Pen Needles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

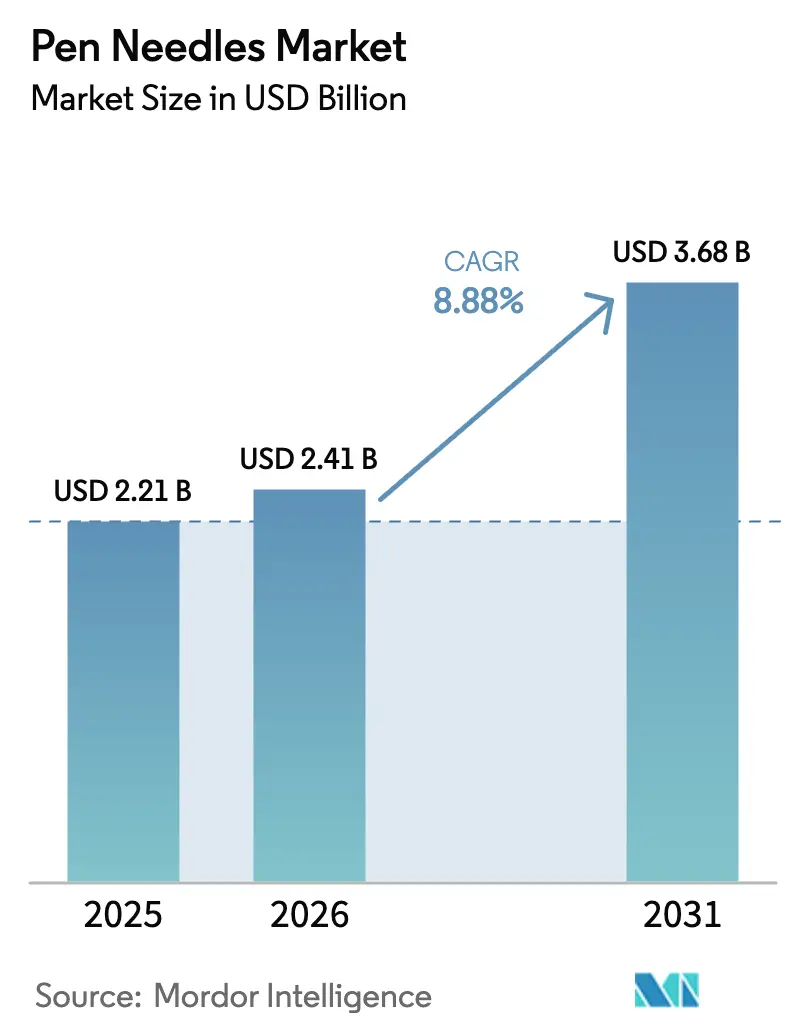

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.68 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pen Needles Market Analysis by Mordor Intelligence

The pen needles market size is expected to grow from USD 2.21 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 3.68 billion by 2031 at 8.88% CAGR over 2026-2031. Sharply rising diabetes prevalence, accelerating uptake of smart injection systems, and policy incentives that favor safety-engineered devices combine to keep demand on a firm upward path. Continuous glucose monitoring (CGM) connectivity built into next-generation smart pens is already reshaping purchasing criteria, as underscored by Medtronic’s FDA-cleared InPe app that interfaces with the Simpler CGM ecosystem [1]Medtronic plc, “Medtronic Launches InPen App with Simplera CGM Integration,” news.medtronic.com . North America stays dominant thanks to well-established reimbursement structures, while Asia-Pacific is growing faster as production-linked incentive programs lure contract manufacturers. Insulin therapy still accounts for most unit volumes, yet soaring demand for GLP-1 injectables used in weight-management programs is enlarging the total addressable base. Hospital groups and retail chains continue to bulk-buy standard needles, but procurement directives that prioritize needlestick-injury prevention are accelerating the shift toward safety variants.

Key Report Takeaways

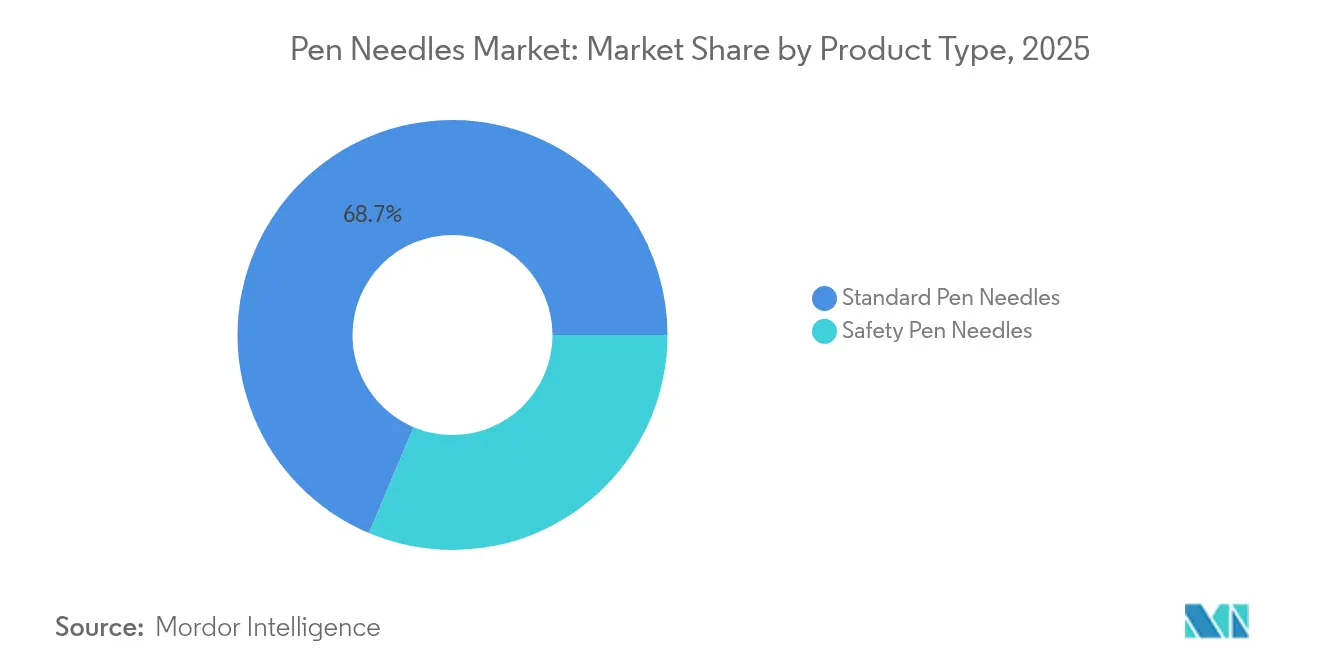

- By product type, standard designs led with a 68.65% revenue share in 2025, while safety models are projected to advance at a 10.12% CAGR through 2031.

- By application, insulin therapy accounted for 70.78% of the pen needles market share in 2025, whereas GLP-1 therapy is on track for the highest growth at 10.18% through 2031.

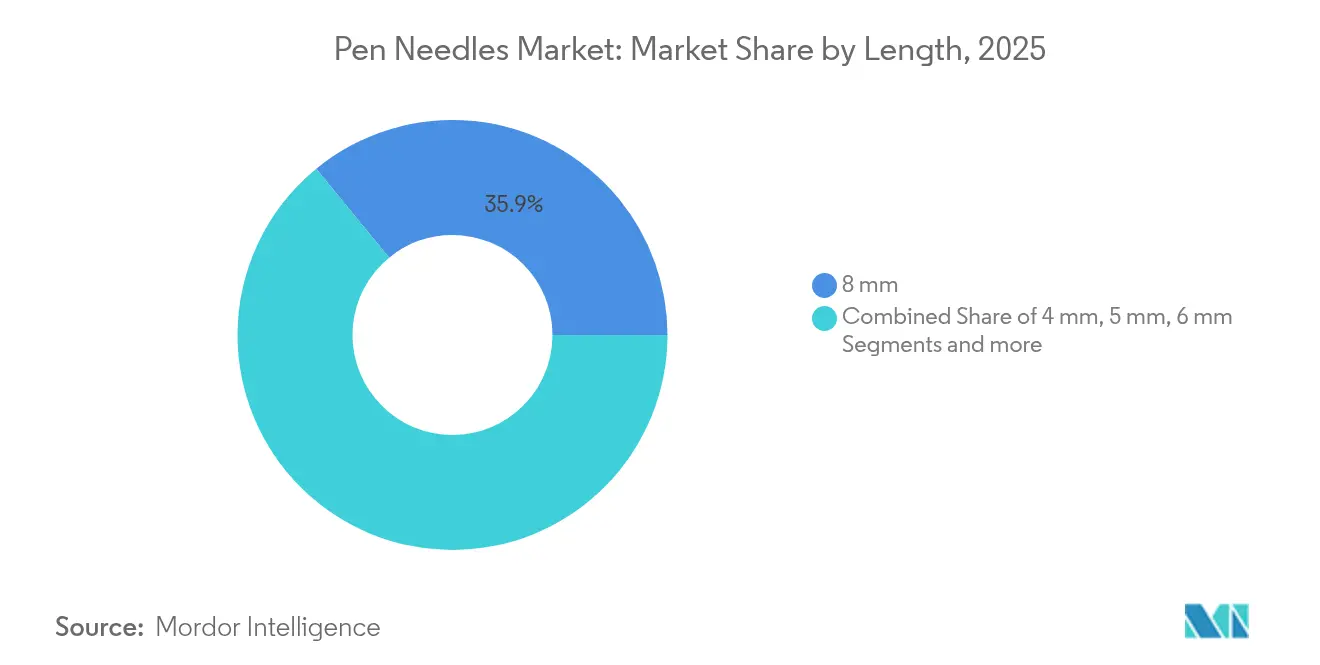

- By length, 8 mm formats commanded 35.92% of the pen needles market size in 2025; 4 mm formats are forecast to expand at a 10.19% CAGR during 2026-2031.

- By distribution channel, retail pharmacies held a 45.76% slice of the pen needles market in 2025, yet online pharmacies show the fastest rise at a 10.25% CAGR.

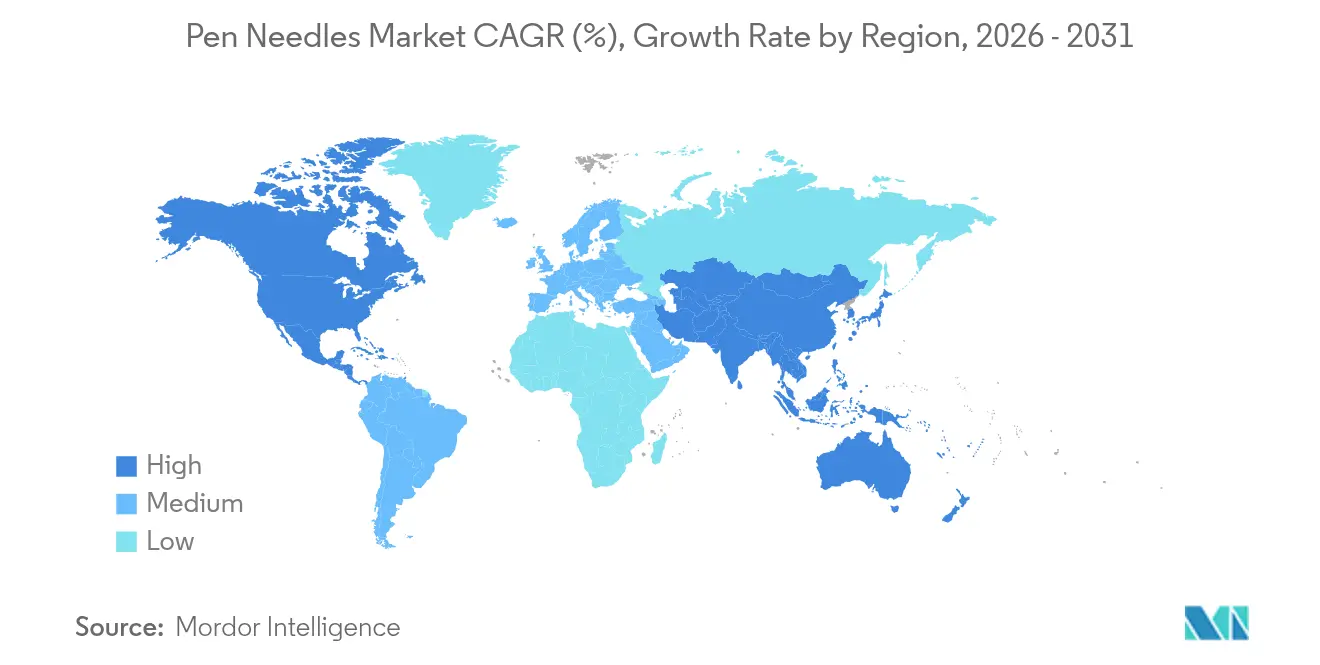

- By geography, North America retained 39.78% of global revenue in 2025, whereas Asia-Pacific is projected to grow the quickest at a 10.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pen Needles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes & obesity | +2.1% | Global, highest in North America & Asia-Pacific | Long term (≥ 4 years) |

| Declining insulin prices & improved reimbursement | +1.8% | North America & Europe, expanding to emerging markets | Medium term (2-4 years) |

| Shift toward safety pen needles | +1.5% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Miniaturised 32-34 G formats enabling smart pens | +1.3% | North America & Europe, APAC following | Short term (≤ 2 years) |

| At-home GLP-1 therapy boom | +1.7% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Localised manufacturing incentives | +1.1% | Asia-Pacific & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Obesity

Type 1 diagnoses in the United States climbed to 2.07 million in 2024 and are projected to reach 2.29 million by 2033, extending lifetime demand for injectable therapies [2]Rebecca Smith, “Prevalence Trends in Type 1 Diabetes,” Journal of Health Economics and Outcomes Research, jheor.org . Surging obesity rates reinforce this trend because pharmacologic weight-loss regimens rely on the same subcutaneous delivery mechanisms used for insulin. Brazil alone recorded sales exceeding BRL 3 billion (USD 589 million) of GLP-1 drugs between September 2023 and September 2024, underscoring how non-diabetes indications now fuel incremental needle demand. Collectively, these epidemiological forces underpin a multi-year expansion in the pen needles market.

Declining Insulin Prices & Improved Reimbursement

Price caps such as the USD 35 monthly insulin ceiling for Medicare beneficiaries have reduced economic barriers that previously suppressed optimal dosing frequency. Parallel price cuts by Novo Nordisk and Eli Lilly have magnified that accessibility effect, translating directly into higher needle throughput as patient rationing declines. Payers are further rewarding devices that demonstrate adherence improvements, giving connected pens a favorable reimbursement trajectory.

Shift Toward Safety Pen Needles

Hospitals and outpatient clinics face escalating liability costs linked to occupational needlestick injuries. Intermountain Healthcare cut its incidence rate from 1.78 to 0.88 per 10,000 injections after switching to safety designs, saving USD 24,875 in related costs. Similar outcomes are reported in multiple Asia-Pacific studies, prompting procurement teams to embed safety criteria into tenders. These economics are accelerating migration toward shielded and passive-retraction products.

Miniaturised 32–34 G Needles Enabling Smart Pens & CGM Integration

The latest smart pens rely on ultra-thin wall cannulas for reliable Bluetooth or NFC module fitment without enlarging device footprints. Novo Nordisk’s NovoPen 6 roll-out to NHS patients in 2025 exemplifies how 32 G needles serve dual goals of user comfort and sensor accommodation. Clinical societies now specify 4 mm length, 32 G gauge, five-facet tips as best practice, steering design road-maps worldwide [3]Giancarlo Tonolo, “Italian Consensus on Optimal Pen Needle Specifications,” MDPI, mdpi.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternate drug-delivery (pumps, patches) | -1.4% | North America & Europe, global expansion | Medium term (2-4 years) |

| High unit-price premium for safety variants | -0.9% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Needle reuse & infection risk | -0.7% | Global, highest in emerging markets | Medium term (2-4 years) |

| ESG pressure on single-use plastics | -0.5% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternate Drug-Delivery Systems

Insulin pumps already cover 78% of US type 1 patients, eroding some periodic needle demand. EU-funded projects such as BuBble Gun are prototyping needle-free micro-jet injectors aimed at commercial readiness by 2025. Should automated closed-loop platforms gain broad reimbursement, the pen needles market could cede share in intensive therapy settings.

High Unit-Price Premium for Safety Variants in Low-Income Nations

Where patients self-fund care, cost differentials curtail upgrades. Mexican households unable to access public-sector insulin pay USD 35–109 per vial, leaving scant budget for premium safety needles. Similar affordability gaps persist across parts of South Asia and sub-Saharan Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safety Innovation Drives Premium Segment Growth

Safety formats remain a minority by volume but grow the quickest, posting a 10.12% CAGR versus the mainstream standard segment’s lower trajectory. The United States FDA issued a Class 2 recall of one BD Nano batch in 2024 over labeling irregularities, highlighting the intensified regulatory oversight that favors certified safety designs. Many procurement contracts now stipulate integrated shields, ensuring repeat orders once conversions occur. Embecta capitalized on these trends when Meridian Health added its safety line to an exclusive Medicaid formulary that took effect in August 2025. Nonetheless, standard needles preserve incumbent status in price-sensitive tenders, keeping overall pen needles market diversity intact. Manufacturers are therefore embedding retractable features into legacy SKUs rather than running parallel lines, smoothing the upgrade path. Global production tooling is also shifting toward modular molds that can accommodate both shielded and unshielded variants, lowering switchover costs. The pen needles market consequently benefits from a natural replacement cycle as hospitals deplete old stock. In the long term, regulatory harmonization across the European Union and North America is set to make safety certification a de-facto requirement, positioning premium products for dominance.

Even with momentum on their side, safety brands must combat higher unit costs in emerging economies. Tender data from Southeast Asia show a price delta of up to 25% between shielded and unshielded SKUs, curbing uptake among under-funded public hospitals. Several Asian contract manufacturers have announced new ISO-13485-compliant lines dedicated to safety devices, aiming to close that gap through local scale. As a result, the pen needles market anticipates incremental margin compression but larger absolute revenue given stronger volume growth.

By Application: GLP-1 Therapy Disrupts Traditional Insulin Dominance

Insulin treatment continues to underpin 70.78% of sales, yet the highest growth belongs to GLP-1-based protocols for obesity and type 2 diabetes, which are escalating at a 10.18% CAGR. Investment bank TD Securities estimates the global GLP-1 drug category could top USD 139 billion in revenue by 2030, extending needle usage to tens of millions of new users. Unlike insulin—where pumps offer a substitution threat—GLP-1 injections often remain pen-delivered due to dosing frequency and viscosity constraints, reinforcing demand. Meanwhile, growth hormone applications, including once-weekly somapacitan pens, sustain a niche that benefits from high ASPs. Osteoporosis therapies such as daily teriparatide require precise dosing delivered via disposable pen systems containing 28 shots, guaranteeing steady base consumption. By widening disease coverage, these varied indications diversify revenue streams, insulating the pen needles market from single-therapy volatility.

For payers, therapy-wide adherence metrics are emerging as performance indicators, nudging formulary planners to pair medication approvals with proven delivery solutions. Smart-pen analytics reveal missed-dose patterns in both insulin and GLP-1 regimens, enabling targeted interventions. As digital dashboards become common, manufacturers that bundle connected needles with cloud platforms stand to capture premium contracts. The cross-pollination of diabetes tech and obesity-management programs therefore anchors long-term expansion in the pen needles market.

By Length: Shorter Needles Gain Traction Through Comfort Innovation

The 8 mm sub-segment still leads with 35.92% sales because clinicians have decades of familiarity with that depth. However, robust clinical evidence shows that 4 mm variants perform just as effectively while lowering intramuscular risk, and they are forecast to grow at 10.19% through 2031. Regulatory bodies in Europe and Japan already cite 4 mm designs in pediatric dosing guidelines, accelerating their mainstream acceptance. High-volume producers have retooled automated bevel-grinding machines to deliver five-facet geometry on ultra-short cannulas, ensuring flow rates stay within pharmacopoeial spec. This reengineering supports the wider move toward patient-centric design.

Longer needles nonetheless serve specific populations. People with higher BMI or cases requiring high-viscosity biologics still rely on 8 mm or even 10 mm lengths. BD’s partnership with Ypsomed to develop an 8 mm solution tailored for thick GLP-1 formulations illustrates the ongoing relevance of legacy sizes. Niche 5 mm and 6 mm categories are favored in select European markets where physician preference shapes prescribing habits. The coexistence of varied lengths underscores how customization sustains the pen needles market size even as comfort-driven innovation tilts the mix toward shorter formats.

By Distribution Channel: Online Pharmacies Capitalize on Digital Health Transformation

Retail outlets retained 45.76% distribution share in 2025 owing to immediate pick-up convenience and insurance integration. Yet online pharmacies, buoyed by telemedicine and subscription models, are accelerating at a 10.25% CAGR. Leading digital clinics now bundle medication, needles, and CGM sensors into auto-replenishment packs, increasing stickiness. During 2024, several top-five US tele-pharmacies reported triple-digit growth in pen-needle SKUs as weight-loss programs moved to virtual consults. Litigation initiated by Novo Nordisk against compounders of semaglutide underscores the regulatory tightrope digital sellers must walk, but it has not slowed legitimate volumes.

Hospital pharmacies continue to secure high-volume institutional contracts, although outpatient shifts are nudging chronic-care patients toward community collection points or home delivery. For manufacturers, multi-channel presence is now imperative: exclusive deals with integrated delivery networks secure baseline volumes, while direct-to-consumer portals capture incremental growth. As more health systems integrate pharmacy APIs into electronic health-record platforms, replenishment triggers linked to smart-pen usage data could further cement online pharmacy gains, adding structural momentum within the pen needles market.

Geography Analysis

North America led with 39.78% revenue in 2025. High disease prevalence, insurance coverage, and the early adoption of safety-engineered devices underpin that leadership. Nonetheless, technology substitution risk is rising: 78% of type 1 diabetes patients already use pumps, and closed-loop systems are gaining traction. Counterbalancing that threat is the rapid expansion of GLP-1 prescriptions for obesity; analysts project out-of-pocket spending on weight-loss drugs could surpass USD 100 billion annually, opening a new revenue vein for the pen needles market. Furthermore, the FDA’s 2024 alert over Chinese-sourced syringes prompted BD to raise domestic output by 2 billion units, strengthening local supply resilience.

Asia-Pacific is the fastest-advancing region with a 10.27% CAGR to 2031. India’s Production-Linked Incentive program, covering 26 approved device projects worth USD 147 million, exemplifies policy-led manufacturing acceleration. Multiple states are building dedicated medical-device parks, enabling localized needle production that trims logistics costs and import duties. In China, domestic suppliers are scaling 32 G cannula lines to compete globally, though FDA quality-system requirements remain a barrier. Regulatory alignment efforts underway in ASEAN are expected to shorten product-registration timelines, further spurring regional volume.

Europe posts steady single-digit growth supported by well-funded national health systems that mandate safety compliance. The NHS explores reusable alternatives under its circular-economy agenda, estimating potential yearly savings of USD 11 million. Such ESG considerations could temper disposable-needle demand, yet current guidelines still recommend single-use for biohazard control.

Latin America, led by Brazil, is emerging as a newly important supply node; Novo Nordisk’s USD 1.09 billion expansion in Minas Gerais will add GLP-1 vial and pen-fill capacity by 2026. Meanwhile, cost-constrained Middle East and African markets prioritize affordability, delaying broad safety-needle roll-outs but sustaining basic unit growth owing to rising diabetes incidence.

Competitive Landscape

The pen needles market remains moderately concentrated. BD, Novo Nordisk, and Terumo leverage vertically integrated supply chains spanning cannula drawing, pen filling, and global distribution. BD’s broad catalog covers standard and safety SKUs and now includes high-viscosity formats unveiled at Pharmapack 2025. Novo Nordisk enjoys locked-in device revenues tied to its proprietary insulin and GLP-1 franchises; the 2025 NHS release of NovoPen 6 reinforces sticky ecosystem economics. Terumo, combining needlemaking with infusion pump expertise, focuses on premium safety formats for acute-care settings.

Consolidation is under way in contract manufacturing. Gilde Healthcare combined EUROPIN and Acti-Med in 2024 to create a platform producing over 2 billion needles each year, giving pharmaceutical sponsors a European outsourcing alternative. Such scale backs smaller regional suppliers into either niche specialties or private-label roles.

Technology-driven entrants are testing needle-free delivery. NuGen Medical Devices signed multiple distributors for its InsuJet platform in 2024, targeting patients averse to injections. Medtronic, better known for insulin pumps, presses into the smart-pen field via the Simplera-enabled InPen app, blurring competitive lines with traditional needle vendors. Sustainability positions are also emerging: several European startups are prototyping compostable hubs and bio-based caps to pre-empt stricter waste rules. These developments collectively raise the innovation bar and intensify differentiation based on ecosystem value rather than pure unit cost.

Pen Needles Industry Leaders

Becton and Dickinson Company

Novo Nordisk A/S

B.Braun Melsungen AG

Terumo Corporation

Nipro Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novo Nordisk invested USD 1.09 billion to upgrade its Montes Claros, Brazil, site, adding aseptic lines for GLP-1 injectables and creating 600 jobs.

- January 2025: BD showcased Neopak XtraFlow glass pre-fillable syringes and iDFill identification tech for biologics at Pharmapack 2025.

- October 2024: Apollo announced the forthcoming Pro-Shield Duo safety pen needle featuring dual-end shielding, slated for early 2025 launch.

- August 2024: MedExel commercialized 33 G and 34 G pen needles, expanding ultra-fine offerings for sensitive patients.

Global Pen Needles Market Report Scope

As per the scope of this report, pen needles are disposable, sterile devices used with injection pens to deliver medications such as insulin. They are designed to provide precise dosing, minimize discomfort, and ensure safe administration for patients. The pen needles market is segmented by product type, application, length, distribution channel, and geography. The product type segment is further bifurcated into safety pen needles and standard pen needles. The application segment is segmented into growth hormone therapy, insulin therapy, glucagon-like peptide-1 therapy, osteoporosis, and other applications. The length segment is further segmented into 4mm, 5mm, 6mm, 8mm, 10mm, and others. The distribution channel segment is divided into hospital pharmacies, retail pharmacies, and others. The geography segment is divided into North America, Europe, Asia-Pacific, Middle East and Africa , and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

| Safety Pen Needles |

| Standard Pen Needles |

| Insulin Therapy |

| Growth-Hormone Therapy |

| GLP-1 Therapy |

| Osteoporosis |

| Other Applications |

| 4 mm |

| 5 mm |

| 6 mm |

| 8 mm |

| 10 mm |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Safety Pen Needles | |

| Standard Pen Needles | ||

| By Application | Insulin Therapy | |

| Growth-Hormone Therapy | ||

| GLP-1 Therapy | ||

| Osteoporosis | ||

| Other Applications | ||

| By Length | 4 mm | |

| 5 mm | ||

| 6 mm | ||

| 8 mm | ||

| 10 mm | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the pen needles market?

The pen needles market size stood at USD 2.41 billion in 2026 and is projected to reach USD 3.68 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 10.27% CAGR through 2031, driven by government production incentives and rising diabetes prevalence.

Why are safety pen needles gaining popularity?

Hospitals cut occupational needlestick injuries by more than 50% after switching to safety-engineered designs, creating clear cost-avoidance incentives for adoption.

How is GLP-1 therapy affecting demand?

Widespread use of GLP-1 injectables for weight management introduces millions of new users to pen-based delivery, making GLP-1 the fastest-growing application segment at 10.18% CAGR.

Do online pharmacies threaten traditional retail channels?

Online pharmacies are growing at 10.25% CAGR thanks to telehealth and subscription models, but retail outlets still provide nearly half of global sales, so multi-channel strategies remain essential.

Could pump technology shrink the pen needles market?

Insulin pumps already serve a large share of type 1 patients, yet expanding GLP-1 and other injectable therapies offset potential volume loss, keeping the overall market on a growth trajectory.

Page last updated on: