Maggot Debridement Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

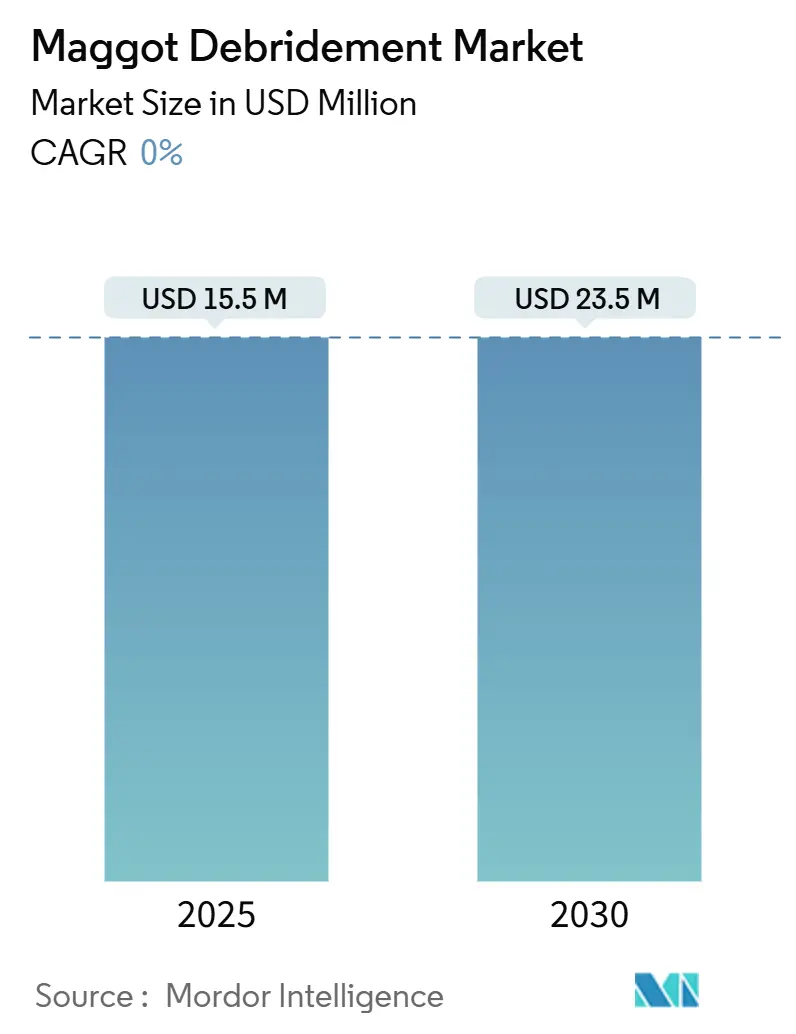

| Market Size (2025) | USD 15.5 Million |

| Market Size (2030) | USD 23.5 Million |

| Growth Rate (2025 - 2030) | 0.00% CAGR |

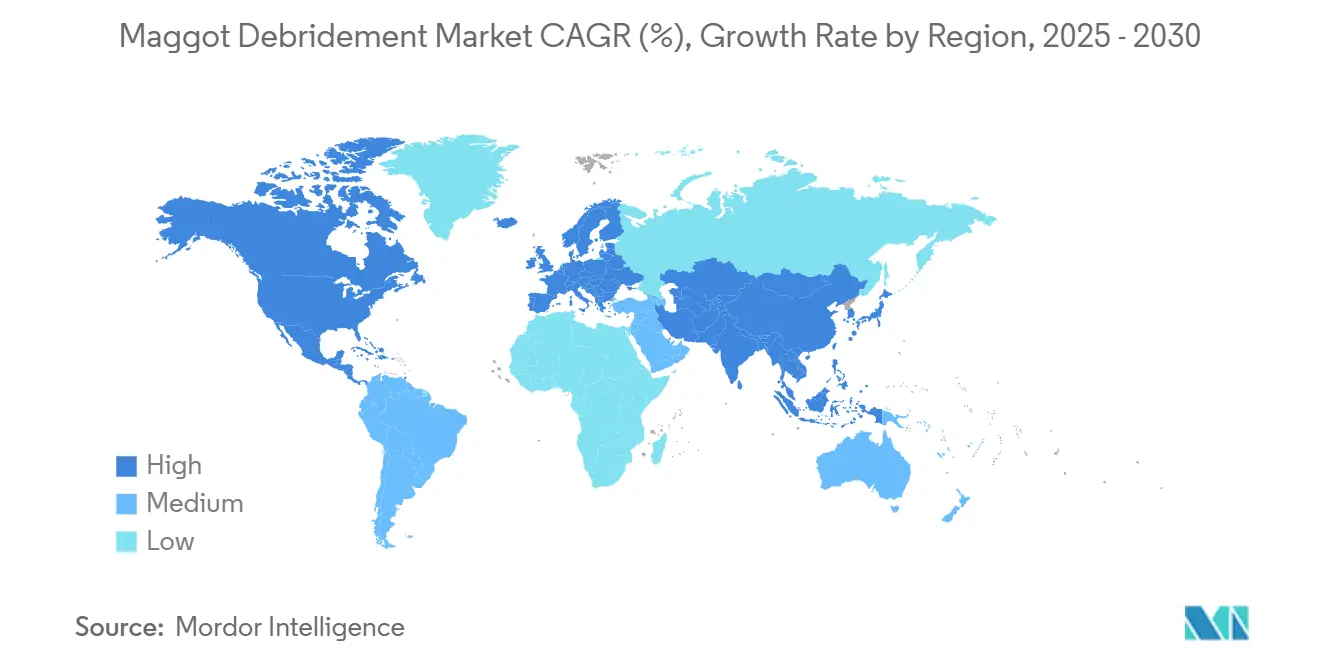

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maggot Debridement Market Analysis by Mordor Intelligence

The maggot debridement therapy market size stood at USD 15.5 million in 2025 and is on course to reach USD 23.5 million by 2030, reflecting a robust 8.6% CAGR over the forecast window. Rising antimicrobial resistance, clearer regulatory pathways, and payer acceptance have moved the therapy from a niche option to a mainstream component of advanced wound-care protocols. North America remains the revenue anchor thanks to well-established reimbursement, while Asia Pacific is expanding fastest as health-system investments broaden access. Contained larvae delivery systems, genetic engineering breakthroughs, and telehealth-enabled home applications are removing historical barriers, especially the long-standing “yuck factor.” Intensifying cost pressure across healthcare systems further tilts decision-makers toward a biological solution that frequently shortens healing time and reduces antibiotic courses. Competitive intensity is still low, yet pipeline activity points toward rising proprietary products, including enzyme-based gels that leverage maggot-derived compounds without using live insects.

Key Report Takeaways

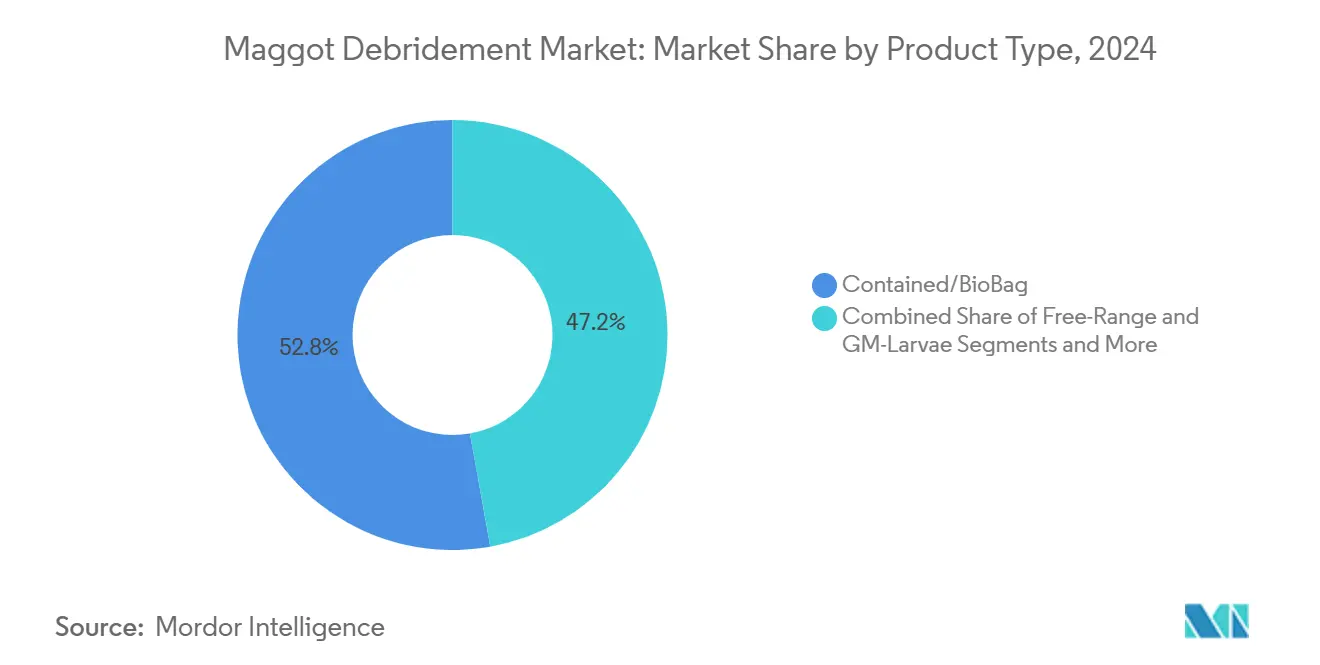

- By product type, contained larvae held 52.8% of the maggot debridement therapy market share in 2024; genetically-modified variants are projected to advance at 13.4% CAGR through 2030.

- By application, diabetic foot ulcers captured 38.2% share of the maggot debridement therapy market size in 2024, whereas oncology-related necrotic lesions are set to grow at 14.1% CAGR between 2025-2030.

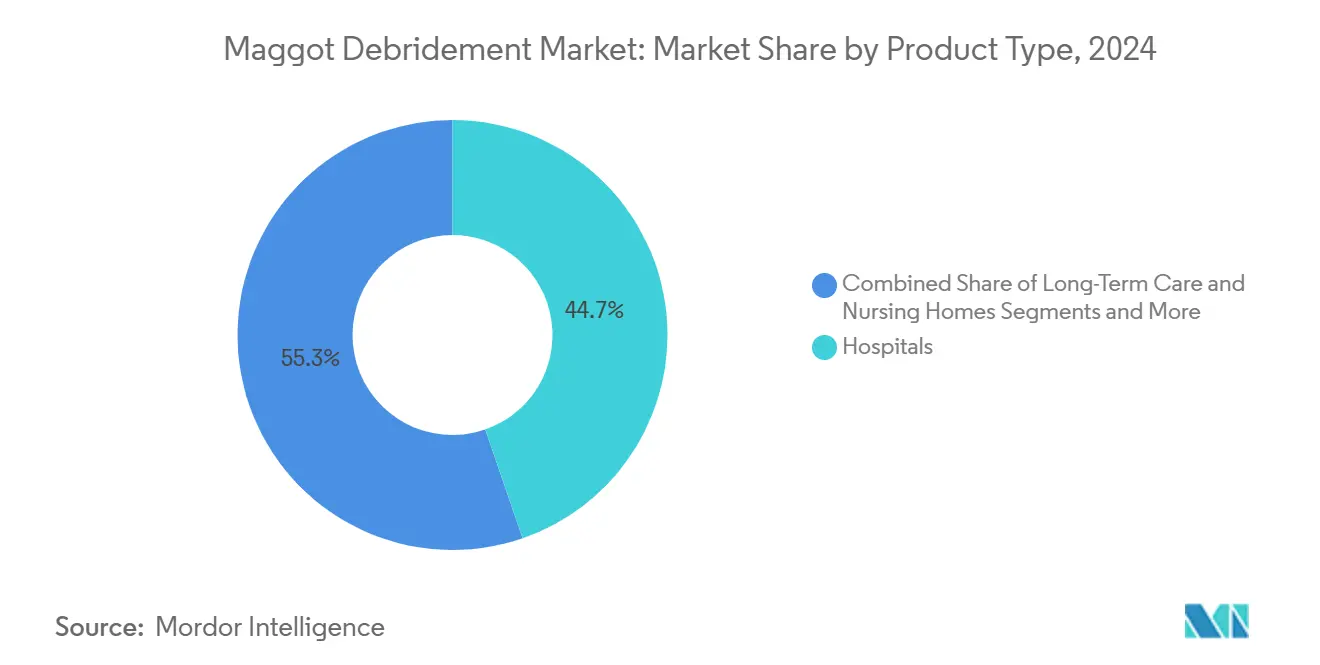

- By end user, hospitals generated 44.7% of 2024 revenue, while home-care settings are poised to post a 15.8% CAGR to 2030 as tele-MDT models proliferate.

- By geography, North America commanded 38.5% revenue share in 2024; Asia Pacific is forecast to expand at a 10.6% CAGR through 2030 on the back of widening diabetic populations and regulatory clearances.

Global Maggot Debridement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Chronic Wounds Among Diabetic & Geriatric Population | +2.10% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Escalating Antibiotic-Resistant Infections Driving Alternative Therapies | +1.80% | Global, particularly acute in hospital settings | Medium term (2-4 years) |

| Growing Reimbursement Coverage For Biotherapy Across OECD Markets | +1.40% | OECD countries, expanding to emerging markets | Medium term (2-4 years) |

| Regulatory Green Lights (FDA, CE-Mark) For Sterile Larval Products | +1.20% | North America & Europe, influencing Asia Pacific adoption | Short term (≤ 2 years) |

| Genetically-Engineered Larvae With Amplified Antimicrobial Peptides | +0.90% | Research-intensive markets, early adoption in US | Long term (≥ 4 years) |

| Tele-MDT Platforms Enabling Home-Based Treatments | +0.70% | Developed markets with robust telehealth infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Wounds Among Diabetic & Geriatric Populations

Roughly 15% of people with diabetes develop foot ulcers, and fewer than 50% heal under conventional care, fueling a steady influx of cases that need faster, deeper debridement.[1]Thao Lam et al., “Efficacy of Larval Therapy for Wounds,” mdpi.com Aging populations compound this pressure because compromised vascularization and slower cell turnover hamper healing. Medicare’s 2025 fee-schedule update now covers caregiver training for advanced wound modalities, signaling payer awareness that traditional protocols no longer suffice. Systematic reviews confirm that maggot therapy clears necrotic tissue more completely than scalpel or enzymatic methods in diabetic ulcers, cutting healing time and amputation risk. As national diabetes registries swell, hospitals face mounting resource strain, pushing clinicians to adopt modalities that truncate healing timelines without escalating antibiotic exposure.

Escalating Antibiotic-Resistant Infections Driving Alternative Therapies

Methicillin-resistant Staphylococcus aureus and biofilm-forming Pseudomonas species now dominate chronic wounds in tertiary centers, rendering many topical antibiotics ineffective. Larval secretions carry potent antimicrobial peptides that dismantle biofilms and lower pathogen burden, a mechanism that pathogens struggle to resist. Clinical audits show bacterial counts trending downward within 48 hours of maggot application, often without adjunct antibiotics. Infection control committees increasingly treat MDT as a frontline option when antibiograms suggest multidrug resistance. This recalibration aligns with global antimicrobial stewardship mandates that favor biologics capable of curbing resistance propagation.

Growing Reimbursement Coverage for Biotherapy Across OECD Markets

Aetna, Blue Cross, and multiple EU statutory insurers now publish explicit medical-necessity language for MDT in non-healing necrotic wounds, eliminating administrative ambiguity that previously discouraged ordering physicians. Medicare Administrative Contractors revised local coverage determinations in early 2025, standardizing coding and documentation and accelerating claims approval. Economic modeling across 10 OECD systems shows median per-wound savings of 51-94% when MDT shortens treatment from 12 to 6 weeks. As fiscal scrutiny heightens, finance departments are lobbying wound-care clinics to privilege regimens with demonstrable net savings, positioning MDT as a budget-positive line item rather than a niche experiment.

Regulatory Green Lights for Sterile Larval Products

The December 2024 transfer of maggot oversight from CDRH to CBER aligns these products with other living therapeutics, ensuring review teams possess relevant biologics expertise.[2]Food and Drug Administration, “Transfer of Regulatory Responsibility…,” fda.gov In Europe, CE-marking harmonizes quality and sterility standards, letting suppliers distribute across 27 nations without renegotiating national clearances. SolasCure’s enzyme-based Aurase Wound Gel secured FDA Fast-Track status in June 2025, indicating the agency’s appetite for derivative innovations that still draw on maggot biology. These policy signals lower developer risk and accelerate venture funding into both contained larvae and secretome-based dressings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| "Yuck Factor" Limiting Clinician & Patient Acceptance | -1.80% | Global, particularly acute in Western markets | Medium term (2-4 years) |

| Competing Advanced Wound-Debridement Devices & Dressings | -1.20% | Developed markets with established wound care infrastructure | Short term (≤ 2 years) |

| Supply Chain Fragility After Facility Closures & Biosecurity Events | -0.90% | Global, with highest vulnerability in specialized production centers | Short term (≤ 2 years) |

| Regulatory Ambiguity For Veterinary Off-Label Use In Emerging Markets | -0.60% | Emerging markets in Asia Pacific, Latin America, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

“Yuck Factor” Limiting Clinician & Patient Acceptance

Surveys across 600 wound nurses in the United Kingdom and the United States found that 54% hesitate to recommend larvae because they fear patient refusal.[3]Tom Ireland, “Learning to love Lucilia,” rsb.org.uk Pain-monitoring trials report transient discomfort in roughly 29% of cases, handing detractors anecdotal ammunition. Public-awareness campaigns such as Swansea University’s “Love a Maggot” are closing the knowledge gap, yet cultural aversion to insects lingers, especially in outpatient settings. Contained BioBag systems have softened the optics, but achieving parity with vacuum or ultrasonic devices still hinges on persistent clinician education and patient testimonials. Until perception aligns with evidence, adoption will progress unevenly across regions.

Competing Advanced Wound-Debridement Devices & Dressings

Negative-pressure devices, ultrasonic probes, and antimicrobial foams from companies like Smith & Nephew and ConvaTec clocked mid-single-digit revenue growth in 2024. Their installed base, Salesforce reach, and procedural familiarity make them formidable alternatives. Clinicians facing tight scheduling gravitate toward modalities that require less preparation than live larvae. Manufacturers of maggot products must therefore demonstrate superior clinical endpoints—often a 1-to-2-day faster debridement—and competitive cost of consumables to displace incumbents. Without clear hospital-level protocols favoring biologics, purchasing committees will default to devices already stocked on shelves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Contained Systems Drive Adoption

Contained larvae products delivered 52.8% of 2024 revenue, mirroring clinician demand for sterile, mess-free application that shields patients from visible crawling activity. Hospitals report a 34% rise in first-time usage once containment became available, underscoring aesthetics’ outsized influence on decision-making. Free-range larvae remain indispensable for cavernous or irregular wounds, yet their share is contracting as delivery pouches improve conformability. The maggot debridement therapy market size for genetically-modified variants is forecast to swell at 13.4% CAGR to 2030 as PDGF-expressing strains finish safety studies. These enhanced larvae promise simultaneous debridement and growth-factor dosing, a dual-function competitive devices that struggle to match. Growth is attracting private-equity interest, and at least four start-ups announced Series A rounds focused on “designer” insects in 2025.

Research momentum also fuels larval extract gels that eliminate live organisms entirely. Early data show secretome-based dressings clearing slough in 5.3 days on average, nearly matching live larvae while erasing the acceptance barrier. If Phase III endpoints hold, the maggot debridement therapy market could bifurcate: live products for deep, infected wounds and bioactive dressings for outpatient maintenance. Such diversification would expand addressable patients and create tiered pricing, sharpening competition yet growing overall penetration. Ancillary kits, including breathable securing tapes and pH-monitoring overlays, represent a budding accessories line with gross margins above 65%, enticing wound-care distributors to champion the category.

By Application: Diabetic Care Dominates, Oncology Emerges

Roughly 38.2% of 2024 revenue stemmed from diabetic foot ulcers, cementing the segment as MDT’s proving ground. Payers track average length-of-stay savings of 2.3 days in hospitals using larvae for infected ulcers, enough to justify higher unit prices even under capitated payment models. Oncology-related necrotic lesions, while only 8% of the current volume, show 14.1% CAGR through 2030 due to growing palliative-care caseloads and FDA Fast-Track status for enzyme gels targeting calciphylaxis. Venous leg ulcers and pressure sores form a stable, albeit slower-growing, customer base where device competitors are well entrenched. The maggot debridement therapy market share for oncology wounds could touch double digits by 2028 if Phase II data translate into guideline inclusion.

Treatment protocols are diverging: high-exudate ulcers lean on free-range larvae for faster fluid management, while oncology lesions prefer contained systems to limit accidental dislodgement during radiotherapy sessions. Post-surgical wounds represent an untapped frontier; early case series in orthopedic centers report 21% faster granulation with larvae than hydrogel dressings, hinting at perioperative bundles that may open new reimbursement codes. As indication breadth widens, suppliers are investing in application-specific packaging—smaller pouch sizes for toe wounds, bio-occlusive breathable membranes for cavernous cavities—thereby boosting unit differentiation and reducing price erosion risk.

By End User: Hospitals Lead, Home Care Accelerates

Hospitals generated 44.7% of global sales in 2024 thanks to multidisciplinary wound-care teams and sterility-controlled environments. Intensive-care units particularly value larvae for septic pressure ulcers, often using MDT after negative-pressure therapy plateaus. Still, the fastest secular rise is occurring in home-care settings, advancing at 15.8% CAGR through 2030, as payers reimburse tele-MDT kits that ship overnight and include video guidance.

Specialized outpatient wound clinics remain an essential middle layer, blending hospital-grade infection control with community proximity. They account for 27% of 2025 orders and often serve as initial prescribers before transitioning stable patients to home monitoring. Nursing homes, managing a surging geriatric demographic, have begun adopting larvae under bundled per-diem rates, citing fewer transfer outs for surgical debridement. Veterinary hospitals round out demand with equine and exotic-animal cases, though regulatory ambiguity in some countries still limits off-label use. Collectively, this end-user mosaic shields suppliers from overreliance on any single channel.

Geography Analysis

North America commanded 38.5% of 2024 revenue on the back of concrete reimbursement paths and clear FDA oversight. U.S. academic centers spearheaded landmark trials that infused confidence throughout community hospitals, while insurers such as Aetna codified medical-necessity clauses that sharply reduced denial rates. Canada follows similar patterns, leveraging national diabetic foot-care strategies that explicitly reference biological debridement. Mexico, though smaller in absolute terms, is experimenting with public-sector formularies that include contained larvae to curb amputation-related disability costs.

Europe retains a deep MDT heritage dating back to World War I, with Germany, France, and the United Kingdom accounting for nearly 70% of regional volume. BioMonde’s centralized production system in Wales supplies much of the continental demand, ensuring consistent sterility and same-day shipment to clinical hubs. EU-wide CE-mark rules streamline distribution, though language-specific labeling still injects modest friction. Adoption is buoyed by guideline references from vascular-surgery societies and cost-utility studies from German sickness funds that highlight hospital stay reductions. Southern European nations show rising uptake as diabetic prevalence climbs and austerity budgets seek lower-cost wound solutions.

Asia Pacific is the fastest-growing territory at a 10.6% CAGR, driven by exploding diabetes incidence and healthcare infrastructure build-outs. Singapore and Hong Kong cleared Cuprina’s MEDIFLY in 2024, marking the region’s first approved live-maggot dressing. China is piloting domestic production to hedge supply risk, while India’s tertiary centers are importing BioBag systems under compassionate-use provisions. Regulatory heterogeneity remains a hurdle, yet knowledge transfer via tele-education is narrowing practice gaps. Australia and New Zealand, with robust telehealth frameworks, are experimenting with remote MDT supervision for rural patients, demonstrating that logistical challenges can be solved with digital tools.

Competitive Landscape

The maggot debridement therapy market is inherently fragmented because production requires sterile insectaries that few companies operate at scale. BioMonde dominates Europe but lacks direct U.S. presence. Monarch Labs and Cuprina Holdings serve North America and select Asia Pacific geographies, respectively, each leveraging proprietary rearing protocols. Market entrants such as SolasCure and ByBug are bypassing live-larvae bottlenecks by focusing on purified enzymes and recombinant peptides that can be manufactured in bioreactors, potentially breaking capacity ceilings once approved. Wound-care conglomerates Smith & Nephew and ConvaTec are exploring licensing deals rather than in-house breeding, signaling that partnerships, not greenfield build-outs, may shape consolidation.

Technology differentiation revolves around genetic engineering. North Carolina State University’s PDGF-expressing larvae achieved 41% faster re-epithelialization in murine trials, spurring venture-capital inflows into “bio-boosted” insect programs. Intellectual-property fencing on gene-editing vectors could create royalty streams akin to monoclonal antibodies. Tele-MDT platforms form another competitive layer: vendors bundle kits with HIPAA-compliant monitoring apps, forging sticky clinic relationships. Regional distributors gravitate toward suppliers offering these digital adjuncts, recognizing that clinical hand-holding is integral to uptake.

Pricing remains modest—USD 96-135 per treatment cycle for contained bags—yet gross margins exceed 55% owing to low feedstock costs. That margin attracts small biotechs, but scale-up complexities, including biosecurity and continuous egg supply, deter generic copycats. Regulatory changes aligning MDT with biologics tighten quality controls, favoring incumbents already compliant with GMP standards. Collectively, these dynamics point to gradual consolidation around firms that can marry insect breeding expertise with recombinant technology and service-layer software.

Maggot Debridement Industry Leaders

BioMonde

Monarch Labs

Zoobiotic Ltd

Merck KGaA (Larval Media Services)

BioSystems Technology (TruLarv Ltd)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: FDA transferred maggot oversight from CDRH to CBER, enhancing biologics review alignment.

- July 2024: USDA opened an USD 8.5 million sterile fly facility in Texas to bolster biosecurity and therapeutic insect supply

- June 2024: Swansea University launched “Love a Maggot” to reshape public perception of larval therapy.

Global Maggot Debridement Market Report Scope

| Free-Range (Loose) Larvae |

| Contained / BioBag Larvae |

| Genetically-Modified Larvae |

| Larval Extracts / Secretomes |

| Ancillary MDT Dressings & Kits |

| Diabetic Foot Ulcers |

| Venous Leg Ulcers |

| Pressure Ulcers |

| Post-Surgical & Traumatic Wounds |

| Oncology-Related Necrotic Lesions |

| Hospitals |

| Specialty Wound-Care Clinics |

| Long-Term Care & Nursing Homes |

| Home-Care Settings |

| Veterinary Hospitals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Free-Range (Loose) Larvae | |

| Contained / BioBag Larvae | ||

| Genetically-Modified Larvae | ||

| Larval Extracts / Secretomes | ||

| Ancillary MDT Dressings & Kits | ||

| By Application | Diabetic Foot Ulcers | |

| Venous Leg Ulcers | ||

| Pressure Ulcers | ||

| Post-Surgical & Traumatic Wounds | ||

| Oncology-Related Necrotic Lesions | ||

| By End User | Hospitals | |

| Specialty Wound-Care Clinics | ||

| Long-Term Care & Nursing Homes | ||

| Home-Care Settings | ||

| Veterinary Hospitals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is maggot debridement therapy revenue projected to grow through 2030?

Global revenue is forecast to rise from USD 15.5 million in 2025 to USD 23.5 million by 2030, reflecting an 8.6% CAGR.

Which region shows the quickest expansion for maggot debridement therapy?

Asia Pacific is advancing at a 10.6% CAGR, fueled by rising diabetes prevalence and recent regulatory clearances.

What drives adoption of maggot debridement therapy in diabetic foot care?

Superior debridement efficacy, reduced amputation risk, and payer support for advanced biological treatments are key factors behind its 38.2% revenue share in this application.

Why are payers broadening reimbursement for maggot-based wound care?

Economic studies show per-wound cost savings of 51-94% when larvae shorten healing timelines, prompting insurers such as Aetna and Medicare contractors to formalize coverage.

How do contained larvae systems influence clinician acceptance?

Sterile pouches eliminate direct insect contact, easing the 'yuck factor' and underpinning the 52.8% share held by contained products in 2024.

What competitive edge do genetically modified larvae offer?

PDGF-expressing strains combine debridement with growth-factor delivery, enabling faster tissue regeneration and supporting a 13.4% CAGR outlook for this product niche.

Page last updated on: