Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.52 Billion |

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 3.83% CAGR |

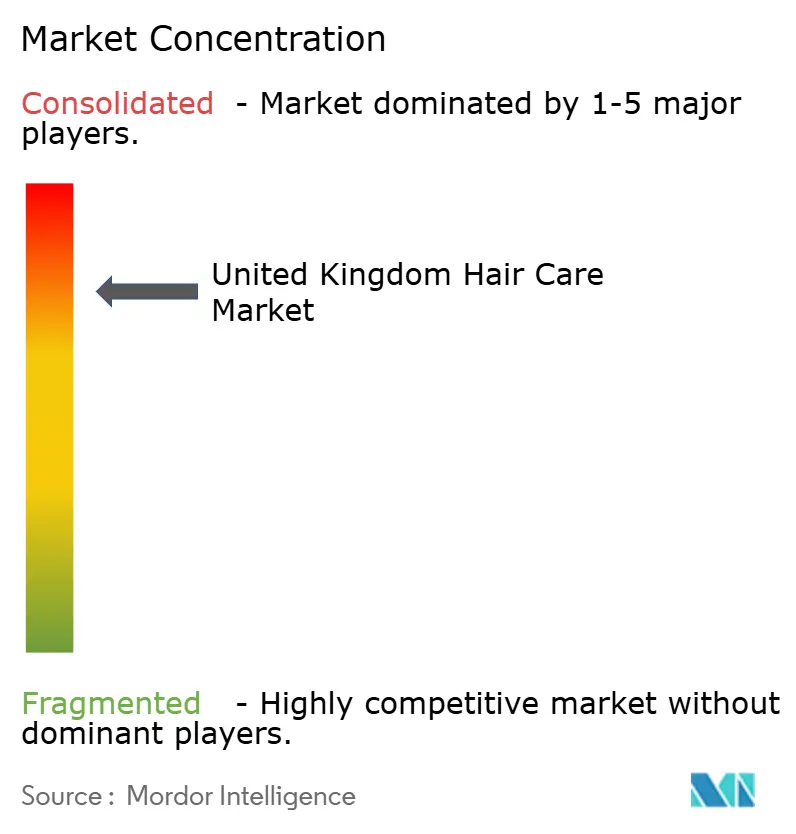

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Hair Care Market Analysis by Mordor Intelligence

The United Kingdom Hair Care Market size is projected to be USD 2.52 billion in 2025, USD 2.66 billion in 2026, and reach USD 3.21 billion by 2031, growing at a CAGR of 3.83% from 2026 to 2031. Increasing online penetration, a shift towards premium products, and post-Brexit regulatory changes are reshaping the competitive landscape. Online retail now accounts for over one-third of sales, and the rise in direct-to-consumer sales is driving multinationals to enhance their social-commerce strategies and subscription models. Despite cost-of-living challenges, consumers continue to favor premium products, prioritizing proven benefits such as bond-repair actives, scalp-microbiome ingredients, and UV protection over basic offerings. Supply-side consolidation is evident, with KKR acquiring Wella and L’Oréal purchasing Color Wow, strengthening their portfolios in professional and prestige markets. The upcoming 2026 ingredient bans are accelerating reformulation efforts, increasing entry barriers, and giving an edge to brands with strong regulatory capabilities.

Key Report Takeaways

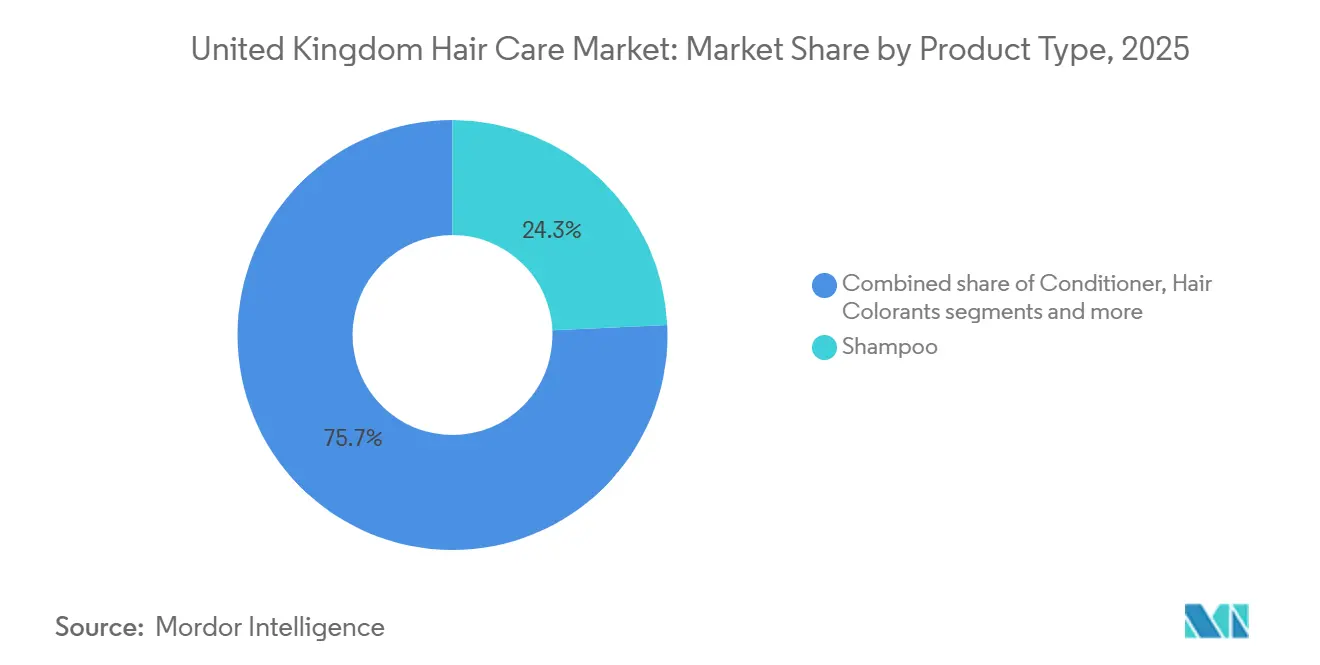

- By product type, shampoo led with 24.26% of the United Kingdom hair care market share in 2025, while styling products recorded the fastest projected 5.1% CAGR through 2031.

- By category, mass-market lines held 71.65% share of the United Kingdom hair care market size in 2025, whereas the premium segment is set to expand at a 5.7% CAGR to 2031.

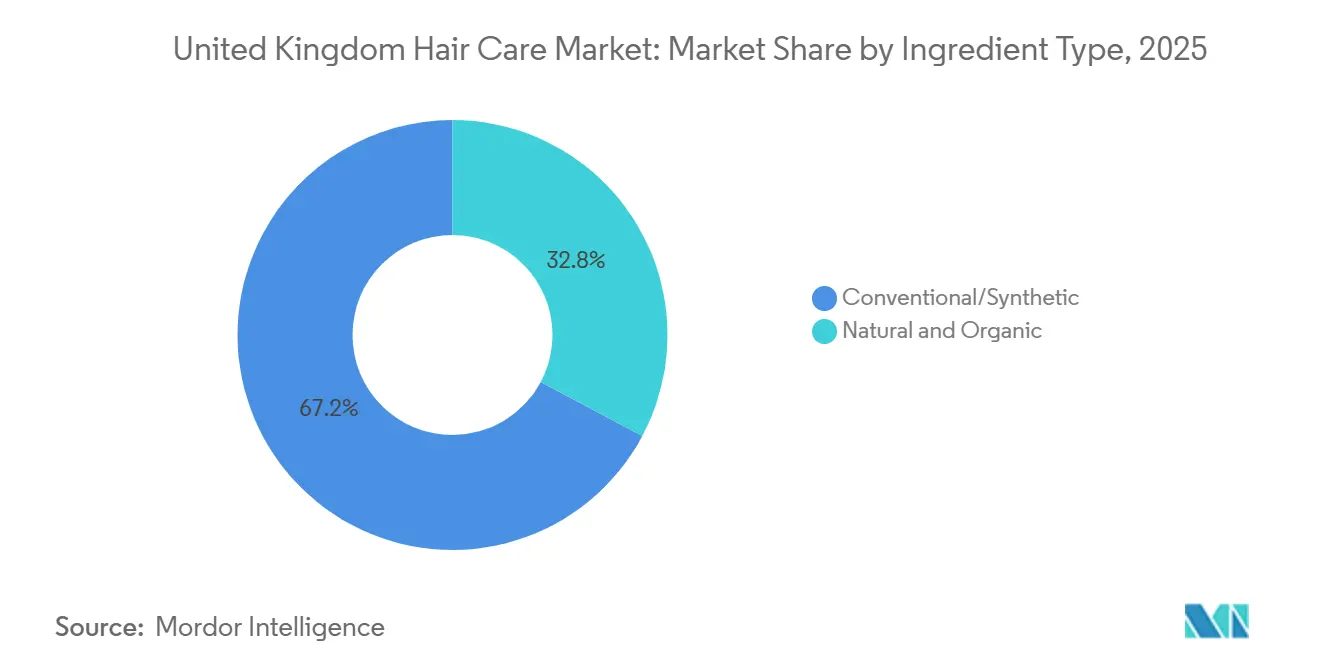

- By ingredient type, conventional synthetics dominated, yet natural and organic lines captured 32.78% share in 2025 and are growing at a 5.6% CAGR.

- By distribution channel, online retail accounted for 38.10% share in 2025 and is advancing at a 5.7% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumers' inclination toward natural and organic products | +0.9% | National, with concentration in London, Southeast, and urban centers | Medium term (2-4 years) |

| Increased awareness of pollution and UV damage drives demand for protective hair care products | +0.6% | National, elevated in urban areas with higher pollution exposure | Short term (≤ 2 years) |

| Rising influence of social media and celebrity endorsement | +0.7% | National, amplified among 18-34 demographic | Short term (≤ 2 years) |

| Growing demand for personalised/AI-driven hair-care solutions | +0.5% | National, early adoption in premium segment and specialty retail | Medium term (2-4 years) |

| Water-scarcity push toward waterless and solid formats | +0.4% | National, with stronger uptake in environmentally conscious consumer segments | Long term (≥ 4 years) |

| Breakthrough scalp-microbiome actives spur new product lines | +0.5% | National, concentrated in premium and professional channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumers' inclination toward natural and organic products

United Kingdom consumers are shifting their spending toward natural-origin formulations, surpassing broader European trends. This change is primarily driven by increasing skepticism toward traditional synthetic ingredients and a preference for transparent supply chains. The Soil Association's Organic Market Report 2025 highlights that organic beauty and personal-care sales in the UK reached GBP 151 million, reflecting an 11 percent year-on-year growth[1]Source: Soil Association, "Organic Market Report", soilassociation.org. Hair-care products, in particular, are gaining momentum as brands reformulate to comply with COSMOS certification standards. This intersection of consumer demand and sustainable sourcing is revolutionizing ingredient procurement. Leading brands are investing in fermentation platforms to ensure supply and support clean-beauty claims, while avoiding the land-use and deforestation issues linked to botanical extraction. In the UK, the lack of a legal definition for "natural" in cosmetics regulation compels brands to depend on third-party certifications such as COSMOS, Soil Association Organic, or B Corp. This approach not only strengthens compliance but also provides a marketing advantage for certified brands, while exposing uncertified ones to potential greenwashing allegations.

Increased awareness of pollution and UV damage drives demand for protective hair care products

Urban pollution and increased UV exposure are driving significant demand for hair-care products that protect the cuticle and scalp from oxidative stress. This segment, which was almost non-existent a decade ago, now occupies premium shelf space and features dedicated product lines. In October 2024, the UK's Scientific Advisory Group on Chemical Safety (SAG-CS) issued Opinion 14, approving benzophenone-3 as a UV filter. Brands can now use it at concentrations of up to 2.2 percent for full-body applications and up to 6 percent in products for the face, hands, and lips. This decision provides regulatory clarity for brands looking to incorporate UV filters into leave-on hair treatments and scalp serums. However, challenges remain: the UK's Cosmetic Products Regulation 2026 will ban Enzacamene, another UV filter, starting July 15, 2026. This will require reformulation for any products still relying on that molecule. The strategic takeaway is clear: brands that adopt next-generation UV-defense technologies, such as antioxidant complexes, film-forming polymers, and approved UV filters, are poised to capture market share in the protective hair-care segment. Conversely, those slow to reformulate risk delisting or regulatory penalties. Reflecting the urgency, public sector spending on pollution abatement in the UK rose from GBP 761 million in 2024 to GBP 1,357 million in 2025, highlighting growing pollution concerns and the resulting demand for protective hair-care products[2]Source: Government of the United Kingdom, "UK Public Expenditure Statistical Analyses, "gov.uk.

Rising influence of social media and celebrity endorsement

Social media has revolutionized the marketing approach for hair-care products. Platforms like TikTok, Instagram, and YouTube have expedited the journey from product discovery to trial and repurchase, condensing what once took months into mere weeks. According to Boots' Beauty Trends Report 2025, TikTok has emerged as the go-to platform for 18-to-34-year-olds discovering new hair-care products. Viral hashtags such as #BondRepair and #ScalpTok have not only garnered millions of impressions but have also translated into significant sales boosts for the brands highlighted. UK consumers are more likely to trust influencer recommendations for hair-care products when influencers are transparent about ingredient sourcing and clinical testing. This underscores the idea that transparency can significantly enhance conversion rates. While celebrity endorsements still hold sway, there's a noticeable shift in the UK market. Consumers are increasingly gravitating towards endorsements from micro-influencers and clinically-credentialed trichologists, marking a move towards expertise-driven marketing. The economic rationale is clear: direct-to-consumer brands can secure customer acquisition costs under GBP 20 through targeted social campaigns. In contrast, traditional retail promotions often exceed GBP 50. Moreover, the immediacy of data feedback allows brands to tweak products in real-time based on consumer feedback. Yet, with these rapid advancements come heightened risks. The same social channels that fuel growth can also magnify reputational threats. Counterfeit products and misleading claims can spread like wildfire, prompting brands to bolster their defenses. Investing in social listening tools and agile legal teams has become paramount for brands aiming to safeguard their intellectual property and maintain consumer trust.

Growing demand for personalized/ai-driven hair-care solutions

Artificial intelligence is transitioning from a marketing tactic to a fundamental product development tool in the UK hair care market. This advancement enables brands to deliver precise diagnostics and personalized regimens, previously accessible only in trichology clinics. GHD has launched its CurlFinder AI quiz, designed to help consumers identify the best heat-styling tool for their specific curl pattern. Similarly, Dyson's Omega range uses machine-learning algorithms to adapt heat and airflow based on hair type and environmental humidity. The advantages of AI-driven personalization extend beyond improving conversion rates. It also generates valuable first-party data on hair concerns, product usage, and product efficacy, which brands can utilize for targeted product development and retention marketing strategies. The integration of AI diagnostics, clinical collaborations, and supplements marks a shift from generic formulations to modular, data-driven regimens. This shift creates opportunities for brands that combine digital tools with product performance and for retailers offering in-store diagnostic services to compete with online personalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over legacy chemical ingredients | -0.5% | National, with heightened scrutiny in premium and natural segments | Short term (≤ 2 years) |

| Proliferation of counterfeit and grey-market products | -0.4% | National, concentrated in online marketplaces and discount retailers | Short term (≤ 2 years) |

| Stringent regulations on cosmetic ingredients | -0.3% | National, affecting all manufacturers and importers | Medium term (2-4 years) |

| Supply-chain shocks for key botanicals (argan, jojoba, etc.) | -0.3% | Global, with direct impact on UK brands sourcing Moroccan argan and other botanicals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns over legacy chemical ingredients

Consumer and regulatory scrutiny of synthetic preservatives, UV filters, and colorants is driving reformulation cycles that disrupt product portfolios and place pressure on research and development budgets. Beginning in July and August 2026, the UK's Cosmetic Products Regulation 2026 will enforce significant bans. Enzacamene, along with 16 other substances classified as carcinogenic, mutagenic, or reprotoxic, will be prohibited. This includes trimethylbenzoyl diphenylphosphine oxide (TPO), widely used in nail products, and tetrabromobisphenol-A, a flame retardant. Furthermore, the regulation will lower the formaldehyde-release labeling threshold from 0.05 percent to 0.001 percent. These changes follow the January 2025 implementation of restrictions on 64 CMR substances and kojic acid under UK SI 2024/1334. While kojic acid was banned in hair-care products, it remains permitted at 1 percent in facial and hand formulations. These cumulative regulations are reducing the pool of approved ingredients and driving up formulation costs. Brands are now required to conduct new safety assessments, stability tests, and clinical trials to validate reformulated products. Multinational brands operating across both the UK and EU markets face additional challenges due to regulatory divergence. The EU implemented bans on certain substances earlier, while the UK's phased approach, which includes transitional sell-through periods, demands parallel SKU management and dual labeling. Smaller brands and contract manufacturers are disproportionately burdened, as they often lack in-house toxicology expertise and regulatory-affairs teams to navigate these changes. This dynamic is driving consolidation in the market, favoring larger, well-resourced players.

Proliferation of counterfeit and grey-market products

Counterfeit hair-care products and unauthorized grey-market imports are diminishing brand equity, disrupting pricing strategies, and creating safety risks that regulators and industry associations are finding difficult to manage. The economic impact extends beyond lost revenue. Brands are required to invest in anti-counterfeiting solutions (including holograms, QR codes, and blockchain authentication), pursue legal actions, educate consumers, and address reputational harm caused by counterfeit products leading to adverse effects. Online marketplaces like Amazon, eBay, and social-commerce platforms are the primary channels for distributing counterfeit goods. Although these platforms have introduced seller-verification programs and takedown mechanisms, enforcement remains inconsistent and reactive. A robust strategy is essential for brands: securing supply chains with serialized packaging, collaborating with customs and trading standards for border enforcement, and educating consumers through social media and in-store signage to identify genuine products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Styling Outpaces Cleansing in Growth

In 2025, shampoo held a significant 24.26% share of the UK's hair care market. This dominance was primarily attributed to its high purchase frequency and the introduction of bond-repair innovations, which transitioned from exclusive salon offerings to widely available mass-market products. On the other hand, the UK's market for hair styling products is anticipated to expand at a robust 5.1% CAGR during the forecast period of 2026 to 2031. This growth is driven by the increasing adoption of multi-step hair care routines, which prominently feature products like heat protectants and texturizing sprays. Henkel, in 2024, reported notable organic sales growth, largely propelled by the rising demand for styling products.

Consumers are demonstrating a growing willingness to allocate a larger portion of their spending to styling products, motivated by the desire to achieve salon-quality results in the comfort of their homes. Additionally, the emergence of leave-in hybrid products is blurring the lines between hair treatments and styling solutions, offering dual benefits. In 2025, Tesco listed an extensive range of over 1,600 hair SKUs, with pricing data indicating that styling creams achieved profit margins 2-3 times higher than those of shampoos. This substantial margin potential is attracting investments from both mass-market and premium brands, underscoring the likelihood that the styling segment will remain a key driver of incremental revenue growth within the hair care sector.

By Category: Premium Gains Share Despite Mass Dominance

In 2025, mass lines held a commanding 71.65% share of the UK hair care market, driven by the robust performance of supermarket own-label products and the preferences of price-conscious consumers. However, the premium segment is anticipated to grow at a notable 5.7% CAGR through 2031. This growth is attributed to a shift in consumer behavior, where individuals are increasingly focusing on purchasing effective "hero" products that deliver tangible results, rather than diversifying their shopping baskets. Social commerce is now playing a pivotal role in directing consumer traffic straight to brand websites and specialized e-tailers, effectively bypassing the traditionally price-driven supermarket aisles.

Premium brands are distinguishing themselves in the market by forming strategic partnerships with dermatologists, utilizing AI-powered diagnostic tools, and introducing refillable product ecosystems. These initiatives not only enhance the consumer experience but also justify the higher price points of GBP 20-60. Furthermore, subscription-based models and exclusive collaborations with retailers are helping these brands safeguard their profit margins. In contrast, mass-market brands are facing challenges such as promotional fatigue and rising raw material costs. To address these issues and defend their market share, these brands are focusing on innovation by incorporating multiple benefits, such as bond repair, scalp health, and appealing fragrances, into products priced under GBP 10, aiming to sustain their sales volumes.

By Ingredient Type: Natural Formulations Narrow the Gap

Conventional synthetics continue to dominate the market in terms of volume, primarily due to their affordability and consistent performance. However, the market share of natural and organic products is projected to rise significantly, reaching 32.78% by 2025. This growth is being driven by advancements in biotechnology, which are improving key product attributes such as foam quality, slip, and shelf stability, all while eliminating the need for sulfates and silicones. In the United Kingdom, the hair care market associated with natural-certified SKUs is expanding at a compound annual growth rate (CAGR) of 5.6%. This trend reflects growing consumer trust in third-party certifications and a strategic reallocation of shelf space by retailers to accommodate these products.

Global corporations are adopting a hedging strategy by introducing silicone-free product lines that are co-developed with botanical research institutions. At the same time, independent brands are focusing on delivering ultra-clean formulations and ensuring transparency across their supply chains. The ability to succeed in this evolving market depends on achieving an optimal balance between price and performance. Excessive price premiums can deter mainstream consumers, while products that fail to deliver satisfactory sensory experiences may lead customers to revert to synthetic alternatives.

By Distribution Channel: Online Dominates and Accelerates

Online channels currently account for a 38.10% share of the United Kingdom's hair care market, and this segment is anticipated to grow at a compound annual growth rate (CAGR) of 5.7% through 2031. The convenience offered by e-commerce platforms is driven by features such as same-day delivery, an extensive and diverse product assortment, and personalized algorithmic recommendations. Additionally, social-commerce platforms like TikTok Shop are revolutionizing the shopping experience by integrating product discovery and checkout within a single interface. This streamlined process shortens the purchasing funnel and significantly boosts impulse buying behavior.

Physical retailers are countering this trend by enhancing in-store experiences to attract and retain customers. For instance, Boots has implemented in-store K-SCAN diagnostics to provide personalized solutions, while Superdrug is focusing on exclusive innovations within its own-brand product lines. According to the Office for National Statistics UK, retail sales volumes increased by 0.4% in December 2025, following a 0.1% decline in November and a 0.8% drop in October[3]Source: Office for National Statistics UK, "Retail industry", ons.gov.uk. Salons continue to hold a strong position in delivering professional coloring and treatment services. However, to remain competitive in an increasingly omnichannel environment, they are also expanding their presence online by retailing companion products.

Geography Analysis

London and the Southeast, characterized by higher income levels and a concentration of specialty retail outlets, dominate premium spending in the United Kingdom. In contrast, regions such as the Midlands, North, Scotland, Wales, and Northern Ireland exhibit a preference for value SKUs and online replenishment options. The UK hair care market benefits significantly from a well-established and advanced logistics network, which ensures equitable access across regions. The growth of e-commerce in 2025 has further reduced the traditional advantage held by urban areas, leveling the playing field for consumers nationwide.

Brexit-related regulatory divergence has introduced significant complexities into supply chains. Brands are now required to maintain separate inventories to comply with both GB and EU regulations. Furthermore, Northern Ireland's adherence to EU cosmetic laws under the Windsor Framework adds an additional layer of compliance, creating a three-tiered regulatory structure. This fragmentation disproportionately impacts small and medium-sized enterprises (SMEs), as they often lack the resources to manage such complexities. Consequently, larger market players with dedicated regulatory teams are gaining a competitive edge and increasing their market share.

Demographic diversity plays a crucial role in shaping geographic demand within the UK hair care market. Major cities, which are home to significant Afro-Caribbean and South Asian communities, drive demand for specialized products such as curl-enhancing and moisture-focused SKUs. While mainstream retailers have expanded their offerings to include textured-hair products, there remains substantial untapped potential in inclusive product development. By engaging in regional marketing efforts that involve partnerships with community influencers and trichologists, brands can effectively unlock latent demand in areas outside of London, thereby broadening their consumer base.

Regulatory Landscape

Hair care in Great Britain is governed by the retained UK Cosmetics Regulation framework, based on Regulation (EC) No 1223/2009 as amended following EU exit, with the Office for Product Safety and Standards (OPSS) acting as the lead regulator for cosmetics. Products placed on the GB market require a UK-established Responsible Person, and compliance typically includes maintaining the Product Information File as well as meeting labeling and safety obligations, along with notification via the UK Cosmetics products system for GB market access.

The UK has continued to update substance restrictions through statutory instruments and phased compliance dates that affect formulation and labeling choices. The Cosmetic Products Regulation 2026/23 sets new restrictions effective 15 July 2026, including prohibiting 3-(4'-methylbenzylidene)-camphor (Enzacamene) and tightening formaldehyde releaser labeling thresholds. Additional CMR-related prohibitions take effect from 15 August 2026, along with transitional sell-through provisions for certain products already on the market. Northern Ireland continues to follow EU cosmetics rules under the Windsor Framework, which adds operational complexity for brands managing parallel GB, NI, and EU assortments.

Competitive Landscape

The United Kingdom hair care market is consolidated, with a few international and regional players dominating the competitive landscape. Prominent companies such as Kao Corporation, Unilever PLC, L'Oreal S.A., Procter and Gamble Company, and Henkel AG and Co. KGaA are actively implementing strategic initiatives, including mergers, geographic expansions, acquisitions, partnerships, and the introduction of innovative products. These efforts aim to solidify their market presence while fostering stronger connections with consumers.

There is a significant untapped potential in the market, particularly within the textured hair care segment, where mainstream brands have historically struggled to address specific consumer requirements. This unmet demand has created opportunities for specialized companies to thrive, as highlighted by Treasure Tress's analysis of Afro haircare opportunities. Furthermore, the integration of advanced technologies is becoming a pivotal factor in differentiating brands. Companies are increasingly channeling investments into personalized product recommendations, virtual consultations, and engaging social media strategies to enhance customer experiences and optimize acquisition costs. For instance, L'Oréal's development of the AirLight Pro serves as a clear example of how technological advancements can cater to consumer preferences for high performance and sustainability, while simultaneously providing a competitive advantage.

The regulatory framework also plays a crucial role in shaping the competitive dynamics of the market. Companies with strong research and development capabilities are better equipped to swiftly adapt to evolving ingredient restrictions and safety standards, thereby gaining a competitive edge. At the same time, emerging disruptors are leveraging direct-to-consumer business models and social media marketing to bypass traditional retail channels. This shift is prompting established players to adopt omnichannel strategies that seamlessly integrate online and offline customer touchpoints, ensuring consistent brand messaging and delivering a cohesive consumer experience across various platforms.

United Kingdom Hair Care Industry Leaders

-

Kao Corporation

-

Unilever PLC

-

L'Oreal S.A.

-

Henkel AG and Co. KGaA

-

The Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven reformulation and clearer UK positions on certain actives are expanding the room for science-led, claims-supported hair care in the UK, especially across scalp-first, bond-repair, and UV-defense leave-on routines. Online retail already accounts for 38.10% of hair care value in 2025, and social-commerce is accelerating discovery. In this context, brands that combine clinically framed hero products with direct-to-consumer sampling, subscriptions, and diagnostic-led regimens have a more defined path to premium conversion, while building first-party data.

Sustainability-led format and ingredient innovation are also moving into broader commercialization, supporting traction for waterless and low-water formats and circular inputs that fit both consumer scrutiny and regulatory compliance. In March 2026, Waterless Limited launched Nilaqua biodegradable, rinse-free shampoo and conditioner wraps manufactured in the UK using 100% renewable energy, indicating active entry and scale-ready alternatives to traditional liquid formats. Inclusive and specialized hair solutions remain under-served at mass retail despite demand in major UK cities, leaving room for textured-hair, scalp-health, and protective styling adjacencies to expand beyond specialty channels.

Recent Industry Developments

- July 2026: Henkel completed its acquisition of OLAPLEX after receiving required regulatory approvals, adding a premium, bond-repair focused brand to its hair care portfolio. The deal strengthens Henkel's position in prestige and professional-adjacent segments where performance claims and salon influence support higher price points.

- June 2025: L'Oréal signed an agreement to acquire Color Wow, expanding its Professional Products Division with a fast-growing brand that has strong traction in the UK and an established online community. The acquisition increases L'Oréal's exposure to premium styling and treatment routines that are increasingly driven by social commerce and salon credibility.

- May 2024: TYPEBEA entered the UK market with a focused range including shampoo, conditioner, a treatment mask, and an overnight scalp serum built around clinically framed ingredients. This launch added competitive intensity in the scalp-health and hair-growth adjacency, where consumers are consolidating spend into fewer, efficacy-led hero products.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market includes consumer hair care products sold in the United Kingdom through retail and online channels, measured as value sales in USD. It covers routine cleansing and conditioning, styling and finishing products, and color and treatment items bought for personal use.

Scope exclusions: Professional salon services revenue (haircuts, coloring services, and treatments delivered as services) is excluded, while only the retail sale of take-home products is counted.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

-

By Category

- Premium Products

- Mass Products

-

By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the market context and to ground key assumptions in public, checkable data. We review official consumer and retail indicators (such as the UK Office for National Statistics releases), trade and tariff signals from HM Revenue and Customs, and market surveillance or safety notes from the UK government and regulators.

To make the model realistic, we also pull product and category clues from sources such as trade association updates, peer reviewed cosmetics science journals, company annual reports and investor decks, and trusted retail press coverage. Where available, paid subscriptions are used in a limited way for company financials, patent databases, and shipment level import and export signals to sanity check direction and timing. The sources listed here are illustrative only, and many other public and internal references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions and to fill gaps that public data does not answer cleanly, like premiumization pace, channel mix shifts, and typical price movements by format. We speak with a mix of brand teams, distributors, retailers, and industry specialists across the United Kingdom so the demand picture is not driven by a single channel or product type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 22% | |

| Mid tier: 46% | Functional/Unit leaders: 33% | |

| Smaller Players: 22% | Managers: 45% |

Market-Sizing & Forecasting

The sizing starts from a top-down view where household consumption and retail sell-through indicators are translated into a value pool for hair care in the United Kingdom, and then aligned to category totals seen in public retail and macro series. To keep the number practical, we corroborate the output with selective bottom-up checks such as sampled average selling price (ASP) by pack type multiplied by estimated volumes, and supplier and retailer channel checks to adjust obvious overcounts.

Inputs that matter in this market include the split between mass and premium ranges, online share changes, the mix shift across shampoo, conditioner, styling, and colorants, and inflation-led price resets that affect ASP more than unit growth. We also track promotional intensity and ingredient or formulation related changes that can move pricing and assortment faster than underlying demand. For forecasting, scenario analysis is used so the base case reflects what interviewees expect on pricing and channel mix, and the downside and upside capture different outcomes on consumer spending and promotional depth.

Data Validation & Update Cycle

Model outputs are checked against independent signals like retail value growth, channel level directionality, and the implied per-household spend, and then reviewed for unusual jumps by year and by category mix. When a variance looks large, we recheck the driver assumption, and follow up with additional expert calls to confirm if the change is real or a modeling artifact.

Before sign-off, the work goes through a multi-step internal review where assumptions, math links, and year-to-year continuity are validated. Reports are refreshed annually, with interim updates when major events occur (for example, sudden pricing shocks or regulatory changes), and a final pre-delivery pass is completed so the latest public information is reflected.

Mordor Intelligence's United Kingdom Hair Care Market Market Size Versus Other Published Estimates

Published market sizes for UK hair care do not always line up because the year chosen, the currency used, and what is counted as hair care can change from one publisher to another. Differences also show up when price inflation is treated as the main growth lever versus when volume and mix are emphasized.

The main gap comes from whether the estimate is built around a retail-only product basket or if it blends in adjacent areas like hair loss remedies and broader treatment categories, and in how currency conversion timing is handled, which is where Mordor Intelligence keeps the scope tied to consumer retail hair care products and uses a consistent USD conversion approach for the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.52 B (2025) | |

| Trade Publisher A | USD 2.40 B (2024) | Uses retail selling price including taxes and a different base year, and it also explicitly includes hair loss treatments inside the haircare total, which can lift the value pool versus a core haircare-only scope. |

| Industry Source B | USD 2.71 B (2024) | Runs a longer forecast horizon and appears to apply a faster price-led growth curve from a 2024 base, with less visible cross-checking to near-term UK channel mix and promotion intensity. |

Overall, the spread is mainly explained by scope choices around treatment items, base-year timing, and how pricing assumptions are carried forward. With clear product inclusion rules, practical checks against channel signals, and repeatable steps, the estimates become easier for decision-makers to compare and use.

Key Questions Answered in the Report

What is the projected value of the United Kingdom hair care market in 2031?

The market is forecast to reach USD 3.21 billion by 2031.

Which product segment is expected to grow fastest through 2031?

Styling products, supported by demand for heat protectants and multi-benefit creams, are projected to post a 5.1% CAGR.

How large is online retail’s current role in U.K. hair-care sales?

Online channels already contribute 38.10% of market value and are growing faster than all offline channels.

Why is premium hair care expanding despite cost-of-living pressures?

Shoppers are consolidating routines around fewer, high-efficacy products with clinical claims, driving premium-segment growth of roughly 5.7% CAGR.

Page last updated on: