Telecom Generative AI Applications Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 33.38% CAGR |

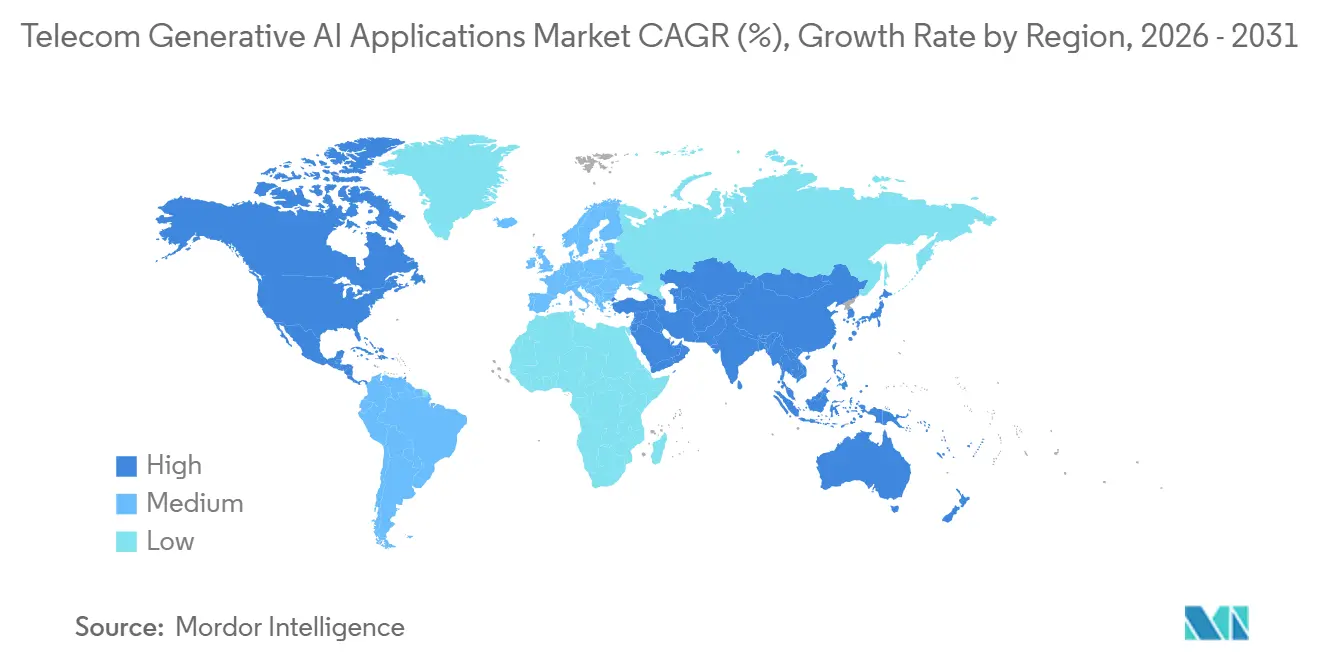

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Generative AI Applications Market Analysis by Mordor Intelligence

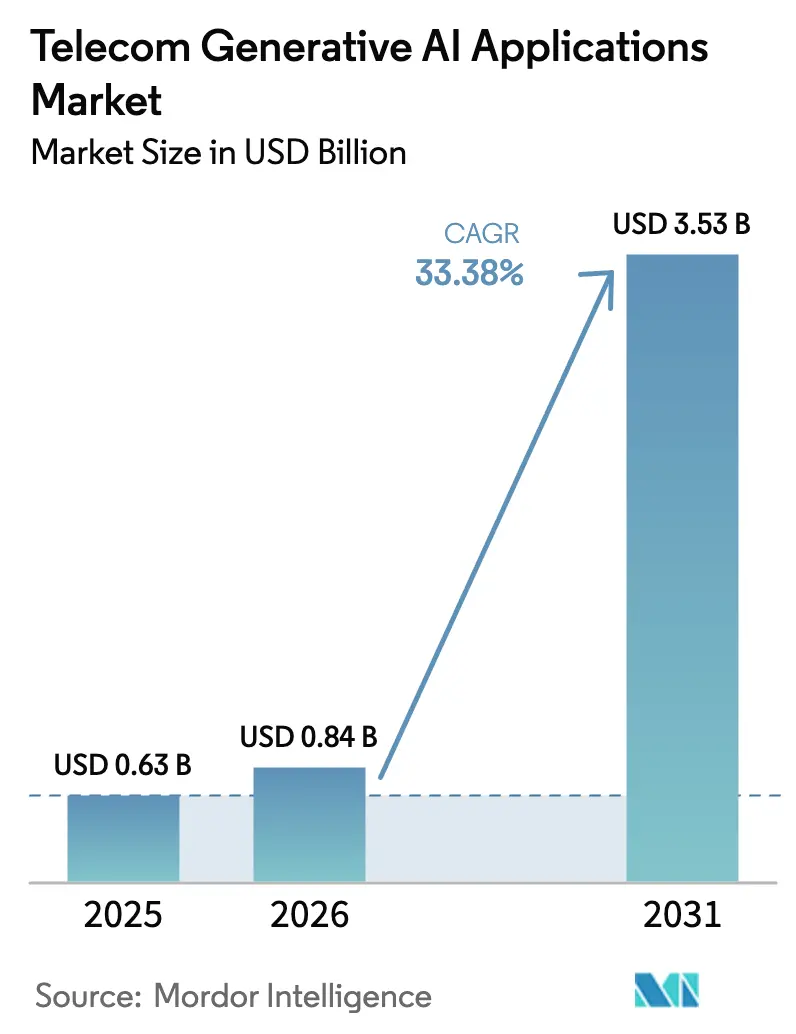

The Telecom Generative AI Applications Market size was valued at USD 0.63 billion in 2025 and is estimated to grow from USD 0.84 billion in 2026 to reach USD 3.53 billion by 2031, at a CAGR of 33.38% during the forecast period (2026-2031). Generative AI is shifting from small-scale chatbots to production-grade platforms that automate network orchestration, fraud detection, and predictive maintenance, replacing manual workflows that once dominated operations. North American operators are leading cost-optimization efforts, exemplified by AT&T’s 90% drop in inference costs after deploying a multi-model routing fabric that allocates queries to the cheapest model that meets accuracy thresholds. Infrastructure vendors now embed AI as a native layer. Ericsson and Google Cloud’s 5G core-as-a-service offering speaks directly to this trend, bundling real-time policy tuning into the core software rather than selling it as an extra module. Equipment makers and hyperscalers are racing to lock in early adopter contracts, so the Telecom generative AI applications market is moving from experimentation to mainstream capital budgeting.

Key Report Takeaways

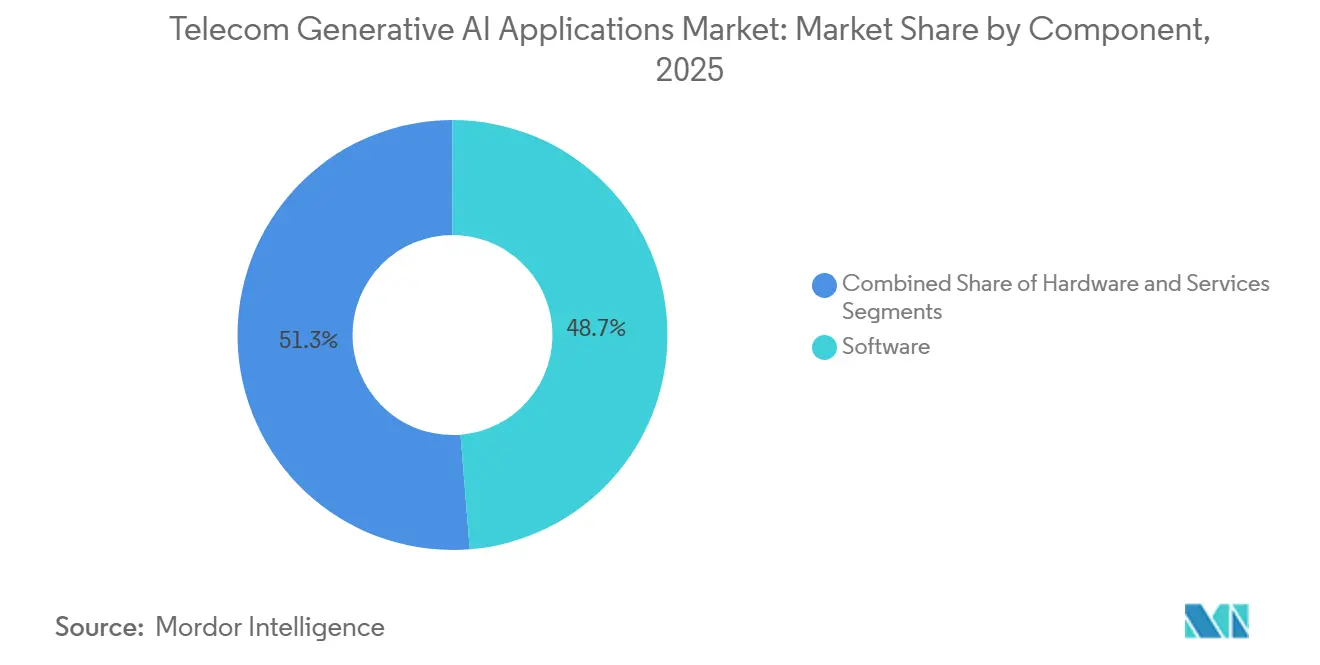

- By component, software accounted for 48.72% of the Telecom generative AI applications market share in 2025; however, services are projected to expand at a 35.40% CAGR through 2031, the fastest rate among all components.

- By application, customer service automation accounted for 27.81% of the Telecom generative AI applications market in 2025, while predictive maintenance is advancing at a 37.01% CAGR through 2031, outpacing every other application.

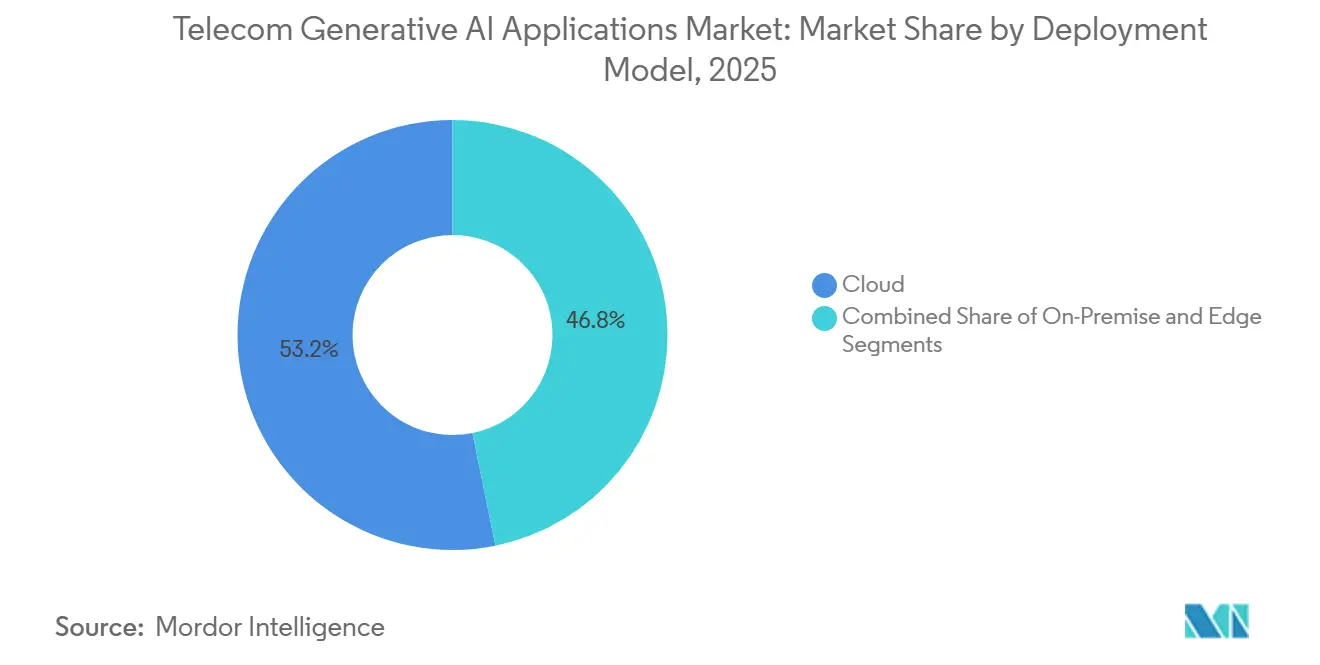

- By deployment model, cloud accounted for 53.20% of the Telecom generative AI applications market share in 2025, whereas edge deployments are forecast to grow at a 35.04% CAGR through 2031.

- By telecom operator type, mobile network operators led with 42.03% share of the Telecom generative AI applications market size in 2025, while mobile virtual network operators are on track to record a 36.41% CAGR through 2031.

- By geography, North America led with 35.88% share of the Telecom generative AI applications market size in 2025, while Asia-Pacific are on track to record a 36.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telecom Generative AI Applications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI Powered Network Automation | +7.2 % | Global, early traction in North America and Asia-Pacific | Medium term (2-4 years) |

| Hyper-Personalized Customer Experience Solutions | +6.8 % | North America, Europe, Asia-Pacific urban clusters | Short term (≤ 2 years) |

| Surge in AI-Native 5G Stand-Alone Deployments | +6.5 % | Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| Cost Deflation via Large Language Model Optimization | +5.9 % | Global, cost-sensitive emerging markets | Short term (≤ 2 years) |

| Ecosystem Push for Open RAN and ORAN-Aligned AI Toolkits | +4.1 % | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Telco-specific Foundation Models and Verticalized APIs | +5.3 % | Global, led by large-subscriber operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative-AI Powered Network Automation

Operators are field-testing multi-agent systems that auto-adjust radio parameters, reroute traffic, and provision network slices in seconds, replacing hours-long manual tasks. Deutsche Telekom’s proof-of-concept reduced human configuration work by 40% across 50,000 cell sites, freeing engineers for strategic planning.[1]Telekom AG, “Multi-Agent AI Orchestration Platform,” telekom.com Nokia and AWS reenacted a live demo at Mobile World Congress 2025 in which virtual assistants negotiated quality-of-service targets in natural language, removing the need for dedicated provisioning portals.[2]Nokia Corp., “Agentic AI Network Slicing,” nokia.com Labor shortages in mature markets magnify ROI because AI inference costs undercut the fully loaded cost of radio-frequency engineers. The caveat is that true real-time control depends on dense edge-compute nodes; operators missing that layer will incur latency penalties, pushing them to launch network modernization programs in parallel with AI rollouts.

Hyper-Personalized Customer Experience Solutions

First-generation chatbots delivered static FAQ responses, but generative AI now tailors offers and troubleshooting steps to each subscriber’s device, location, and history, yielding 20-30% higher conversion in pilot runs. Verizon blended Google’s Gemini model into its support stack and shortened average handle time by 18%, a hard metric that finance teams recognize.[3]Verizon Inc., “Google Gemini Customer Service Integration,” verizon.com Salesforce observed a 25% upsell lift when AI-curated recommendations were pushed via SMS, underlining that delivery channel and model output must co-evolve.[4]Salesforce Inc., “Einstein GPT Upsell Impact,” salesforce.com Prepaid markets reap the fastest gains because operators iterate offers within minutes, but privacy statutes in Europe and California require explicit consent for behavioral analytics, stretching deployment roadmaps in high-value regions.

Surge in AI-Native 5G Stand-Alone Deployments

Stand-alone cores break free from legacy EPC stacks, allowing AI microservices to run alongside user-plane functions without translation layers. Ericsson-Google’s core-as-a-service launched with tier-1 operators spanning Europe to Japan, enabling policy engines to shift QoS thresholds based on predicted load rather than preset rules. China Mobile’s nationwide deployment trained a 10-billion-record foundation model to refine handovers in high-speed rail corridors, boosting call-completion rates by 15%. For smaller carriers, capex remains daunting, but core-as-a-service eases entry by converting fixed costs into variable opex.

Cost Deflation via Large Language Model Optimization

Routing simple intents to compact models and complex tasks to frontier models cut AT&T’s monthly AI spend from USD 2 million to USD 200,000 while holding customer satisfaction steady. Huawei’s TelecoLM trimmed per-query costs to USD 0.0001, 10 times lower than public APIs, appealing to operators with average revenue per user below USD 5. The challenge is version sprawl, as every new fine-tuned checkpoint needs monitoring, or else performance drifts unnoticed across geographies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hallucination-Driven Regulatory Non-Compliance Risk | -3.8 % | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Scarcity of Telecom-Grade Annotated Data Assets | -4.2 % | Global, severe in emerging markets | Medium term (2-4 years) |

| High Inference Cost on Legacy Core Networks | -3.1 % | Emerging markets, older networks in developed regions | Medium term (2-4 years) |

| Evolving Standards Fragmentation Across Regions | -2.6 % | Global, cross-border deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Inference Cost on Legacy Core Networks

Many operators still lean on legacy packet-core hardware that was never designed for the compute-intensive workloads of generative models. When those aging switches and EPC platforms attempt real-time inference, the silicon bottlenecks push per-query charges up to USD 0.002 on public endpoints, 20 times the rate achieved on modern, AI-optimized cores. Carriers in low-ARPU regions feel the squeeze most acutely because even modest AI adoption can swamp thin operating margins. As a result, boards in parts of Africa, Latin America, and Southeast Asia are shelving customer-facing use cases and instead reserving scarce capacity for fraud detection and other back-office tasks that deliver a clearer return on spend.

Evolving Standards Fragmentation Across Regions

Telecom engineers now juggle an alphabet soup of rulebooks, 3GPP Release 18, O-RAN Alliance ML specifications, the EU AI Act, and a patchwork of national privacy codes that seldom align. A model cleared for deployment in Japan can stumble on documentation mandates in Germany or fail data-residency checks in Saudi Arabia, forcing vendors to maintain parallel code branches and audit trails for each jurisdiction. Every divergence inflates certification timelines and drains research and development budgets, nudging smaller suppliers toward niche markets where compliance overhead is manageable. Until regulators harmonize AI governance, interoperability promises will stay aspirational, and multi-country rollouts will proceed one waiver at a time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge as Operators Outsource AI Governance

Software retained 48.72% of the Telecom generative AI applications market share in 2025, owing to telco-tuned foundation models delivered as consumable APIs. Hardware shipments decelerated as inference-optimized chips deliver 10× the performance per watt, enabling carriers to install fewer accelerators per data center. Conversely, services revenue is clocking a 35.40% CAGR, reflecting operator preference for managed fine-tuning and compliance outsourcing. The Telecom generative AI applications market size for services is projected to climb from USD 0.26 billion in 2026 to USD 1.38 billion by 2031 as MSPs introduce outcome-based pricing.

Competitive differentiation in services now pivots on governance. Amdocs and IBM position unified control planes that handle version tracking, prompt logging, and regulator-ready audit trails. Hardware vendors such as NVIDIA partner with Nokia to pre-integrate accelerators into base stations, collapsing the boundaries between boxes and code. Operators thus negotiate bundles instead of line-item licenses, compressing procurement cycles and magnifying vendor bargaining power.

By Application: Predictive Maintenance Outpaces Customer Automation

Customer service automation maintained a 27.81% share in 2025, as chatbots deflected tier-1 queries. Yet predictive maintenance will command the fastest growth, as the Telecom generative AI applications market devoted to predictive maintenance is forecast to expand at a 37.01% CAGR, taking share as AI agents pre-empt failures 72 hours before they occur. Nokia’s roll-out across 15 networks saved USD 50 million per carrier by cutting truck rolls and slashing mean time to repair to 2 hours.

Fraud detection and security workloads rise in tandem as adversaries generate synthetic voices and spoofed traffic; Pindrop’s platform reduced account takeovers by 40% at North American telcos. Network optimization uses generative models to stress-test digital twins under congestion, while marketing personalization remains a smaller slice but earns budget in prepaid battlegrounds where churn tops 30% annually. Convergence across use cases favors unified platforms that pool telemetry and retrain shared embeddings, reducing redundant compute spend.

By Deployment Model: Edge Gains as Latency Trumps Centralization

Cloud deployments accounted for 53.20% of the Telecom generative AI applications market share in 2025, bolstered by hyperscaler marketplaces that package telecom APIs with pay-as-you-go pricing. Yet edge installations will grow 35.04% CAGR as sub-10 ms latency becomes mandatory for AR, V2X, and industrial automation. NVIDIA’s AI-on-5G kits colocate GPUs with radio units, securing robotics and video analytics workloads without costly backhaul.

Hybrid patterns reign. Operators are trained centrally for scale, then weights are distilled to edge nodes, ensuring real-time inference even if core links fail. AWS and Verizon’s Wavelength alliance monetizes this architecture by selling spare edge compute to enterprises, repurposing cell sites as micro-clouds. On-premise remains viable where data-sovereignty rules bar cloud export; sovereign clouds in Europe and the Middle East earmark sensitive police or defense workloads for private stacks.

By Telecom Operator Type: MVNOs Leverage Asset-Light AI

Mobile network operators held a 42.03% share in 2025, underpinned by privileged access to core telemetry that refines models. Mobile virtual network operators, however, will post a 36.41% CAGR by running lightweight generative models on leased spectrum without sunk capex. Tello Mobile’s chatbot handles 80% of tickets, proving that customer experience is the prime MVNO battleground.

Fixed-line carriers pilot generative AI for fiber build planning, using models to predict optimal trench paths and flag cable degradation, saving 15% on deployment costs during European rollouts. Internet service providers embed AI portals that automatically generate router troubleshooting steps, improving first-call resolution. Slower uptake among legacy fixed operators stems from integration pain with antiquated billing engines, but greenfield fiber builds in Africa and Southeast Asia are AI-native from day one, skipping legacy drag.

Geography Analysis

North America retained 35.88% share in 2025 as FCC explainability rules sharpened demand for audit-friendly platforms and proximity to hyperscaler regions compressed integration timelines. AT&T’s plunge in inference costs illustrates the region’s focus on opex efficiency, while Canada’s disclosure mandates slowed front-office AI but nurtured customer trust. Mexico’s draft guidelines tilt the compliance burden toward larger players able to absorb legal costs, consolidating share.

Asia-Pacific will register a 36.72% CAGR, the highest worldwide, propelled by China Mobile’s 10 billion Call Detail Record model and Reliance Jio’s AI-enabled MyJio app handling 50 million daily queries. Japan’s NTT DoCoMo offers conversational network slicing; SK Telecom’s churn predictor reduced attrition by 1.2 points. Australia, burdened by strict liability laws, confines AI to back-office scenarios.

Europe is growing more slowly due to the EU AI Act’s high-risk label, but Telia’s GDPR-compliant slice configurator shows that compliance paths are viable. Deutsche Telekom’s 40% cut in manual tasks shows that productivity gains can coexist with regulation. The Middle East invests aggressively in AI-native 5G to power smart-city agendas; du’s bilingual chatbot exemplifies regional localization. Latin America’s uptake centers on Brazilian fraud-detection projects, whereas Argentina delays due to macroeconomic volatility. Africa faces cloud scarcity, but South Africa and Nigeria test edge AI for rural optimization, highlighting latent potential.

Competitive Landscape

The value chain is splitting into three power blocs, each leveraging unique strengths. Hyperscalers like Microsoft, Google, and AWS offer vast GPU farms and telecom-tuned APIs, urging operators to shift training and orchestration to their clouds in exchange for long-term commitments. This approach reduces capex but locks carriers into ecosystems with high exit fees and data-egress costs.

Equipment vendors such as Ericsson, Nokia, and Huawei embed generative AI into their radio and core software, turning upgrades into platforms for new inference features. Positioned at the network's core, they ensure deterministic latency and compliance, which public clouds struggle to match. Nokia’s partnership with NVIDIA to integrate accelerators into base stations exemplifies this hardware-software convergence, steering operators toward vendor-centric procurement.

Specialist AI labs like Cohere and Anthropic address hallucination risks by integrating telecom-specific language models with constitutional or retrieval-augmented frameworks, cutting error rates below the 2% regulatory threshold. Their neutrality allows tools to run on Azure, Ericsson cores, or MVNO edge nodes, offering operators flexibility. The competitive landscape remains fluid since hyperscalers provide scale, equipment vendors deliver proximity, and AI labs ensure trust, enabling operators to balance risk and capital.

Telecom Generative AI Applications Industry Leaders

OpenAI LP

Cohere Technologies Inc.

Anthropic PBC

NVIDIA Corporation

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GSMA has unveiled Open Telco AI, a worldwide initiative aimed at fast-tracking telco-grade AI. This effort emphasizes open collaboration among operators, vendors, AI developers, and academic institutions. As part of the launch, a new portal has been introduced, offering telco open models, data, computing resources, and tools. This portal is set to expedite the development and assessment of AI models tailored for the telecommunications sector.

- February 2026: Mistral AI and Ericsson have partnered to apply advanced AI in the telecom industry, aiming to enhance network intelligence, efficiency, and trust. Combining Mistral AI’s model customization with Ericsson’s research and development expertise and Ericsson as the platform's telecom industry design partner, the collaboration focuses on automating legacy code translation, AI-driven 6G research, and the development of custom AI agents for complex workflows, accelerating software delivery and improving network performance.

Global Telecom Generative AI Applications Market Report Scope

The Telecom Generative AI Applications Market Report is Segmented by Component (Hardware, Software, and Services), Application (Customer Service Automation, Network Optimization, Fraud Detection and Security, Predictive Maintenance, and Marketing Personalization), Deployment Model (Cloud, On-Premise, and Edge), Telecom Operator Type (Mobile Network Operators, Fixed-Line Operators, Internet Service Providers, and Mobile Virtual Network Operators), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Customer Service Automation |

| Network Optimization |

| Fraud Detection and Security |

| Predictive Maintenance |

| Marketing Personalization |

| Cloud |

| On-Premise |

| Edge |

| Mobile Network Operators |

| Fixed-Line Operators |

| Internet Service Providers |

| Mobile Virtual Network Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Application | Customer Service Automation | ||

| Network Optimization | |||

| Fraud Detection and Security | |||

| Predictive Maintenance | |||

| Marketing Personalization | |||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Edge | |||

| By Telecom Operator Type | Mobile Network Operators | ||

| Fixed-Line Operators | |||

| Internet Service Providers | |||

| Mobile Virtual Network Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the Telecom generative AI applications market in 2031?

The market is projected to reach USD 3.53 billion by 2031, expanding at a 33.38% CAGR from 2026 to 2031.

How quickly is generative AI reducing telecom operational costs?

AT&T cut monthly inference expense by 90% after routing queries across multiple models, showing sizable opex relief within 12 months of deployment.

Which application will grow fastest to 2031?

Predictive maintenance is forecast to post a 37.01% CAGR as AI agents pre-empt equipment failures and shrink mean time to repair from 8 hours to 2 hours.

Why are edge deployments accelerating?

Latency-sensitive uses such as AR and autonomous vehicles require sub-10 ms response, pushing operators to embed inference chips at cell sites instead of central clouds.

What hampers AI adoption in Europe?

The EU AI Act labels telecom network automation high-risk, so operators must secure third-party audits and explainability reports, stretching project timelines by up to a year.

How are MVNOs benefiting from generative AI?

MVNOs leverage lightweight models running on leased infrastructure; Tello Mobile’s chatbot now resolves 80% of inquiries without human agents, letting the provider scale with minimal headcount.

Which vendors are addressing hallucination risks?

Cohere and Anthropic supply constitutional AI layers that cap hallucinations under 2%, meeting regulatory thresholds for customer-facing telecom applications.

Page last updated on: