Prefilled Syringes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.77 Billion |

| Market Size (2031) | USD 18.12 Billion |

| Growth Rate (2026 - 2031) | 10.96% CAGR |

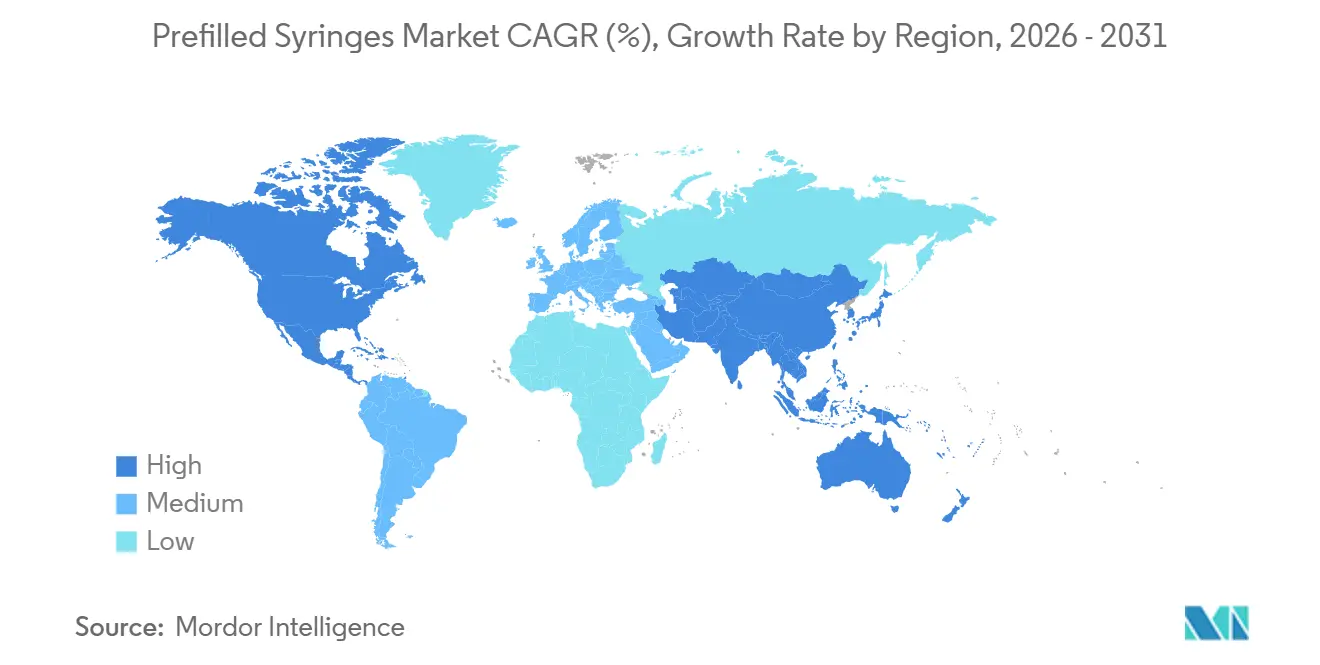

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prefilled Syringes Market Analysis by Mordor Intelligence

The Prefilled Syringes Market size is expected to increase from USD 9.74 billion in 2025 to USD 10.77 billion in 2026 and reach USD 18.12 billion by 2031, growing at a CAGR of 10.96% over 2026-2031.

Capacity bottlenecks in medical-grade borosilicate glass, the maturation of cyclic-olefin polymer alternatives, and stricter safety regulations are redefining competitive dynamics across the supply chain. Biologic drugs that demand cold-chain integrity are displacing vial-and-syringe workflows and anchoring long-term demand for ready-to-administer devices. Hospitals are purchasing safety-engineered formats to comply with needlestick-injury mandates, while payers reward home-care pathways that rely on user-friendly autoinjectors. Suppliers that bundle nested-tub packaging, automated particle inspection, and connected-device telemetry are winning long-term agreements with tier-1 pharmaceutical companies.

Key Report Takeaways

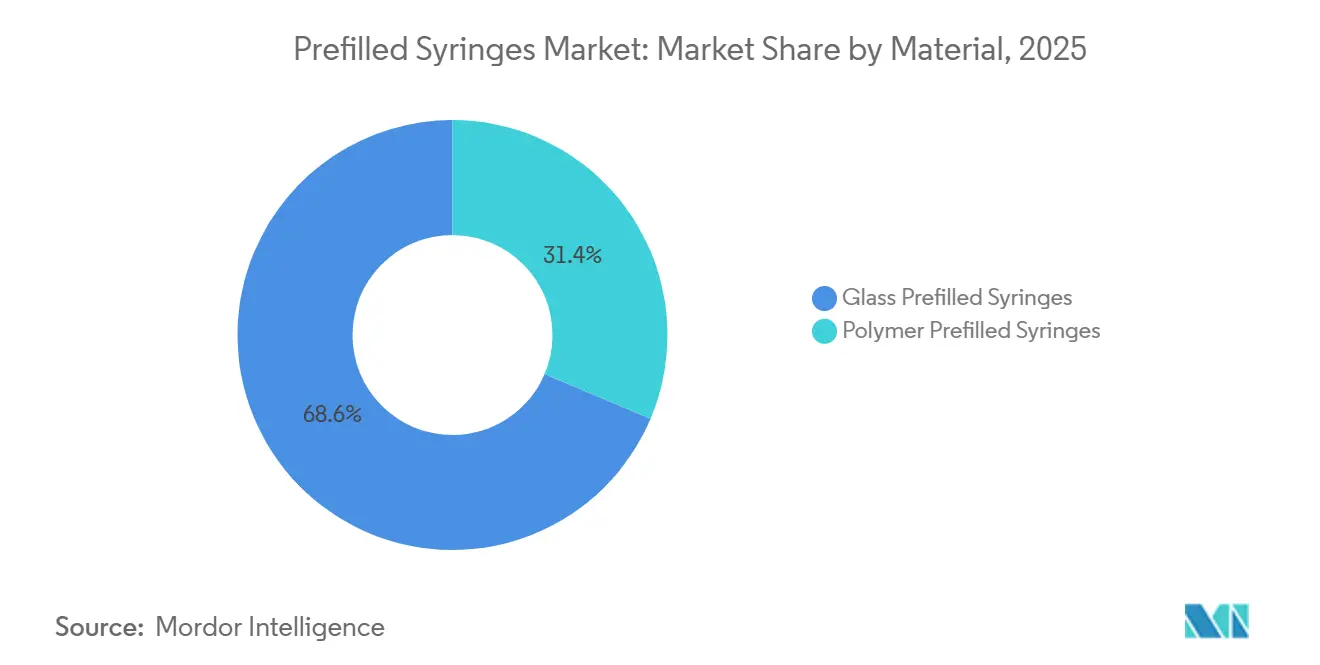

- By material, glass captured 68.63% of 2025 revenue, whereas polymer is the fastest-growing segment, with a 11.06% CAGR to 203.

- By application, diabetes led with 34.76% of the prefilled syringes market share in 2025; vaccines are forecast to expand at a 13.63% CAGR through 2031.

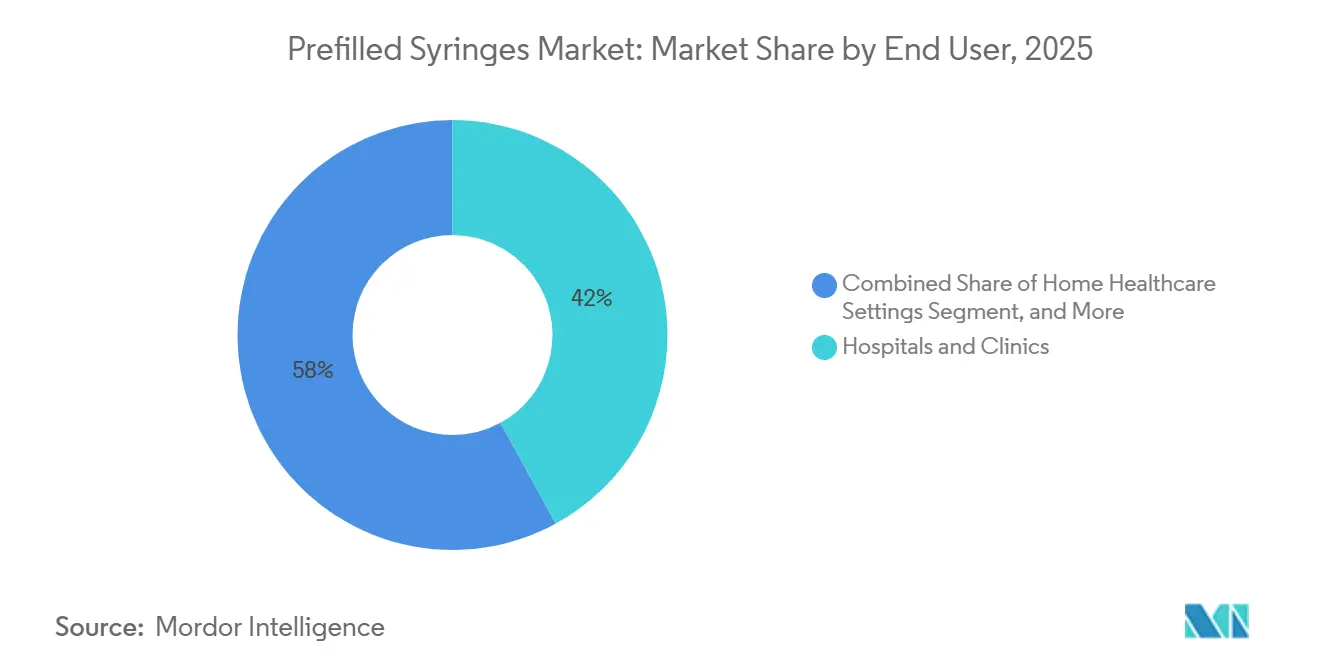

- By end user, hospitals and clinics held a 42.02% share of the prefilled syringes market in 2025, while home healthcare is advancing at a 11.92% CAGR.

- By geography, North America accounted for 38.41% of 2025 value, whereas Asia-Pacific is projected to post a 12.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Prefilled Syringes Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases | 1.8% | Global, with highest intensity in North America and Europe | Long term (≥ 4 years) |

| Shift Toward Self-Administration & Home-Healthcare Models | 1.5% | North America and Europe core, expanding to urban APAC | Medium term (2-4 years) |

| Acceleration of Biologics/Biosimilars Pipeline Requiring Ready-To-Fill Containers | 2.0% | Global, led by North America and EU manufacturing hubs | Long term (≥ 4 years) |

| Regulatory Emphasis on Needlestick-Injury Prevention | 0.8% | EU and North America mandated, gradual APAC adoption | Medium term (2-4 years) |

| Emergence of Connected "Smart" Syringes Enabling Dose-Tracking | 0.6% | North America and select EU markets, pilot programs in Japan | Short term (≤ 2 years) |

| Capacity Investments In Polymer PFS Lines to Mitigate Glass Shortages | 1.2% | Global, concentrated in Germany, US, and Japan manufacturing sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Diabetes prevalence doubled between 1990 and 2022, climbing to 14.0% of the global adult population and pushing weekly GLP-1 therapies into mainstream use. Prefilled syringes eliminate reconstitution errors and shorten training time, thereby lowering annual treatment costs by USD 8,000–12,000 per rheumatoid arthritis patient compared with infusion-center administration.[1]Global Diabetes Report 2025, World Health Organization, who.int Payer contracts in the United States and Germany already link reimbursement to adherence metrics pulled from Bluetooth-enabled autoinjectors, giving manufacturers a revenue-protection incentive to supply smart formats. Chronic-disease growth, therefore, delivers a structural lift to the prefilled syringes market, especially for long-acting biologics that require precise dosing. Forward pipelines of subcutaneous antibodies suggest a durable demand floor extending past 2031.

Shift Toward Self-Administration & Home-Healthcare Models

Medicare Part B coverage expanded in 2024 to support home-injected biologics, shifting an estimated 25–30% of specialty injectable volume out of hospital outpatient departments by 2028. Telehealth platforms paired with Bluetooth autoinjectors reduced readmissions due to non-compliance by up to 22% in U.S. pilots. European structural funds worth EUR 5 billion are earmarked for home-care infrastructure, accelerating the policy’s export to the EU. Prefilled formats remove the final reconstitution barrier, lowering skill requirements and enabling direct-to-consumer channels. Combined, these factors expand the addressable market for prefilled syringes beyond hospital walls.

Acceleration of Biologics / Biosimilars Pipeline Requiring Ready-To-Fill Containers

The FDA Purple Book listed 48 approved biosimilars by end-2025, most launched in prefilled syringe clones to mirror originator devices and encourage switching.[2]FDA Combination-Product Guidance, fda.gov Monoclonal antibodies are viscous and shear-sensitive; siliconized glass or cyclic-olefin polymer syringes minimize protein aggregation compared with vial transfer. CDMOs have responded with 15–20% capacity growth in 2024–2025, favoring isolator-based lines that support quick changeovers at ≤400 units per minute. Device suppliers offering nested-tub packaging reduce line prep time, giving biologics sponsors a speed-to-launch advantage that deepens the moat for integrated syringe platforms. Consequently, the prefilled syringes market benefits directly from every new biologic or biosimilar license.

Regulatory Emphasis on Needlestick-Injury Prevention

OSHA fines for noncompliance reached USD 15,625 per infraction in 2025, steering U.S. hospitals toward prefilled passive-safety syringes. EU Directive 2010/32/EU carries similar obligations, yet 23% of Eastern European facilities lag in implementation due to budget gaps. Reported needlestick incidents surged by 23% during COVID-19 staffing shortages, reinforcing the need to switch to sharps with automatic needle shields. Hospitals justify the 15–25% device premium by avoiding post-exposure prophylaxis, typically costing USD 500–3,000 per event. Safety regulation, therefore, underpins a predictable tailwind for the prefilled syringes market.

Restraints Impact Analysis of Prefilled Syringes Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Extractables/Leachables Compliance Elevating CMC Costs | -1.2% | Global, most acute for small biotech firms in North America and EU | Medium term (2-4 years) |

| Supply-Chain Constraints for Medical-Grade Borosilicate Glass | -0.9% | Global, with tightest supply in North America and Europe | Short term (≤ 2 years) |

| Tightening PFAS & Silicone-Oil Regulations Impacting Legacy Lubricants | -0.5% | North America and EU regulatory focus, spillover to APAC | Medium term (2-4 years) |

| Growing Environmental Scrutiny on Single-Use Plastics Disposal | -0.4% | EU leading, with emerging pressure in North America and select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Extractables / Leachables Compliance Elevating CMC Costs

ISO 10993-18:2020 compels exhaustive chemical characterization under worst-case temperature and time scenarios, often adding 6–9 months to CMC timelines.[3]ISO 10993-18:2020, International Organization for Standardization, iso.org FDA guidance sets an analytical threshold of 0.15 µg/day above which toxicology justifications are mandatory. Redundant regional standards force duplicate testing for U.S., EU, and Asian submissions, consuming up to 12% of mid-tier biosimilar development budgets. Cyclic-olefin polymers lack the historical safety database of glass, so sponsors face even more scrutiny, extending review cycles. These delays temper near-term growth for the prefilled syringes market, especially for cash-constrained biotech entrants.

Supply-Chain Constraints for Medical-Grade Borosilicate Glass

Vial demand monopolized furnace capacity through 2025, pushing syringe-grade glass lead times to more than 18 months. New furnaces cost USD 216–324 million and have decade-long lifecycles, limiting rapid expansion. Shortages lifted spot prices by 20–30% above contract levels; firms without long-term agreements weighed the cost of polymer requalification against delayed launches. Concentrated production in Germany and Japan exposes the supply chain to energy-price shocks and labor disputes. These structural weaknesses curb near-term upside for the prefilled syringes market until diversified capacity comes online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Prefilled Syringes Market Segment Analysis

By Material:

Polymer Gains Ground Amid Glass FragilityGlass accounted for 68.63% of 2025 revenue, reflecting entrenched regulatory acceptance and mature extractables data. Nonetheless, polymer’s 11.06% CAGR signals a decisive tilt in new capacity adds and future launches, particularly for high-viscosity monoclonal antibodies at fracture risk during autoinjector actuation. Polymer also shields sponsors from glass-particle recalls and borosilicate shortages, prompting parallel validation programs despite the upfront burden of extractables testing. SCHOTT and Gerresheimer are hedging by adding polymer lines while maintaining glass leadership, confirming a dual-track strategy. These moves ensure the prefilled syringes market retains supplier diversity and capacity resilience, even as glass remains indispensable for oxygen-sensitive vaccines requiring long shelf lives.

By Application:

Diabetes Dominates, Vaccines SurgeDiabetes accounted for 34.76% of 2025 revenue, as GLP-1 agonists scaled rapidly and insulin analogs remained stable. The launch pace of GLP-1 class line extensions suggests a sustained volume floor, anchoring one-third of the prefilled syringes market share through mid-decade. RSV and endemic COVID-19 campaigns boost vaccine volume, delivering a 13.63% CAGR that will lift the prefilled syringes market size for immunizations by 2031.

Rheumatoid-arthritis biosimilars and anticoagulants provide steady mid-single-digit expansion, while fertility, immunoglobulins, and emergency drugs contribute niche but lucrative margins. Collectively, high-frequency dosing regimens favor connected autoinjectors that feed adherence data into payer dashboards, reinforcing the shift away from vial formats.

By End-User:

Home Healthcare Gains MomentumHospitals and clinics retained 42.02% of 2025 spending due to complex cold-chain biologics and strict sharps-safety protocols. Yet home healthcare’s 11.92% CAGR indicates a structural hand-off of chronic-disease administration to patients. By 2031, home settings are positioned to overtake ambulatory centers and claim nearly one-third of the prefilled syringes market. Medicare policy changes, telehealth integration, and cost parity between home injection and clinic visits accelerate this trend.

Retail pharmacies, long-term care, and occupational clinics round out the landscape, with influenza and B12 shots anchoring predictable annual volume. Human-factors design—audible clicks, large grips, and clear dose windows remain critical to reduce user error across all sites.

Geography Analysis

North America Prefilled Syringes Market

North America captured 38.41% of 2025 revenue, buoyed by dense biologics clusters in New Jersey, North Carolina, and California, as well as OSHA safety mandates. Medicare home care coverage is projected to divert up to 30% of specialty injectable volume by 2028, cementing demand for patient-centric devices. Canada’s regulatory reciprocity and Mexico’s CDMO expansions extend the regional supply chain, supporting steady growth in the prefilled syringes market.

Eastern Europe Prefilled Syringes Market

Europe’s regulatory drivers include EU Directive 2010/32/EU and aggressive biosimilar adoption, keeping the region a stronghold for glass-to-polymer innovation. Structural funds of EUR 5 billion for home-care programs through 2027 will expand decentralized administration in underserved Eastern regions, though uneven compliance with sharps mandates continues to restrain uptake.

APAC Prefilled Syringes Market

Asia-Pacific is the growth engine at a 12.27% CAGR. India’s Production Linked Incentive scheme, China’s shortened biosimilar approval windows, and Japan’s reimbursement premium for connected devices combine to amplify local manufacturing and consumption. Australia and South Korea, with tight regulatory regimes, serve as beachheads for smart-device pilots that later scale across ASEAN.

Regulatory Landscape

Prefilled syringes, particularly integral drug-device combination products, sit at the intersection of medicinal-product and medical-device controls, which tightens documentation and lifecycle oversight for component suppliers, fill-finish CDMOs, and marketing authorization holders. In the United States, the FDA Quality Management System Regulation (QMSR) became effective on February 2, 2026, replacing the former 21 CFR 820 framework and incorporating ISO 13485:2016 by reference. This raises the compliance bar for quality systems supporting device constituent parts used in prefilled syringes and autoinjector presentations.

In Europe, EU MDR 2017/745 Article 117 continues to require a Notified Body Opinion or CE evidence for the device constituent part within the medicinal product dossier. It also pushes earlier alignment between pharma sponsors and syringe, needle, and closure suppliers on GSPR evidence. Standards work remains a key reference point for design and performance expectations, with ISO 11040-4:2024 (glass barrels) as a core component benchmark, and ISO 11040-8:2026 for finished prefilled syringes published on June 8, 2026, reinforcing system-level testing expectations for finished units used in ready-to-administer formats. The European Commission proposal COM(2025) 1023 final (published in December 2025) to amend MDR and IVDR is also being tracked by manufacturers, as it may affect transition planning and documentation workloads for EU market access.

Competitive Landscape

The market is moderately consolidated. Becton, Dickinson, and West Pharmaceutical Services leverage vertical integration across glass tubing, elastomers, and inspection systems to secure long-term supply contracts. BD’s Neopak and Effivax lines underpin 5.9% organic growth, supported by capacity expansions in North Carolina and Ireland. West Pharmaceutical Services pairs Daikyo stoppers with SmartDose wearables, capturing high-margin demand for combination products.

CDMOs, notably Vetter Pharma and Catalent, provide turnkey fill-finish solutions that de-risk launches for sponsors without in-house aseptic capability. Their investments in isolator lines and FlexDirect small-batch modules answer the biosimilar wave. Polymer specialists such as SiO2 Materials Science and Stevanato Group push cyclic-olefin innovation, aided by silicon-free technologies that sidestep PFAS scrutiny.

Technology differentiation revolves around nested-tub packaging, automated sub-visible particle inspection, and connected caps. Suppliers able to satisfy ISO 11608 ergonomics while bundling telemetry enjoy superior pricing power. Regional production footprints further influence buyer decisions in an era of supply-chain de-risking.

Prefilled Syringes Industry Leaders

Becton Dickinson and Company

West Pharmaceutical Services, Inc.

Gerresheimer AG

Terumo Corporation

SCHOTT AG

- *Disclaimer: Major Players sorted in no particular order

Prefilled Syringes Market Companies Covered in this Report

- Abbvie

- Amgen

- AptarGroup Inc.

- Baxter

- Beckton Dickinson

- Catalent

- Fresenius

- Gerresheimer

- Johnson & Johnson

- Medtronic

- Nipro

- Novartis

- Pfizer

- Roche

- Sanofi

- SCHOTT

- Smiths Group

- Terumo

- Vetter Pharma International GmbH

- West Pharmaceutical Services

- Ypsomed

Market Opportunities and Future Outlook

A near-term opportunity is expanding ready-to-use (RTU) prefillable syringe supply and sterile fill-finish capacity that can handle high-viscosity and higher-volume biologics, particularly amid ongoing constraints in syringe-grade borosilicate glass and the operational premium associated with nested-tub workflows and isolator-based filling. In January 2026, BD announced a USD 110 million investment to expand prefillable syringe production at its Columbus, Nebraska facility, including establishing BD Neopak glass prefillable syringe production, which aligns with customer demand for localized, contracted supply. Capacity additions on the CDMO side are also clustering around prefilled syringes and cartridges, including Grand River Aseptic Manufacturing’s USD 100 million investment announced in April 2026 for a fifth sterile filling line for high-volume prefilled syringes and cartridges with 50 million units of annual capacity, and PCI Pharma Services’ USD 100 million investment announced in April 2026 at its San Diego campus for a high-speed isolator filling line for RTU prefilled syringes and cartridges.

Another whitespace area is compliance-enabling, polymer-focused platforms that reduce breakage risk while addressing increasingly explicit expectations on extractables/leachables and device-grade evidence for combination products. The FDA QMSR effective date of February 2, 2026 and EU MDR Article 117 mechanics are pushing sponsors to select suppliers that can provide ISO-aligned quality systems, standardized test packages, and structured change-control on materials, lubricants, and coatings. Standardization activity is also widening the addressable base for plastic prefillable formats, with the European Pharmacopoeia proposing a new chapter 3.3.9 for prefillable plastic syringes for liquid preparations in July 2026 (public comment deadline September 30, 2026). This supports clearer compendial expectations for COP/COC syringe adoption in sensitive biologics and emerging modalities, reinforcing demand for suppliers that bundle container, closure, inspection, and documentation into a submission-ready system rather than selling components in isolation.

Recent Industry Developments in Prefilled Syringes Market

- March 2026: West Pharmaceutical Services officially opened a 165,000 square foot expansion at its Damastown, Dublin site to enhance contract manufacturing capabilities with advanced automation and drug-handling capacity. The added footprint supports higher-throughput assembly and processing activities that are increasingly paired with prefilled syringe and combination-product programs.

- September 2025: Celltrion Pharm signed a strategic trilateral agreement with Becton, Dickinson and Company and BD Korea to accelerate its global prefilled syringe (PFS) CMO business. The collaboration ties a biosimilar-focused manufacturer more closely to a leading syringe platform provider, strengthening end-to-end capability for device-forward injectable launches.

- September 2024: BD launched the Neopak XtraFlow Glass Prefillable Syringe and unveiled new capacity for the wider Neopak platform. The product and capacity move targeted biologics that demand robust functional performance during injection and increased availability of advanced syringe formats amid industry-wide constraints in syringe-grade glass supply.

Prefilled Syringes Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the prefilled syringes market is defined as ready-to-administer syringes that come pre-filled with a measured drug dose and are sold for clinical and home use, across major global regions.

Scope exclusions: The sizing excludes needles and safety accessories sold separately, along with drug value when the revenue is not captured in the syringe device and fill-finish packaging economics.

Segments Covered in This Report

- By Material

- Glass Prefilled Syringes

- Polymer Prefilled Syringes

- By Application

- Diabetes

- Rheumatoid Arthritis

- Vaccines

- Anticoagulants

- Other Applications

- By End-user

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home Healthcare Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping demand signals for injectable therapies and the packaging shift toward unit-dose delivery, then aligning those signals to device and fill-finish value pools. We rely on public health and regulatory signals, including FDA guidance and recalls databases, CDC immunization and disease burden statistics, and WHO program updates, to understand application mix and adoption patterns.

We also use UN Comtrade trade flows for relevant medical device and glass/plastics inputs, OECD and World Bank macro indicators for healthcare spend context, and peer-reviewed journals for trends such as biologics delivery and safety-device adoption. Company annual reports, investor presentations, and press releases help verify capacity additions and product launches, and a paid subscription focused on company financials and news is used to cross-check revenue ranges and ownership structures. These examples are not exhaustive, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary checks were run with a spread of participants across packaging, device manufacturing, and downstream buying roles, so assumptions on volumes, pricing, and mix were not built from desk signals alone. Inputs were validated across APAC, EMEA, and the Americas, with specific attention on shifts between glass and polymer formats, and the growing use of ready-to-fill components in high-volume applications.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 41% |

| Mid tier: 42% | Functional/Unit leaders: 29% | EMEA: 37% |

| Smaller Players: 21% | Managers: 57% | Americas: 22% |

Market-Sizing & Forecasting

The core model uses a top-down approach where injectable therapy demand and delivery setting patterns are used to reconstruct the addressable prefilled syringe requirement, which is then translated into value using application-level pricing logic. To keep totals realistic, we corroborate them with selective bottom-up approximations, such as supplier revenue ranges, sampled ASP bands by material type, and channel checks on ready-to-fill adoption in large therapy areas.

Key inputs include: the split between glass and polymer prefilled formats, safety feature penetration, application mix (for example vaccines and chronic therapies), utilization by end user setting, and regional regulatory and quality events that can temporarily shift supply. When bottom-up details are missing for smaller markets, gaps are handled through conservative adoption curves that are anchored to trade indicators and the closest comparable country patterns.

For forecasting, scenario analysis is used around two or three practical drivers, such as therapy growth, mix shift toward self-administration, and pricing progression by material, and then stress-tested using expert consensus ranges gathered during interviews.

Data Validation & Update Cycle

Checks are performed in stages so the final number is not driven by any one source. We compare outputs against independent signals such as trade movement direction, reported expansion activity, and the implied per-unit economics from interview-based ASP ranges, and any large variance is reviewed before sign-off.

If a data point looks inconsistent, the assumption is revisited and the relevant respondents are re-contacted to confirm what changed, and whether it is structural or temporary. The study is refreshed annually, and interim updates are made when material events occur, such as major regulatory actions or notable capacity shifts. Before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Prefilled Syringes Market Estimate Compared With Other Published Estimates

Published market sizes for prefilled syringes can differ even when the topic name looks the same, because firms do not always align on what revenue is counted and which year is treated as the start of the forecast. Differences also come from how application mix, material split, and price progression are modeled when public pricing is limited.

Shipment direction, application-level adoption signals, and supplier capacity announcements are used as checks that keep Mordor Intelligence's estimate tied to a defined device and packaging revenue pool, rather than blending in adjacent drug value or loosely related consumables.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.77 B (2026) | |

| Industry Research Publisher A | USD 9.48 B (2026) | Uses a different base-year setup and estimation path that can understate near-term value when price progression and safety-feature penetration are kept conservative, and when some end-user setting mix is treated at a higher level. |

| Global Consultancy B | USD 9.59 B (2025) | Anchors the headline to a prior year and may apply a broader market boundary across regions, which can shift the year-to-year comparability if currency timing, scope of device-only revenue, and refresh dates are not aligned. |

Overall, the spread is mainly explained by base-year choice and what each model counts inside the revenue boundary, plus how ASP movement is carried forward by material and application. By keeping the inputs traceable to observable adoption and supply signals and then cross-checking totals with practical bottom-up approximations, the final number stays repeatable for users who want to sanity-check assumptions.

Key Questions Answered in the Report

What is the projected value of the prefilled syringes market in 2031?

The market is forecast to reach USD 18.12 billion by 2031, growing at a 10.96% CAGR from 2026 to 2031.

Which application is expanding fastest through 2031?

Vaccines lead growth at a 13.63% CAGR as RSV and endemic COVID-19 shots shift to prefilled formats.

Why are polymer syringes gaining share?

They resist breakage, avoid glass-particle contamination, and enable silicone-free designs, supporting 11.06% CAGR adoption.

How is Medicare policy influencing demand?

Part B now reimburses home-injected biologics, redirecting up to 30% of specialty volume from hospitals to patient homes by 2028.

Which region shows the highest future CAGR?

Asia-Pacific is set to expand at 12.27% CAGR, driven by India’s incentives, China’s faster approvals, and Japan’s premium for connected devices.

Page last updated on: