Market Overview

| Study Period | 2021 - 2031 |

|---|---|

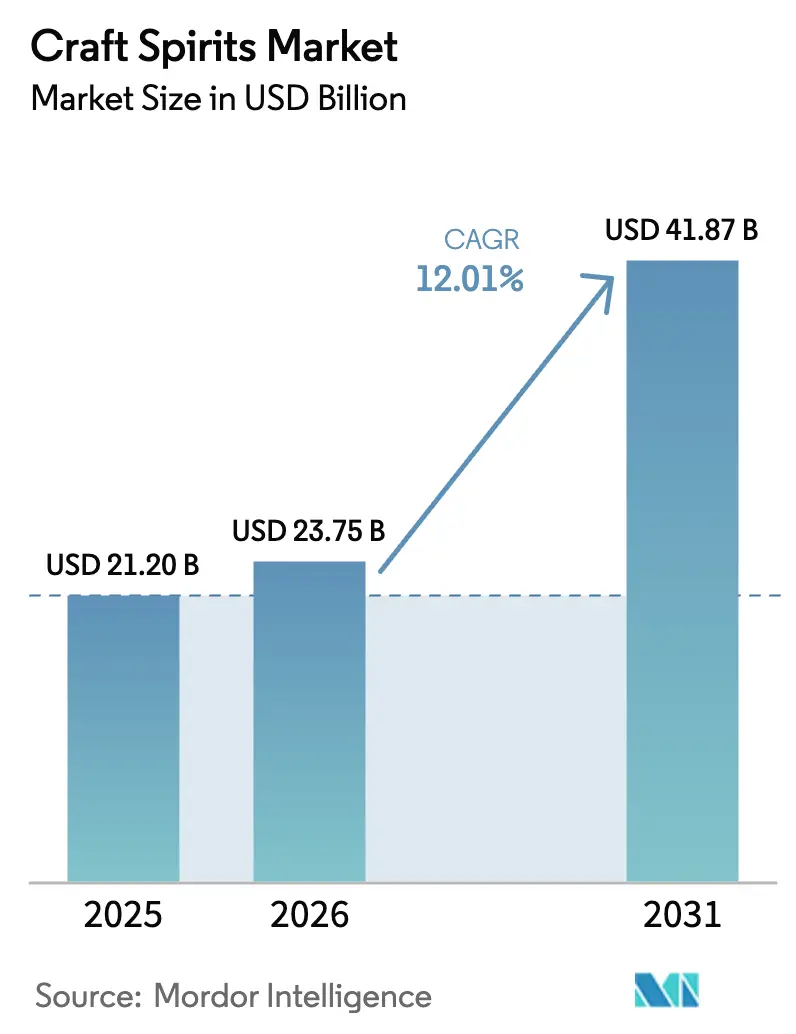

| Market Size (2026) | USD 23.75 Billion |

| Market Size (2031) | USD 41.87 Billion |

| Growth Rate (2026 - 2031) | 12.01% CAGR |

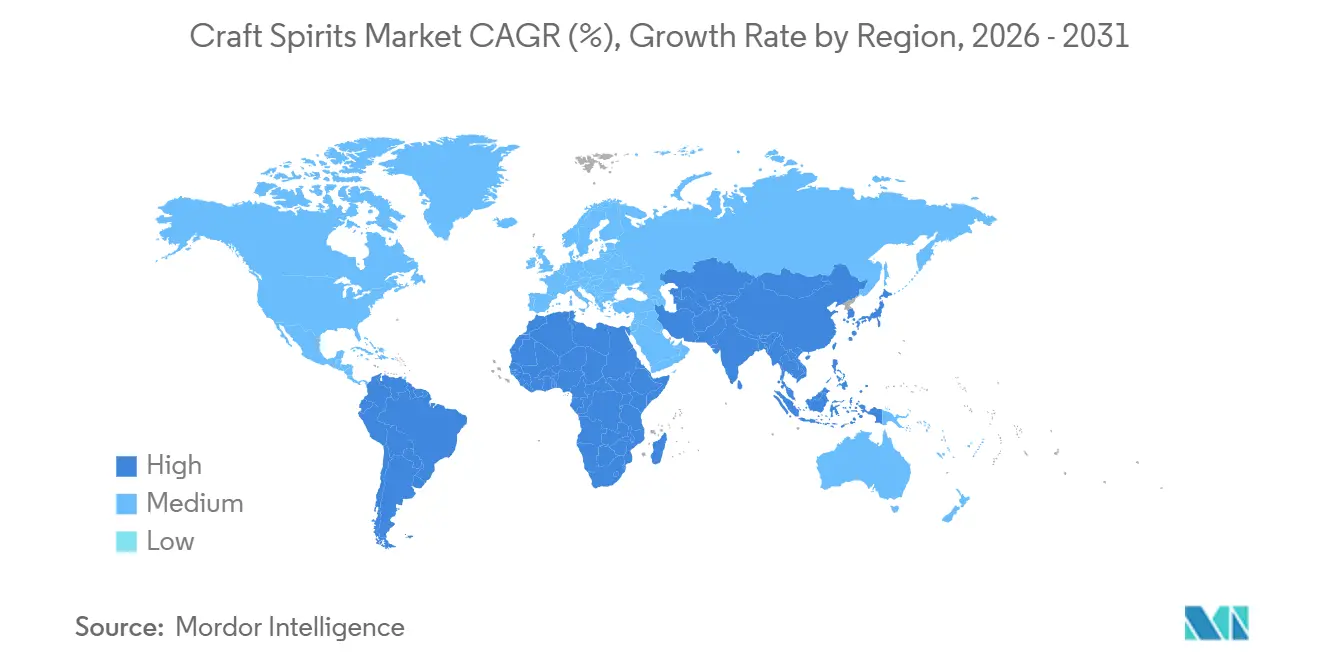

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Craft Spirits Market Analysis by Mordor Intelligence

The Craft Spirits Market size is projected to expand from USD 21.20 billion in 2025 and USD 23.75 billion in 2026 to USD 41.87 billion by 2031, registering a CAGR of 12.01% between 2026 to 2031. This growth is driven by changing consumer tastes, new distribution methods, and a growing interest in artisanal products. Whiskey remains the top segment in the market, supported by its global popularity and the trend of premiumization. Craft producers are focusing on creating aged and small-batch whiskey offerings. Gin is growing quickly, especially with its botanical-infused and locally inspired varieties that appeal to younger consumers. Grain-based spirits dominate the market due to their flexibility and traditional uses, while fruit-based spirits are gaining popularity for their regional flavors and sustainable production methods. In terms of distribution, on-trade channels like bars and restaurants generate significant revenue through tasting events and craft cocktails. At the same time, off-trade sales are increasing through convenience stores and direct-to-consumer platforms. North America leads the market, thanks to its established craft ecosystem and supportive regulations for small producers. Europe is also showing strong growth potential, driven by renewed interest in artisanal distilling, government support, and rising demand for local premium spirits.

Key Report Takeaways

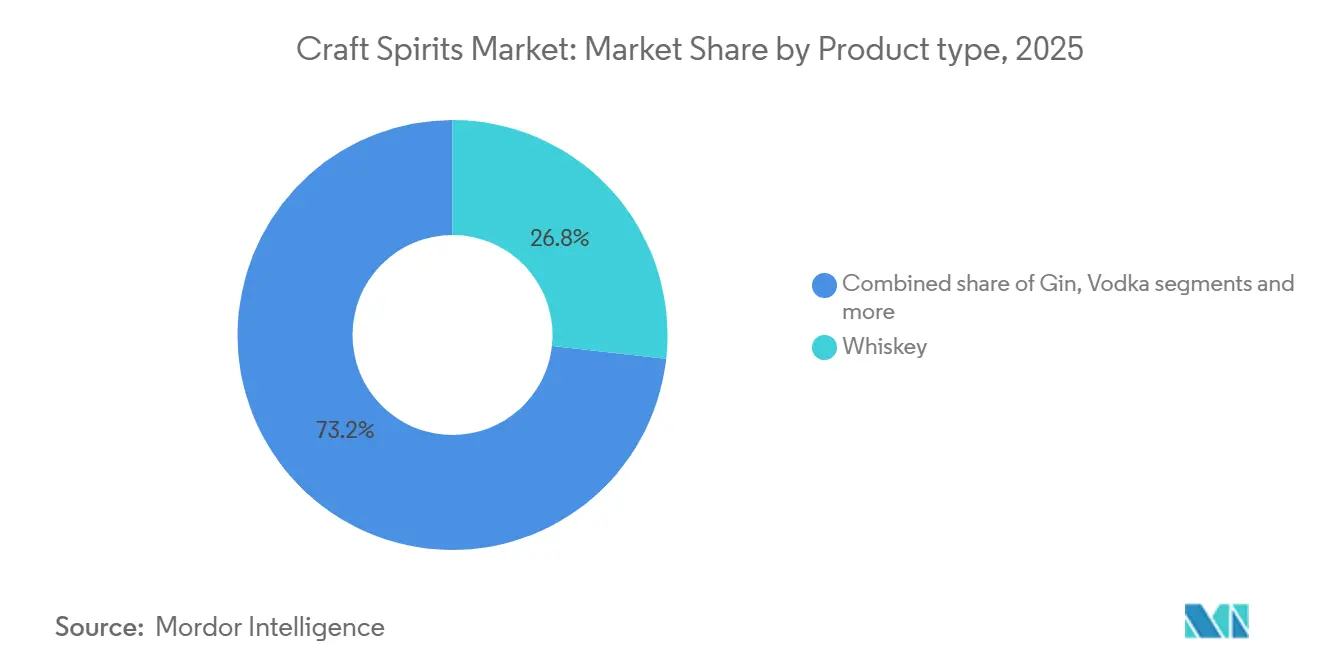

- By product type, whiskey led with 26.77% of craft spirits market share in 2025, whereas gin is projected to grow at a 12.25% CAGR to 2031.

- By ingredient, grain-based formulations held 62.88% share of the craft spirits market size in 2025; fruit-based spirits are forecast to expand at a 12.43% CAGR to 2031.

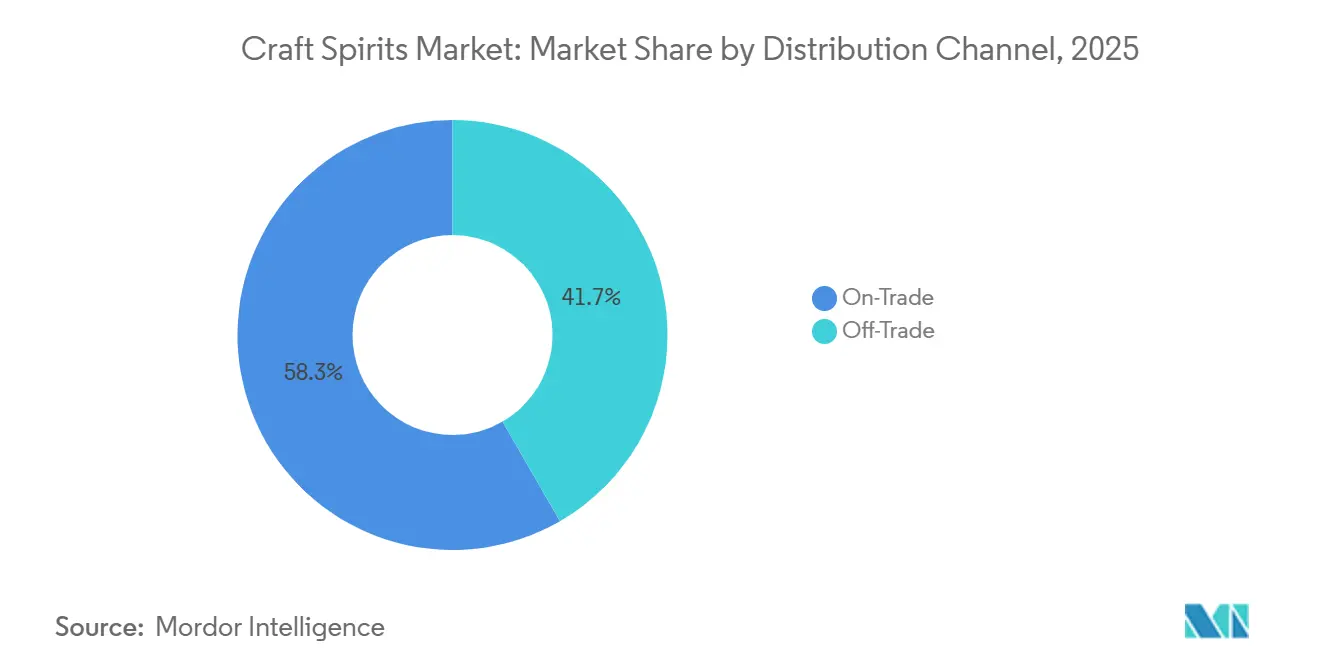

- By distribution channel, the on-trade segment accounted for 58.34% revenue in 2025; off-trade is poised for an 11.95% CAGR through 2031.

- By geography, North America commanded 38.75% of the craft spirits market size in 2025, while Europe is projected to post the fastest 12.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Craft Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of microbreweries propelling the demand for craft spirits | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Product differentiation in terms of ingredients and alcohol content | +2.5% | Global, with early adoption in premium markets | Medium term (2-4 years) |

| Surge in demand for premium alcoholic beverages | +3.8% | Global, particularly strong in North America, Europe, and emerging Asian markets | Long term (≥ 4 years) |

| Increasing preference for innovative flavors | +2.1% | Global, with strongest impact in urban centers | Short term (≤ 2 years) |

| Growth of cocktail culture and mixology | +1.9% | Global, with highest concentration in urban markets and hospitality hubs | Medium term (2-4 years) |

| Tourism and experiential marketing | +1.4% | Global, particularly strong in tourism-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Microbreweries Propelling the Demand for Craft Spirits

The growth of microbreweries has established a strong foundation for craft spirits development, as many beer producers have expanded into distillation operations. According to the American Craft Spirits Association, the number of active craft distillers in the United States reached 3,069 by 2024, showing an 11.5% increase despite challenging market conditions. States such as California, New York, Pennsylvania, Texas, and Washington have emerged as major centers for craft production [1]Source: American Craft Spirits Association (ACSA), "Craft Spirits Data Project", americancraftspirits.org. Micro-distilleries are now using fruit fermentation to create unique vodka bases, combining skills from craft brewing and distilling. Improved production capabilities have enabled these producers to offer small-batch and limited-edition products, increasing consumer interest and expanding the market. This trend is expected to continue until 2031.

Product Diffrentiation in Terms of Ingredients And Alcohol Content

Craft distillers are using product differentiation as a key strategy by incorporating unique ingredients and offering varied alcohol content levels. This approach helps them create distinct market positions and attract specific consumer groups. The market is expanding its alcohol content options, as seen in April 2024 when Barrell Craft Spirits launched its first Full Proof Bourbon at 123 proof (61.5% ABV) to meet the demand for stronger flavor profiles. Additionally, the low and no-alcohol spirits segment is growing rapidly. Leading companies like Heineken are planning to achieve a 90% market share in zero-alcohol options by 2025. This strategy addresses the rising demand from health-conscious consumers and changing drinking habits. These trends highlight the industry's focus on meeting diverse consumer preferences.

Surge in Demand for Premium Alcoholic Beverages

The spirits market is growing rapidly due to rising demand for premium alcoholic drinks that highlight quality, authenticity, and brand heritage. Higher disposable incomes and urbanization have encouraged consumers to spend more on luxury spirits, with whiskey, especially Scotch, leading the way. Companies like Diageo and Pernod Ricard have expanded their premium Scotch offerings to meet this demand. The revival of international travel and social events has boosted Scotch exports through duty-free and gifting channels. Scotch whisky holds a strong market share in Asia, North America, and Europe, supported by effective marketing, unique brand experiences, and increasing e-commerce sales. According to the Scotch Whisky Association, the Asia Pacific region held the largest share of Scotch whiskey exports worldwide in 2024, accounting for 29.1% of the export market [2]Source: The Scotch Whisky Association, "Scotch Whisky industry records £5.4bn global exports in 2024, amid 'Turbulent' Global Trading Conditions", scotch-whisky.org.uk.

Increasing Preference For Innovative Flavors

As consumers increasingly seek out innovative flavor experiences, the craft spirits industry is undergoing a significant transformation. In response to this shift, manufacturers are rolling out sophisticated product developments. A prime example is Diageo's introduction of the Smirnoff Spicy Tamarind. Meanwhile, craft distillers are setting themselves apart in a crowded market by infusing botanicals like tahini and white pepper. A growing trend in the industry sees players harnessing local botanicals and fruits, crafting regional variations that resonate with both local and global audiences. A case in point: in August 2024, Johnnie Walker Blue Label unveiled its Elusive Umami variant in India, seamlessly blending umami notes from Japanese cuisine into its Scotch whisky.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -1.8% | Global, with highest impact in highly regulated markets like India and Nordic countries | Long term (≥ 4 years) |

| Consumers' inclination toward low/no-alcohol spirits | -0.9% | Global, particularly strong in North America and Western Europe | Medium term (2-4 years) |

| Supply chain disruptions affecting equipment and packaging | -1.2% | Global, with highest impact in import-dependent regions | Short term (≤ 2 years) |

| Premium pricing of craft spirits faces resistance from price-sensitive consumers | -1.5% | Global, particularly pronounced in emerging markets and during economic downturns | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations

The craft spirits industry faces complex regulatory challenges that affect market entry and growth. In the U.S., the three-tier distribution system remains a major hurdle for small producers, though recent changes in regulations have created new opportunities. Despite 85% of craft spirits consumers wanting easier access, only nine states and D.C. currently allow direct-to-consumer (D2C) spirits shipping (Crafted ERP). Trade disputes add further complications, with the U.S. reintroducing steel and aluminum tariffs in Q1 2025, which may lead to a 50% EU tariff on American whiskey, impacting exports (The Whiskey Lab). Additionally, the Tobacco Tax and Trade Bureau (TTB) plans to introduce mandatory "Alcohol Facts" labels. While this will improve transparency for consumers, it will also increase compliance costs for craft producers.

Consumers Inclination Towards low/no Alcohol Spirits

The demand for low-alcohol and alcohol-free beverages is growing, reshaping the craft spirits market with both challenges and opportunities. Diageo's "Distilled 2025" report highlights "zebra striping," where consumers alternate between alcoholic and non-alcoholic drinks at social events. This trend shows a shift as more traditional spirits consumers explore alcohol-free options. Generation Z is at the forefront, focusing on mindful drinking and healthier lifestyles. Changes like the U.S. Surgeon General's warning on alcohol-cancer risks and Ireland's new labeling laws have influenced choices, leading to a 1% drop in traditional alcohol sales in 2024. While this shift challenges traditional craft spirits makers, it also sparks innovation. Craft distillers are responding by creating high-quality non-alcoholic alternatives that retain the elegance and traditions of classic spirits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whiskey Dominates While Gin Accelerates

In 2025, whiskey commands a dominant 26.77% share of the craft spirits market, buoyed by a consumer shift towards premium offerings and a nod to traditional production methods. However, this category grapples with challenges stemming from oversupply, leading to pricing pressures and inventory management dilemmas. In May 2025, Radico made a strategic move, unveiling TRIKAL Indian Single Malt and Morpheus Super Premium Whisky, aiming squarely at the luxury and super-premium segments.

Gin is poised for the most significant growth, projected to achieve a CAGR of 12.25% from 2026 to 2031. This surge is largely attributed to innovative flavor developments and regional adaptations. Distillers in numerous countries are harnessing local botanicals, crafting unique products tailored for both domestic and global markets. Vodka remains a staple segment, with craft producers innovating through fruit fermentation to craft distinctive base spirits. While brandy holds a smaller slice of the market, it's witnessing a surge in popularity, especially in regions like South Korea, where there's a notable uptick in premium spirit imports.

By Ingredient: Grain-Based Dominance with Fruit-Based Innovation

Grain-based spirits hold a dominant 62.88% share of the craft spirits market in 2025, highlighting the fundamental role of traditional ingredients such as corn, rye, barley, and wheat in whiskey and vodka production. The United States spirits industry consumed 2.8 billion pounds of grain in 2023, representing a 121% increase over the past decade [3]Source: Distilled Spirits Council of the United States, "Distilled Spirits Council of the United States October 2024", distilledspirits.org. In the premium whiskey segment, craft producers differentiate their products through mash bill composition and grain origin to support premium pricing strategies.

Fruit-based spirits are expected to be the fastest-growing ingredient segment, with a projected CAGR of 12.43% from 2026 to 2031. This growth is fueled by advancements in traditional brandy production and the popularity of fruit-infused vodkas and gins. Micro-distilleries are using fruit fermentation techniques to produce vodka, supporting sustainability goals and creating unique flavors. Agave-based spirits continue to grow steadily, while craft producers are exploring alternative bases like honey and maple. These producers aim to use local agricultural resources and adopt sustainable practices. The focus on innovation and sustainability is driving the demand for these spirits. This trend highlights the evolving preferences of consumers in the spirits market.

By Distribution Channel: On-Trade Leadership with Off-Trade Growth

In 2025, the on-trade channel holds a 58.34% share of the craft spirits distribution market. Bars, restaurants, and hospitality venues play a key role in increasing brand awareness and encouraging customers to try premium craft products. After recovering from the pandemic, this channel has grown significantly, driven by the global popularity of cocktail culture. In Singapore, the strong cocktail scene supports the demand for premium spirits, while Thailand's tourism recovery provides craft brands with more visibility in hospitality venues. The on-trade channel remains important for craft spirits, as bartenders act as brand ambassadors and give customers the chance to sample products before buying full bottles.

The off-trade channel is expected to grow at a CAGR of 11.95% from 2026 to 2031, supported by improved retail strategies and the expansion of direct-to-consumer sales. Specialty and liquor stores continue to be important for craft spirits distribution, offering carefully selected products and expert staff to help customers choose premium options. Although e-commerce is growing, its progress has been slowed by regulatory restrictions in many markets. However, recent changes in regulations show promise. For example, New York now allows direct-to-consumer spirits shipping, and Mississippi will permit direct-to-consumer wine shipments starting February 2025. These developments suggest that this distribution model could expand further in the future.

Geography Analysis

In 2025, North America held the largest market share at 38.75%. The United States has a strong craft distilling industry, with 3,069 active craft distillers, according to the American Craft Spirits Association. However, the sector faced its first decline in 2023, with a 3.6% drop in production volumes and a 1.1% decrease in value, based on the same source. Regulations are changing, with nine states and Washington, D.C., now allowing direct-to-consumer spirits shipping. Trade tensions remain a challenge, as the U.S. planned to introduce a 25% tariff on Canadian and Mexican imports in March 2025. This could lead to retaliatory actions and disrupt supply chains.

Europe is expected to grow the fastest, with a projected CAGR of 12.96% from 2026 to 2031. This growth is driven by strong craft traditions, a well-established cocktail culture, and rising demand for premium products. In Asia, the market is expanding, especially in South Korea, where whisky imports reached a record 30,586 tons in 2023, a 13.1% increase from the previous year, according to the Korea Customs Service.

South America and the Middle East and Africa are emerging markets. Brazil and the UAE are seeing higher consumption of premium spirits. Distillers in these regions are using local botanicals to create unique gin products for both domestic and international markets. These regions offer growth opportunities for craft spirits manufacturers who can adapt to local regulations and meet consumer preferences.

Competitive Landscape

The craft spirits market features a competitive landscape where global spirits companies and independent craft distillers coexist. Small-batch producers focus on flexibility and innovation, while multinational companies use their strong distribution networks and financial resources to gain an edge. Leading companies like Diageo, Pernod Ricard, and Constellation Brands strengthen their market presence through strategic acquisitions and investments in the craft spirits segment.

Large corporations are actively shaping the market by creating dedicated craft divisions and innovation centers. They acquire craft distilleries, launch brand development programs, and implement targeted strategies to meet the growing demand for premium and super-premium spirits. This approach helps them stay efficient while maintaining the unique appeal of craft production.

In May 2025, Heaven Hill Distillery introduced the "Family Farms First" program in partnership with Farm Rescue to support family-owned farms. This initiative is part of the Heaven Hill "Grain to Glass" program, which helps farming families that supply ingredients for food and whiskey production. Constellation Brands is also focusing on sustainability, aiming to achieve "TRUE Zero Waste to Landfill" certification for key facilities by fiscal year 2025 and adopting circular packaging across its beverage alcohol products.

Craft Spirits Industry Leaders

-

Pernod Ricard SA

-

Diageo PLC

-

Bacardi Limited

-

Constellation Brands Inc.

-

Remy Cointreau SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Skull X Vodka entered the Indian travel retail market through airport duty-free locations in Delhi, Bangalore, Hyderabad, and Mumbai. The vodka, produced in Slovakia, undergoes five distillations and platinum filtration.

- March 2025: Ochre Spirits introduced its premium product, Ochre Saffron Vodka, in Goa. The vodka features a clear appearance with a golden sheen, incorporating Kashmiri saffron and citrus notes.

- February 2025: Amrut has released Amrut Expedition, a 15-year-old single malt whisky, making it the longest-aged Indian whisky to date. This release represents a significant development in India's alcoholic beverage industry.

- February 2025: ZigZag Vodka launched in Bangalore, India, offering Original, Lime, Orange, and Green Apple flavors. The vodka variants can be consumed neat, with ice, or mixed in cocktails.

Global Craft Spirits Market Report Scope

Craft spirits are hand-crafted and manufactured by a small distillery using locally sourced materials and ingredients. The craft spirits market is segmented based on type, distribution, and geography. Based on type, the market is segmented into whiskey, gin, vodka, brandy, rum, and other types, by distribution channel into on-trade channels and off-trade channels, and by geography into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on value (in USD million).

By Product Type

| Whiskey |

| Gin |

| Vodka |

| Brandy |

| Other Types |

By Ingredient

| Grain-based |

| Fruit-based |

| Agave-based |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off Trade Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Whiskey | |

| Gin | ||

| Vodka | ||

| Brandy | ||

| Other Types | ||

| By Ingredient | Grain-based | |

| Fruit-based | ||

| Agave-based | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current craft spirits market size?

The craft spirits market size reached USD 23.75 billion in 2026 and is projected to grow to USD 41.87 billion by 2031.

Which product category leads the craft spirits market?

Whiskey leads, accounting for 26.77% of craft spirits market share in 2025, buoyed by premium single-malt and small-batch demand.

Why is Europe the fastest-growing region for craft spirits?

Europe blends heritage distilling with modern cocktail culture and shows a projected 12.96% CAGR from 2026 to 2031, aided by premium demand and sustainability priorities.

How are craft distillers addressing the surge in low/no alcohol interest?

Many producers introduce botanical non-alcoholic spirits and lower-ABV variants to capture health-conscious consumers while maintaining brand engagement.

Page last updated on: