Flea And Tick Product Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

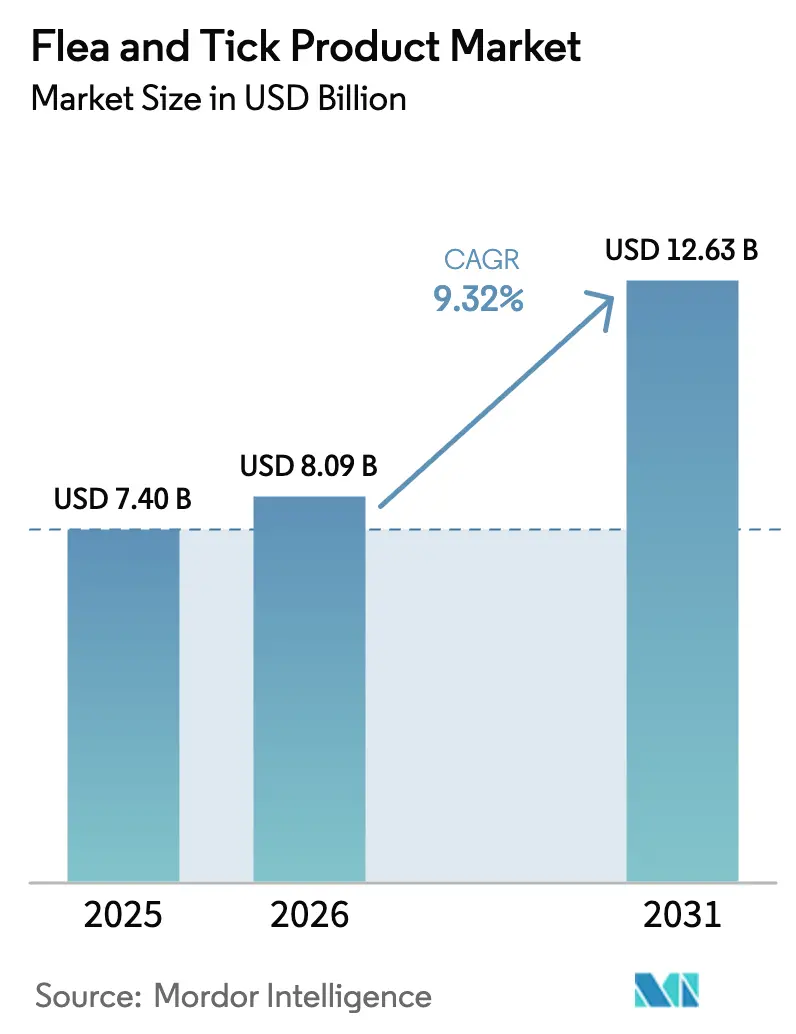

| Market Size (2026) | USD 8.09 Billion |

| Market Size (2031) | USD 12.63 Billion |

| Growth Rate (2026 - 2031) | 9.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flea And Tick Product Market Analysis by Mordor Intelligence

The flea and tick product market size is expected to grow from USD 7.40 billion in 2025 to USD 8.09 billion in 2026 and is forecast to reach USD 12.63 billion by 2031 at 9.32% CAGR over 2026-2031. Robust urban pet ownership, higher vector-borne disease incidence, and the growing appeal of long-acting combination formulations collectively accelerate growth across every major region. Heightened media coverage of zoonotic risks, especially Lyme disease, spurs preventive spending, while e-commerce auto-ship programs raise adherence and widen rural access.[1]Centers for Disease Control and Prevention, “Lyme Disease Data and Surveillance,” cdc.gov Competitive intensity rises as incumbents defend isoxazoline franchises against natural-product entrants, even as regulators fast-track 6- to 12-month options that tackle fleas, ticks, heartworm, and intestinal parasites in a single dose. Manufacturers also leverage subscription pricing and breed-specific palatability formats to retain customers. On the downside, acaricide resistance, safety-label revisions, and counterfeit items threaten both confidence and future revenue trajectories.[2]Merck Animal Health, “2025 Global Parasitology Survey,” merck-animal-health.com

Key Report Takeaways

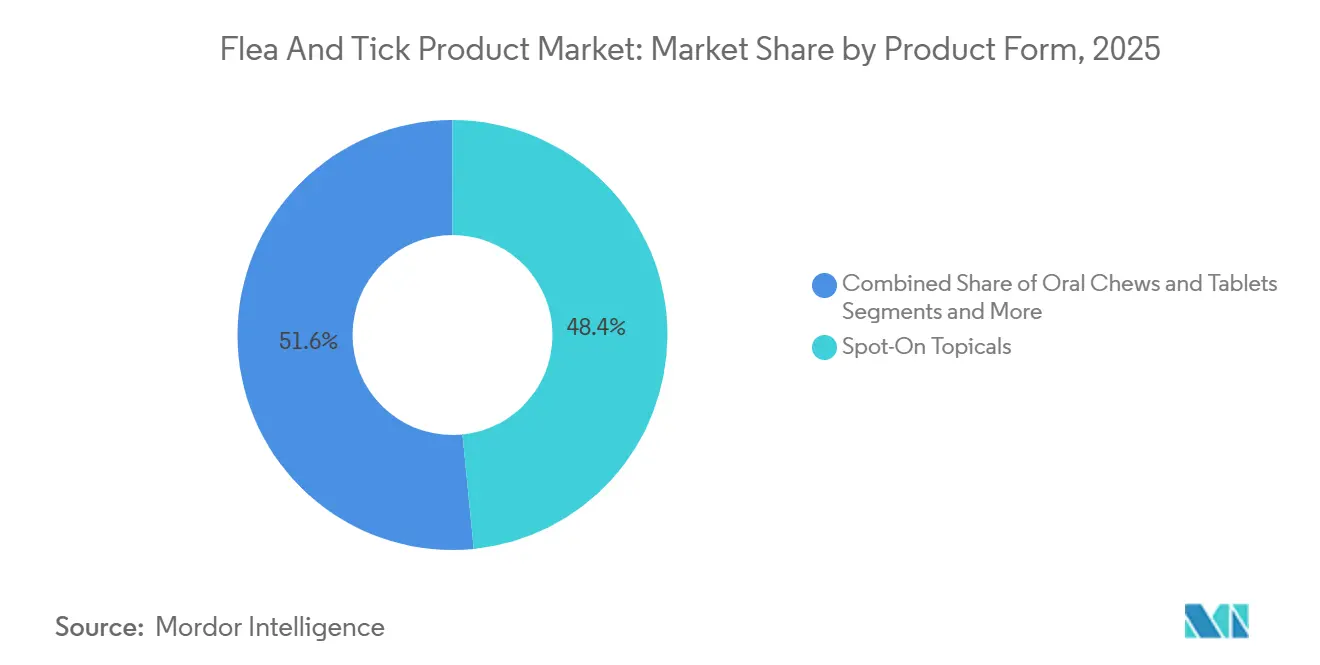

- By product form, spot-on topicals led with 48.42% of flea and tick products market share in 2025, whereas oral chews and tablets are forecast to expand at a 10.49% CAGR through 2031.

- By animal, dogs represented 58.87% of 2025 revenue, while the cat segment is poised to grow at a 10.44% CAGR through 2031.

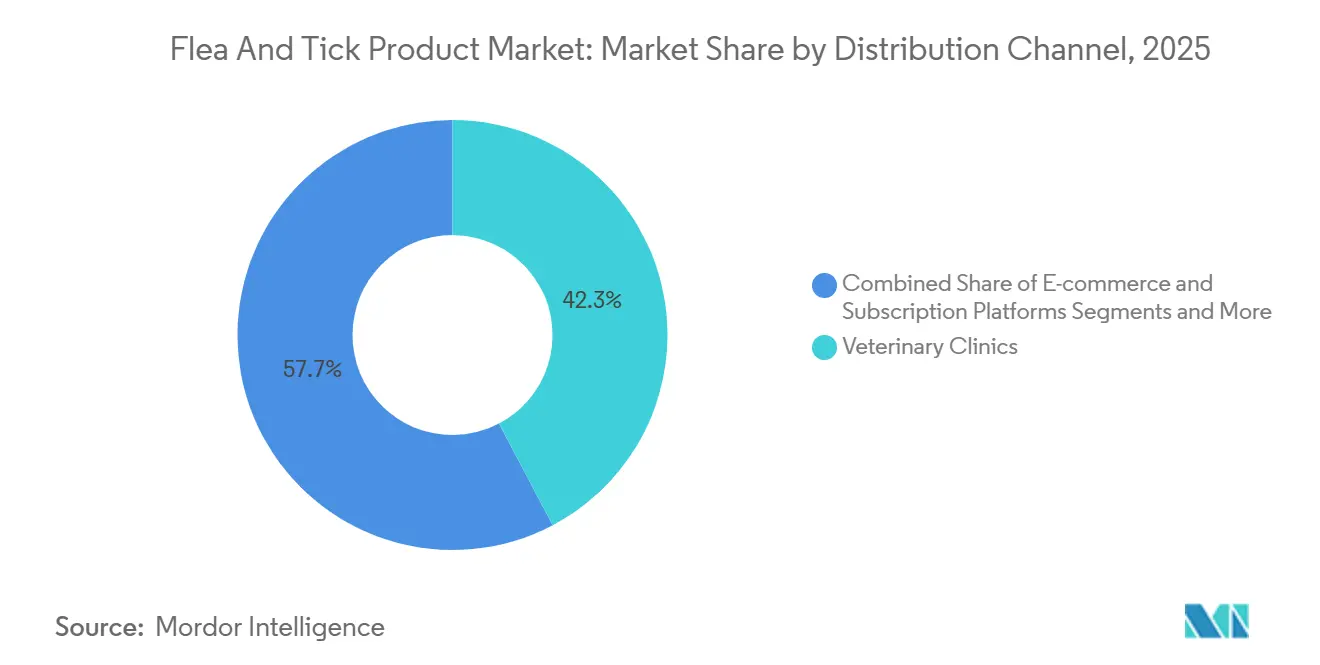

- By distribution channel, veterinary clinics held 42.29% of the flea and tick products market size in 2025, yet e-commerce and subscription platforms carry the fastest projected CAGR at 10.39% to 2031.

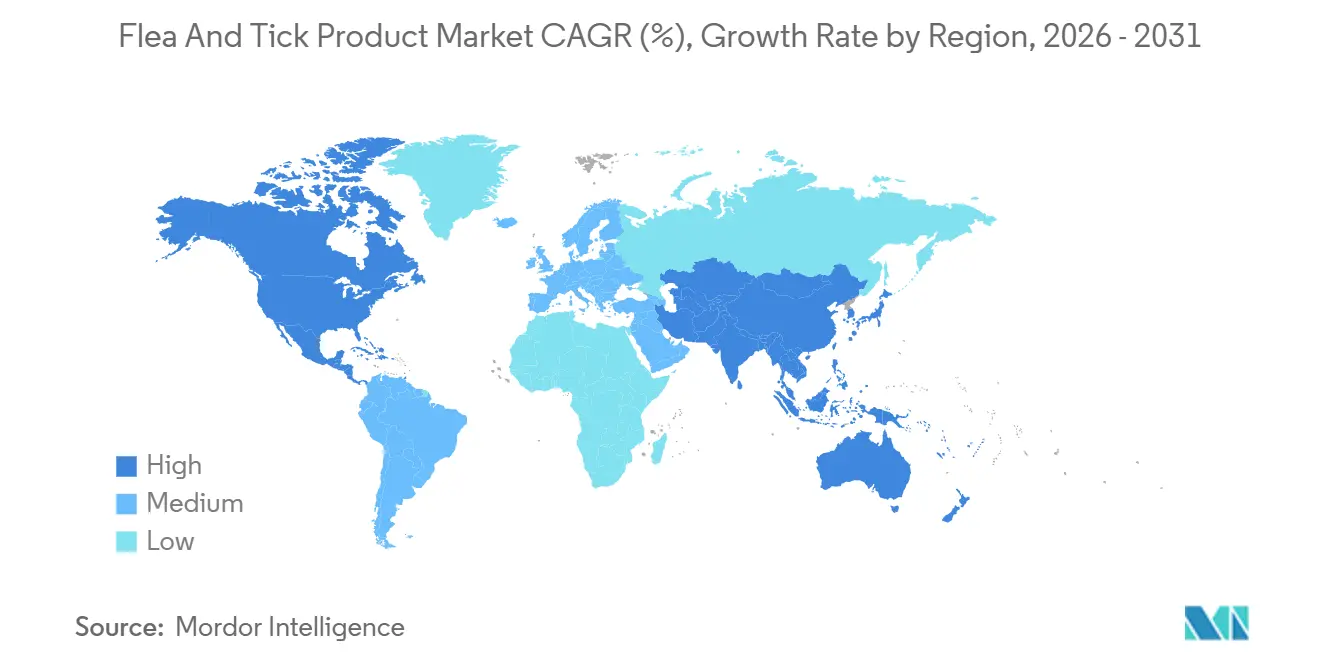

- By geography, North America captured 41.98% of 2025 revenue, whereas Asia-Pacific is the quickest-growing region at a 10.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flea And Tick Product Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of flea- and tick-borne diseases in pets | +2.1% | Global, with acute pressure in North America (Lyme endemic zones) and Europe (Mediterranean spotted fever regions) | Medium term (2-4 years) |

| Increasing pet adoption and humanization trend | +2.5% | Global, led by Asia-Pacific urban centers (China, India) and Latin America (Brazil, Argentina) | Long term (≥ 4 years) |

| Growing owner awareness of zoonotic risks | +1.4% | North America and Europe, spillover to APAC metropolitan areas | Short term (≤ 2 years) |

| Tele-health and e-commerce subscriptions expand access | +1.8% | North America and Europe core, early adoption in APAC (Japan, South Korea) | Medium term (2-4 years) |

| Regulatory push for long-duration combo formulations | +0.9% | Global, with FDA and EMA as primary drivers | Long term (≥ 4 years) |

| Climate-driven expansion of tick habitats | +0.6% | North America (Canada), Northern Europe, temperate Asia-Pacific zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Flea- and Tick-Borne Diseases in Pets

CDC surveillance logged 89,000 Lyme disease cases in 2023, 68.5% above the 2017-2019 baseline, while veterinary laboratories report Ehrlichia and Anaplasma positivity exceeding 5% in 15 U.S. states. Rising Babesia gibsoni detection in Japanese and South Korean dogs further widens the prophylaxis addressable base. Treatment outlays ranging from USD 500 to USD 2,000 per canine case contrast with annual preventive costs near USD 300, prompting owners to view year-round regimens as a cost-saving necessity. The resulting demand uptick directly underpins current double-digit expansion of oral, long-duration options.[3]World Health Organization, “Vector-Borne Diseases Fact Sheet,” who.int

Increasing Pet Adoption and Humanization Trend

The American Pet Products Association documented pet ownership in 66% of U.S. households in 2024, up 10 percentage points versus 2019. China reached 120.75 million companion animals in 2023, while India’s pet sector is set to hit USD 24.8 billion by 2032 on a 20% CAGR. Owners increasingly select premium combination chewables - exemplified by Simparica Trio and NexGard Plus - to bundle flea, tick, heartworm, and intestinal parasite control into one monthly dose. Growing pet insurance eligibility for preventive care in the U.K. and Scandinavia also nudges compliance.

Growing Owner Awareness of Zoonotic Risks

The WHO’s 2024 vector-borne disease bulletin states that 17% of infectious illnesses are vector-transmitted. After a 2024 three-fatality Powassan virus cluster in the U.S. Northeast, media reports spiked veterinary inquiries about year-round protection. Safety advisories on isoxazolines, updated in 2024, pushed manufacturers to refine labeling and bolster veterinarian training, maintaining product confidence despite social-media amplification of adverse-event anecdotes. The net result is rising demand among owners who prioritize both efficacy and documented safety.

Tele-Health and E-Commerce Subscriptions Expand Access

Amazon’s May 2025 prescription launch allows owners to upload veterinary-verified scripts and receive same-day delivery, accelerating digital adoption. Chewy’s pharmacy arm neared USD 1 billion in fiscal 2023, driven by auto-ship adherence rates of 89% versus 62% for one-off purchases. California’s AB 1399 and Arizona’s ARS 32-2240.03 permit 14-day tele-Rx supplies, gently eroding clinic gatekeeping. In India, tele-veterinary startups mitigate the 1:5,000 veterinarian-to-pet ratio, thereby unlocking demand in cities such as Mumbai and Bengaluru.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event and safety concerns with chemicals | -1.2% | Global, with heightened scrutiny in North America and EU due to FDA/EMA pharmacovigilance | Short term (≤ 2 years) |

| Counterfeit and sub-standard products in grey market | -0.7% | Asia-Pacific (China, India), Latin America (Brazil), and e-commerce channels globally | Medium term (2-4 years) |

| Emerging acaricide resistance in tick populations | -0.5% | Global, with documented cases in Mediterranean Europe, southern US, and Australia | Long term (≥ 4 years) |

| Tightening EU eco-toxicology regulations on actives | -0.4% | European Union, with spillover to UK and Switzerland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event and Safety Concerns with Chemicals

The FDA’s updated 2024 alert on isoxazolines details neurologic events in a small subset of pets, recommending caution for animals with seizure histories. The EMA’s pharmacovigilance panel reviewed 1,200 Bravecto reports and reaffirmed a positive benefit-risk ratio while advising closer veterinarian guidance. Social-media groups spotlight anecdotal cases, pushing a minority of owners toward botanical choices such as cedar-oil sprays from Wondercide, which posted 40% revenue growth in 2024.

Emerging Acaricide Resistance in Tick Populations

Studies confirm permethrin resistance in Rhipicephalus sanguineus across Mediterranean Europe and the southern United States. French and German Ixodes ricinus populations show 3- to 5-fold higher fipronil LC50 values. As no global monitoring network for companion-animal tick resistance exists, early-stage detection remains fragmented, potentially limiting the lifetime of both legacy and new actives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Oral Adoption Accelerates

Oral chews and tablets are slated for a 10.49% CAGR, the quickest within the flea and tick products market, as FDA-approved Simparica Trio and NexGard Plus add heartworm and intestinal parasite coverage in a single monthly chew. Spot-on topicals still held 48.42% of 2025 revenue, but their share is eroding as owners prefer mess-free systemic options. Collars capture an 8-month window of efficacy yet face environmental scrutiny over neonicotinoid residues. Sprays, powders, and shampoos account for <10% combined, confined to shelter and kennel usage. Bravecto Quantum’s 12-month injectable model exemplifies the shift toward ultra-long-duration solutions, eliminating monthly owner reminders and bolstering adherence documented as low as 45% among non-subscription users.

Consumer preference for flavored chewables also lifts palatability R&D, with beef, chicken, and fish variants tailored to breed size. Systemic delivery avoids dermal irritation, a frequent pyrethroid complaint, reinforcing oral dominance within the flea and tick products market.

By Animal: Cat Segment Closes the Gap

Dogs contributed 58.87% of 2025 revenue, yet the cat segment will expand at a 10.44% CAGR through 2031 on the back of Credelio CAT’s U.S. emergency authorization and Bravecto TriUNO’s EU approval. Historical feline under-representation stemmed from pyrethroid toxicity and smaller wallet share, but rising urban cat ownership—73.8 million in the United States—now justifies targeted R&D. Future pipelines prioritize feline combination chewables that integrate flea, tick, and heartworm control, narrowing a long-standing therapeutic gap.

Other companion species remain niche, accounting for <5% revenue. Ferret and rabbit treatments rely on off-label dosing of canine products, creating veterinary liability hurdles. Equine ectoparasite prevention centers on spray formulations and feed-through larvicides distinct from companion-animal segments.

By Distribution Channel: Digital Disruption Holds

Veterinary clinics retained 42.29% of 2025 revenue within the flea and tick products market, yet e-commerce and subscription portals deliver the steepest 10.39% CAGR through 2031. Amazon’s script upload function and Chewy’s auto-ship model illustrate how digital channels erode the traditional Veterinary-Client-Patient Relationship barrier. U.S. state tele-health rules now permit short-term prescriptions online, allowing refill capture after an initial clinic visit. Retail pet chains and human pharmacies cater to cost-sensitive owners via OTC fipronil and permethrin products, but their single-active coverage limits uptake among multi-pet households seeking comprehensive protection. Subscription adherence gains of 27 percentage points over single-purchase cohorts translate into measurably lower parasite incidence.

Geography Analysis

North America commanded 41.98% of 2025 revenue, anchored by USD 200 – USD 400 annual per-pet preventive spending and an entrenched clinic network. Continued vector-borne disease growth sustains demand, especially as Ixodes scapularis pushes into Canada’s southern provinces. Europe follows at 28%, yet faces emerging eco-toxicology regulations that may limit fipronil and permethrin usage.

Asia-Pacific posts the fastest 10.54% CAGR through 2031 owing to China’s expanding urban pet base and India’s rapid 20% sector CAGR. Slower regulatory approvals can extend launch cycles by up to 36 months, affording local generics an interim share. South America and the Middle East & Africa jointly deliver under 15% but hold headroom as veterinary infrastructure improves; the African Medicines Agency, founded 2024, intends to streamline approvals across 55 member states.

Competitive Landscape

Zoetis, Elanco, and Boehringer Ingelheim collectively capture an estimated 55 – 60% of 2025 revenue, cementing a moderately concentrated arena. Zoetis’ Simparica Trio logged double-digit gains, pushing companion-animal sales to USD 2.37 billion in Q3 2024. Elanco continues to rationalize its Seresto collar acquisition while absorbing litigation costs tied to imidacloprid residue claims. Merck’s Bravecto franchise broadened with a 12-month injectable that directly addresses documented owner non-adherence.

Natural-product challengers such as Wondercide exploit chemical-averse segments, albeit with limited field efficacy data. Retail-oriented PetIQ undercuts prescription brands on price via Walmart and Amazon, yet its single-active formulas lack multi-parasite reach. Innovation pipelines point to transdermal patches and IoT-enabled collars that pair GPS tracking with dosing alerts, indicating rising tech convergence inside the flea and tick products industry.

Flea And Tick Product Industry Leaders

Ceva

Elanco

Virbac

Boehringer Ingelheim

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Merck Animal Health obtained FDA clearance for Bravecto Quantum, a 12-month injectable fluralaner product.

- May 2025: Amazon began pet prescription fulfillment through Prime, broadening e-commerce penetration.

- May 2025: The EMA issued a positive opinion for Fluralaner Intervet, a 6-month oral targeting 90 million EU dogs.

- October 2024: Boehringer Ingelheim earned EU approval for Bravecto TriUNO, a quarterly feline combination tablet.

Global Flea And Tick Product Market Report Scope

As per the scope of this report, flea and tick products refer to various chemicals, drugs, and equipment that prevent the infestation of fleas and ticks in animals and cure the diseases caused by those parasites.

The flea and tick product market is segmented by product, animal, and geography. By product, the market is segmented as oral pill, spray, spot-on, powder, shampoo, collar, and other products. By animal, the market is segmented as dogs, cats, and other animals. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Oral Chews and Tablets |

| Spot-On Topicals |

| Sprays & Mists |

| Collars |

| Shampoos & Dips |

| Powders & Dusts |

| Others |

| Dogs |

| Cats |

| Other Animals |

| Veterinary Clinics |

| Retail Pet Stores & Pharmacies |

| E-commerce and Subscription Platforms |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Form | Oral Chews and Tablets | |

| Spot-On Topicals | ||

| Sprays & Mists | ||

| Collars | ||

| Shampoos & Dips | ||

| Powders & Dusts | ||

| Others | ||

| By Animal | Dogs | |

| Cats | ||

| Other Animals | ||

| By Distribution Channel | Veterinary Clinics | |

| Retail Pet Stores & Pharmacies | ||

| E-commerce and Subscription Platforms | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the flea and tick products market?

The flea and tick products market size totals USD 8.09 billion in 2026.

Which product form is growing the fastest?

Oral chews and tablets are projected to post a 10.49% CAGR through 2031, outpacing all other forms.

Why is Asia-Pacific the fastest-growing region?

Rising urban pet ownership in China and India, plus improving veterinary access, drive a 10.54% regional CAGR.

How are e-commerce platforms affecting sales?

Amazon and Chewy auto-ship programs lift adherence to 89%, fueling the channel’s 10.39% CAGR to 2031.

Which companies lead the competitive landscape?

Zoetis, Elanco, and Boehringer Ingelheim collectively hold about 55 – 60% of global revenue.

What long-acting innovation recently entered the market?

Bravecto Quantum, a 12-month injectable fluralaner solution, gained FDA approval in July 2025.

Page last updated on: