Beard Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

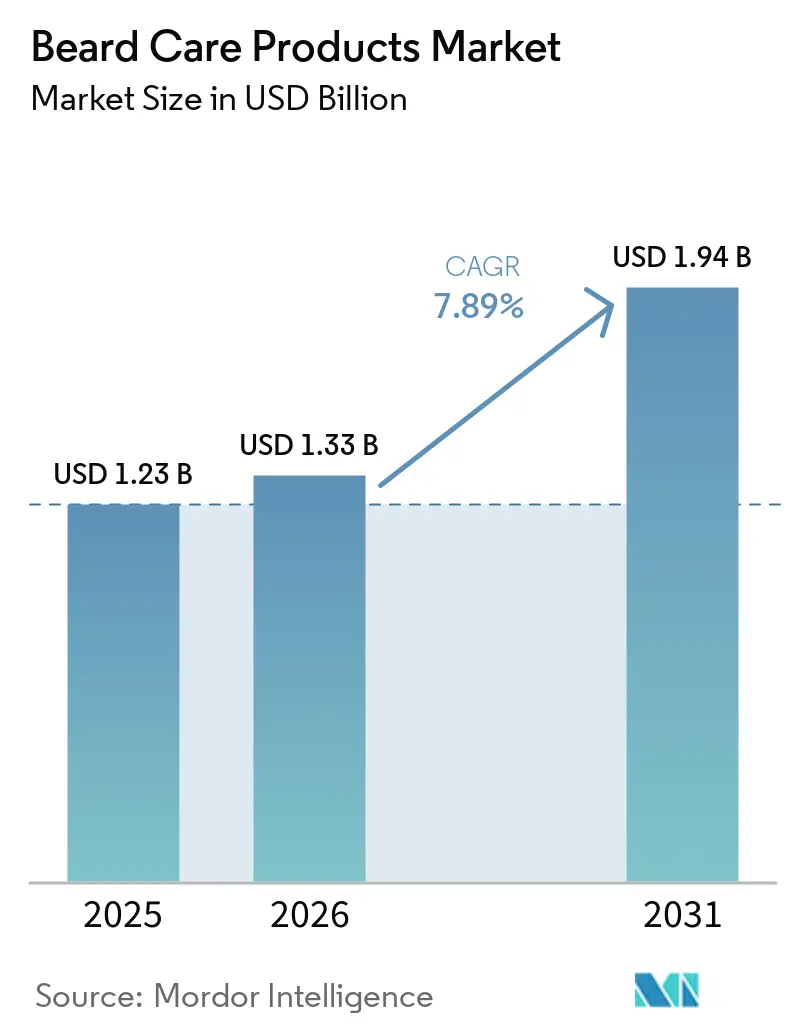

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

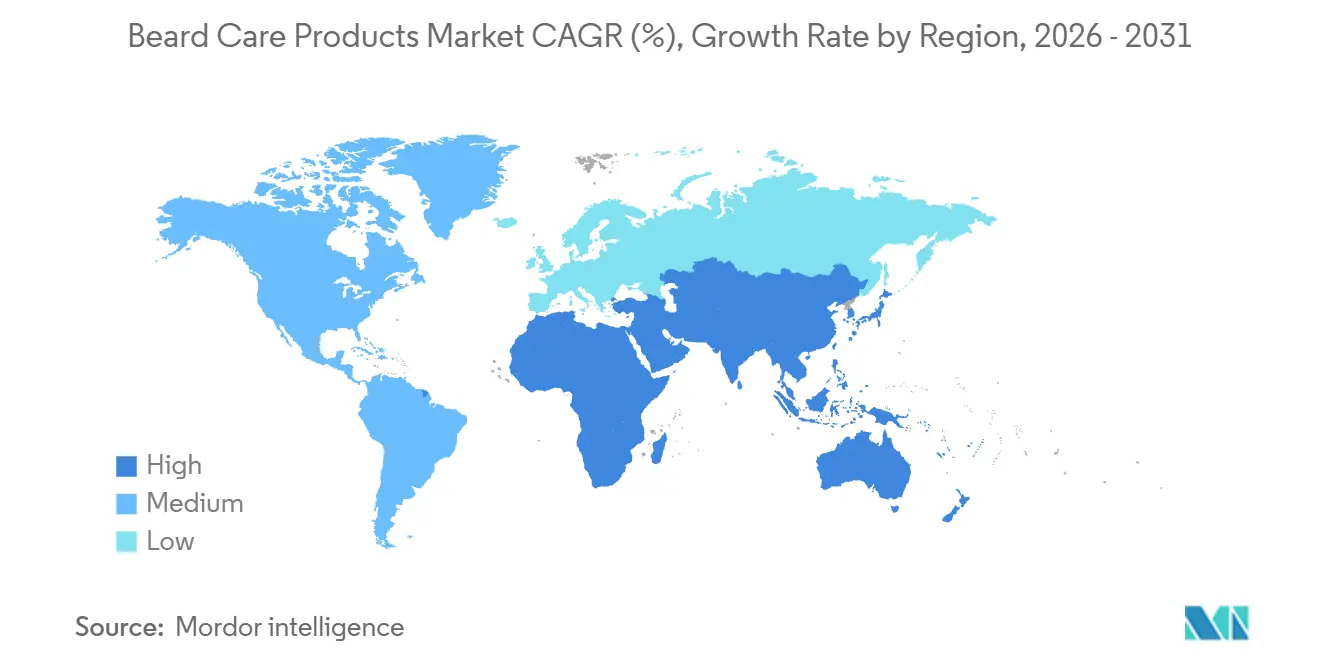

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beard Care Products Market Analysis by Mordor Intelligence

The Beard Care Products Market size is expected to grow from USD 1.23 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 1.94 billion by 2031 at 7.89% CAGR over 2026-2031. Facial hair is gaining cultural acceptance, men's personal-care routines are becoming more premium, and specialized formulas are evolving beyond basic hygiene. This shift is driven by changing consumer preferences and the growing emphasis on self-expression and individuality. Millennials, viewing grooming as self-care, now expect multi-step regimens, ingredient transparency, and experiential shopping, reflecting their desire for both functionality and indulgence in their routines. While digital commerce reshapes channel dynamics by offering convenience and variety, the resurgence of curated health-and-beauty stores underscores the enduring value of expert advice for premium purchases, particularly for consumers seeking personalized recommendations. Natural-origin products are rapidly expanding, fueled by increasing consumer awareness of sustainability and clean-label trends, but they haven't yet challenged the dominance of cost-effective, performance-driven conventional formulas that continue to meet the demands of a broader audience.

Key Report Takeaways

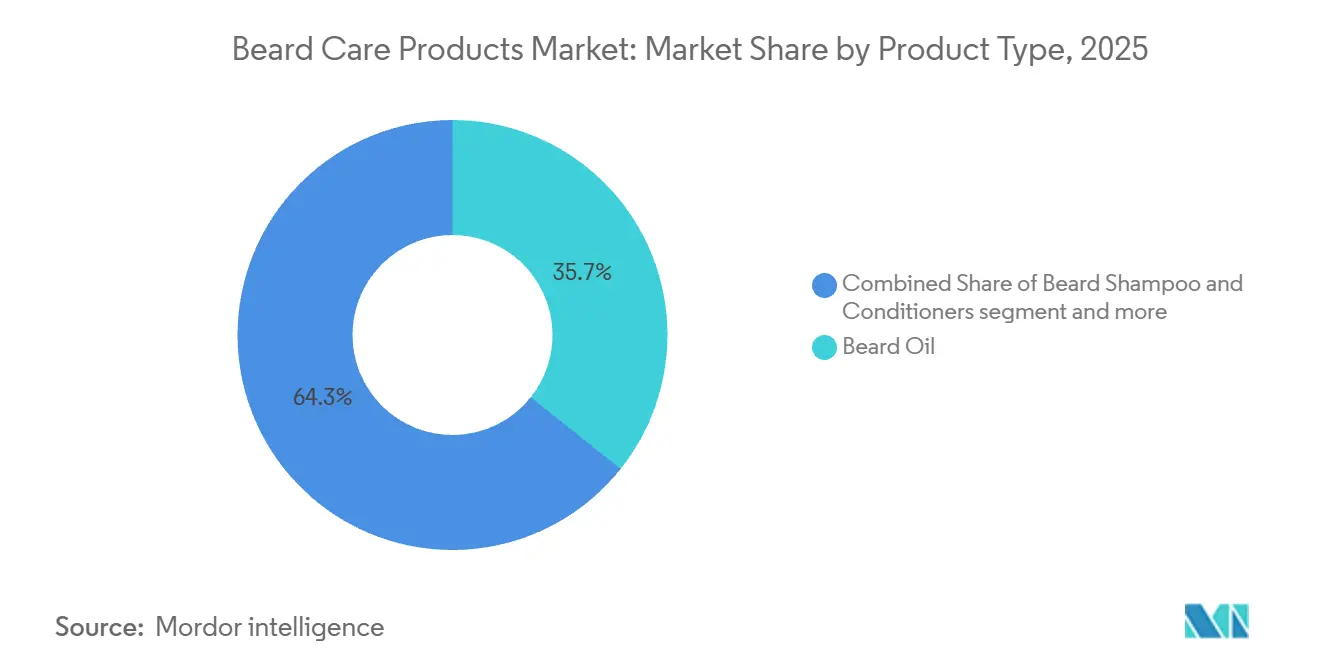

- By product type, beard oil captured 35.70% of the beard care products market share in 2025, while beard shampoo and conditioner are projected to deliver an 8.25% CAGR between 2026 and 2031.

- By formulation, conventional products accounted for 55.82% of the beard care products market size in 2025, and natural and organic offerings are set to rise at an 8.96% CAGR through 2031.

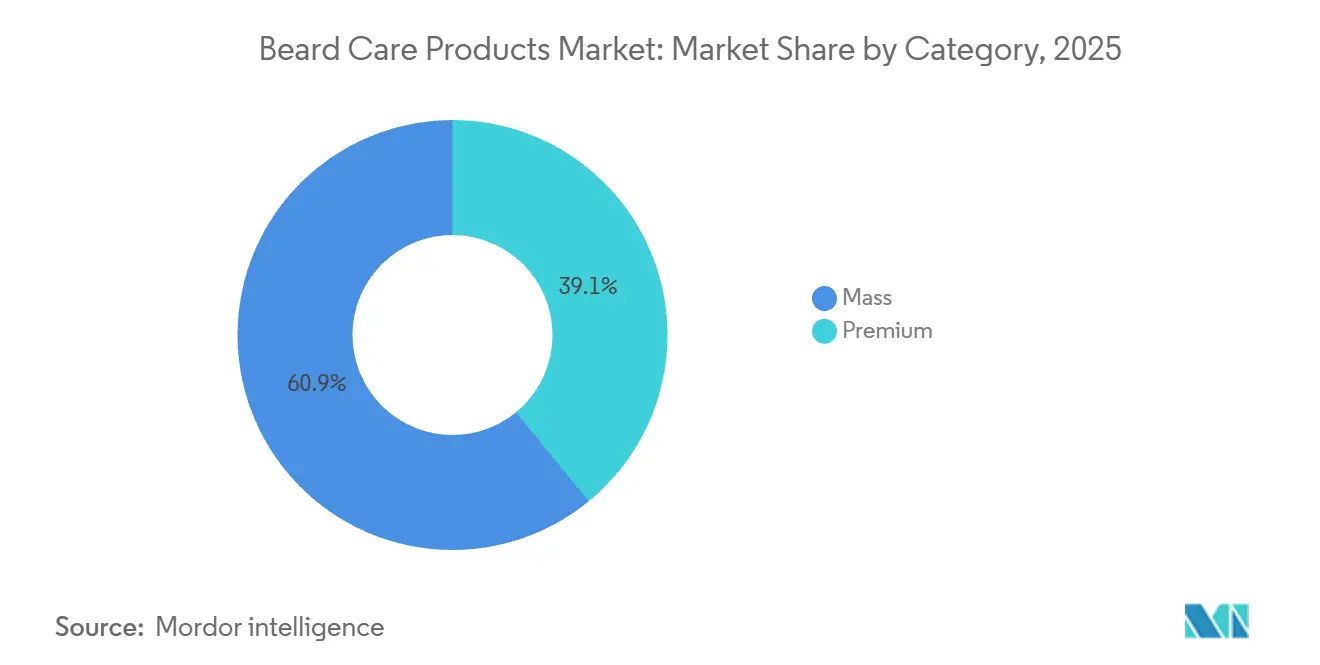

- By category, mass-market lines held 60.93% revenue share in 2025; premium lines are forecast to expand at an 9.13% CAGR during the same period.

- By distribution channel, online retail stores generated 35.67% sales in 2025, whereas health and beauty stores are advancing at an 10.23% CAGR to 2031.

- By geography, North America led with 35.78% share in 2025, but Asia-Pacific is growing fastest at a 9.78% CAGR during the outlook window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Beard Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Millennial men increasingly embrace premium grooming routines | +1.2% | North America, Europe, spill-over global | Medium term (2-4 years) |

| E-commerce and D2C subscription boxes for beard products are booming | +1.8% | North America, Asia-Pacific, global | Short term (≤ 2 years) |

| Preference for organic oils, butters, and plant-based formulas appeals to health-conscious users | +1.5% | Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Innovations are emerging in multifunctional hybrid beard-skin formulations | +0.9% | Global premium niches | Medium term (2-4 years) |

| Micro-brands proliferate on TikTok and Instagram, driven by influencers | +1.1% | North America, Europe, global | Short term (≤ 2 years) |

| Barber collaborations and grooming challenges foster brand advocacy | +0.8% | Developed markets, global spill-over | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Millennial men increasingly embrace premium grooming routines

Millennial consumers are reshaping the landscape of beard care, opting for premium grooming products once deemed luxuries by older generations. This shift isn't just about adopting new products; for millennials, grooming has evolved into a wellness practice, seamlessly blending into their broader self-care routines. Social media amplifies this trend, with grooming tutorials and product reviews crafting aspirational content that influences purchasing choices. Platforms like Instagram, YouTube, and TikTok play a significant role in showcasing grooming techniques and product effectiveness, creating a sense of community and engagement among users. By positioning themselves as premium brands, brands not only enjoy higher profit margins but also cultivate customer loyalty, underscoring perceived quality and status. Additionally, the rise of subscription-based models and personalized product offerings further strengthens brand-consumer relationships. However, the longevity of this trend hinges on sustained income growth for millennials and their commitment to grooming habits formed in their younger years.

E-commerce and D2C subscription boxes for beard products are booming

Subscription models are driving the rapid growth of the beard care market, ensuring brands enjoy recurring revenue streams and an enhanced customer lifetime value. These subscription boxes not only help consumers navigate an overwhelming array of product choices but also offer brands a steady revenue stream and insights for personalized marketing. By analyzing customer preferences and purchasing patterns, brands can tailor their offerings to meet specific needs, fostering stronger customer relationships. This approach is especially appealing to younger consumers, who prioritize convenience and are open to regular payments for essentials. Additionally, subscription models provide an opportunity for brands to introduce new products and gather feedback, creating a continuous cycle of innovation and improvement. By adopting direct-to-consumer strategies, brands can sidestep traditional retail margins, channeling those savings into acquiring and retaining customers. Yet, the long-term success of these subscription models hinges on consistently delivering quality and variety to keep customers engaged, all while managing logistics costs that threaten profitability.

Preference for Organic Oils, Butters, and Plant-Based Formulas Appeals to Health-Conscious Users

Consumers are increasingly focusing on the ingredients in personal care products, preferring those free from parabens, sulfates, phthalates, and synthetic fragrances. Natural and organic beard oils with argan, jojoba, hemp seed, and coconut oils are outperforming conventional options due to their benefits like moisture retention, anti-inflammatory properties, and suitability for sensitive skin. However, supply chain issues are driving up costs. Argan oil prices have risen sharply from USD 2.50 to USD 60 per liter due to a 40% decline in Morocco's argan forests, forcing brands to reformulate or absorb costs. Jojoba and other botanical oils face similar price volatility caused by climate change and geopolitical factors. Companies securing long-term supplier contracts, adopting vertical integration, or creating synthetic alternatives can better manage margins. Stricter regulations, such as the FDA's Modernization of Cosmetics Regulation Act of 2022, are raising compliance costs but also setting quality standards that challenge smaller competitors.

Innovations are emerging in multifunctional hybrid beard-skin formulations

Market differentiation is increasingly driven by product innovation, with multifunctional formulations catering to both beard maintenance and skin health. This trend mirrors a growing consumer preference for streamlined yet effective grooming routines. As more brands align with evolving regulations, the appetite for beard care products surges. For example, under U.S. law, items like beard oils, balms, shampoos, and conditioners fall under the cosmetic category. Consequently, brands and manufacturers in the U.S. must navigate the new mandates set by MoCRA[1]Source: United States Food and Drug Administration," Registration & Listing of Cosmetic Product Facilities and Products", fda.gov. Furthermore, these innovative formulations harness advancements in cosmetic chemistry, merging traditional beard care with skin moisturization, anti-aging benefits, and sun protection. This trend underscores a more discerning consumer base, attuned to the link between facial hair and skin health. As consumers increasingly seek transparency, the scientific validation of ingredient benefits and formulation choices gains prominence. Ultimately, the triumph of these multifunctional products hinges on authentic efficacy enhancements, steering clear of mere marketing embellishments that might dilute core performance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and poor-quality products are damaging brand trust | -1.1% | Global, with highest incidence in Asia-Pacific and online marketplaces (Amazon, third-party sellers) | Short term (≤ 2 years) |

| Fluctuations in natural oil supply chains, such as argan and jojoba, are reducing profit margins | -0.9% | Global, particularly affecting premium and natural/organic segments in North America and Europe | Medium term (2-4 years) |

| Regulators are tightening scrutiny on beard-growth claims and masculinity-focused marketing | -0.7% | North America, Europe; emerging in Asia-Pacific as regulatory frameworks mature | Medium term (2-4 years) |

| The market is overcrowded with small private-label brands, driving intense price competition | -0.8% | Global, most acute in North America and Europe mass retail channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit and poor-quality products are damaging brand trust

Counterfeit beard care products are undermining consumer trust and creating an uneven playing field for legitimate brands that prioritize quality and safety. These counterfeit items, often laced with harmful ingredients or failing to meet their promises, tarnish the reputation of the entire category. The issue is particularly pronounced in emerging markets, where lax regulatory enforcement and a price-sensitive consumer base lean towards cheaper, often counterfeit, options. In a bid to combat this, the Cosmetic Products Notification Portal (CPNP) has linked up with EU customs IT systems, enabling real-time digital product tracking. This integration allows authorities to quickly verify the authenticity of beard care products and identify counterfeits at border checkpoints. With features like mandatory ingredient disclosures, electronic listings, and inter-agency data sharing, the process of product verification and regulatory oversight has become more efficient. However, safeguarding a brand against counterfeits demands significant investment in anti-counterfeiting strategies, legal actions, and consumer awareness initiatives, often at the expense of product innovation and marketing. Ultimately, the effectiveness of these measures hinges on the dedication of regulatory bodies to enforce them and the commitment of platforms to adopt stringent verification processes for beauty product vendors.

Fluctuations in natural oil supply chains, such as argan and jojoba, are reducing profit margins

Key natural ingredients, such as argan and jojoba oils, are facing supply chain disruptions, leading to cost volatility. This volatility is particularly challenging for premium brands that emphasize natural formulations. In Europe, the spotlight on sustainability and ethical sourcing is intensifying. This push, largely fueled by initiatives like the European Green Deal and the Chemicals Strategy for Sustainability, mandates companies to uphold transparency and ensure their sourcing practices are free from deforestation[2]Source: Centre for the Promotion of Imports from Developing Countries," Which trends offer opportunities or pose threats on the European market for natural ingredients for cosmetics?", cbi.eu. The specialty oils market is notably vulnerable due to its concentrated supply sources. These sources can be easily disrupted by regional challenges, be it weather anomalies, political unrest, or trade conflicts. Brands find themselves at a crossroads, needing to satisfy consumer cravings for natural ingredients while ensuring their supply chains remain stable and cost-effective. To adeptly maneuver these challenges, brands are diversifying their supplier bases, forging sustainable sourcing partnerships, and innovating synthetic alternatives that resonate with consumer preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oils Dominate While Shampoos Surge

In 2025, beard oil commands a dominant 35.70% share of the beard care market, highlighting its pivotal role in grooming routines. Its multifunctionality, offering moisturization, styling aid, and fragrance, drives its widespread adoption, especially among newcomers to beard care. This versatility consolidates multiple grooming needs into one product, emphasizing simplicity and efficiency. Its popularity is further enhanced by its accessibility and seamless integration into daily routines, particularly for novices wary of intricate regimens. Despite a more segmented market, beard oil's broad appeal and perceived necessity solidify its cornerstone status. Consequently, it not only anchors most grooming routines but also serves as an introductory product, guiding consumers toward more specialized beard care solutions over time.

While beard shampoo and conditioner haven't yet claimed the largest market segment, they're on a rapid ascent with a projected CAGR of 8.94% through 2031. This surge signals a shift toward more discerning and health-focused grooming habits. Consumers are increasingly aware that regular hair shampoo can deplete facial hair of its natural oils, resulting in dryness, irritation, and potential long-term damage. As this awareness amplifies, so does the demand for products tailored to the unique needs of facial hair and its underlying skin. This trend dovetails with the growing adoption of multi-step grooming routines, akin to skincare regimens, underscoring a holistic approach to personal care. The 2024 Beauty Trend Report highlights this shift, noting consumers' heightened awareness of the interplay between skin and hair health. Brands that introduce well-formulated beard shampoos and conditioners, especially when integrated into a comprehensive grooming solution lineup, are poised to capitalize on this burgeoning segment.

By Formulation: Conventional Leads, Natural Gains Ground

In 2025, conventional synthetic formulations command a dominant 55.82% share of the beard care market. Their affordability, consistent performance, and widespread availability make them the go-to choice. These products resonate particularly with consumers in budget-conscious regions, where daily grooming routines prioritize reliability over botanical purity. Synthetic formulations consistently deliver predictable results in cleansing, conditioning, and styling, reinforcing their mainstream appeal. Their longer shelf life and ease of mass production bolster their retail dominance. While they might not boast the marketing allure of natural alternatives, consumers prioritize function and price over ingredient origin. Even with a rising interest in cleaner labels, the performance and accessibility of synthetics ensure their relevance, especially for those seeking practical grooming solutions.

Natural and organic beard care products are on the rise, projected to grow at an 8.96% CAGR from 2026 to 2031. This surge is fueled by heightened consumer awareness regarding ingredient safety and environmental concerns. Shoppers, now more ingredient-conscious, are not just looking for cleaner beard oils but are extending this scrutiny to shampoos, conditioners, and styling products. This shift has led brands to delve into biodegradable surfactants and plant-based preservatives. Moreover, transparent sourcing and eco-friendly narratives strike a chord with this audience. However, brands face challenges with supply chain volatility, necessitating strategies like multi-origin sourcing and investments in regenerative agriculture. Another emerging trend is hybrid formulations, which meld natural emollients with lab-developed actives, striking a balance between efficacy and a clean-label image. As skepticism towards marketing claims grows, third-party certifications and batch-level traceability are becoming vital for brands to uphold credibility and sidestep greenwashing pitfalls.

By Category: Mass Market Rules, Premium Accelerates

In 2025, mass-priced beard care products dominated the market, claiming 60.93% of total revenue. These products flourish in retail hubs like supermarkets, pharmacies, and discount chains, where their affordability and accessibility drive purchases. Thanks to economies of scale, mass-market brands offer competitive pricing, showcasing resilience even in economic downturns. Their broad appeal caters especially to consumers who value practicality over luxury. Historically basic in formulation, these brands are now rolling out enhanced sub-lines, infusing functional ingredients like anti-aging antioxidants to woo discerning buyers. Despite facing stiff competition from premium brands, the mass segment's ability to deliver reliable results at accessible price points ensures its continued significance.

On the other hand, premium beard care products, though currently holding a smaller market share, are on a rapid ascent with a projected CAGR of 9.13% from 2026 to 2031. This surge is fueled by affluent consumers in pursuit of elevated grooming experiences. Premium products entice with sophisticated packaging, unique textures, distinct fragrance profiles, and narratives that spotlight artisanal or heritage ingredients. These brands carve out a niche through emotional connections and compelling brand stories, often showcased during unboxing and through tailored customer service. To foster loyalty amidst premium pricing, they prioritize consistent quality and swift adaptability to consumer feedback. As this segment expands, it exerts pressure on mass brands to innovate, leading to a "barbell market strategy" where companies cater to both premium and mass consumers, ensuring distinct offerings that maximize value without internal rivalry.

By Distribution Channel: Online Dominates, Specialty Stores Thrive

In 2025, online platforms captured 35.67% of the beard care product distribution channel share, highlighting a shift towards convenience, variety, and competitive pricing. E-commerce, bolstered by influencer endorsements and customer reviews, especially resonates with first-time buyers, streamlining their journey from discovery to purchase. The vast selection and easy comparisons empower informed consumer choices, while swift shipping and doorstep delivery elevate the shopping experience. With rising digital literacy and the ubiquity of mobile shopping, online sales are on an upward trajectory. Projections indicate that the e-commerce segment of the beard care market, emphasizing its robust growth potential. To stay ahead, online retailers are adopting strategies like virtual consultations, subscription models, and loyalty programs, aiming to deepen customer engagement and mimic the in-store ambiance.

While not yet dominant, health-and-beauty specialist retailers are the fastest-growing channel, boasting a CAGR of 10.23%. These retailers attract consumers with personalized advice, in-store sampling, and curated product selections—elements pivotal for premium segment trade-ups. Physical retail offers a hands-on experience, from barber-station demos to skin-analysis kiosks, allowing real-time product trials, an edge over e-commerce. Brands are seizing this opportunity, crafting omnichannel strategies that merge digital and physical realms, like click-and-collect services and interactive pop-up stores. Many of these venues feature content creation zones, spurring social sharing and user-generated excitement. To sidestep channel conflicts, savvy brands synchronize pricing, inventory, and promotional messaging across platforms, ensuring a cohesive customer journey. The revival of brick-and-mortar shopping underscores its significance, especially in fortifying brand equity and cultivating shopper trust.

Geography Analysis

In 2025, North America commanded a significant 35.78% share of the market, driven by its deep-rooted grooming culture and a consumer base eager to splurge on premium offerings. With market penetration nearing saturation, brands are shifting focus to niche innovations, delving into areas such as personalized scent blending and eco-conscious refill formats. Meanwhile, the FDA's rollout of the Modernization of Cosmetics Regulation Act mandates facility registrations, product listings, and adverse event reporting, adding layers of operational complexity. However, these regulations also pave the way for burgeoning brands in the United States and beyond[3]Source: United States Food and Drug Administration," Cosmetics Constituent Update", fda.gov.

Asia-Pacific, charting a robust 9.78% CAGR, stands as the primary engine driving global expansion. Urban millennials in both China and India are increasingly mirroring Western-style icons, and the surge in e-commerce is effectively bridging previous distribution gaps. Given the region's climatic diversity, research and development efforts are becoming localized: lightweight serums are gaining traction in the humid climates of Southeast Asia, while richer balms are preferred for the colder, drier winters of Northern China. Furthermore, cross-border platforms and live-commerce streams are significantly reducing the time from exposure to purchase, benefiting brands adept at the nuances of local social-commerce practices.

Europe's market is characterized by a steady, values-driven demand. The continent's green-deal policies emphasize sustainable ingredients and recyclable packaging. This push is steering formulators towards adopting bio-based solvents and mono-material components. Meanwhile, South America and the Middle East, and Africa, though still in their infancy, present enticing opportunities for pioneering brands. However, success hinges on their ability to navigate diverse facial-hair norms and regional climatic demands. Additionally, infrastructure enhancements and regional trade agreements are poised to influence the speed of market adoption.

Competitive Landscape

The beard care products market is moderately fragmented, and competition is evenly matched between multinational FMCG giants and nimble indie labels. Global players like Unilever, L’Oréal, and Procter & Gamble harness their scale to dominate shelf space and secure raw material contracts. They boast diverse portfolios that span both mass-market and premium offerings. Notably, their acquisition of digital-first brands, exemplified by the USD 1.5 billion Dr. Squatch deal, enriches their narrative authenticity and provides specialized formulations.

Specialist brands like The Man Company, Ustraa, and Bombay Shaving Company leverage direct-to-consumer logistics and culturally resonant marketing strategies. By utilizing data analytics, they curate product launches, regional fragrances, and grooming content, enhancing consumer engagement. While their supply-chain agility facilitates swift iterations, it also introduces complexities as volumes increase. To navigate these challenges, they forge strategic alliances with third-party fulfillment providers, reducing operational risks and bolstering international growth.

Instead of overhauling formulations, these brands focus on integrating technology—employing AI-driven recommendation systems, managing subscriptions, and ensuring ingredient traceability through blockchain. As regulations tighten, companies that weave compliance into their design processes gain a competitive edge, raising barriers for newcomers. Today's branding skirmishes emphasize credibility—underscored by clinical endorsements, ethical sourcing, and open communication—over mere price competition.

Beard Care Products Industry Leaders

-

L’Oréal S.A.

-

Unilever PLC

-

Procter & Gamble

-

Marico Ltd

-

Honest Amish

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unilever bolstered its foray into premium segments by acquiring Dr. Squatch, a direct-to-consumer men's personal care brand, from Summit Partners. This move underscores Unilever's emphasis on natural products, often propelled by viral marketing.

- December 2024: Weatherbeard unveiled a new line of beard oils, crafted from essential oils like tea tree, cedarwood, and lavender. These oils are now available through various online retail platforms.

- October 2024: The Noble Product Co. introduced nutrient-rich beard butters, formulated for enduring softness. Packed with essential nutrients, these butters not only ensure a polished appearance but also promote healthy beard growth.

- August 2024: Emami, having secured full ownership, strengthened its foothold in India's digital-first men's grooming arena, broadening its premium online offerings and gaining operational oversight of The Man Company.

Global Beard Care Products Market Report Scope

| Beard Oil |

| Beard Shampoo and Conditioner |

| Others |

| Natural and Organic |

| Conventional |

| Mass |

| Premium |

| Supermarkets and Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distibution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Beard Oil | |

| Beard Shampoo and Conditioner | ||

| Others | ||

| By Formulation | Natural and Organic | |

| Conventional | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distibution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the beard care products market?

The beard care products market size reached USD 1.33 billion in 2026.

How fast is the beard care products market expected to grow?

The market is forecast to register a 7.89% CAGR between 2026 and 2031.

Which region is growing fastest for beard care sales?

Asia-Pacific leads growth with a projected 9.78% CAGR through 2031.

Which product segment shows the strongest expansion?

Beard shampoos and conditioners are set to rise at an 8.25% CAGR, the quickest among product types.

Page last updated on: