LLM and Generative AI Energy Optimization Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 5.07 Billion |

| Growth Rate (2026 - 2031) | 26.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LLM and Generative AI Energy Optimization Software Market Analysis by Mordor Intelligence

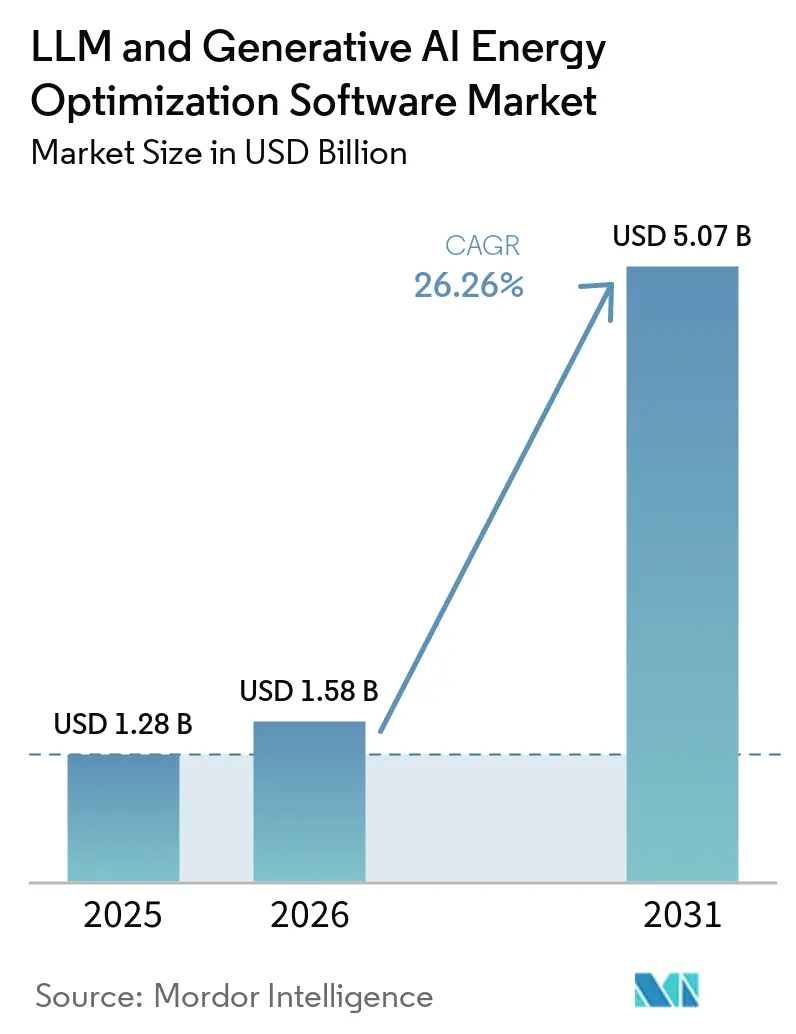

The LLM and generative AI energy optimization software market size is expected to increase from USD 1.28 billion in 2025 to USD 1.58 billion in 2026 and reach USD 5.07 billion by 2031, growing at a CAGR of 26.26% over 2026-2031. The market moved into a stronger growth phase when electricity demand from data centers rose 17% in 2025, while AI-focused facilities expanded power use even faster than the broader power system. At the same time, capital spending by 5 large technology companies rose above USD 400 billion in 2025 and is set to increase by another 75% in 2026, shifting energy optimization from a support function to a direct operating and revenue concern. The cost issue is now tied to physical infrastructure limits, because GPU rack density is rising faster than cooling and power upgrades can be planned and delivered. That is why software-led optimization is being adopted not only to reduce energy waste but also to recover usable compute capacity within fixed grid allocations. The main downside risk remains tied to the pace of AI workload growth, because any slowdown in training and inference expansion would weaken the urgency behind software spending in this category.

Key Report Takeaways

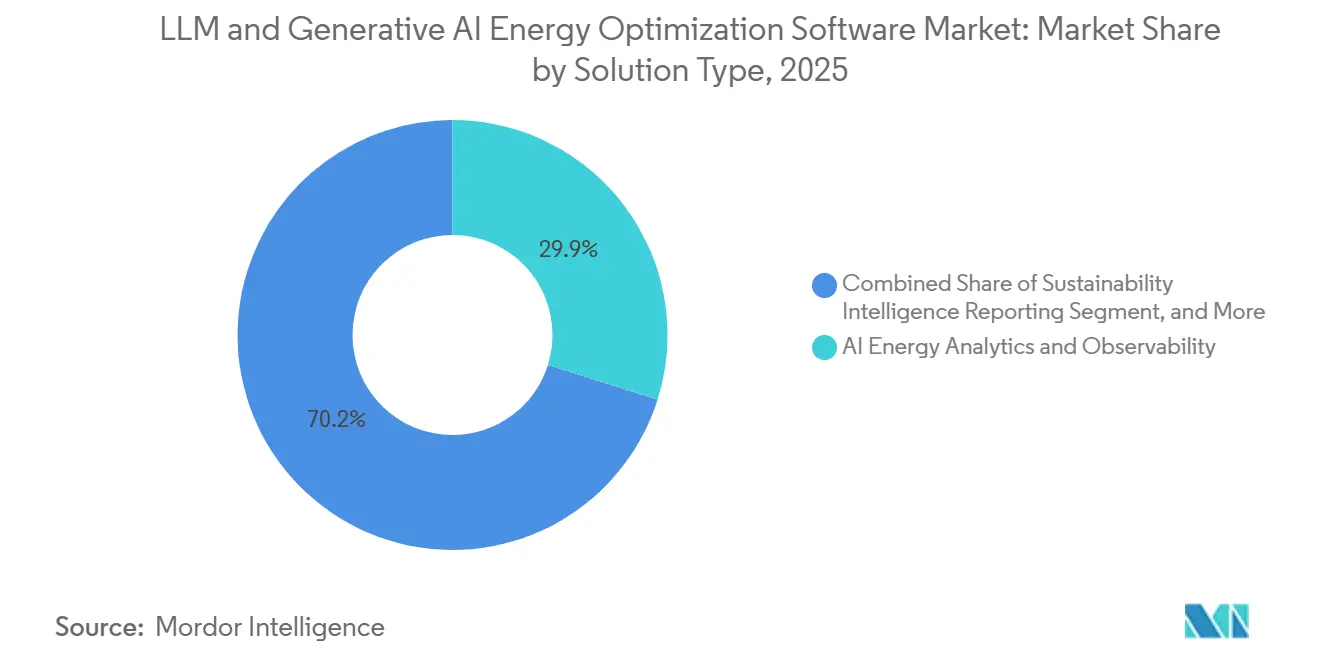

- By solution type, AI Energy Analytics and Observability held 29.85% of the LLM- and generative-AI energy-optimization software market in 2025, while Sustainability Intelligence and Reporting is projected to expand at a 27.34% CAGR through 2031.

- By deployment mode, Cloud-Based solutions held 66.41% share in 2025, while Hybrid deployments are projected to record the highest CAGR at 26.92% through 2031.

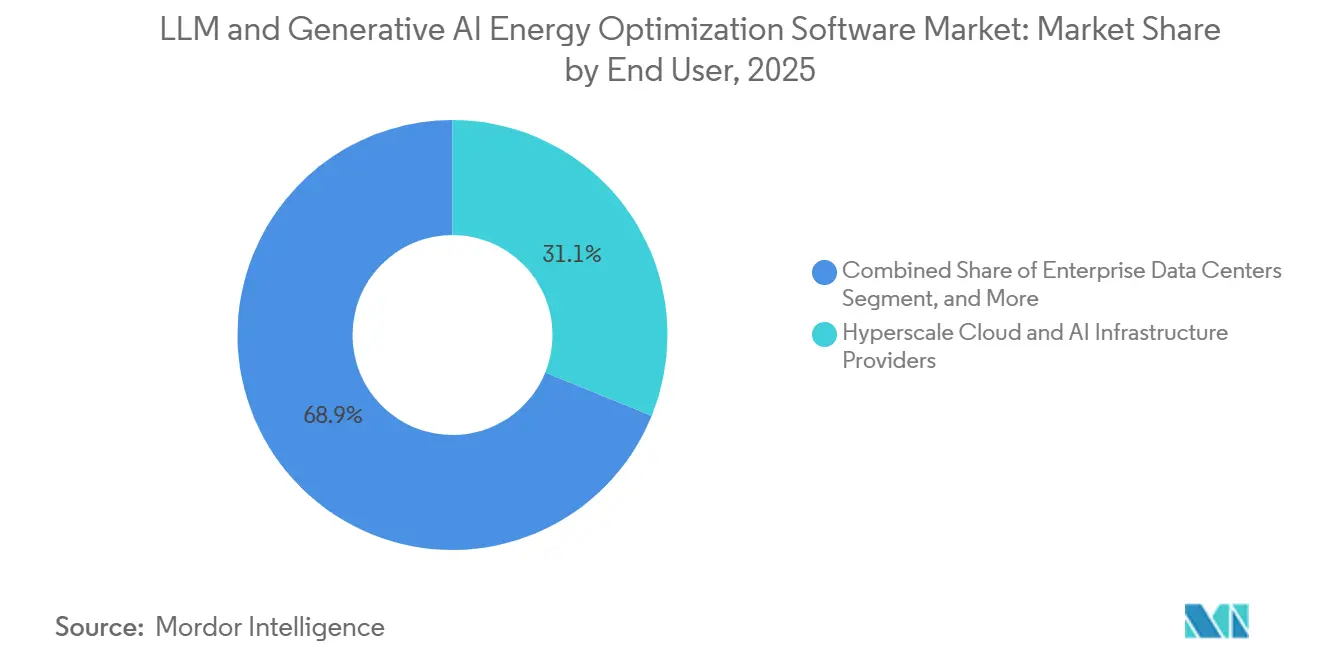

- By end user, Hyperscale Cloud and AI Infrastructure Providers accounted for 31.12% share in 2025, while Enterprise Data Centers are expected to expand at a 27.05% CAGR through 2031.

- By optimization objective, Energy and Carbon Optimization captured 30.45% share in 2025, while Reliability and Availability Optimization is projected to advance at a 26.87% CAGR through 2031.

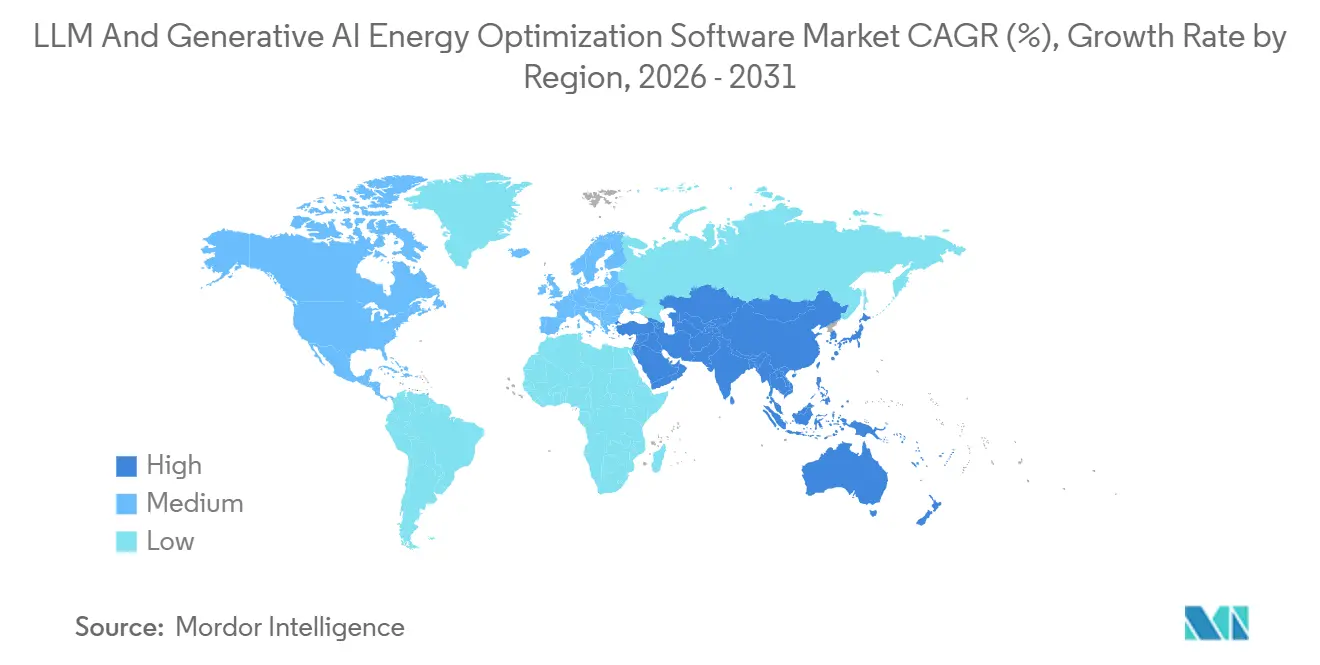

- By geography, North America held 34.56% share in 2025, while Asia-Pacific is projected to grow at a 27.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LLM and Generative AI Energy Optimization Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of AI-Heavy Workloads in Data Centers | +8.5% | Global, concentrated in North America and APAC | Short term (≤ 2 years) |

| Rising Electricity Cost Exposure for AI Infrastructure Operators | +5.8% | Global, acute in North America, EU, and Japan | Short term (≤ 2 years) |

| Regulation-Driven Need for Auditable Energy and Carbon Optimization | +4.2% | EU core, spill-over to APAC and North America | Medium term (2-4 years) |

| Shift from Rule-Based DCIM to Agentic AI Orchestration | +3.1% | Global, hyperscale-led | Medium term (2-4 years) |

| Hidden Power and Cooling Stranding in GPU-Dense Facilities | +2.4% | North America and APAC AI factory clusters | Short term (≤ 2 years) |

| Demand for Real-Time Workload Placement Across Compute and Energy Constraints | +1.9% | Global, with early gains in North America data center corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of AI-Heavy Workloads In Data Centers

The LLM and generative AI energy optimization software market is being driven by the rapid expansion of training and inference workloads in modern data centers. A single NVIDIA H100 GPU node rated at 10.2 kW thermal design power drew only 76% of that level during transformer model training in measured tests, underscoring why planning based solely on nameplate ratings can leave operators with a distorted view of actual power behavior. At the cluster scale, that mismatch creates both planning errors and stranded capacity, because facilities still need enough thermal and electrical headroom to cover real-time workload swings.[1]Imran Latif, Alex C. Newkirk, Matthew R. Carbone, et al., “Empirically-Calibrated H100 Node Power Models for Accurate AI Training Energy Estimation,” IOP Publishing, iopscience.iop.org The LLM and generative AI energy optimization software market benefits from this shift because legacy monitoring tools were built for steadier enterprise loads and cannot manage rapid variation with the same precision. The International Energy Agency projected that electricity use from AI-focused data centers would triple by 2030 relative to 2025, underscoring the multi-year need for software that matches compute intensity with available power and cooling resources. As a result, the LLM and generative AI energy optimization software market is increasingly tied to whether operators can keep new GPU capacity active instead of leaving equipment underused while infrastructure catches up.

Rising Electricity Cost Exposure for AI Infrastructure Operators

The LLM and generative AI energy optimization software market is also benefiting from the fact that electricity exposure has moved closer to the center of infrastructure strategy. The International Energy Agency reported that data center electricity demand surged 17% in 2025 alone, while AI-focused facilities grew even faster, which raised the cost base that operators must manage in real time.[2]International Energy Agency, “Data Centre Electricity Use Surged in 2025, Even with Tightening Bottlenecks Driving a Scramble for Solutions,” International Energy Agency, iea.org The same update stated that capital expenditure by 5 large technology companies exceeded USD 400 billion in 2025 and is set to rise another 75% in 2026, which means the LLM and generative AI energy optimization software market now sits closer to revenue protection than simple utility savings. Hammerhead AI stated that each additional megawatt of stranded power recovered through orchestration can be worth USD 20 million to USD 50 million in constrained infrastructure markets, which changes the value logic behind optimization spending. That framing gives the LLM and generative AI energy optimization software market a stronger role in board-level investment decisions, because recovered power can support more productive compute without waiting for a new grid connection. It also explains why buyers are more willing to fund real-time control software when delayed action can leave expensive AI capacity underutilized.

Regulation-Driven Need for Auditable Energy And Carbon Optimization

Formal reporting and compliance obligations are also supporting the LLM and generative AI energy optimization software market. Under EU Delegated Regulation 2024/1364, data center operators with more than 500 kW of installed IT capacity must report annual indicators, including energy consumption, power utilization effectiveness, and water use, to the European database.[3]European Commission, “Commission Delegated Regulation (EU) 2024/1364,” EUR-Lex, eur-lex.europa.eu The European Parliament noted that the EU was moving toward a broader cloud and AI development framework that would expand processing capacity while maintaining sustainability requirements, thereby increasing the need for auditable data at both facility and model levels. In Japan, the Ministry of Economy, Trade, and Industry updated the policy framework around data center efficiency and highlighted benchmark performance expectations that make energy management more measurable and enforceable. These shifts matter for the LLM and generative AI energy optimization software market because many buyers now need a system that can document performance, not just improve it. That is why sustainability reporting tools are moving from an optional dashboard function to a compliance-linked software layer inside the LLM and generative AI energy optimization software market.

Shift From Rule-Based DCIM to Agentic AI Orchestration

The LLM and generative AI energy optimization software market is moving beyond static monitoring because AI clusters create power behavior that rule-based systems were not built to handle. Research cited in the market showed that an 80,000-chip cluster can experience demand swings of 24 MW in 20 milliseconds, which is far too dynamic for many traditional control approaches. Phaidra stated that its reinforcement-learning agents reduced cooling energy by 25% and lowered thermal spikes by nearly 80% during tests on NVIDIA GB200 and GB300 systems, demonstrating the growing commercial case for adaptive control. NVIDIA said its DSX OS provides modular software components for AI factory operations, including GPU-aware workload placement and dynamic power allocation, which creates a structured base for third-party optimization agents to act within defined safety boundaries. The LLM and generative AI energy optimization software market, therefore, reflects a wider shift from alert-based infrastructure management toward software that continuously weighs thermal state, queue depth, and power availability together. Over time, that makes the LLM and generative AI energy optimization software market less about dashboards and more about direct control over the economics of compute delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity Across DCIM, BMS, And IT Stack | -3.2% | Global, most acute in legacy enterprise and colocation facilities | Medium term (2-4 years) |

| Cybersecurity And Control-Plane Risk In Autonomous Optimization | -2.1% | Global, particularly North America, EU, and government-sensitive deployments | Long term (≥ 4 years) |

| Data Fragmentation Limits Model Accuracy And ROI Visibility | -1.8% | Global, acute in multi-vendor and multi-site environments | Medium term (2-4 years) |

| Long Procurement Cycles In Mission-Critical Infrastructure Environments | -1.5% | North America and EU enterprise data centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across DCIM, BMS, And IT Stack

The LLM and generative AI energy optimization software market still faces a significant restraint: the difficulty of integrating facility systems, IT operations, and workload controls into a single usable loop. Many buyers need bidirectional connections across asset data, power telemetry, and orchestration layers before they can safely automate any response, which slows deployment and lengthens proof-of-value cycles.[4]Sunbird Software, “Sunbird dcTrack DCIM Operations Release 9.2.3 Available Now,” Sunbird Software, prweb.com Vendors are responding with broader operational platforms, and Nlyte positioned its Operational AI offering around data center, colocation, hybrid cloud, and edge visibility from a single interface, which shows where the market is trying to remove friction. Even so, the LLM and generative AI energy optimization software market still encounters problems when data refresh rates, control permissions, and vendor interfaces do not align across systems. Research on future data center operations also pointed to operator caution about granting more authority to AI systems, reflecting concern about acting on incomplete or inconsistent telemetry. Until integration becomes easier, the LLM and generative AI energy optimization software market will continue to see slower adoption in legacy enterprise estates and complex colocation environments.

Cybersecurity And Control-Plane Risk In Autonomous Optimization

The LLM and generative AI energy optimization software market also faces resistance due to cybersecurity concerns as the software shifts from advisory outputs to active control. CISA warned in December 2025 that AI integration into operational technology environments can create risks such as process-model drift, safety-process bypasses, and adversarial data manipulation that reaches physical infrastructure before people can intervene. This matters because the LLM and generative AI energy-optimization software market is increasingly touching cooling systems, power delivery equipment, and supervisory controls that sit inside mission-critical facilities. Buyers in financial services, healthcare, government, and sensitive cloud environments tend to apply additional validation when a platform can directly influence those systems. That scrutiny does not remove demand for optimization, but it extends testing, governance review, and procurement timelines inside the LLM and generative AI energy optimization software market. The result is a slower path from pilot to full deployment whenever autonomous optimization moves closer to the control plane of essential infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Analytics Foundations Support Broader Control And Reporting Demand

AI Energy Analytics and Observability held 29.85% of the LLM- and generative-AI energy-optimization software market in 2025, making it the largest solution type, as most operators start with visibility before automating any intervention. The category remains the base layer of the LLM and generative AI energy-optimization software market, since workload orchestration and thermal control are difficult to trust without circuit-level, near-real-time telemetry. Verdigris stated that its sensing platform helped one Fortune 500 operator recover more than 1 MW of stranded capacity across more than 60 facilities, while T-Mobile identified degradation in 4% of its UPS rectifier fleet 21 days before failure without standard alarms. Those examples show why buyers first spend on measurement: the operational case becomes stronger once hidden capacity and early failure risk become visible. In practice, the largest slice of the LLM and generative AI energy optimization software market still starts with data quality, electrical intelligence, and continuous observability.

Sustainability Intelligence and Reporting is expected to expand at a 27.34% CAGR through 2031, which makes it the fastest-growing solution type in the LLM and generative AI energy optimization software market. Its growth is tied to mandatory disclosure and audit needs, especially where data center performance must be reported in standardized formats under European rules. The LLM and generative AI energy optimization software market is also seeing stronger interest in orchestration, thermal optimization, and digital twin tools as operators move beyond first deployments and begin asking how to raise compute output per watt. NVIDIA and Jacobs announced work around AI factory digital twins to simulate facility equipment efficiency, thermal performance, and throughput before physical deployment, which supports this shift toward planning-led optimization. Across the LLM and generative AI energy optimization software market, the common direction is toward integrated suites that link observability, scheduling, thermal response, and reporting rather than keeping each function in a separate tool.

By Deployment Mode: Hybrid Architecture Gains Ground Beside Cloud Scale

Cloud-Based solutions held 66.41% of the LLM and generative AI energy optimization software market in 2025, reflecting the ease of rolling out software across distributed estates through centralized delivery models. That position remains strong because many operators still want continuous updates, broad remote visibility, and lower deployment friction across multiple facilities. Even so, the LLM and generative AI energy optimization software market is moving toward hybrid setups where local control and cloud analytics can coexist. This is especially important where inference latency is sensitive or where facility control signals should not depend entirely on public cloud endpoints. In those environments, the LLM and generative AI energy optimization software market is being shaped by architecture choices as much as by algorithm quality.

Hybrid deployments are projected to grow at a 26.92% CAGR through 2031, which makes them the fastest-growing mode in the LLM and generative AI energy optimization software market. The main reason is that operators do not want to choose between local control over cooling and power systems and broader analytics that span sites and workloads. Nlyte positioned its Operational AI platform around data center, colocation, hybrid cloud, and edge operations, which reflects how vendors are adapting their products to this demand pattern. On-premises models also remain relevant in the LLM and generative AI energy optimization software market for regulated sectors and sovereign AI programs where data residency, network isolation, and direct control of optimization logic remain essential. As a result, deployment demand in the LLM and generative AI energy optimization software market is broadening from SaaS convenience toward a more mixed architecture that mirrors how AI infrastructure is actually being built and governed.

By End User: Enterprise Adoption Broadens Demand Beyond Hyperscalers

Hyperscale Cloud and AI Infrastructure Providers held 31.12% of the LLM and generative AI energy-optimization software market share in 2025, indicating that the first major spending wave came from the largest AI infrastructure owners. This was expected since hyperscalers were the earliest to run dense training clusters at a scale where power, cooling, and utilization had to be managed together. Their role remains central because the market continues to learn from hyperscale operating practices, especially in workload placement, thermal control, and power-aware scheduling. Colocation operators are also becoming more relevant as they aim to offer AI-ready sites with better tenant-level visibility and operational coordination. A Uptime Institute industry survey found that operators were rethinking capacity and cloud strategies amid mounting demand pressure, supporting the case for more active optimization software across shared infrastructure environments.

Enterprise Data Centers are projected to advance at a 27.05% CAGR through 2031, making them the fastest-growing end-user group in the market. This reflects a delayed but accelerating shift as more enterprises move LLM inference inside their own environments after cloud-led experimentation. The market benefits from this transition because enterprise sites often require software-led load shaping and monitoring before they can confidently support denser AI workloads. Sovereign and government deployments add another layer of demand, with the Government of Canada seeking proposals for sovereign AI data centers above 100 MW in early 2026, and South Korea advancing a national sovereign AI foundation model program using Backend.AI cluster infrastructure software. Together, these shifts mean the market is no longer dependent on hyperscalers alone, as enterprise, colocation, and public-sector buyers are building a wider and more diverse demand base.

By Optimization Objective: Reliability Gains Weight As Compute Value Rises

Energy and Carbon Optimization accounted for 30.45% of the LLM and generative AI energy optimization software market in 2025, making it the largest optimization objective. That ranking reflects the immediate pressure operators feel from rising power use, tighter grid access, and growing demand for measurable efficiency. The LLM and generative AI energy optimization software market still carries this cost-focused foundation, because energy remains one of the first variables buyers can quantify during software evaluation. At the same time, buyers are increasingly looking beyond simple savings and asking how software affects uptime, throughput, and usable capacity within the constraints of existing infrastructure. This is one reason the LLM and generative AI energy optimization software market is shifting toward multi-objective platforms rather than tools built around a single metric.

Reliability and Availability Optimization is projected to grow at a 26.87% CAGR through 2031, making it the fastest-growing objective in the LLM and generative AI energy optimization software market. That pattern reflects the high value of uninterrupted GPU operations, because failures during long model training runs can carry a far greater cost than the electricity used during those workloads. Phaidra linked its platform to lower thermal spikes during tests on NVIDIA GB200 and GB300 environments, which supports the growing focus on operational stability rather than energy savings alone. Buyers are also paying more attention to cost optimization, demand-response participation, carbon-aware scheduling, and performance tuning inside the LLM and generative AI energy optimization software industry, because these goals now interact in the same operating environment. That leaves the LLM and generative AI energy optimization software market moving toward platforms that can balance reliability, performance, cost, and carbon outcomes simultaneously.

Geography Analysis

North America held 34.56% of the LLM and generative AI energy optimization software market share in 2025, making it the largest regional market. The region maintained this lead thanks to its concentration of hyperscale and cloud AI infrastructure, alongside early large-scale demand for integrated energy, cooling, and compute management. The White House issued an executive order in July 2025 to accelerate federal permitting for data center infrastructure and energy transmission, supporting continued expansion of AI campuses that require optimization systems from the outset. Canada added a public-sector demand layer when the federal government sought proposals for sovereign AI data centers above 100 MW in early 2026. Together, these factors kept North America at the center of the market in 2025 and sustained new software demand into 2026.

Asia-Pacific is projected to grow at a 27.45% CAGR through 2031, making it the fastest-growing geography in the market. Japan strengthened its efficiency efforts through METI policy updates and collaborative programs for software-defined liquid-cooling facilities. China introduced a formal evaluation framework with T/CCSA 619-2025, setting AI-based methods for data center energy-saving evaluation. South Korea's advanced national AI programs, with Lablup and Upstage passing Phase 1 evaluation under the sovereign AI foundation model project. These developments give Asia-Pacific a mix of regulatory pressure, infrastructure buildout, and national AI investment, driving adoption.

Europe remains strategically important because it combines capacity expansion with structured efficiency and reporting requirements. Germany approved a national data center strategy in March 2026, aiming to double total capacity and quadruple AI compute capacity by 2030, while tying new assets to strict efficiency and renewable power expectations. The wider EU framework also supports adoption by imposing standardized reporting requirements for larger data centers, making software-based measurement and disclosure unavoidable. Meanwhile, the Middle East, Africa, and South America remain earlier-stage opportunities, with adoption likely to follow sovereign AI buildouts, new capacity programs, and rising interest in sustainability-linked infrastructure procurement.

Competitive Landscape

The LLM and generative AI energy optimization software market remained moderately fragmented across circuit-level observability, thermal and infrastructure optimization, workload orchestration, and sustainability reporting. That fragmentation shaped buying behavior because operators often had to connect separate tools rather than procure one platform that covered every layer. The market, therefore, carried both opportunity and complexity, with white space still open for vendors that can unify multiple functions in a single control plane. Phaidra represented one of the clearest full-stack moves in this direction after raising a USD 50 million Series B in October 2025, bringing total capital raised to USD 120 million and expanding its work across cooling systems, workload management, and international growth. That left the market with a visible group of specialists, but without a single vendor that had clearly established platform leadership across all capability layers.

Hardware-linked differentiation also remained important in the market. Verdigris built part of its position around high-frequency electrical sensing and early fault visibility, which gave it a stronger data foundation than software-only competitors in some deployments. Southwire reinforced that point in March 2026 when it made a strategic investment in Verdigris and entered a product integration agreement tied to AI-scale data center power delivery infrastructure. The market also saw incumbents widen their reach, with Nlyte launching Version 16 in November 2025 to add executive dashboards, expanded sustainability reporting, and tighter alignment with Carrier’s QuantumLeap suite. These moves show that competition is increasingly centered on product breadth, integration depth, and control relevance rather than on monitoring alone.

A second competitive theme is the push toward multi-objective optimization. NVIDIA’s DSX OS highlights an open, modular software base for operating AI factories at scale, making it easier for third-party providers to plug workload placement and power-aware logic into broader AI infrastructure stacks. That matters because buyers now want systems that can balance electricity use, thermal headroom, performance, and uptime within a single operating framework. The market still lacks a dominant player in that space, leaving room for both organic expansion and later consolidation. Until one vendor proves it can tie observability, orchestration, facility control, and reporting together at scale, the LLM and generative AI energy optimization software market is likely to remain specialized and only moderately coordinated.

LLM and Generative AI Energy Optimization Software Industry Leaders

Phaidra Inc.

Schneider Electric SE Br

Vertiv Holdings Co.

Sunbird Software, Inc.

C3.ai, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: EkkoSense released EkkoSoft Critical 9.4, incorporating Auto Cooling Anomaly Detection for hybrid air and liquid cooling environments, with automatic setpoint detection, chilled water flow rate anomaly alerts, and BMS integration via Teams and JSON webhooks.

- March 2026: Southwire Company LLC announced a strategic investment in Verdigris Technologies, with both companies entering a product integration agreement to embed Verdigris's AI-native electrical intelligence into Southwire offerings for AI-scale data center power delivery infrastructure, targeting per-circuit visibility and validated operating limits for GPU rack deployments.

- March 2026: IIJ, Preferred Networks (PFN), and JAIST launched joint R&D on a Software Defined Liquid Cooling Facility, a direct-water-cooled modular AI data center with AI compute resource allocation and energy efficiency optimization coordinated as a single software-controlled system, with a benchmark pPUE target below 1.1.

- January 2026: Lablup (Backend.AI) and Upstage passed Phase 1 evaluation for South Korea's national Sovereign AI Foundation Model project, deploying Backend.AI's GPU cluster infrastructure operating platform with maximum throughput and automatic fault recovery on a government-provisioned 500-plus NVIDIA B200 GPU cluster.

Global LLM and Generative AI Energy Optimization Software Market Report Scope

The LLM and Generative AI Energy Optimization Software market refers to platforms and solutions designed to reduce the energy consumption, carbon footprint, and operational costs associated with training, deploying, and running large language models (LLMs) and generative AI workloads. These systems provide functionalities such as AI energy analytics and observability, workload orchestration and scheduling, thermal and infrastructure optimization, digital twin–based simulation, and sustainability intelligence with automated reporting.

The LLM and Generative AI Energy Optimization Software market report is segmented by Solution Type (AI Energy Analytics and Observability, AI Workload Orchestration and Scheduling, Thermal and Infrastructure Optimization, Digital Twin and Simulation Platforms, Sustainability Intelligence and Reporting), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), End User (Hyperscale Cloud and AI Infrastructure Providers, Colocation Data Center Operators, Enterprise Data Centers, Sovereign and Government AI Infrastructure Operators), Optimization Objective (Energy and Carbon Optimization, Performance Optimization, Cost Optimization, Reliability and Availability Optimization), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| AI Energy Analytics and Observability |

| AI Workload Orchestration and Scheduling |

| Thermal and Infrastructure Optimization |

| Digital Twin and Simulation Platforms |

| Sustainability Intelligence and Reporting |

| Cloud Based |

| Hybrid |

| On Premises |

| Hyperscale Cloud and AI Infrastructure Providers |

| Colocation Data Center Operators |

| Enterprise Data Centers |

| Sovereign and Government AI Infrastructure Operators |

| Energy And Carbon Optimization |

| Performance Optimization |

| Cost Optimization |

| Reliability And Availability Optimization |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | AI Energy Analytics and Observability | ||

| AI Workload Orchestration and Scheduling | |||

| Thermal and Infrastructure Optimization | |||

| Digital Twin and Simulation Platforms | |||

| Sustainability Intelligence and Reporting | |||

| By Deployment Mode | Cloud Based | ||

| Hybrid | |||

| On Premises | |||

| By End User | Hyperscale Cloud and AI Infrastructure Providers | ||

| Colocation Data Center Operators | |||

| Enterprise Data Centers | |||

| Sovereign and Government AI Infrastructure Operators | |||

| By Optimization Objective | Energy And Carbon Optimization | ||

| Performance Optimization | |||

| Cost Optimization | |||

| Reliability And Availability Optimization | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and projected size of the LLM and generative AI energy optimization software market?

The market was valued at USD 1.28 billion in 2025, rose to USD 1.58 billion in 2026, and is forecast to reach USD 5.07 billion by 2031 at a 26.26% CAGR.

Which solution category leads revenue in this space?

AI Energy Analytics and Observability led with 29.85% share in 2025 because most operators first need accurate circuit-level and facility-level visibility before they automate optimization actions.

Why are hybrid deployments growing faster than cloud-only models?

Hybrid deployments are projected to grow at a 26.92% CAGR because operators want local control over power and cooling systems while still using cloud-scale analytics across sites.

Which end-user group is expanding fastest?

Enterprise Data Centers are expected to grow at a 27.05% CAGR through 2031 as more firms bring LLM inference in-house for stronger control over cost, privacy, and performance.

Which region is expanding fastest for energy optimization software tied to AI infrastructure?

Asia-Pacific is forecast to grow at a 27.45% CAGR through 2031, supported by national AI infrastructure programs, energy efficiency standards, and data center policy updates.

What is the main buyer priority beyond energy savings?

Reliability and Availability Optimization is the fastest-growing objective at a 26.87% CAGR, which shows that operators are increasingly focused on avoiding failures that disrupt expensive GPU workloads.

Page last updated on: