Syringes Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

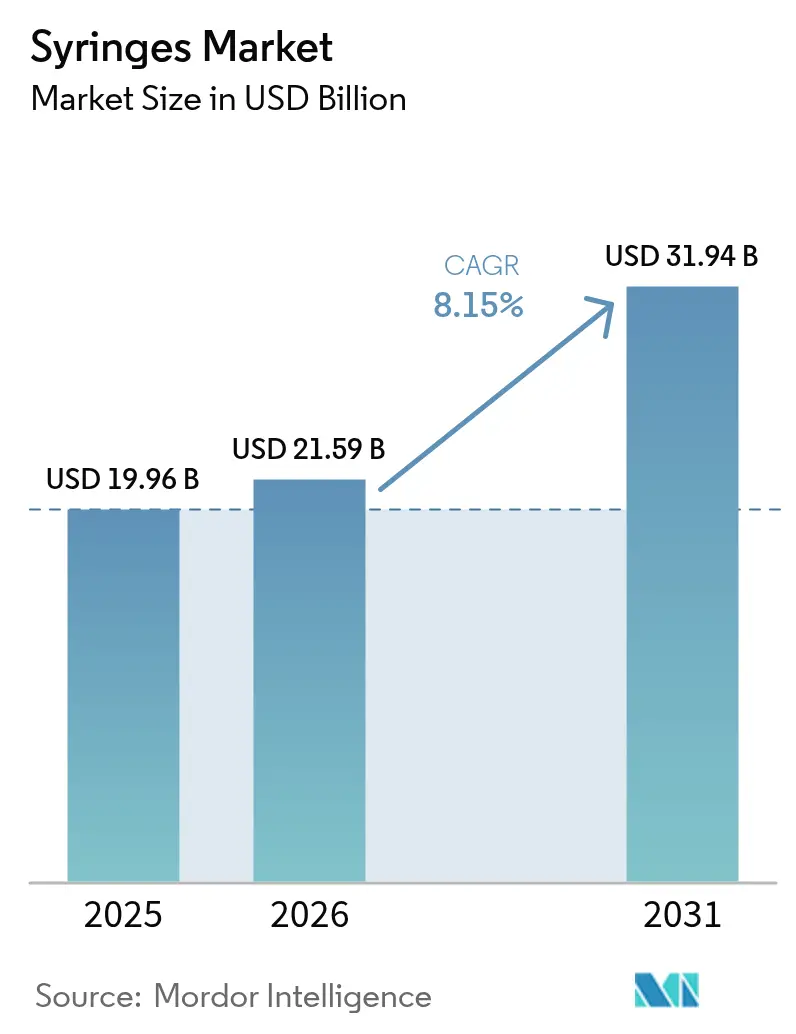

| Market Size (2026) | USD 21.59 Billion |

| Market Size (2031) | USD 31.94 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

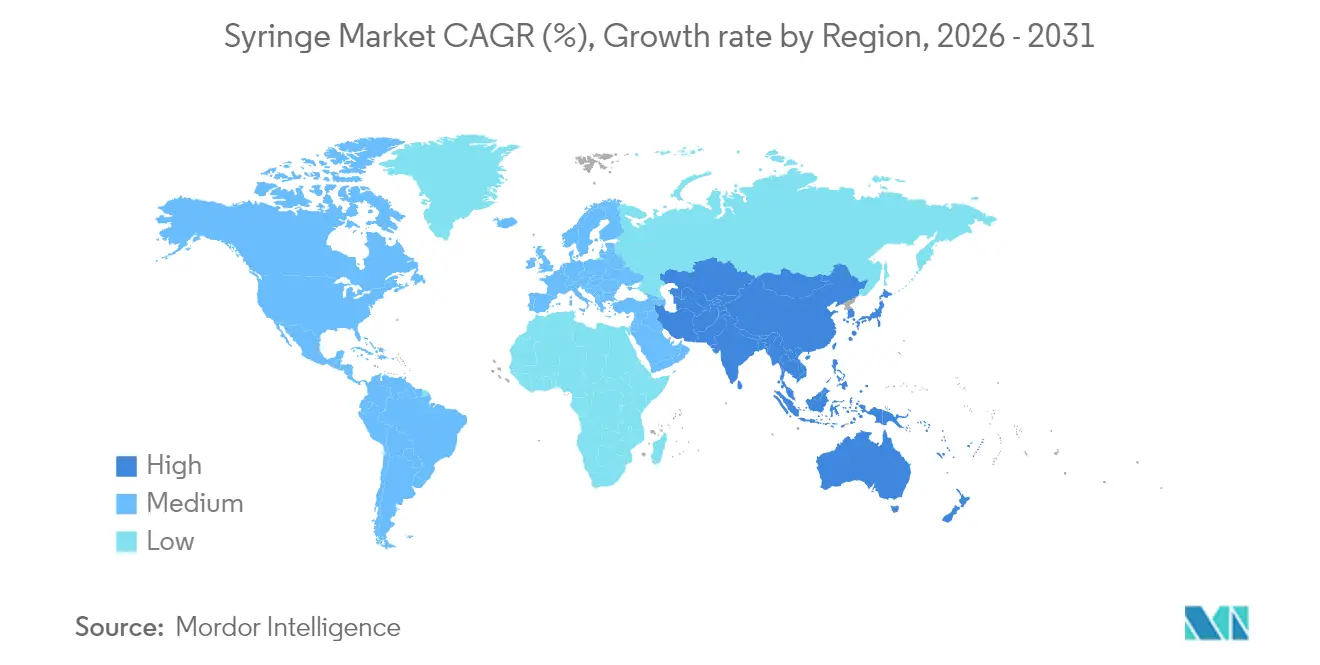

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

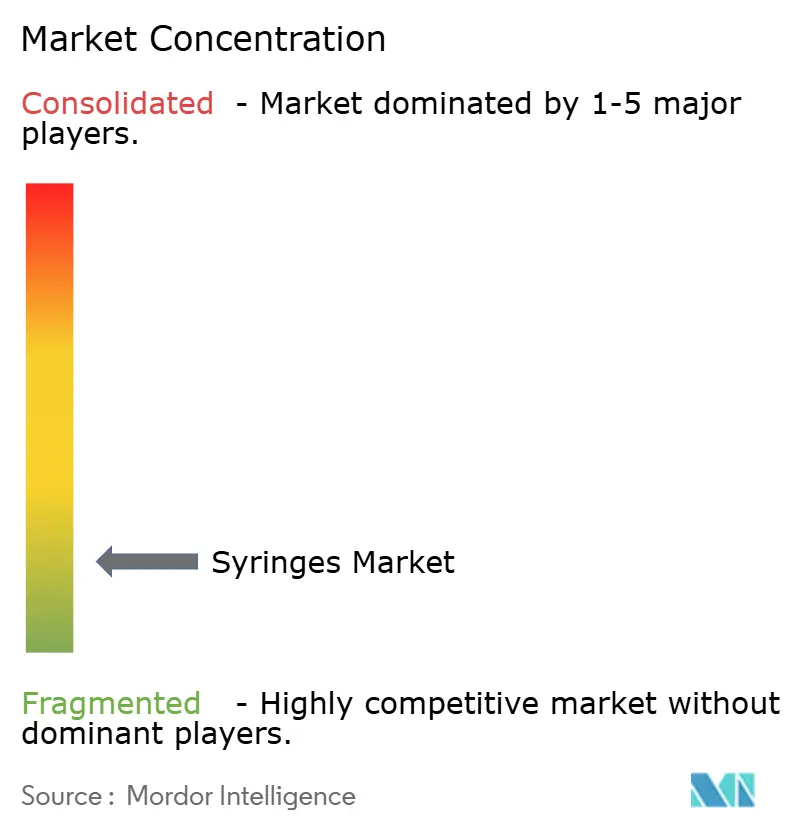

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Syringes Market Analysis by Mordor Intelligence

The syringes market size was valued at USD 19.96 billion in 2025 and estimated to grow from USD 21.59 billion in 2026 to reach USD 31.94 billion by 2031, at a CAGR of 8.15% during the forecast period (2026-2031). Growth momentum is rooted in three converging forces: a steady rise in chronic illnesses that require frequent injections, a structural commitment to mass‐vaccination capacity, and the pharmaceutical industry’s pivot toward biologics that need precise, low-dead-space delivery. Regulatory convergence around ISO 13485 standards, effective in the United States from February 2026, is recalibrating competitive stakes by making quality systems a prerequisite for market access. Meanwhile, sustained supply disruptions tied to sub-standard imports have prompted more than USD 400 million in domestic capacity expansions, led by BD’s two-year USD 40 million program to scale Connecticut and Nebraska plants. Across geographies, North America commands purchasing power and accounts for nearly 4 in 10 syringe shipments, while Asia-Pacific delivers the fastest unit growth at 9.32% CAGR, supported by public-health investments and rising chronic-disease incidence. Disposable formats dominate usage because infection-control protocols align with hospital workflow efficiencies, yet specialized syringes—prefillable, safety-engineered, and low-dead-space designs—post the strongest growth as biologics pipelines lengthen and unit economics allow premium pricing.

Key Report Takeaways

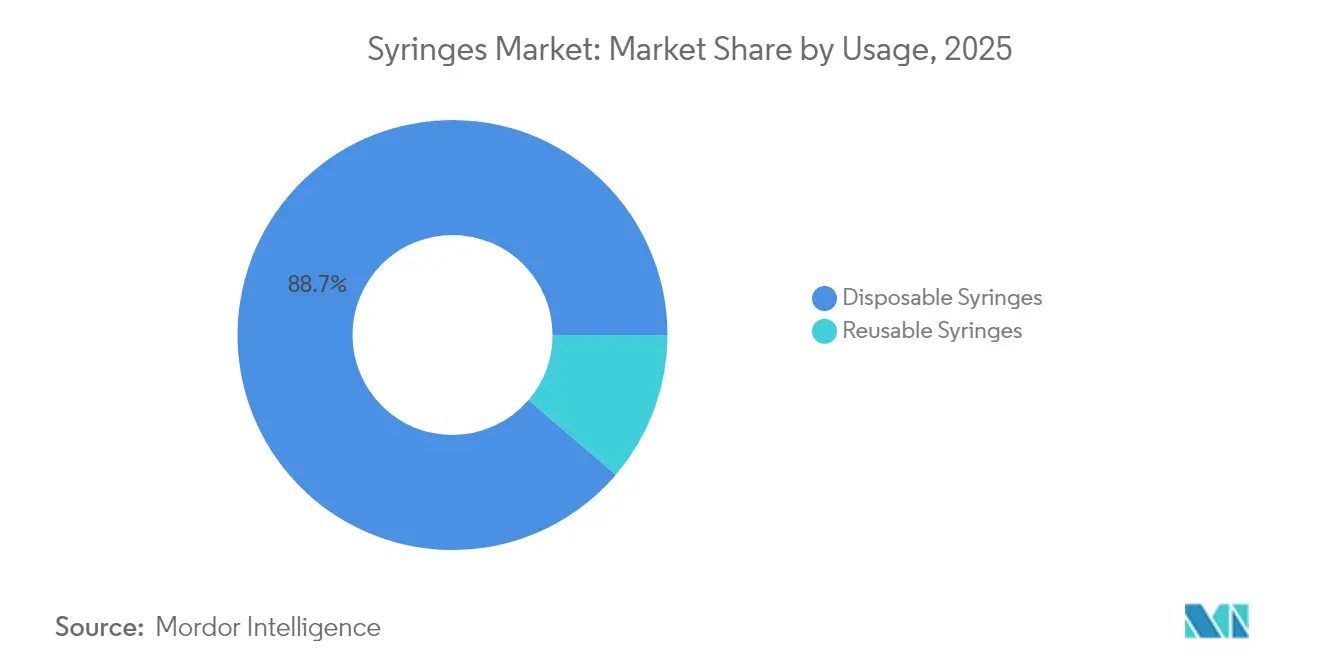

- By usage, disposable devices captured 88.74% of syringes market share in 2025.

- By product type, general-purpose variants led with 64.62% revenue share in 2025, while specialized syringes are on track for a 9.05% CAGR through 2031.

- By material, plastic formats accounted for 66.78% of the syringes market size in 2025 and are slated to expand at 9.08% CAGR between 2026 and 2031.

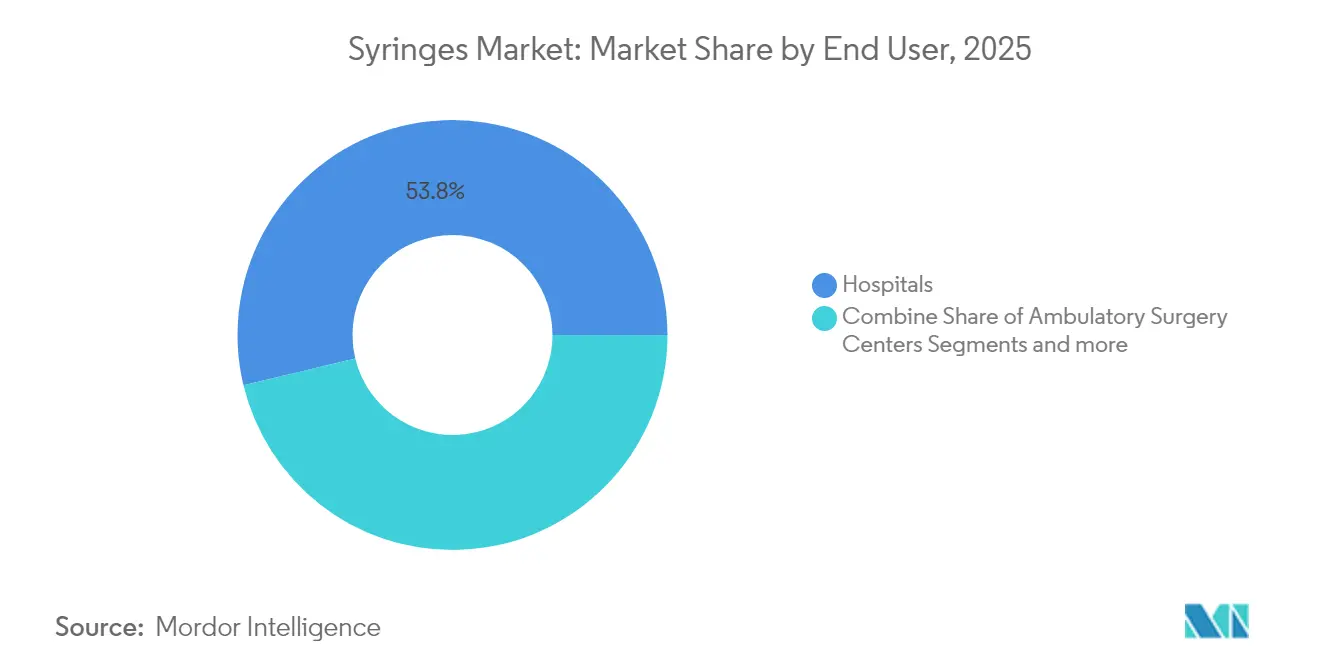

- By end user, hospitals held 53.76% of the syringes market size in 2025; home-care settings record the highest projected CAGR at 9.12% through 2031.

- By application, diabetes management controlled 36.45% revenue share in 2025, whereas vaccination and immunization use-cases are growing at 9.02% CAGR.

- Regionally, North America led with 39.12% share of the syringes market in 2025, and Asia-Pacific is forecast to grow the quickest at 8.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Syringes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic & infectious diseases | +1.8% | Global, concentrated in aging North American and European populations | Long term (≥ 4 years) |

| Growth in mass-vaccination programs | +1.5% | Global, emphasis on emerging markets and pandemic preparedness | Medium term (2-4 years) |

| Self-administration trend & dose precision | +1.2% | North America and EU lead, Asia-Pacific follows | Medium term (2-4 years) |

| Regulatory push for safety & smart syringes | +1.0% | North American and EU regulatory domains | Short term (≤ 2 years) |

| Uptake of low-dead-space syringes for CGT | +0.8% | North American and EU biotech hubs | Long term (≥ 4 years) |

| RFID-enabled waste traceability | +0.6% | North America and EU, expanding into Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Infectious Diseases

Global diabetes cases are projected to reach 783 million by 2045, intensifying demand for insulin delivery systems that support multiple daily injections. The volume effect is amplified by precision needs because viscous biologics require low-dead-space barrels that limit residual waste [1]World Health Organization, "New report highlights need for redoubled efforts to reach 2030 global immunization targets," who.int. Aging demographics raise injection frequency per patient, driving procurement of advanced syringes that maintain drug stability and ensure dose accuracy. Manufacturers capable of producing specialized formats command price premiums, benefiting from tight alignment with biologics developers. Pharma companies also explore combination therapies, increasing unit value per treatment episode and cementing the role of specialty syringes in chronic-disease care. Over the forecast horizon, the chronic-disease driver will reinforce steady, predictable volume growth across high-income regions while accelerating adoption of premium designs in emerging markets.

Growth in Mass-Vaccination Programs

Post-pandemic health policy now institutionalizes large buffer inventories, evidenced by UNICEF’s purchase of 1 billion syringes that remain in stock for future campaigns. Gavi’s 2026-2030 roadmap earmarks USD 500 million for emergency immunization reserves, anchoring baseline demand for auto-disable devices that conform to WHO pre-qualification standards. Governments in Africa, Southeast Asia, and Latin America invest in local assembly lines to mitigate import dependence, presenting technology-transfer opportunities for established suppliers. Procurement models increasingly emphasize long-term framework agreements, stabilizing production schedules and enabling suppliers to leverage high-volume tooling. Standardized barrel volumes and luer-lock designs emerge as default specifications, further concentrating volume in dominant disposable categories. The driver’s medium-term influence translates into reliable replenishment cycles and incremental unit-price uplift for safety-engineered variants.

Self-Administration Trend & Dose Precision Demand

The push toward patient self-care underpins rapid adoption of autoinjectors, a device category forecast to reach USD 19.67 billion by 2028. Although autoinjectors coexist with syringes, they create derivative demand for pre-fillable cartridges that share material technologies with specialty syringes. Training gaps and user-interface complexity can trigger negative transfer effects, compelling device makers to refine ergonomic designs. Hybrid solutions that let patients transition between manual and automated modes are gaining favor, lifting requirements for modular syringe platforms. Early drug–device pairing encourages pharma firms to lock in syringe specifications during clinical phases, granting upstream suppliers longer revenue visibility. The driver’s impact resonates most in chronic therapies handled at home, where dose precision and user confidence outweigh marginal price differentials.

Regulatory Push for Safety & Smart Syringes

FDA warnings on non-compliant imports triggered hospital directives to replace suspect devices and stimulated a USD 40 million domestic expansion by BD focused on RFID-enabled prefilled formats for traceable waste management [2]BD, "BD and ten23 health partner to advance efficiency and quality in aseptic manufacturing with RFID-enabled prefillable syringes," bd.com. The 2026 harmonization of U.S. quality-system regulations with ISO 13485 obliges every market entrant to upgrade documentation, risk management, and post-market surveillance protocols. Compliance costs elevate barriers to entry, incentivizing healthcare providers to narrow vendor rosters toward certified suppliers. Smart syringes embed passive RFID tags that track usage and disposal, enabling data-driven waste-reduction programs that align with emerging extended-producer-responsibility statutes. As reimbursement models reward device safety, manufacturers recoup higher production costs through differentiated value propositions. The regulator-driven driver is most intense over the next two years while suppliers adjust processes and hospitals requalify inventories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of safety syringes | -0.9% | Global, cost sensitivity acute in emerging markets | Medium term (2-4 years) |

| Alternative drug-delivery technologies | -0.7% | North America and EU spearhead adoption | Long term (≥ 4 years) |

| Plastic-medical-waste compliance | -0.5% | Global, stricter enforcement in EU and North America | Medium term (2-4 years) |

| Borosilicate glass-tubing shortages | -0.4% | Global, supply concentrated among specialized manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Safety Syringes & Needlestick-Injury Concerns

Safety-engineered models retail at 2–3 times the price of conventional variants, making budget-constrained facilities reluctant to switch even when regulations recommend safer devices. Central-medical-store tenders in lower-middle-income countries line-item cost above long-term injury liabilities, delaying widespread adoption. Manufacturing scale and polymer automation are gradually compressing unit premiums, but price parity remains several years away for most low-income settings. Innovative procurement mechanisms that amortize device cost against potential litigation savings help reframe the value proposition. Suppliers offering clinical-outcome data and training bundles demonstrate total cost-of-ownership benefits, easing affordability barriers. Over the medium term, combined regulatory pressure and gradual cost convergence are expected to limit the restraint’s impact.

Alternative Drug-Delivery Technologies

Needle-free patches, smart insulin pumps, and dry-powder inhalers command attention as patient-centric options, especially in chronic disease management across North America and Europe. Yet molecular weight, viscosity, and stability constraints keep many biologic therapies injection-dependent. Comparative clinical data often show superior bioavailability for injectable routes, reinforcing syringe relevance. Nonetheless, large patient segments with injection aversion push payers to authorize alternative modalities where therapeutic equivalency exists. Syringe manufacturers hedge exposure by supplying primary containers for pump reservoirs and co-developing device combinations. Over the long term, the restraint will stay moderate because evolving biologic portfolios continue to favor parenteral administration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage: Disposables Drive Market Dominance

Disposable formats held 88.74% of syringes market share in 2025, underscoring infection-control imperatives and the logistical advantage of single-use inventory cycles. Hospital protocols standardized on disposable devices after evidence linked reusable barrels to cross-contamination risks, and the shift accelerated following FDA notices on sub-standard imports . Unit-cost economics favor disposables because high-volume molding amortizes tooling quickly, while central sterilization of reusables remains labor-intensive. BD’s domestic expansion alone will boost annual output by 600 million units, reinforcing the disposable supply backbone.

Reusable syringes now occupy niche roles such as veterinary surgeries and select low-resource settings where sterilization autoclaves are already in use. Even in those arenas, grant-funded upgrades to single-use devices are progressing as donors apply stricter safety metrics. Training materials, regulatory audits, and electronic inventory platforms increasingly presume disposable workflows. The result is a self-reinforcing cycle where suppliers prioritize disposable innovation and clinicians build familiarity with single-use protocols, further entrenching category leadership across the syringes market.

By Product Type: Specialized Solutions Gain Momentum

General-purpose devices retained 64.62% revenue share in 2025 by supplying routine injections, vaccine campaigns, and low-viscosity therapies. Specialized syringes—prefillable, safety-engineered, and low-dead-space models—are projected to post a 9.05% CAGR, the fastest among all product categories. The segment’s expansion mirrors pharma’s biologics investment, with GLP-1 agonists, mRNA therapeutics, and CAR-T infusions depending on high-precision containers. SCHOTT Pharma’s USD 371 million facility in North Carolina exemplifies capacity added to satisfy these advanced formats.

Specialized units command price premiums of 20-150% over commoditized barrels, cushioning suppliers from resin cost volatility. Device complexity, including built-in needle-safety sheaths and RFID tags, also creates intellectual-property moats. Contract manufacturers tailor plunger stoppers and silicone-oil coatings to each molecule, embedding suppliers deeper into pharma value chains. Consequently, specialized formats capture disproportionate value and shape the technology roadmap for the syringes market.

By Material: Plastic Dominance Amid Innovation

Plastic barrels secured 66.78% of the syringes market size in 2025 owing to automated injection-molding lines that drive down cost per unit and facilitate rapid design iterations. Demand for polypropylene and cyclic-olefin polymers (COP) is expanding at 9.08% CAGR as drug manufacturers sanction compatibility data that validate leachables and extractables profiles. Conversely, glass remains indispensable for oxygen-sensitive biologics, yet borosilicate supply constraints limit volume scalability in the near term. Gerresheimer’s launch of COP syringes for mRNA vaccines illustrates how polymer innovation addresses stability while bypassing glass bottlenecks.

Environmental considerations push the market toward recyclable resin grades and lower-mass designs. The trade-off centers on mechanical integrity: reduced wall thickness tightens dimensional tolerances, prompting investments in machine-vision inspection. Suppliers able to reconcile weight reduction with performance retain an edge as sustainability metrics gain procurement weight. As a result, plastic’s leadership in the syringes market will likely hold, even while material science diversifies to serve specialized pharmacology.

By End User: Home-Care Acceleration Reshapes Dynamics

Hospitals accounted for 53.76% of the syringes market size in 2025 thanks to centralized purchasing and high patient throughput. Yet home-care settings are forecast to grow at 9.12% CAGR as health systems shift chronic-disease management out of inpatient facilities. Patient self-injection protocols for diabetes, rheumatoid arthritis, and fertility treatments underpin the trend, and autoinjector packages reduce training time. SHL Medical cites double-digit demand growth for home-care-optimized devices that integrate ergonomic triggers and audible completion cues.

Healthcare payers encourage at-home therapy because it cuts per-episode costs by 20-30%, releasing funds for premium devices that improve adherence. Digital-health overlays—Bluetooth dose logging and smartphone reminders—ride on pre-fillable cartridges that share manufacturing lines with advanced syringes. Consequently, device makers blending mechanical precision with connected medicine platforms position themselves favorably for long-term volume gains in the syringes market.

By Application: Vaccination Growth Outpaces Traditional Leaders

Diabetes therapy maintained 36.45% of syringes market share in 2025 because insulin’s parenteral nature anchors daily injection regimens. Vaccination, however, is the fastest-expanding use-case at 9.02% CAGR as global health bodies intensify immunization schedules. WHO reports 14.5 million “zero-dose” children whose primary series remains incomplete, spurring catch-up campaigns that require high unit volumes. UNICEF’s open tenders for mpox vaccines through 2025 further underline demand persistence.

Other segments, including osteoarthritis viscosupplementation and aesthetic‐medicine injections, register mid-single-digit CAGRs but contribute lucrative margin pools. Botox administrations rely on ultra-fine needles embedded in prefilled units that present low-risk entry points for specialized suppliers. Application diversification thus balances portfolio risk and keeps the syringes market resilient even as any single therapy class faces competitive alternatives.

Geography Analysis

North America controlled 39.12% of syringes market revenue in 2025, propelled by high per-capita healthcare spending, early biologic adoption, and mandatory safety-device use in most clinical workflows. Domestic reshoring accelerates as BD upgrades multiple U.S. plants, adding capacity that cuts lead times by 40% and meets stricter FDA track-and-trace mandates. Federal funding incentives, tied to pandemic preparedness, further underwrite expansion of fill-finish infrastructure, ensuring downstream demand for specialized syringes.

Asia-Pacific delivers the fastest regional CAGR at 8.95%, underpinned by rapidly expanding middle-class populations and government healthcare reforms that subsidize chronic-disease medications. Japan and South Korea anchor high-value biologic fill-finish activities, while India and Vietnam absorb large volumes of commodity disposables for immunization programs. Regulatory scrutiny of Chinese plants—sparked by FDA quality alerts—drives multinational pharma to diversify toward ASEAN suppliers with higher compliance credentials. This diversification strategy redistributes orders and sets a higher baseline for regional quality expectations.

Europe retains a stronghold in specialized formats and eco-design leadership, buoyed by comprehensive reimbursement frameworks that reward safety and sustainability. Gerresheimer’s German production lines offer cyclo-olefin-polymer barrels that meet stringent EU recyclable-content thresholds, giving European buyers compliant options without switching material classes. Middle East and Africa, along with South America, represent emerging opportunity corridors where vaccination rollouts and improving hospital infrastructures drive steady syringe demand. Nevertheless, currency volatility and slower regulatory harmonization temper investment speed in those regions.

Mordor Intelligence provides coverage of the syringes market across other key regional markets, including Asia, Europe, and South America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The syringes market remains fragmented, with top five manufacturers capturing slightly more than one-third of global shipments, yet hundreds of regional firms compete on price within commodity tiers. BD, Terumo, and B. Braun leverage automation scale, integrated needle production, and proprietary safety mechanisms to defend share. Mid-size challengers exploit white spaces in low-dead-space, glass-replacement, and RFID-enabled products. FDA removal of non-compliant suppliers post-2024 effectively pruned fringe competitors and reshaped purchasing rosters.

Strategically, incumbents pursue vertical integration and strategic alliances that lock in material supply and accelerate device innovation. BD’s collaboration with ten23 health embeds RFID tags directly into prefillable formats, creating a differentiator that aligns with hospital waste-tracking mandates. SCHOTT Pharma’s U.S. greenfield site co-locates glass tubing pull lines with final container finishing, cutting logistics steps and improving lead-time agility. Supply-chain digitization, including blockchain lot tracking, is another arena where early movers gain procurement credit during hospital quality audits.

Emerging entrants concentrate on digital-health overlays and patient-centric ergonomics, but capital intensity and regulatory burdens slow scaling. Competitive intensity is expected to inch upward as biologic pipelines expand device complexity requirements, offering premium niches. However, the learning curve for advanced molding and glass-forming lines cements the advantage of established firms, keeping substitution risk moderate. The syringes market therefore exhibits balanced dynamics where scale, compliance, and technology interlock to create defensible moats.

Syringes Industry Leaders

-

Becton Dickinson and Company

-

B. Braun Melsungen AG

-

Hindustan Syringes & Medical Devices Limited

-

Gerresheimer AG

-

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BD announced an additional wave of investment in its U.S. manufacturing network to expand syringe, needle, and IV catheter capacity.

- July 2024: BD announced an additional wave of investment in its U.S. manufacturing network to expand syringe, needle, and IV catheter capacity.

- March 2024: Hindustan Syringes & Medical Devices introduced Dispojekt single-use syringes in India.

- March 2024: BD accelerated U.S. output after the FDA cautioned against using plastic syringes sourced from select Chinese factories.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global syringe market as the annual value generated from new, factory-sterilized devices, reusable and disposable, that deliver or extract fluids in human healthcare, including conventional, safety-engineered, and prefilled formats. Drug-specific variants such as insulin, vaccination, and aesthetic syringes sit inside this frame, and revenue is captured at ex-factory average selling price before distributor mark-ups.

Scope Exclusions: Veterinary, micro-analytical, and laboratory automation syringes are excluded to avoid inflating the clinical demand pool.

Segmentation Overview

-

By Usage

- Reusable Syringes

- Disposable Syringes

-

By Product Type

- General Purpose

- Specialized

-

By Material

- Glass

- Plastic

- Others

-

By End User

- Hospitals

- Ambulatory Surgery Centers

- Home-care

- Others

-

By Application

- Diabetes

- Vaccination & Immunization

- Botox / Aesthetic

- Osteoarthritis

- Human Growth Hormone

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement heads at public hospitals in the United States, Germany, India, and Brazil, along with contract manufacturers in Asia and infection-control experts. These conversations clarified real purchase prices, safety-syringe adoption curves, and the seasonality of vaccination drives, filling gaps left by desk work.

Desk Research

We began by mapping supply using public customs records, UN Comtrade export codes 901831 and 901832, and production filings from the US FDA 510(k) database, which reveal unit flows and price brackets across major manufacturing hubs. Epidemiological datasets from WHO's Immunization Monitoring, the International Diabetes Federation Atlas, and OECD surgical volumes helped approximate use-rate fingerprints by application. Additional depth came from trade-body white papers, such as the International Pharmaceutical Federation, and company 10-Ks that disclose syringe or injector lines. Proprietary screens on D&B Hoovers and Dow Jones Factiva then supplied plant capacities and recent capacity expansions. This list is illustrative; many other open sources were tapped for cross-checks and context.

Market-Sizing & Forecasting

Top-down "demand pool" modeling starts with procedure counts (immunizations, insulin injections, inpatient IV pushes, aesthetic treatments) multiplied by verified average needles-per-procedure. Outputs are pressure-tested with bottom-up roll-ups from sampled supplier revenue and channel checks, after which volumes convert to value through regional ASP bands. Key variables embedded in the multivariate regression forecast include diabetes prevalence growth, national immunization budgets, elective surgery backlogs, safety-mandate implementation timelines, and plastic resin price trends. Where supplier data are sparse, we impute volumes using export share ratios and validate against customs tallies.

Data Validation & Update Cycle

Every model run passes a three-layer review: automated variance scans, peer review by a senior analyst, and final sign-off from the sector lead. We refresh the dataset annually and trigger interim revisions when material events, regulatory bans, pandemics, or major plant fires shift the baseline. A last-minute sense check is completed before client delivery.

Why Mordor's Syringe Market Baseline Earns Decision Maker Confidence

Published estimates often diverge because firms choose different device scopes, currency bases, or refresh cadences.

Key gap drivers include whether safety-engineered units are folded into totals, how aggressively future vaccination rounds are priced, and the cadence at which currency translations are updated. Mordor reports current-year values and uses mixed top-down plus supplier roll-ups, while some peers rely on single-factor extrapolations or subset segments only.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.96 B (2025) | Mordor Intelligence | - |

| USD 17.50 B (2023) | Regional Consultancy A | Older base year and limited country weighting |

| USD 24.59 B (2024) | Industry Data Hub B | Omits safety syringes and applies single exchange-rate snapshot |

| USD 7.10 B (2024) | Global Publisher C | Reports only prefilled segment, not full market |

The contrast shows that Mordor's balanced scope, mixed-method modeling, and annual refresh deliver a dependable, clearly traceable baseline that buyers can rely on for budgeting and strategic planning.

Key Questions Answered in the Report

What is the current size of the syringes market?

The syringes market stands at USD 21.59 billion in 2026 and is projected to reach USD 31.94 billion by 2031.

Which region is growing the fastest in the syringes market?

Asia-Pacific records the highest CAGR at 8.95% through 2031 due to expanding healthcare access and chronic-disease prevalence.

Why are disposable syringes dominant?

They capture 88.74% market share because single-use protocols reduce infection risk and align with streamlined hospital workflows.

What segment shows the strongest growth potential?

Specialized syringes, including prefillable and low-dead-space designs, are set for a 9.05% CAGR as biologics pipelines expand.

How are regulations shaping market dynamics?

ISO 13485 alignment and FDA quality enforcement increase compliance costs, favoring manufacturers with robust domestic production and advanced safety features.

What technologies are influencing future syringe designs?

RFID tagging for waste traceability, low-dead-space barrels for cell and gene therapies, and recyclable polymer materials are key innovation areas driving next-generation products.

Page last updated on: