Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 24.98 Billion |

| Market Size (2026) | USD 25.15 Billion |

| Market Size (2031) | USD 30.94 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

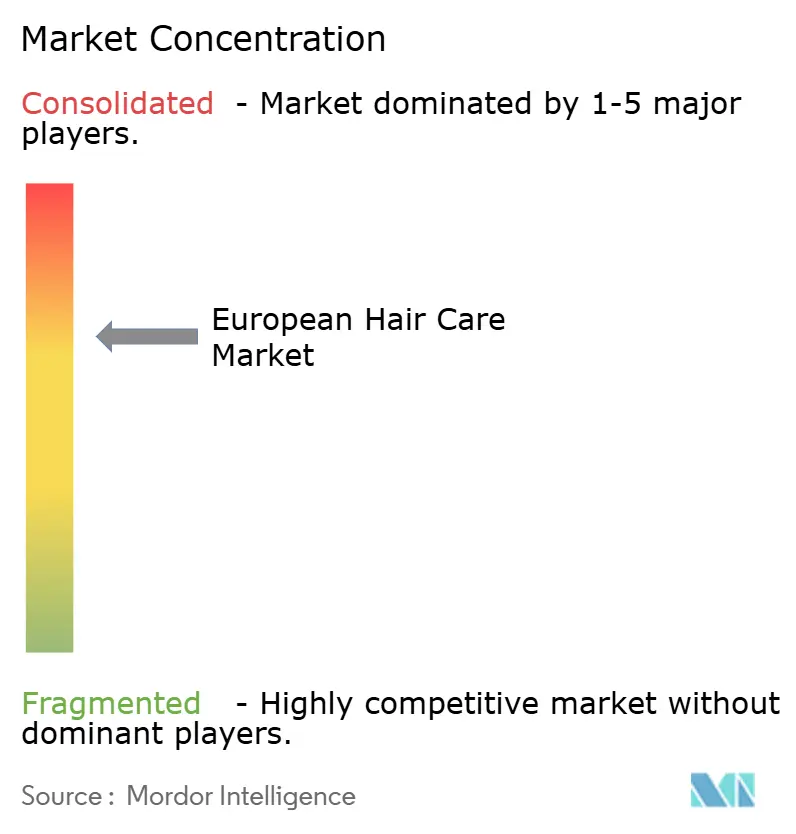

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Hair Care Market Analysis by Mordor Intelligence

The Europe hair care market size is expected to grow from USD 24.98 billion in 2025 to USD 25.15 billion in 2026 and is forecast to reach USD 30.94 billion by 2031 at a 4.23% CAGR over 2026-2031. Consumers in Europe are driving the hair care market toward cleaner, more innovative options, shaped by stricter regulations and smart shopping habits. While shampoos remain popular, multifunctional styling products with heat protection and botanicals are surging for busy lifestyles. Brands like Rossmann's Alterra and dm's Alverde lead Germany's natural scene, offering affordable organics that shoppers scan online for clean ingredients. In France, eco-buyers turn to verified organic lines, checking databases to avoid conventional formulas. Luxury products like Kérastase and Olaplex shine for damaged hair repair, delivering salon results worth the premium price. Sustainability rules like Directive 2024/825 require real green proof, while wastewater controls spur innovative, cleaner shampoos from smaller brands. Platforms like Douglas boost online growth with AI matching and refills, letting consumers skip stores for home delivery. Consumers act by prioritizing third-party verified products, dodging fines on fake claims, and choosing refillable options to cut waste, empowering healthier, greener hair routines across the region.

Key Report Takeaways

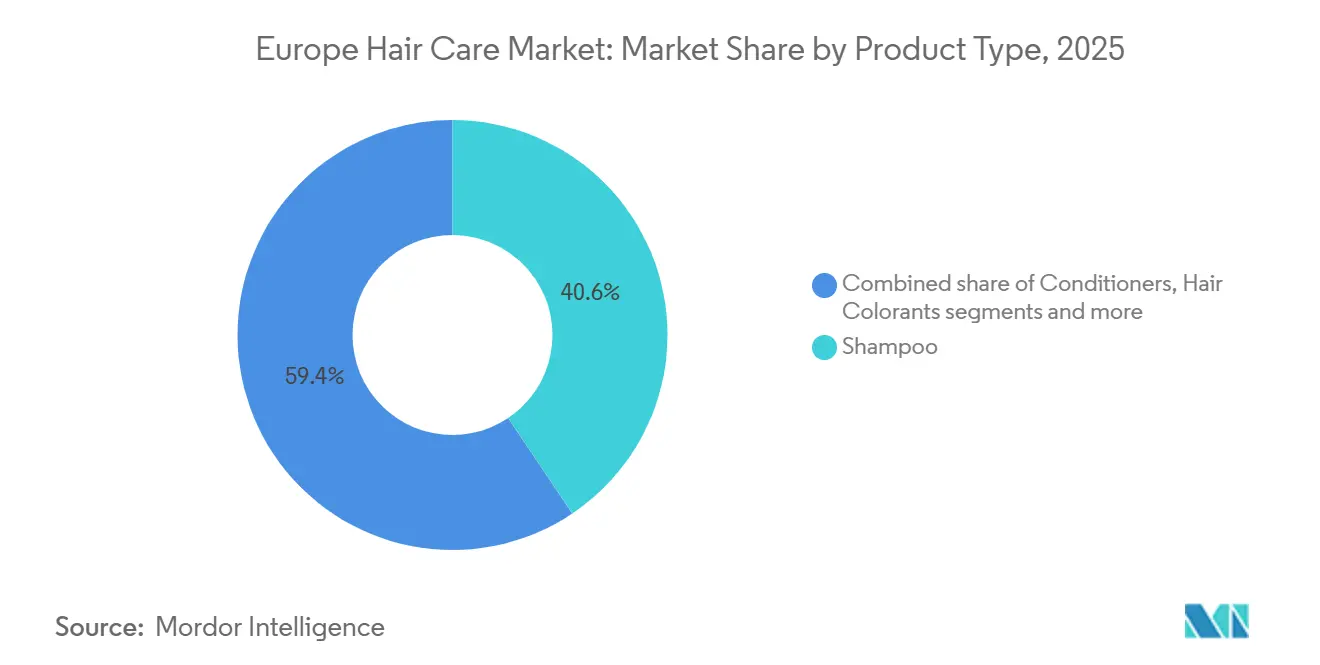

- By product type, shampoo accounted for 40.59% of the Europe hair care market size in 2025, whereas hair styling products are poised to expand at a 4.59% CAGR through 2031.

- By category, conventional offerings commanded 73.28% of the Europe hair care market size in 2025, yet organic products are projected to grow 4.91% annually.

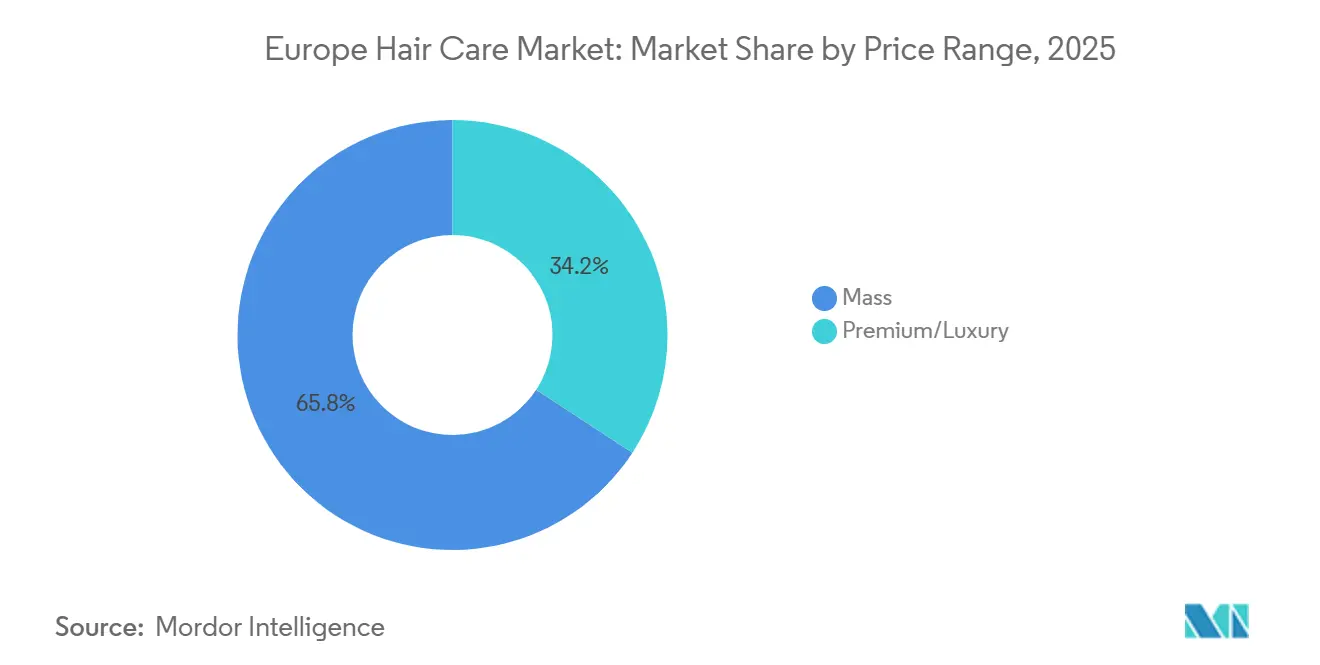

- By price range, mass products held 65.78% of the Europe hair care market share in 2025; the Luxury/premium segment is expected to post a 5.08% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets retained a 36.87% share in 2025, while online retail store sales are advancing 5.54% each year.

- By geography, Germany held 22.92% of the Europe hair care market share in 2025; Spain is expected to post a 4.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Age-ing population elevating demand for anti-hair-fall and grey-coverage solutions | +0.8% | Germany, Italy, France, Benelux, and Nordic countries | Long term (≥ 4 years) |

| Influence of social media and digital marketing | +1.2% | United Kingdom, Germany, and Spain | Short term (≤ 2 years) |

| Growing preference for organic and herbal hair care | +0.9% | Germany, France, Netherlands, and Sweden | Medium term (2-4 years) |

| Rise of multifunctional shampoos with innovative active ingredients | +0.7% | Germany, United Kingdom, France, and Italy | Medium term (2-4 years) |

| Climate-linked "anti-pollution" claims amid European Union Green Deal focus | +0.5% | France, Italy, Poland (urban centers) | Medium term (2-4 years) |

| Growing demand for AI-personalized and custom hair care | +0.6% | United Kingdom, Germany, France, and Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing preference for organic and herbal hair care

Consumers in Europe are rapidly shifting toward organic and herbal hair care, favoring clean, natural formulas over traditional options as awareness of ingredient safety and sustainability grows. German shoppers lead this trend, routinely cross-checking products against trusted BDIH and Ecocert databases before checkout, while Rossmann's Natrue-certified Alterra line demonstrates how affordable organics thrive through direct sourcing from botanical cooperatives delivering quality without luxury price tags. Science backs popular ingredients like argan oil, packed with tocopherols that protect chemically treated hair from damage, making these choices appealing for everyday repair and maintenance. France and the Netherlands show the highest organic penetration, with specialty retailers like Biocoop and Ekoplaza dedicating entire aisles to sulfate-free and silicone-free formulations that cater to health-conscious buyers. The European Union Cosmetics Regulation Annex II prohibits over 1,600 harsh substances, establishing a strong clean-beauty baseline, while forthcoming digital ingredient passports will trace every batch back to its farm origin, enhancing transparency and building shopper confidence [1]Source: European Chemicals Agency, "cosmetics-prohibited-subs - ECHA - European Union", echa.europa.eu. This regulatory support, combined with maturing supply chains and consumer demand for verified naturals, positions organic hair care for sustained outperformance across retail, e-commerce, and professional channels.

Influence of social media and digital marketing

Social media and digital marketing have transformed the Europe hair care market seamlessly, blending discovery with instant purchases through viral content and smart platform integrations. According to the European Union, the percentage of online buyers in Europe increased to 77% in 2024 [2]Source: European Union, "E-commerce statistics for individuals", ec.europa.eu. For instance, TikTok's #hairtok hashtag amassed billions of views by late 2025, where micro-influencers delivered 60-second demos of bond-repair masks and curl routines, catapulting Olaplex from salon-exclusive to everyday drugstore staple via authentic user before-and-afters that outshone traditional ads. Similarly, Douglas Group transformed hair care into its fastest-growing premium category by embedding influencer links directly on product pages, enabling same-day deliveries that convert scrolls into sales. This trend extends to brands mastering rapid response, for example, Davines' OI styling mist exploded via Instagram reels, highlighting its plant-based shine, while Henkel's Syoss dominated with the #SyossSalonAtHome TikTok challenge, sparking user color transformations and e-commerce spikes. In Spain and Italy, Briogeo's scalp-care rituals gained traction through local influencers, and L'Oréal Paris cemented YouTube dominance with tutorials across France and Germany. These examples underscore how new Europen Union rules requiring paid partnership disclosures in the first 3 seconds build trust, empowering consumers to pursue trending dupes, verify creator reviews, and snag feed-driven deals while bypassing physical stores entirely.

Growing demand for AI-personalized and custom hair care

European hair care consumers increasingly seek tailored solutions that match their unique hair type, lifestyle, and concerns, fueling the rapid adoption of AI-driven personalization and custom formulations. Brands like Prose and Function of Beauty lead by analyzing user quizzes on porosity, scalp health, and styling habits to create bespoke shampoos and conditioners, delivering noticeable results. Consumers appreciate how virtual try-on tools from L'Oréal's Beauty Genius or Kérastase's app use computer vision to recommend shade-matched colors and regimen bundles, bridging the gap between online shopping and salon precision. This demand thrives as AI chatbots on platforms like Douglas and Sephora build personalized routines suggesting anti-frizz serums for Spain's humidity or bond-builders for color-treated hair, while subscription models ensure consistent replenishment without overbuying. Privacy-focused tech like on-device processing addresses data concerns, building trust among German and French shoppers who prioritize secure personalization. With e-commerce platforms integrating these tools, consumers enjoy shorter decision paths, lower cart abandonment, and higher satisfaction, driving double-digit growth for custom hair care across mass, premium, and professional segments as personalization becomes table stakes.

Rise of multifunctional shampoos with innovative active ingredients

Consumers now demand all-in-one solutions that tackle multiple concerns in a single wash, propelling multifunctional shampoos to the forefront as busy lifestyles prioritize efficiency over single-purpose products. Brands like L'Oréal's Elvive 6-in-1 and Henkel's Schwarzkopf 3D Miracle lines blend cleansing with heat protection, scalp soothing, and color-lock technology, appealing to consumers juggling styling, repair, and hydration without multiple steps. Ingredients such as bond-building peptides, caffeine for follicle stimulation, and plant-derived texturizers deliver salon results at home, making these formulas ideal for aging hair, color-treated locks, or humidity-prone regions like Spain. This shift reflects broader routines in which consumers seek proven actives backed by studies, such as hydrolyzed keratin and amino-acid complexes that can increase hair tensile strength by 12% to 15%, which fit hybrid work schedules and frequent washing cycles. As formulations evolve with bio-fermented keratin and microbiome-balancing prebiotics, multifunctional shampoos capture share from traditional categories, offering time-strapped shoppers visible improvements and value in one streamlined ritual.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory challenges | -0.6% | European Union-wide | Medium term (2-4 years) |

| Private-label price competition in drugstores and discounters | -0.9% | Germany, Poland, Spain, and Belgium | Short term (≤ 2 years) |

| Counterfeit products and parallel imports | -0.7% | United Kingdom, Italy, Spain, and Eastern Europe | Short term (≤ 2 years) |

| Consumer scepticism around green-washing claims | -0.5% | Germany, Netherlands, Sweden, and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory challenges

European hair care brands face mounting regulatory hurdles that slow innovation and raise costs, particularly around environmental claims and pollution controls that demand rigorous proof over marketing promises. The Directive (EU) 2024/825, effective since March 2024, bans vague "eco-friendly" or "green" labels on shampoos unless backed by third-party certifications, with fines up to 4% of annual revenue for unsubstantiated leaf icons or sustainability boasts [3]Source: The Luxembourg Government, "EU Empowering consumers directive (EmpCo)", gouvernement.lu. Consumers benefit from clearer truths, but smaller organic players struggle as the wastewater directive labels cosmetics as a polluter, forcing them to fund 80% of micropollutant removal systems they can't easily afford on a small scale. These rules hit harder in practice. Germany's UBA pilots digital product passports, tying every bottle to its carbon footprint and sourcing, requiring costly ERP upgrades that sideline contract manufacturers. The EU's ongoing Cosmetics Regulation review adds uncertainty around digital labels, refill mandates, and impact assessments, delaying launches as brands await clarity. While these measures protect consumers from greenwashing and pollution, in the fiercely competitive and consolidated Europe hair care market, they create barriers for nimble entrants, favor compliant giants like L'Oréal, and push mid-tier firms toward conservative formulations over bold naturals.

Counterfeit products and parallel imports

Online marketplaces are grappling with a surge of counterfeit shampoos, undermining consumer trust and stunting market growth. Counterfeit hair care products and parallel imports drain approximately EUR 3 billion annually from Europe's legitimate cosmetics market, equivalent to 4.8% of total sales, exploiting regulatory gaps that let salon-grade concentrates flow into discount chains unchecked [4]Source: European Union Intellectual Property Office, "Counterfeit goods cost EU industries billions of euros and thousands of jobs annually", euipo.europa.eu. These fakes thrive because regional exhaustion rules allow parallel traders to reroute premium formulas at 20-30% discounts, while customs authorities test fewer than 2% of incoming shipments due to limited lab capacity, letting toxic batches slip through to online marketplaces and low-end retailers. UK tests found carcinogens, mercury, and lead in fake hair dyes, yet budget shoppers sometimes opt for them anyway, prioritizing price over safety. This restraint hits hardest in Eastern Europe and cross-border e-commerce, where under-resourced enforcement creates wide openings for imports from China and Turkey. Hair care proves especially vulnerable; shampoos, styling products, and colorants mimic big brands like L'Oréal and Olaplex but deliver subpar results or health hazards. Brands counter with holograms, blockchain tracking, and platform partnerships, but the scale of the problem slows trust in online channels and forces legitimate players to hike prices to cover lost volume, constraining overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Styling Products Outpace Core Cleansing

In Europe’s hair care market, shampoos dominate with a 40.59% share, underscoring their foundational role in consumer routines as consumers' essential replenishment staple across mass-market and premium channels. Brands like L’Oréal Paris, Elvive, and Garnier Ultra Doux are leveraging premiumization, focusing on claims of repair, nourishment, and scalp care, which resonate with health-conscious consumers. However, traditional unit volumes face pressure from multifunctional formulas that extend wash cycles, shifting routines from every other day to twice a week use, while co-wash cleansers and leave-in treatments further erode rinse-out dependency. Shoppers value these innovations for time savings and reduced waste, particularly in fast-paced urban markets like Germany and France, where convenience drives category evolution.

Hair styling products are witnessing the fastest growth, boasting a 4.59% CAGR, fueled by demand for leave-in treatments that combine heat protection, frizz control, and lasting hold in single applications, perfect for busy consumers streamlining routines. This segment thrives as "skinification" trends extend to styling, with scalp serums and bond-repair concentrates incorporating actives like niacinamide gaining traction alongside L'Oréal's Color Wow acquisition signaling styling's rising importance. Aging markets sustain hair colorants through convenient at-home kits like P&G's Gemz powder system, while Spain's humidity challenges boost texturizing sprays year-round.

By Category: Organic Gains Share Despite Premium Pricing

Conventional hair care products command a dominant 73.28% market share in Europe, buoyed by established distribution channels and competitive pricing. built on decades of strong brand trust and widespread availability in supermarkets, pharmacies, and online platforms across Europe. These familiar formulas from leaders like L'Oréal and P&G benefit from massive retail presence and consumer loyalty, though their position faces gradual erosion as shoppers shift toward cleaner options, especially in urban areas where education campaigns highlight synthetic concerns. Shoppers continue choosing conventional for proven performance and affordability, particularly for everyday needs like basic cleansing and detangling, but expect brands to evolve with milder surfactants to compete.

Organic hair care is on the rise, with a 4.91% CAGR, outpacing conventional rates, driven by German and French consumers who demand full transparency on sourcing and production, verified by checks against BDIH, Ecocert, and Cosmébio standards. Brands like Klorane with its botanical shampoos, Davines with the OI Hair Mask, and L’Oréal's organic-inspired Serioxyl serums highlight the allure of ingredient transparency and premium positioning for eco-conscious consumers. Rossmann's Nature-certified Alterra proves organics can stay affordable through smart vertical integration, while Netherlands stores like Ekoplaza dedicate up to 62% of shelf space to sulfate-free, silicone-free lines favored by millennials who scan EWG databases. Strict European Union rules like Regulation (EC) No 834/2007 mandate 95% organic agricultural ingredients, ensuring authenticity.

By Price Range: Luxury Premiums Justified by Peptide Technology

In 2025, mass-market hair care dominates Europe's landscape, commanding a 65.78% market share, thriving on high turnover, everyday affordability, and broad availability that puts them in every shopping basket. Brands like Dove, L’Oréal Elvive, and Garnier Ultra Doux, with their accessible pricing and strong retail presence, have become household names. These accessible options from brands hold strong consumer loyalty for reliable basics, but face growing competition as direct-to-consumer players ship innovative refills straight to doors via social media. Consumers value the low price point for frequent repurchase staples, though multifunctional upgrades are needed to counter premium dupes eroding share in value-conscious markets like Germany and Poland.

Luxury/premium hair care is on the rise, boasting a 5.08% CAGR. This growth is driven by offering salon-grade innovation, such as Olaplex's bond-repair peptides and Kérastase's microbiome actives, backed by clinical validation and professional salon endorsements, to justify their premium pricing. Salon professionals demonstrate strength gains to build trust by partnering with influencers and leveraging direct-to-consumer channels; these brands are not only educating discerning buyers but also bolstering trust. The segment's expansion mirrors a broader trend of premiumization, where consumers increasingly value performance, transparency, and sustainability.

By Distribution Channel: E-Commerce Accelerates Digital Transformation

In 2025, supermarkets/ hypermarkets dominate Europe's distribution landscape, commanding a 36.87% market share, capturing high foot traffic and impulse buys that keep everyday brands like Dove, L’Oréal Elvive, Pantene, and Garnier front and center on accessible shelves. Their strength lies in convenience for weekly grocery runs where consumers grab replenishment staples without extra trips, though growth slows as shoppers shift repeat orders to subscription auto-delivery, reducing in-store restocking. Retailers are evolving, melding in-store displays with digital tools like QR codes for tutorials and loyalty programs, enriching the shopper's journey while ensuring consistent sales.

Online retail stores is witnessing a robust 5.54% CAGR, emerging as the fastest-growing segment, fueled by the rise of e-commerce, personalization through AI, subscription refills, and direct influencer links, features that physical stores can't match. Consumers favor the ease of same-day delivery, virtual try-ons, and curated bundles tailored to hair type or climate needs, especially in urban France and Spain. Independent and premium brands, like Hailey Bieber’s Rhode and Davines, adeptly utilize social media and influencer marketing, with Rhode making strides on European online platforms and Davines championing digital campaigns for their hair masks and serums. The Digital Services Act bolsters trust by forcing marketplaces to verify sellers and swiftly remove counterfeits, positioning big players for explosive expansion as direct-to-consumer brands cut wholesale margins to fuel customer acquisition.

Geography Analysis

Germany holds a dominant 22.92% share of the Europe market, driven by its dermocosmetics heritage, robust clinical-trial infrastructure, and consumer preference for ingredient transparency, which supports pharmacy-channel sales. Consumers prioritize transparency over flashy marketing. The market is expanding with brands like Schwarzkopf, Wella Professionals, and L’Oréal Professional leading the way. Beiersdorf has invested USD 324 million in its Leipzig plant, increasing capacity to 450 million units annually for hair sprays and styling products. This nature-conscious ecosystem reflects consumer preference for reliable, eco-verified formulas sourced directly from botanical cooperatives, maintaining low costs without compromising quality.

Spain is emerging as Europe's fastest-growing market, with a projected CAGR of 4.51% through 2031. This growth is fueled by rising incomes, year-round humidity driving demand for anti-frizz serums, and young TikTok shoppers seeking viral textures. Brands like Davines, L’Oréal Elvive, and Klorane are capitalizing on this trend, effectively leveraging lifestyle-centric positioning and the influence of digital and social media to meet the demand for multifunctional, premium products. Vytrus Biotech has invested EUR 3.5 million in a production plant in Spain to manufacture active ingredients for anti-aging and scalp-health formulations, showcasing how local suppliers are capturing value by serving multinational brands.

Across Europe, diverse markets are charting unique growth trajectories. In the United Kingdom, post-Brexit regulations allow quicker ingredient approvals, though major brands such as Dove, TRESemmé, and Joico adhere to pan-European formulas to avoid dual inventory challenges and additional costs. France leverages its luxury edge as Europe's top cosmetics exporter, with iconic salon brands like L'Oréal's Kérastase and Redken, although strict distribution laws limit online discounting to protect premium salon margins. Italy's stylist-driven culture sustains high demand for bond-repair and color-protect products, with premium brands like Framesi and Alfaparf Milano leading the market. Meanwhile, countries such as the Netherlands, Poland, Belgium, and Sweden are carving out niches in areas like eco-conscious products or specialized scalp care, requiring tailored marketing strategies. These localized approaches, while catering to smaller market shares, are crucial for driving sustained growth through specialized channels.

Competitive Landscape

Europe's hair care market is moderately consolidated, with multinational conglomerates such as L'Oréal, Unilever, Procter & Gamble, and Henkel dominating the landscape. These companies leverage extensive product portfolios, robust clinical-trial infrastructure, and selective distribution agreements to maintain their market leadership. Smaller entrants face challenges in gaining retail access, but niche players are finding opportunities by targeting specific consumer needs, such as eco-conscious formulations and personalized solutions. Established and emerging brands are increasingly adopting subscription models, loyalty programs, and lifestyle-centric messaging to strengthen consumer engagement and drive repeat purchases.

Technology continues to play a pivotal role in shaping the competitive landscape. Leading brands are investing in AI-driven personalization tools to enhance customer experiences. For instance, L'Oréal introduced Kérastase K Scan, a smartphone-enabled tool that analyzes hair conditions and recommends tailored formulations. Emerging disruptors are capitalizing on social-media virality to bypass traditional retail channels, while major brands are responding by reinforcing clinical claims through dermatologist endorsements, expanding direct-to-consumer channels to reduce retailer markups, and deploying AI-powered diagnostics to meet evolving consumer expectations.

Strategic acquisitions and regulatory developments are also influencing market dynamics. Major multinationals are acquiring niche or regional brands to enter specialized segments or expand eco-friendly product lines. For example, L'Oréal's acquisition of Color Wow in June 2025 and its October 2025 stake in Medik8 highlight a strategic focus on styling innovation and dermatologist-endorsed scalp care. Additionally, the European Union Greenwashing Directive (EU) 2024/825, effective March 2026, is expected to raise the evidentiary standards for environmental claims, it is likely to consolidate market share among certified-organic players with COSMOS or Ecocert seals, while eliminating ambiguous positioning previously exploited by mid-tier brands. These developments, combined with advancements in technology and marketing strategies, are shaping the future of Europe's hair care market, driving innovation and fostering growth across the region.

Europe Hair Care Industry Leaders

-

Henkel AG & Co., KGaA

-

Unilever PLC

-

L'Oréal S.A.

-

Procter & Gamble Company

-

Wella Company GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Rehab expanded its haircare range with the introduction of a new shampoo and conditioner line, enhancing its presence in the daily haircare category. This launch aligns with the brand's broader strategy to develop a comprehensive product portfolio, extending beyond its existing offerings to include core cleansing and care essentials.

- June 2025: L’Oréal announced the acquisition of Color Wow, a rapidly growing, professional haircare brand known for its "silicone-free" anti-frizz, color-treated hair, and styling product, increasing L’Oréal's foothold in haircare and styling category.

- May 2025: Unilever PLC, under its Dove brand, launched a damage-repair peptide range with the ‘Reborn Stronger’ campaign, featuring proprietary Bio-Protein Care technology, designed to repair extreme molecular-level damage in hair using amino acids and peptides. This new lineup includes shampoo, conditioner, and specialized treatments.

- January 2025: UK-registered start-up LUNESI debuted a 15-minute ritual collection in London, targeting time-pressed consumers with concentrated actives and refillable packaging.

Europe Hair Care Market Report Scope

Hair care is an overall term for hygiene and cosmetology involving hair. It encompasses a wide range of products, including shampoos, conditioners, hair colorants, and styling agents, designed to maintain, protect, and enhance the health, hygiene, and appearance of hair. Europe's hair care market is segmented by product type, category, price range, distribution channel, and geography. The market is segmented based on product type: shampoo, conditioners, hair colorants, hair styling products, and other hair care products. Based on category, the market is segmented into organic and conventional. Based on price range, the market is segmented into mass and luxury/premium. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, health and wellness stores, online retail stores, and other distribution channels. By geography, the market is segmented into Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts are provided in terms of value (USD).

By Product Type

| Shampoo |

| Conditioners |

| Hair Colorants |

| Hair Styling Products |

| Other Hair Care Products |

By Category

| Organic |

| Conventional |

By Price Range

| Mass |

| Luxury/Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Heath and Wellness Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Shampoo |

| Conditioners | |

| Hair Colorants | |

| Hair Styling Products | |

| Other Hair Care Products | |

| By Category | Organic |

| Conventional | |

| By Price Range | Mass |

| Luxury/Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Heath and Wellness Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Country | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe hair care market space in 2026?

The Europe hair care market has reached USD 25.15 billion in 2026 and is forecast to reach USD 30.94 billion by 2031.

Which country currently generates the highest revenue?

Germany leads with 22.92% share of overall value.

What compound annual growth rate is expected through 2031?

The segment is forecast to expand at a 4.23% CAGR between 2026 and 2031.

Which sales channel is expanding the quickest?

Online retail is growing at a 5.54% annual pace as consumers shift to direct-to-consumer and subscription models.

Page last updated on: