Magnetic Beads Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.91 Billion |

| Market Size (2030) | USD 5.29 Billion |

| Growth Rate (2025 - 2030) | 12.73% CAGR |

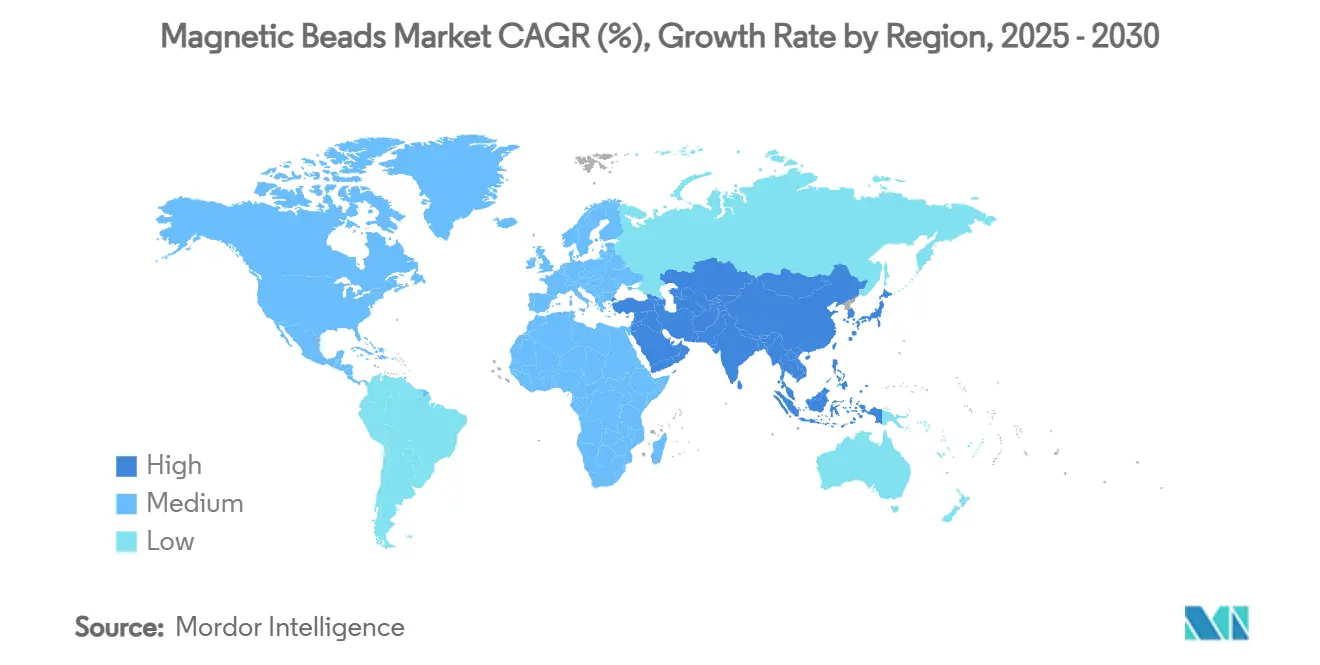

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

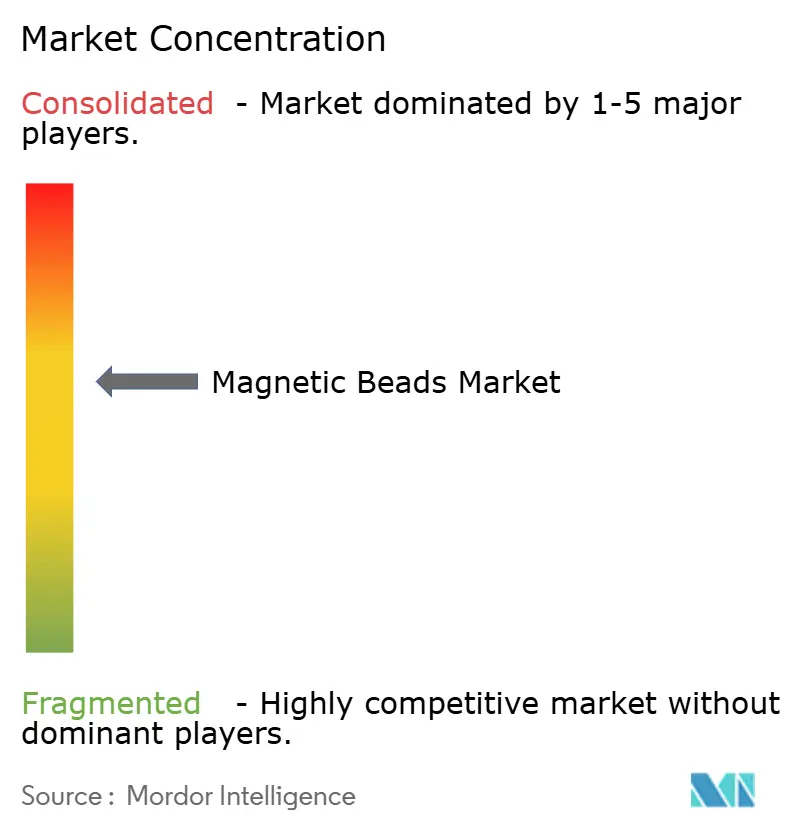

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Magnetic Beads Market Analysis by Mordor Intelligence

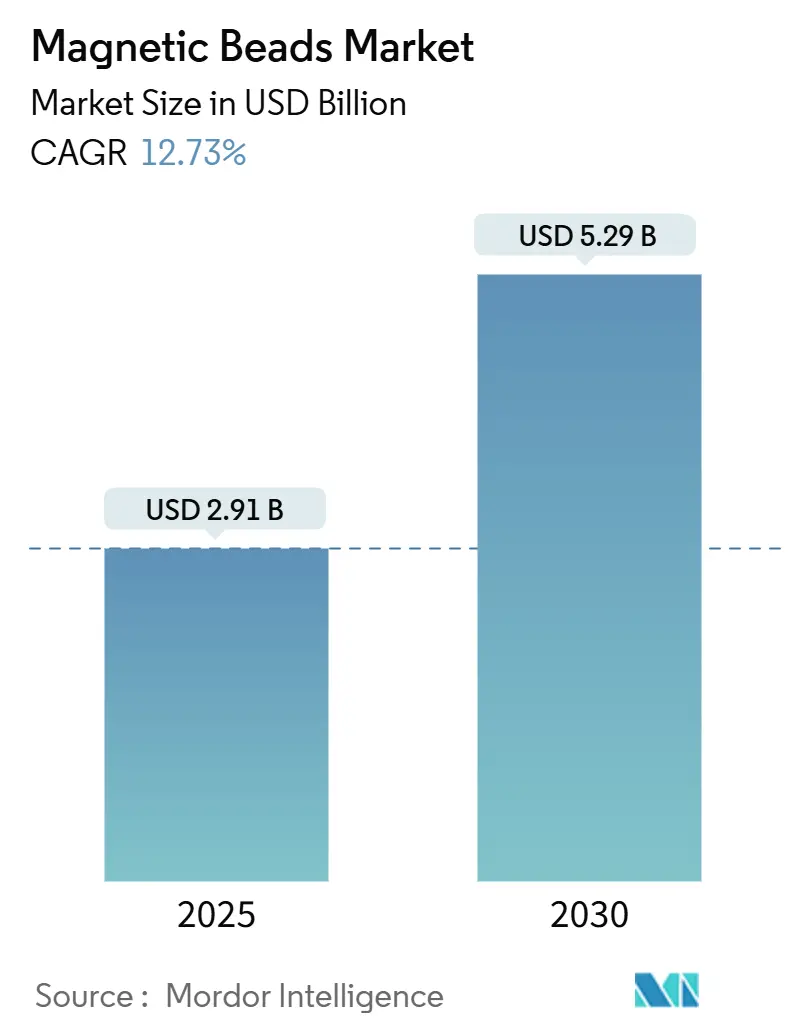

The Magnetic Beads Market size is estimated at USD 2.91 billion in 2025, and is expected to reach USD 5.29 billion by 2030, at a CAGR of 12.73% during the forecast period (2025-2030).

Rising automation in molecular diagnostics, the growing need for streamlined mRNA vaccine purification, and the shift toward magnetic-activated cell sorting in cell and gene therapy production continue to fuel demand. The convergence of high-throughput proteomics, point-of-care diagnostic expansion, and reusable low-gradient magnetic separators is widening the technology’s footprint across research and manufacturing workflows. Major suppliers are responding with surface-chemistry innovations that improve binding specificity, while buyers focus on platforms that cut hands-on time and reduce plastic use. Competitive activity remains intense: top vendors deploy acquisition strategies to secure core technologies and strengthen regulatory readiness. Regions with pro-innovation rules and large installed bases of laboratory automation equipment account for the highest near-term revenue pools, yet future growth pivots on emerging Asian manufacturing hubs building domestic bioprocess capacity.

Key Report Takeaways

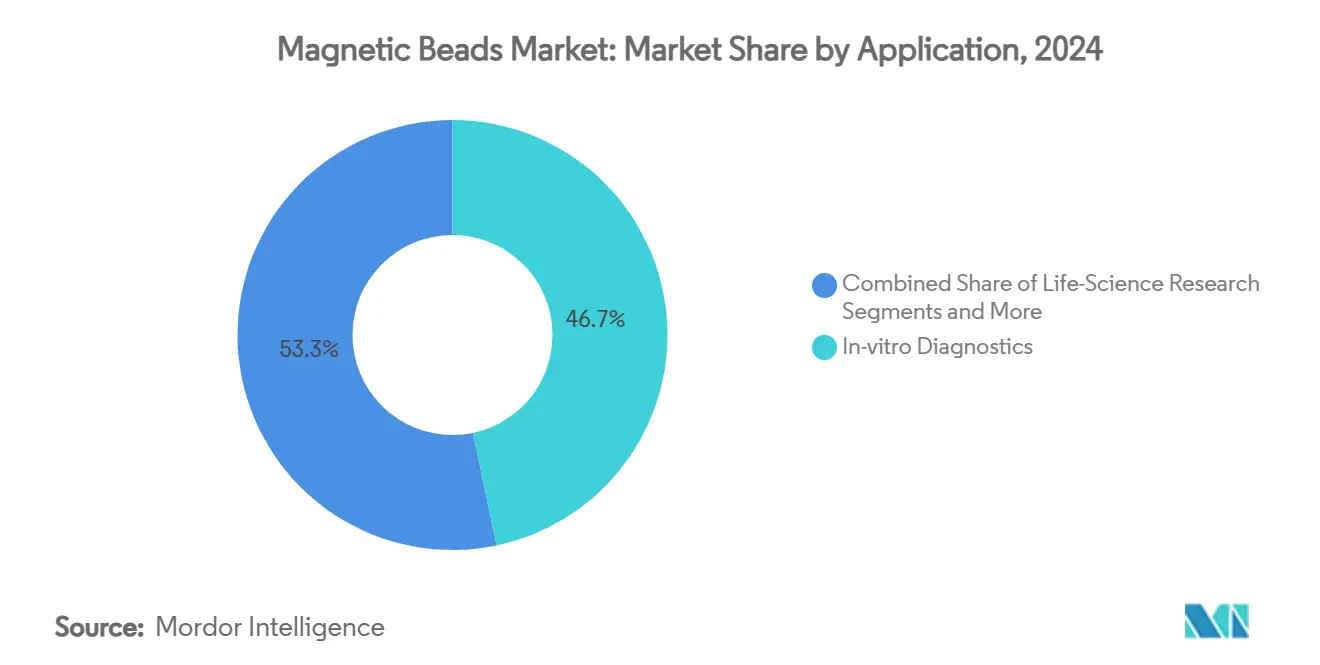

- By application, in-vitro diagnostics led with 46.72% revenue share in 2024 and cell separation and therapy is projected to advance at a 15.34% CAGR through 2030.

- By magnetic core material, iron oxide captured 68.79% of the magnetic beads market share in 2024, while cobalt ferrite is set to grow at a 16.23% CAGR to 2030.

- By surface chemistry, silica-coated beads accounted for 31.25% of the magnetic beads market size in 2024 and streptavidin/biotinylated coatings are expanding at a 15.79% CAGR during the same horizon.

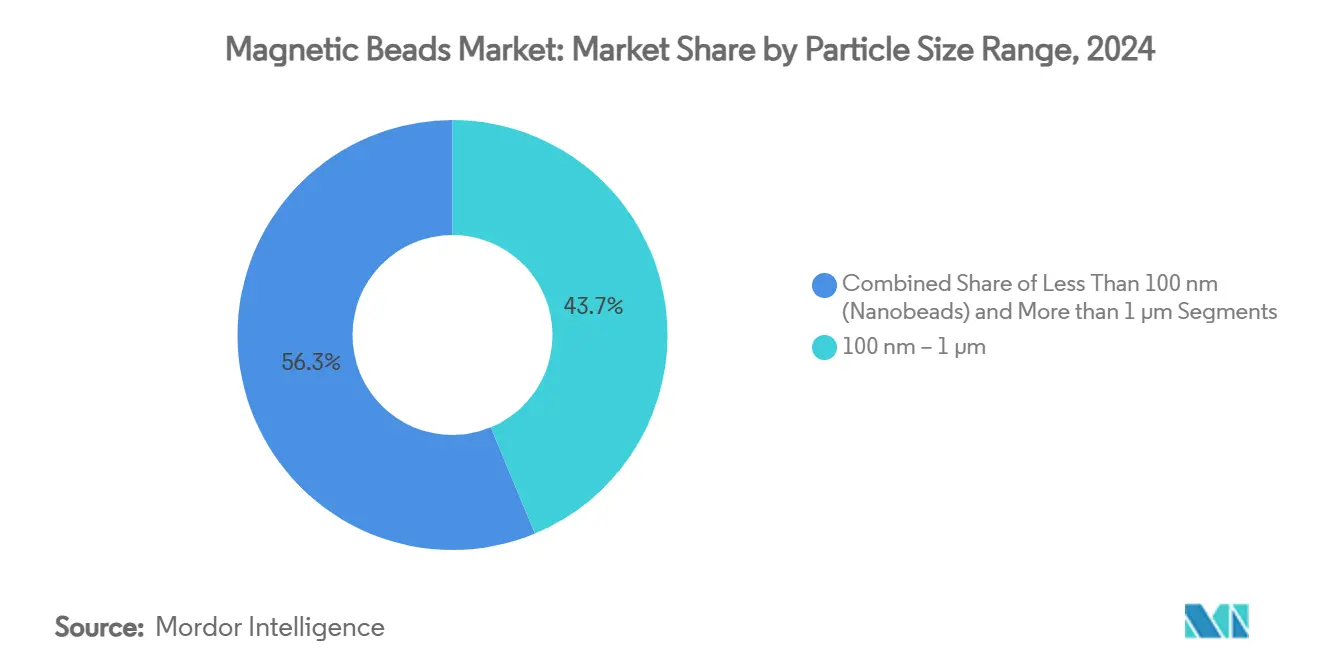

- By particle size, the 100 nm–1 µm range represented 43.74% of 2024 revenues and sub-100 nm nanobeads are forecast to post a 16.61% CAGR through 2030.

- By end user, pharmaceutical and biotechnology companies held 36.42% of the magnetic beads market 2024 sales and contract research organizations are tracking a 14.64% CAGR to 2030.

- By geography, North America dominated with 39.81% revenue share in 2024, whereas Asia-Pacific is on course for a 14.43% CAGR up to 2030.

Global Magnetic Beads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation-ready nucleic-acid extraction in molecular diagnostics | +2.1% | North America, Europe | Medium term (2-4 years) |

| Rapid adoption of magnetic-activated cell sorting in cell and gene therapy manufacturing | +2.8% | North America, Europe, emerging Asia | Long term (≥ 4 years) |

| Surging demand for high-throughput proteomics and interactomics research | +1.9% | Global, academic clusters | Medium term (2-4 years) |

| Mainstreaming of point-of-care IVD kits employing bead-based enrichment | +2.3% | Global, fastest in emerging markets | Short term (≤ 2 years) |

| Emergence of bead-assisted mRNA vaccine purification workflows | +1.7% | North America, Europe, technology transfer to Asia | Medium term (2-4 years) |

| Development of reusable low-gradient separators for bioprocess scale-up | +1.5% | Global manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automation-ready nucleic-acid extraction in molecular diagnostics

Automated magnetic bead protocols are replacing manual spin-column steps, letting laboratories process hundreds of respiratory, blood, or stool samples per shift while lowering contamination risk. Instruments launching through 2026 promise 192-sample batches that cut plastic use by half, supporting sustainability goals. Fully robotic “dark labs” already run 24/7 with almost no technologist intervention, helping hospitals cope with workforce shortages. Portable extraction modules powered by patented bead-stirring or smart-lid designs now deliver 12-sample viral RNA purification in under 10 minutes at the point of care. National regulators classify laboratory-developed molecular tests as medical devices, pushing manufacturers toward standardized, automation-friendly consumables.[1]U.S. Food and Drug Administration Staff, “Laboratory Developed Tests Regulatory Impact Analysis (Final Rule),” Food and Drug Administration, fda.gov The combined effect is sustained equipment refresh cycles and growing reagent pull-through across the magnetic beads market.

Rapid adoption of magnetic-activated cell sorting in cell and gene therapy manufacturing

MACS has evolved from a benchtop research tool into a GMP-qualified workhorse for commercial-scale T-cell and stem-cell processi ng. Automated, traceless chromatography modules achieve 90% depletion of unwanted subsets without harming viability, meeting stringent release criteria for autologous CAR-T batches.[2]Sabine Radisch et al., “Next Generation Automated Traceless Cell Chromatography Platform for GMP-Compliant Cell Isolation and Activation,” Nature Scientific Reports, nature.comNew detachable bead formats allow gentle removal before infusion, easing regulatory concerns over residual particles. Counter-flow systems that integrate magnetics with centrifugation deliver >90% cell recovery in washing steps, supporting continuous-flow operations. Vendors add AI-driven process-control algorithms that fine-tune magnetic field exposure in real time, boosting lot-to-lot consistency.[3]Niklas Bäckel et al., “Elaborating the Potential of Artificial Intelligence in Automated CAR-T Cell Manufacturing,” Frontiers in Molecular Medicine, frontiersin.org As more therapies move from pilot to commercial volumes, the magnetic beads market benefits from contracts tied to long-term cell-therapy production runs.

Surging demand for high-throughput proteomics and interactomics research

Mass-spectrometry-based proteomics has shifted from discovery science to large-cohort biomarker validation, demanding enrichment tools that can handle thousands of samples per week. Mag-Net technology speeds membrane-particle isolation, raising plasma proteome coverage while maintaining throughput. Multi-plex proximity assays merged into magnetic bead workflows now quantify 5,300 protein targets in one run, accelerating drug-target confirmation. Ultra-deep interactome methods combining bead capture with native gel fractionation map dynamic protein complexes at unprecedented depth. Isotopically barcoded nanobeads enable 18,000 simultaneous serological readouts, overcoming spectral overlap limits. These breakthroughs reinforce the magnetic beads market as a foundational enabler of next-generation proteomic pipelines that demand both scale and sensitivity.

Mainstreaming of point-of-care IVD kits employing bead-based enrichment

Emergency rooms and field clinics now run rapid nucleic-acid tests without central labs. Portable devices integrate dropper-based sampling with bead-mediated pathogen lysis and cleanup, reading results inside 30 minutes. Corporate investments worth EUR 111 million bring microfluidic bead-chips that deliver high-sensitivity troponin results from whole blood, speeding heart-attack triage. Dual-membrane cartridges coupled to magnetic capture detect hepatitis C in 16 minutes, meeting global hepatitis-elimination targets RSC.ORG. Power-free extraction units achieve >94% sensitivity for monkeypox in rural clinics. Finger-prick bead assays that recognize stroke biomarkers within 15 minutes aim to improve decision times in ambulances. The expanding installed base of such platforms secures recurring reagent demand for the magnetic beads market.

Restraints Impact Analysis*

| Restraint | (~) ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Batch-to-batch variability of bead surface chemistry | -1.8% | Global high-volume manufacturers | Medium term (2-4 years) |

| Price premium over chromatographic resins in large-volume bioprocessing | -1.2% | Cost-sensitive emerging markets | Long term (≥ 4 years) |

| Regulatory uncertainty for bead carry-over in cell therapies | -0.9% | North America, Europe | Short term (≤ 2 years) |

| Supply-risk of high-purity iron-oxide feedstock | -1.1% | Asian manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Batch-to-batch variability of bead surface chemistry

Large therapeutic campaigns depend on consistent ligand density and low nonspecific binding. Controlled hydroxylation and silica interlayers raise functional-group homogeneity, yet minor deviations can alter capture efficiency by double-digit percentages. Leading brands point to proprietary polymer coatings and stringent process analytics as differentiators. Vendors now supply certificates detailing hydrodynamic size, zeta potential, and TEM imagery for every lot, a practice soon expected to become mandatory in regulatory filings. Magnetic separator tuning helps offset variability, but operators still devote extra QC cycles, lifting operating costs and tempering short-term orders within the magnetic beads market.

Price premium over chromatographic resins in large-volume bioprocessing

Magnetic consumables often cost 3-5 times more per litre of slurry than legacy resins when deployed at kilogram protein scales. While single-use magnetic routines offer labor savings, finance teams in emerging-market facilities focus on direct material cost. Suppliers counter by demonstrating lower buffer usage and shorter campaigns that shrink facility footprint, yet adoption slows when capital budgets tighten. Progressive price erosion and bead-recycling protocols should narrow the differential over the forecast horizon, but sticker shock remains a drag on uptake in cost-driven segments of the magnetic beads market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Diagnostics anchor current demand

The in-vitro diagnostics segment generated 4 6.72% of the magnetic beads market revenues in 2024, underlining the clinical community’s reliance on bead-based enrichment for automated molecular panels. Hospital labs adopt 96-well magnetic robots that process swabs, blood, and stool samples with minimal hands-on time. Pathogen surveillance programs order bulk bead kits to support respiratory-virus testing surges. The magnetic beads market size for cell separation and therapy is projected to grow at 15.34% CAGR through 2030 as CAR-T production, NK-cell pipelines, and mesenchymal-stem-cell platforms scale. Combined, diagnostics and cell-therapy workflows secure recurring consumable demand that buffers cyclicality in research budgets. Niche verticals such as environmental testing gain visibility through compact bead-based analyzers assessing food safety and water quality for pathogens, pesticides, or heavy metals.

A rapid embrace of decentralized testing pushes diagnostics further ahead. Mobile labs, cruise ships, and sports venues deploy all-in-one bead-cartridge modules that return qPCR results in under an hour. Emergency-department throughput improvements attract procurement managers, reinforcing long-term commitments to magnetic consumables. Simultaneously, cell-therapy facilities integrate traceless bead systems into closed automated lines. Faster vein-to-vein timelines secure reimbursement and draw venture funding, which accelerates order flow into the magnetic beads market.

By Magnetic Core Material: Iron oxide dominance challenged

Iron oxide accounted for 68.79% of 2024 shipments thanks to its established regulatory track record and abundance of safety data. Multi-modal production routes, including co-precipitation and thermal decomposition, give manufacturers flexibility to tailor particle sizes from 20 nm to 1 µm. Stringent process controls ensure superparamagnetism and narrow size distributions suited to DNA binding or antibody capture. The magnetic beads market size linked to cobalt ferrite is forecast to grow at a 16.23% CAGR to 2030 because higher magnetic moments cut separation times, which appeals to high-throughput facilities. Nickel ferrite finds traction where elevated chemical resistance offsets slightly lower magnetic responsiveness. Research teams also explore composite core-shell particles that balance biocompatibility with signal amplification for diagnostic imaging, hinting at diversification beyond traditional iron-oxide supply chains and expanding the magnetic beads market footprint.

Ongoing iron-oxide feedstock constraints could spur adoption of high-moment alternatives. Lifecycle-assessment studies rate cobalt ferrite beads favorably when recycling offsets initial mining impacts. End users weigh these benefits against the need for fresh toxicology packages. If cobalt-based formats achieve parity on regulatory clarity, iron-oxide’s commanding share may erode faster than current projections, reshaping competitive positions within the magnetic beads market.

By Surface Chemistry: Functionalization drives specificity

Silica-coated beads delivered 31.25% of the magnetic beads market sales in 2024 because their silanol groups bind nucleic acids under chaotropic conditions, enabling repeatable DNA and RNA extraction. Carboxyl-functionalized particles succeed in antibody purification workflows where ionic interactions dominate. Streptavidin/biotinylated formats display the steepest curve, registering a 15.79% CAGR through 2030 as proteomics labs seek attomole-level pull-down specificity. Custom conjugation services that attach antibodies, proteins, or oligonucleotides are proliferating. Vendors guarantee ligand densities and supply comprehensive CoAs, soothing QC managers’ concerns over lot variability. The magnetic beads market thus shifts from commodity cores to differentiated surface chemistries that can command premium pricing.

As research dives deeper into cross-linking mass spectrometry, enrichable cros s-linkers anchored on magnetic beads emerge. These pairs stabilize transient protein interactions, enabling mass-spectrometric detection of low-abundance complexes. Robust functionalization that withstands organic solvents and elevated temperatures becomes critical, opening white-space for novel chemistries.

By Particle Size Range: Nanobead innovation accelerates

Particles in the 100 nm–1 µm band remained the workhorse, delivering 43.74% of 2024 revenue because they strike a balance between magnetic pull strength and surface-to-volume ratio. Yet sub-100 nm nanobeads post the highest 16.61% CAGR to 2030, supported by column-free T-cell isolation and intracellular delivery trials. Smaller beads disperse uniformly, resist sedimentation, and leave minimal process residue, meeting rising purity requirements in cell therapies. Equipment makers release agitation systems optimized for low-Stokes nanoparticles to avoid aggregation under magnetic fields. Conversely, micro-scale beads (>1 µm) stay relevant in crude-lysate clarification where rapid settling outranks gentle processing.

Expanded use of finite-element modeling helps predict chain formation and separation kinetics for each size tier, informing scale-up decisions. This data-driven approach accelerates customization, reinforcing customer loyalty as suppliers tailor bead sizes to unique unit operations across the magnetic beads market.

By End User: Pharmaceutical companies lead adoption

Pharmaceutical and biotechnology companies absorbed 36.42% of the magnetic beads market demand in 2024, compelled by large-molecule pipelines and accelerating cell-therapy launches. Automated magnetic workstations tighten batch consistency, easing regulatory submissions. Contract research organizations represent the fastest-growing buyer pool at 14.64% CAGR to 2030 as sponsors outsource process development and specialty analytics. Diagnostic laboratories, facing staff shortages, invest in walk-away magnetic robots that cut turnaround time by half. Academia continues to seed future expansion through discovery research, often supported by grant-funded core facilities that purchase high-spec bead variants. Collectively, these segments uphold a broad user base, cushioning the magnetic beads market against downturns in any single vertical.

Pharma’s sustained capital expenditure signals durable demand: a EUR 300 million antibody and mRNA research center coming online in 2027 underpins multi-year supply contracts. Meanwhile, midsize CROs bundle bead-based purification with analytical services, expanding addressable consumption. As the diversity of operating environments widens—from hospital cleanrooms to field-deployable kits—suppliers tailor packaging, sterility, and shelf-life attributes, deepening penetration across each end-user niche.

Geography Analysis

North America generated 39.81% of 2024 revenue on the back of rigorous FDA oversight that favors validated, automation-ready consumables. Hospitals modernize core labs with dark-lab architectures that rely on magnetic workflows to keep instruments running round-the-clock. A newly built biologics resin plant creating 150 skilled jobs strengthens regional supply resilience for bead and resin inputs. Mergers worth more than USD 7 billion consolidate technology portfolios, making it easier for integrated vendors to cross-sell beads alongside purification resins and downstream filters. Artificial intelligence modules embedded in automated CAR-T suites push the envelope of closed, magnet-based cell-processing lines. Collectively, these dynamics should keep the magnetic beads market expanding, albeit at a mature growth clip compared with emerging regions.

Asia-Pacific is the standout growth engine with a 14.43% CAGR expected through 2030. A EUR 300 million bioprocessing hub under construction in South Korea illustrates the region’s intent to localize high-value consumable manufacturing. India eyes opportunities created by US trade restrictions on certain Chinese biotech firms, with contract manufacturers adding magnetic bead purification capabilities to win global outsourcing business. Grants that support leukemia and lymphoma testing in Kenya reveal how bead-based diagnostics permeate lower-income settings, expanding total addressable demand. Collectively, rising R&D spending, expanding biomanufacturing capacity, and localized production underpin the region’s rapid ascent in the magnetic beads market.

Europe posts steady mid-single-digit gains anchored by collaborative research consortia funded through Horizon Europe. A 22-institution extracellular-vesicle project drives bead consumption for vesicle isolation assays. Completion of a large bioprocess merger stitches together upstream and downstream assets, facilitating bundled procurement deals for EU CDMOs. Academic-industry partnerships, such as isotopically barcoded bead development at leading universities, ensure a pipeline of high-value applications feeding regional demand. Despite tighter capital budgets in parts of the bloc, commitment to mRNA infrastructure and green biomanufacturing keeps the magnetic beads market trajectory positive.

Competitive Landscape

Strategic consolidation shapes the competitive order. A USD 7.5 billion merger combined complementary portfolios spanning filtration, chromatography, and magnetic separation, giving the new entity full-line leverage when negotiating with biopharma customers. Thermo Fisher cemented leadership by closing a USD 3.1 billion proteomics acquisition in 2024 and announcing a USD 4.1 billion purification-and-filtration deal slated for completion by end-2025, further integrating bead solutions with analytics, columns, and single-use hardware. Mid-tier specialists pursue tuck-ins: a USD 10 million buy delivers dye-encapsulating magnetic beads that expand multi-plex assay menus, while chromatography innovators are snapped up to bolt on advanced resin know-how.

Technology differentiation gravitates to surface-chemistry innovations, AI-powered process control, and compatibility with closed, automated manufacturing lines. Firms stipulate in-house production of base nanoparticles to ensure tight particle-size distributions, fortifying quality claims. Patent filings surge in microrobot-guided magnetic devices for minimally invasive medicine, hinting at adjacency expansion. Start-ups leverage venture backing to advance true-nanoglue discovery engines, underscoring the appeal of magnetic motifs in drug-target modulation. Meanwhile, customers scrutinize sustainability credentials, pushing suppliers to certify recycled content and solvent-free production. The magnetic beads market thus balances scale advantages held by large incumbents with innovation hotbeds fostered by nimble newcomers.

Magnetic Beads Industry Leaders

-

Thermo Fisher Scientific Inc.

-

Merck KGaA

-

Danaher

-

Miltenyi Biotec

-

Promega Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion, aiming to broaden bioproduction offerings.

- February 2025: Magnet Biomedicine partnered with Eli Lilly in a USD 1.25 billion molecular-glue discovery collaboration that validates magnetic-inspired degrader platforms.

- December 2024: Quanterix closed a USD 10 million deal for EMISSION to secure proprietary dye-encapsulating magnetic beads for its ultra-sensitive Simoa assays.

Global Magnetic Beads Market Report Scope

| In-vitro Diagnostics |

| Life-Science Research |

| Cell Separation & Therapy |

| Drug Delivery & Therapeutics |

| Environmental & Food Testing |

| Others |

| Iron Oxide (Fe₃O₄ / Magnetite) |

| Cobalt Ferrite |

| Nickel Ferrite |

| Others |

| Silica-coated |

| Polystyrene-coated |

| Agarose-coated |

| Carboxyl-functionalized |

| Streptavidin / Biotinylated |

| Tosyl-activated |

| Others |

| <100 nm (Nanobeads) |

| 100 nm – 1 µm |

| >1 µm |

| Pharmaceutical & Biotechnology Companies |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Contract Research Organizations |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | In-vitro Diagnostics | |

| Life-Science Research | ||

| Cell Separation & Therapy | ||

| Drug Delivery & Therapeutics | ||

| Environmental & Food Testing | ||

| Others | ||

| By Magnetic Core Material | Iron Oxide (Fe₃O₄ / Magnetite) | |

| Cobalt Ferrite | ||

| Nickel Ferrite | ||

| Others | ||

| By Surface Chemistry / Coating | Silica-coated | |

| Polystyrene-coated | ||

| Agarose-coated | ||

| Carboxyl-functionalized | ||

| Streptavidin / Biotinylated | ||

| Tosyl-activated | ||

| Others | ||

| By Particle Size Range | <100 nm (Nanobeads) | |

| 100 nm – 1 µm | ||

| >1 µm | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Contract Research Organizations | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the magnetic beads market?

The magnetic beads market size reached USD 2.91 billion in 2025 and is projected to hit USD 5.29 billion by 2030.

2. Which application area generates the most revenue?

In-vitro diagnostics leads, accounting for 46.72% of 2024 global sales.

3. What segment is expanding the fastest?

Cell separation and therapy applications are forecast to grow at a 15.34% CAGR through 2030, propelled by automated CAR-T workflows.

4. Why are cobalt-ferrite beads gaining popularity?

Cobalt ferrite offers higher magnetic moments that shorten separation times, driving a 16.23% CAGR for this material class.

5. Which region will contribute most to future growth?

Asia-Pacific is expected to post a 14.43% CAGR through 2030 thanks to large bioprocess investments in South Korea, India, and other emerging hubs.

Page last updated on: