Low Alcohol Beverage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

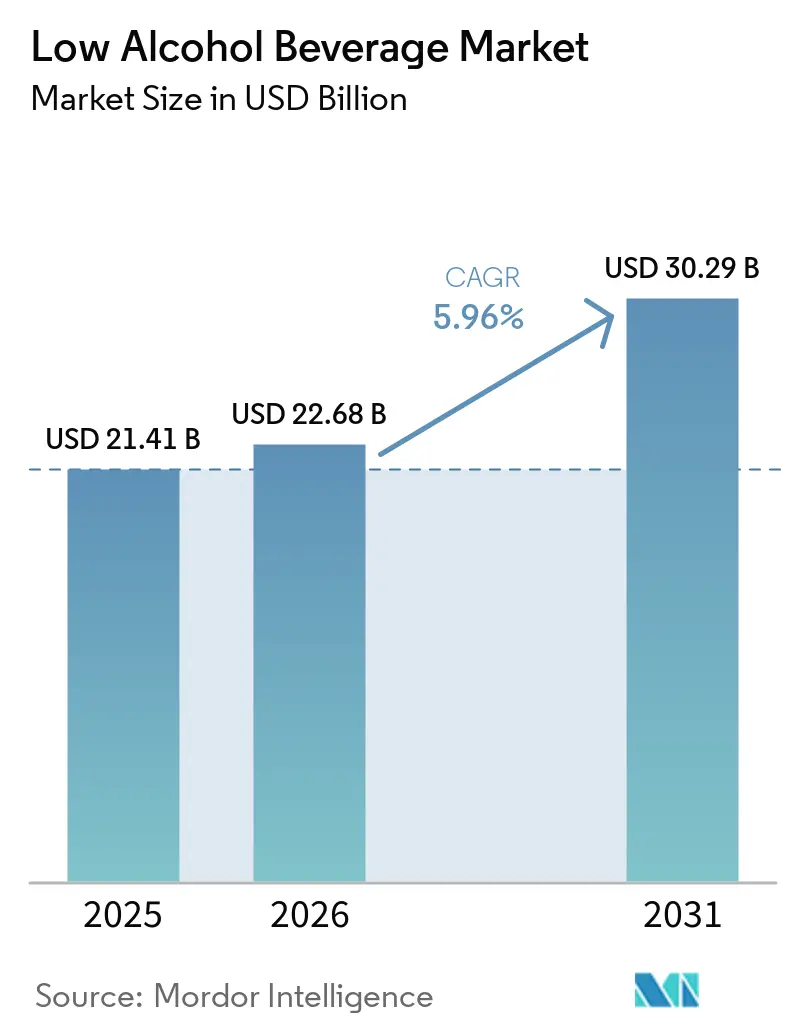

| Market Size (2026) | USD 22.68 Billion |

| Market Size (2031) | USD 30.29 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Low Alcohol Beverage Market Analysis by Mordor Intelligence

The low-alcohol beverage market is experiencing consistent growth, driven by a global shift in drinking habits toward moderation, wellness, and lifestyle compatibility. The market was valued at USD 21.41 billion in 2025 and grew to USD 22.68 billion in 2026, with forecasts estimating it will reach USD 30.29 billion by 2031, registering a CAGR of 5.96% during 2026–2031. This growth highlights a significant change in consumer preferences, with increasing demand for beverages that provide the social and sensory appeal of alcohol while reducing its adverse health impacts. Greater awareness of fitness, mental health, calorie management, and chronic disease prevention is shaping purchasing decisions, positioning low-alcohol beverages as a balanced choice rather than a compromise.

Key Report Takeaways

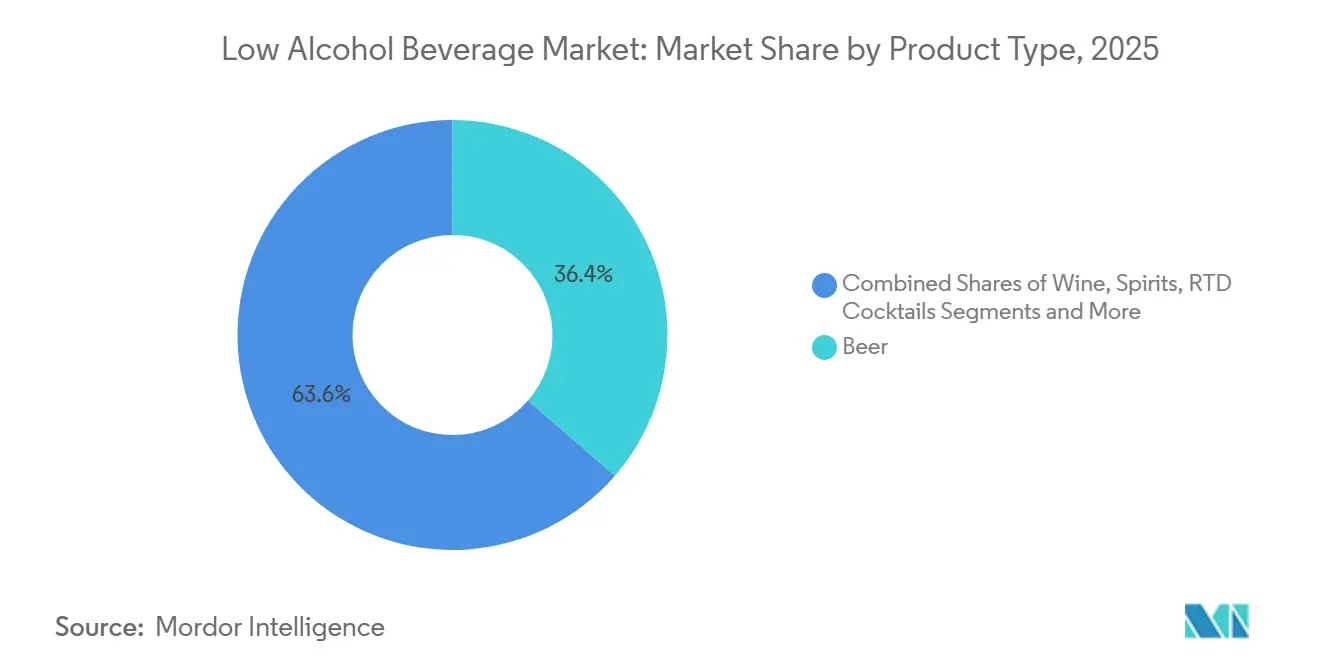

- By product type, beer led with 36.37% of low-alcohol beverage market share in 2025, while RTD cocktails are projected to rise at a 6.56% CAGR through 2031.

- By alcohol band, the 0.0-0.5% tier accounted for 68.17% of the low-alcohol beverage market size in 2025 and will advance at 6.42% CAGR to 2031.

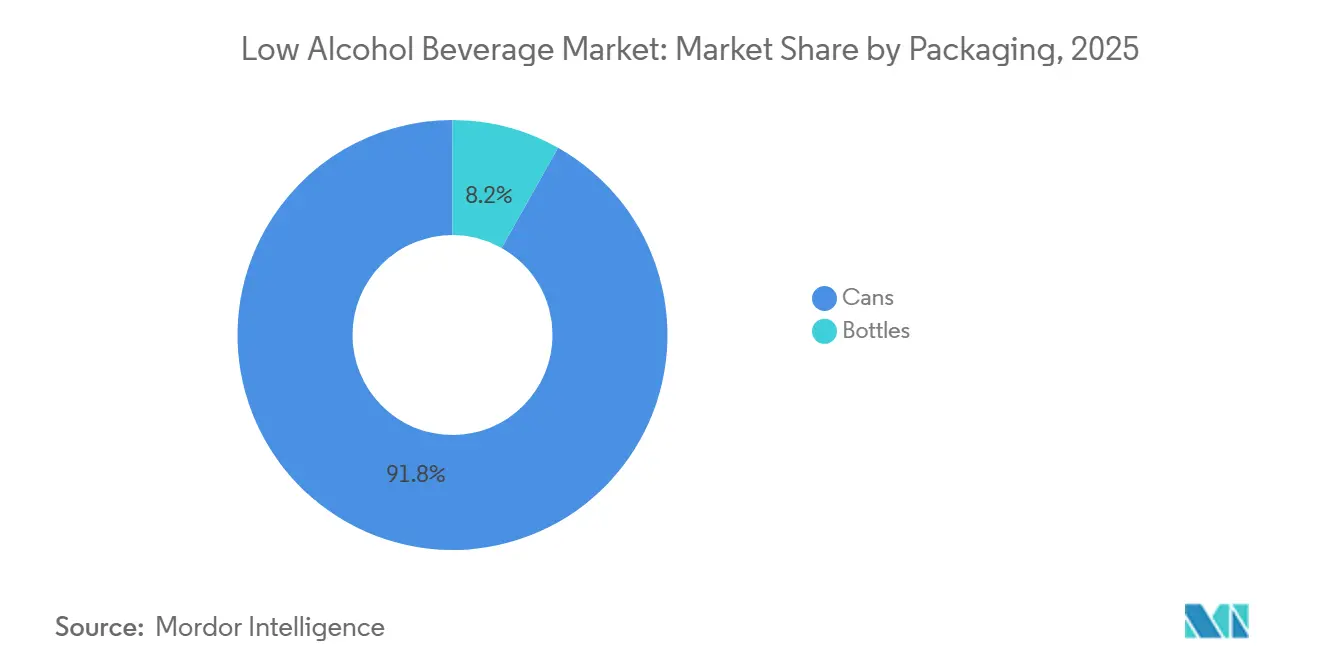

- By packaging, cans claimed 67.23% revenue share in 2025, whereas bottles are forecast to post a 5.98% CAGR on premium positioning.

- By distribution channel, retail captured 70.04% revenue in 2025; foodservice is the fastest-growing channel at a 6.12% CAGR to 2031.

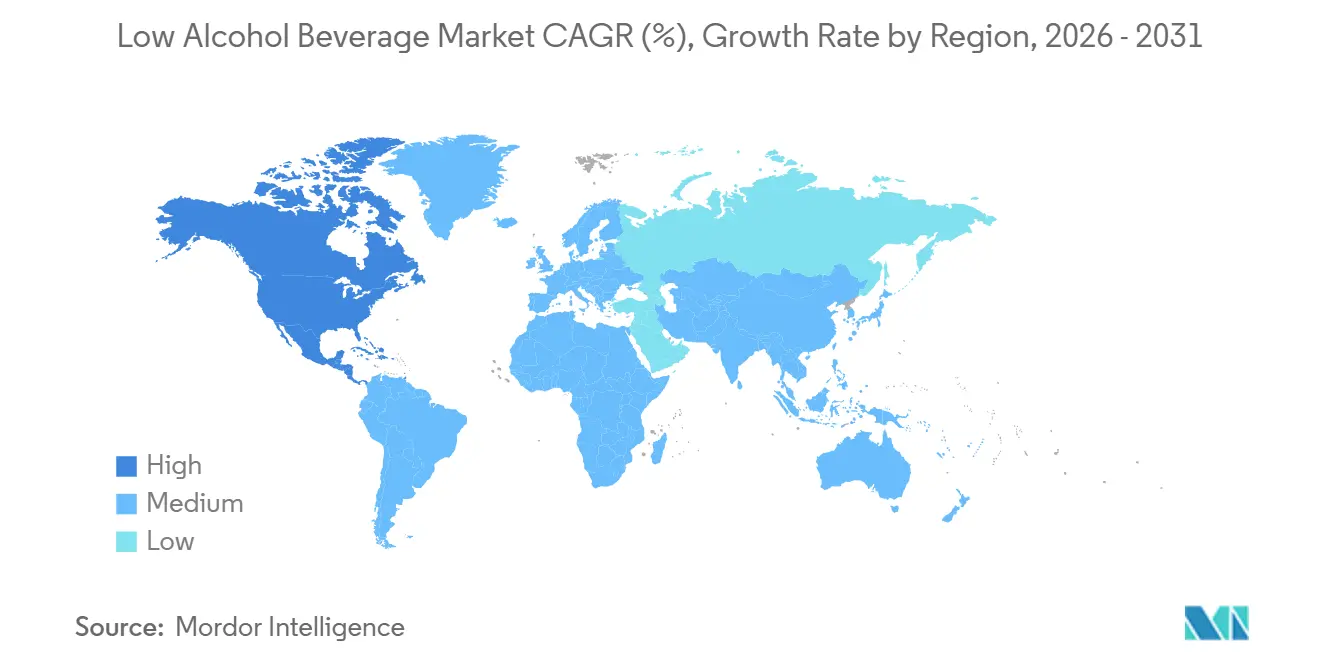

- By geography, Europe generated 34.49% of 2025 revenue; Asia-Pacific is the fastest-growing region at a 6.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Alcohol Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness awareness | +1.2% | Global, with strongest uptake in North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Increasing demand for ready-to-drink (RTD) products | +1.0% | North America, Europe, Australia; emerging in Latin America | Short term (≤ 2 years) |

| Changing drinking culture among younger generations | +1.4% | Global, led by North America and Europe; accelerating in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Strong influence of social media and lifestyle trends | +0.8% | Global, with peak influence in North America, Europe, and digitally connected Asia-Pacific markets | Short term (≤ 2 years) |

| Increasing popularity of premiumization | +0.9% | North America, Europe, Middle East; selective Asia-Pacific luxury segments | Medium term (2-4 years) |

| Innovation in brewing and distillation technologies | +0.7% | Global, with early adoption in Europe and North America; scaling in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness awareness

Increasing health and wellness awareness is a significant driver of the low-alcohol beverage market, as consumers focus more on long-term well-being, chronic disease prevention, and calorie management in their lifestyle choices. Concerns about conditions such as obesity, liver disorders, and cardiovascular health are prompting individuals to reduce alcohol consumption or opt for low- and non-alcoholic alternatives that pose fewer health risks while allowing for social engagement. Additionally, the growing emphasis on fitness, clean-label products, and balanced diets is steering consumers toward beverages with lower calorie content, reduced sugar levels, and minimal alcohol content. For example, the 2024 National Survey on Drug Use and Health (NSDUH) in the United States reported that approximately 228.4 million individuals aged 12 and older had consumed alcohol at some point in their lives, underscoring a broad consumer base that is increasingly reconsidering drinking habits in favor of moderation [1]Source: National Survey on Drug Use and Health (NSDUH), "Alcohol Use in the United States: Age Groups and Demographic Characteristics", niaaa.nih.gov.

Increasing demand for ready-to-drink (RTD) products

The growing demand for ready-to-drink (RTD) products is a key driver of the low-alcohol beverage market. This trend is supported by changing consumer lifestyles that emphasize convenience, portability, and time efficiency. RTD beverages require no preparation or mixing, making them particularly appealing for on-the-go consumption, casual gatherings, and at-home use. This convenience resonates strongly with younger consumers and urban populations who value quick, consistent, and hassle-free drinking experiences without sacrificing taste or quality. Consequently, low-alcohol RTD cocktails, spritzers, and flavored beverages are gaining significant traction across retail and foodservice channels. Additionally, many low-alcohol RTDs feature attributes such as reduced sugar, natural ingredients, and lower calorie content, aligning with the growing health and wellness trends.

Changing drinking culture among younger generations

The evolving drinking habits of younger generations are driving growth in the low-alcohol beverage market. Millennials and Gen Z consumers are increasingly shifting away from traditional heavy drinking patterns, favoring moderation, wellness, and experience-focused consumption. These younger demographics are adopting "mindful drinking" practices, often selecting low- or no-alcohol beverages that enable socialization without the adverse effects of higher alcohol consumption. This trend is influenced by heightened awareness of mental health, fitness objectives, and overall lifestyle balance, alongside the rising popularity of movements like the sober-curious trend. Demographic data further supports this generational shift. The Office for National Statistics in the United Kingdom reported that the Gen Z population reached approximately 13.6 million in 2024, encompassing individuals aged 12 to 27 years [2]Source: Office for National Statistics, "Population of Generation Z in the United Kingdom in 2024", ons.gov.uk. This substantial consumer group is actively transforming alcohol consumption patterns, favoring lighter and more adaptable drinking options that align with their values.

Strong influence of social media and lifestyle trends

The growing influence of social media and lifestyle trends is a significant driver of the low-alcohol beverage market. Digital platforms are increasingly shaping consumer preferences, brand perceptions, and purchasing behaviors. Platforms like Instagram, TikTok, and YouTube have enhanced the visibility of low- and no-alcohol beverages through influencer partnerships, lifestyle-focused content, and visually appealing product presentations. Younger demographics, in particular, are strongly influenced by online trends that promote moderation, wellness, and sober-curious lifestyles, which are becoming more normalized and aspirational. This digital exposure fosters product trials and accelerates the adoption of low-alcohol alternatives across various regions. Additionally, social media has been instrumental in popularizing modern drinking occasions and experiences, such as brunch culture, at-home mixology, and outdoor social gatherings, all of which align with the demand for lighter and more versatile beverage options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perception of inferior taste and quality | -0.9% | Global, particularly acute in traditional beer markets (Europe, North America) | Medium term (2-4 years) |

| Regulatory barriers for new ingredients | -0.5% | North America (FDA), Europe (EFSA), Asia-Pacific (varied national bodies) | Long term (≥ 4 years) |

| Limited consumer awareness in emerging markets | -0.6% | South America, Middle East and Africa, rural Asia-Pacific | Medium term (2-4 years) |

| Higher production complexity | -0.4% | Global, with greater impact on smaller producers lacking scale | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Perception of inferior taste and quality

The perception of inferior taste and quality remains a significant restraint in the low-alcohol beverage market. Many consumers associate reduced alcohol content with diminished flavor, aroma, and overall drinking experience. Although technological advancements in dealcoholization and brewing processes have improved product quality, some traditional consumers still view low- and no-alcohol beverages as lacking the depth, body, and authenticity of full-strength options. This perception is particularly prevalent among experienced drinkers who prioritize complexity and are less inclined to switch unless the sensory profile closely resembles that of conventional products. Furthermore, earlier generations of low-alcohol beverages often failed to meet taste expectations, leaving a lasting bias that continues to shape consumer attitues.

Regulatory barriers for new ingredients

Regulatory barriers for new ingredients pose a significant challenge in the low-alcohol beverage market. As formulations increasingly include functional components such as botanicals, adaptogens, vitamins, and natural extracts, manufacturers must navigate extensive regulatory approvals, safety assessments, and compliance with diverse food and beverage standards across regions. These processes are often time-consuming and costly, delaying product launches and hindering the ability to quickly adapt to consumer trends. Additionally, the lack of global harmonization in regulatory frameworks adds complexity for companies operating in multiple markets. Authorities like the United States Food and Drug Administration and the European Food Safety Authority enforce stringent guidelines on ingredient usage, health claims, and permissible alcohol content, requiring careful compliance from manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RTD Cocktails Outpace Beer's Dominance

The beer segment accounted for 36.37% of the low-alcohol beverage market revenue in 2025 and continues to dominate due to its alignment with evolving consumer preferences and adaptability to innovation. Beer has historically been one of the most widely consumed alcoholic beverages globally, and its transition into low- and no-alcohol variants has been smoother compared to other categories. This is primarily due to brewing techniques like controlled fermentation, which allow manufacturers to retain familiar taste profiles. This sensory familiarity is crucial for consumer acceptance, enabling traditional beer drinkers to adopt low-alcohol options without compromising their experience.

RTD (ready-to-drink) cocktails are projected to grow at a robust CAGR of 6.56% through 2031, driven by their ability to offer convenience, consistency, and premium drinking experiences in a single format. This segment is gaining traction as consumers increasingly prefer hassle-free beverages that eliminate the need for mixing or bartending skills, making them suitable for home consumption, outdoor events, and social gatherings. The segment appeals particularly to younger consumers, who prioritize variety, portability, and visually appealing products. Additionally, social media and the growing cocktail culture further enhance its popularity. The inclusion of better-for-you attributes, such as low sugar, natural ingredients, and clean-label positioning, aligns RTD cocktails with broader health and wellness trends.

By Alcohol by Volume (ABV): Zero-Proof Formulations Dominat

The 0.0–0.5% ABV tier accounted for 68.17% of the market share in 2025 and is projected to grow at a CAGR of 6.42% through 2031, underscoring its role as the primary driver of the low-alcohol beverage market. This segment's dominance is primarily due to the increasing consumer preference for complete or near-complete alcohol avoidance while still enjoying the sensory and social aspects of traditional alcoholic beverages. Products in this range are commonly regarded as "alcohol-free," making them particularly attractive to health-conscious consumers, individuals with fitness-focused lifestyles, and those engaging in trends like mindful drinking and the sober-curious movement.

The 0.5–1.2% and 1.2–2.5% ABV tiers cater to niche consumer needs, targeting individuals who prefer a mild alcoholic experience while maintaining control over their intake and functionality. These segments are especially appealing to those who are not fully abstaining but seek a light buzz or a gradual drinking experience, making them suitable for extended social events, casual gatherings, and daytime consumption. Additionally, these tiers are gaining popularity among experimental consumers and craft beverage enthusiasts who appreciate nuanced flavor profiles and are willing to explore differentiated low-ABV options.

By Packaging Type: Cans Lead, Bottles Gain Premium Ground

Cans accounted for 67.23% of the packaging share in 2025, maintaining their position as the leading format in the low-alcohol beverage market. This dominance is primarily attributed to the functional and sustainability benefits of aluminum cans, which align with shifting consumer and regulatory preferences. According to the International Aluminium Institute, aluminum achieved a global recycling rate of 75% in 2025, making cans an appealing choice for environmentally conscious brands and consumers. Their lightweight design reduces transportation costs and carbon emissions, while their durability and faster chilling capabilities provide convenience for on-the-go consumption and outdoor events.

Bottles are expected to grow at a CAGR of 5.98% through 2031, underscoring their sustained importance in the low-alcohol beverage market despite the prevalence of cans. This growth is driven by their association with premiumization, product authenticity, and traditional drinking experiences, particularly in segments such as low-alcohol wines, craft beers, and specialty fermented beverages. Glass bottles, in particular, are viewed as high-quality packaging that enhances brand image and consumer trust, especially in formal dining, gifting, and upscale retail settings. Additionally, they offer excellent barrier properties, preserving flavor, carbonation, and aroma over extended shelf lives, which is essential for maintaining product quality.

By Distribution Channel: Foodservice Gains Despite Retail Dominance

Retail channels are projected to account for 70.04% of the distribution share in 2025, highlighting their significant role in enhancing accessibility and driving volume growth in the low-alcohol beverage market. This dominance is supported by the broad reach and convenience provided by supermarkets, hypermarkets, convenience stores, and e-commerce platforms. These channels collectively offer consumers easy access to a wide range of low-alcohol options. Retail environments facilitate effective product visibility through dedicated shelf placements, in-store promotions, and category segmentation, enabling consumers to compare brands, flavors, and ABV levels efficiently.

The foodservice segment is expected to grow at a CAGR of 6.12% through 2031, emphasizing the increasing importance of on-premise consumption in the low-alcohol beverage market. This growth is driven by the rising inclusion of low- and no-alcohol options in bars, restaurants, cafés, hotels, and lounges, where consumers are seeking diverse beverage menus that align with moderation and wellness trends. Foodservice outlets are incorporating low-alcohol beers, wines, and particularly RTD cocktails and mocktail-style offerings, allowing patrons to engage in social drinking occasions while limiting alcohol intake.

Geography Analysis

Europe accounted for 34.49% of global revenue in 2025, maintaining its leading position in the low-alcohol beverage market. This dominance is attributed to a well-established culture of moderation, strong regulatory support, and early adoption of alcohol-free innovations. The region has experienced widespread acceptance of low- and no-alcohol beers, wines, and ready-to-drink (RTD) beverages, particularly in countries such as Germany, the United Kingdom, and Spain, where consumers increasingly adopt mindful drinking habits. Major brewers and beverage companies have invested significantly in product innovation, premiumization, and branding, ensuring high product quality and variety. Additionally, supportive government initiatives promoting responsible alcohol consumption, coupled with strong retail penetration and a robust horeca culture, continue to reinforce Europe’s dominant market position.

The Asia-Pacific region is projected to grow at a CAGR of 6.69% through 2031, driven by rapid urbanization, evolving lifestyles, and changing social norms around alcohol consumption. Countries such as Japan, China, and South Korea are experiencing rising demand for low-alcohol beverages, particularly among younger urban consumers seeking balanced and healthier alternatives. Japan stands out as a key growth market, with beer production and imports increasing to meet shifting consumer preferences. For example, according to the Ministry of Finance Japan, beer import volumes reached 44.4 million liters in 2024, up from 42.75 million liters in 2023, reflecting strong momentum in the category [3]Source: Ministry of Finance Japan, "Import volume of beer to Japan", mof.go.jp. The expansion of convenience stores, premium retail outlets, and innovative product launches, especially in RTDs and flavored low-alcohol beverages, further supports the region's growth.

North America remains a competitive market, characterized by rapid innovation, a strong presence of craft producers, and increasing consumer interest in functional and better-for-you beverages. The United States and Canada are key contributors, with growing demand for low-alcohol craft beers, hard seltzers, and RTD cocktails driven by wellness trends and the sober-curious movement. Meanwhile, South America is gradually emerging as a market, supported by expanding urban populations and increasing exposure to global beverage trends, particularly in countries like Brazil and Argentina. In the Middle East & Africa, growth remains in its early stages but shows promise. Cultural preferences for low- or no-alcohol beverages, combined with a young demographic and rising tourism, are driving the introduction of innovative low-ABV and alcohol-free products across hospitality and retail channels.

Competitive Landscape

The low-alcohol beverage market is moderately fragmented, featuring a mix of global beverage leaders and an increasing number of regional and craft-focused producers. Prominent companies such as Heineken N.V., Anheuser-Busch InBev, Carlsberg Group, Asahi Group Holdings, Ltd., and Diageo plc maintain dominance through extensive global distribution networks, robust brand portfolios, and ongoing investments in product innovation. These companies utilize advanced brewing and dealcoholization technologies to create high-quality low- and no-alcohol variants that closely mimic the taste of traditional beverages. Their product offerings span categories such as beer, wine, and ready-to-drink (RTD) cocktails.

Simultaneously, emerging disruptors and craft producers are targeting underserved niches, intensifying competition within the market. Smaller players emphasize premiumization, distinctive flavor profiles, and functional ingredients, including botanicals and low-sugar formulations, to differentiate themselves from mass-market brands. These companies often leverage local consumer preferences, sustainability-focused branding, and direct-to-consumer channels to establish strong connections with younger, health-conscious audiences. The growing popularity of RTD cocktails and artisanal low-alcohol-by-volume (ABV) beverages has further reduced entry barriers, enabling innovative startups to gain visibility and compete effectively despite their smaller scale.

Competitive advantage in the low-alcohol beverage market increasingly depends on the ability to balance economies of scale with brand differentiation. Large corporations benefit from cost efficiencies, robust supply chains, and global reach but must continuously innovate and premiumize their offerings to sustain consumer interest. Conversely, niche players rely on agility, compelling brand narratives, and unique product offerings to capture market share. As competition intensifies, strategies such as partnerships, acquisitions, and portfolio diversification are becoming critical. Major players are actively investing in or acquiring smaller brands to strengthen their foothold in rapidly growing market segments.

Low Alcohol Beverage Industry Leaders

-

Heineken N.V.

-

Anheuser-Busch InBev

-

Carlsberg Group

-

The Asahi Group Holdings, Ltd.

-

Diageo plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Heineken 0.0 introduced its first zero-alcohol, zero-calorie, and zero-sugar brew. The Heineken 0.0 Ultimate offers soft fruity notes complemented by a delicate malty body, all without alcohol, calories, or sugar. It is double-brewed to eliminate alcohol.

- July 2025: Asahi Brewery Introduced Low-Alcohol Beer "Super Dry Dry Crystal". This new beer features an alcohol by volume (ABV) of 3.5%, compared to the 5% ABV of the classic Super Dry series, while maintaining a rich and refreshing flavor.

- January 2025: Lumo has introduced Big Nothing 0.5%, a locally-sourced, low-alcohol beer developed in collaboration with Newcastle’s Donzoko Brewing Company. This new offering will be available on services between Edinburgh and London.

Global Low Alcohol Beverage Market Report Scope

The low-alcohol beverage market encompasses the global industry involved in the production, distribution, and sale of beverages that contain reduced levels of alcohol compared to traditional alcoholic drinks. The low-alcohol beverage market is segmented by product type, alcohol by volume (ABV), packaging type, distribution channel, and geography. Based on product type, the market includes beer, wine, spirits, ready-to-drink (RTD) cocktails, and other low-alcohol beverages. Based on alcohol by volume (ABV), the market is segmented into 0.0 - 0.5%, 0.5 - 1.2%, 1.2 - 2.5%, and 2.5 - 3.5%. Based on packaging type, the market is segmented into cans and bottles. Based on distribution channel, the market is segmented into foodservice and retail, with retail further divided into supermarkets and hypermarkets, convenience stores, online retail, and other distribution channels.Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Beer |

| Wine |

| Spirits |

| RTD Cocktails |

| Others |

| 0.0 - 0.5% |

| 0.5 - 1.2% |

| 1.2 - 2.5% |

| 2.5 - 3.5% |

| Cans |

| Bottles |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Beer | |

| Wine | ||

| Spirits | ||

| RTD Cocktails | ||

| Others | ||

| By Alcohol by Volume (ABV) | 0.0 - 0.5% | |

| 0.5 - 1.2% | ||

| 1.2 - 2.5% | ||

| 2.5 - 3.5% | ||

| By Packaging Type | Cans | |

| Bottles | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the low-alcohol beverage market be by 2031?

The low-alcohol beverage market size is projected to reach USD 30.29 billion by 2031, expanding at a 5.96% CAGR from 2026 to 2031.

Which product type is growing fastest in low-alcohol drinks?

Ready-to-drink cocktails are forecast to record the highest 6.56% CAGR through 2031, outpacing beer’s current volume leadership.

What alcohol band holds the majority share today?

Zero-proof (0.0-0.5% ABV) beverages command 68.17% of 2025 sales and will keep growing at 6.42% CAGR, reinforcing regulatory alignment and consumer trust.

Which region delivers the strongest near-term growth?

Asia-Pacific leads with a 6.69% forecast CAGR, powered by Japan’s production scale-up and urban demand across Southeast Asia.

Page last updated on: