Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.40 Billion |

| Market Size (2026) | USD 4.61 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Hair Care Market Analysis by Mordor Intelligence

The Germany hair care market size was valued at USD 4.40 billion in 2025 and estimated to grow from USD 4.61 billion in 2026 to reach USD 5.76 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031). This growth is attributed to increasing awareness of scalp and hair health, driving demand for specialized treatments. Consumers, especially those with sensitivities, are showing a stronger preference for natural, organic, and "free-from" formulations. Social media, beauty trends, and endorsements significantly influence product choices and styling habits. Holistic scalp care is gaining traction, integrating seamlessly with broader self-care routines. In this mature market, value growth is primarily driven by premiumization, clean-beauty innovations, and shifts in sales channels rather than unit sales expansion. Leading multinationals are intensifying research and development efforts, focusing on scalp-health actives, natural polymers, and sustainable packaging. Meanwhile, private labels are leveraging competitive pricing to close the perceived quality gap. The aging population is expanding the demand for gentle formulations, while social media platforms are fostering trend-conscious Gen Z consumers and accelerating product launch cycles. Regulatory developments, particularly upcoming PFAS and CMR restrictions, are increasing compliance costs. However, these regulations also benefit companies with strong toxicological expertise, effectively raising the barriers to market entry.

Key Report Takeaways

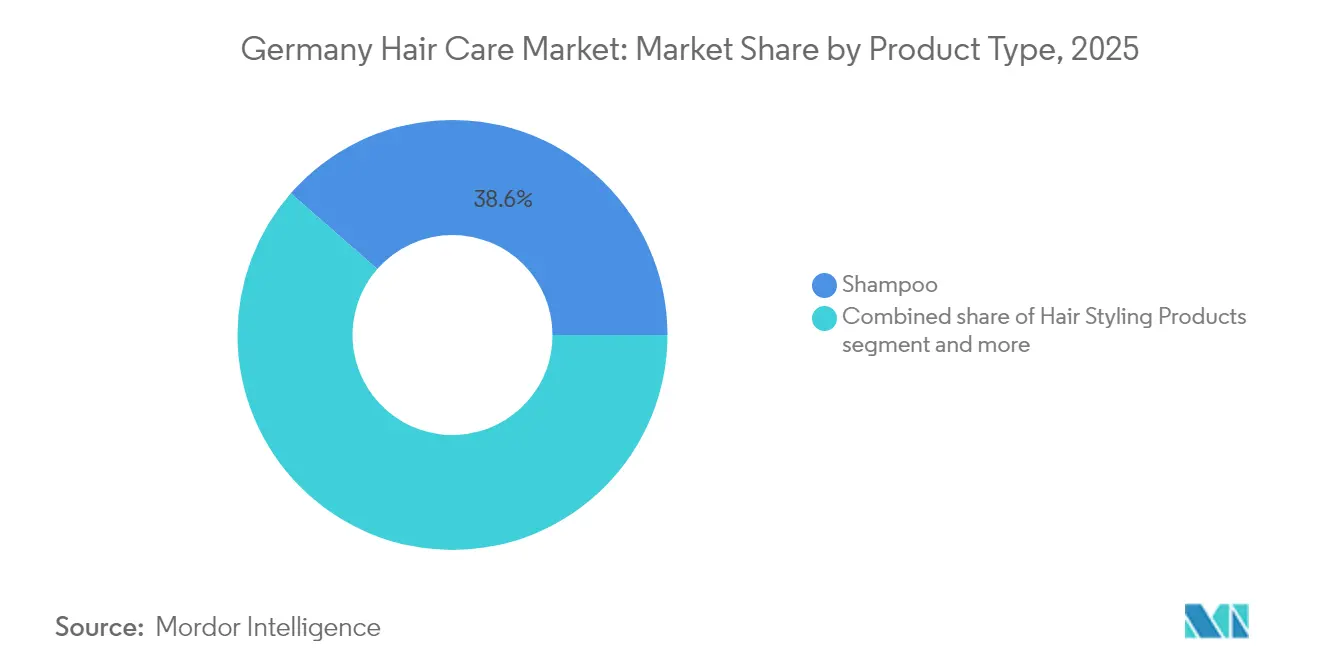

- By product type, shampoo led with 38.55% revenue share in 2025 while hair styling products are advancing at a 4.45% CAGR through 2031.

- By category, synthetic/conventional formulas retained 71.78% of the 2025 pie; natural and organic offerings are pacing ahead at a 4.96% CAGR to 2031.

- By price tier, mass products held 64.87% in 2025, whereas premium lines are projected to compound at 4.82% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets captured 38.82% in 2025, yet online retail is accelerating at a 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population spurring scalp-health products | +0.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Greater demand for premium and customized hair care | +0.6% | National, strongest in metropolitan areas | Medium term (2-4 years) |

| Rising demand for natural/organic formulations | +0.5% | National, with early adoption in Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Influence of social media and celebrity endorsements | +0.4% | National, Gen Z and Millennial focus | Short term (≤ 2 years) |

| Product innovation and packaging | +0.3% | National, premium segment emphasis | Medium term (2-4 years) |

| Trend toward multipurpose and convenient products | +0.2% | National, urban lifestyle driven | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing population spurring scalp-health products

Germany's ageing population is driving significant growth in the demand for scalp-health products, particularly those addressing hair loss, thinning, and scalp sensitivity. The country's demographic shift is creating a steady need for hair care solutions tailored to age-related issues. Individuals aged 55 and above are leading the consumption of health-focused personal care products. According to Statistisches Bundesamt, Germany's population aged 65 and older reached 19.01 million in 2024[1]Source: Statistisches Bundesamt, "Population - German Federal Statistical Office", www.destatis.de. This group not only maintains long-standing product preferences but also actively seeks solutions for thinning hair, sensitive scalps, and hair color coverage. With their strong purchasing power and preference for at-home care, this demographic is pushing the market towards innovations in gentle formulations and dermatologist-approved products. Companies are responding by launching specialized product lines featuring keratin repair technologies and active ingredients for scalp health. This trend is further supported by Germany's salon industry, which is adapting to meet the needs of older clients by focusing on hair preservation treatments rather than dramatic styling changes. Additionally, compliance with EU Cosmetics Regulation ensures high safety standards, benefiting older consumers who prioritize gentle yet effective formulations.

Greater demand for premium and customized hair care

German consumers, despite their price sensitivity, are increasingly drawn to premium positioning. Brands are effectively validating their higher price points through personalization and efficacy claims. The customization trend leverages digital diagnostics and AI-driven recommendations, with leading players investing in data collection platforms to deliver personalized formulations. German consumers are willing to pay premiums for products tailored to specific hair types and concerns, particularly when supported by scientific validation and visible results. According to the Statistisches Bundesamt, private household spending on personal care in Germany amounted to EUR 63.78 billion in 2024[2]Source: Statistisches Bundesamt, "Genesis-Online Datenbank", www.destatis.de. This shift is disrupting traditional mass-market strategies, pushing brands to adopt more advanced segmentation approaches and strengthen their direct-to-consumer capabilities. Professional salon channels are capitalizing on this trend by offering exclusive product lines and in-salon diagnostic services that justify premium pricing. This move toward customization aligns with broader European beauty trends that focus on individual needs rather than one-size-fits-all solutions.

Rising demand for natural/organic formulations

Germany's hair care market is experiencing significant growth due to the rising demand for natural and organic formulations, which are transforming product development, branding, and consumer positioning across major segments. German consumers are becoming more ingredient-conscious, actively preferring hair care products that are botanical, free from harsh chemicals, vegan, cruelty-free, and sustainably produced. Transparency in ingredient sourcing is increasingly critical, with brands focusing on sustainable supply chains and ethical sourcing practices. This trend creates opportunities for specialty ingredient suppliers offering plant-based alternatives to synthetic components while challenging formulators to maintain performance standards using natural actives. Regulatory frameworks support this transition by restricting certain synthetic ingredients and providing clear guidelines for natural product claims. As consumers perceive natural and organic products as safer, more effective, and environmentally responsible, this category is growing faster than conventional lines, driving double-digit growth for leading clean-label brands.

Influence of social media and celebrity endorsements

In Germany, younger consumers increasingly rely on social media platforms, particularly TikTok and Instagram, for discovering and purchasing hair care products. TikTok, in particular, has become a significant driver of beauty purchases following initial product discovery. Reflecting the growing importance of celebrity partnerships, Schwarzkopf named Lindsay Lohan as its global brand ambassador in July 2025. This initiative, part of an integrated marketing campaign, aims to engage both professional colorists and everyday consumers. The rise in internet adoption in Germany has amplified the impact of social media and celebrity endorsements, transforming the hair care market by influencing how consumers discover, evaluate, and purchase products. According to Statistisches Bundesamt, 98% of internet users in Germany in 2024 were aged between 16 and 44 years[3]Source: Statistisches Bundesamt, "Internet use by individuals and age groups", www.destatis.de. Digital platforms now play a crucial role not only in creating awareness but also in educating consumers. Beauty influencers build consumer confidence by demonstrating product usage and showcasing results. In response to this shift, German brands are increasingly allocating their marketing budgets to social media partnerships and user-generated content campaigns, moving away from traditional advertising methods. This shift highlights the growing importance of social media in modern marketing strategies and accelerates product launch cycles as brands quickly adapt to viral beauty trends and seasonal influences amplified on these platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated market and high brand rivalry | -0.4% | National, intense in retail channels | Long term (≥ 4 years) |

| Price sensitivity amid private-label rise | -0.3% | National, strongest in discount retail | Medium term (2-4 years) |

| Consumer skepticism about product claims | -0.2% | National, educated consumer base | Medium term (2-4 years) |

| Regulatory challenges and compliance costs | -0.1% | National, German implementation focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Saturated market and high brand rivalry

Established players face mounting competitive pressure as they defend their market share against private label growth and the entry of emerging natural brands. In Germany, the retail landscape is dominated by major chains such as Edeka, Rewe, and Schwarz Group, leading to limited shelf space and forcing brands to compete fiercely for distribution. The proliferation of brands across different price tiers creates consumer confusion and weakens marketing effectiveness, prompting higher advertising expenditures to sustain visibility. This heightened competition reduces pricing flexibility and squeezes margins, particularly for mid-tier brands caught between premium and value segments. The market becomes even more crowded with the growth of private labels, niche products, and substitutes like home-based DIY regimens. These trends raise consumer expectations and make it increasingly difficult for any single player to secure lasting loyalty or market dominance. Smaller brands struggle to manage regulatory compliance costs, especially when competing with larger players capable of absorbing higher expenses for product testing, reformulation, and multi-channel distribution. This dynamic raises barriers to entry and hinders innovation from new market entrants.

Price sensitivity amid private-label rise

Price sensitivity in Germany's hair care market, driven by ongoing economic uncertainties, is significantly influencing consumer behavior, leading to a noticeable shift from premium brands to more affordable private-label products commonly found in supermarkets and drugstores. This growing preference for cost-effective alternatives is intensifying competition among brand manufacturers, while simultaneously compressing their profit margins. As inflationary pressures persist, German consumers are increasingly prioritizing affordability, opting for lower-cost options and engaging in promotional purchasing to manage their expenses. Private label manufacturers are effectively leveraging this trend by offering products that match the quality of branded alternatives but at reduced prices, further appealing to price-conscious buyers. In response, branded manufacturers are compelled to adapt by introducing value-tier product lines and implementing promotional strategies aimed at retaining sales volumes and safeguarding brand equity. Moreover, the expanding market share of discount retail formats is creating additional challenges for premium brands, as they struggle to maintain their distribution channels and uphold their positioning in a highly competitive market landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Dominance Faces Styling Innovation

Shampoo holds a leading 38.55% market share in 2025, highlighting its critical role in daily hair care and frequent consumer repurchases. The shampoo segment, which includes anti-dandruff, moisturizing, color protection, volumizing, medicated, and natural/organic variants, meets diverse consumer preferences and hair types, sustaining its demand. Hair styling products represent the fastest-growing segment, with a projected 4.45% CAGR through 2031, driven by social media influence and the availability of professional-grade formulations in the consumer market. Conditioners are benefiting from increased awareness of hair health and damage prevention, while hair colorants face challenges from salon competition and fluctuating DIY trends. The rapid growth of the styling segment reflects the increasing sophistication of German consumers, who are more inclined to experiment with professional-quality products at home.

Brands like Henkel's Gliss differentiate themselves in competitive segments by leveraging innovations such as "Liquid Hair-Repair Technology," showcasing the impact of liquid keratin technologies and bond-building formulations. Other product categories, including treatments and masks, are gaining incremental market share through premiumization and targeted solutions for specific hair concerns. This shift aligns with a broader beauty industry trend that prioritizes multi-step routines and specialized products tailored to individual needs over generic hair care solutions.

By Category: Synthetic Strength Challenged by Natural Acceleration

Synthetic and conventional formulations dominate the market with a 71.78% share in 2025, owing to their proven efficacy and cost-effectiveness, which resonate with budget-conscious consumers. Manufacturers leverage synthetic ingredients to craft products that are stable, long-lasting, and consistent in texture, scent, and performance. Meanwhile, natural and organic alternatives are on a growth trajectory, expanding at a 4.96% CAGR through 2031, underscoring the sustainability and clean beauty values of German consumers. The natural segment gains an edge from certification frameworks like NATRUE and COSMOS, which enhance credibility and differentiation in saturated markets. As consumers become more discerning, ingredient transparency takes center stage, with many seeking products devoid of contentious synthetic components.

This shift in consumer preference poses formulation challenges for brands. They grapple with maintaining a natural image while meeting performance standards, especially in color and styling applications where synthetics have historically outperformed. To navigate this, hybrid formulations are gaining traction, melding natural actives with select synthetic ingredients to strike a balance between sustainability and efficacy. Furthermore, EU regulatory changes bolster the natural ingredient movement, curbing certain synthetic components and clarifying guidelines for marketing natural products.

By Price Tier: Mass Market Resilience Under Premium Pressure

Mass market products hold a 64.87% market share 2025, driven by their extensive distribution and value-oriented appeal to Germany's cost-conscious consumers. These products, with their affordable pricing, serve a broad demographic, ensuring availability for both urban and rural German consumers. At the same time, premium segments are expected to grow at a 4.82% CAGR through 2031. This growth is supported by an aging population seeking tailored solutions and younger consumers influenced by social media trends. The rise in premium segments stems from strategic brand positioning focused on efficacy, sustainability, and personalization, moving away from traditional luxury marketing. Furthermore, the introduction of professional-grade products into retail channels is redefining traditional price tiers and creating new competitive dynamics.

In Germany, the dominance of major retail chains facilitates the distribution of mass market products but poses challenges for premium brands, restricting their growth mainly to specialty channels. This shift in price tiers aligns with a broader European beauty trend, emphasizing a divide between value-driven and premium-oriented consumer groups. To address this, brands are increasingly implementing portfolio strategies that cover multiple price tiers, enabling them to appeal to a diverse consumer base while maintaining brand consistency and clear positioning.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Supermarkets and hypermarkets hold a leading 38.82% share 2025, leveraging their convenience and extensive product ranges to meet mainstream consumer demands. These retailers, with their broad presence across urban and rural Germany, provide consumers with easy access to essential hair care products during routine shopping trips. Online retail stores are expected to grow at a 4.88% CAGR through 2031, driven by the expansion of German e-commerce. Specialty stores remain crucial for premium and professional products, while convenience stores are increasingly benefiting from urban lifestyle trends and impulse purchases. This shift in distribution channels reflects evolving consumer shopping behaviors, accelerated by the pandemic's influence on digital adoption.

In Germany, digital transformation extends beyond e-commerce to include omnichannel strategies that combine online research with in-store purchases. This approach is particularly significant for German consumers, who often prefer physical stores for personal care products. Additionally, channels such as direct-to-consumer and subscription models are gaining popularity among younger demographics, emphasizing convenience and personalization. These changes in distribution channels offer brands opportunities to develop tailored strategies for each channel while maintaining consistent brand positioning across all touchpoints.

Geography Analysis

Germany is Europe's largest and most advanced hair care market. High levels of consumer education, strong regulatory frameworks, and established distribution networks support both domestic and international brands. Stable economic conditions and high disposable incomes drive the adoption of premium products, while regional differences reflect cultural and demographic diversity across federal states. Urban centers such as Berlin, Munich, and Hamburg lead in trend adoption and premium branding, while rural areas favor traditional mass-market products. The concentration of beauty retail in major metropolitan areas provides brands with strategic advantages for entering or expanding within the German market.

Germany's market dynamics not only shape its domestic landscape but also influence broader European trends. The country's regulatory leadership and consumer sophistication often set benchmarks for product development and marketing strategies. Centrally located within European supply chains, Germany's strong manufacturing base supports domestic production and international trade. Regional preferences vary, with southern states favoring natural and organic products, while northern regions exhibit greater price sensitivity. The market's maturity creates opportunities for niche products tailored to specific regional or demographic needs.

Consumer behavior in Germany reflects cultural values that prioritize quality, reliability, and environmental responsibility. These preferences reward brands that focus on authentic positioning and long-term relationship building rather than short-term promotions. The regulatory environment, led by the German Federal Institute for Risk Assessment, establishes safety standards that influence product development and market access across the European Union. Digital adoption is growing across all demographics, with younger consumers heavily influenced by social media, while older demographics continue to prefer traditional retail channels and professional recommendations.

Competitive Landscape

The German hair care market is moderately consolidated, with established multinational companies dominating due to their extensive portfolios and strong distribution networks. However, the growth of natural brands and the expansion of private labels are increasing competition across various price segments. Market leaders are leveraging technological advancements, sustainability initiatives, and professional channel partnerships to protect their market share against rising competition from premium niche brands and value-focused private labels. Companies are strategically optimizing their brand portfolios. For example, Henkel is divesting non-core assets while strengthening its position in high-growth segments through targeted acquisitions and investments in product innovation.

Major players hold a significant share of the market. These companies are actively implementing strategies such as product innovation, rapid market expansion, mergers and acquisitions, and partnerships to enhance their market share, expand their consumer base, and gain a competitive advantage. Key players in the market include L'Oreal SA, Henkel AG and Co.KGaA, Proctor and Gamble Company, Unilever PLC, and Beiersdorf AG. These companies are focusing on launching new products and entering new markets to meet consumer demands and secure a larger market share.

Opportunities are emerging in personalized formulations, sustainable packaging, and hybrid products that combine professional and consumer use, bridging the gap between salon and retail channels. The adoption of technology is accelerating differentiation, with innovations such as AI-driven product recommendations, digital diagnostic tools, and direct-to-consumer platforms that bypass traditional retail limitations. Established players benefit from their regulatory compliance capabilities, which provide a competitive edge, while smaller entrants face challenges due to the resource-intensive nature of safety testing and documentation requirements. In a market with limited organic growth potential, brands are focusing on continuous innovation in formulations, packaging, and marketing to stand out.

Germany Hair Care Industry Leaders

-

L'Oreal SA

-

Beirsdorf AG

-

Unilever PLC

-

Henkel AG and Co.KGaA

-

The Proctor and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: MONAT Global Corp, a globally recognized leader in social selling, has expanded into Germany, offering premium products in haircare, skincare, wellness, and beauty innovation. This launch represents the most successful international debut in the company’s history, exceeding all expectations.

- March 2025: Essence has opened one of Germany's inaugural TikTok Shops, bridging the gap between its community's active engagement and their shopping habits.

- August 2024: Kao has broadened its iconic Guhl hair care brand to include products specifically designed for children. With the debut of the new Guhl Kids line, Kao furthers its successful rebranding of Guhl, now providing multifunctional, certified natural cosmetics tailored to both parents' and children's needs.

- January 2023: L’Oréal launched a new DACH (Austria, Germany, Switzerland) organization to drive growth in a dynamic market of approximately 100 million consumers. This cluster spans six sites across the three countries, supported by a regional production and distribution hub, as well as specialized centers in digital, market intelligence, and IT.

Germany Hair Care Market Report Scope

Hair care is an overall term for hygiene and cosmetology involving the hair which grows from the human scalp and, to a lesser extent, facial and other body hair. Hair care products include Hair Conditioners, Shampoo, Hair Spray, Hair Oil, Hair Wax, Beard Oil, etc. Product types like hair spray, conditioner, shampoo, hair oil, and other product types segment Germany's hair care market. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other distribution channels. The report offers market size and forecasts in value (USD million) for the above segments. For each piece, the market sizing and forecasts have been done based on weight (in USD million).

By Product Type

| Shampoo |

| Conditioner |

| Hair Colorants |

| Hair Styling Products |

| Other Product Types |

By Category

| Synthetic/Conventional |

| Natural /Organic |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Specialty Stores |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Shampoo |

| Conditioner | |

| Hair Colorants | |

| Hair Styling Products | |

| Other Product Types | |

| By Category | Synthetic/Conventional |

| Natural /Organic | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Germany hair care market in 2026?

It is valued at USD 4.61 billion, with a projected 4.60% CAGR to 2031.

Which product category is growing fastest?

Hair styling products are expanding at a 4.45% CAGR, driven by social-media trends and salon-grade innovations.

What share do natural and organic formulas hold?

They represent the minority today but are rising at a 4.96% CAGR, gradually eroding synthetic dominance.

How important is e-commerce for hair care sales in Germany?

Online retail is the quickest-growing channel at a 4.88% CAGR, yet supermarkets still lead overall value.

Page last updated on: