LPDDR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 39.58 Billion |

| Market Size (2031) | USD 86.63 Billion |

| Growth Rate (2026 - 2031) | 16.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LPDDR Market Analysis by Mordor Intelligence

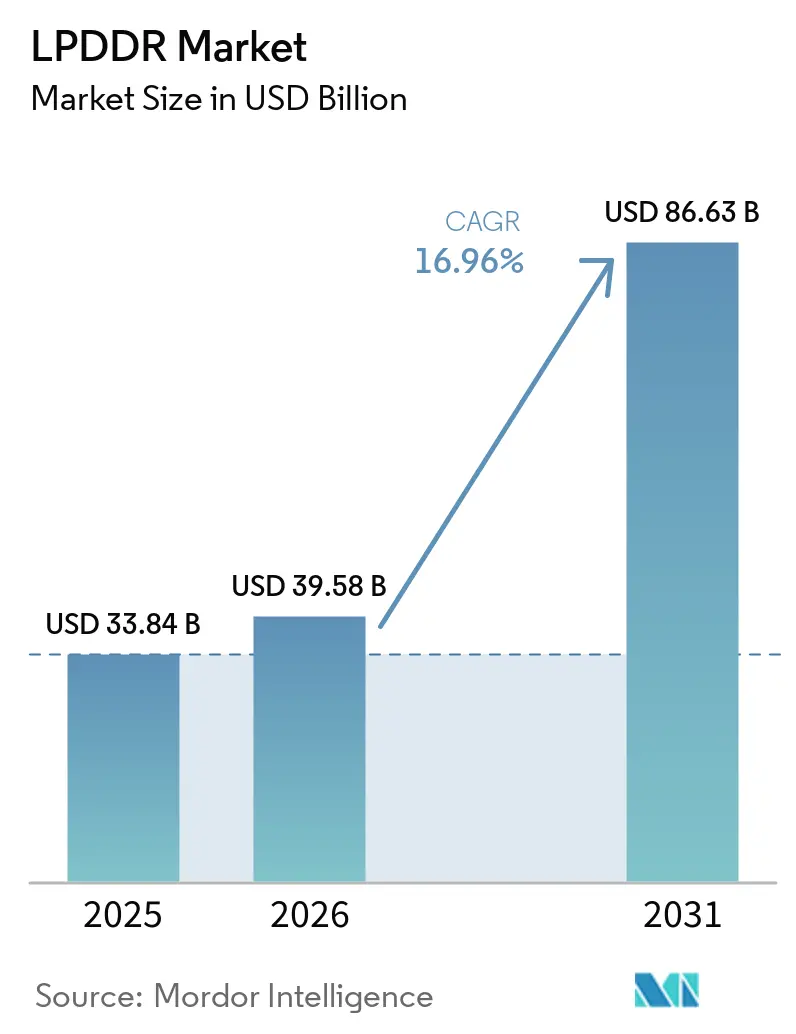

The LPDDR market size is expected to increase from USD 33.84 billion in 2025 to USD 39.58 billion in 2026 and reach USD 86.63 billion by 2031, growing at a CAGR of 17% over 2026-2031. The LPDDR market is moving beyond its older dependence on smartphone replacement cycles because demand is now being reinforced by on-device AI, AI server memory architectures, and software-defined vehicle platforms. A second shift in the LPDDR market comes from the way major suppliers are directing advanced capacity toward high-bandwidth memory, which tightens LPDDR supply even as demand broadens across devices and infrastructure. The next technology step also supports this expansion, as LPDDR6 is nearing commercial production and is set to push higher bandwidth and lower power use into premium mobile and server designs. Competitive behavior in the LPDDR market remains shaped by a narrow supplier base, and that structure is helping incumbents protect pricing and allocation power through the first half of the forecast period. The result is that the LPDDR market is being driven by both stronger end demand and tighter supply discipline at the same time.

Key Report Takeaways

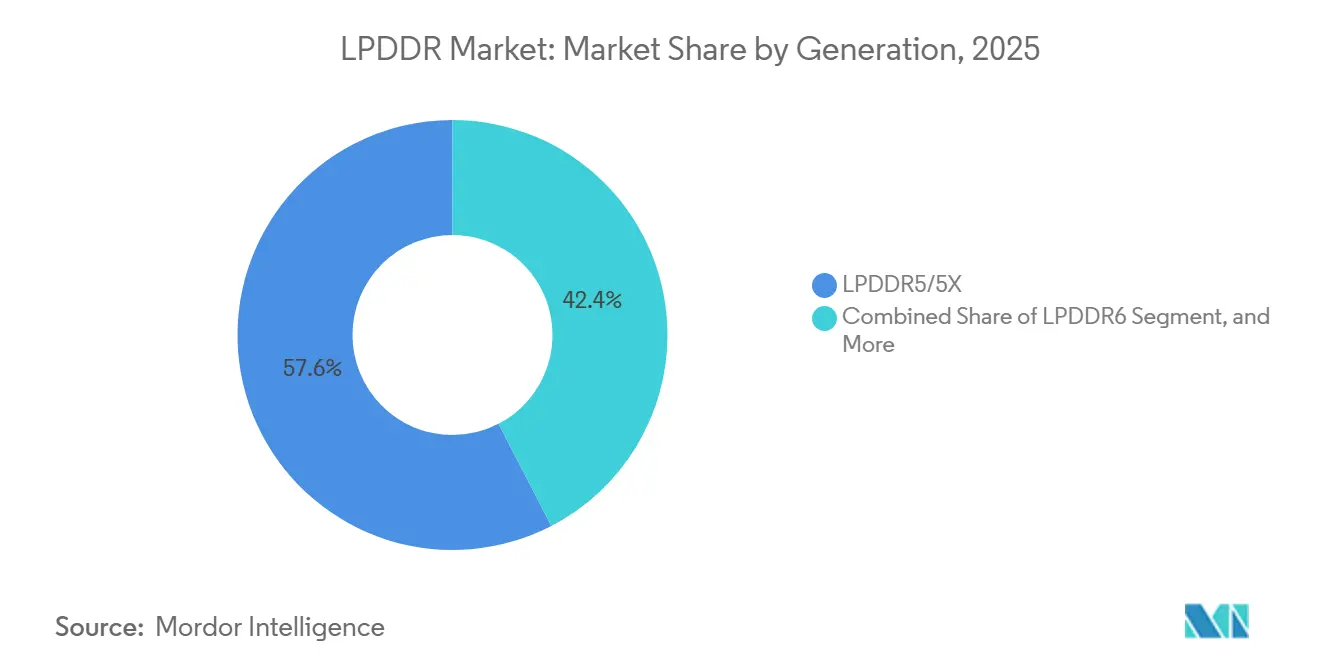

- By generation, LPDDR5/5X led with 57.6% revenue share of the LPDDR Market in 2025, while LPDDR6 is forecast to expand at an 18.9% CAGR through 2031.

- By package capacity, the 8 GB to 16 GB tier held 40.7% revenue share in 2025, while the above-16 GB tier is projected to grow at an 18.6% CAGR through 2031.

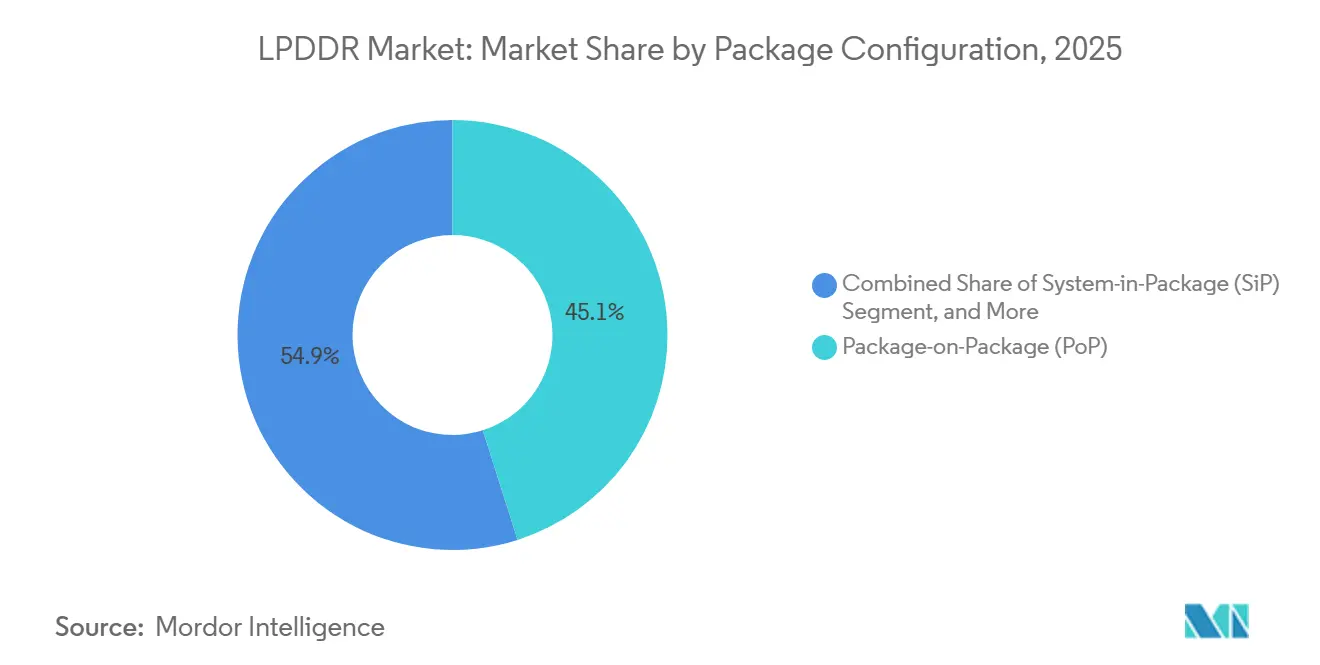

- By package configuration, Package-on-Package held 45.1% revenue share in 2025, while System-in-Package is forecast to advance at an 18.8% CAGR through 2031.

- By application, consumer electronics accounted for 72.4% revenue shareof the LPDDR market in 2025, while server and data center modules are projected to record an 18.1% CAGR through 2031.

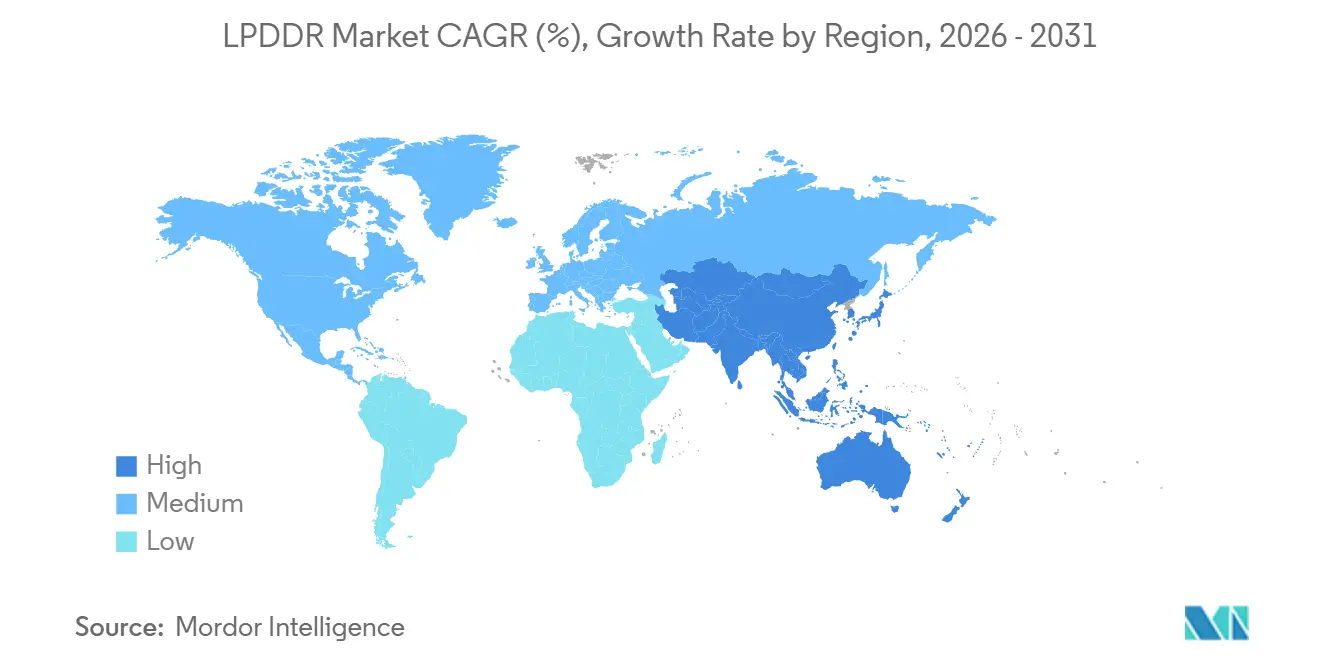

- By geography, Asia-Pacific captured 51.8% revenue share in 2025 and is also projected to post the highest regional CAGR at 17.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LPDDR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ai Smartphones Raising Lpddr Content Per Device | +5.0% | Global, led by APAC, China, South Korea, India | Short term (≤ 2 years) |

| Lpddr Expansion Into Ai Server And Client Modules | +4.5% | Global, North America and APAC core | Medium term (2-4 years) |

| 5g Premium-To-Mid-Tier Migration Into Lpddr5/5x | +2.5% | APAC core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Sdv And Adas Memory Demand Scaling In Vehicles | +1.8% | Europe and North America, APAC emerging | Medium term (2-4 years) |

| Ai Pcs And Ultra-Thin Notebooks Preferring Soldered Lpddr | +1.2% | Global, North America and East Asia | Short term (≤ 2 years) |

| Lpddr4x Scarcity Accelerating Forced Refresh Cycles | +0.9% | APAC core, spill-over to Middle East and Africa and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI Smartphones Raising Lpddr Content Per Device

The LPDDR market is benefiting from the way on-device AI is changing the minimum memory requirement for premium smartphones. Device makers are no longer treating memory as a background component because AI assistants, local inference, image generation, and always-on language features all place more weight on memory bandwidth and power efficiency. Samsung is already positioning LPDDR6 as memory optimized for high-performing on-device AI, which shows that mobile AI demand is influencing memory road maps before the broad commercial rollout begins.[1]Samsung Semiconductor, “Introducing Samsung's SOCAMM2: New LPDDR Memory Module Empowering Next-generation AI Infrastructure,” Samsung Semiconductor Global Newsroom, semiconductor.samsung.com Samsung also began mass production of thinner LPDDR5X packages for mobile AI devices, which supports the need for more memory in compact form factors without giving up thermal stability. In the LPDDR market, this means memory content per phone is becoming a product-defining specification rather than a background cost line.

LPDDR Expansion Into Ai Server And Client Modules

The LPDDR market is also expanding because low-power DRAM is now moving into AI server and client module designs. Samsung introduced its SOCAMM2 module for AI data centers and disclosed technical collaboration with NVIDIA, which confirms that LPDDR is now part of mainstream accelerator infrastructure planning rather than a side experiment. SK Hynix is in mass production of a 192 GB SOCAMM2 module for NVIDIA's Vera Rubin platform, and the company said the module offers more than double the bandwidth and over 75% better power efficiency than conventional RDIMM.[2]SK Hynix, “SK hynix Begins Mass Production of 192GB SOCAMM2,” SK Hynix Newsroom, news.skhynix.com Micron has also shipped customer samples of a 256 GB SOCAMM2 and said the design improves time-to-first-token for long-context inference while delivering stronger performance per watt.[3]Micron Technology, “Micron Sets New Benchmark with the World's First High-Capacity 256GB LPDRAM SOCAMM2 for Data Center Infrastructure,” NASDAQ Press Release, nasdaq.com In the LPDDR market, server adoption matters because it adds a durable infrastructure demand stream that is not tied to handset shipment cycles.

5g Premium-To-Mid-Tier Migration Into Lpddr5/5x

The LPDDR market is seeing broader support from the spread of 5G features into mid-tier phones. As more devices need to manage modem workloads, camera processing, AI tasks, and battery limits at the same time, LPDDR5 and LPDDR5X move deeper into volume segments that once depended on older memory generations. GSMA stated that mobile technologies generated USD 7.6 trillion for the global economy in 2025 and projected that value to reach USD 11.3 trillion by 2030 as 5G and AI adoption accelerate.[4]GSMA, “The Mobile Economy 2026,” GSMA Intelligence, gsma.com That wider mobile upgrade cycle supports the LPDDR market because the addressable base expands even when flagship volumes alone are not enough to explain growth. It also keeps demand distributed across premium and mid-range devices, which is important when supply remains selective.

Sdv And Adas Memory Demand Scaling In Vehicles

The LPDDR market is gaining a second long-cycle demand base from software-defined vehicles and advanced driver assistance systems. EE Times Asia reported that automakers are now competing with AI infrastructure developers for memory supply, which shows that automotive demand is large enough to affect broader allocation patterns. Samsung's 12nm-class automotive LPDDR5X achieved ASIL D certification, which places low-power DRAM into safety-critical vehicle systems where qualification demands are much higher than in consumer devices. The LPDDR market benefits from this shift because vehicle programs run on long design cycles and create revenue visibility once platforms move into production. Automotive demand is therefore not only adding volume, but it is also adding a slower and more durable replacement rhythm to the LPDDR market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Three-To-Four-Vendor Concentration Amplifying Pricing Swings | -1.5% | Global | Short term (≤ 2 years) |

| Advanced-Node Yield Pressure Delaying Lpddr6 Cost Curves | -0.9% | East Asia, South Korea, Taiwan | Medium term (2-4 years) |

| Hbm And Ddr5 Allocation Crowding Out Mobile LPDDR Supply | -0.7% | Global | Short term (≤ 2 years) |

| Automotive Safety And Thermal Qualification Lengthening Design-Ins | -0.5% | Europe, North America, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Three-To-Four-Vendor Concentration Amplifying Pricing Swings

The LPDDR market remains exposed to pricing swings because supply is concentrated in a small number of producers. That structure helps leading vendors protect margins, but it also makes downstream device makers more sensitive to abrupt changes in allocation and contract terms. The rise of CXMT offers some counterweight, and the company began mass production of LPDDR5X memory chips in 2025 for several Chinese device makers. Even so, export controls continue to limit how quickly new capacity can close the gap at advanced nodes, which keeps the LPDDR market dependent on a narrow set of established suppliers. This leaves the LPDDR market vulnerable to price-driven demand stress in cost-sensitive smartphones and other lower-end devices.

Advanced-Node Yield Pressure Delaying Lpddr6 Cost Curves

The LPDDR market also faces a timing risk because LPDDR6 performance gains do not automatically translate into fast cost normalization. JEDEC workshop materials showed that LPDDR6 introduces dual-domain core power, mandatory DVFS across all operating modes, and broader reliability requirements, which means platform integration work is more demanding than a simple speed upgrade. Additional JEDEC material from Micron described new power supply, interface, and reliability features that further raise the amount of validation needed across controllers, PMICs, and system designs. SK Hynix has already developed 1c LPDDR6 and is preparing shipments in the second half of 2026, but early production still depends on stable yields at advanced nodes. For the LPDDR market, that means commercialization can begin before cost curves fully settle, which keeps near-term pricing power with incumbent suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Generation: Lpddr5/5x Leads Current Demand While Lpddr6 Builds The Next Upgrade Cycle

LPDDR5/5X held 57.6% of the LPDDR market share in 2025, and LPDDR6 is projected to expand at an 18.9% CAGR through 2031. The leading position of LPDDR5/5X comes from its wide use across flagship phones, upper mid-range devices, AI PCs, and the first wave of server SOCAMM2 modules. In the LPDDR market, that breadth matters because one memory interface is now serving mobile, client, and infrastructure use cases at the same time. AMD said LPDDR5X will support its push for server energy efficiency, which shows that the standard is being validated well beyond handsets.

LPDDR6 is the next growth point in the LPDDR market because it raises both bandwidth and power efficiency for AI-heavy devices. SK Hynix said its 1c LPDDR6 improves power efficiency by more than 20% over LPDDR5X and targets AI-enabled smartphones and tablets in the second half of 2026. Samsung is also framing LPDDR6 around on-device AI performance, which suggests the transition will start at the premium end before moving into broader volume bands. Legacy LPDDR4 and LPDDR4X remain in structural decline as suppliers reduce commitment to older nodes, and JEDEC's published LPDDR6 architecture sets a higher baseline for future compliance, power management, and reliability in the LPDDR industry.

By Package Capacity: Mid-To-High Density Tiers Gain Ground As Ai Workloads Expand

The 8 GB to 16 GB band captured 40.7% of the LPDDR market size in 2025, while the above-16 GB tier is set to grow at an 18.6% CAGR through 2031. This middle tier sits at the center of the LPDDR market because it matches the memory needs of premium smartphones and thin notebooks without creating the full thermal and cost burden of the highest configurations. In practical terms, 12 GB and 16 GB configurations are becoming the working floor for devices that need local AI features, stronger multitasking, and longer software support windows. The LPDDR market is then pulled upward by a different group of products, namely, premium phones and AI server modules that require much larger memory footprints.

That second group gives the above-16 GB tier unusual resilience inside the LPDDR market. SK Hynix is in mass production of a 192 GB SOCAMM2 module, and Micron has sampled a 256 GB design, which shows that very high-capacity LPDDR is already moving into deployed server architectures. Lower capacity bands still serve entry devices and cost-sensitive regions, but supplier focus is shifting toward denser, higher-margin products. In the LPDDR market, that supply preference strengthens the long-term case for high-capacity tiers even when low-end device demand remains uneven. The transition also reflects how the LPDDR industry is moving from pure volume growth to value growth driven by more memory per device.

By Package Configuration: Pop Remains The Core Mobile Format While Sip Gains In Tighter Designs

Package-on-Package held 45.1% of the LPDDR market size in 2025, while System-in-Package is projected to expand at an 18.8% CAGR through 2031. PoP remains central to the LPDDR market because mobile SoCs still depend on tight memory-to-logic integration, short trace lengths, and very thin package profiles. Samsung said its 12nm-class LPDDR5X packages reduced thickness by 9% and improved heat resistance by 21.2% versus the prior generation, which supports PoP's position in compact AI devices. In the LPDDR market, ongoing gains in package thickness and thermal behavior help PoP defend its lead even as workloads become heavier.

SiP is rising because some device categories now need more functional density in less board area than PoP alone can provide. That is especially relevant in compact edge AI devices, wearables, and some automotive control units, where memory, logic, and power management need to sit in one tightly managed module. MCP still has a role in lower-tier smartphones and entry IoT products, where combining LPDDR and storage supports cost control. Discrete packages also remain important in applications that value board-level serviceability and separate qualification cycles, but the overall LPDDR market is moving toward denser integration paths. Rambus reinforced that direction by launching a SOCAMM2 server module chipset, which broadens the ecosystem around modular low-power memory integration above the die level.

By Application: Consumer Electronics Stays Largest While Server Demand Reshapes The Opportunity

Consumer electronics accounted for 72.4% of the LPDDR market size in 2025, and server and data center modules are advancing at an 18.1% CAGR through 2031. Smartphones and tablets still anchor the LPDDR market because they account for the largest installed base and the highest shipment volumes. Even so, the faster rise of server demand is starting to change the shape of the LPDDR market by adding a new source of recurring procurement from hyperscalers and accelerator platforms. Samsung's SOCAMM2 program for NVIDIA, SK Hynix's 192 GB module, and Micron's 256 GB sample all show that low-power memory is moving into mainstream AI infrastructure design.

Micron's white paper also showed that high-capacity LPDDR5X SOCAMM2 can improve long-context inference efficiency, which gives infrastructure buyers a practical reason to add LPDDR alongside accelerator deployments. Automotive electronics is the next strategically important application in the LPDDR market because qualification cycles are long, and once designed in, memory content tends to stay attached to a platform for years. Industrial and edge AI demand is smaller but diverse, and it values extended temperature performance, long life cycles, and lower power use. Networking and embedded systems add steady demand as LPDDR continues to fit controllers and gateways that need stronger efficiency than conventional DDR options. This mix shows that the LPDDR market is broadening from a consumer-led base into a multi-application demand structure.

Geography Analysis

Asia-Pacific held 51.8% of the LPDDR market share in 2025, and it is projected to record the fastest regional CAGR at 17.9% through 2031. The region leads the LPDDR market because it combines South Korean production strength, Taiwanese packaging depth, and Chinese end demand in one closely linked supply chain. South Korea remains the main supply anchor, with Samsung and SK Hynix driving the transition into LPDDR6 and server-class SOCAMM2 products. China is important both as a major buyer and as an emerging producer, with CXMT pushing deeper into advanced mobile DRAM while still facing equipment-related constraints. The LPDDR market in Asia-Pacific also reflects a split between strong premium demand and pressure at the lower end when memory costs rise too quickly.

North America holds a strategically important role in the LPDDR market because it concentrates many of the largest AI infrastructure buyers. Demand from hyperscalers and platform developers is now helping shift LPDDR into server architectures, and that gives the region influence beyond its share of direct wafer capacity. Micron remains the only large-scale North American DRAM producer, and the company said its 1-gamma node was on track to become the majority of its DRAM bit production by mid-2026. AMD's support for LPDDR5X in future server platforms also shows that North America is shaping system architecture choices that ripple across the LPDDR market.

Europe is more of a demand center than a production base in the LPDDR market, with automotive and industrial electronics driving most of its strategic importance. Germany, France, and the United Kingdom are central because vehicle platforms and industrial controls increasingly need qualified low-power memory. Samsung's automotive LPDDR5X reached ASIL D certification, which supports use in the European shift toward higher-content ADAS and centralized vehicle computing. Rest-of-the-World markets remain more dependent on consumer electronics demand, and in the LPDDR market their growth is more exposed to affordability pressure when memory becomes a larger part of total device cost.

Competitive Landscape

The LPDDR market is highly concentrated, and Samsung Electronics, SK Hynix, and Micron Technology together represented a significant share of global DRAM revenue in Q1 2026. That concentration gives the LPDDR market a clear triopoly structure in which capital allocation, node migration, and customer prioritization by a few suppliers can shape supply conditions for the entire value chain. Samsung and SK Hynix are competing for technology leadership in LPDDR6, while Micron is pushing process execution and very high-capacity server modules to protect its position. SK Hynix has developed 1c LPDDR6 for AI mobile devices, and Micron has shipped the industry's highest-capacity 256 GB LPDRAM SOCAMM2 sample for data center infrastructure. Samsung also disclosed LPDDR6 architecture work through JEDEC materials and has paired that with early SOCAMM2 collaboration, which shows that the LPDDR market is being contested at both the standards layer and the product layer.

CXMT is the main disruptive force outside the Big Three in the LPDDR market, and its move into LPDDR5X mass production gives Chinese OEMs a more local sourcing option. Even so, the company still faces export-control limits that slow its ability to scale at the most advanced nodes, which means the broader balance of power in the LPDDR market has not shifted in a decisive way. Taiwan-based Nanya is using stronger memory conditions to fund new capacity, and the company completed a NTD 78.7 billion private placement, equivalent to USD 2.49 billion, to support advanced fab construction in Taishan District. These moves matter in the LPDDR market because second-tier producers can improve supply resilience even if they do not break the triopoly in the near term.

Competition is also widening above the die level in the LPDDR market. Rambus launched a SOCAMM2 chipset for AI servers, which can support third-party module development and reduce how much of the ecosystem depends on vertically integrated memory vendors alone. Qualcomm and MediaTek remain important to demand creation, but they act as LPDDR customers and SoC integrators rather than core supply-side memory manufacturers. That distinction matters because the LPDDR market still captures value primarily through DRAM design, process technology, yield control, and advanced packaging execution. The competitive picture therefore remains concentrated at the chip level even as ecosystem participation broadens around modules, controllers, and system integration.

LPDDR Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

ChangXin Memory Technologies, Inc.

Nanya Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nanya Technology completed a NTD 78.7 billion, approximately USD 2.49 billion, private placement, bringing Kioxia, Solidigm, and Cisco as strategic investors, with all proceeds designated for advanced memory fab construction in New Taipei City's Taishan District and targeting 80-100% capacity expansion within 3 years.

- April 2026: Rambus announced a SOCAMM2 chipset for AI server platforms, including SPD Hub and 12 A and 3 A voltage regulators, extending the ecosystem for third-party LPDDR5X-based server module development and broadening the competitive landscape above the DRAM die level.

- March 2026: SK Hynix announced the successful development of 16 Gb LPDDR6 DRAM on its sixth-generation 10nm-class, 1c, process, achieving operating speeds above 10.7 Gbps with over 20% improved power efficiency compared to LPDDR5X. The company plans to complete mass-production preparations in H1 2026 and begin shipments in H2 2026, targeting AI-enabled smartphones and tablets.

- February 2026: Samsung Electronics and SK Hynix jointly demonstrated LPDDR6 silicon achieving 14.4 Gbps per pin at the International Solid-State Circuits Conference in San Francisco, representing 35% bandwidth improvement over LPDDR5X's maximum 10.7 Gbps speed, in compliance with the JEDEC LPDDR6 standard published in August 2025.

Global LPDDR Market Report Scope

The LPDDR Market refers to the market for low-power dynamic memory used in mobile and power-sensitive devices such as smartphones, tablets, laptops, wearables, and edge devices. It includes LPDDR chips and related memory solutions designed to deliver high bandwidth while reducing power consumption and heat generation.

The LPDDR Market Report is Segmented by Generation (LPDDR3, LPDDR4/4X, LPDDR5/5X, and LPDDR6), Package Capacity (Up to 4 GB, 4GB to 8 GB, 8 GB to 16 GB, and Above 16 GB), Package Configuration (Discrete LPDDR Packages, Package-on-Package (PoP), Multichip Packages (MCP), and System-in-Package (SiP)), Application (Consumer Electronics, Automotive Electronics, Industrial and Edge AI Devices, Networking and Embedded Systems, and Server and Data Center Modules), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| LPDDR3 |

| LPDDR4/4X |

| LPDDR5/5X |

| LPDDR6 |

| Up to 4 GB |

| 4 GB to 8 GB |

| 8 GB to 16 GB |

| Above 16 GB |

| Discrete LPDDR Packages |

| Package-on-Package (PoP) |

| Multichip Packages (MCP) |

| System-in-Package (SiP) |

| Consumer Electronics | Smartphones and Tablets |

| Laptops | |

| Other Consumer Electronics | |

| Automotive Electronics | |

| Industrial and Edge AI Devices | |

| Networking and Embedded Systems | |

| Server and Data Center Modules | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Generation | LPDDR3 | |

| LPDDR4/4X | ||

| LPDDR5/5X | ||

| LPDDR6 | ||

| By Package Capacity | Up to 4 GB | |

| 4 GB to 8 GB | ||

| 8 GB to 16 GB | ||

| Above 16 GB | ||

| By Package Configuration | Discrete LPDDR Packages | |

| Package-on-Package (PoP) | ||

| Multichip Packages (MCP) | ||

| System-in-Package (SiP) | ||

| By Application | Consumer Electronics | Smartphones and Tablets |

| Laptops | ||

| Other Consumer Electronics | ||

| Automotive Electronics | ||

| Industrial and Edge AI Devices | ||

| Networking and Embedded Systems | ||

| Server and Data Center Modules | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the LPDDR market?

The market stood at USD 33.84 billion in 2025 and is projected to reach USD 86.63 billion by 2031, growing at an 16.96% CAGR from 2026 to 2031.

Which LPDDR generation is leading today?

LPDDR5/5X led with 57.6% revenue share in 2025 because it serves flagship phones, AI PCs, and early server module deployments.

Why is LPDDR6 important for the next upgrade cycle?

LPDDR6 is projected to grow at an 18.9% CAGR through 2031 and brings higher bandwidth with lower power use, making it important for AI phones and future high-density computing platforms.

Which application area is changing the demand picture fastest?

Server and data center modules are the fastest-growing application, with an 18.1% CAGR through 2031, because hyperscalers and accelerator platforms are adopting LPDDR5X-based SOCAMM2 designs.

Why does Asia-Pacific lead this space?

Asia-Pacific held 51.8% revenue share in 2025 and is growing at 17.9% through 2031 because the region combines South Korean memory production, Taiwanese packaging capability, and strong Chinese device demand.

How concentrated is the supplier base?

The supplier base is highly concentrated, with Samsung, SK Hynix, and Micron accounting for more than 89% of DRAM revenue in Q1 2026, which supports pricing power and tight supply control.

Page last updated on: