Industrial MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

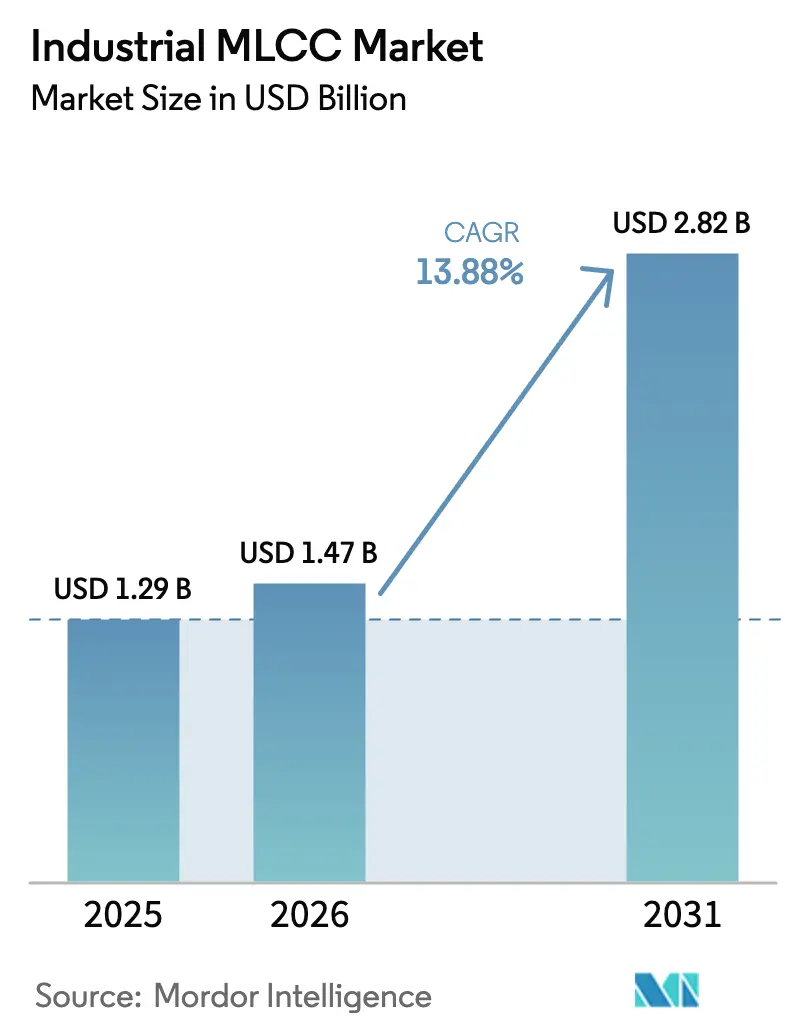

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.82 Billion |

| Growth Rate (2026 - 2031) | 13.88% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial MLCC Market Analysis by Mordor Intelligence

The Industrial MLCC market size is expected to grow from USD 1.29 billion in 2025 to USD 1.47 billion in 2026 and is forecast to reach USD 2.82 billion by 2031 at 13.88% CAGR over 2026-2031. Expanding AI data-center deployments, faster industrial automation cycles, and renewable-energy inverters together reinforce demand for high-capacitance multilayer ceramic capacitors that tolerate wide temperature swings and high ripple currents. North American reshoring programs elevate domestic output of high-Q Class 1 parts suited for 0603-100 µF rails that feed next-generation GPU clusters.[1]Josue Navarro, “Meeting the Demanding Energy Needs of AI Servers with Advanced Technology,” Microchip Technology, microchip.com Asia-Pacific suppliers protect scale advantages through vertically integrated nickel powder and dielectric supply chains, yet their dominance faces intensifying competition from North American wafer-level process houses installing advanced nano-BME lines. Raw-material exposure to nickel price shock and limited AEC-Q200 test slots remain the two largest supply-side risks, while premium opportunities emerge in above 1 kV snubbers for SiC solar inverters and rugged metal-cap packages for collaborative-robot joints.[2]“Motor/Inverter Circuit Configuration Example,” TDK, tdk.com

Key Report Takeaways

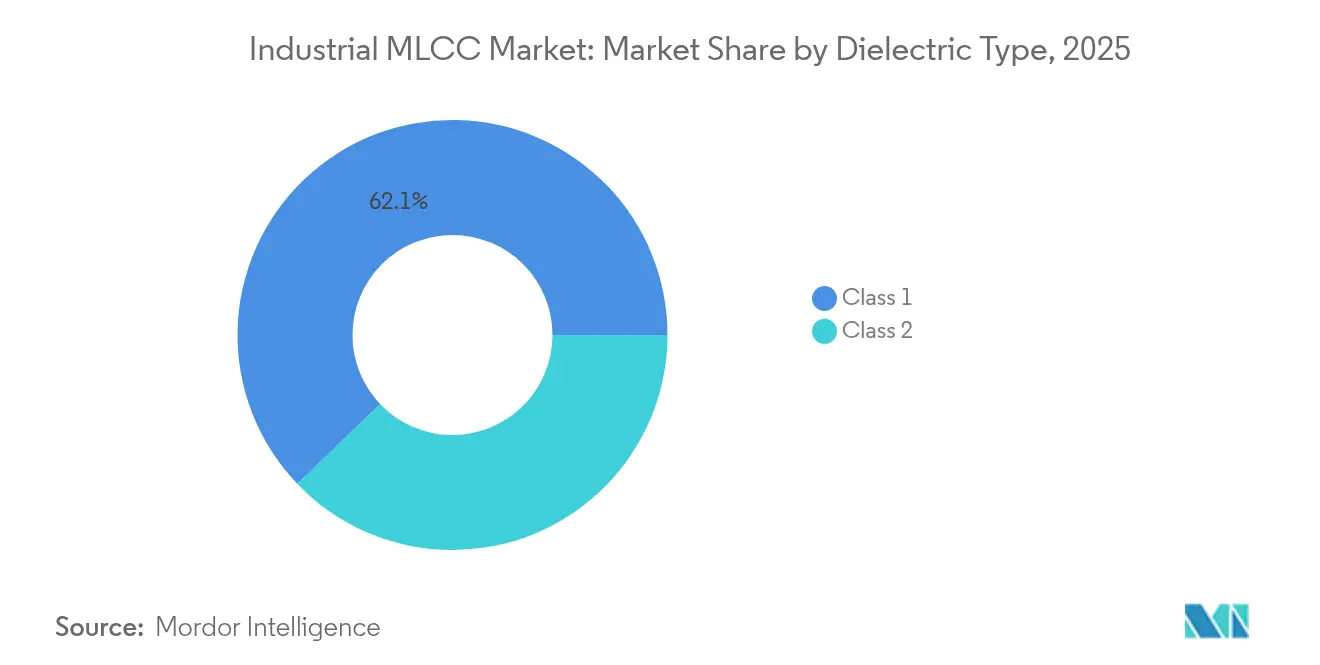

- By dielectric type, Class 1 parts held 62.15% share of the Industrial MLCC market size in 2025 and are expanding at a 15.28% CAGR to 2031.

- By case size, the 201 package commanded 55.92% share in 2025 in the Industrial MLCC market; 402 packages record the highest projected CAGR at 15.1% through 2031.

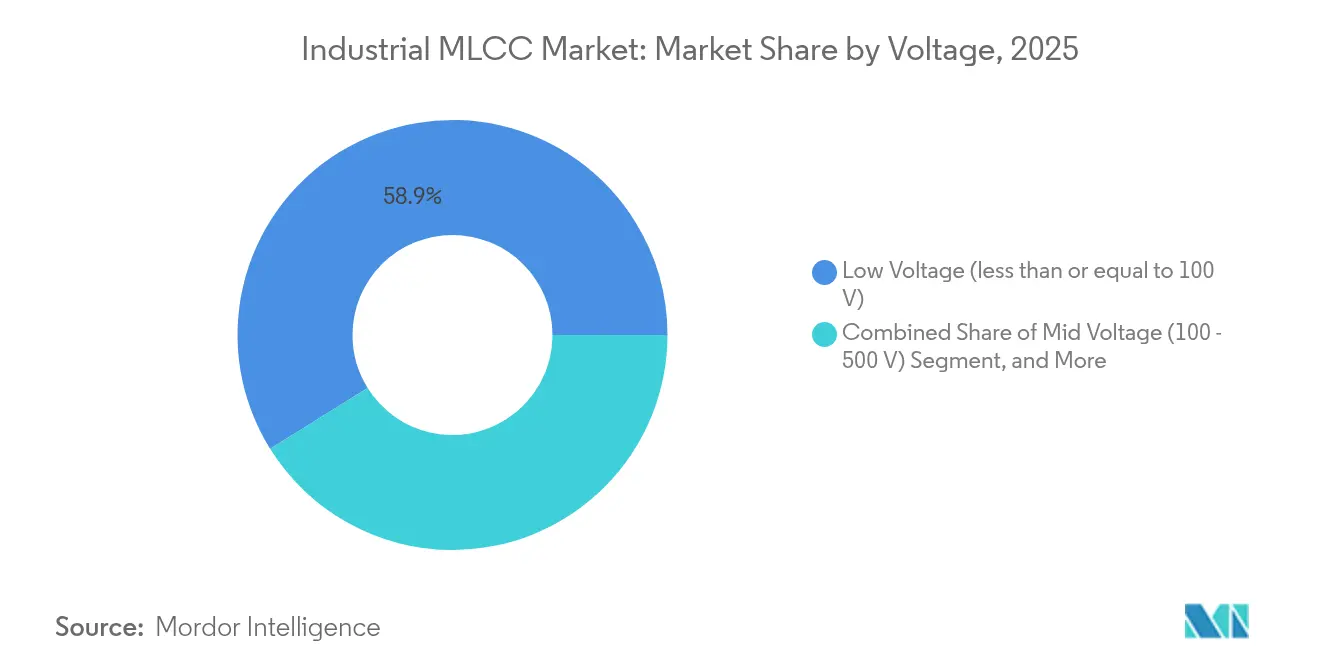

- By voltage rating, less than or equal to 100 V MLCCs accounted for 58.88% share of the Industrial MLCC market size in 2025 and lead growth at a 15.16% CAGR.

- By mounting type, surface-mount units represented a 41.12% share in 2025 in the Industrial MLCC market; metal-cap variants posted the quickest 14.61% CAGR through 2031.

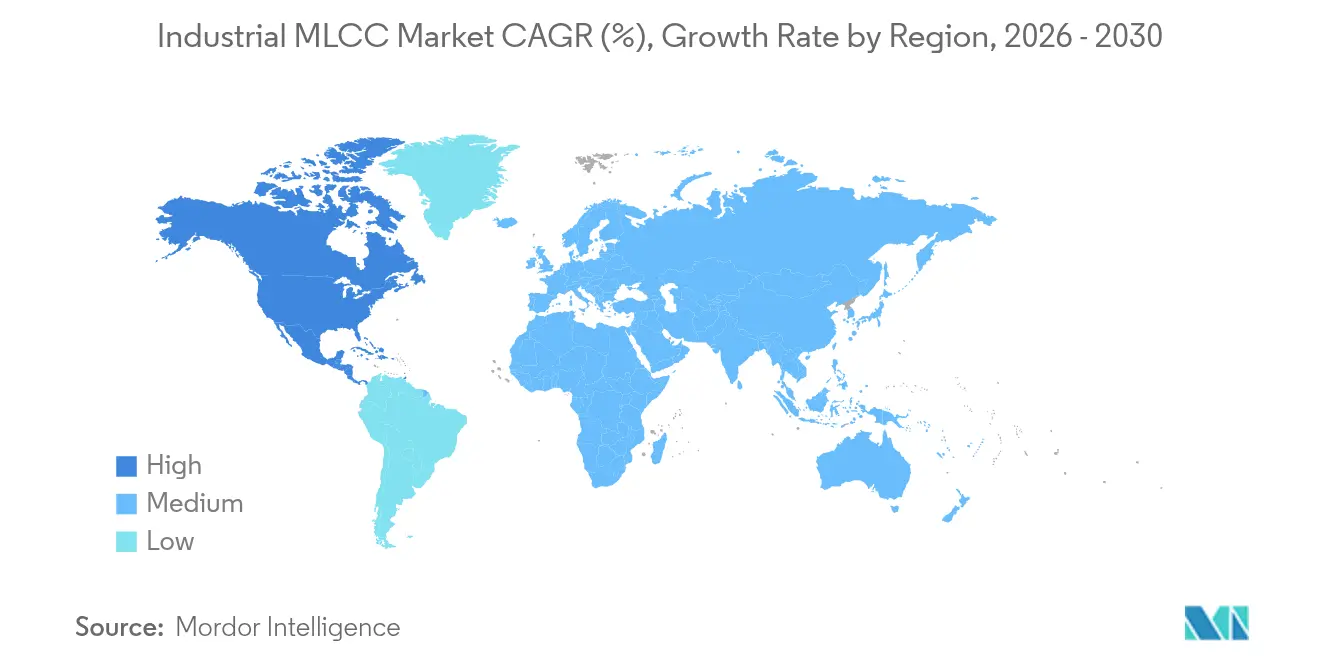

- By geography, Asia-Pacific captured 57.12% of Industrial MLCC market share in 2025, while North America is advancing at a 15.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reshoring of high-Q MLCC lines | +3.2% | North America and Mexico | Medium term (2-4 years) |

| AI-server power-rail miniaturization | +2.8% | United States and China data-center corridors | Short term (≤2 years) |

| Electrification of industrial robotics | +2.1% | Asia-Pacific core with spillover to North America and Europe | Medium term (2-4 years) |

| Rapid PV-inverter voltage step-ups | +1.9% | China, India, and United States solar programs | Long term (≥4 years) |

| Three-terminal MLCC arrays for maintenance | +1.5% | European and North American industrial corridors | Long term (≥4 years) |

| Nano-BME dielectric CAPEX race | +1.8% | Japanese manufacturing, global supply outcome | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capacity-Driven Reshoring of High-Q MLCC Lines in North America

Domestic MLCC foundries increase production of high-Q Class 1 devices to shorten lead times for AI servers that require sub-nanosecond response power rails. New 0603 lines with 100 µF capability rely on precision nano-BME dielectrics and automated visual inspection that previously resided almost exclusively in East Asia. Vendors also forge direct partnerships with U.S. hyperscale operators, enabling just-in-time deliveries that trim buffer inventory. State incentives lower initial capital hurdles for thin-film co-firing kilns, accelerating build-out before 2027. Tooling and powder suppliers inside the region benefit from increased orders for advanced spray-dried BaTiO₃.

AI-Server Power-Rail Miniaturization Requirements (0603-100 µF Parts)

AI accelerator racks draw up to 4 kW per board, pushing current densities beyond traditional 1210 decoupling limits. Engineers therefore specify 0603 capacitors that deliver 100 µF with stable capacitance under high DC bias to maintain target impedance. Vertical power-delivery architectures position the MLCC arrays directly below the GPU package, minimizing loop inductance to under 50 pH. Suppliers gain pricing power as process yields for these dense parts remain lower than mainstream Class 2 items. Inventory pull-ins ahead of major AI cluster rollouts produce cyclic demand spikes that reward vendors maintaining buffered capacity.

Electrification of Industrial Robotics and Cobots

Collaborative robots integrate more sensors per joint and rely on distributed 48 V buses to reduce copper weight, each trend inflating MLCC counts per unit. High-frequency wireless charging stations for factory AGVs demand compensation capacitors rated at 80 kHz, introducing an incremental niche for high-Q Class 1 parts. Cobots also embed safety circuits with strict capacitance tolerance to protect human operators, again favoring temperature-stable dielectrics. Asian robot makers specify metal-cap MLCCs to mitigate vibration stress, reinforcing growth in this premium package class. The result is higher bill-of-materials value per installed robot.

Rapid PV-Inverter Voltage Step-Ups Needing ≥1 kV MLCC Snubbers

SiC-based solar inverters now switch at speeds that create sharper dv/dt edges, making low-ESL ceramic snubbers essential to control overshoot. Engineers migrate from film capacitors to compact CeraLink and similar MLCC designs that combine up to 1 kV ratings with inductance below 2 nH. Demand scales with record global photovoltaic installations, particularly in India and the United States. Suppliers able to coat thicker dielectric layers without voids secure earlier design wins. Long operational lifetimes in rooftop environments justify premium pricing against electrolytic alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel powder cost volatility | -2.4% | Global with heavier burden on Asian fabs | Short term (≤2 years) |

| Six-month lead-times for above 500 V high-Q parts | -1.8% | North America and Europe | Medium term (2-4 years) |

| Limited AEC-Q200 test capacity | -1.2% | Asia and Europe test houses | Medium term (2-4 years) |

| IP disputes over ultra-thin layer counts | -0.9% | Worldwide licensing negotiations | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Nickel Powder Cost Volatility Tied to EV Battery Demand

Nickel cathode expansion in electric vehicles continues to tighten availability of high-purity nickel needed for MLCC inner electrodes. Spot prices slid to USD 15,000–16,000 per metric ton in 2024 yet remain subject to abrupt rallies that squeeze capacitor makers on fixed supply contracts. Smaller foundries without long-term procurement agreements face greater margin compression. Larger players counteract volatility by securing offtake with Indonesian smelters and diversifying toward manganese-doped electrodes that reduce nickel intensity.

Six-Month Lead-Times for Above 500 V High-Q MLCCs

Manufacturing yields for thick dielectric stacks stay below those of mainstream above 100 V lines, making high-voltage capacity scarce. Combined with mandatory burn-in and surge testing under AEC-Q200 protocols, supply pipelines can stretch to six months.[3]Panasonic Industrial Devices, “What Is AEC-Q200,” panasonic.com Industrial inverter and traction-drive manufacturers consequently carry larger buffer inventories, thereby raising their working capital needs. Vendors investing in plasma-clean kilns and real-time X-ray inspection aim to halve cycle time by 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Dominance Enables Precision Stability

Class 1 MLCCs captured 62.15% Industrial MLCC market share in 2025 and are projected to grow at a 15.28% CAGR, reflecting their unrivaled thermal and DC bias stability. Industrial oscillators, inverter snubbers, and medical imaging chains consistently specify C0G or NP0 formulations that limit capacitance drift across –55 °C to 125 °C swings. The Industrial MLCC market outlets prize this predictability, accepting lower volumetric efficiency relative to Class 2 parts. Manufacturers leverage nano-BME dielectrics to raise layer counts without compromising dielectric loss, enabling 0603 form factors to reach values previously reserved for X7R. Extended ceramic firing cycles remain the primary cost driver, but end users willingly absorb premiums where uptime is mission-critical.

Class 2 MLCCs retain a role in bulk decoupling where high capacitance density overrides drift concerns. X7R grades satisfy wideband energy storage adjacent to FPGAs and servo drives, while Y5V participation stays limited to non-precision circuits. Vendors mitigate DC bias loss through doped structures and thicker margins between layers. Continuous improvement downgrades the capacitance penalty gap, yet Class 1 remains the preferred option for timing and safety circuits where failure carries steep downtime penalties. As a result, Class 1 shipments will outpace the broader Industrial MLCC market over the forecast window.

By Case Size: 201 Footprint Balances Density With Process Yields

The 201 package held 55.92% share in 2025, striking the optimal compromise between board density and reliablity. These components typically operate at voltages below 100 V, making them a staple in AI server voltage regulator modules and factory automation PLC cards. The Industrial MLCC market size for 201 parts is forecast to track overall sector growth as engineers standardize pick-and-place tooling around this footprint. Suppliers attain higher yields by reusing established stencil and reflow profiles, sustaining cost competitiveness.

402 devices will grow at a sector-leading 15.1% CAGR. The marginally larger footprint allows dielectric stacks thick enough to reach 250 V without field failures, critical for industrial drives that migrate to 1500 V DC links. Additionally, thermal resistance improves due to a larger pad area, lowering hotspot temperatures in high ripple environments. Breakthroughs such as Murata’s 006003-inch product showcase theoretical miniaturization, yet mass adoption will likely concentrate on mature sizes where automated optical inspection metrics are already validated. Hence, 402 remains the bellwether for capacity expansion through 2031.

By Voltage Rating: Low-Voltage Prevalence Mirrors Distributed Power Trends

Less than or equal to 100 V MLCCs comprised 58.88% Industrial MLCC market share in 2025 and are expected to rise by 15.16% CAGR, driven by 48 V bus architectures inside AI servers and robotics. Engineers deploy numerous low-value capacitors near point-of-load converters to minimize path impedance. High-frequency characteristics and self-resonant points above 20 MHz make class-leading low-voltage capacitors ideal for fast transient suppression. Mid-voltage devices between 100 V and 500 V cover auxiliary drives and sensor conditioning. Above 500 V designs represent a niche yet profitable domain targeting SiC traction and grid-tied solar, where fewer qualified suppliers command unit prices up to five times mainstream levels.

Advancements in nickel electrode uniformity and dielectric layer thinning allow 100 V parts to deliver capacitance once confined to bulkier electrolytics. Samsung Electro-Mechanics’ 100 V 0603 launch tailored for 48 V DC systems illustrates how production learning curves are closing volumetric gaps. The Industrial MLCC market therefore remains skewed to low-voltage volumes even as specialty high-voltage lines enjoy elevated margins.

By Mounting Type: Surface Mount Efficiency Versus Metal-Cap Durability

Surface-mount MLCCs maintained 41.12% share in 2025 as automated assembly and compact layouts remain the industry norm. Pick-and-place throughput and reduced parasitics keep SMT attractive for volume lines. The Industrial MLCC market still shows a distinct shift toward metal-cap formats growing at 14.61% CAGR, primarily in railway, heavy-equipment, and robotics sectors that face high vibration and thermal cycling. Metal caps absorb mechanical strain and distribute heat more evenly, extending mean time between failures.

Radial leads persist for retrofit designs and high-voltage modules where through-hole mounting offers creepage benefits. Despite assembly-line inefficiencies, their share holds steady because legacy drives and UPS boards cannot migrate to SMT without redesign costs. Looking forward, hybrid boards may co-locate SMT decouplers with metal-cap snubbers, letting designers optimize each function by mechanical and electrical priority.

Geography Analysis

Asia-Pacific held 57.12% of Industrial MLCC market share in 2025, underpinned by entrenched powder-line ecosystems and patented multilayer firing know-how in Japan, South Korea, and China. Murata’s proprietary 0.5 µm layer technology enables high production yields at volumes unmatched elsewhere, and its local nickel recycling plants reduce raw material exposure. Samsung Electro-Mechanics aligns with automakers’ shift to 48 V subsystems, targeting USD 760 million in regional automotive MLCC revenue for 2025. Chinese vendors scale aggressively on low-cost lines, yet they still trail on dielectric purity required for Class 1 export grades.

North America is expected to record the highest regional CAGR of 15.22% through 2031, driven by AI server build-outs and federal incentives that subsidize the purchase of capacitor fabrication equipment. New fabs in Texas and Arizona reach early production in 2026, focusing on high-Q less than or equal to 0603 parts that traditionally relied on air freight from Asia. Close collaboration between capacitor producers and hyperscale operators reduces qualification cycles, embedding local parts in server reference designs from inception. Although raw-material import reliance remains high, renewed nickel supply contracts with Canadian miners offer hedge against Indonesian export policy swings.

Europe sustains moderate single-digit growth as OEMs in Germany and Italy mandate AEC-Q200 Grade 0 parts for both e-mobility chargers and industrial automation. The region’s aggressive carbon-neutral targets catalyze renewable inverter installations that need above 1 kV snubbers, a niche dominated by TDK’s CeraLink series. Rest-of-World markets such as Brazil and Saudi Arabia invest in solar and desalination plants, importing MLCC arrays for high-voltage DC links. Despite smaller base volumes, these projects broaden geographic diversity and raise after-sales demand for replacement stock.

Competitive Landscape

Japanese and Korean firms dominate the Industrial MLCC market through vertical integration spanning BaTiO₃ calcination to automated optical inspection. Murata leverages 700-layer standard products and invests USD 11.2 billion in Philippines expansion that adds 10 billion units of annual capacity focused on automotive and industrial designs. TDK increases CeraLink output by 40% to exploit SiC inverter growth, while Samsung Electro-Mechanics targets premium 48 V capacitors that offer threefold operating margin over commodity smartphones parts.

The market’s high capital and knowledge barriers foster concentration around fewer than ten global suppliers. Smaller specialists like Knowles Precision Devices carve out niches in defense and medical where Q-temperature ratings justify higher price points. Western start-ups explore polymer-ceramic hybrids but face IP minefields around thin-film deposition processes already patented by incumbents. Raw-material control, especially nickel electrode powder, emerges as a top differentiator; vertically integrated players cushion cost spikes better than fab-lite rivals.

Strategic moves highlight pursuit of geographic risk diversification and technology moat reinforcement. Murata’s Philippines site lowers exposure to Japanese seismic risk, Samsung’s Philippine plant doubles automotive line throughput, and Taiyo Yuden’s USD 200 million dielectric research campus works on sub-0.4 µm layer targets expected to unlock 30% capacitance uplift by 2028. Patent litigation over layer count techniques intensifies, signaling sustained entry hurdles.

Industrial MLCC Industry Leaders

Taiyo Yuden Co., Ltd

Walsin Technology Corporation

Yageo Corporation

Murata Manufacturing Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Murata Manufacturing announced USD 11.2 billion expansion of its Philippines MLCC facility to scale advanced thin-layer lines for automotive and industrial applications.

- August 2024: Samsung Electro-Mechanics completed inspection of its Philippines plant aiming for 1 trillion won automotive MLCC revenue in 2024.

- July 2024: TDK Corporation grew CeraLink ceramic capacitor capacity by 40% to serve renewable-energy inverters and automation drives.

- June 2024: Murata released a 006003-inch MLCC, the smallest to date, targeting power rails in AI servers and miniaturized sensors.

Global Industrial MLCC Market Report Scope

0 201, 0 402, 0 603, 1 005, 1 210, Others are covered as segments by Case Size. 600V to 1100V, Less than 600V, More than 1100V are covered as segments by Voltage. 10 μF to 100 μF, Less than 10 μF, More than 100 μF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 – 500 V) |

| High Voltage (above 500 V) |

| Metal Cap |

| Radial Lead |

| Surface Mount |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 201 | |

| 402 | ||

| 603 | ||

| 1005 | ||

| 1210 | ||

| Other Case Sizes | ||

| By Voltage | Low Voltage (less than or equal to 100 V) | |

| Mid Voltage (100 – 500 V) | ||

| High Voltage (above 500 V) | ||

| By MLCC Mounting Type | Metal Cap | |

| Radial Lead | ||

| Surface Mount | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform