GDDR Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

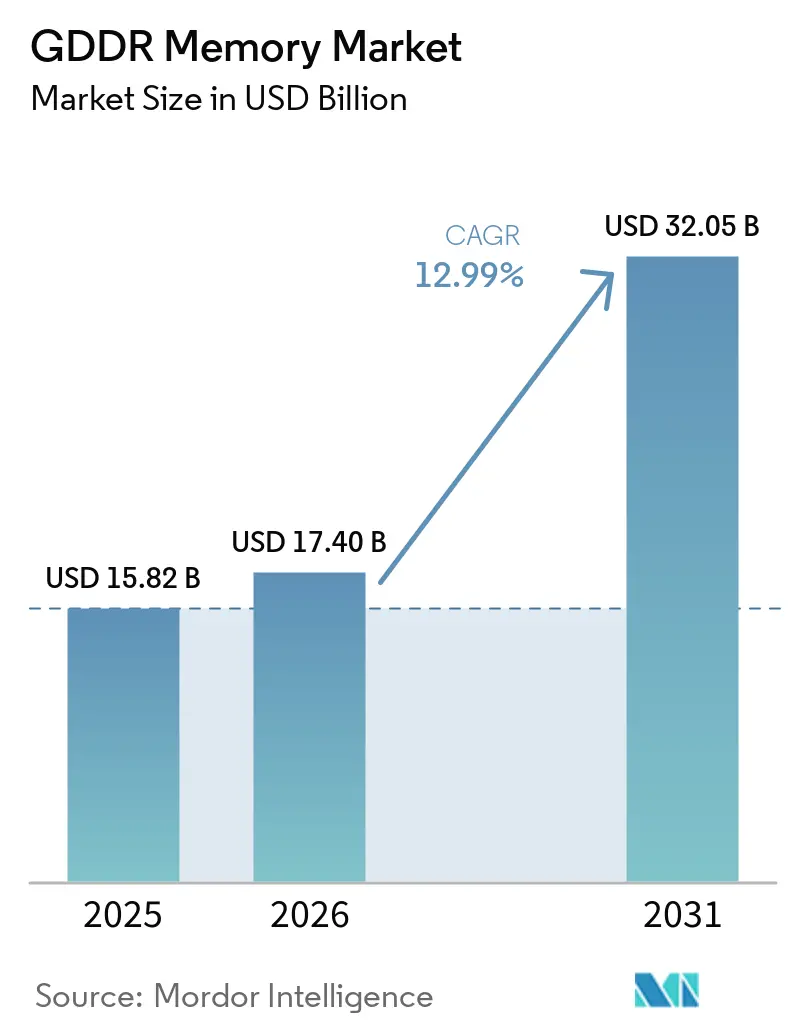

| Market Size (2026) | USD 17.40 Billion |

| Market Size (2031) | USD 32.05 Billion |

| Growth Rate (2026 - 2031) | 12.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GDDR Memory Market Analysis by Mordor Intelligence

The GDDR memory market size is expected to increase from USD 15.82 billion in 2025 to USD 17.4 billion in 2026 and reach USD 32.05 billion by 2031, growing at a CAGR of 12.99% over 2026-2031. Strong unit shipments of gaming GPUs from early-2025 launches, rapid uptake of GDDR6 and GDDR7 in AI workstations, and accelerating cloud gaming rollouts underpin this expansion. Samsung’s decision to supply GDDR6 for Tesla infotainment units in 2026 signals widening adoption of graphics DRAM in non-traditional verticals, while Asia-Pacific fabrication clusters continue to anchor supply. Allocation tension between high-bandwidth memory (HBM) and GDDR wafer starts is expected to keep average selling prices elevated until new cleanrooms come online from 2027. Despite these supply constraints, sustained demand from premium gaming cards and enterprise AI inference workloads positions the GDDR memory market for double-digit growth throughout the forecast horizon.

Key Report Takeaways

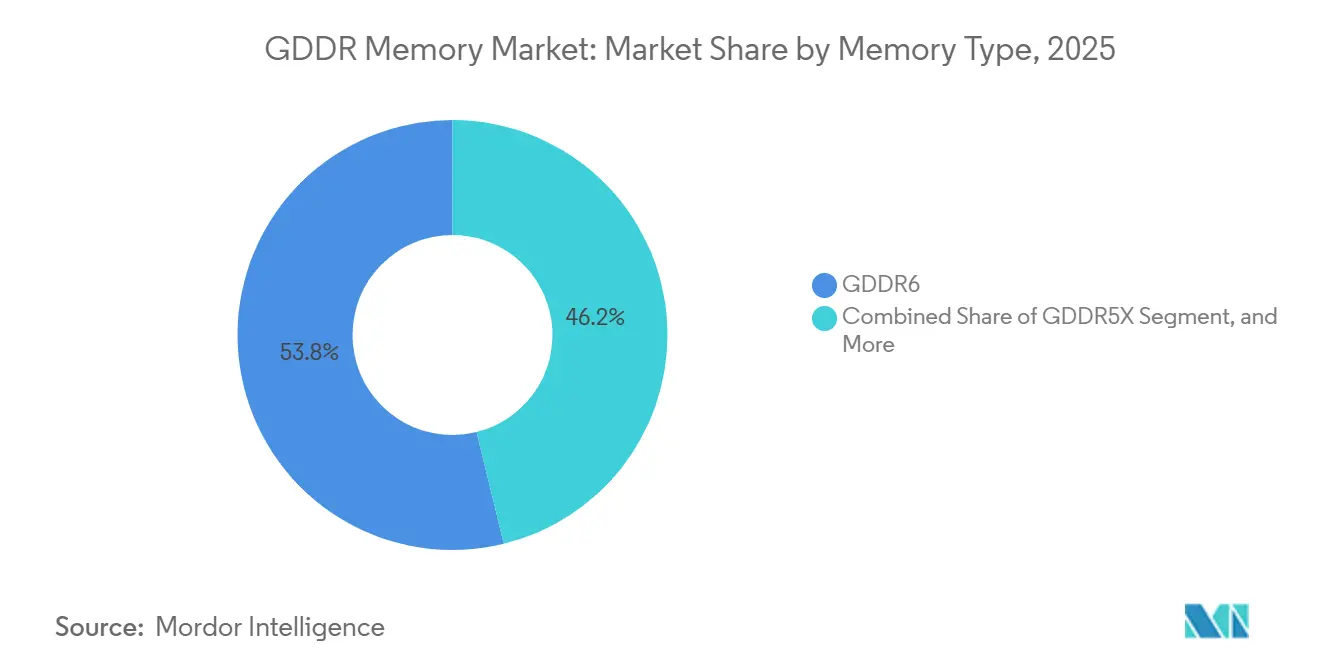

- By memory type, GDDR6 accounted for 53.84% of 2025 revenue, while GDDR6X is projected to grow at a 13.79% CAGR through 2031.

- By application, gaming graphics led with 59.32% share in 2025, and AI and compute are forecast to grow at 13.68% to 2031.

- By density, 8-16 GB devices accounted for 53.16% of 2025 sales, whereas modules above 16 GB are set to rise at a 13.83% CAGR.

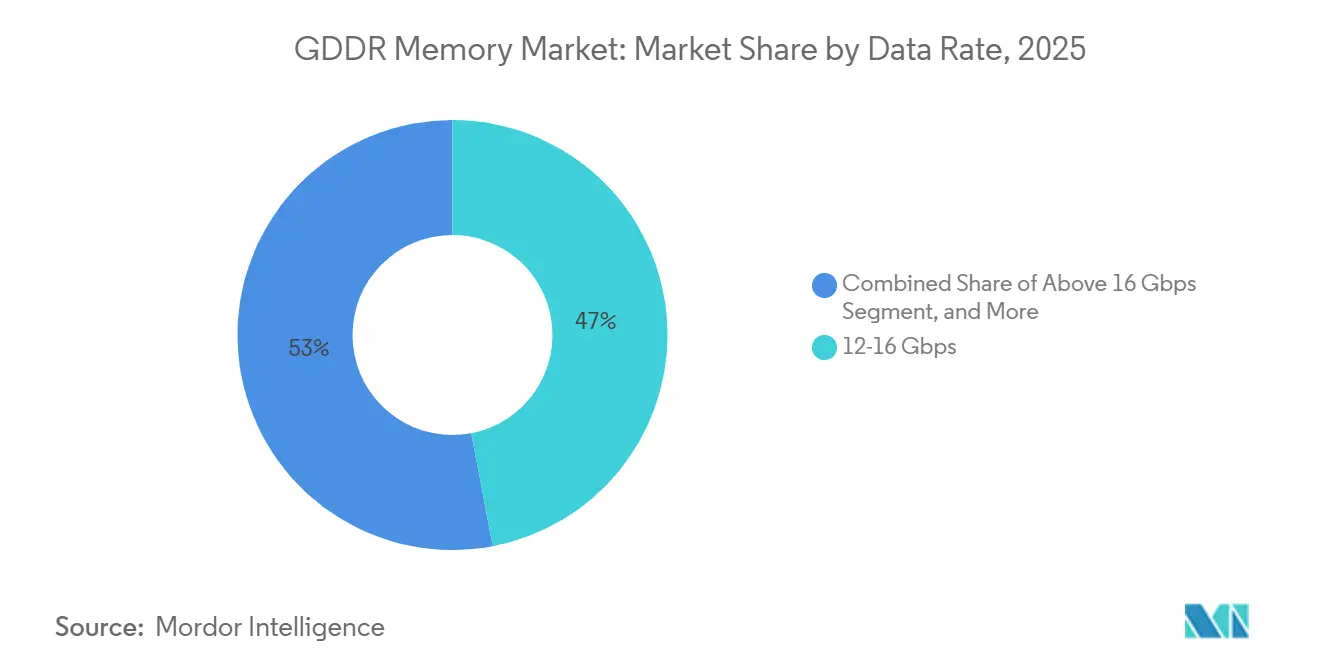

- By data rate, 12-16 Gbps products captured 47.39% of the 2025 value, yet speeds above 16 Gbps are expected to climb at 13.77% through 2031.

- By end-user industry, consumer electronics commanded 68.31% share in 2025, but IT and data centers are anticipated to record a 13.99% CAGR to 2031.

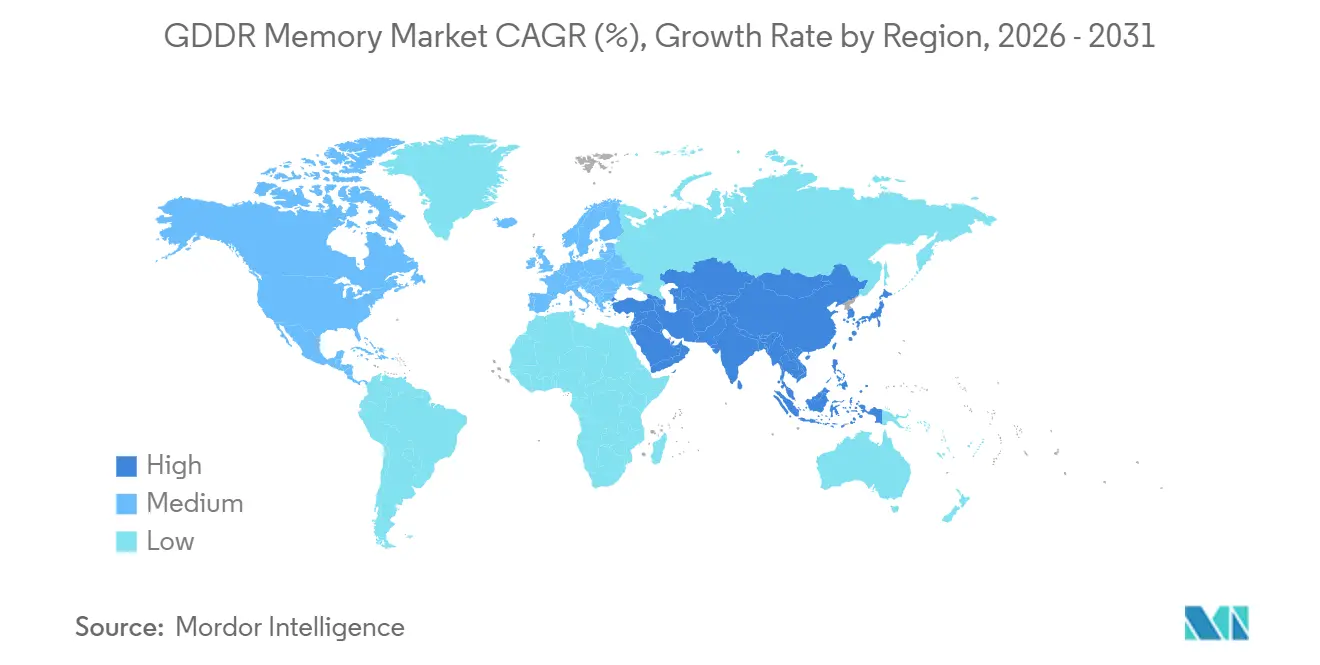

- By geography, Asia-Pacific dominated with 68.42% of 2025 revenue and is projected to expand at 14.19% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GDDR Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Real-Time Ray Tracing in AAA Games | +2.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2–4 years) |

| Expansion of AI Accelerator Cards Requiring High-Bandwidth Memory | +2.5% | Global, led by North America data centers and Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Increasing Adoption of 4K/8K Displays in Consumer Electronics | +1.9% | Global, with early adoption in Asia-Pacific and North America | Medium term (2–4 years) |

| Rising Data Center GPU Deployments for Cloud Gaming Services | +1.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2–4 years) |

| Maturing 10 nm-Class DRAM Node Enabling Cost-Effective GDDR6 Production | +1.4% | Asia-Pacific (South Korea, Taiwan), spill-over to global supply | Long term (≥ 4 years) |

| Government Incentives for Domestic Semiconductor Manufacturing | +1.2% | North America (CHIPS Act), Europe (EU Chips Act), Asia-Pacific (South Korea, Japan) | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Growing Demand for Real-Time Ray Tracing in AAA Games

NVIDIA’s GeForce RTX 50 series debuted in January 2025 with GDDR7 running at 30 Gbps, delivering 1.7 TB/s aggregate bandwidth on the RTX 5090 and enabling path-traced lighting pipelines previously limited to offline renders. DLSS 4 adoption expanded to more than 250 titles the same year, escalating bandwidth needs for pixel-accurate reflections and global illumination. AMD’s Radeon RX 9000 family, released in February 2025, relied on 18-20 Gbps GDDR6 to service mainstream ray-traced workloads, reinforcing GDDR6 as the volume node while ceding the performance crown to GDDR7. Micron data shows 30% higher frame rates for GDDR7-equipped boards across 1080p to 4K tests relative to GDDR6, confirming bandwidth as the critical performance lever.[1]Micron Technology, “Micron® GDDR7 Product Brief,” micron.com As studio pipelines shift from rasterization to hybrid tracing, GPU vendors market sustained memory throughput as a headline spec, propelling the GDDR memory market.

Expansion of AI Accelerator Cards Requiring High-Bandwidth Memory

Edge inference and workstation AI workloads increasingly opt for GDDR7 over costly HBM stacks. NVIDIA’s RTX PRO 6000 Blackwell, launched in March 2025, integrates 96 GB of GDDR7 memory, delivering 1.79 TB/s and supporting local large-language-model inference and generative image synthesis.[2]Samsung Electronics, “Samsung Develops Industry's First 24Gb GDDR7 DRAM,” news.samsung.com Samsung’s 24 Gb GDDR7, introduced in October 2024, uses PAM3 signaling to exceed 40 Gbps while cutting power draw by more than 30% through clock-gating and dual-VDD rails. Micron benchmarks suggest 20% lower inference latency than GDDR6 at 32 Gbps. These performance and cost dynamics widen the GDDR memory market beyond gaming into enterprise AI hardware.

Increasing Adoption of 4K/8K Displays in Consumer Electronics

Higher native resolutions in monitors, televisions, and creative workstations demand larger frame buffers and faster memory throughput. Samsung’s 24 Gbps GDDR6 delivers roughly 1.1 TB/s on 384-bit buses, sufficient to stream 275 Full-HD movies each second and sustain 8K playback without frame drops. An uncompressed 8K HDR frame can exceed 200 MB, meaning 60-fps playback requires more than 96 GB/s just for pixel data, before shading overhead. GDDR7’s 1.5 TB/s ceiling provides 60% more headroom than GDDR6, directly addressing this bottleneck. Console roadmaps for 2026 point to GDDR6X or GDDR7 adoption to hit 120 Hz 4K targets, shifting high-speed GDDR from enthusiast PCs into living-room devices. This resolution race keeps the GDDR memory market on a high-volume trajectory.

Rising Data Center GPU Deployments for Cloud Gaming Services

Cloud gaming converts capital-intensive GPUs into subscription revenue, but only when memory bandwidth supports 4K streams at sub-40 ms latency. GeForce NOW rolled out RTX 5080 servers sporting 48 GB GDDR7 in August 2025, enabling 4K120 streaming with ray tracing. Micron’s GDDR7 improves performance per watt by 50% versus GDDR6 through lower 1.2 V core voltage and deep-sleep modes that trim standby power 70%. Samsung mirrors this efficiency gain with power gating derived from mobile-DRAM. These cost-to-serve improvements make GDDR-equipped blades more attractive than HBM accelerators for consumer-facing GPU-as-a-service models, thereby expanding GDDR memory's footprint in hyperscale facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions Due to Geopolitical Tensions | -1.8% | Global, with acute impact on Taiwan and South Korea production, spill-over to North America and Europe | Short term (≤ 2 years) |

| Rising ASP Volatility Linked to Cryptocurrency Mining Cycles | -1.5% | Global, with price spikes concentrated in Asia-Pacific and North America retail channels | Short term (≤ 2 years) |

| Thermal Design Constraints in High-Density GDDR Packages | -0.9% | Global, affecting compact form factors in gaming laptops and embedded systems | Medium term (2–4 years) |

| Competition From HBM3 in High-Performance Computing | -0.7% | North America and Asia-Pacific data centers, limited impact on consumer and embedded segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions Due to Geopolitical Tensions

US export rules tightened in December 2024, adding 140 mainland Chinese entities to the Entity List and restricting on-site tool service critical for 10 nm DRAM lines. ChangXin Memory Technologies has stockpiled spares to buffer until 2027, but lead times for niche lithography modules remain above 60 weeks. South Korea’s dominance, with USD 173.4 billion in semiconductor exports in 2025, creates single points of failure that are further amplified by maritime choke points. Alleged intellectual-property leaks worth KRW 5 trillion (USD 3.56 billion) in December 2025 underscore rivalry risks. Buyers now carry 40-week inventories, inflating working capital and pressuring OEM margins, a drag on the GDDR memory market growth vector.

Rising ASP Volatility Linked to Cryptocurrency Mining Cycles

Between May 2025 and January 2026, DDR5 16 Gb spot prices tripled, dragging GDDR6 and GDDR7 quotes higher by 20% quarter-on-quarter in Micron’s fiscal Q1 2026. While major coins pivoted to proof-of-stake, smaller algorithms still lean on GPU hash power, periodically sapping retail supply. Morningstar expects tight conditions to persist until late 2027, when incremental cleanroom capacity from the Yongin and Idaho fabs comes online. Limited DRAM inventories, just 2-3 weeks in early 2026, leave the GDDR memory market exposed to fresh price spikes should mining profitability rebound.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: Volume GDDR6 Persists as GDDR6X and GDDR7 Scale

GDDR6's market share reached 53.84% in 2025, reflecting broad design wins across gaming, workstation, and automotive boards. Sustained 18-20 Gbps speed bins and mature yield profiles enable cost advantages that keep GDDR6 the default choice for mainstream cards. Momentum for GDDR6X is strongest in enthusiast GPUs, where its 13.79% forecast CAGR mirrors rising appetite for 20-23 Gbps lanes. At the cutting edge, Micron and Samsung now sample GDDR7 with 32-40 Gbps capability, promising 60% higher system bandwidth and resetting performance expectations.[3]Micron Technology, “GDDR7 | Micron Technology Inc.,” micron.com Over the medium term, OEMs are expected to split workflows: cost-sensitive SKUs on GDDR6, flagship parts on GDDR7, and sustain healthy multi-node demand within the GDDR memory market share landscape.

Backward-compatible GDDR5 and GDDR5X continue to play a significant role in supporting consoles and value GPUs, providing a cost-effective solution for these segments. However, the increasing obsolescence of these nodes and the reduction in wafer allocations indicate their gradual phase-out, which is expected to be completed by 2028. Samsung’s strategy of sampling 24 Gbps GDDR6 highlights the company's focus on extending the lifecycle of the current node, ensuring its relevance until GDDR7 production capacity becomes more widely available. As a result, buyers will face an extended transition period where GDDR5, GDDR5X, and GDDR6 coexist in the market. During this time, they will need to carefully balance their bill-of-materials (BOM) budgets with their performance requirements to make optimal purchasing decisions.

By Application: Gaming Dominance Meets AI-Centric Upside

Gaming graphics captured 59.32% of the GDDR memory market share in 2025, driven primarily by the consistent demand for discrete GPU shipments to PC builders and console OEMs. However, unit growth in this segment is showing signs of plateauing, prompting suppliers to shift their focus to emerging AI and compute workflows. These workflows are now demonstrating the fastest growth, with a compound annual growth rate (CAGR) of 13.68%. The RTX PRO 6000 Blackwell, with a 96 GB frame buffer, is a prime example of this strategic shift. It highlights the adoption of GDDR7 as a cost-effective alternative to HBM for inference cards, particularly in scenarios where latency and board-level simplicity take precedence over achieving multi-terabyte-per-second aggregates.

In the professional visualization segment, the market is increasingly adopting a hybrid approach that blends traditional gaming technologies with advanced AI capabilities. Meanwhile, embedded graphics for automotive clusters are leaning toward mid-speed GDDR6, as the extended qualification cycles in this sector favor the use of mature nodes. Across various verticals, the ongoing transition from pure raster pipelines to a combination of ray-traced and AI-enhanced workloads is further reinforcing the structural demand for high-bandwidth graphics DRAM, ensuring its critical role in supporting next-generation applications.

By Density: Mainstream 8-16 GB Still Leads as >16 GB Adds Headroom

Devices in the 8-16 GB band accounted 53.16% of 2025 sales, highlighting their suitability for 1440p gaming and mid-range workstation cards. These devices strike a balance between performance and cost, making them a preferred choice for gamers and professionals seeking reliable solutions for moderate workloads. The GDDR memory market size for densities above 16 GB, however, is forecast to grow faster, with a 13.83% CAGR, driven by increasing demand from 4K cloud-gaming servers and AI inference boards that support multiple concurrent tenants. Samsung’s 24 GB dies, for instance, enable 96 GB configurations on single-slot add-in cards, which not only reduce the number of boards required but also simplify PCB routing, thereby improving overall efficiency and cost-effectiveness.

Sub-8 GB offerings continue to dominate as price leaders in entry-level SKUs, catering to budget-conscious consumers. However, these products face growing competition as unified memory footprints expand, leading to a gradual shift in market dynamics. To address this, suppliers are advancing their 24 Gb and 32 Gb node roadmaps, ensuring alignment with JEDEC standards while minimizing per-bit cost declines. This strategic approach aims to meet evolving market demands while maintaining competitive pricing and performance benchmarks.

By Data Rate: 12-16 Gbps Retains Volume, Above 16 Gbps Becomes New Normal

Roughly 47% of 2025 revenue flowed through 12-16 Gbps channels, leveraging GDDR6’s 18–20 Gbps performance range, which has become a key sweet spot for the market. However, the industry is under increasing pressure to transition to higher-bandwidth solutions. GDDR7, with its initial 32 Gbps bins and Samsung’s experimental 40 Gbps targets, offers significant bandwidth improvements, achieving up to 2× gains without the need to double the clock frequency. These advancements are expected to drive the next wave of innovation in the market, addressing the growing demand for higher performance in gaming and professional applications.

One of the key technological advancements in GDDR7 is the adoption of PAM3 encoding, which delivers 1.5 bits per unit interval (UI). This approach helps mitigate eye-margin erosion and simplifies PHY design compared to PAM4 encoding used in GDDR6X. As GPU shader counts continue to increase, memory speeds exceeding 16 Gbps are anticipated to become the standard for high-performance enthusiast and workstation boards with a CAGR of 13.77%. This shift is likely to gradually erode the market share of legacy memory solutions, further solidifying the role of advanced memory technologies in meeting the industry's evolving needs.

By End-User Industry: Consumer Electronics Still Commanding, Enterprise Momentum Accelerates

Consumer electronics accounted for 68.31% of 2025 shipments, driven by strong demand across gaming PCs, laptops, and consoles. This dominance has solidified GDDR memory's presence on retail shelves, catering to the growing demand for high-performance computing in consumer devices. Enterprise IT and data centers are projected to exhibit the highest CAGR of 13.99%, driven by the expansion of cloud gaming server infrastructure and edge inference appliances. These applications leverage GDDR’s pin-compatible architectures, which offer advantages over DDR or HBM in terms of flexibility and performance. Media and entertainment studios are also transitioning to GDDR7 to support real-time VFX pipelines, further contributing to the market's growth trajectory.

The industrial and healthcare sectors continue to maintain steady demand for ruggedized GDDR6 modules designed to withstand challenging environments. Meanwhile, the aerospace and defense sectors, though representing a niche market, command premium average selling prices (ASPs) for specialized variants such as extended-temperature and radiation-hardened modules. These high-margin products provide lucrative opportunities for suppliers willing to meet the stringent specifications required in these industries. Collectively, these diverse applications underscore the versatility and growing adoption of GDDR memory across various end-user segments, ensuring sustained market growth in the forecast period.

Geography Analysis

Asia-Pacific accounted for 68.42% of the GDDR memory market share in 2025 and is projected to expand at a 14.19% CAGR to 2031. South Korea hosts the world’s largest DRAM mega-fabs, including Samsung’s Pyeongtaek and SK hynix’s Icheon and Yongin campuses, which together churn out more than 65% of global GDDR wafers. Samsung increased Xi’an NAND investment by 67.5% year on year to KRW 465.4 billion (USD 308.8 million), diverting capital toward memory capacity for AI workloads. SK hynix, meanwhile, committed KRW 21.6 trillion (USD 15.2 billion) to accelerate Yongin’s cleanroom start to February 2027, positioning the cluster as the first high-volume 1γ DRAM site. China’s ChangXin Memory Technologies crept to roughly 5% global DRAM share by Q3 2025, buoyed by state-backed funds and a planned USD 4.2 billion Shanghai IPO.

North America represents the fastest strategic shift in fabrication localization. Micron’s USD 20 billion FY 2026 CAPEX is allocated to finance new DRAM fabrication facilities in Idaho and New York, as well as a USD 7 billion advanced-packaging hub in Singapore. This significant investment is supported by the CHIPS and Science Act, which awarded Micron USD 6.165 billion and Intel USD 7.865 billion in direct grants. These grants aim to anchor a robust domestic back-end ecosystem, reducing reliance on overseas production. In contrast, Europe’s EU Chips Act lags behind with smaller pilot lines, leaving the region heavily dependent on imports to meet its semiconductor needs.

South America and the Middle East and Africa currently account for marginal volumes in the global semiconductor market. However, these regions are experiencing low-teens demand growth, driven primarily by the import of gaming rigs and OEM-distributed products. Despite this growth, limited local assembly capacity and underdeveloped semiconductor policies hinder their ability to establish a significant manufacturing presence. As a result, these regions are expected to continue relying on Asia-Pacific-produced dies throughout the forecast period, maintaining their current share in the GDDR memory market.

Competitive Landscape

The GDDR memory market remains highly concentrated, with Samsung, SK hynix, and Micron collectively accounting for over 90% of the global die supply. Samsung achieved a significant milestone by commercializing the first 24 GB GDDR7 in early 2025, specifically targeting high-performance applications such as workstation AI and automotive ADAS sockets. SK hynix, meanwhile, has been prioritizing its HBM expansion efforts, with its KRW 31 trillion (USD 23.25 billion) Yongin project housing phased 1β and 1γ DRAM lines. However, this focus on HBM production may constrain its near-term GDDR output.[4]SK hynix Newsroom, “New Facility Investment for Yongin Semiconductor Cluster,” news.skhynix.com Micron, on the other hand, has introduced its 1β-node GDDR7, which delivers 50% higher performance per watt and 70% lower standby current. This innovation has secured Micron design slots in NVIDIA GeForce RTX 50 and RTX PRO 6000 boards, further solidifying its competitive position in the market.

Emerging players, such as ChangXin Memory Technologies, are attempting to establish a foothold in the market by pivoting to multi-stack HBM3E while simultaneously seeking GDDR qualifications. However, these efforts face significant challenges due to technological and export barriers, resulting in a lag of 2-3 years compared to established players. In the downstream segment, module makers like ADATA, Kingston, Corsair, G.Skill, TeamGroup, and Crucial are focusing on differentiation through advanced thermal solutions rather than competing on silicon. This approach allows them to address specific market needs and carve out a niche despite the dominance of the top suppliers in the GDDR memory market.

As competition between HBM and GDDR lines intensifies, customers are increasingly adopting multi-source contracts to mitigate the risks of supply constraints and allocation battles. However, the oligopolistic nature of the supplier base enables dominant players to maintain pricing power, thereby ensuring robust margins across the GDDR memory market. This dynamic not only reinforces profitability for leading suppliers but also presents significant challenges for new entrants and downstream players attempting to compete in this highly consolidated market.

GDDR Memory Industry Leaders

Samsung Electronics Co., Ltd.

SK Hynix Inc.

Micron Technology, Inc.

Winbond Electronics Corporation

Powerchip Semiconductor Manufacturing Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Samsung ramped GDDR6 output for Tesla infotainment units, extending graphics DRAM into automotive electrification platforms.

- February 2026: SK hynix added KRW 21.6 trillion (USD 15.2 billion) to Yongin Phase 2-6 construction, bringing the first cleanroom launch forward to Feb 2027.

- March 2025: NVIDIA released the RTX PRO 6000 Blackwell with 96 GB of GDDR7, delivering 1.79 TB/s of bandwidth.

- February 2025: AMD introduced Radeon RX 9000 series featuring 8-16 GB 18-20 Gbps GDDR6 modules for mid-tier gaming.

Global GDDR Memory Market Report Scope

The GDDR (Graphics Double Data Rate) Memory Market refers to the global industry focused on the design, manufacturing, and commercialization of high-speed graphics memory used primarily in graphics processing units (GPUs) and other high-performance computing devices. GDDR memory is optimized for high bandwidth and fast data transfer rates, enabling efficient rendering, parallel processing, and compute-intensive operations across a wide range of applications.

The GDDR Memory Market Report is Segmented by Memory Type (GDDR5, GDDR5X, GDDR6, and GDDR6X), Application (Gaming Graphics, Professional Visualization, AI and Compute, and Embedded and Industrial Graphics), Density (≤ 8 Gb, 8-16 Gb, and > 16 Gb), Data Rate (≤ 12 Gbps, 12-16 Gbps, and > 16 Gbps), End-User Industry (Consumer Electronics, IT and Data Centers, Media and Entertainment, Industrial and Healthcare, and Aerospace and Defense), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| GDDR5 |

| GDDR5X |

| GDDR6 |

| GDDR6X |

| Gaming Graphics |

| Professional Visualization |

| AI and Compute |

| Embedded and Industrial Graphics |

| ≤ 8 Gb |

| 8-16 Gb |

| Above 16 Gb |

| ≤ 12 Gbps |

| 12-16 Gbps |

| Above 16 Gbps |

| Consumer Electronics (Gaming, Consoles) |

| IT and Data Centers (AI, Cloud Inference) |

| Media and Entertainment (Rendering, VFX) |

| Industrial and Healthcare |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East and Africa |

| By Memory Type | GDDR5 | |

| GDDR5X | ||

| GDDR6 | ||

| GDDR6X | ||

| By Application | Gaming Graphics | |

| Professional Visualization | ||

| AI and Compute | ||

| Embedded and Industrial Graphics | ||

| By Density | ≤ 8 Gb | |

| 8-16 Gb | ||

| Above 16 Gb | ||

| By Data Rate | ≤ 12 Gbps | |

| 12-16 Gbps | ||

| Above 16 Gbps | ||

| By End-User Industry | Consumer Electronics (Gaming, Consoles) | |

| IT and Data Centers (AI, Cloud Inference) | ||

| Media and Entertainment (Rendering, VFX) | ||

| Industrial and Healthcare | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the GDDR memory market and how fast will it grow through 2031?

The GDDR memory market size stands at USD 17.4 billion in 2026 and is forecast to reach USD 32.05 billion by 2031, registering a 12.99% CAGR.

Which memory type is expected to grow the fastest by 2031?

GDDR6X shows the highest projected growth rate at 13.79% CAGR because premium gaming and visualization GPUs continue to migrate to higher pin speeds.

Why is Asia-Pacific so dominant in GDDR production?

South Korea's large-scale DRAM fabs and China's expanding GPU demand result in Asia-Pacific holding more than two-thirds of global revenue, a share bolstered by ongoing capacity expansions from Samsung and SK hynix.

How will AI workloads influence future GDDR demand?

Edge and workstation inference cards increasingly favor GDDR7 for its latency and cost advantages over HBM, driving the AI and compute segment's 13.68% CAGR through 2031.

What geopolitical factors could disrupt GDDR supply?

Tightened US export controls and heightened Taiwan Strait tensions threaten equipment servicing and wafer shipments, potentially extending lead times and elevating prices.

How do GDDR7 efficiency gains translate into data center economics?

GDDR7 consumes roughly 50% less energy per bit than GDDR6 thanks to lower operating voltage and deep-sleep modes, cutting power budgets and improving total cost of ownership for cloud-gaming fleets.

Page last updated on: