Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

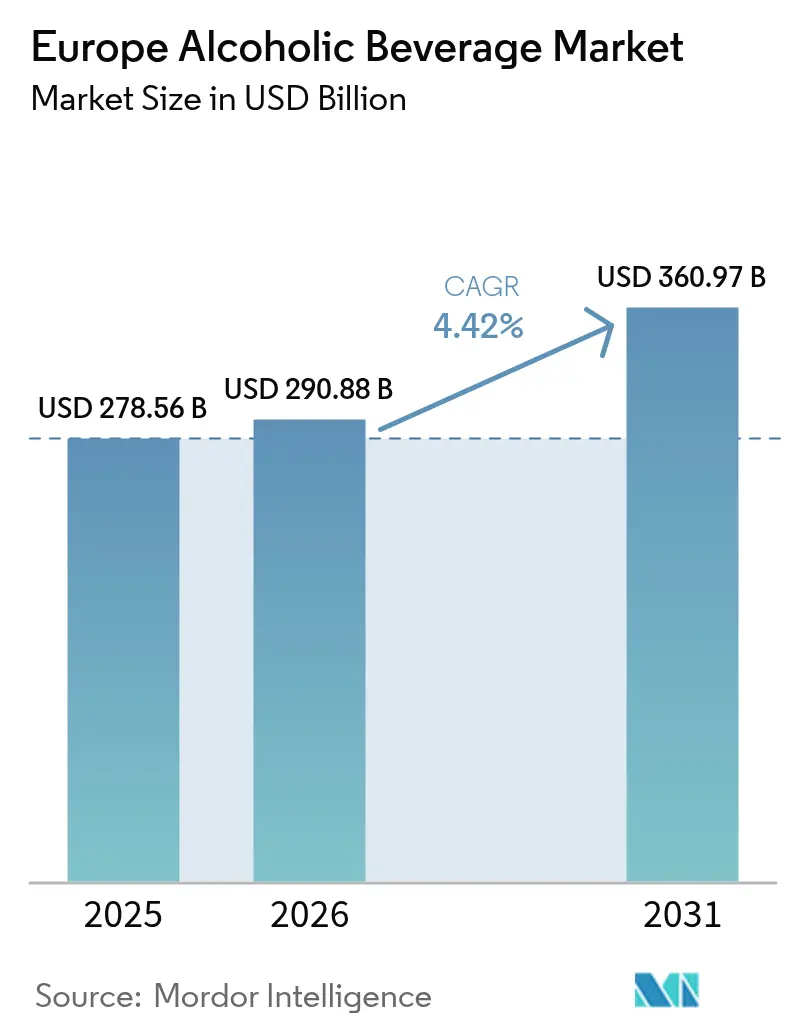

| Base Year Market Size (2025) | USD 278.56 Billion |

| Market Size (2026) | USD 290.88 Billion |

| Market Size (2031) | USD 360.97 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Alcoholic Beverage Market Analysis by Mordor Intelligence

Europe alcohol beverage market size in 2026 is estimated at USD 290.88 billion, growing from 2025 value of USD 278.56 billion with 2031 projections showing USD 360.97 billion, growing at 4.42% CAGR over 2026-2031. This growth in value is largely attributed to the recovery of tourism, the shift toward premium products, and the rapid adoption of e-commerce. However, volume growth remains limited in mature categories like mainstream beer. Consumers are increasingly favoring premium spirits, low-alcohol beers, and ready-to-drink (RTD) cocktails, driven by a preference for quality, authenticity, and convenience. A rising female consumer base, the normalization of at-home drinking occasions, and increased digital engagement are transforming distribution and marketing strategies. Additionally, digital platforms and influencer marketing are playing a significant role in influencing product discovery and consumer preferences. On the regulatory side, there is growing momentum toward sustainability, particularly in reducing packaging waste and implementing health labeling. This shift is directing investments toward low-carbon packaging solutions and innovations in non-alcoholic products.

Key Report Takeaways

- By product type, beer led with 45.32% of Europe alcohol beverage market share in 2025; spirits are projected to expand at a 5.12% CAGR through 2031.

- By end user, male consumers held 62.10% of the Europe alcohol beverage market size in 2025, while female consumers are advancing at a 5.88% CAGR to 2031.

- By packaging type, bottles dominated with 71.10% revenue share in 2025; cans represent the fastest-growing format at a 5.05% CAGR between 2026-2031.

- By distribution channel, off-trade captured 62.74% of the Europe alcohol beverage market size in 2025 and is growing at a 4.66% CAGR to 2031.

- By geography, Germany remained the largest contributor with 21.38% market share in 2025; Poland is set to rise at a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Alcoholic Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for premium alcoholic beverages | +1.2% | Global, strongest in Germany, France, United Kingdom | Medium term (2-4 years) |

| Low/no-alcohol product uptake | +0.8% | United Kingdom, Germany, Nordic countries | Long term (≥ 4 years) |

| Growth in craft and small-batch production | +0.6% | Germany, Belgium, Netherlands, United Kingdom | Medium term (2-4 years) |

| Growing tourism and hospitality impact positive growth | +0.9% | Spain, Italy, France, Greece | Short term (≤ 2 years) |

| Growth of online alcohol sales | +0.5% | Led by United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| Digital and social media influence | +0.4% | Strongest impact in Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for premium alcoholic beverages

In key European markets, demographic changes and increasing disposable incomes are driving premium alcohol consumption patterns, emphasizing quality over quantity. The premiumization trend has accelerated post-pandemic, with consumers showing a greater willingness to spend on artisanal and heritage brands. As European consumers develop more refined tastes, they are seeking unique, high-quality beverages characterized by authentic flavors and craftsmanship. This shift towards premiumization not only highlights evolving consumer preferences but also significantly contributes to market expansion, with a preference for artisanal, small-batch, and craft products over mass-produced alternatives. Although LVMH's Wines and Spirits segment experienced a 4% organic decline in 2023, champagne sales, particularly in Europe and Japan, demonstrated growth, reflecting selective premium consumption. This shift towards premium products is especially notable in the spirits category, where consumers are attracted to authentic experiences and craftsmanship narratives that justify higher price points.

Low/no-alcohol product uptake

European consumption patterns are experiencing a notable transformation, with the low and no-alcohol segment leading the change. This evolution is primarily driven by increasing health awareness and shifting generational preferences. Across all demographics, there is a clear cultural movement toward moderating alcohol consumption, which has significantly boosted the demand for low and no-alcohol options. Younger consumers are at the forefront of this trend, often motivated by goals to reduce calorie intake or avoid intoxication. In 2024, alcohol consumption is associated with one in every 11 deaths in the WHO European Region[1]World Health Organization, "General facts about alcohol", who.int. Addressing these concerns, the EU has introduced a new classification system for no and low-alcohol wines. This system defines terms such as 'alcohol-free' (≤0.5% ABV) and '0.0%' (≤0.05% ABV), providing regulatory clarity and fostering market growth. Leading beverage companies like Anheuser-Busch InBev, Heineken, Carlsberg, and Diageo are actively driving innovation and expanding their low and no-alcohol product portfolios, thereby enhancing consumer trust and increasing product availability.

Growth in craft and small-batch production

Craft production is steadily increasing its market share across Europe, driven by rising consumer demand for authenticity and locally sourced products. The craft movement benefits from supportive regulatory frameworks in several EU member states, which include reduced excise duties and simplified licensing processes for small producers. Germany exemplifies this trend, with 1,459 breweries operating in 2024[2]German Federal Statistical Office, "Number of the Week No. 17 of April 22, 2025", destatis.de, despite ongoing market consolidation. Craft producers effectively utilize digital marketing and direct-to-consumer channels to strengthen brand loyalty and justify premium pricing. Microbreweries, independent distillers, and small producers energize the market with innovative brewing and distillation methods, unique flavors, and health-conscious offerings (such as organic and low-alcohol options). These strategies help brands differentiate themselves and attract trend-focused consumers. Additionally, the segment's growth is bolstered by the recovery of tourism, as craft breweries and distilleries increasingly serve as destination attractions for both local and international visitors.

Growing tourism and hospitality impact positive growth

European tourism has surpassed pre-pandemic levels, fueling significant demand for alcoholic beverages in on-trade channels. According to the European Travel Commission, foreign tourist arrivals and overnight stays in early 2024 exceeded 2019 figures by 7.2% and 6.5%, respectively[3]European Travel Commission, "European Tourism Recovery Continues Into 2024", etc-corporate.org. Additionally, consumer travel spending reached EUR 742.8 billion, reflecting a 14.3% rise from 2023. This recovery has notably boosted premium alcohol categories, as tourists often spend more on high-quality beverages during their trips. Tourism promotes the exploration and sampling of local wines, craft beers, and artisanal spirits. Visitors, driven by the desire to experience native products, support local producers, and enhance brand identities on a global scale. Major sporting events, such as the UEFA Champions League, have further driven consumption. The revival of the hospitality sector has created ripple effects across the alcohol supply chain, benefiting stakeholders from importers to local distributors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent excise taxes and regulation | -0.7% | Particularly United Kingdom, Nordic countries | Short term (≤ 2 years) |

| Rising health consciousness | -0.5% | Strongest in Northern Europe | Long term (≥ 4 years) |

| High competition from non-alcoholic alternatives | -0.4% | United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| CO₂ supply shortages for brewing | -0.3% | Episodic regional impacts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent excise taxes and regulation

Excise taxation policies in Europe are exerting significant pressure, restricting volume growth and limiting market accessibility. In February 2025, the UK introduced a major reform to its alcohol duty system, transitioning to a per-liter-of-alcohol model. This change resulted in a slight 0.5% increase in duty receipts, totaling GBP 12.646 billion for the 2024-2025 fiscal year. The complexity of the new system has imposed additional administrative challenges on producers and distributors, while the expected rise in public revenue has not materialized. According to WHO data, only 28 out of 53 European member states currently impose excise taxes on wine, indicating room for potential tax expansions that could further restrict market growth. Furthermore, the European Commission reports that, as of January 2024, key European markets are facing increased pricing pressures due to VAT rate adjustments. Luxembourg raised its VAT from 16% to 17%, the Czech Republic consolidated its rate to 12%, and Estonia increased its VAT from 20% to 22%[4]European Commission, "Changes in VAT rates in certain EU Member States", trade.ec.europa.eu.

Rising health consciousness

Health awareness campaigns and advancements in medical research have established a strong link between alcohol consumption and various health conditions, prompting significant behavioral changes, especially among younger demographics. According to the World Health Organization (WHO), European adults consume an average of 9.2 liters of pure alcohol per year, positioning them as the highest consumers globally. Furthermore, the WHO attributes approximately 800,000 deaths annually to alcohol consumption[5]World Health Organization, "General facts about alcohol", who.int. These statistics underscore the importance of public health initiatives aimed at encouraging moderation or complete abstinence from alcohol. The 'Sober Curious' movement, which advocates for a more mindful approach to drinking, is gaining momentum among Gen Z and Millennials. Notably, 52% of individuals who consume low and no-alcohol beverages express concerns about alcohol's negative impact on sleep quality. These evolving demographic preferences are creating sustained challenges for traditional alcohol categories while simultaneously driving the growth of low and no-alcohol alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirits Drive Premium Growth

Beer maintains its dominant position with 45.32% market share in 2025, reflecting its cultural significance and accessibility across European markets. This enduring popularity is attributed to its affordability and the strong tradition of beer consumption in the region. Within the beer category, the low-alcohol beer segment demonstrates remarkable growth potential. Alcohol-free beer, in particular, is projected to become the second-largest beer category globally, driven by increasing health consciousness and changing consumer lifestyles. In contrast, the wine market faces significant challenges due to climate change, which has adversely impacted European wine production in 2024. Additionally, wine consumption has also declined, reflecting shifting consumer preferences and external pressures.

On the other hand, spirits emerge as the fastest-growing segment, achieving a robust 5.12% CAGR through 2031. This growth is primarily driven by the increasing demand for premium products and the expanding cocktail culture, which appeals to younger demographics and urban consumers. The spirits category also benefits from the recovery of tourism and the revitalization of on-trade channels, as consumers show a growing willingness to pay premium prices for authentic and high-quality experiences. Spirits are also capitalizing on innovation in the ready-to-drink (RTD) segment. Meanwhile, wine producers are adapting to new EU labeling regulations that took effect in December 2023. These regulations mandate the inclusion of detailed nutritional information and ingredient lists on wine labels. While this compliance requirement increases operational costs for producers, it enhances transparency and fosters greater trust among consumers.

By End User: Female Segment Accelerates

Male consumers represent 62.10% market share in 2025, maintaining their traditional dominance in alcohol consumption patterns.The World Health Organization states that men in the region consumed nearly four times more alcohol than women in 2024, with men averaging 14.9 liters annually compared to women's 4.0 liters. However, female consumers are experiencing significant growth, with a 5.88% CAGR projected through 2031. This growth reflects evolving social norms and targeted marketing efforts. This trend is particularly evident in the premium spirits and wine categories, where brands are creating products and experiences tailored to female preferences. The rise in female consumption aligns with broader lifestyle trends that emphasize social experiences and a focus on quality over quantity.

Generational trends indicate distinct preferences within both segments. Gen Z and Millennial consumers are driving demand for low-alcohol alternatives and authentic brand experiences. Diageo's research identifies a 'zebra striping' trend, where consumers alternate between alcoholic and non-alcoholic beverages during the same occasion, reflecting changing consumption behaviors across genders. Marketing strategies are increasingly adopting inclusive messaging and experience-driven positioning, moving away from traditional gender-specific approaches.

By Packaging Type: Sustainability Drives Innovation

In 2025, bottles hold a 71.10% market share, highlighting consumer preferences for premium presentation and product protection. Glass bottles, the traditional choice, continue to be the preferred packaging for wine, spirits, and premium beer due to their ability to preserve quality, flavor, and elegance. Cans are the fastest-growing packaging format, with a 5.05% CAGR projected through 2031. Their growth is driven by sustainability, convenience, and advancements in barrier technologies that maintain product quality. The EU's Packaging and Packaging Waste Regulation (PPWR) is driving changes in the packaging industry, requiring 80% recyclability and a 15% reduction in packaging volume by 2040.

Innovation in sustainable packaging is gaining momentum, with Diageo testing 90% paper-based bottles for its Johnnie Walker Black Label, while Absolut collaborates with Blue Ocean Closures to develop caps made from over 95% FSC-certified fibers. Nordic alcohol monopolies have initiated a program to reduce carbon emissions by 50% by 2030, focusing on minimizing the use of heavy glass bottles and increasing the adoption of low-carbon footprint packaging. Tetra Pack and Bag-in-Box formats are becoming more popular, particularly in the wine segment, where functionality and environmental considerations are outweighing traditional packaging aesthetics.

By Distribution Channel: Off-Trade Dominance Persists

In 2025, Off-Trade channels hold a 62.74% market share and represent the fastest-growing segment, with a projected 4.66% CAGR through 2031. This growth reflects enduring shifts in consumer behavior from the pandemic era and the expansion of e-commerce. The prominence of Off-Trade channels highlights a significant change: consumers are increasingly purchasing alcohol for home consumption rather than for on-premise occasions. Growth drivers include a wider product range, competitive pricing, and the convenience that appeals to time-pressed consumers.

Although the tourism sector is improving, the On-Trade segment is recovering at a slower pace. Consumers remain cautious with their spending and prefer controlled consumption settings. At the same time, Off-Trade channels are accelerating digital integration. Retailers are heavily investing in online platforms and delivery services to expand their market reach. In the Nordic markets, regulatory changes in Sweden and Finland now allow direct-to-consumer sales from producers, marking a significant shift that could transform distribution dynamics. Overall, the evolution of these channels aligns with broader retail trends, emphasizing convenience, product variety, and digital integration.

Geography Analysis

Germany maintains its position as Europe's largest alcohol market with a 21.38% share in 2025, driven by its rich beer culture and a robust tourism industry. German beer production reached 7.2 billion liters in 2024, the highest in the EU, although domestic sales declined by 1.4% to approximately 8.3 billion liters. This decrease reflects ongoing trends of moderated consumption, according to the Statistisches Bundesamt. The market's resilience is evident in its export performance, with beer exports increasing by 1.6% despite production challenges. Additionally, premium spirits consumption is on the rise, supported by the recovery in tourism and urban consumers' growing demand for authentic experiences.

Poland is emerging as the fastest-growing European market, with a 4.86% CAGR projected through 2031. This growth is fueled by economic progress, higher disposable incomes, and changing consumption patterns. The market benefits from EU integration and increased tourism, which drive both domestic consumption and export opportunities. As the EU's third-largest beer producer, following Germany and Spain, Poland has a strong foundation for market expansion, according to Eurostat. Pernod Ricard's strong performance in Poland during FY24 highlights the market's appeal to international spirits brands. Moreover, the regulatory framework, supported by EU harmonization and reduced trade barriers, facilitates market growth.

France remains a key market for premium wines and spirits, despite facing production challenges due to climate-related issues. Even with these obstacles, France continues to lead the EU in alcoholic beverage exports, generating EUR 12.1 billion, representing 41% of the EU's total exports, mainly from wine categories, as reported by Eurostat. The market demonstrates resilience by employing premiumization strategies and leveraging brand heritage to achieve premium pricing, even amid volume pressures. Diageo's decision to reclaim distribution rights from the Moët Hennessy joint venture, effective January 2025, reflects a strategic shift by global players to capitalize on market opportunities. Southern European countries such as Spain, Italy, and Greece benefit from tourism-driven hospitality, seasonal cocktails, and venue-based experiential drinking. Meanwhile, Nordic countries in Northern Europe are leading the way in low-alcohol regulations and eco-friendly packaging, setting trends that influence the broader European market.

Competitive Landscape

The European alcohol beverage market is moderately fragmented, with established multinational companies maintaining dominant positions while contending with the rise of craft producers and evolving consumer preferences. Market concentration differs significantly by category; the beer segment is more consolidated, led by major players such as Anheuser-Busch InBev, Heineken, and Carlsberg, whereas the spirits and wine segments remain fragmented, offering opportunities for regional and craft producers. The Belgian Competition Authority's investigation into AB InBev for alleged anti-competitive practices, particularly regarding conditions imposed on wholesalers and hospitality operators, underscores regulatory scrutiny of dominant market positions.

Premiumization, sustainability initiatives, and digital transformation are key competitive strategies. Companies are adopting asset-light operating models, as seen with Diageo selling its shareholdings in Guinness operations across West Africa while retaining brand ownership and licensing agreements. Product launches, mergers and acquisitions, partnerships, and expansions are the most common strategies employed by companies to strengthen their market positions. Despite the large number of players in the market studied, major market shares are held by key players, including Diageo Plc, Bacardi Limited, Heineken Holding NV, Pernod Ricard, and Anheuser-Busch InBev. The premiumization of the industry remains a significant driver of the alcoholic beverage market, particularly in the spirits and wine segments.

Opportunities exist in low-alcohol segments, sustainable packaging innovations, and direct-to-consumer channels, supported by regulatory relaxation in Nordic markets. Technology adoption is focused on optimizing supply chains, enhancing consumer engagement through digital platforms, and implementing sustainability tracking systems to meet evolving regulatory requirements and consumer expectations. Compliance with the EU Packaging and Packaging Waste Regulation (PPWR) presents both challenges and opportunities for companies investing in sustainable packaging technologies and circular economy initiatives.

Europe Alcoholic Beverage Industry Leaders

-

Pernod Ricard

-

Diageo Plc

-

Bacardi Limited

-

Anheuser-Busch InBev

-

Heineken Holding NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: HEINEKEN has opened a global research and development centre in the Netherlands to drive brewing innovations and advance next-generation product development. The EUR 45 million investment highlights HEINEKEN's role as a pioneer in the beer industry and its commitment to maintaining leadership in the Dutch food technology sector.

- June 2025: Brewdog introduced an exclusive beer for the England v India test match at Lord’s. The new beer is crafted with Luminosa and Galaxy hops. This beer is light, refreshing, and tropical, featuring flavors of peach-mango lemonade, candied orange peel, papaya, and guava. It's a brew that's sure to impress.

- May 2025: BrewDog, the Scottish craft brewery, has revamped the branding of its core beer lineup. This update touches on well-loved variants like Punk IPA, Hazy Jane, Lost Lager, and Elvis Juice. Though the signature BrewDog brandmark and its color palette stay consistent, each beer now boasts a unique aesthetic, boosting its shelf presence and recognizability.

- January 2025: Diageo has restructured its distribution model in France by reclaiming distribution rights for key brands, including Johnnie Walker, J and B, and Gordon's, from its joint venture with Moët Hennessy. This move establishes Diageo France as an independent in-market company.

Europe Alcoholic Beverage Market Report Scope

An alcoholic beverage is a drink containing ethanol, commonly known as alcohol. Alcoholic beverages are typically divided into three general classes: beers, wines, and spirits.

The European alcoholic beverage market is segmented by product type, distribution channel, and country. Based on product type, the market is segmented into beer, wine, and spirits. Based on the distribution channel, the market is segmented into on-trade and off-trade. The off-trade segment is further segmented into supermarkets/hypermarkets, specialist stores, online retail stores, and other off-trade channels. Based country, the market is segmented into the United Kingdom, Germany, France, Italy, Spain, Russia, and the Rest of Europe.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Beer | Ale Beer |

| Lager | |

| Low-Alcohol Beer | |

| Other Beer Types | |

| Wine | Fortified Wine |

| Still Wine | |

| Sparkling Wine | |

| Others Wine Types | |

| Spirits | Brandy and Cognac |

| Liquer | |

| Tequilla and Mezcel | |

| Rum | |

| Whisky | |

| Other Spirit Types | |

| Others |

By End User

| Male |

| Female |

By Packaging Type

| Bottles |

| Cans |

| Others (Tetra Pack) |

By Distribution Channel

| On-Trade |

| Off-Trade |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| By Product Type | Beer | Ale Beer |

| Lager | ||

| Low-Alcohol Beer | ||

| Other Beer Types | ||

| Wine | Fortified Wine | |

| Still Wine | ||

| Sparkling Wine | ||

| Others Wine Types | ||

| Spirits | Brandy and Cognac | |

| Liquer | ||

| Tequilla and Mezcel | ||

| Rum | ||

| Whisky | ||

| Other Spirit Types | ||

| Others | ||

| By End User | Male | |

| Female | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Others (Tetra Pack) | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe alcohol beverage market in 2026?

The Europe alcohol beverage market size reached USD 290.88 billion in 2026 and is projected to grow to USD 360.97 billion by 2031.

Which product segment is expanding fastest?

Spirits show the highest momentum, advancing at a 5.12% CAGR on the back of premiumization and cocktail culture.

Why are low- and no-alcohol drinks gaining traction?

Health awareness, new EU labeling rules, and innovative flavors are pushing alcohol-free beer and spirits toward double-digit growth.

Which country offers the strongest growth prospects?

Poland leads with a forecast 4.86% CAGR through 2031 thanks to rising incomes and supportive EU integration effects.

Page last updated on: