Luxury Hair Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 21.32 Billion |

| Market Size (2031) | USD 30.56 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

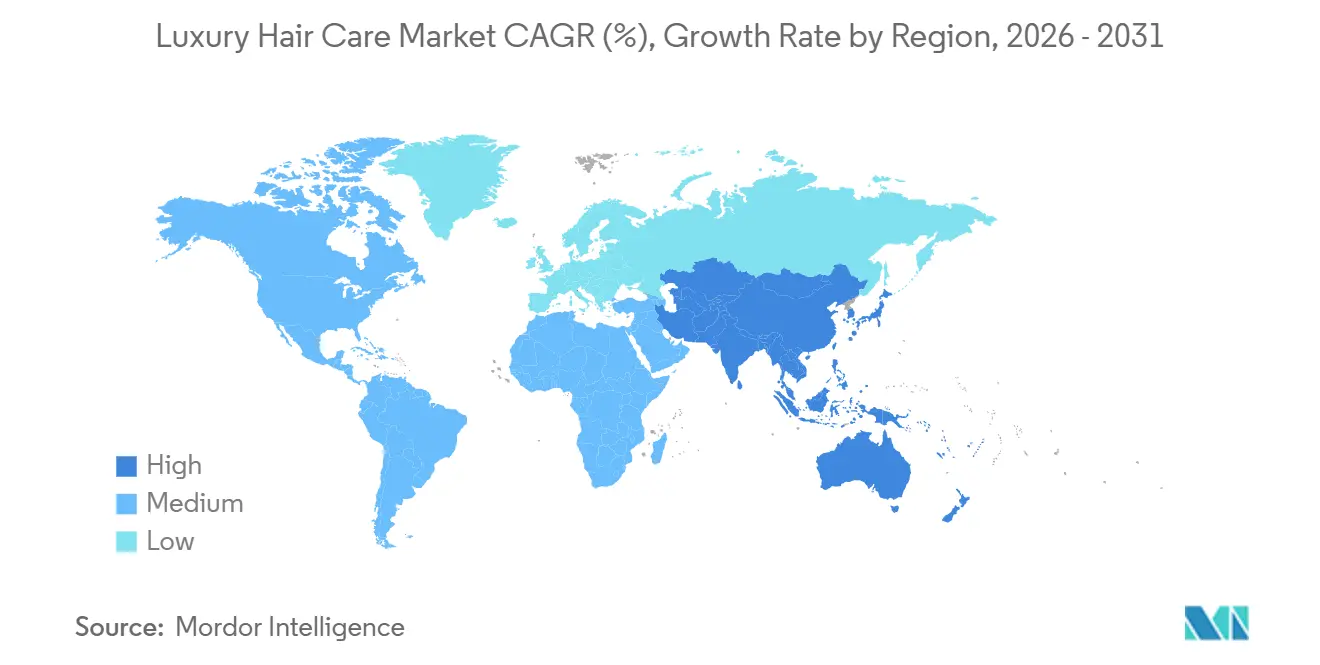

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

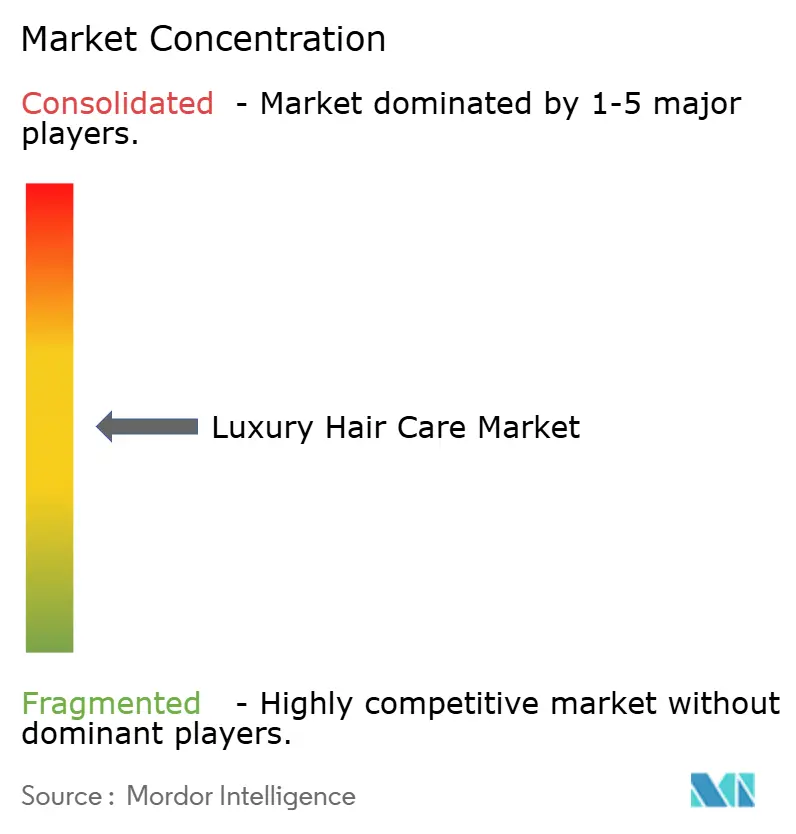

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Hair Care Market Analysis by Mordor Intelligence

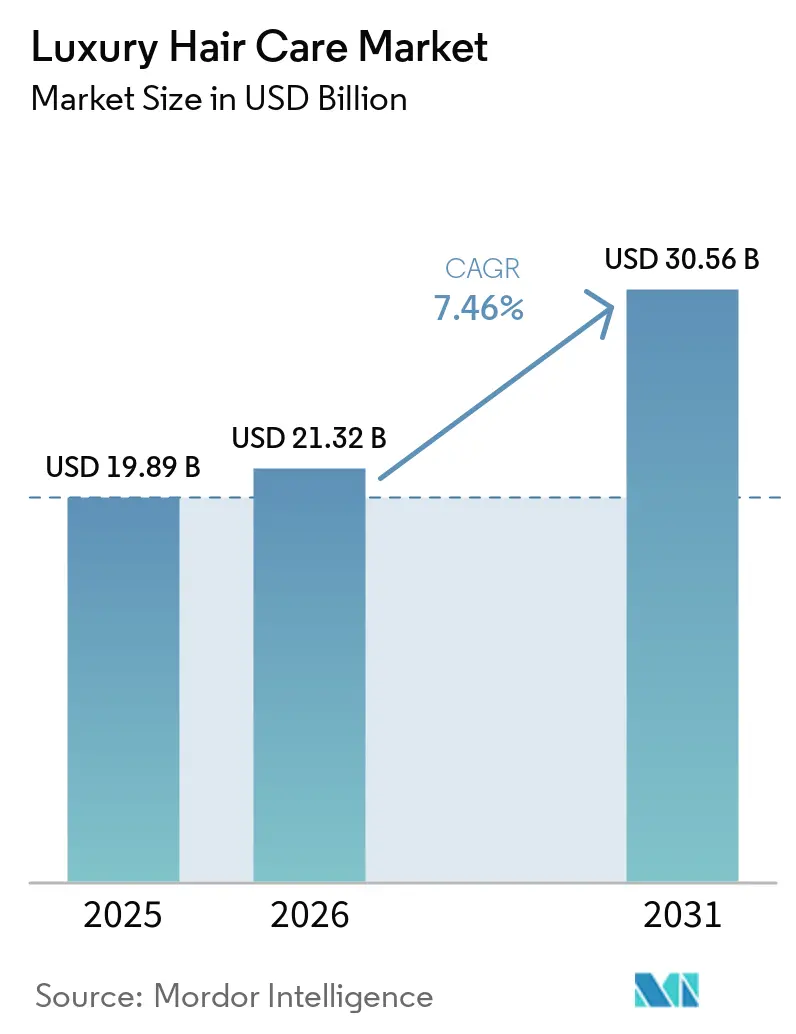

The luxury hair care market size is expected to grow from USD 19.89 billion in 2025 to USD 21.32 billion in 2026 and is forecast to reach USD 30.56 billion by 2031 at a 7.46% CAGR over 2026-2031. The luxury haircare market is driven by increasing consumer demand for premium hair products that feature advanced formulations, personalized solutions, and exclusive branding. Rising disposable incomes and heightened beauty consciousness among affluent consumers have further boosted the preference for luxury haircare products, often viewed as status symbols. Additionally, social media influence and celebrity endorsements have increased awareness of premium brands, motivating consumers to invest in high-end treatments and products. Innovations in ingredients, such as the use of organic and natural components, along with a focus on sustainable and ethically sourced products, are attracting environmentally conscious buyers. Furthermore, the growing presence of luxury salons and spas globally enhances accessibility and expands the consumer base.

Key Report Takeaways

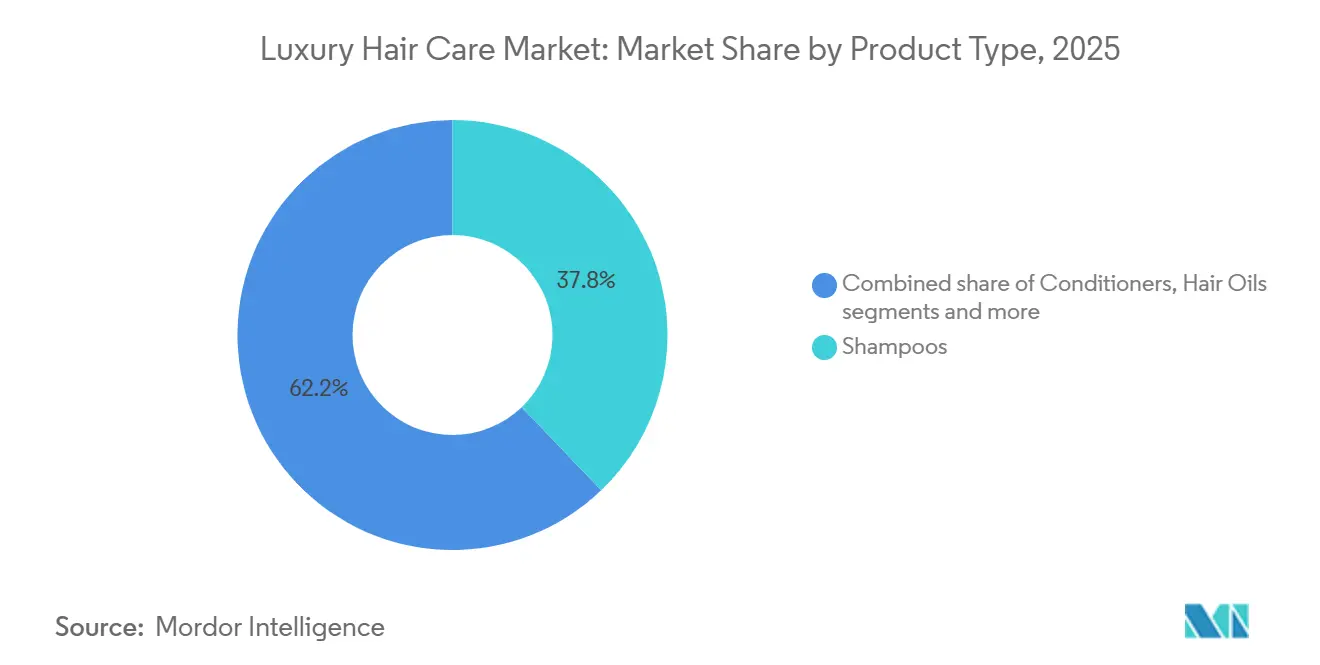

- By product type, shampoos held 37.83% of the luxury hair care market in 2025, while hair oils are projected to grow at an 8.16% CAGR through 2031.

- By nature, conventional and synthetic products accounted for 71.63% of the luxury hair care market in 2025, while natural and organic products are expected to advance at an 8.64% CAGR through 2031.

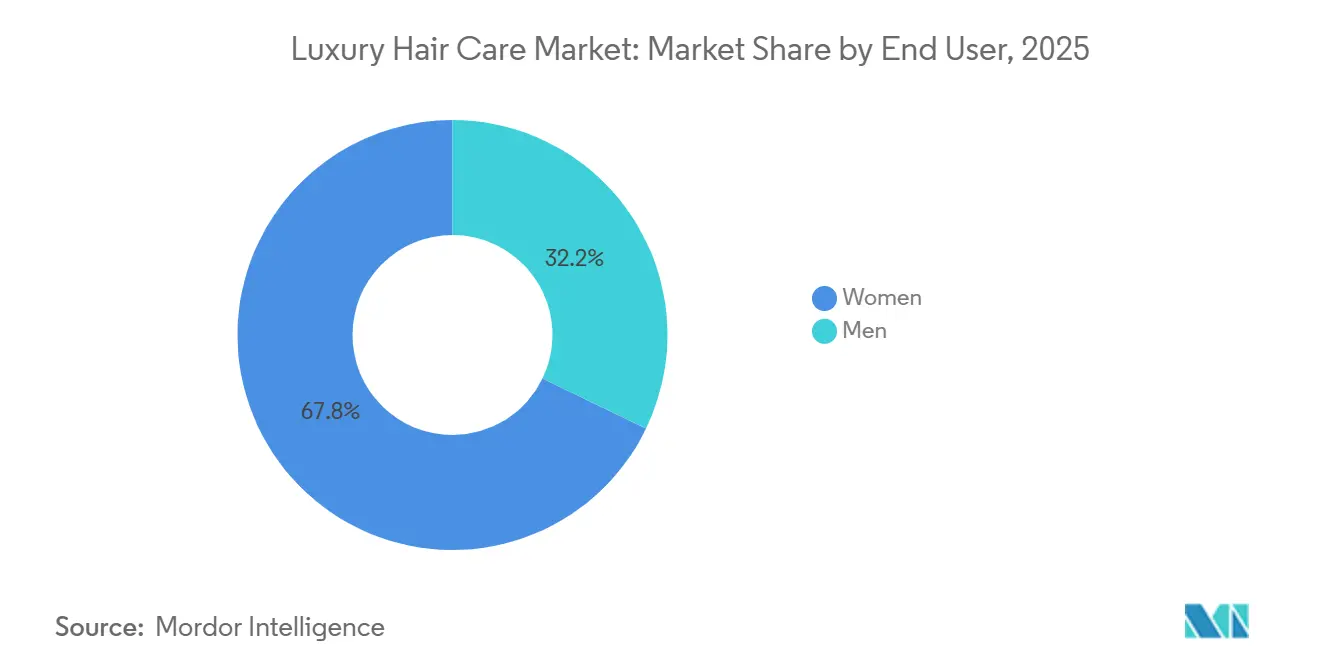

- By end user, women represented 67.83%% of the luxury hair care market in 2025, while men are forecast to expand at an 8.08% CAGR through 2031.

- By distribution channel, specialty stores captured 39.23% of the luxury hair care market in 2025, while online retail is projected to record a 9.03% CAGR through 2031.

- By geography, Europe held 34.55% of the luxury hair care market in 2025, while Asia-Pacific is forecast to grow at a 9.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Luxury Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for natural and organic ingredients | +2.0% | Global, concentrated in Europe and North America | Long term (≥ 4 years) |

| Advancements in hair care technology | +1.5% | Global; early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Influence of social media and celebrity culture | +1.2% | Global; driven by North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Shifts toward sustainable and ethical practices | +0.8% | Europe and North America core; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Growing awareness of hair health and scalp care | +1.0% | Global; particularly Asia-Pacific and Europe | Medium term (2-4 years) |

| Shift toward male grooming and unisex products | +0.8% | North America and Europe; Asia-Pacific rising | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for natural and organic ingredients

The growing consumer preference for natural and organic ingredients is a key driver shaping the future of the luxury haircare market. As consumers become increasingly conscious of the ingredients in their products and seek safer, more eco-friendly options, brands are responding by emphasizing natural formulations that deliver visible and effective benefits. This shift toward natural ingredients not only aligns with health and environmental concerns but also enhances the perceived value and luxury appeal of haircare products, fostering stronger brand loyalty and differentiating products in a competitive marketplace. Supporting this trend, a recent survey published by Impactfactor and conducted in Himachal Pradesh with 450 respondents on May 2026 highlights the positive consumer perception of natural hair care benefits. The survey revealed that 89% of users reported experiencing reduced hair breakage, further emphasizing the importance of visible and effective results[1]Source: Himachal Pradesh University Business School, “Consumer Perception towards Hair Care Product Benefits,” impactfactor.org.

Influence of social media and celebrity culture

The social media and celebrity culture heavily influence the luxury hair care market. Consumers increasingly rely on social platforms for inspiration, product discovery, and purchases, making digital presence and influencer collaborations essential. Celebrity endorsements and influencer marketing boost brand visibility, especially among younger, social media-savvy consumers. Short-form videos on TikTok and Instagram Reels dominate content, with TikTok being the top searched platform globally and influencing 51% of impulse buys. According to data published by the National University in March 2026, 92% of consumers trust peer reviews over traditional ads, highlighting the power of influencer and user-generated content[2]Source: National University, “Social Media Trends in 2026: What’s Next,” nu.edu. The shift toward authenticity favors real reviews and creator recommendations, with Gen Z spending 54% more time on social media than traditional media[3]Source: National University, “Social Media Trends in 2026: What’s Next,” nu.edu. Overall, these trends are transforming how brands engage with their audience in the sector.

Advancements in hair care technology

Luxury brands are now anchoring their innovative product lines on advancements in bond-repair science. These innovations, once primarily driven by marketing claims, are now increasingly supported by rigorous research and clinical validation, emphasizing proven efficacy. A case in point: The Estée Lauder Companies unveiled groundbreaking hair research at the World Congress for Hair Research on April 2024, highlighting strides in ingredients, scalp health, and damage mitigation. Such milestones not only redefine industry benchmarks but also elevate consumer anticipations. By melding hardware, formulation, and clinical backing, brands cultivate robust ecosystems that enhance loyalty and trust. In the premium segment, where verifiable proof is paramount, brands jeopardize their credibility without substantial research and development investments in scientifically validated technologies.

Shift toward male grooming and unisex products

The luxury hair care market is evolving, driven by a surge in demand for male grooming and unisex products. Once predominantly targeting women, the segment now sees men actively seeking premium solutions for styling, scalp health, and nourishment. This shift underscores a wider cultural embrace of grooming, highlighting its role in self-expression and aesthetics. KT Men, for instance, made its mark in India's flourishing men's grooming arena on March 2026, aligning with cricket legends to resonate with the youth. Aiming for a INR 100 crore milestone in its debut year, KT Men is banking on its unique, plant-based formulations. Their approach underscores a trend where brands meld quality, inclusivity, and aspirational marketing to tap into this expanding market. As consumers increasingly gravitate towards versatile, gender-neutral products that resonate with their identities, the market braces for further growth and innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory and compliance standards | -1.5% | Global; Europe and North America most affected | Long term (≥ 4 years) |

| Counterfeit and gray-market products | -0.8% | Global; highest exposure in e-commerce-led markets | Medium term (2-4 years) |

| High costs and affordability constraints | -0.7% | South America, Middle East and Africa, Asia-Pacific emerging markets | Medium term (2-4 years) |

| Competition from mass-market hair care products | -0.5% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory and compliance standards

Luxury hair care brands worldwide must navigate stringent regulatory frameworks, adhering to safety, quality, and ingredient standards set by authorities such as the Food and Drug Administration and European Medicines Agency. These regulations require brands to conduct rigorous testing for safety and efficacy, provide transparent ingredient disclosures, and comply with restrictions on certain chemicals. Non-compliance can lead to penalties, product recalls, and tarnished brand reputations. Furthermore, as consumers increasingly prioritize transparency, sustainability, and eco-friendliness, brands are under pressure to source ingredients responsibly and steer clear of harmful chemicals. This complex regulatory landscape poses ongoing challenges, often demanding substantial investments in research, quality assurance, and regulatory expertise.

Counterfeit and gray-market products

Counterfeit and gray-market luxury hair care products pose a major challenge, damaging brand reputation and risking consumer health. These fake products often look authentic but contain harmful ingredients like industrial dyes and toxic chemicals, leading to scalp and hair damage. Sold through unverified online platforms, street markets, and unauthorized stores, these products are difficult to regulate and trace. Gray-market items, though sometimes genuine, may be expired or improperly stored, risking safety and quality. Brands are adopting authentication measures like holograms and QR codes to combat counterfeiting. Educating consumers to buy only from authorized channels is essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hair Oils Signal a Treatment-Led Revenue Shift

Shampoos continue to dominate the market, accounting for 37.83% of the 2025 market share. They serve as the primary entry point for consumers and a key product for brand trials across specialty retail and salon channels. This position is supported by their frequent purchase cycles and their role as a foundational category product. Conditioners and hair styling products occupy the mid-tier, with increasing consumer willingness to invest in these products as clinical performance claims become essential for justifying premium pricing.

The hair oil category is projected to be the fastest-growing product segment, with a CAGR of 8.16% through 2031. This growth reflects a shift in consumer preferences from cleansing-focused to treatment-focused hair care routines within the luxury segment. The growth of the hair oil category is closely tied to the trend of scalp skinification. Consumers who have adopted multi-step facial serum routines are applying the same approach to hair and scalp care, driving both basket size growth and higher per-unit value in the luxury segment.

By Nature: Organic Certification Reshapes the Premium Proof Point

In 2025, conventional and synthetic formulations dominated the luxury hair care market, holding a substantial 71.63% share. This stronghold can be traced back to established prestige brands. These brands have effectively harnessed science-backed synthetic active ingredients, earning both clinical credibility and a deep-seated trust from consumers. Additionally, the consistent quality, improved stability, and precise ingredient delivery offered by conventional products contribute to their widespread adoption across retail channels, reinforcing the segment's position in the global luxury hair care market.

Natural and organic products are set to outpace their counterparts, projected to grow at an impressive CAGR of 8.64% through 2031. This surge marks them as the fastest-growing segment in the market. The driving force behind this growth is a rising consumer appetite for certified, clean-label formulations. This demand is further amplified by tightening regulatory disclosure standards, especially in the European Union and North America. Brands that overlook these evolving expectations stand to alienate a discerning and affluent consumer base.

By End User: Men's Grooming Resets Market Boundaries

Women continue to dominate the luxury hair care market, accounting for 67.83% of the 2025 market share. Their evolving preferences remain a key driver of category-level demand. Starting in 2026, the State of New York will require cosmetology schools to include textured hair care training, creating a downstream professional demand for luxury textured-hair products. This alignment of professional education with consumer behavior is expected to benefit brands with credible luxury positioning in the textured-hair care segment.

The men's end-user segment, growing at a CAGR of 8.08% through 2031, is the fastest-expanding segment in the market. This growth is driven by the increasing acceptance of multi-step grooming routines among Gen Z and millennial men, as well as the growing perception of scalp health as a functional concern rather than merely a cosmetic one. Male consumers are actively seeking specialized solutions for scalp care, hair thinning, and precise styling. In these categories, luxury brands with clinically validated formulations and premium ingredient profiles maintain a competitive edge over mass-market alternatives.

By Distribution Channel: Online Retail Redefines Luxury Accessibility

Specialty stores dominated the market in 2025, holding a significant 39.23% share. This strong performance is attributed to their ability to provide personalized consultations, product trials, and diagnostic services, which are highly valued by consumers. Specialty retailers enhance consumer trust by employing knowledgeable staff and focusing on high-end beauty and personal care products. This approach makes them a preferred choice for shoppers seeking customized solutions and premium hair care products. As a result, specialty stores continue to play a crucial role in meeting customer preferences for tailored services and in-person interactions.

Meanwhile, online retail is emerging as the fastest-growing channel in the industry, with a projected CAGR of 9.03% through 2031. This growth is fueled by a shift in how consumers discover luxury brands, moving away from traditional settings like physical salons and specialty counters to curated digital platforms such as TikTok Shop and other direct-to-consumer channels. The increasing integration of online and specialty channels is also driving the adoption of omnichannel strategies, enabling businesses to offer a seamless shopping experience across multiple platforms.

Geography Analysis

Europe is anticipated to remain the largest market for luxury hair care products, accounting for approximately 34.55% of the market share by 2025. The region's established beauty industry, high consumer purchasing power, and preference for premium-quality products contribute to its dominant position. Additionally, increasing awareness among European consumers regarding hair health and beauty trends, along with the presence of numerous luxury brands and advanced distribution networks, reinforces Europe's leadership in the global market.

The Asia-Pacific region is expected to be the fastest-growing market between 2026 and 2031, with a compound annual growth rate (CAGR) of 9.23%. Factors such as rapid urbanization, rising disposable incomes, and the expansion of the middle class are driving demand for luxury hair care products in countries like China, India, and Japan. Furthermore, growing beauty consciousness and a shift towards premium and innovative products are accelerating market growth, positioning Asia-Pacific as a key area of focus for global brands seeking expansion opportunities.

In addition to Europe and Asia-Pacific, other regions are also gaining momentum in the luxury hair care market. North America maintains a significant market share, supported by high consumer spending and the strong presence of luxury brands. Meanwhile, regions such as the Middle East are experiencing steady growth due to the increasing adoption of premium lifestyles, heightened awareness of hair health, and the expansion of distribution networks. These emerging markets offer substantial opportunities for brands aiming to reach new consumer bases and enhance their global presence.

Competitive Landscape

The luxury hair care market is moderately fragmented, with key players including L'Oréal S.A., The Procter & Gamble Company, Unilever Plc, Henkel AG, and Shiseido Company, Limited. These companies utilize their research and development capabilities to create high-end, premium hair care products. Their focus is on offering superior formulations that emphasize quality, aesthetics, and exclusivity to appeal to affluent consumers.

L'Oréal and Shiseido are prioritizing luxury branding by introducing sophisticated packaging and personalized solutions for high-end clients. In contrast, P&G, Unilever, and Henkel are expanding their premium product portfolios through strategic acquisitions and partnerships to strengthen their position in this niche market. Innovation in ingredients and the adoption of sustainable practices are also significant differentiators among these companies.

Despite the competitive environment, these companies continue to invest in marketing and distribution channels to broaden their reach. They target affluent consumers seeking premium hair care solutions that align with their lifestyle and status. Overall, the market remains dynamic, with players striving to achieve differentiation and enhance brand prestige.

Luxury Hair Care Industry Leaders

Unilever Plc

Henkel AG

L'Oréal S.A.

The Procter & Gamble Company

Shiseido Company, Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Reliance Retail Limited announced the acquisition of Priyanka Chopra Jonas’s global haircare brand, Anomaly, including its trademarks and digital assets. This acquisition is intended to expand Reliance’s beauty portfolio and drive growth both in India and international markets by utilizing Anomaly’s high-performance, vegan formulations.

- March 2026: Henkel announced the USD 1.4 billion acquisition of OLAPLEX, a science-led, high-performance hair brand. The deal expands Henkel’s premium portfolio, leveraging OLAPLEX’s global presence and innovation capabilities to drive growth and product development. This move strengthens Henkel’s position in the premium hair care market.

- July 2025: L’Oréal announced the acquisition of Color Wow, a fast-growing professional haircare brand recognized for its aerosol styling products, including Dream Coat. Established in 2013 by Gail Federici, the brand is well-known for its humidity-resistant treatments catering to both salon and consumer markets.

Global Luxury Hair Care Market Report Scope

The scope of this report covers the luxury hair care market, focusing on premium hair care products. These products are designed to enhance the aesthetic appeal and maintenance of hair, targeting affluent consumers seeking high-quality solutions. The report provides a comprehensive analysis of market dynamics, key players, and growth opportunities within this specialized segment. The market is segmented by product type, including shampoos, conditioners, hair oils, styling products, and other related categories, analyzing their specific roles and consumer preferences. Products are further categorized by nature into conventional/synthetic and natural/organic variants, reflecting the growing consumer interest in sustainability. End-user segmentation differentiates between women and men, highlighting varying needs and purchasing behaviors. Distribution channels are examined across hypermarkets, specialty stores, online retail platforms, and other channels, offering insights into sales strategies. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, enabling a regional analysis of demand and competitive dynamics.

| Shampoos |

| Conditioners |

| Hair Oils |

| Hair Styling Products |

| Other Product Types |

| Conventional/Synthetic |

| Natural/Organic |

| Women |

| Men |

| Hypermarkets and Supermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Shampoos | |

| Conditioners | ||

| Hair Oils | ||

| Hair Styling Products | ||

| Other Product Types | ||

| By Nature | Conventional/Synthetic | |

| Natural/Organic | ||

| By End User | Women | |

| Men | ||

| By Distribution Channel | Hypermarkets and Supermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the luxury hair care space and how fast is it growing?

The luxury hair care market stood at USD 21.32 billion in 2026 and is projected to reach USD 30.56 billion by 2031, projected to grow at a 7.46% CAGR.

Which product category leads revenue today?

Shampoos led with 37.83% share in 2025 because they remain the most common entry point across salons, specialty stores, and premium beauty retail.

Which product type is expanding the fastest?

Hair oils is projected to the fastest-growing product type with an 8.16% CAGR through 2031, reflecting the shift toward treatment-led and scalp-focused routines.

What are the main strategic themes shaping competition?

The category is being shaped by science-led product systems, scalp care, selective mergers and acquisitions, and tighter channel control, with examples including Henkel’s Olaplex deal.

Page last updated on: