Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.05 Billion |

| Market Size (2031) | USD 35.47 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

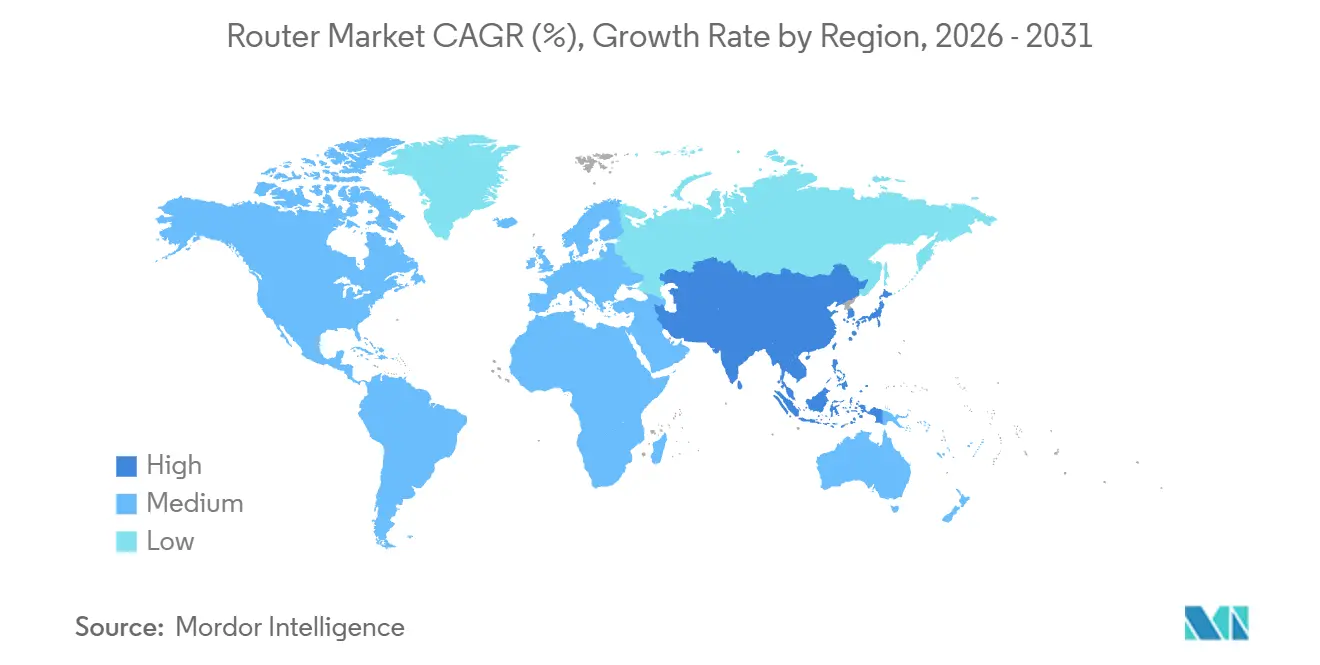

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Router Market Analysis by Mordor Intelligence

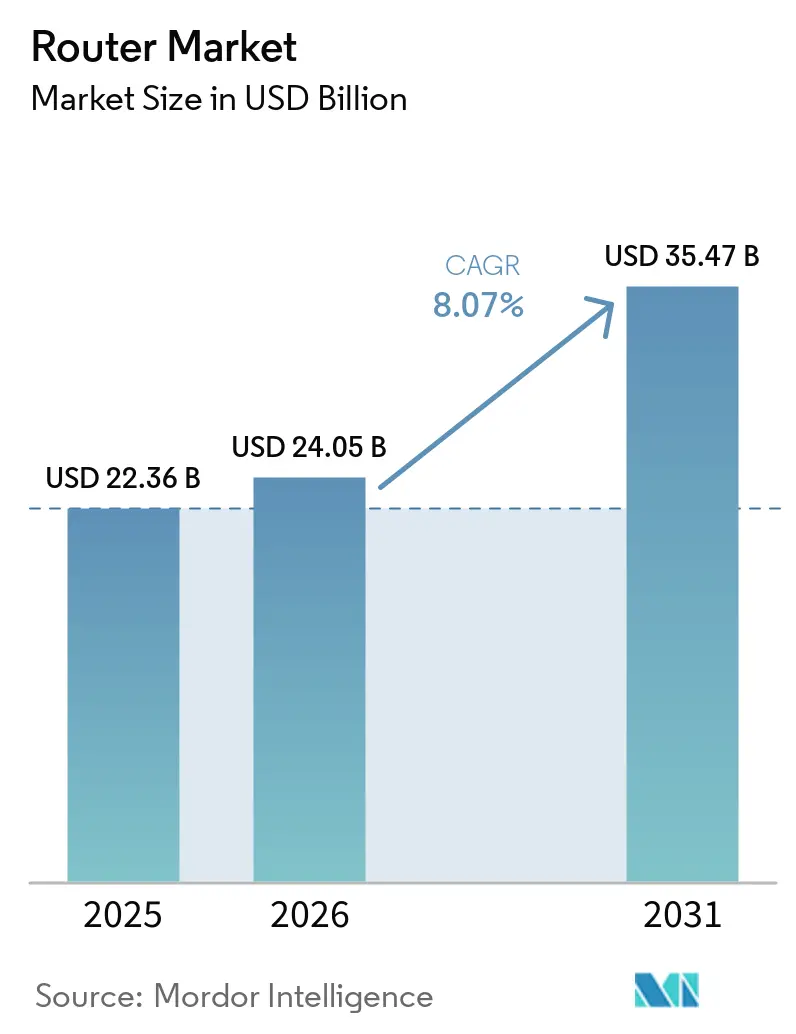

The router market size is projected to expand from USD 22.36 billion in 2025 and USD 24.05 billion in 2026 to USD 35.47 billion by 2031, registering a CAGR of 8.07% between 2026 and 2031. Continuing cloud migration, fiber-to-the-premises rollouts, and industrial deterministic-networking needs are reshaping routing architectures across consumer, telecom, and manufacturing settings. Wireless platforms still dominate the router market, yet 5G-ready cellular models are capturing the fastest incremental demand as private-network pilots shift into scaled production. Mid-throughput systems for 1-10 Gbps traffic remain the workhorse of enterprise campuses, while hyperscalers are already ordering ultra-high-throughput chassis that handle 400 GbE and 800 GbE links for distributed AI clusters. Regionally, North America benefits from zero-trust programs and broadband-equity grants, whereas Asia-Pacific leads growth on the back of dense 5G deployments and smart-city investments. Competitive intensity is rising as open-standards consortia promote disaggregated software and erode legacy vendor margins, yet feature-rich management stacks and bundled security remain effective defensive moats for incumbents.

Key Report Takeaways

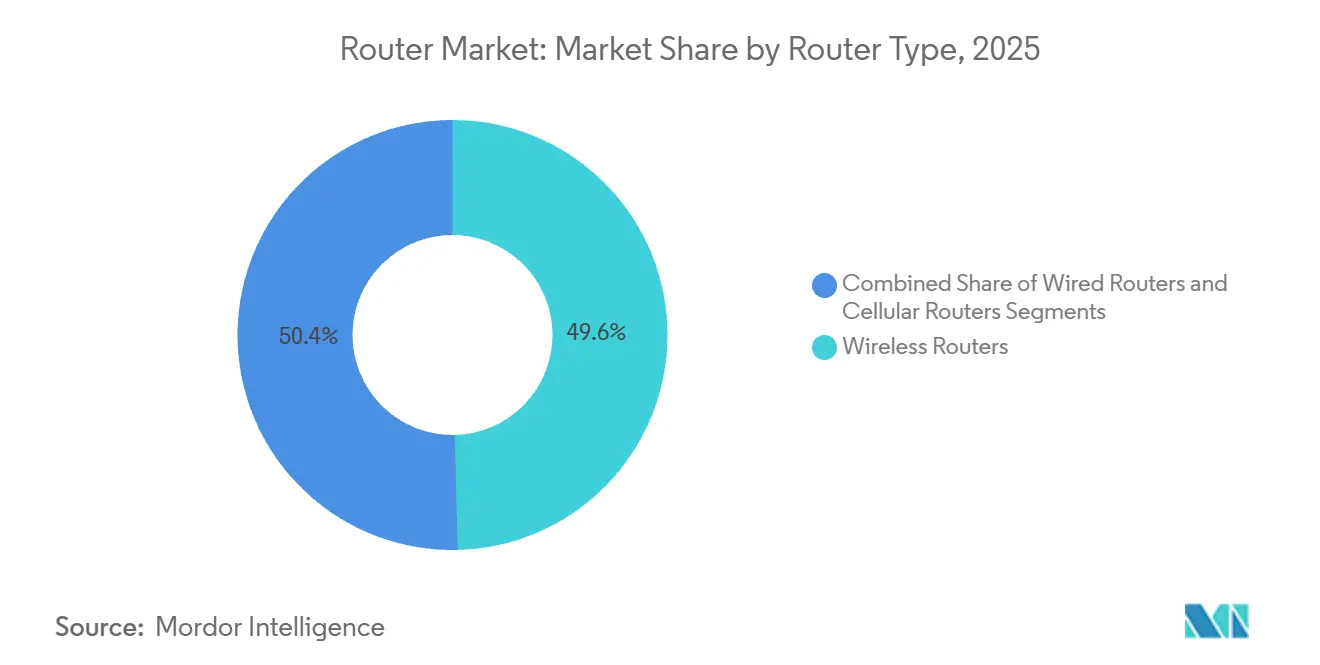

- By router type, wireless models held 49.62% of the router market share in 2025, while cellular platforms are projected to advance at an 11.24% CAGR through 2031.

- By performance tier, mid-throughput systems accounted for 39.18% of the router market size in 2025, whereas ultra-high-throughput platforms above 100 Gbps are set to grow at an 11.67% CAGR to 2031.

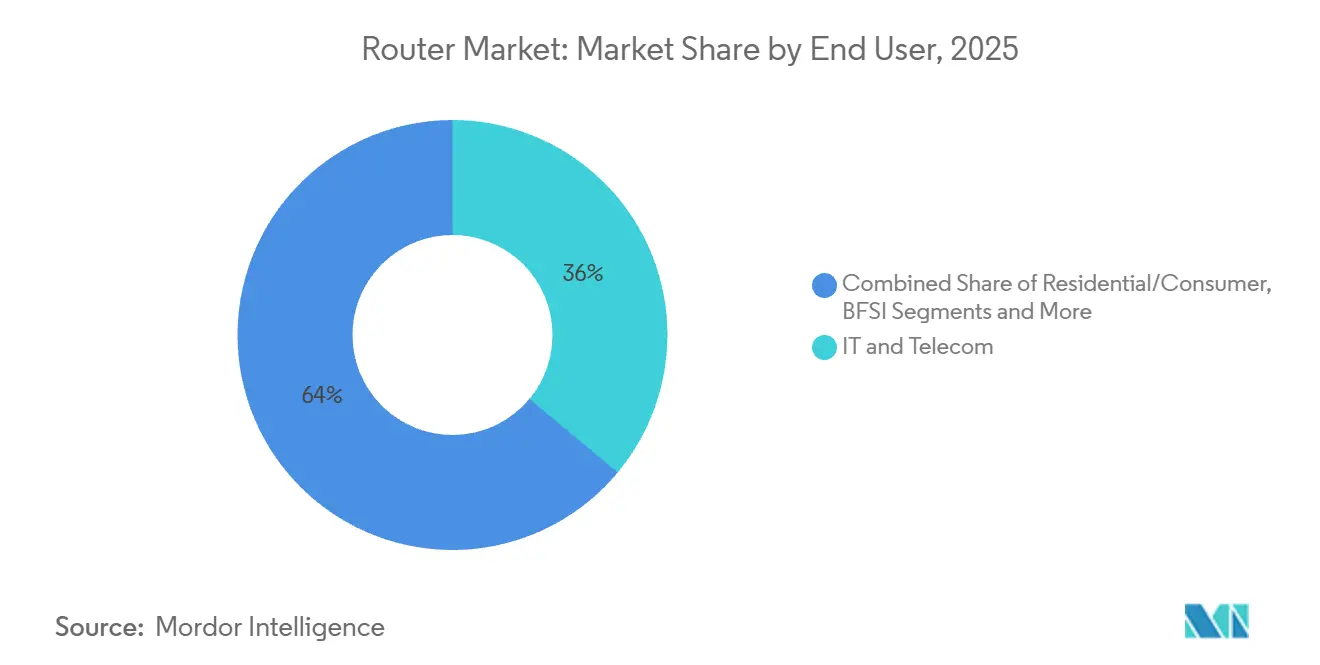

- By end user, IT and telecom led with 36.04% of router market share in 2025, while manufacturing is forecast to expand at a 9.94% CAGR through 2031.

- By sales channel, distributors and value-added resellers represented 46.35% of the router market size in 2025, and online marketplaces are expected to register a 10.28% CAGR to 2031.

- By geography, North America commanded 34.68% revenue share in 2025, yet Asia-Pacific is on track to post the fastest 10.36% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cross-Border Hiring in the Post-Pandemic Digital Economy | +2.3% | Global, strongest in North America and Europe with rapid growth in Asia-Pacific | Medium term (2–4 years) |

| Accelerating Adoption of Remote-First and Distributed Workforce Models | +2.0% | Global, led by North America and Western Europe | Short to Medium term (≤ 4 years) |

| Increasing Regulatory Scrutiny on Worker Classification and Compliance | +1.7% | North America and Europe | Medium term (2–4 years) |

| Growing Preference for Asset-Light International Expansion Among SMEs | +1.5% | Asia-Pacific, Latin America, and Europe | Medium term (2–4 years) |

| Expansion of Digital Nomad Visa Programs Across Multiple Countries | +1.2% | Europe, Middle East, and Asia-Pacific | Long term (≥ 4 years) |

| Rising Integration of HR Tech Platforms with EOR Solutions | +0.9% | Global, strongest in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Broadband Penetration And Demand For High-Speed Home Networking

Fiber-to-the-premises subscriptions exceeded 44.6% of fixed broadband lines across OECD economies in 2024, lifting household expectations for multi-gigabit Wi-Fi performance. Operators also forecast 350 million fixed-wireless access links by 2030, a figure that requires ruggedized outdoor 5G routers to bypass last-mile copper.[1]Ericsson, “Mobility Report 2024,” ericsson.com Full-fiber availability surpassed 69% of U.K. premises in 2024, causing service providers to bundle Wi-Fi 6E tri-band routers with gigabit plans. New residential gateways therefore integrate advanced QoS engines that prioritize latency-sensitive traffic such as cloud gaming and video conferencing. The result is a bifurcated router market: premium mesh systems for fiber homes and cellular gateways for underserved regions, each demanding unique supply-chain, pricing, and support models.

Proliferation Of Cloud Services Requiring Advanced Enterprise Routing

Hybrid and multicloud adoption is forcing enterprises to refresh branch and data-center routing so that SD-WAN overlays, automated failover, and application-aware path selection work seamlessly across public and private clouds. Cisco’s Cloud OnRamp delivers intent-based routing into AWS, Azure, and Google Cloud without manual BGP tuning. Arista’s CloudEOS extends consistent segmentation across on-prem and cloud fabrics, reducing operational toil for DevOps teams. Palo Alto Networks has fused routing with zero-trust security in a single appliance that lowers branch TCO and speeds deployment. Demand is therefore shifting toward routers with deep packet inspection and encrypted-traffic analytics, prompting vendors to monetize integrated software far more than raw port counts.

Rapid Adoption Of Wi-Fi 6 And Wi-Fi 7 Standards

Volume shipments of Wi-Fi 6E routers throughout 2024 and 2025 brought sub-5 millisecond latency and higher throughput for AR/VR headsets and industrial sensors. Early Wi-Fi 7 certification in 2024 unlocked 320 MHz channels and 4K-QAM, enabling over 40 Gbps theoretical speeds. The Telecom Infra Project’s OpenLAN specifications in 2025 further catalyzed disaggregated designs that let operators mix radio units and software stacks at will. While enterprise uptake leads, premium consumer demand is emerging among early adopters seeking future-proof mesh kits for metaverse workloads. Vendors that quickly pair Wi-Fi 7 radios with cloud-hosted management and cybersecurity add-ons are positioned to win share despite the inevitable commoditization of standalone hardware.

Emergence Of Multi-Access Edge Computing Driving Micro-Edge Routers

ETSI MEC specifications call for low-latency routers at cell sites and enterprise premises so that traffic can be processed locally rather than backhauled to regional data centers.[2]European Telecommunications Standards Institute, “MEC Specifications,” etsi.org 3GPP Release 17 adds detailed orchestration hooks between 5G user-plane functions and edge routers, making sub-10 millisecond latency feasible for autonomous vehicles and remote surgery. Nokia piloted MEC platforms with automotive OEMs in 2025, embedding slicing-aware routers that prioritize collision-avoidance telemetry. Cisco has ruggedized its industrial routers for hazardous oil and gas sites, where real-time sensor analytics boost drilling efficiency. As compute acceleration moves into routers through FPGAs and GPUs, the traditional boundary between networking and edge compute blurs, unlocking new revenue pools for vendors who master both domains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Divergent Social Security and Labor Regulations Increasing Compliance Complexity | -1.60% | Global, most complex in Europe and Latin America | Medium term (2–4 years) |

| High Cost of EOR Services Compared to Local Hiring in Low-Cost Markets | -1.30% | Asia-Pacific, Africa, and Latin America | Medium term (2–4 years) |

| Limited Awareness and Trust in EOR Model in Emerging Economies | -1.10% | Africa, Southeast Asia, and parts of the Middle East | Long term (≥ 4 years) |

| Data Privacy and Cross-Border Data Transfer Restrictions | -0.90% | Europe (GDPR), China, and Middle East | Medium term (2–4 years) |

| Risk of Permanent Establishment and Misclassification Liabilities | -0.70% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Shortages And Semiconductor Price Volatility

Lead times for routing ASICs stretched to 52 weeks in late 2024, postponing enterprise refresh cycles and lifting expedite fees that eroded margins. Broadcom projected AI-related networking silicon to top USD 100 billion by 2027, pitting hyperscalers against network-equipment makers for limited advanced-node capacity. Cisco disclosed lower hardware revenue in fiscal 2024 as it diverted scarce parts to high-margin software bundles. Arista secured multi-year wafer contracts to sustain 20% YoY growth despite shortages. Chiplet-based designs may diversify supply but raise testing complexity and leave smaller vendors exposed to allocation shocks during demand spikes.

Intense Price Competition Commoditizing Consumer Routers

Chinese ODMs now push dual-band Wi-Fi 6 routers below USD 50, undercutting legacy brands by as much as 40%. White-label devices and ISP-bundled gateways erode consumer brand loyalty, particularly in price-sensitive markets across Southeast Asia. Premium vendors, therefore, bundle parental controls, security subscriptions, and cloud management, yet attach rates remain below 15% of shipped units. ISP-supplied hardware already covers roughly 60% of North American and European households, limiting retail shelf space. Profitability is consequently concentrated in high-end mesh kits, a niche that cannot compensate for eroding entry-level margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Router Type: Cellular Platforms Gain Ground

Wireless routers, while still leading with 49.62% router market share in 2025, now face slowed growth as urban fiber penetration approaches saturation. Cellular platforms captured mounting attention in the router market as 5G private-network pilots became full commercial rollouts. Cellular routers are forecast to grow at an 11.24% CAGR through 2031, outpacing every other category. They anchor warehouse automation, mining telemetry, and smart-city lighting, where hard-wired links prove impractical. The GSM Association counted more than 1,000 commercial private-5G networks in 2024, each deploying multiple cellular gateways for low-latency connectivity.

Competition intensifies as vendors embed eSIMs and 5G modems into enterprise-grade wireless routers, delivering automatic failover when fixed lines drop. Cradlepoint’s 2025 portfolio added network-slicing support to split bandwidth between telematics and passenger Wi-Fi.[3]Cradlepoint, “5G-Advanced Router,” cradlepoint.com Teltonika and Digi International released rugged devices qualified for rail and maritime uses, broadening the addressable router market size for cellular-first deployments. Regulatory support for open APIs under Telecom Infra Project initiatives lowers switching costs, amplifying software as the true differentiator across router industry contenders.

By Performance Tier: Ultra-High Throughput Surges

Hyperscalers and telecom carriers are driving double-digit demand for routers exceeding 100 Gbps, a sub-segment expected to post an 11.67% CAGR to 2031. Arista’s 7800R4 and Juniper’s PTX10000 lines together illustrate the premium buyers place on density per rack unit and sub-microsecond latency. In contrast, mid-throughput routers held 39.18% router market share in 2025, underpinning campus cores and regional points of presence where balanced cost and feature sets suffice.

Low-throughput routers below 1 Gbps still ship in volume to small offices, yet the router market size growth story concentrates in high and ultra-high tiers as AI workloads spike east-west traffic. Cisco’s 8000 series integrated silicon photonics to lower energy per bit, aligning with European idle-power rules. Nokia’s coherent-optics approach allows carriers to collapse routing and transport, conserving power budgets and rack space. Vendors that optimize packet buffering and congestion algorithms for bursty AI traffic will capture an outsized share as 800 GbE becomes table stakes inside data centers.

By End User: Manufacturing Accelerates Adoption

IT and telecom players retained 36.04% router market share in 2025, due to core-network upgrades for 5G slicing and enhanced mobile broadband. Manufacturing, however, is projected to register a 9.94% CAGR between 2026 and 2031, lifting its portion of the router market size as automotive and semiconductor fabs pursue deterministic networking. IEC 60802 profiles make time-sensitive networking mandatory for robot arms and metrology cameras, pushing demand for routers capable of sub-millisecond jitter budgets.[4]IEC, “IEC/IEEE 60802,” iec.ch

Industrial giants such as Siemens and ABB now embed cybersecurity inspection and anomaly detection into shop-floor routers to thwart ransomware. Meanwhile, Rockwell Automation’s partnership with Cisco packages converged Ethernet and TSN functions for carmakers wishing to harmonize operational technology and IT traffic. As Industry 4.0 spreads, router industry suppliers must tailor certification, support, and lifecycle guarantees to mission-critical manufacturing environments.

By Sales Channel: Online Marketplaces Expand Reach

Distributors and value-added resellers controlled 46.35% of the router market size in 2025, underwriting complex deployments with financing, staging, and multi-vendor design services. Still, online marketplaces are projected to compound at 10.28% annually through 2031, buoyed by small firms buying subscription-based, cloud-managed devices that arrive overnight. Simplified zero-touch provisioning lowers technical barriers, allowing procurement managers rather than network architects to finalize purchases.

Hyperscalers are getting into last-mile access as well. Amazon’s Project Kuiper bundles satellite service with phased-array routers for rural subscribers, inserting a new vertically integrated competitor into the router market. Value-added resellers counter by layering managed services over hardware, shifting revenue toward recurring fees. The regulatory embrace of open-standards hardware pushes distributors to curate white-box line cards and software images, compressing vendor margins even as total router industry volumes rise.

Geography Analysis

North America retained 34.68% of 2025 revenue in the router market as zero-trust mandates and broadband-equity subsidies kept enterprises and ISPs upgrading to multi-gigabit gateways. Federal funding streams accelerate fiber builds in underserved counties, stimulating router demand across consumer and carrier aggregation layers. Meanwhile, data-center operators in the North America regionphase in 400 GbE fabrics to accommodate Artificial Intelligence training clusters, reinforcing orders for ultra-high-throughput chassis.

Asia-Pacific is the growth engine of the router market, forecast to log a 10.36% CAGR from 2026 to 2031. China had already erected 3.95 million 5G base stations by 2024 and is trialing 5G-Advanced features that demand edge routers with slicing awareness and AI-based traffic steering. India’s Smart Cities Mission added municipal edge routers for traffic management, video analytics, and automated utility metering, broadening the regional router market size. Emerging players like Huawei are shipping AI-enhanced power-optimized routers to fit stringent energy caps in dense metros.

Europe emphasizes sustainability. The European Commission’s Code of Conduct on Broadband Equipment Energy Consumption and Standby Regulation 2023/826 impose idle-power ceilings that trigger redesigned power-management circuits in new models.[5]European Commission, “Standby Regulation 2023/826,” ec.europa.eu Carriers in Germany, France, and Spain now bundle more efficient mid-throughput devices into business fiber contracts, while data-center operators slot silicon-photonic routers to align with carbon budgets. South America and Africa rely heavily on cellular routers for fixed-wireless access, bypassing capital-intensive fiber builds. The International Telecommunication Union recorded 8% YoY growth in developing-market fixed broadband lines during 2024, affirming the continued need for cost-effective routers that straddle Ethernet backhaul and LTE or 5G uplinks.

Competitive Landscape

The router market shows moderate concentration, with the top five vendors accounting for a substantial share of 2025 revenue. Cisco Systems safeguards leadership by bundling SD-WAN, firewall, and zero-trust functions into integrated appliances that simplify branch deployment. Arista Networks exploits hyperscale demand for 800 GbE with sub-500-nanosecond latency systems, carving a share in east-west AI fabrics. Juniper Networks agreed to a USD 14 billion takeover by Hewlett Packard Enterprise in January 2024, fusing AI-native routing with HPE’s edge cloud platforms.

White-box momentum continues under the Telecom Infra Project’s OpenLAN blueprint, letting carriers disaggregate hardware and software, which squeezes incumbent gross margins. Smaller challengers such as MikroTik and Ubiquiti leverage direct-to-customer e-commerce to undercut legacy list prices by up to 50%, drawing small and medium enterprises that value affordability over enterprise-grade support.

Technology differentiation is shifting from proprietary ASICs to software automation, threat detection, and AI-based analytics as merchant silicon from Broadcom and Marvell Technology levels raw throughput differences. Vendors that master lifecycle services, security subscriptions, and cloud-native orchestration will defend share even as hardware margins compress, while increasing investments in AI-driven network observability and intent-based networking are expected to further redefine competitive positioning.

Router Industry Leaders

Cisco Systems Inc.

Huawei Technologies Co Ltd.

Nokia Corporation

Hewlett Packard Enterprise Company

Arista Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cisco Systems launched its Silicon One G300 AI networking chip alongside a new router designed to accelerate data center traffic and improve AI workload efficiency by up to 28%.

- February 2026: Hewlett Packard Enterprise introduced new Juniper Networks PTX series routers (including PTX12000) with up to 49% better power efficiency and 800G/1.6T-ready capacity for AI-driven network infrastructure.

- February 2026: Arista Networks reported strong momentum in AI-driven routing and switching, with enterprise and hyperscale demand accelerating revenue growth and reinforcing its position in high-performance Ethernet networking.

- January 2026: Cisco Systems outlined its 2026 strategy focused on AI-ready networking infrastructure, emphasizing routing innovations to support exponential growth in AI and cloud data traffic.

Global Router Market Report Scope

The router market refers to the revenue generated from the sale of devices that direct and manage data traffic between different networks, enabling connectivity across homes, enterprises, data centers, and telecom infrastructures. Routers determine optimal paths for data transmission and are essential for linking local networks to external networks such as the internet, cloud platforms, and private WAN environments. The market includes wired, wireless, and cellular routers across performance tiers ranging from low-throughput consumer devices to high-capacity core and hyperscale routers exceeding 100 Gbps.

The Router Market Report is Segmented by Router Type (Wired Routers, Wireless Routers, and Cellular Routers), Performance Tier (Low Throughput, Mid Throughput, High Throughput, and Ultra-High), End User (Residential/Consumer, IT and Telecom, BFSI, Government and Defense, Manufacturing, Transportation and Logistics, and Other End Users), Sales Channel (Online Marketplaces, Direct Sales, and Distributors/Value-Added Resellers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Wired Routers |

| Wireless Routers |

| Cellular Routers |

| Low Throughput (<1 Gbps) |

| Mid Throughput (1-10 Gbps) |

| High Throughput (10-100 Gbps) |

| Ultra-High (>100 Gbps) |

| Residential/Consumer |

| IT and Telecom |

| BFSI |

| Government and Defense |

| Manufacturing |

| Transportation and Logistics |

| Others End Users |

| Online Marketplaces |

| Direct Sales |

| Distributors/Value-Added Resellers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Router Type | Wired Routers | |

| Wireless Routers | ||

| Cellular Routers | ||

| By Performance Tier | Low Throughput (<1 Gbps) | |

| Mid Throughput (1-10 Gbps) | ||

| High Throughput (10-100 Gbps) | ||

| Ultra-High (>100 Gbps) | ||

| By End User | Residential/Consumer | |

| IT and Telecom | ||

| BFSI | ||

| Government and Defense | ||

| Manufacturing | ||

| Transportation and Logistics | ||

| Others End Users | ||

| By Sales Channel | Online Marketplaces | |

| Direct Sales | ||

| Distributors/Value-Added Resellers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the global router market?

The router market size is USD 24.05 billion in 2026 and is projected to reach USD 35.47 billion by 2031, reflecting an 8.07% CAGR (Mordor Intelligence).

Which router segment is expanding the fastest?

Cellular routers are anticipated to post the highest 11.24% CAGR through 2031 as enterprises scale 5G private networks (Mordor Intelligence).

Which performance tier dominates enterprise upgrades?

Mid-throughput systems handling 1-10 Gbps traffic represent 39.18% of 2025 revenue, yet ultra-high-throughput platforms above 100 Gbps are the fastest growing at 11.67% CAGR (Mordor Intelligence).

Which region will contribute most to future growth?

Asia-Pacific is forecast to advance at a 10.36% CAGR between 2026 and 2031, driven by dense 5G infrastructure and smart-city projects (Mordor Intelligence).

What channel is gaining share in router sales?

Online marketplaces are set to grow at 10.28% annually to 2031 as small enterprises favor subscription-based, cloud-managed devices (Mordor Intelligence).

Page last updated on: