Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

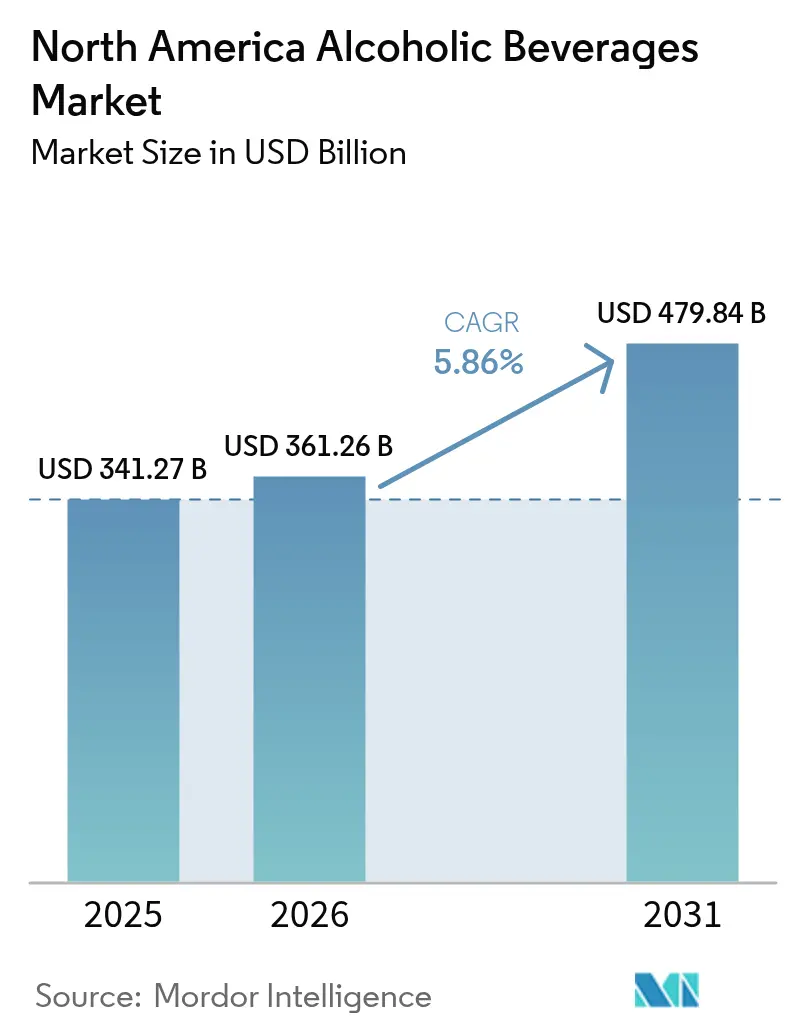

| Base Year Market Size (2025) | USD 341.27 Billion |

| Market Size (2026) | USD 361.26 Billion |

| Market Size (2031) | USD 479.84 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

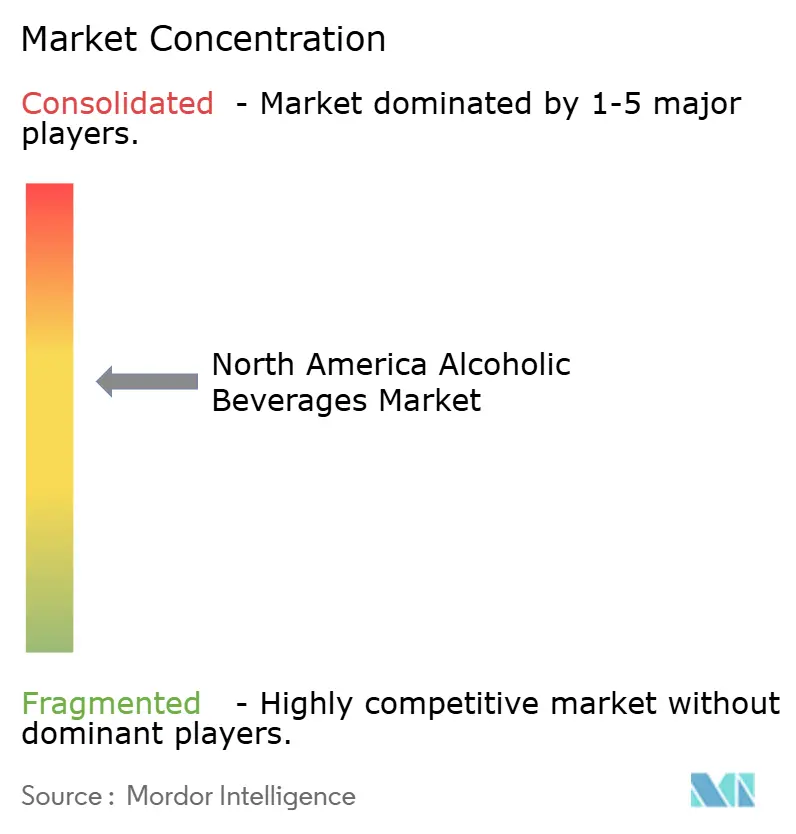

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Alcoholic Beverages Market Analysis by Mordor Intelligence

The North America Alcoholic Beverages Market size was valued at USD 341.27 billion in 2025 and estimated to grow from USD 361.26 billion in 2026 to reach USD 479.84 billion by 2031, at a CAGR of 5.86% during the forecast period (2026-2031). The market's growth stems from established alcohol consumption patterns across the region. Beer dominates the market share, with a robust craft brewing industry and sustained demand for traditional lager and light beer products. The spirits category shows significant growth, particularly in premium whiskey, tequila, and vodka segments. The wine segment maintains steady growth through increased consumption of sparkling wines, rosé, and organic varieties, especially among health-conscious consumers and younger age groups. Consumer preferences are evolving toward premium, craft-produced, and lower alcohol content options, reflecting increased interest in moderate consumption and health-conscious choices. The expansion of e-commerce and direct-to-consumer channels has improved product accessibility, supporting traditional retail and on-premise consumption. The market has experienced substantial growth in ready-to-drink cocktails, flavored beverages, and hard seltzers, particularly appealing to younger consumers and women.

Key Report Takeaways

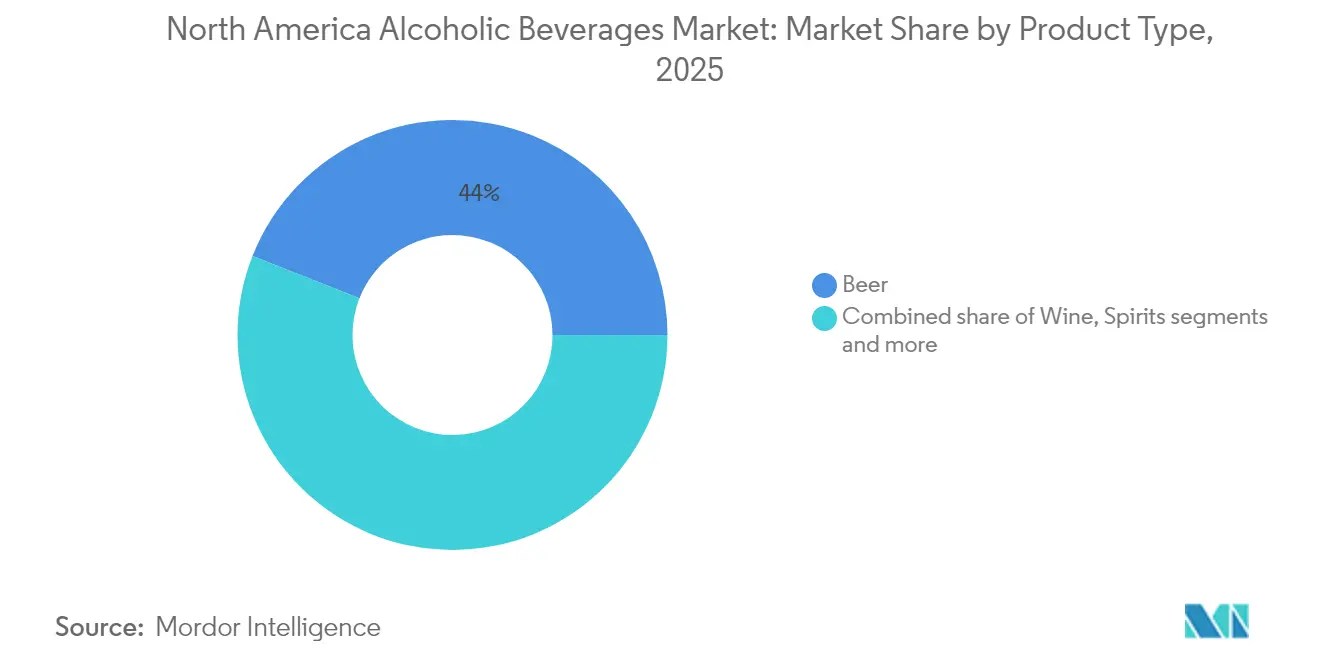

- By product category, beer led with 44.02% revenue share in 2025, while ready-to-drink/hard-seltzers are projected to expand at an 8.37% CAGR through 2031.

- By end user, male consumers accounted for a 66.10% share of the North American alcoholic beverages market in 2025, whereas female consumption is rising at an 7.92% CAGR to 2031.

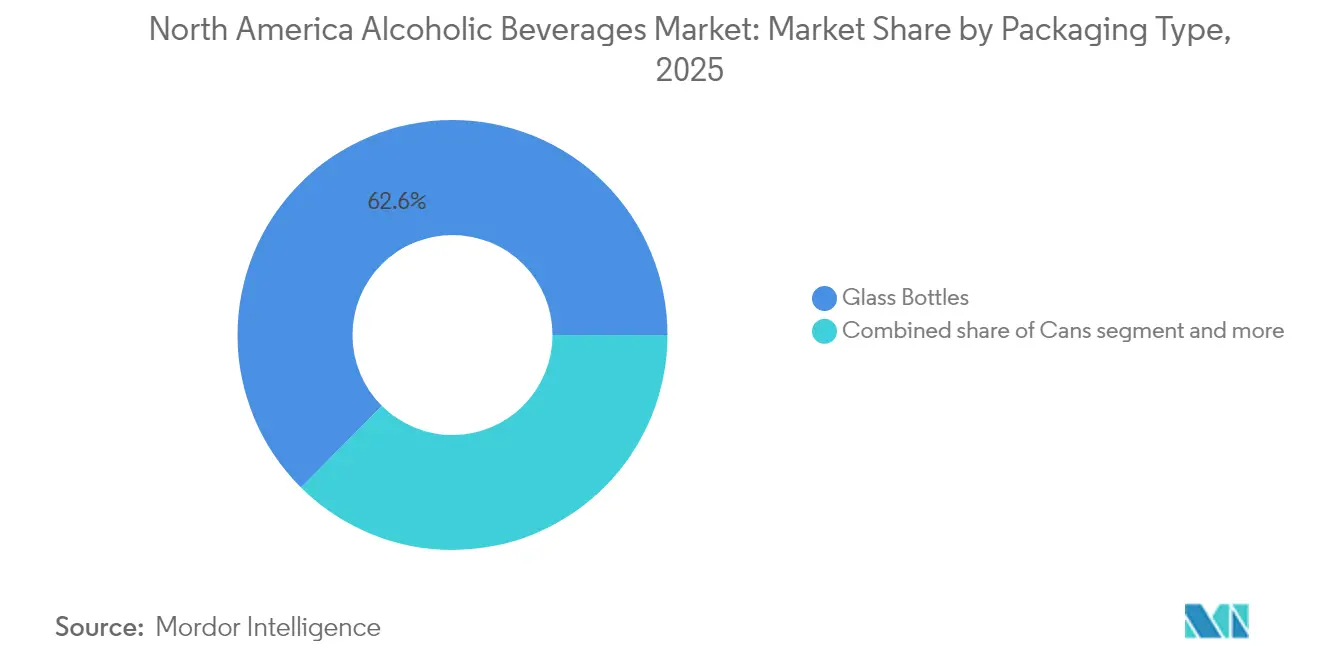

- By packaging type, glass bottles dominated with 62.55% share in 2025; cans represent the fastest-growing format at a 6.95% CAGR over the forecast horizon.

- By distribution channel, off-trade controlled 69.60% of 2025 sales, yet the on-trade channel is rebounding at a 6.05% CAGR as experiential consumption returns to prominence.

- By geography, the United States commanded a 75.80% share in 2025, while Mexico is forecast to post the region’s quickest advance at a 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Alcoholic Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and craft innovation | +1.2% | United States and Canada, spillover to Mexico | Medium term (2-4 years) |

| Flavored and functional alcoholic beverages | +1.1% | North America, strongest in the United Statesurban markets | Short term (≤ 2 years) |

| Convenient ready-to-drink (RTD) offerings | +0.9% | United States and Canada, emerging in Mexico | Short term (≤ 2 years) |

| Cultural integration and diversity of alcohol preferences | +0.8% | United States, Canada metropolitan areas | Medium term (2-4 years) |

| Rise of sustainable and ethical consumption | +0.7% | Canada and the United States West Coast, expanding nationally | Long term (≥ 4 years) |

| Celebrity and influencer endorsements | +0.6% | United States, Canada urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization and Craft Innovation

The North America Alcoholic Beverages Market demonstrates significant growth through premiumization and craft innovation, driven by consumer demand for superior-quality and distinctive beverage experiences. Premium and craft offerings address market requirements through the incorporation of refined ingredients, distinguished flavor profiles, and traditional production methodologies. The beer segment exemplifies this market evolution, with craft breweries expanding their operational presence and developing diversified, region-specific products. According to the Brewers Association, the United States recorded 9,796 operational craft breweries in 2024, consisting of 2,029 microbreweries, 3,552 brewpubs, and 3,936 taproom breweries [1]Source: Brewers Association, "Brewers Association Reports 2024 U.S. Craft Brewing Industry Figures", brewersassociation.org. The emphasis on craft production facilitates premium pricing strategies and enhances consumer loyalty while fostering product diversification across beer, wine, and spirits segments. This market development encompasses sophisticated packaging design and strategic brand communication, which substantially influence consumer value perception and price acceptance.

Flavored and Functional Alcoholic Beverages

The North American market shows increasing demand for flavored and functional alcoholic beverages. Consumer preferences are shifting toward unique taste experiences and beverages with additional health-oriented benefits beyond alcohol content. These products particularly attract younger consumers and experimental drinkers seeking diverse flavor options and personalized choices. The integration of functional ingredients, including vitamins, antioxidants, and adaptogens, aligns with current wellness trends, appealing to consumers who want to balance enjoyment with health-conscious choices. This market evolution combines innovative flavors with functional elements, driving both initial purchases and consumer loyalty. For instance, Jack Daniel's introduction of Blackberry Flavored Whiskey in August 2025 reflects how established brands adapt their product lines to meet current consumer preferences and maintain market relevance.

Convenient Ready-to-Drink (RTD) Offerings

Convenient Ready-to-Drink (RTD) offerings are rapidly expanding within the North American Alcoholic Beverages Market. driven by consumers’ growing preference for on-the-go, easy-to-consume alcoholic options that do not compromise on quality or flavor. The millennial and Generation Z demographic segments prioritize accessible options that maintain premium characteristics and quality standards for social functions, outdoor recreational activities, and routine consumption. The market exhibits comprehensive flavor development initiatives, with manufacturers implementing diverse taste profiles to address both experimental and health-conscious consumer segments. Ready-to-Drink (RTD) products incorporate reduced-calorie and lower-alcohol formulations, aligning with emerging consumer preferences for moderate consumption and wellness objectives. For instance, in March 2025, Smirnoff Vodka initiated operations in the Canadian RTD market through the introduction of cocktail variants, including Raspberry Mule, Cosmo Bellini, and Passion Fruit Martini, incorporating premium-grade ingredients.

Cultural Integration and Diversity of Alcohol Preferences

The North American Alcoholic Beverages Market demonstrates significant influence from cultural integration and diverse beverage preferences. The region's multicultural demographic composition generates substantial demand across various alcoholic beverage categories, encompassing traditional beers, spirits, and ethnic and craft products. This diversification facilitates consumer exploration of distinct flavors and styles within multiple alcohol segments, establishing these beverages as fundamental components of social and cultural gatherings. For instance, the National Institute on Alcohol Abuse and Alcoholism indicates that in 2024, approximately 228.4 million individuals aged 12 and older in the United States reported alcohol consumption at least once in their lifetime, substantiating alcohol's considerable presence in American culture [2]Source: National Institute on Alcohol Abuse and Alcoholism, "Alcohol Use in the United States", niaaa.nih.gov. The market exhibits continuous expansion through product development initiatives and specialized offerings that address both established preferences and emerging consumer requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Stringent regulatory environment | -0.8% | North America, strongest in Canada | Long term (≥ 4 years) | |

| High taxation and excise duties | -0.5% | United States and Canada, provincial variations | Medium term (2-4 years) | |

| Public health campaigns and anti-alcohol sentiment | -0.4% | North America, focus on urban markets | Medium term (2-4 years) | |

| Minimum legal drinking age enforcement | -0.3% | United States and Canada | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Stringent Regulatory Environment

The stringent regulatory environment in the North America Alcoholic Beverages Market presents a major restraint, characterized by complex and multifaceted regulatory frameworks across federal, state, and provincial jurisdictions. These regulations create substantial compliance costs, particularly affecting smaller craft producers and innovative brands with limited resources to manage licensing, labeling, and distribution requirements. The United States Alcohol and Tobacco Tax and Trade Bureau (TTB) approval process for product formulation, labeling, and advertising standards often results in extended time-to-market periods, particularly for new product categories like flavored spirits, low-alcohol beverages, and ready-to-drink (RTD) products. The varying state-level regulations create additional distribution and market expansion challenges, especially for smaller producers seeking to grow their operations. These regulatory requirements create market entry barriers and operational challenges that impact innovation and competition in the North American alcoholic beverage market.

High Taxation and Excise Duties

The implementation of substantial taxation and excise duties presents a significant impediment to the North American alcoholic beverages market through increased product costs and diminished consumer purchasing capacity. Government-mandated excise taxes, implemented to regulate consumption patterns and enhance revenue streams, subsequently manifest in elevated retail price points. These fiscal obligations impact operational margins throughout the industry, with particularly adverse effects on small-scale producers and craft manufacturers who encounter substantial challenges in managing incremental costs. The heterogeneous tax structure across states and provinces introduces operational complexities in pricing mechanisms and distribution networks. Furthermore, elevated taxation levels potentially contribute to the proliferation of unauthorized trade and counterfeit products, compromising market integrity and safety protocols. These tax-related impediments subsequently influence market volume expansion, new product introduction capabilities, and industry innovation potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RTD Innovation Disrupts Traditional Categories

Beer holds a commanding 44.02% market share in 2025, driven by multiple factors rooted in consumer preference shifts, market innovation, and demographic trends. According to the Beverage Information Group, beer consumption in the United States reached approximately 2.65 billion 2.25-gallon cases in 2023, demonstrating its dominant presence in the regional alcoholic beverage market. Beer remains deeply embedded in social and cultural occasions such as sports events, barbecues, and festivals, making it a preferred choice for casual and group consumption. The ongoing consumer demand for craft and specialty beers, which offer unique flavors, local authenticity, and artisanal quality, continues to drive growth. This trend has led to the expansion of microbreweries and craft beer festivals across the region, meeting consumer demands for personalized and experiential drinking occasions.

RTD (Ready-to-Drink) and Hard Seltzers are projected to grow at a CAGR of approximately 8.37% through 2031 in the North American alcoholic beverage market. This growth stems from a shift in consumer preferences toward healthier, lighter alcoholic beverages. Health-conscious consumers seeking to reduce calorie and sugar intake while enjoying alcoholic drinks gravitate toward the low-calorie, gluten-free, and low-alcohol characteristics of hard seltzers. Younger demographics favor these beverages for their refreshing taste, convenience, and perceived wellness benefits, aligning with balanced lifestyle trends. Manufacturers continue to drive market expansion through flavor innovation, introducing diverse options from tropical fruits to botanical infusions, which cater to various taste preferences and encourage both initial and repeat purchases.

By End User: Female Consumption Accelerates Market Evolution

Male consumers constitute 66.10% of the North American alcoholic beverage market in 2025, primarily attributed to established sociocultural consumption patterns. The market composition demonstrates a significant concentration in beer and brown spirits, where male consumers maintain a substantial market presence. Male consumption behavior exhibits dual characteristics: volume-driven purchasing and premium product acquisition, particularly in traditional beer categories such as lager and ale during social gatherings, sporting events, and recreational occasions. This demographic segment additionally influences the expansion of the premium and craft spirits segments.

The female segment within the North American alcoholic beverage market demonstrates projected growth at a CAGR of 7.92% through 2031. This expansion is attributed to the evolution of societal paradigms and the increased normalization of alcohol consumption among female consumers. Strategic product development and marketing initiatives targeting the female demographic emphasize flavored beverages, reduced-calorie alternatives, and ready-to-drink (RTD) formulations. Female consumer preferences predominantly align with wellness-oriented consumption patterns, subsequently influencing product innovation, particularly in the organic and natural ingredient-based alcoholic beverage categories. The increased participation of women in professional and social environments where alcohol consumption occurs further substantiates this market segment's expansion trajectory.

By Packaging Type: Sustainability Drives Can Innovation

Glass bottles constitute 62.55% of the North American alcoholic beverage market share in 2025, demonstrating significant market dominance. This market position is attributed to glass's established reputation in premium product segments, specifically within wine, spirits, and craft beer categories. The material's inherent properties facilitate optimal preservation of flavor profiles, aromatic compounds, and carbonation levels, ensuring product integrity and meeting consumer quality expectations. Glass's recyclable composition and environmental sustainability characteristics correspond to increasing consumer environmental consciousness. The medium enables manufacturers to implement distinctive brand identities through structural design variations and label applications, facilitating product differentiation in retail environments.

The aluminum can segment demonstrates a projected CAGR of 6.95% through 2031 in the North American alcoholic beverage market. This trajectory is attributed to increasing market demand for portable and lightweight packaging solutions, particularly among younger demographic segments and outdoor consumption occasions. The format presents substantial environmental advantages through established recycling infrastructure and contributes to corporate sustainability objectives. Additionally, the aluminum can configuration provides enhanced protection against light penetration and oxygen exposure, thereby maintaining optimal beverage quality and product stability.

By Distribution Channel: On-Trade Recovery Reshapes Strategy

The Off-trade channel dominates the North American alcoholic beverage market with a 69.60% market share. This dominance reflects consumer preferences for convenience, variety, and competitive pricing. Off-trade outlets, including supermarkets, hypermarkets, convenience stores, and online retailers, offer consumers extensive product ranges at lower prices compared to on-trade venues. The growth of e-commerce platforms has strengthened the off-trade channel by enabling home delivery and direct-to-consumer sales, aligning with consumer preferences for efficient shopping. Off-trade retail environments also support bulk purchases and value packs, attracting cost-conscious consumers and large households.

The On-trade segment in the North American alcoholic beverage market projects a CAGR of 6.05% through 2031. This growth stems from increasing consumer confidence and higher foot traffic in bars, restaurants, nightclubs, and hospitality venues. The segment benefits from consumer interest in experiential drinking, including craft cocktails, tasting events, and premium offerings that drive higher per-occasion spending. Innovation in beverage offerings, distinct flavor profiles, and mixology expertise attracts younger, urban consumers seeking social experiences. Events, festivals, and sports venues support on-trade consumption, while the segment maintains its importance for brand development and product sampling. These factors contribute to the segment's recovery and growth trajectory through the forecast period.

Geography Analysis

The United States holds 75.80% market share in 2025, supported by extensive production infrastructure, distribution networks, and strong consumer purchasing power. These factors create significant competitive advantages for established companies while limiting international market entry. The United States market influences global trends through consumer preferences and regulatory standards that shape international market development. While the United States market initiates trends like craft beer, celebrity brands, and ready-to-drink (RTD) innovations that later expand globally, its maturity and complex regulations now favor growth in emerging markets over domestic expansion.

Mexico's alcoholic beverage market projects a 6.82% CAGR through 2031. This growth stems from increasing disposable income, middle-class expansion, and urbanization, which boost consumer purchasing power and premium beverage demand. The country's cultural heritage and traditions surrounding tequila and mezcal contribute to both local consumption and export growth.

Canada's alcoholic beverage market continues to expand through changing consumer preferences and demand for diverse beverage options. The market growth reflects the increasing popularity of craft beers, premium spirits, and flavored RTDs among health-conscious and experience-seeking consumers. Statistics Canada reports that in 2023, Newfoundland and Labrador recorded heavy drinking rates of 28.3% among men and 16.5% among women, indicating strong regional consumption patterns that support market growth . These provincial variations in consumption rates contribute to overall market expansion.

Regulatory Landscape

Alcohol regulation in North America remains fragmented across federal and sub-national jurisdictions, influencing labeling, formulation, and route-to-market decisions. In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) continues rulemaking activity around Alcohol Facts statements and major food allergen declarations for wines, distilled spirits, and malt beverages (Federal Register activity in 2025), which is likely to increase compliance workload for brand owners expanding flavored spirits and RTD portfolios.

In Canada, labeling and compositional compliance is handled through federal frameworks enforced by the Canadian Food Inspection Agency (CFIA) under the Safe Food for Canadians Act and related regulations. Health Canada sets requirements for categories such as flavoured purified alcohol (SOR/2019-147), and it is consolidating maximum levels for contaminants such as ethyl carbamate into a central list. Beyond product compliance, interprovincial and cross-border market access is also shaped by provincial liquor control policies, which have become a focal point in US-Canada trade discussions since provincial restrictions affecting US alcohol have been in place since March 2025.

Competitive Landscape

The North America Alcoholic Beverages Market maintains a moderate concentration level, with competition between multinational corporations and emerging craft producers, and celebrity-backed brands. Major companies, including Anheuser-Busch InBev, Constellation Brands, Molson Coors Beverage Company, Diageo PLC, and Heineken NV, control significant market share through diverse product portfolios across beer, wine, and spirits categories. These companies focus on portfolio expansion and premiumization, often acquiring craft and artisanal brands to serve niche markets and meet consumer demand for premium beverage options.

Companies in the market primarily implement technology in supply chain optimization, direct-to-consumer (DTC) sales, and data analytics for marketing purposes rather than product development. Market participants use digital platforms to enhance customer engagement through personalized promotions and delivery services. While production methods remain conventional, the integration of digital marketing tools has become essential for maintaining market position and customer relationships in the digital environment.

New market participants differentiate themselves through brand storytelling promoted via social media and influencer partnerships. These companies frequently employ DTC distribution models to maintain control over customer interactions and pricing strategies. Their focus on limited availability and exclusive offerings allows them to achieve premium pricing and build customer loyalty, particularly among younger consumers.

North America Alcoholic Beverages Industry Leaders

-

Anheuser-Busch InBev

-

Constellation Brands, Inc.

-

Molson Coors Beverage Co.

-

Diageo PLC

-

Heineken NV

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity investment in beverage alcohol production and packaging capability is creating room for suppliers and brand owners to improve throughput, automation, and can-format flexibility as cans gain share in the region. In April 2026, Diageo opened a 360,000-square-foot manufacturing and warehousing facility in Montgomery, Alabama (approximately USD 415 million). Anheuser-Busch also highlighted investments across 2025 and 2026 totaling USD 600 million to advance technology systems and expand production and packaging capacity for brands including Michelob ULTRA, with additional site-specific investments announced in Florida (January 2026) and Missouri (June 2026). These steps support localized production, faster innovation cycles for RTDs and flavor-led extensions, and broader availability of canned formats across off-trade and on-trade.

Opportunities also tie to evolving route-to-market permissions and category adjacency. Canada is working toward a direct-to-consumer alcohol sales framework through provincial and territorial coordination, with a target milestone referenced for May 2026, which opens space for DTC enablement, compliant fulfillment partnerships, and portfolio plans aligned to provincial rules. In parallel, state-by-state rulemaking in the United States is shaping adjacent ready-to-drink concepts such as hemp-infused beverages, including Connecticut THC-per-container limits effective October 1, 2026. This regulatory direction supports value in regulatory-ready product development, labeling systems, and distributor education as companies expand beyond traditional beer, wine, and spirits lineups.

Recent Industry Developments

- July 2026: Representative Claudia Tenney introduced the CANADA Act, directing the U.S. Trade Representative to investigate Canadian provincial restrictions affecting imports of American beer, wine, and spirits under Section 301. The proposal elevated provincial liquor board market-access rules into an active trade-policy track, adding uncertainty for cross-border brand planning and supplier allocation.

- May 2026: Molson Coors Beverage Company priced a public offering of U.S. dollar-denominated senior notes. The financing action supported balance-sheet flexibility for portfolio and operational initiatives, including continued investment in categories beyond core beer.

- April 2024: The US Alcohol and Tobacco Tax and Trade Bureau (TTB) advanced rulemaking activity through a Federal Register notice tied to labeling and regulatory administration for beverage alcohol. Continued federal rulemaking signaled ongoing compliance attention for producers managing multi-SKU portfolios and frequent innovation cycles in flavored spirits and RTDs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the North America alcoholic beverage market is defined as the value generated from legally sold alcoholic drinks across beer, wine, spirits, and other alcoholic beverages in the region, captured across on-trade and off-trade channels.

Scope exclusions: This sizing excludes non-alcoholic substitutes, illicit or unrecorded alcohol, and taxes and fees that do not accrue to beverage sales value.

Segmentation Overview

-

By Product Type

-

Beer

- Ale Beer

- Lager

- Low-Alcohol Beer

- Other Beer Types

-

Wine

- Fortified Wine

- Stilll Wine

- Sparkling Wine

- Other Wines Types

-

Spirits

- Brandy and Cognac

- Liquer

- Tequilla and Mezcel

- Rum

- Whisky

- Other Spirit Types

- Others

-

Beer

-

By End User

- Male

- Female

-

By Packaging Type

- Bottles

- Cans

- Others

-

By Distribution Channel

- On-trade

- Off-trade

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work begins with building a clean fact base on alcohol consumption and supply signals, so the model starts from real-world volumes and trade flows before value is projected. Public sources such as the US Alcohol and Tobacco Tax and Trade Bureau (TTB), the US International Trade Commission (USITC) trade data, Statistics Canada, and Mexico INEGI are used to anchor category definitions and historical direction.

To avoid relying on a single data stream, we also review industry association publications (such as beer, wine, and spirits associations), peer-reviewed studies on drinking patterns, and company filings and investor presentations that explain mix shifts and pricing actions. In a few steps, paid subscriptions for company financials and news intelligence, plus shipment-level import and export databases, are used to sanity check trend breaks and category momentum. This list is illustrative, and many other sources were reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary discussions are used to pressure-test the desk assumptions and to fill gaps that public data does not fully explain, such as channel mix changes, premiumization, and timing of price resets. We speak with producers, distributors, retailers, and trade participants, and the inputs are balanced across the United States, Canada, and Mexico so regional differences do not get averaged out too early.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 17% | |

| Mid tier: 54% | Functional/Unit leaders: 26% | |

| Smaller Players: 18% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts from a top-down rebuild of demand using alcohol sales and consumption indicators by country, and then those totals are translated into value through category level pricing and mix. Because the market has clear product and channel structures, we track a short list of practical inputs such as recorded per-capita consumption trends, share of on-trade versus off-trade, import and export momentum by beverage type, packaging mix (bottles versus cans), and price per liter movement by major category.

Once the regional total is formed, it is cross-checked with selective bottom-up approximations, such as supplier revenue roll-ups from sampled filings, distributor channel checks, and volume times average selling price calculations for beer, wine, and spirits. Where bottom-up coverage is incomplete (for example, smaller local brands), the gap is handled using category shares observed in public statistics and then confirmed through interviews.

Forecasting is built through scenario analysis supported by trend smoothing on the historical series, and it is adjusted using expert views on inflation, discretionary spending, premiumization, and shifts toward ready-to-drink formats. When the main drivers align and the implied pricing and volume outcomes stay realistic for each country, the final forecast is signed off.

Data Validation & Update Cycle

Validation is done in a few passes so the final number is not decided in a single step. We compare the modeled totals against independent signals like alcohol tax removals and shipments, trade direction, and large category revenue disclosures, and then unusual jumps are re-checked for currency timing, one-off stock building, or channel disruptions.

Before release, the work is reviewed by another analyst and differences are discussed until the assumptions can be explained in plain language. The report is refreshed annually, and if material events occur (policy changes, sharp price spikes, or major category disruptions) the model is revisited and the impacted assumptions are re-confirmed through follow-up calls. A final update pass is completed close to delivery so clients receive a current view.

Mordor Intelligence's North America Alcoholic Beverage Market Size Compared Against Other Published Estimates

Published numbers for this market do not always line up because firms often include different beverage definitions, use different value bases, and apply different price and currency timing. Another common reason is that some studies lean heavily on a single dataset and do not re-check the implied volume and pricing outcomes at a category level.

Some external estimates fold in adjacent areas like non-alcoholic alternatives or apply broad retail value assumptions that can inflate totals when definitions are loose. In Mordor Intelligence, the market is counted only for alcoholic drinks (beer, wine, spirits, and other alcoholic beverages) sold across on-trade and off-trade in North America, and the 2025 base is tied back to category signals like trade direction, channel mix, and price per liter checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 341.27 B (2025) | |

| Regional Consultancy A | USD 212.73 B (2025) | Uses a narrower geographic construct (US, Canada, and Rest of North America) and appears to apply simpler category value translation with fewer channel and packaging cross-checks, which can understate on-trade value capture in some years. |

| Global Consultancy B | USD 1579.10 B (2023) | Combines broader beverage scope and adjacent categories (including non-alcoholic alternatives) and relies on a different value basis and base year, which can inflate totals when retail value layers and category boundaries are not kept consistent. |

The spread in the table mainly comes from definition choices and how value is constructed from real consumption and trade signals. By keeping the scope limited to alcoholic beverages and by checking the implied pricing and channel mix country by country, our estimate stays traceable to inputs that can be re-tested and updated when market conditions change.

Key Questions Answered in the Report

Why are ready-to-drink hard seltzers forecast to expand faster than beer and wine through 2031?

Convenience packaging, lower calories, and flavor variety support an 8.37% CAGR for RTD/hard-seltzers, eclipsing the mature 44.02% share beer currently holds.

How large is the male consumer base today, and what change is expected among women drinkers?

Men account for 66.10% of 2025 sales, yet female consumption is set to climb at an 7.92% CAGR as brands introduce lighter, flavor-forward, and lower-ABV options.

What forces are shifting alcoholic beverages from glass to cans?

Although glass bottles command 62.55% share, rising sustainability expectations and portability needs push cans to a 6.95% CAGR between 2026 and 2031.

Why is Mexico slated to be the fastest-growing country in the region?

Premium tequila export momentum and rising domestic disposable income underpin Mexico’s projected 6.82% CAGR through 2031.

Page last updated on: