LPDDR5 Package-on-Package (PoP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

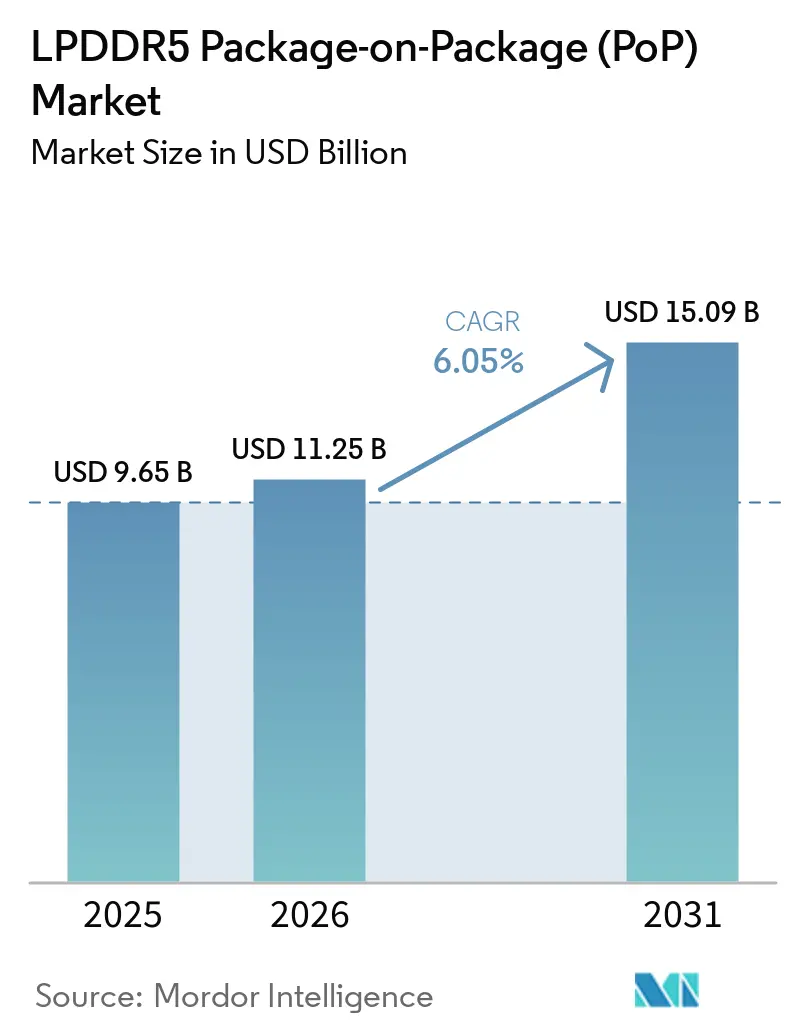

| Market Size (2026) | USD 11.25 Billion |

| Market Size (2031) | USD 15.09 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LPDDR5 Package-on-Package (PoP) Market Analysis by Mordor Intelligence

The LPDDR5 Package-on-Package market size is expected to increase from USD 9.65 billion in 2025 to USD 11.25 billion in 2026 and reach USD 15.09 billion by 2031, growing at a CAGR of 6.05% over 2026-2031. The market is moving on the back of higher memory needs in premium smartphones, where on-device AI features are lifting the amount of DRAM required per device and pushing OEMs toward denser PoP stacks. The competitive landscape is also changing because access to advanced DRAM nodes, thin-package design, and stable thermal behavior now matter as much as scale. Growth is no longer tied solely to smartphones, as automotive cockpit platforms and newer XR devices are expanding the addressable market for the LPDDR5 Package-on-Package market. Supply conditions remain important because leading-edge memory capacity is being shared across several high-value applications, which keeps pricing firm and favors suppliers with secured output. These factors support revenue expansion even when unit demand in some consumer device tiers remains uneven.

Key Report Takeaways

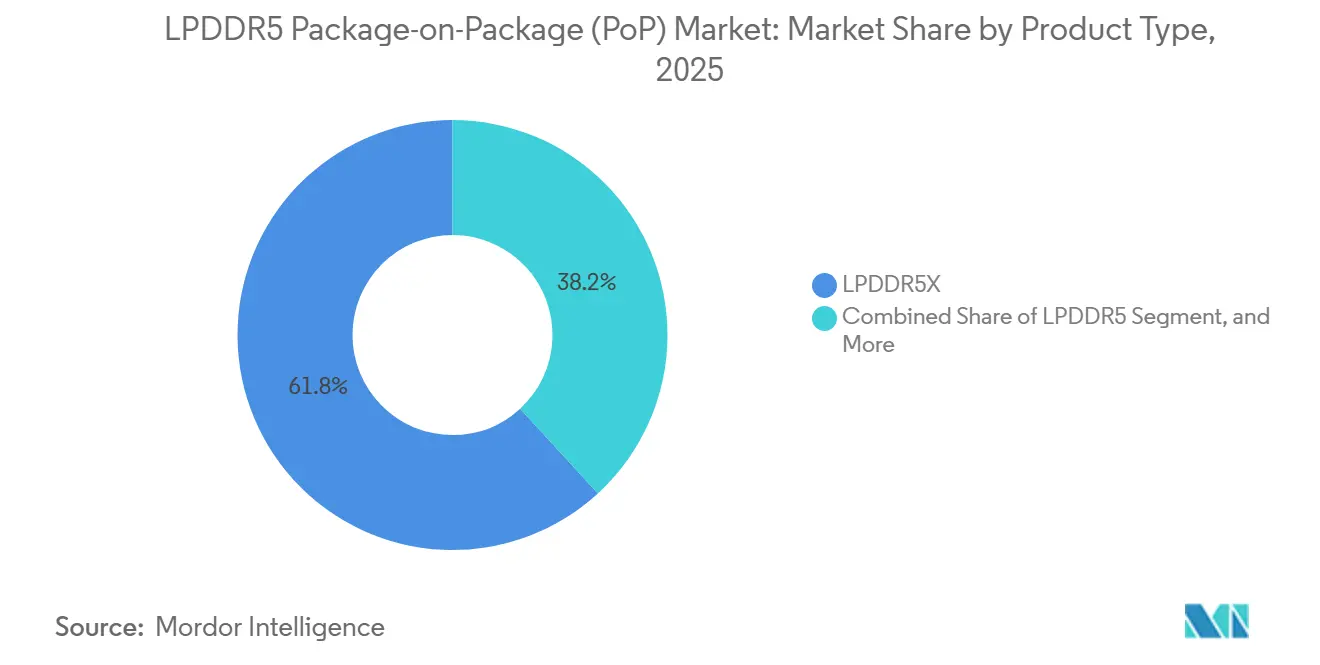

- By product type, LPDDR5X held 61.82% of 2025 revenue, while High-Speed LPDDR5X and LPDDR5T-class packages are projected to expand at a 6.64% CAGR through 2031.

- By package capacity, 12 GB held 37.16% of 2025 revenue, while 24 GB and above is projected to grow at a 6.78% CAGR through 2031.

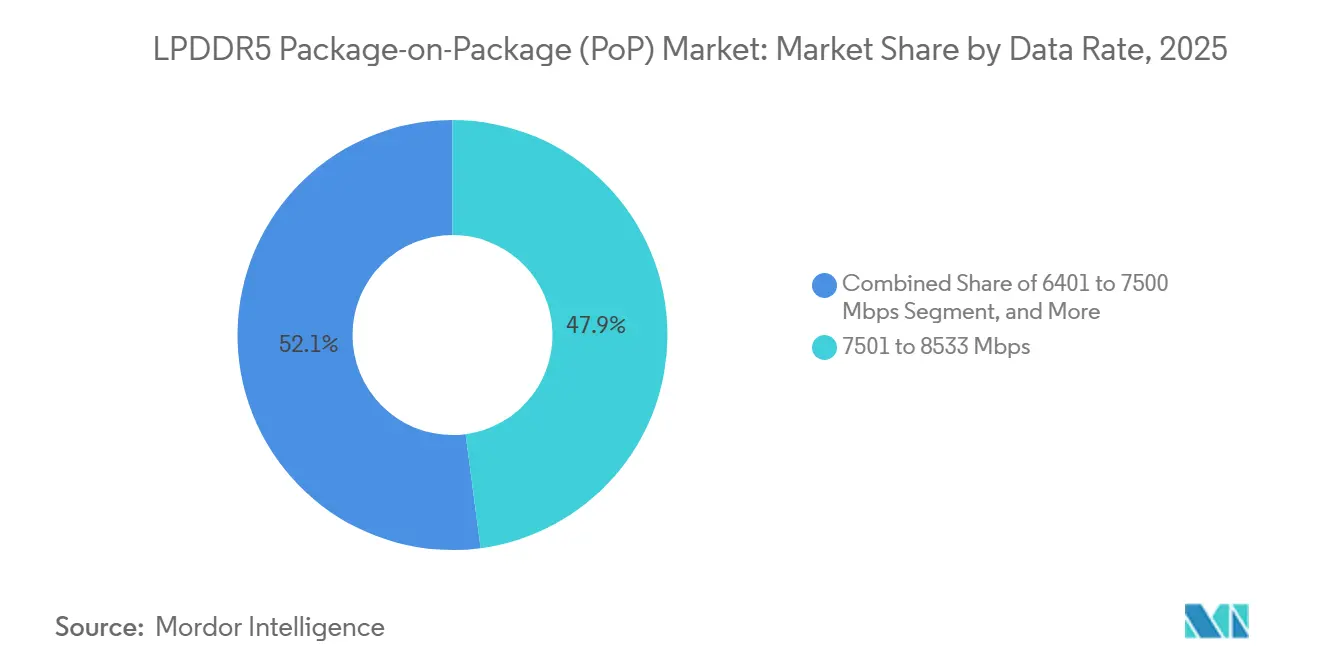

- By data rate, 7,501-8,533 Mbps accounted for 47.91% of the LPDDR5 Package-on-Package market in 2025, while rates above 8,533 Mbps are projected to expand at a 6.81% CAGR through 2031.

- By end device, smartphones accounted for 42.61% of 2025 revenue, while automotive cockpit and infotainment compute platforms are projected to grow at a 7.23% CAGR through 2031.

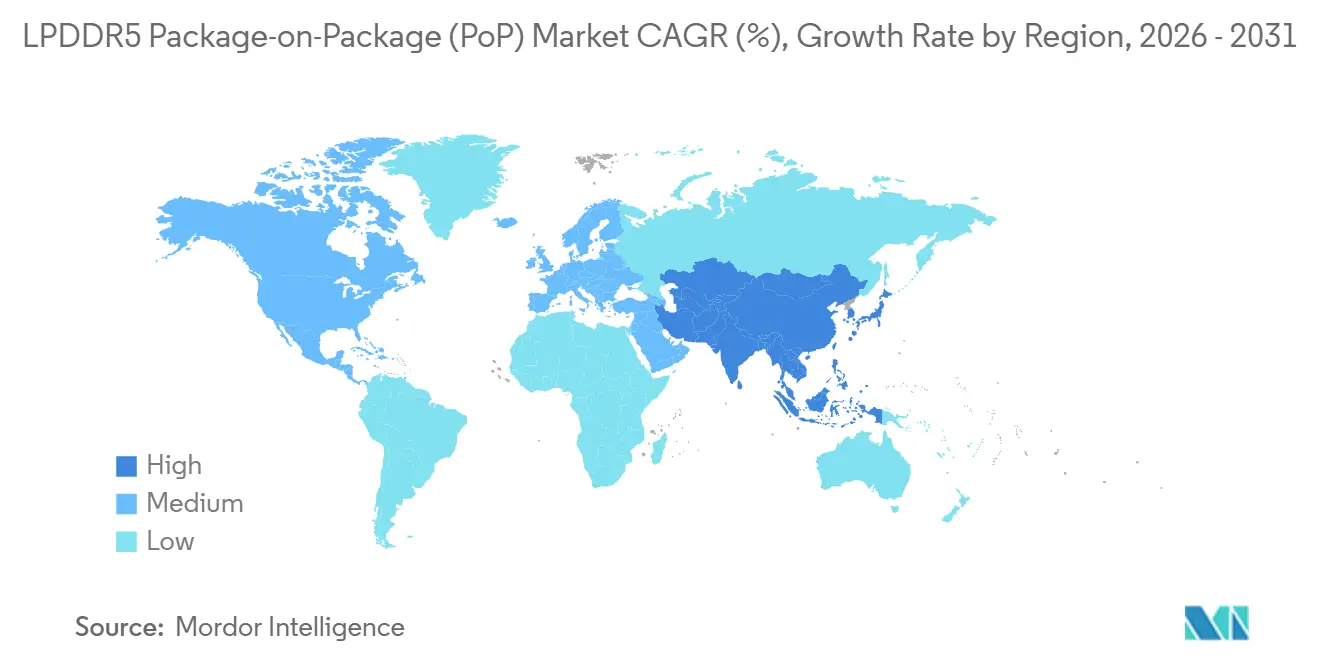

- By geography, Asia-Pacific held 86.19% of the LPDDR5 Package-on-Package market share in 2025, while the region is projected to expand at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LPDDR5 Package-on-Package (PoP) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising On-Device AI Memory Footprints | +2.4% | Global, especially Asia-Pacific, China, and South Korea | Short term (≤ 2 years) |

| LPDDR5 and LPDDR5X Mix Expansion in Mobile DRAM | +1.5% | Asia-Pacific core, with spillover to North America and Europe | Medium term (2-4 years) |

| 5G Bandwidth Uplift for Premium Handsets | +0.8% | Global, with early gains in China, South Korea, and North America | Medium term (2-4 years) |

| LPDDR5 Trickle-Down Into Upper Mid-Range Smartphones | +0.6% | Asia-Pacific, especially China, India, and Southeast Asia | Medium term (2-4 years) |

| Faster AP-Memory Qualification Cycles | +0.4% | Global, centered on Taiwan and South Korea supply chains | Short term (≤ 2 years) |

| Thermal-Optimized Ultra-Thin Package Engineering | +0.3% | Global, with early gains in premium smartphone hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising On-Device AI Memory Footprints

On-device AI inference is changing memory planning in premium smartphones and is lifting the base specification for stacked mobile DRAM. Qualcomm stated that Snapdragon 8 Gen 3 supports up to 24 GB of on-device DRAM for 10-billion-parameter models, which raised the ceiling for high-density mobile memory configurations. Samsung said its 12 nm-class LPDDR5X DRAM packages improved heat resistance by 21.2%, indicating that thermal control is advancing alongside density increases.[1]Edge AI and Vision Alliance, “Smartphone Memory, Generational AI Upgrades Will Drive a Spike in DRAM Demand,” Edge AI and Vision Alliance, edge-ai-vision.com This matters for the LPDDR5 Package-on-Package market because AI workloads demand capacity, speed, and package efficiency simultaneously. The LPDDR5 Package-on-Package market, therefore, benefits when memory stops being a background component and becomes part of the device's performance story.

LPDDR5 And LPDDR5X Mix Expansion In Mobile DRAM

The mix of mobile DRAM is shifting toward newer LPDDR5-class products, widening the addressable socket base for advanced PoP packages. Micron said its 1γ-node LPDDR5X spans 8 GB to 32 GB and was built for 2026 flagship smartphones, underscoring how vendors are broadening density coverage within a single process family. Samsung also positioned LPDDR5 uMCP as a way to enable next-generation smartphone features through tighter memory and storage integration, helping make LPDDR5-class performance more practical across a broader range of handset designs. The LPDDR5 Package-on-Package market benefits from this mix expansion as newer platforms increasingly standardize on higher-performance memory interfaces. The LPDDR5 Package-on-Package market also benefits, as each transition away from legacy memory increases the likelihood of retiring older PoP designs.

5G Bandwidth Uplift For Premium Handsets

Premium 5G phones generate heavier, more sustained memory traffic than earlier handset generations, especially when camera processing, translation, and AI functions run concurrently. Lexar Enterprise noted that LPDDR5X at 8,533 Mbps and LPDDR5T at 9,600 Mbps on a 64-bit bus provide the bandwidth needed to avoid performance bottlenecks in edge AI inference. SK hynix completed compatibility validation of LPDDR5T with Qualcomm's Snapdragon 8 Gen 3, which reduced uncertainty around the adoption of faster mobile DRAM grades in premium designs. The LPDDR5 Package-on-Package market is supported by this shift because higher network and compute throughput makes memory interface upgrades harder to postpone. The LPDDR5 Package-on-Package market also gets a durable lift because 5G performance depends on a system-level response rather than a narrow modem upgrade.

LPDDR5 Trickle-Down Into Upper Mid-Range Smartphones

The upper mid-range smartphone tier is becoming increasingly important to suppliers, as packaging and process improvements are lowering the barrier to LPDDR5-class adoption beyond the highest-priced devices. Samsung said its 12 nm-class LPDDR5X package reached a height of 0.65 mm, demonstrating how newer packaging can fit into thinner device designs without sacrificing thermal reliability. Samsung's LPDDR5 uMCP roadmap also points to a cost-conscious path to bring LPDDR5-level capabilities into broader smartphone portfolios.[2]Samsung Semiconductor, “LPDDR5 uMCP Opening Up Next-Generation Smartphone Features,” Samsung Semiconductor Global, semiconductor.samsung.com The LPDDR5 Package-on-Package market stands to gain, as each move into upper-mid-range phones adds volume without relying solely on flagship replacement cycles. The LPDDR5 Package-on-Package market also becomes more balanced when growth comes from both premium and upper mid-range device programs.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM-Driven Advanced-Node Capacity Crowd-Out | -1.9% | Global, centered on South Korea and Taiwan fabs | Short term (≤ 2 years) |

| Rising Memory Bill-of-Materials Pressure | -1.4% | Global, most severe in Asia-Pacific OEM hubs | Short term (≤ 2 years) |

| PoP Thermal Hotspot Risk | -0.5% | Global, especially in ultra-thin flagship segments | Medium term (2-4 years) |

| AP Validation Bottlenecks for Challenger Suppliers | -0.4% | Primarily China and Taiwan supply chains | Medium term (2 |

| Source: Mordor Intelligence | |||

HBM-Driven Advanced-Node Capacity Crowd-Out

A major restraint for the LPDDR5 Package-on-Package market is that advanced-node DRAM capacity is being pulled toward higher-value AI memory programs. Tech industry coverage in 2025 reported that HBM was absorbing a growing share of leading-edge memory resources, tightening supply for other DRAM categories. DRAM supply growth would remain below historical norms, suggesting a structural rather than a temporary constraint. The LPDDR5 Package-on-Package market feels this pressure directly because advanced PoP products depend on the same node progression that AI memory programs are pursuing. That makes supplier access to secured wafer starts and packaging capacity a larger competitive advantage than before.

Rising Memory Bill-Of-Materials Pressure

Rising memory costs are another restraint, as they increase the total handset bill of materials and put pressure on device pricing in volume-sensitive tiers. Pricing commentary in 2026 indicated that LPDDR5X contract prices were climbing sharply, which made adoption timing more difficult for brands selling into mid-range price bands. With projected weaker smartphone shipments in 2026, the decline is linked to the broader memory shortage environment. The LPDDR5 Package-on-Package market still gains on a revenue-per-package basis when prices rise, but the unit ramp can slow if OEMs trim specifications or delay upgrades. This means the LPDDR5 Package-on-Package market grows most smoothly when density upgrades are matched by steadier memory procurement conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LPDDR5X Leads While Faster Speed Grades Build Premium Demand

LPDDR5X held 61.82% of the LPDDR5 Package-on-Package market share in 2025, making it the clear lead product type in terms of current revenue generation. Its lead came from broad use in flagship application processor platforms and from supplier readiness across the top tier of mobile DRAM vendors. SK hynix commercialized LPDDR5T as the world's fastest mobile DRAM and later completed compatibility validation with Qualcomm's Snapdragon 8 Gen 3, which strengthened the position of faster speed grades in premium designs. Micron then shipped the first 1γ-based LPDDR5X at 10.7 Gbps with a 0.61 mm package height, showing that performance and thinness are advancing together. As a result, the LPDDR5 Package-on-Package market is seeing premium demand move toward higher-speed LPDDR5X and LPDDR5T-class packages rather than toward standard bins alone.

High-Speed LPDDR5X and LPDDR5T-class packages are projected to grow at a 6.64% CAGR through 2031, which makes them the fastest-growing product type in the LPDDR5 Package-on-Package market. The rise of these variants reflects a simple pattern, because faster memory grades help handset platforms sustain AI workloads without raising package height too aggressively. Standard LPDDR5 still retains a meaningful role in automotive cockpit platforms and industrial edge devices where power, heat, and qualification priorities differ from flagship handset needs. The LPDDR5 Package-on-Package industry is therefore splitting into a premium path focused on speed and thinness, and a broader path focused on reliable integration across a wider range of operating conditions.

By Package Capacity: 12 GB Holds The Center While High-Density Tiers Gain Ground

The 12 GB package capacity tier accounted for 37.16% of total revenue in 2025, making it the anchor of mainstream premium demand. This position aligns with non-Pro flagship Android devices, where OEMs need strong performance without pushing every model into the highest-cost configuration. Samsung began mass production of 12 GB and 16 GB 12 nm-class LPDDR5X packages in August 2024, and it linked those packages to a roadmap that extends to 24 GB and 36 GB modules. Micron also said its 1γ-node LPDDR5X family spans densities from 8 GB to 32 GB, reducing platform fragmentation for OEMs building tiered device lineups. This gives the LPDDR5 Package-on-Package market a stable center of volume even as higher-density products gather momentum.

The 24 GB and above segment is projected to grow at a 6.78% CAGR from 2026 to 2031, which makes it the fastest-growing package capacity tier in the LPDDR5 Package-on-Package market. That expansion is tied to pro-tier smartphones and to dual-die or multi-layer PoP configurations that support heavier local AI execution. The 16 GB tier is also rising as flagship vendors maintain premium specifications even as memory costs remain firm. The LPDDR5 Package-on-Package industry, therefore, benefits from a steady density ladder, where 12 GB remains the volume anchor, while 16 GB to 24 GB and above drive a higher revenue mix over time.

By Data Rate: Mid-Speed Bands Keep Volume Leadership While Higher Rates Expand Fastest

The 7,501-8,533 Mbps band accounted for 47.91% of the LPDDR5 Package-on-Package market in 2025, making it the volume center of current demand. This band has remained important because it aligns with the main certification range used across recent application processor platforms and provides a workable balance between bandwidth and thermal control. Lexar Enterprise described LPDDR5X at 8,533 Mbps and LPDDR5T at 9,600 Mbps as key points on the path to the bandwidth needed for edge AI inference. That helps explain why current flagship designs still leaned heavily on the 7,501-8,533 Mbps range even while suppliers pushed higher bins. In practice, the LPDDR5 Package-on-Package market is still led by this mid-speed band because it aligns with current production economics and design validation practices.

The above 8,533 Mbps tier is projected to grow at a 6.81% CAGR through 2031, which makes it the fastest-growing data rate segment in the LPDDR5 Package-on-Package market. SK hynix's LPDDR5T commercialization and Qualcomm validation provided suppliers with a clear path to premium adoption beyond the earlier LPDDR5X ceiling. Micron's 10.7 Gbps LPDDR5X pushed that ceiling even higher and showed that higher performance can come in very thin packages. SK hynix also developed 1c LPDDR6 in March 2026, but LPDDR5-class products remain the commercial focus for this forecast period, keeping the current transition centered on faster LPDDR5-family grades rather than an immediate node handoff.

By End Device: Smartphones Lead Revenue While Automotive Platforms Post The Fastest Growth

Smartphones accounted for 42.61% of the LPDDR5 Package-on-Package market in 2025, making them the largest end-device category by revenue. Their lead reflects the basic value of PoP architecture in mobile design, because stacking DRAM close to the application processor shortens electrical paths and supports high bandwidth in very thin form factors. Samsung's August 2024 launch of thinner LPDDR5X packages reinforced this fit with premium handsets, where internal space is tightly managed, and thermal behavior remains critical. The smartphone base, therefore, continues to define the scale of the LPDDR5 Package-on-Package market even as newer device categories widen its revenue mix. In simple terms, the largest volume still comes from phones because the package architecture solves both speed and space constraints simultaneously.

Automotive cockpit and infotainment compute platforms are projected to grow at a 7.23% CAGR through 2031, which makes them the fastest-growing end-device category in the LPDDR5 Package-on-Package market. SK hynix's LPDDR5X automotive DRAM received ASIL-D certification in January 2026, and Micron has also positioned LPDDR5X with enhanced ECC features for automotive use, indicating that suppliers are building products around stricter reliability and safety requirements.[3]SK hynix Inc., “SK hynix LPDDR5X Earns ASIL-D, Top Automotive Safety Rating,” SK hynix Newsroom, news.skhynix.com Tablets and detachable devices remain a steady secondary base, while XR, handheld gaming, and compact edge AI devices add a smaller but broader set of sockets over time. The LPDDR5 Package-on-Package industry, therefore, has a clearer second growth pillar beyond smartphones than it did in earlier mobile memory cycles.

Geography Analysis

Asia-Pacific accounted for 86.19% of the LPDDR5 Package-on-Package market share in 2025, and the region is projected to expand at a 6.72% CAGR through 2031. This kept Asia-Pacific as both the largest and the fastest-growing regional cluster in the LPDDR5 Package-on-Package market. Its position rests on a simple structural advantage; DRAM manufacturing, foundry services, packaging capability, and final device assembly are concentrated within the same broad production system. South Korea remains central to the production and supplier qualification. Taiwan continues to anchor foundry, packaging, and test activity that supports the broader mobile memory chain.

China adds demand depth and supply chain weight to the Asia-Pacific by combining very large smartphone OEM procurement with a growing domestic memory push. That makes the LPDDR5 Package-on-Package market in Asia-Pacific more resilient than in regions that rely mainly on design activity or finished device consumption. India and Southeast Asia also matter because handset assembly and demand for upper mid-range smartphones remain important for the next stage of volume expansion. Japan maintains a narrower but useful role through its capabilities in substrate- and packaging-related areas. Together, these countries' positions support a regional structure that is difficult for other geographies to replicate in the medium term.

North America and Europe remained smaller revenue contributors in 2025, but both regions still shape the LPDDR5 Package-on-Package market through premium device design and automotive qualification activity. North America matters because leading smartphone and platform decisions influence memory specifications even when final assembly takes place in Asia. Europe matters because connected vehicle and cockpit programs are building demand for higher-performance, safety-oriented mobile memory. The rest of the World held the smallest regional contribution and mainly consumed LPDDR5 PoP through imported finished devices rather than local manufacturing. In those markets, adoption is more sensitive to smartphone pricing and the pace of 5G rollout, meaning cost pressure can slow volume uptake even when long-term device demand remains intact.

Competitive Landscape

The LPDDR5 Package-on-Package market is concentrated at the die-manufacturing level, with Samsung Electronics, SK hynix, and Micron Technology holding the strongest positions in advanced-node LPDDR5X supply. The top tier competes on process transitions, package height, thermal behavior, and the ability to secure design wins with major platform and device makers. Micron strengthened its position in June 2025 when it shipped the first 1γ-based LPDDR5X at 10.7 Gbps with a 0.61 mm package height, giving it clear leadership in process and package for premium mobile memory. Samsung defended its standing with mass production of very thin 12 nm-class LPDDR5X packages and a roadmap that extends to higher-capacity configurations for on-device AI. These moves show that the LPDDR5 Package-on-Package market is being shaped by execution in both process technology and physical package design.

SK hynix has taken a strong strategic path through performance validation and automotive qualification. Its LPDDR5T compatibility validation with Qualcomm's Snapdragon 8 Gen 3 gave it a clear position in the premium smartphone path, while its ASIL-D-certified LPDDR5X opened a route into more demanding automotive programs. Micron has also targeted automotive-grade differentiation with LPDDR5X, which features enhanced ECC capabilities, strengthening its position beyond smartphones. Samsung, for its part, has continued to link LPDDR5X development to AI-focused device roadmaps and broader memory integration strategies.[4]Samsung Semiconductor, “LPDDR5 uMCP Opening Up Next-Generation Smartphone Features,” Samsung Semiconductor Global, semiconductor.samsung.com As a result, the LPDDR5 Package-on-Package market is no longer competing solely on supply scale, as qualification depth and application fit now carry greater weight.

A smaller but notable competitive shift is the emergence of additional Chinese supply options around LPDDR5X, which adds pricing pressure in domestic OEM channels even though the top tier still dominates the technical frontier. That means the LPDDR5 Package-on-Package market remains open to selective share movement, but not to broad disruption in the forecast window. The largest suppliers continue to hold the advantage because they can combine node progression, packaging know-how, and long customer validation cycles. In this setting, the most durable positions are likely to remain with vendors that can serve both flagship mobile programs and newer automotive or edge-compute sockets.

LPDDR5 Package-on-Package (PoP) Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

ChangXin Memory Technologies, Inc.

Nanya Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Micron Technology showcased its full AI-optimized memory and storage portfolio at COMPUTEX 2026, highlighting LPDDR5X for real-time AI processing across smartphones, PCs, robotics, and automotive platforms. The presentation included LPCAMM2 at 9,600 MT/s, demonstrating the convergence of PoP-adjacent mobile DRAM form factors toward modular server-class memory architectures for edge AI.

- April 2026: SK hynix commenced full-scale mass production of its 192 GB SOCAMM2 product based on its 1c-node LPDDR5X, designed for NVIDIA's next-generation Vera Rubin GPU platform. The module delivers more than double the bandwidth and 5% higher power efficiency than existing Registered DIMMs, extending LPDDR5X's addressable market into AI server infrastructure.

- March 2026: SK hynix successfully developed the world's first 16Gb LPDDR6 DRAM on its 1c, sixth-generation 10 nm-class process, delivering 33% faster speed and 20% improved power efficiency relative to LPDDR5X. Mass production preparation is targeted for H1 2026, with device supply planned for H2 2026, establishing a next-generation roadmap that will eventually succeed LPDDR5X PoP sockets.

- January 2026: SK hynix's LPDDR5X automotive DRAM received ASIL-D certification, the highest functional safety rating under ISO 26262, following a comprehensive assessment by TUV SUD covering development processes, product design, verification, and quality management. The certification meets strict thresholds of SPFM ≥ 99% and LFM ≥ 90%, qualifying the product for ADAS, autonomous driving, and IVI applications.

Global LPDDR5 Package-on-Package (PoP) Market Report Scope

The LPDDR5 Package-on-Package (PoP) Market refers to the global market for LPDDR5-based memory solutions integrated using Package-on-Package (PoP) technology, a semiconductor packaging approach that vertically stacks low-power DRAM memory directly with application processors or system-on-chip (SoC) components to achieve higher performance, reduced footprint, improved power efficiency, and optimized signal integrity. LPDDR5 PoP solutions are widely adopted in space-constrained and performance-intensive devices where high memory bandwidth, low latency, and compact system design are critical requirements.

The LPDDR5 Package-on-Package (PoP) Report is Segmented by Product Type (LPDDR5, LPDDR5X, and High-Speed LPDDR5X / LPDDR5T-class Packages), Package Capacity (Up to 8 GB, 12 GB, 16 GB, and 24 GB and Above), Data Rate (Up to 6400 Mbps, 6401-7500 Mbps, 7501-8533 Mbps, and Above 8533 Mbps), End Device (Smartphones, Tablets and Detachable Mobile Computing Devices, XR Devices / AR-VR Headsets and Smart Glasses, Portable Gaming and Handheld Entertainment Devices, Automotive Cockpit and Infotainment Compute Platforms, and Other End Devices), and Geography (North America, Europe, Asia Pacific, and Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| LPDDR5 |

| LPDDR5X |

| High-Speed LPDDR5X / LPDDR5T-class Packages |

| Up to 8 GB |

| 12 GB |

| 16 GB |

| 24 GB and above |

| Up to 6400 Mbps |

| 6401 to 7500 Mbps |

| 7501 to 8533 Mbps |

| Above 8533 Mbps |

| Smartphones |

| Tablets and Detachable Mobile Computing Devices |

| XR Devices / AR-VR Headsets and Smart Glasses |

| Portable Gaming and Handheld Entertainment Devices |

| Automotive Cockpit and Infotainment Compute Platforms |

| Other End Devices |

| North America | |

| Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia Pacific | |

| Rest of the World |

| By Product Type | LPDDR5 | |

| LPDDR5X | ||

| High-Speed LPDDR5X / LPDDR5T-class Packages | ||

| By Package Capacity | Up to 8 GB | |

| 12 GB | ||

| 16 GB | ||

| 24 GB and above | ||

| By Data Rate | Up to 6400 Mbps | |

| 6401 to 7500 Mbps | ||

| 7501 to 8533 Mbps | ||

| Above 8533 Mbps | ||

| By End Device | Smartphones | |

| Tablets and Detachable Mobile Computing Devices | ||

| XR Devices / AR-VR Headsets and Smart Glasses | ||

| Portable Gaming and Handheld Entertainment Devices | ||

| Automotive Cockpit and Infotainment Compute Platforms | ||

| Other End Devices | ||

| By Geography | North America | |

| Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current and forecast value of the LPDDR5 Package-on-Package market?

The LPDDR5 Package-on-Package market was valued at USD 9.65 billion in 2025, is estimated at USD 11.25 billion in 2026, and is forecast to reach USD 15.09 billion by 2031 at a 6.05% CAGR.

Which product type leads LPDDR5 Package-on-Package demand?

LPDDR5X led revenue with 61.82% in 2025 because it is widely qualified across flagship platforms and supports the speed and density needs of premium devices.

Which package capacity is growing the fastest in LPDDR5 PoP?

The 24 GB and above tier is the fastest-growing package capacity segment, with a projected 6.78% CAGR through 2031, driven by pro-tier smartphones and heavier on-device AI workloads.

Why is Asia-Pacific so dominant in this space?

Asia-Pacific held 86.19% of 2025 revenue and is projected to grow at 6.72% CAGR because DRAM production, foundry services, packaging, and smartphone assembly are concentrated in the region.

Which end-device category creates the most growth opportunity beyond smartphones?

Automotive cockpit and infotainment compute platforms are the fastest-growing end-device segment, with a 7.23% CAGR through 2031, supported by tighter reliability and safety requirements.

What is shaping competition among leading suppliers?

Competition is being shaped by advanced-node access, package height, thermal control, and qualification depth, with Micron, Samsung, and SK hynix all using product launches and validation milestones to secure position.

Page last updated on: