion timing is handled, and how frequently assumptions are refreshed.

Some estimates use a broader outsourced data center services framing that blends managed operations with adjacent hosting or facility-linked charges. For Mordor Intelligence, the market is counted only when there is an ongoing managed service layer for running, monitoring, securing, and optimizing data center environments, which helps prevent one-time build work and pure facility charges from inflating the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 54.23 B (2025) | |

| Global Consultancy A | USD 60.18 B (2025) | Uses an outsourced services framing with limited clarity on separating managed operations from bundled hosting or facility-linked charges, which can lift the starting value. |

| Industry Research House B | USD 57.63 B (2023) | Reports an absolute growth-add figure over a forecast window and anchors on a different base year, so converting it into a comparable 2025 size depends heavily on implied starting levels and timing assumptions. |

The spread across publishers is mainly explained by what gets included in a managed services total and by the year referenced, and then by how bundled pricing is converted into clean service revenue. By tying the model to repeatable demand indicators and applying clear inclusion rules, the final number stays transparent and easier to validate in planning discussions.

Key Questions Answered in the Report

What is the current size of the data center managed services market?

The market stands at USD 62.05 billion in 2026.

How fast is the market expected to grow by 2031?

It is projected to reach USD 121.67 billion, registering a 14.42% CAGR from 2026 to 2031.

Which service type is expanding the quickest?

Managed security services are rising at a 15.52% CAGR on the back of zero-trust mandates and ransomware threats.

Which region shows the fastest future growth?

Asia-Pacific leads with a forecast 15.14% CAGR driven by sovereign cloud policies and hyperscale investments.

Why are hybrid deployment models gaining favor?

Enterprises seek cost savings, latency control, and sovereignty compliance by balancing on-premise and cloud resources.

Page last updated on: